Asia-Pacific Automotive Parts And Components Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

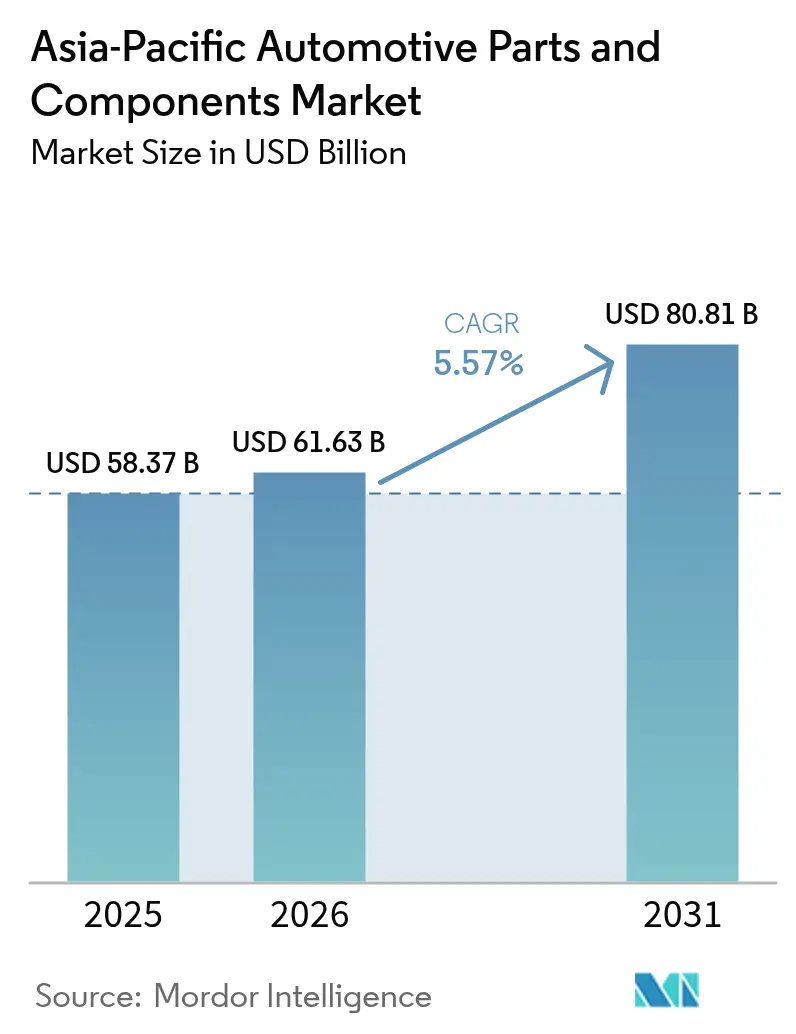

| Base Year Market Size (2025) | USD 58.37 Billion |

| Market Size (2026) | USD 61.63 Billion |

| Market Size (2031) | USD 80.81 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Automotive Parts And Components Market Analysis by Mordor Intelligence

The Asia-Pacific Automotive Parts and Components Market size is expected to increase from USD 58.37 billion in 2025 to USD 61.63 billion in 2026 and reach USD 80.81 billion by 2031, growing at a CAGR of 5.57% over 2026-2031. China's mandate that a significant portion of new-vehicle sales must be new-energy vehicles (NEV) by the near future, coupled with India's substantial incentive for battery-cell makers over the next several years, is driving a significant shift. This shift moves focus from traditional internal combustion engines (ICE) to more lucrative electronics and electrified powertrain modules. As electric vehicle (EV) adoption accelerates, there's a surging demand for domain controllers. These controllers consolidate numerous functions per vehicle, reducing wiring harness weight considerably and facilitating over-the-air software updates. Giga-casting, embraced by both BYD and Tesla, has drastically reduced body-in-white assembly time. This efficiency translates to notable cost savings per unit and has spurred a rise in aluminum demand. In the aftermarket realm, ASEAN's aging vehicle fleet presents opportunities. E-commerce platforms like Tokopedia Automotive capitalized on this, boasting remarkable growth in cross-border parts sales in recent years.

