EV Connector Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.27 Billion |

| Market Size (2030) | USD 4.81 Billion |

| Growth Rate (2025 - 2030) | 16.48% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

EV Connector Market Analysis by Mordor Intelligence

The EV connector market size stood at USD 2.27 billion in 2025 and is projected to reach USD 4.81 billion by 2030, advancing at a 16.48% CAGR over the forecast period. Consistent government pressure to cut vehicular emissions, the rapid commercialization of 800 V+ powertrains, and mandatory High-Voltage Interlock Loop (HVIL) safety rules are expanding per-vehicle connector value. Original equipment manufacturers (OEMs) are moving from sprawling wire harnesses toward zonal electrical and electronic (E/E) architectures, which favor compact board-to-board links and elevate demand for high-density signal connectors. Migration to the North American Charging Standard (NACS) and parallel adoption of megawatt systems in heavy-duty fleets are consolidating interface variants, allowing suppliers to scale precision tooling across larger volumes.

Key Report Takeaways

- By propulsion type, Battery Electric Vehicles commanded 68.42% of the EV connector market size in 2024, while Fuel Cell Electric Vehicles are projected to expand at a 27.53% CAGR between 2025 and 2030.

- By connection type, wire-to-wire held 36.87% share of the EV connector market size in 2024; board-to-board is forecast to rise at a 22.11% CAGR through 2030.

- By voltage, high-voltage connectors captured 52.18% of the EV connector market size in 2024 and are growing at a 19.46% CAGR.

- By component, terminals contributed a 29.27% share in 2024, while lock mechanisms are anticipated to grow at an 18.03% CAGR.

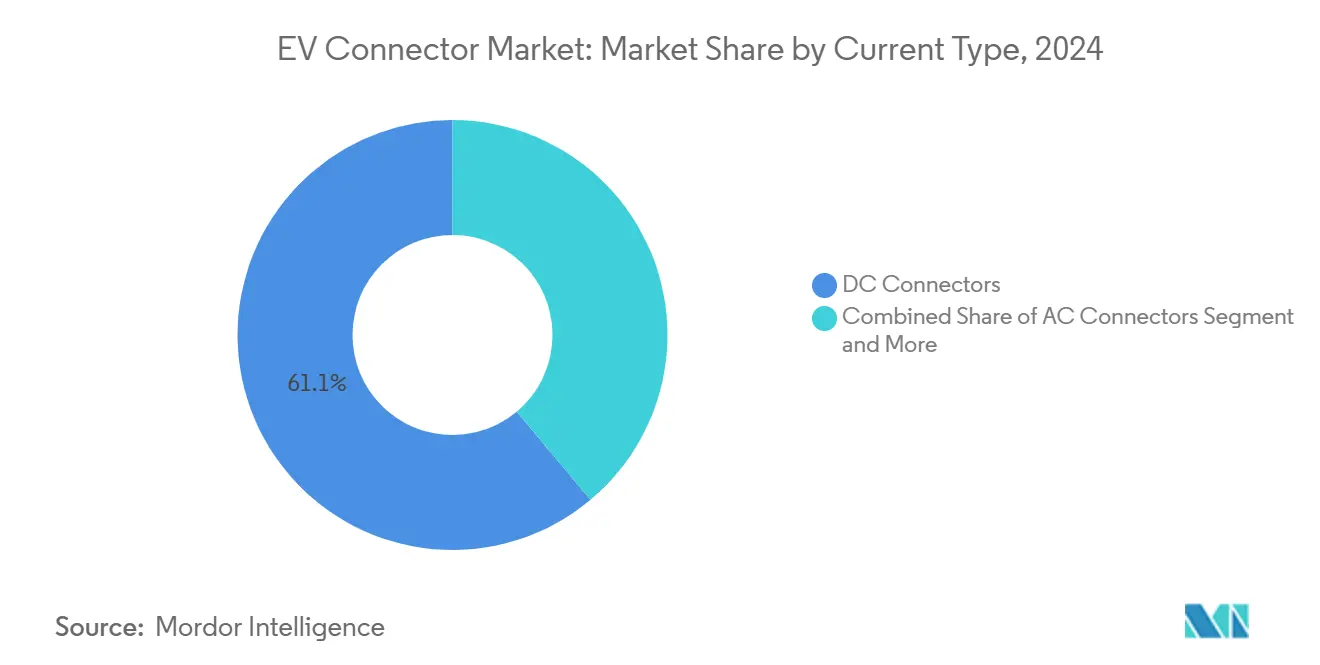

- By current type, DC interfaces dominated with 61.14% of the EV connector market share in 2024; combined AC/DC designs will register the fastest 25.09% CAGR to 2030.

- By geography, Asia-Pacific led with a 44.09% EV connector market share in 2024, whereas the Middle East and Africa is set to post the fastest 18.47% CAGR to 2030.

Global EV Connector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Global 800 V+ EV Architectures | +3.2% | Germany, China, Korea | Medium Term (2-4 Years) |

| Government-Mandated HVIL Safety Standards | +2.8% | North America, European Union, Expanding to Asia-Pacific | Short Term (≤ 2 Years) |

| Rising BEV Production in China and Europe | +2.6% | China, Germany, France, Spillover to ASEAN | Short Term (≤ 2 Years) |

| Transition to NACS Retrofits | +2.3% | United States and Canada, Potential Global Adoption | Medium Term (2-4 Years) |

| Zonal E/E Architecture Adoption | +1.9% | Global, Led by Premium OEMs | Long Term (≥ 4 Years) |

| Liquid-Cooled Ultra-High-Current Charging | +1.5% | Urban Charging Corridors Worldwide | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Expanding Global 800V+ EV Architectures

The automotive industry's migration to 800V+ electrical architectures represents a fundamental shift that quadruples system voltage compared to traditional 400V platforms, enabling faster charging times and improved power efficiency across drivetrain components. Hyundai Motor Group's E-GMP platform and Porsche's Taycan have demonstrated the commercial viability of 800V systems, with charging speeds reaching 350kW and 10-80% battery charging in under 18 minutes. This architectural evolution demands connectors capable of handling higher voltages while maintaining compact form factors, driving innovation in insulation materials and contact design. The transition creates immediate opportunities for connector manufacturers to develop specialized high-voltage solutions, though it also necessitates substantial R&D investments in thermal management and safety systems. Korea's aggressive EV targets and Germany's premium automotive segment lead this adoption, with Chinese manufacturers rapidly scaling 800V platforms across mass-market vehicles.

Government-Mandated HVIL Safety Standards

Regulatory frameworks increasingly mandate High Voltage Interlock Loop (HVIL) safety systems across EV platforms, creating standardized requirements for connector manufacturers to integrate safety circuits directly into high-voltage interconnects. The Federal Highway Administration's recent guidance on EV charging infrastructure emphasizes HVIL compliance as a prerequisite for federal funding eligibility, effectively mandating these safety features across public charging networks. HVIL systems require additional pins and specialized housing designs to accommodate safety circuits, increasing connector complexity and value content per unit. This regulatory push creates barriers to entry for non-compliant suppliers while rewarding established manufacturers with certified HVIL solutions. The standardization of safety requirements across jurisdictions reduces design fragmentation and enables economies of scale, though compliance costs initially pressure margins for smaller connector suppliers.

Rising BEV Production in China and Europe

China's BEV production surge, supported by substantial government subsidies and manufacturing scale advantages, drives exponential demand for automotive connectors across all vehicle segments. European manufacturers simultaneously accelerate BEV production to meet EU emissions regulations, with Germany's automotive sector investing EUR 60 billion in electrification through 2030. This dual-region production expansion creates unprecedented connector demand, particularly for high-voltage applications and battery management systems. Chinese suppliers benefit from proximity to the world's largest EV market and established supply chains, while European manufacturers focus on premium applications requiring advanced materials and precision manufacturing. The geographic concentration of BEV production in these regions influences global connector supply chains, with manufacturers establishing local production capabilities to serve regional OEM requirements and reduce logistics costs.

Transition to NACS Retrofits

The North American Charging Standard (NACS) transition, formalized through SAE J3400 publication, creates a massive retrofit opportunity as existing CCS-equipped vehicles require adapter solutions and new vehicles adopt NACS natively. Tesla's decision to open its Supercharger network and major OEMs' commitment to NACS adoption by 2025 will fundamentally reshape the North American charging landscape. This standardization reduces connector fragmentation while creating short-term demand for adapter products and long-term opportunities for NACS-native connector manufacturing. The transition benefits established connector manufacturers with existing Tesla relationships while challenging CCS-focused suppliers to develop NACS capabilities. Retrofit demand peaks in the medium term as existing vehicle fleets adapt, followed by sustained growth in NACS-native applications as the standard achieves market dominance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Copper and Critical Metals | -2.1% | Global, Acute in Supply-Constrained Regions | Short Term (≤ 2 Years) |

| Thermal-Runaway Risk at > 350 kW Charging | -1.8% | Fast-Charging Sites in Hot Climates Worldwide | Medium Term (2-4 Years) |

| Slow Connector-Standard Harmonization | -1.5% | Global, with Divergent Regional Standards (NACS, CCS, GB/T) | Medium Term (2-4 Years) |

| Tier-1 Supply-Chain Concentration Risk | -1.3% | North America and Europe, with Dependence on Limited High-Voltage Component Suppliers | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Volatility in Copper and Critical Metals

Copper price volatility, exacerbated by supply chain disruptions and geopolitical tensions, directly impacts connector manufacturing costs as copper represents 60-70% of material costs in high-current applications. London Metal Exchange copper prices fluctuated between USD 8,000 and 10,500 per metric ton throughout 2024, creating margin pressure for connector manufacturers unable to implement effective hedging strategies. Critical metals, including nickel for plating applications and rare earth elements for specialized alloys, face similar volatility, with supply concentration in geopolitically sensitive regions amplifying risk. Manufacturers respond through material substitution research and long-term supply agreements, though these strategies require significant capital investment and may compromise performance specifications. The volatility particularly affects smaller connector suppliers lacking negotiating power with metal suppliers, potentially driving industry consolidation toward larger, more resilient manufacturers.

Thermal-Runaway Risk at More Than 350kW Charging

Ultra-high-power charging applications exceeding 350kW create thermal management challenges that risk connector failure and potential safety hazards, limiting the deployment of next-generation charging infrastructure. Resistive heating in high-current connections can trigger thermal runaway events, particularly in ambient temperatures above 40°C or when connector maintenance is inadequate. This technical constraint necessitates expensive liquid-cooling systems and advanced materials, increasing system complexity and infrastructure costs. Connector manufacturers must balance current-carrying capacity with thermal performance, often requiring oversized components that conflict with vehicle packaging constraints. The challenge is most acute in regions with extreme climates and high-utilization charging corridors, where thermal stress accelerates connector degradation and increases maintenance requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: BEV Dominance Drives Volume

Battery Electric Vehicles captured 68.42% market share in 2024, reflecting the automotive industry's primary electrification pathway and substantial OEM investments in pure-electric platforms. Fuel Cell Electric Vehicles, despite representing a smaller absolute volume, exhibit the fastest growth at 27.53% CAGR (2025-2030) as hydrogen infrastructure development accelerates and commercial vehicle applications demonstrate FCEV advantages in long-haul operations[1]"Energy Department Removes Barriers for American Energy Producers, Unleashing Investment in Domestic Hydrogen," U.S. Department of Energy, energy.gov.. Plug-in Hybrid Electric Vehicles maintain steady demand in markets with limited charging infrastructure, while Hybrid Electric Vehicles require specialized connectors for battery management and power distribution between electric and internal combustion systems.

The propulsion type segmentation reveals distinct connector requirements across platforms, with BEVs demanding the highest-voltage and highest-current solutions for both drivetrain and charging applications. FCEV growth creates opportunities for specialized hydrogen-compatible connectors and safety systems, particularly in commercial vehicle segments where hydrogen's energy density advantages overcome infrastructure limitations. The segment's evolution toward pure-electric platforms simplifies connector standardization while increasing per-vehicle connector content as manufacturers eliminate internal combustion engine components and expand electric system complexity.

By Connection Type: Wire-to-Wire Leads Traditional Applications

Wire-to-wire connections dominated with a 36.87% market share in 2024, serving traditional automotive wiring applications, including power distribution and signal transmission across vehicle systems. Board-to-board connections emerged as the fastest-growing segment at 22.11% CAGR (2025-2030), driven by zonal E/E architecture adoption that consolidates electronic control units and reduces wiring harness complexity. Wire-to-board connections serve hybrid applications where traditional wiring interfaces with modern electronic modules, while other connection types address specialized applications, including charging interfaces and sensor connections.

Zonal architecture adoption fundamentally reshapes connection type demand as manufacturers migrate from distributed wiring harnesses toward centralized processing nodes connected via high-speed data links. This architectural shift reduces wire-to-wire connection volume while increasing board-to-board and high-speed data connector requirements. The transition creates opportunities for connector manufacturers with expertise in high-density, high-speed interconnects while challenging traditional automotive wiring suppliers to develop new capabilities.

By Voltage: High-Voltage Applications Drive Growth

High-voltage connectors (>300V) command 52.18% market share in 2024 and maintain the fastest growth trajectory at 19.46% CAGR (2025-2030), reflecting the automotive industry's migration toward higher-power electric drivetrains and charging systems. Medium-voltage applications (60-300V) serve auxiliary systems including 48V architectures that support electric turbocharging and regenerative braking, while low-voltage connectors (<60V) address traditional automotive electronics and control systems. The voltage segmentation directly correlates with connector complexity and value content, as higher voltages require advanced insulation materials and safety features.

The high-voltage segment's dominance reflects fundamental changes in automotive electrical architecture as manufacturers adopt 800V+ systems for improved charging performance and drivetrain efficiency. This voltage escalation demands connector innovations in insulation design, contact materials, and thermal management to ensure reliable operation under extreme electrical stress. Regulatory compliance requirements for high-voltage applications create barriers to entry while rewarding manufacturers with established safety certifications and testing capabilities.

By Component: Terminals Lead Value Content

Terminal components capture 29.27% market share in 2024, representing the core electrical interface within connector assemblies and driving value through material specifications and precision manufacturing requirements. Lock mechanisms exhibit the fastest growth at 18.03% CAGR (2025-2030), reflecting increasing emphasis on connection security and automated coupling systems in high-power charging applications. Housing components provide environmental protection and mechanical support, while other components address specialized functions, including HVIL safety circuits and EMI shielding.

Lock mechanism growth correlates with charging power increases as higher currents demand more secure connections to prevent arcing and thermal damage during coupling and decoupling operations. Advanced lock designs incorporate automated engagement and status monitoring capabilities, particularly in commercial charging applications where operator safety and connection reliability are paramount. The component segmentation reveals opportunities for specialized manufacturers to develop innovative locking systems and high-performance terminal materials that address evolving automotive requirements.

By Current Type: DC Connectors Dominate Fast Charging

DC connectors lead with 61.14% market share in 2024, serving the rapidly expanding fast-charging infrastructure and high-voltage drivetrain applications that define modern EV architectures. Combined connectors represent the fastest-growing segment at 25.09% CAGR (2025-2030), reflecting industry preference for integrated solutions that support both AC and DC charging through single interfaces. AC connectors serve traditional charging applications and auxiliary systems, while the current type segmentation reflects the fundamental division between charging infrastructure and vehicle-internal applications.

The DC connector segment's dominance aligns with consumer preference for fast charging and infrastructure operators' focus on high-utilization, high-revenue charging stations. Combined connector growth indicates industry consolidation toward fewer, more versatile connector types that reduce vehicle complexity and manufacturing costs. This trend benefits connector manufacturers with expertise in multi-protocol designs while challenging single-function connector suppliers to expand their capabilities or focus on specialized applications.

By Application: Battery Management Systems Lead Critical Functions

Battery Management System applications command 34.76% market share in 2024, reflecting the critical importance of battery monitoring and control in EV safety and performance optimization. ADAS and Safety Systems emerge as the fastest-growing application at 20.28% CAGR (2025-2030), driven by increasing sensor density and autonomous driving capabilities that require robust, high-speed data connections. Infotainment systems, engine management, body control, and vehicle lighting applications represent additional connector demand across diverse vehicle systems.

BMS connector requirements emphasize precision and reliability as battery monitoring directly impacts vehicle safety and performance, creating opportunities for specialized manufacturers with automotive safety certifications. ADAS application growth reflects the automotive industry's evolution toward autonomous capabilities, requiring connectors that support high-bandwidth data transmission while maintaining reliability under extreme environmental conditions. The application segmentation demonstrates connector market diversification beyond traditional power applications toward sophisticated electronic systems that define modern vehicle functionality.

Geography Analysis

Asia-Pacific maintains market leadership with 44.09% share in 2024, driven primarily by China's massive BEV production scale and Korea's aggressive electrification targets, including 4.5 million zero-emission vehicles by 2030. China's dominance stems from government subsidies, established supply chains, and proximity to global electronics manufacturing, while Japan contributes through advanced connector technologies and materials science expertise. India emerges as a significant growth market through government incentives and increasing domestic EV adoption, though infrastructure limitations constrain near-term expansion. The region benefits from integrated supply chains spanning raw materials, component manufacturing, and final assembly, creating cost advantages and rapid innovation cycles that support global EV connector demand.

Europe represents the second-largest market, with Germany leading through premium automotive manufacturers' investments in 800V+ architectures and advanced charging infrastructure. The European Union's stringent emissions regulations drive rapid BEV adoption, while the region's focus on sustainability creates demand for environmentally responsible connector materials and manufacturing processes. France, Italy, and the United Kingdom contribute through domestic EV programs and charging network expansion, though Brexit-related supply chain disruptions create temporary challenges for UK-based manufacturers. European manufacturers emphasize high-performance applications and advanced materials, commanding premium pricing in global markets despite higher manufacturing costs.

North America exhibits steady growth driven by the NACS transition and substantial federal infrastructure investments through the Infrastructure Investment and Jobs Act. The Middle East and Africa region demonstrates the fastest growth at 18.47% CAGR (2025-2030), led by the UAE's smart city initiatives and Saudi Arabia's Vision 2030 electrification programs that include substantial EV infrastructure investments. South America represents an emerging market with Brazil leading through domestic EV incentives and charging infrastructure development, though economic volatility and currency fluctuations create challenges for international connector suppliers seeking to establish regional operations.

Competitive Landscape

The EV connector market exhibits moderate concentration with established automotive suppliers leveraging decades of engineering expertise while facing pressure from specialized high-voltage connector manufacturers targeting emerging applications. TE Connectivity and Amphenol dominate across multiple connector categories, with Bishop & Associates data indicating both companies rank in the top 10 across all 12 major connector product segments. Market dynamics favor suppliers with comprehensive product portfolios, global manufacturing capabilities, and established OEM relationships, though technological disruption creates opportunities for innovative entrants focused on next-generation applications, including liquid-cooled charging and zonal architectures.

Strategic patterns emphasize vertical integration and technological differentiation as key competitive advantages, with leading manufacturers investing heavily in advanced materials, automated manufacturing, and digital supply chain capabilities. White-space opportunities emerge in specialized applications, including FCEV connectors, ultra-high-current charging solutions exceeding 500A, and integrated connector-cooling systems for thermal management. Patent activity intensifies around contact terminal designs for high-current applications, with recent innovations focusing on sliding contact mechanisms that maintain electrical performance under mechanical stress and thermal cycling. The competitive landscape increasingly rewards manufacturers capable of supporting OEMs' transition toward software-defined vehicles through connectors that integrate power, data, and safety functions in compact, cost-effective packages.

EV Connector Industry Leaders

-

TE Connectivity

-

Amphenol

-

Yazaki Corporation

-

Aptiv

-

Sumitomo Electric Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Japan Aviation Electronics launched the KW07C CHAdeMO connector and KW51 NACS-compatible connector series, addressing both established and emerging charging standards with waterproof performance equivalent to IPX9K and support for high-frequency transmission up to 3 GHz.

- May 2025: ouser Electronics expanded Molex product availability to over 180,000 SKUs including HyperQube high-power interconnects and Micro-Fit+ PCIe 5.0 connectors designed for high-current, space-constrained applications. The distribution expansion improves global access to advanced connector technologies supporting EV power electronics and onboard charging systems.

Global EV Connector Market Report Scope

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Hybrid Electric Vehicle (HEV) |

| Wire-to-Wire |

| Wire-to-Board |

| Board-to-Board |

| Others |

| Low Voltage (Less than 60 V) |

| Medium Voltage (60 to 300 V) |

| High Voltage (More than 300 V) |

| Terminal |

| Housing |

| Lock |

| Others |

| AC Connectors |

| DC Connectors |

| Combined Connectors |

| Battery Management System |

| Infotainment System |

| ADAS and Safety System |

| Engine Management and Powertrain |

| Body Control and Interiors |

| Vehicle Lighting |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Propulsion Type | Battery Electric Vehicle (BEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| By Connection Type | Wire-to-Wire | |

| Wire-to-Board | ||

| Board-to-Board | ||

| Others | ||

| By Voltage | Low Voltage (Less than 60 V) | |

| Medium Voltage (60 to 300 V) | ||

| High Voltage (More than 300 V) | ||

| By Component | Terminal | |

| Housing | ||

| Lock | ||

| Others | ||

| By Current Type | AC Connectors | |

| DC Connectors | ||

| Combined Connectors | ||

| By Application | Battery Management System | |

| Infotainment System | ||

| ADAS and Safety System | ||

| Engine Management and Powertrain | ||

| Body Control and Interiors | ||

| Vehicle Lighting | ||

| Others | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the EV connector market in 2025 and how fast is it growing?

The EV connector market size reached USD 2.27 billion in 2025 and is forecast to advance at a 16.48% CAGR to 2030.

Which propulsion type requires the most connectors?

Battery Electric Vehicles dominate, accounting for 68.42% of 2024 revenue due to high-voltage drivetrain and charging content.

Why are 800 V systems important for connector demand?

800 V architectures shorten charging times and raise power density, which elevates voltage ratings and complexity of connectors and therefore boosts value per vehicle.

What region leads sales of EV connectors?

Asia-Pacific leads with 44.09% share thanks to China’s large BEV production and established electronics supply chains.

How will the shift to NACS affect suppliers?

SAE J3400 adoption triggers a retrofit wave for adapters in the near term and standardizes ports in new vehicles, benefiting manufacturers that already support Tesla-style interfaces.

What is the biggest technical challenge at ultra-fast charging sites?

Managing thermal runaway above 350 kW requires liquid-cooled connectors and active temperature monitoring to keep contact resistance stable and ensure user safety.

Page last updated on: