Real Estate and Construction

16th MayMapping Real Estate Opportunities in Bali

4 Min Read

The India Prefab Building Market Report is Segmented by Material Type (Concrete, Glass, Metal, Timber, Other Materials), by Application (Residential, Commercial, Others), by Product Type (Modular Buildings, Panelized & Componentized Systems and Other Prefab Types), and by Cities (Delhi-NCR, Bangalore, Mumbai, Chennai, Hyderabad, Pune, Ahmedabad, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

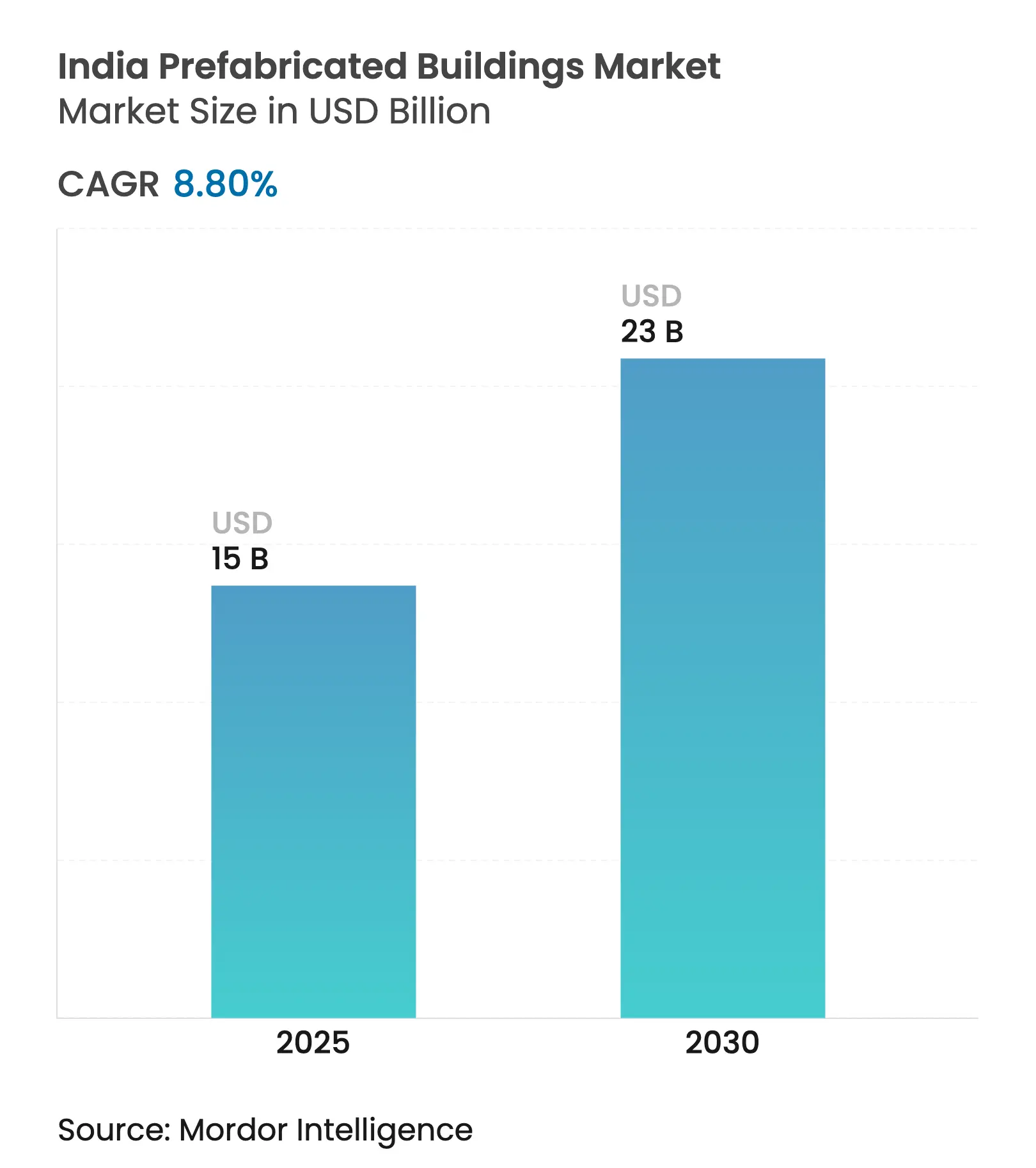

| Market Size (2025) | USD 15 Billion |

| Market Size (2030) | USD 23 Billion |

| Growth Rate (2025 - 2030) | 8.80 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The India prefabriacted building market reached USD 15 billion in 2025 and is expected to reach USD 35.1 billion by 2030 at a CAGR of 8.80% during the forecast period (2025-2030). This expansion shows how a maturing supply base, policy incentives, and digital manufacturing are reshaping construction economics and timelines. Federal housing subsidies worth USD 64.6 billion, a swelling data-center pipeline, and mandatory energy codes create a steady pull for factory-made components. Developers are prioritizing 5% to 6% schedule savings, while suppliers invest in automated plants that cut waste by up to 20%. Fragmented competition is giving way to scale players able to balance low-carbon requirements with cost discipline, keeping barriers to entry manageable but rising. Overall, momentum hinges on policy continuity, transit logistics, and the sector’s success in closing a 45,000-worker skills gap that could temper growth if left unchecked.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government push for affordable housing

Government push for affordable housing

| +1.5% | National, Tier-I and Tier-II cities | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.5%

|

Geographic Relevance

:

National, Tier-I and Tier-II cities

|

Impact Timeline

:

Medium term (2-4 years)

|

Rapid urbanization & housing shortfall

Rapid urbanization & housing shortfall

| +1.2% | Mumbai, Delhi-NCR, Bangalore, Chennai | Long term (≥ 4 years) | |||

Warehousing & data-center boom

Warehousing & data-center boom

| +1.1% | Mumbai, Bangalore, Chennai, Hyderabad, Pune | Short term (≤ 2 years) | |||

Tech leap: BIM, 3-D printing & precast

Tech leap: BIM, 3-D printing & precast

| +1.0% | Metro technology hubs | Medium term (2-4 years) | |||

ESG-linked green-building mandates

ESG-linked green-building mandates

| +0.9% | Maharashtra, Karnataka, Tamil Nadu | Long term (≥ 4 years) | |||

Cost-efficient off-site manufacturing

Cost-efficient off-site manufacturing

| +0.8% | Industrial corridors nationwide | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Urbanization Accelerates Demand for Speed-to-Market Solutions

City populations are swelling by nearly 29 million people between 2025-2030, prompting developers to value every day saved on site. Prefab slabs trimmed average build cycles by 34 days in 2024 studies, a clear competitive edge when order backlogs already stand at 3.5 times annual revenue for top EPC firms. Bangalore’s forecast 65% jump in data-center power by 2030 alone calls for fast-tracked halls and utility buildings. Consequently, the India prefab building market is viewed by contractors as a schedule hedge that unlocks faster revenue recognition[1]R. Sharma et al., “Optimising Precast Construction Timelines in Emerging Economies,” Journal of Construction Engineering & Management, ascelibrary.org.

Technology Integration Transforms Construction Efficiency and Quality

BIM-first workflows allow millimeter-level coordination between architects and plants, slashing rework and wastage. India’s newest precast factories, often German- or Italian-equipped, run 24-hour cycles with computerized curing that outperforms site-poured mixes on strength and consistency. Early pilots of 3-D printed formwork reduce material usage by 10%. These digital gains push the India prefab building market toward higher tolerances demanded by data-center MEP layouts, driving quality benchmarks previously rare in mass housing.

ESG Mandates Create Structural Advantages for Low-Carbon Prefab Solutions

Energy Conservation Building Codes, now compulsory in 25 states, favor wall systems with superior insulation and airtightness achievable in factories. Controlled environments cut concrete waste by 15% and allow the inclusion of recycled aggregates, helping builders meet ESG disclosures under new stock-exchange rules. Because only 5% of India’s built stock is green-certified, prefab manufacturers see headroom to embed low-carbon components and win premium pricing. Such compliance benefits fortify the India prefab building market as investors tilt portfolios toward sustainable assets[2]Saurabh Bharti, “Energy Conservation Building Code 2017 – Status of Implementation,” Bureau of Energy Efficiency, beeindia.gov.in.

Warehousing and Data-Center Boom Drives Large-Span PEB Demand

Logistics operators shifting production from China to India need wide-bay sheds delivered in under six months. Planned capacity of 3.29 GW for hyperscale data centers requires 10 million ft² of airtight halls with integrated cooling plinths. Pre-engineered steel systems offer 30% lighter roofs and column-free interiors, accelerating interior fit-outs. Suppliers able to prefabricate girder assemblies off-site now vie for long-term framework deals, cementing this vertical as the fastest-scaling slice of the India prefab building market[3]Ministry of Electronics & IT Analysts, “India Data Centre Policy Draft 2024,” Ministry of Electronics & IT, meity.gov.in].

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High logistics cost for oversized modules

High logistics cost for oversized modules

| -0.7% | Nationwide, heightened on long routes | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.7%

|

Geographic Relevance

:

Nationwide, heightened on long routes

|

Impact Timeline

:

Short term (≤ 2 years)

|

Scarcity of skilled prefab labor

Scarcity of skilled prefab labor

| -0.5% | Tier-II and Tier-III cities | Medium term (2-4 years) | |||

Fragmented state-level codes

Fragmented state-level codes

| -0.4% | All states | Medium term (2-4 years) | |||

Seismic-safety perception gaps

Seismic-safety perception gaps

| -0.3% | Northern, Western, Northeastern seismic belts | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Logistics Costs Challenge Oversized Module Transportation

Oversized wall and roof cassettes often exceed state axle-load norms, forcing circuitous routes that inflate freight bills by up to 20%. Permit lead times vary widely, three days in Gujarat but 10 days in Uttar Pradesh, complicating project schedules. Battery-electric trucks promise future savings, yet infrastructure gaps and high upfront costs delay mass adoption. Until multi-state corridors harmonize rules, this drag will continue to clip gains for long-span PEB suppliers serving the India prefab building market.

Skilled Labor Shortage Limits Installation and Fabrication Capacity

Even with labor efficiencies, top EPC firms reported a 15% shortfall in certified crane operators and welders in early 2025. Turnover among site supervisors exceeds 10% annually as competing sectors offer higher pay. Urban skill centers are raising prefab-specific curricula, but Tier-III clusters lag, curbing factory output scalability. Hence, workforce scarcity remains a medium-term cap on how quickly the India prefab building market can absorb new demand.

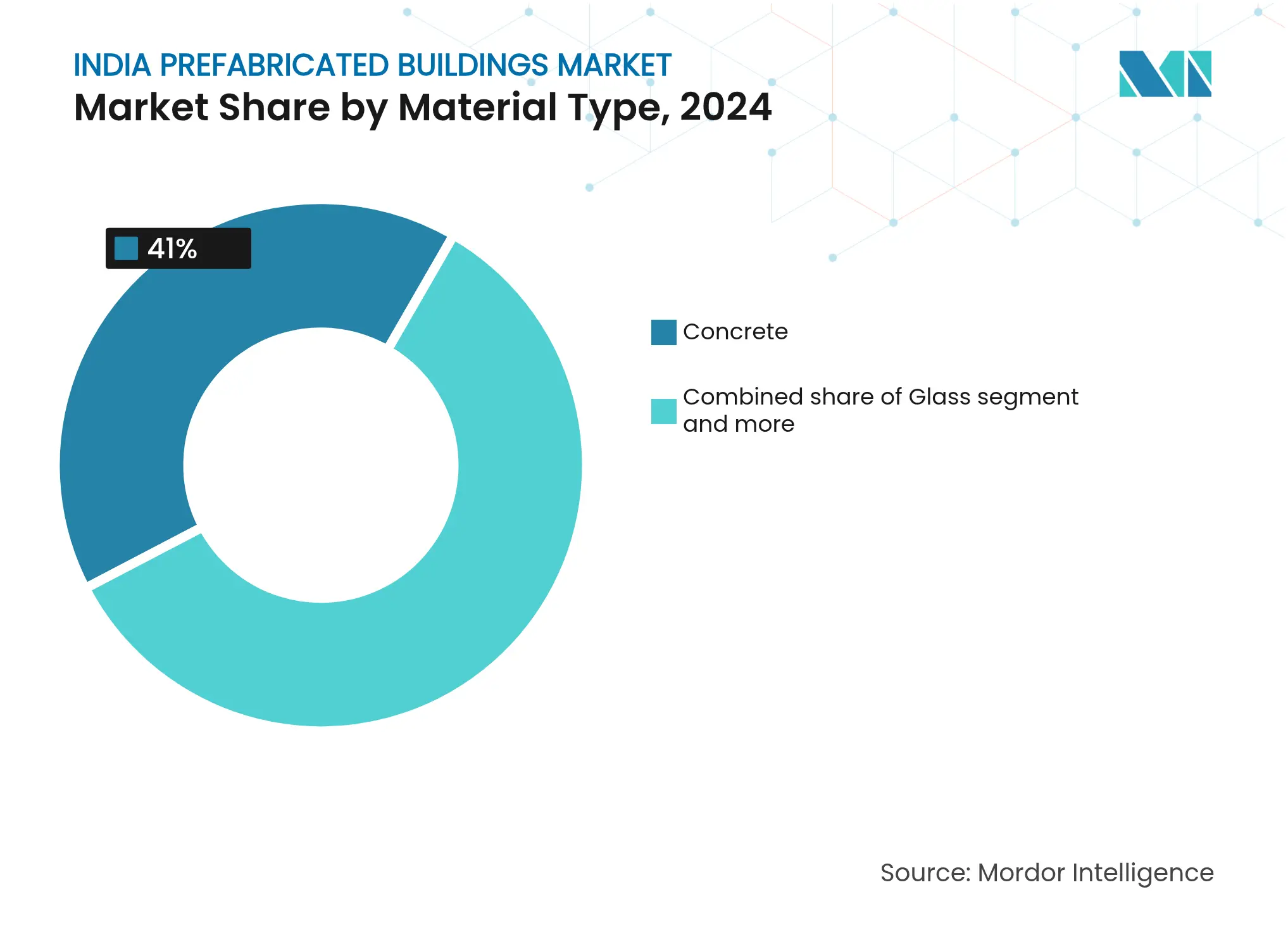

By Material Type: Concrete Dominance Meets Timber Innovation

Concrete held 41% of the India prefab building market in 2024, thanks to its seismic reliability and ready supply chains. Its alignment with national design codes means contractors face minimal re-engineering, preserving margins. Producers now tweak mix designs with recycled aggregates and steel fibers to hit newer ECBC insulation targets, making concrete viable for data centers seeking high thermal inertia. Timber’s 9.71% CAGR outlook benefits from engineered wood lines entering the western region; CLT panels shave floor cycles and lock in lower embodied carbon scores, a plus for ESG-minded funds. Stakeholders see potential policy incentives to widen timber sourcing, although import tariffs still add cost friction.

Demand for glass and composite skins is rising in Tier-I offices where aesthetics and daylighting carry weight. Metal decking continues gaining in multistory industrial parks, favored for speed and compatibility with hybrid concrete columns. As GRIHA points grow more valuable, timber and composite hybrids could erode concrete’s lead, yet price stability keeps concrete the material of choice across low-to-mid-rise housing—still the lion’s share of the India prefab building market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Residential Leadership with Commercial Momentum

Residential projects accounted for 52.1% of the India prefab building market size in 2024, driven by subsidy-backed township rollouts. Developers exploit 20% cost savings and near-zero rework to hold unit prices, critical in low-income segments. Large public contracts bundle thousands of units, enabling factories to run at 80%-plus capacity for months, an efficiency rarely possible in bespoke commercial work. Yet commercial builds are projected to outpace with a 9.26% CAGR as cloud providers and third-party logistics firms lock in multi-year expansion budgets. Their preference for turnkey PEB packages compresses design timelines, shifting value toward suppliers offering integrated MEP and fire-safety modules.

Institutional and infrastructure precast, metro stations, and flyover girders add diversification, ensuring plants are not solely reliant on housing cycles. However, housing’s high policy visibility means any subsidy cuts or code delays could quickly ripple across the India prefab building market and dampen plant utilization rates.

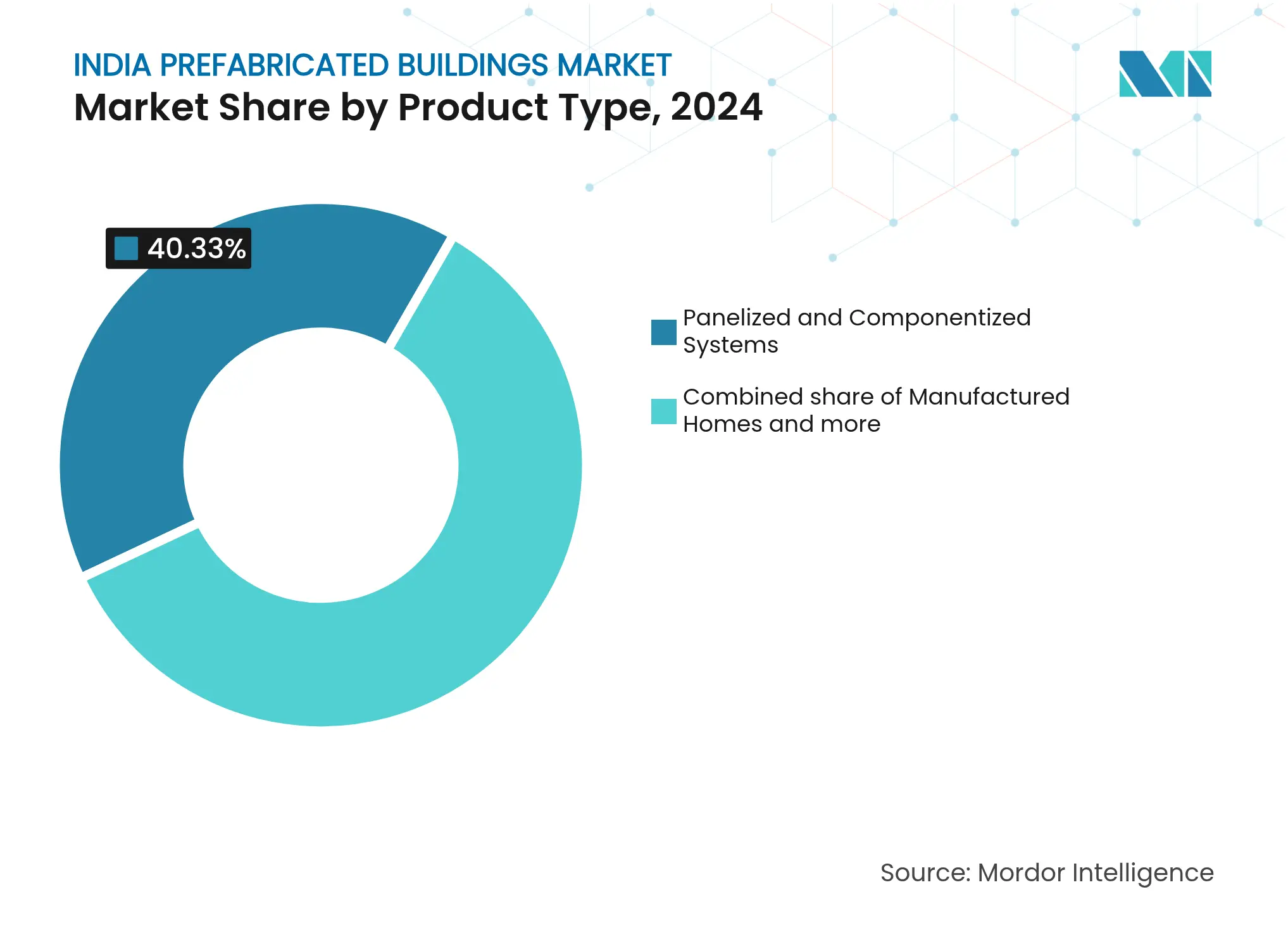

By Product Type: Modular Buildings Lead, Panelized & Componentized Systems Accelerate

Modular buildings commanded 40.33% of the India prefab building market share in 2024, reflecting their ability to deliver fully finished units that drop into place with limited site work. Factory assembly improves quality control, and the PMAY-U Beneficiary-Led vertical reimburses households that choose standardized modules, driving demand among cost-sensitive buyers. Suppliers highlight 60-year durability testing and lower operating energy, advantages that resonate with peri-urban middle-income segments where land parcels are often compact. Relocatable manufactured homes on steel chassis maintain a niche in flood-prone districts, giving families flexibility when seasonal risks rise.

Panelized and componentized systems are set to grow at a 9.62% CAGR through 2030, the fastest rate among all product categories in the India prefab building market size. Their appeal lies in balancing factory precision with on-site adaptability, allowing contractors to tweak wall and floor layouts without costly retooling. Makers now embed wiring and plumbing inside panels, boosting on-site productivity and trimming project timelines. Hybrid products such as steel core pods wrapped in aerated concrete are gaining favor in upscale resorts that want design freedom without sacrificing speed. Most market watchers expect modular units to retain leadership, yet panelized solutions will continue expanding as developers blend mass production with project-specific creativity.

Note: Segment shares of all individual segments available upon report purchase

While the adoption of prefab building concepts in India varies across regions, the progress is clear. Delhi-NCR has taken the lead, thanks to early policy trials and a strong presence of engineering consultants. The city's bylaws requiring seismic retrofits have driven demand for lightweight FRP panels, which reduce the load on existing foundations. In Mumbai, a USD 11 billion metro expansion, combined with the development of private warehouse parks, has pushed suppliers to create saline-resistant coatings suited for coastal conditions. Bangalore, with a robust 9.88% CAGR, is leading growth due to hyperscale data centers and tech-park towers. These projects are standardizing MEP shafts for prefab pod installations, while the city's skilled workforce is accelerating the adoption of BIM, essential for meeting tight installation schedules.

Chennai and Hyderabad are experiencing similar trends, with aerospace and pharmaceutical clusters requiring clean-room facilities that meet both seismic and hygiene standards. Hybrid steel-concrete modules are addressing these needs, offering suppliers opportunities across multiple sectors. Pune's automotive corridors are favoring high-bay paint-shop structures, which align well with craned PEB roofs. Outside the major metros, the Rest of India accounts for 36.10% of the market share in 2024, reflecting the growing influence of Smart-City initiatives and state housing programs. Tier-II cities like Indore and Lucknow are utilizing federal viability-gap funds to introduce prefab solutions in public buildings such as schools and clinics. While improved freight corridors are reducing lead times, inconsistencies in permits remain a challenge, complicating module transportation across state borders and slowing large-scale deployment in India's prefab building market.

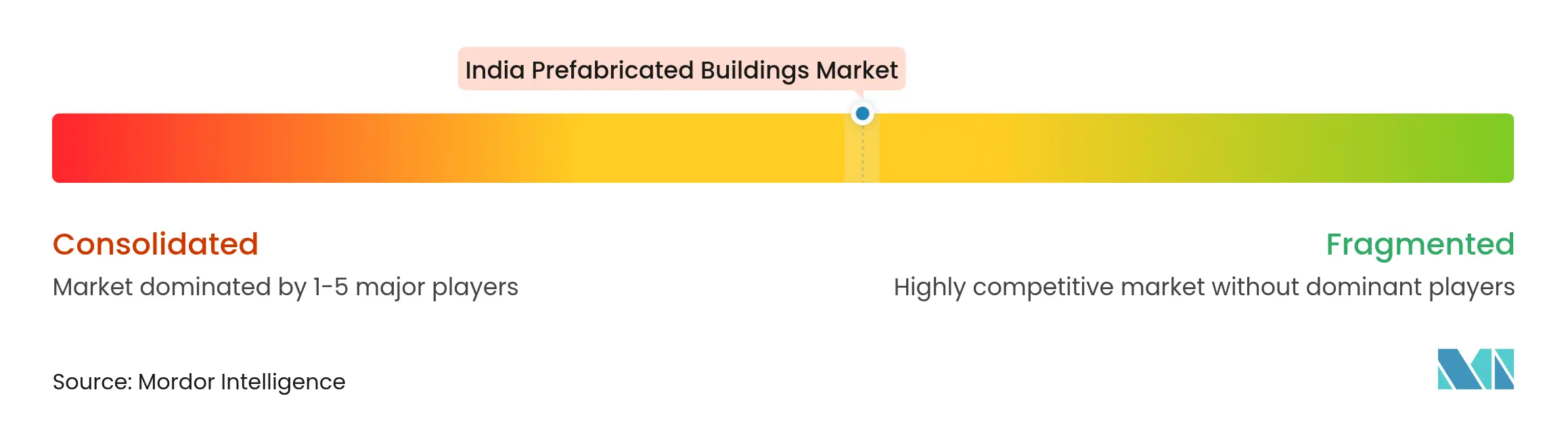

Market Concentration

The India Prefabricated Buildings Market remains moderately fragmented, with a diverse range of companies contributing to the market's overall revenues. Tata BlueScope has set up a USD 106 million greenfield plant, emphasizing automated roof-and-wall roll forming, a move that underscores a shift towards scale economics. EPACK Prefab’s partnership with Hisense showcases its capability to produce one million RAC chassis, marking a strategic move into HVAC sub-assemblies. Both Interarch and Kirby are focusing on wide-span steel for logistics parks, utilizing patented taper-beam sections to reduce tonnage. Meanwhile, mid-tier players are pursuing niche contracts, from seismic core pods in Uttarakhand to timber villas in Goa and container-based classrooms in Assam.

Technology investments have emerged as the primary battleground. Companies that integrate BIM-to-factory data loops can provide quicker quotes and manage warranty risks more effectively. Sustainability credentials further differentiate players; those certifying EPDs for low-carbon panels are witnessing heightened demand from ESG-focused debt investors. Yet, surging steel prices are squeezing margins, prompting companies to secure long-term supplies from mills or to investigate scrap-based electric-arc alternatives. In the broader landscape, supplier bargaining power remains dynamic; while customers emphasize speed and reliability, tech-savvy incumbents gain an advantage, and nimble specialists continue to thrive in less saturated regions of the Indian prefab building market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

A prefabricated building, informally a prefab, is a building that is manufactured and constructed using prefabrication. It consists of factory-made components or units transported and assembled on-site to form the complete building.

The Indian prefabricated buildings market is segmented by material type (concrete, glass, metal, timber, and other material types) and by application (residential, commercial, and other applications [industrial, institutional, and infrastructure]). The report offers market size and forecasts for India's prefabricated buildings industry in value (USD) for all the above segments.

Mapping Real Estate Opportunities in Bali

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.