Key Report Takeaways

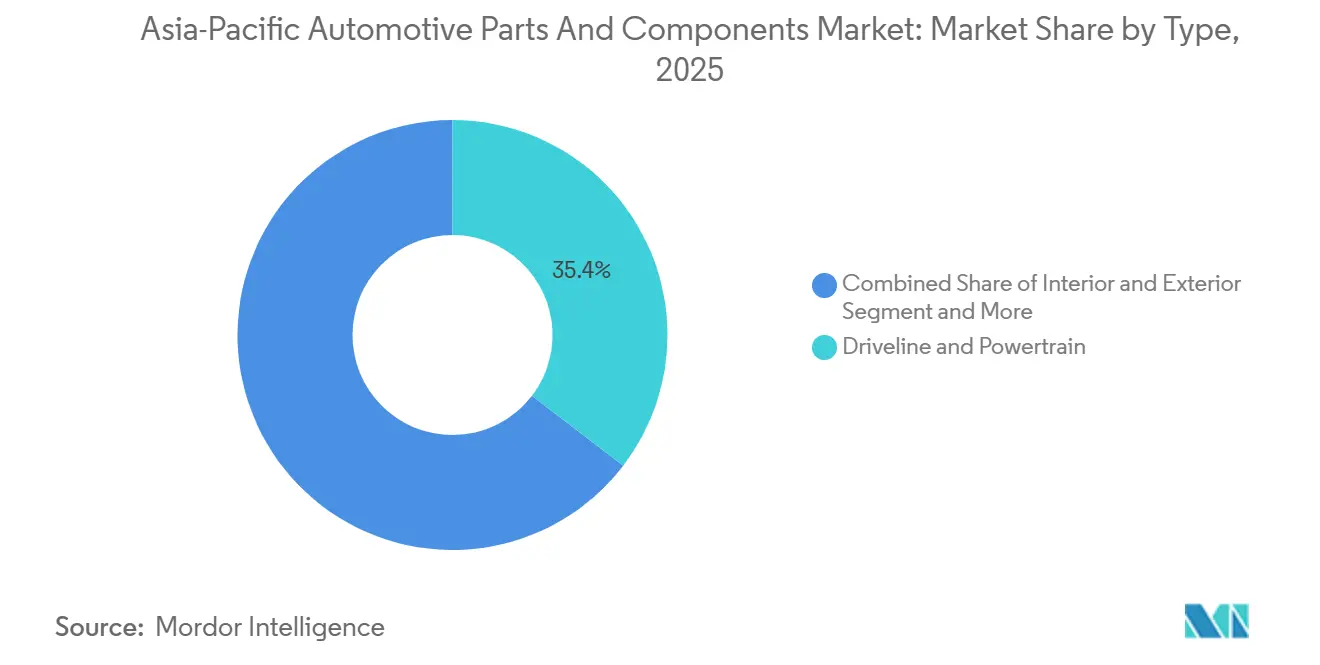

- By type, Driveline and Powertrain parts led with 35.36% of the Asia-Pacific automotive parts and components market share in 2025, while electronics components are projected to record the fastest 5.59% CAGR through 2031.

- By vehicle type, Passenger cars accounted for 63.37% of the market share in 2025; two-wheelers are expected to grow at a 5.67% CAGR through 2031.

- By propulsion, ICE vehicles accounted for 73.14% of the propulsion mix in 2025, yet battery electric vehicles are forecast to grow at a 5.74% CAGR through 2031.

- By sales channel, original-equipment Channels held 65.58% in 2025, whereas the Aftermarket is projected to expand at a 5.69% CAGR due to rising fleet age.

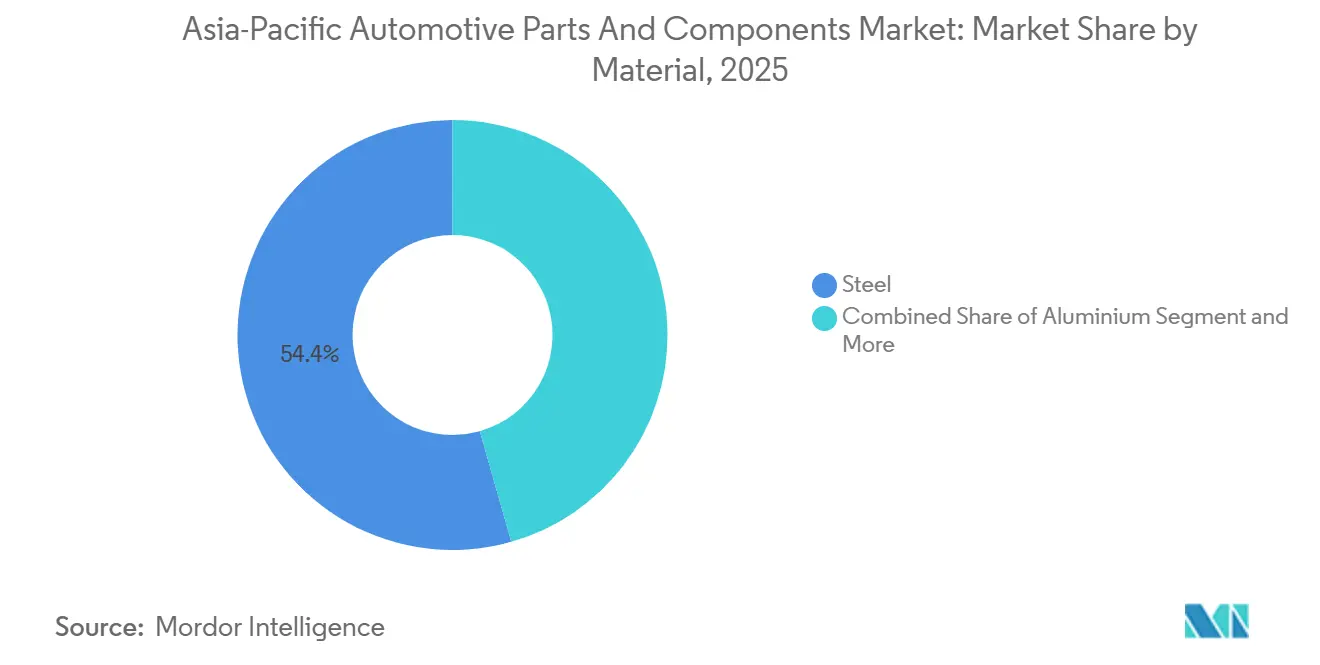

- By material, steel accounted for 54.43% of material tonnage in 2025; aluminum is set to post the fastest 5.63% CAGR as lightweighting targets tighten.

- By manufacturing process, casting processes commanded 42.37% of the share in 2025, while additive manufacturing is expected to accelerate at a 5.71% CAGR.

- By country, China captured 41.22% of regional output in 2025; Indonesia is forecast to register the highest 5.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Automotive Parts And Components Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated EV-Friendly Incentives | +1.5% | Asia Pacific core (China, Japan, South Korea, Thailand, Indonesia) | Short term (≤ 2 years) |

| Rising Adoption of Advanced Automotive Electronics / ADAS | +1.3% | Global, led by Japan, South Korea, China | Long term (≥ 4 years) |

| Expansion of Vehicle-Production Capacity | +1.2% | China, India, spill-over to ASEAN | Medium term (2-4 years) |

| Ageing Fleet Spurring High-Value Aftermarket Demand | +0.8% | ASEAN, India, Australia & New Zealand | Medium term (2-4 years) |

| ASEAN Localization Mandates for EV Supply-Chain Vendors | +0.7% | Thailand, Indonesia, Vietnam, Malaysia | Medium term (2-4 years) |

| Rapid Giga-casting Deployment Driving Lightweight-Alloy Demand | +0.6% | China, spill-over to Japan, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated EV-Friendly Incentives Across Asia Pacific

Thailand's EV 3.5 package offers long-term corporate tax holidays to battery-pack assemblers that source a significant portion of their cells domestically, leading to substantial investment commitments in the near future [1]. Indonesia's Regulation 55/2025 mandates ride-hailing companies to electrify a portion of their fleets within a specified timeframe, generating considerable demand for electric sedans. Japan's Green Transformation fund has allocated a significant budget to support solid-state battery pilots conducted by major industry players like Toyota and Panasonic. These incentives reduce the payback period for EV-component investments and create a notable margin advantage for suppliers focused on electrification.

Rising Adoption of Advanced Automotive Electronics / ADAS

By 2025, a significant portion of new cars in China incorporated Level 2+ driver assistance, marking a considerable increase compared to 2023. This growth aligns with the GB 7258-2024 mandate, which enforces automatic emergency braking for heavier vehicles. DENSO substantially increased its vision-sensor shipments, achieving notable growth. At the same time, Hyundai Mobis captured a prominent share of the ADAS supply market in South Korea. Zonal computing has significantly reduced the number of ECUs in vehicles, leading to notable hardware cost savings while requiring advanced real-time software capabilities. To adapt to this industry transformation, Bosch made a substantial investment in software talent and acquired a minority stake in Apex.AI. Suppliers lacking strong software capabilities face the risk of rapid commoditization.

Expansion of Vehicle-Production Capacity in China and India

In 2025, China approved several new assembly lines for passenger cars, significantly increasing annual capacity across key regions such as Guangdong, Jiangsu, and Sichuan. Meanwhile, India's Automotive Mission Plan aims for substantial growth in production by 2026. Following this trend, tier-1 suppliers made notable investments: ZF inaugurated a major hybrid-transmission facility in Pune, and Aisin launched a new CVT line in Tianjin. Streamlined logistics have considerably reduced lead times and working capital requirements. However, with China's utilization falling below the profitability threshold in 2025, supplier consolidation is anticipated before 2027. While the volume outlook remains positive, the risk of over-capacity poses a challenge.

Aging Fleet Spurring High-Value Aftermarket Demand

In recent years, the average vehicle age in ASEAN has increased, prompting the replacement of high-wear parts like brakes and filters. Independent distributors have significantly reduced OEM service prices, making them more competitive. Leveraging VIN-matching technology, Tokopedia Automotive efficiently connects buyers to the correct part almost instantly, driving substantial growth in e-commerce aftermarket sales. Australia's right-to-repair regulations mandate OEMs to provide diagnostics, further benefiting independent distributors. Meanwhile, revenue from the OEM-linked aftermarket has declined, widening the profit gap between OEMs and independent distributors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Price Volatility | -0.9% | Global, acute in China, Japan, South Korea | Short term (≤ 2 years) |

| Persistent Semiconductor and Logistics Bottlenecks | -0.7% | Asia Pacific core, spill-over to ASEAN | Medium term (2-4 years) |

| OEM Shift to Captive Software-Defined Platforms | -0.5% | Japan, South Korea, China | Long term (≥ 4 years) |

| Fragmented Cross-Border Compliance Costs | -0.4% | ASEAN, India, Australia & New Zealand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Steel, Aluminum, Rare Earths)

In 2025, as carbon-control measures reshaped output, China's hot-rolled coil prices experienced significant fluctuations. Concurrently, aluminum billets saw a notable increase in prices following Indonesia's decision to cap bauxite exports. In early 2026, neodymium-praseodymium oxide prices witnessed a sharp rise after Myanmar put a stop to dysprosium exports. Continental faced a considerable margin squeeze and opted for quarterly price adjustments on a majority of its Asian OEM contracts. Meanwhile, Hyundai Steel, a vertically integrated player, maintained a competitive EBITDA advantage, attributing it to its in-house recycling capabilities.

Persistent Semiconductor and Logistics Bottlenecks

In late 2025, automotive chip lead times remained significantly longer than normal, although they had improved from the peak levels seen a few years earlier. This extended lead time was due to foundries prioritizing advanced AI accelerators over older technology nodes. DENSO's recent joint venture with Renesas highlights a growing trend of suppliers moving into chip design, a strategy that requires substantial investment for each chip family. Freight costs from Shanghai to Los Angeles were considerably higher compared to pre-pandemic levels, while congestion in major ports like Singapore and Busan caused notable delays. Volkswagen's adoption of a domain-controller strategy significantly reduced the number of chips required per car and enabled the company to negotiate substantial discounts from key suppliers, creating challenges for vendors unable to adapt their designs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electronics Outpace Legacy Powertrains

Driveline and Powertrain parts held 35.36% of the Asia-Pacific automotive parts and components market share in 2025, mirroring ICE dominance, but electronics are projected to grow at a 5.59% CAGR through 2031. In 2025, Bosch's automotive electronics revenue grew significantly, driven by a substantial increase in radar volume. The company reaped benefits from domain controllers and ADAS sensors, each capable of reducing materials costs per vehicle. Faurecia’s integrated cockpit offering, which diminishes assembly complexity by a notable percentage, helped elevate the value of interiors and exteriors. Meanwhile, body and chassis components accounted for a considerable share of the value, with giga-casting now replacing traditional multi-piece stampings.

In 2025, the Asia-Pacific automotive electronics market experienced substantial growth, with projections indicating further expansion in the coming years. This growth reflects a consistent shift away from legacy powertrains. Michelin's launch of the UPTIS airless tire, designed for high-mileage fleets, contributed to wheels and tires representing a significant portion of the market value. In China, new cabin air-quality regulations spurred demand for competitively priced activated-carbon filters. Looking ahead, electronics and software modules are expected to dominate a significant share of a vehicle's bill-of-materials value by 2030, compelling mechanical suppliers to adapt or face diminishing margins.

By Vehicle Type: Two-Wheeler Electrification Accelerates

Passenger cars generated 63.37% of volume in 2025 on production of 21.2 million units in China and 4.8 million units in India, yet the two-wheeler segment is on track for a 5.67% CAGR through 2031. In 2025, Indonesia's decision to waive VAT on electric motorcycles priced under a specific threshold led to a significant surge in registrations. This move also catalyzed Yamaha's ambitious investment in building swap stations. Meanwhile, Vietnam's VinFast successfully sold a substantial number of electric scooters, leveraging a battery-lease strategy that reduced the upfront cost to an affordable level. Additionally, Cummins X15N natural-gas engines, known for their fuel-saving benefits, found a notable market share within the commercial vehicle segment.

Forecasts indicate that the Asia-Pacific market for automotive parts and components will witness a significant increase in two-wheeler components, projected to grow substantially over the forecast period. Off-highway vehicles maintained a steady market share, attributed to their duty cycles often exceeding long operational hours. Suppliers in the two-wheeler segment are urged to optimize battery packs within a specific range. They should also consider establishing swapping networks, drawing inspiration from a successful model that is now being replicated across the ASEAN region. On the other hand, passenger-car suppliers are feeling the heat of vertical integration, especially with OEMs making strategic moves in batteries and motors. This shift has resulted in a notable reduction in tier-1 content over recent years.

By Propulsion: BEV Components Command Premium Growth

ICE vehicles still formed 73.14% of the fleet in 2025, but battery electric vehicles are projected to advance at a 5.74% CAGR, faster than the overall Asia-Pacific automotive parts and components market. In 2025, BYD's Blade lithium-iron-phosphate battery pack powered a significant number of vehicles, eliminating the need for costly nickel and cobalt. Due to Toyota's fifth-generation powertrain, which achieved high thermal efficiency, hybrids captured a notable market share. Meanwhile, as battery prices declined significantly by the end of 2025, plug-in hybrids experienced a downturn.

In 2025, the Asia-Pacific market for BEV automotive parts and components achieved substantial growth, with further expansion expected in the coming years. While fuel-cell vehicles held a minimal market share, Hyundai's XCIENT truck demonstrated impressive performance over extensive usage. In India's three-wheeler segment, alternative fuels like compressed natural gas accounted for a small but notable share. Suppliers specializing in BEV packs, thermal management, and power electronics achieved higher profitability margins compared to those focused on ICE portfolios.

By Sales Channel: Aftermarket Gains Share

OEM channels controlled 65.58% of revenue in 2025, yet the aftermarket is estimated to grow at a 5.69% CAGR as the ASEAN fleet age climbs. Independent distributors, by sidestepping dealer markups, secure substantial gross margins. Meanwhile, platforms like Tokopedia Automotive and Lazada Auto Parts offer consumers significant savings, ensuring parts are matched to Vehicle Identification Numbers (VIN) in mere seconds. While OEM service parts previously held a notable share, they now grapple with the challenges posed by digital disruption.

In recent years, the Asia-Pacific aftermarket for automotive parts and components has experienced steady growth, with expectations of continued expansion in the coming years. In a move to level the playing field, Australia enacted a right-to-repair law mandating OEMs to share diagnostic information. Responding to this shift, Continental launched a direct-to-consumer portal in Southeast Asia, boasting a promise of rapid delivery across multiple nations. Additionally, remanufactured components have gained a growing share of the aftermarket's value, aligning with the circularity objectives outlined in China's latest Five-Year Plan.

By Material: Aluminum Gains on Lightweighting

Steel provided 54.43% of tonnage in 2025, leveraging ultra-high-strength grades above 1,500 MPa that meet China’s C-NCAP crash rules. Aluminum is projected to expand at a 5.63% CAGR as giga-casting soaks up A356 alloy and OEMs chase minimal weight cuts by 2030. Carbon-fiber roofs in BMW's i7, which significantly reduce weight per unit, led composites to capture a notable market share, despite facing high raw-material costs.

In recent years, the Asia-Pacific market for aluminum in automotive parts and components has shown substantial growth, with projections indicating continued expansion in the coming years. Plastics accounted for a significant portion of the market value, as polypropylene parts, being considerably lighter than steel, offer rapid molding capabilities. While magnesium provides notable cost advantages over aluminum, its requirement for protective coatings introduces additional expenses. Integrated extrusion operations, like Novelis Changzhou's large-scale sheet mill, command higher margin premiums due to their efficiency and scale.

By Manufacturing Process: Additive Gains Traction

Casting processes represented 42.37% of 2025 output, led by high-pressure die casting of drive housings and giga-cast structural parts. Additive manufacturing is expected to post a 5.71% CAGR, helped by Bosch’s metal binder-jet line that trims hydraulic manifolds. While stamping and forging once dominated with a significant share, they're now ceding ground to single-piece castings, which are increasingly supplanting multi-part assemblies.

In recent years, the Asia-Pacific market for automotive parts and components utilizing additive production has experienced notable growth, with expectations of further expansion in the coming years. Machining continues to play a key role, particularly in the production of precision injectors and gears. The additive approach enables suppliers to print low-volume spares in a fraction of the time required by traditional methods, proving invaluable for supporting aging fleets. While metal additive manufacturing (AM) remains focused on complex geometries due to its production constraints, polymer AM has already demonstrated its efficiency in high-volume production during standard operational shifts.

Geography Analysis

In 2025, China is set to dominate the Asia-Pacific automotive parts and components market, holding a commanding 41.22% share. This surge is largely attributed to CATL's expansive separator plant in Sichuan and Geely's stamping hub in Ningbo. The latter not only ships a notable volume of aluminum closures but also accounts for a significant share of the year's output [2]“Sichuan Separator Plant Milestone,” CATL, catl.com . With passenger-vehicle capacity utilization below optimal levels, consolidation pressures loom, potentially sidelining a notable portion of tier-2 suppliers within a few years. Due to a significant battery-cell incentive, India secured a considerable share, spurring Motherson to ramp up Noida's harness capacity to meet growing demand by the latter half of the decade [3]“Wiring Harness Capacity Expansion in India,” Motherson Group, motherson.com . Japan, holding a notable stake, saw DENSO's substantial investment in silicon-carbide fabs, which not only enhanced inverter efficiency but also extended the BEV range by a measurable margin.

South Korea, which contributed a significant portion of the value, witnessed Hyundai Mobis's strategic acquisition of a majority stake in Hyundai Kefico, bolstering its semiconductor design capabilities. Thailand's notable stake is anchored in the EV 3.5 package, reaping substantial commitments in pack-assembly projects. Forecasts suggest Indonesia will lead with the fastest growth rate, driven by Hyundai's Cikarang plant targeting a significant production volume and LG's shipment of a large capacity of cells in the mid-decade. Meanwhile, Vietnam, Australia, New Zealand, and other Asia-Pacific regions collectively accounted for a considerable share, with Vietnam's decree paving the way for VinFast's ambitious motor project.

Indonesia is set to achieve a CAGR of 5.65% during the forecast period. Due to local-content regulations that shorten module lead times and significantly enhance OEM ROIC, both Indonesia and Vietnam are positioned to attract a substantial share of the region's growing investments. In China, an oversupply situation opens the door for financially robust tier-1 companies to step in, acquire struggling tier-2 firms, and smoothly merge their battery and power-electronics divisions. With its carefully crafted silicon-carbide strategy, Japan aims to secure a hefty slice of the global automotive power-electronics market by decade's end, provided its local foundries can outpace their Chinese rivals in yield efficiency.

Competitive Landscape

The Asia-Pacific automotive parts and components market remains moderately fragmented. The leading suppliers collectively accounted for a significant portion of the revenue, with no single company dominating the market. In recent years, OEM vertical integration into software stacks and battery management has led to a noticeable reduction in tier-1 gross margins. DENSO’s joint venture with Renesas and Hyundai Mobis’s acquisition of Hyundai Kefico highlight a strategic push towards chip design, anticipating a future where electronics and software will represent a substantial share of a vehicle's value.

Battery thermal-management offers considerable opportunities, as achieving optimal pack temperature uniformity commands a notable price premium. Solid-state pilot lines, supported by substantial subsidies from Toyota and Panasonic, further emphasize this potential. Disruptors like CATL and BYD, having expanded into thermal modules and inverters, have significantly impacted tier-1 content. In response, Bosch launched a Southeast Asian e-commerce parts portal, drastically reducing lead times. Patent activity underscores the shift: Bosch has been highly active in electronics patents, while Hyundai Mobis has concentrated on patents related to radar-camera modules.

Suppliers lacking expertise in software or access to semiconductors are experiencing declining volumes and margins. This trend is driving a wave of consolidation, which could result in a smaller number of dominant suppliers in the coming years. Companies investing in additive manufacturing, domain-controller software, and localized EV supply chains are better positioned to sustain profitability, even amidst challenges such as raw material price fluctuations and logistical constraints.

Asia-Pacific Automotive Parts And Components Industry Leaders

DENSO Corporation

ZF Friedrichshafen AG

Robert Bosch GmbH

Hyundai Mobis Co., Ltd.

Aisin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: VinFast has launched production at its USD 500 million facility in Tamil Nadu, signifying Vietnam's inaugural major automotive presence in India and boosting annual EV capacity by 150,000 units.

- June 2025: China is set to introduce mandatory performance benchmarks for driver-assistance systems by 2027, as its draft national safety standard enters stakeholder review.

- May 2025: DENSO invested in Rohm Semiconductor to co-develop SiC power devices, securing long-term wafer supply for 800-V e-axles.

Asia-Pacific Automotive Parts And Components Market Report Scope

The scope of the report includes Type (Driveline & Powertrain and More), Vehicle Type (Passenger Cars and More), Propulsion (ICE, BEV, and More), Sales Channel (OEM and More), Material (Steel and More), Manufacturing Process (Stamping & Forging and More), and Geography.

| Driveline & Powertrain |

| Interiors & Exteriors |

| Electronics |

| Bodies & Chassis |

| Wheels & Tires |

| Other Components (Filtration, Fluids, etc.) |

| Passenger Cars |

| Commercial Vehicles |

| Two-Wheelers |

| Off-Highway Vehicles |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicles (BEV) |

| Hybrid Electric Vehicles (HEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Fuel Cell Electric Vehicles (FCEV) |

| Alternative Fuels (CNG, LPG, Biofuels) |

| Original Equipment Manufacturers (OEM) |

| Aftermarket |

| Original Equipment Service (OES) |

| Independent Aftermarket and E-Commerce Aftermarket |

| Steel |

| Aluminium |

| Composites |

| Plastics & Polymers |

| Others (Magnesium, Carbon Fibre) |

| Stamping & Forging |

| Casting (Die, Sand, Investment) |

| Machining |

| Additive Manufacturing |

| China |

| India |

| Japan |

| South Korea |

| Thailand |

| Indonesia |

| Vietnam |

| Australia & New Zealand |

| Rest of Asia-Pacific |

| By Type | Driveline & Powertrain |

| Interiors & Exteriors | |

| Electronics | |

| Bodies & Chassis | |

| Wheels & Tires | |

| Other Components (Filtration, Fluids, etc.) | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| Two-Wheelers | |

| Off-Highway Vehicles | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Battery Electric Vehicles (BEV) | |

| Hybrid Electric Vehicles (HEV) | |

| Plug-in Hybrid Electric Vehicles (PHEV) | |

| Fuel Cell Electric Vehicles (FCEV) | |

| Alternative Fuels (CNG, LPG, Biofuels) | |

| By Sales Channel | Original Equipment Manufacturers (OEM) |

| Aftermarket | |

| Original Equipment Service (OES) | |

| Independent Aftermarket and E-Commerce Aftermarket | |

| By Material | Steel |

| Aluminium | |

| Composites | |

| Plastics & Polymers | |

| Others (Magnesium, Carbon Fibre) | |

| By Manufacturing Process | Stamping & Forging |

| Casting (Die, Sand, Investment) | |

| Machining | |

| Additive Manufacturing | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Australia & New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large could electronics components become within the Asia-Pacific vehicle bills of materials?

Electronics are projected to capture 45% of vehicle BOM value by 2030 as domain controllers, ADAS sensors, and power electronics displace legacy mechanical content.

Which country will add capacity fastest through 2031?

Indonesia is expected to post a 5.65% CAGR, driven by Hyundai’s Cikarang complex and LG’s Karawang battery plant coming online.

Why is aluminum demand rising in regional vehicle production?

Giga-casting and 15% lightweighting targets under China’s dual-credit policy and Japan’s Top Runner program push aluminum content from 12% of curb weight in 2025 to 18% by 2031.

What is the outlook for the aftermarket channel?

Rising fleet age to 11.2 years in ASEAN and strong e-commerce adoption should lift aftermarket revenue at a 5.69% CAGR through 2031.

How are suppliers mitigating semiconductor shortages?

Strategies include vertical integration into chip design, as seen in the DENSO-Renesas JV, and ECU consolidation that trims per-car chip counts by 40%.

Where do battery thermal-management systems offer margins?

Suppliers achieving 2 °C temperature uniformity across 200-cell packs can charge 22% price premiums amid rapid BEV adoption.

Page last updated on: