Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9 Billion |

| Market Size (2026) | USD 9.59 Billion |

| Market Size (2031) | USD 13.25 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Agrochemicals Industry Analysis by Mordor Intelligence

India Agrochemicals market size in 2026 is estimated at USD 9.59 billion, growing from 2025 value of USD 9 billion with 2031 projections showing USD 13.25 billion, growing at 6.66% CAGR over 2026-2031. Strong domestic manufacturing capacity, expanding export pipelines, and policy incentives that favor sustainable inputs are propelling this momentum. India remains the fourth-largest global producer, shipping finished products worth USD 5 billion each year to destinations in Europe, Southeast Asia, and West Africa [1]Source: S. Amin, “India’s Crop-Protection Exports Scale New High,” epw.in. Formulation science is also evolving, nano-nutrient liquids and water-dispersible granules are gaining farmer acceptance because they cut dosage rates and improve field safety. Nonetheless, raw-material dependence on China and a patchwork of state-level toxicity bans continue to inject cost volatility and compliance complexity into the India agrochemicals market.

Key Report Takeaways

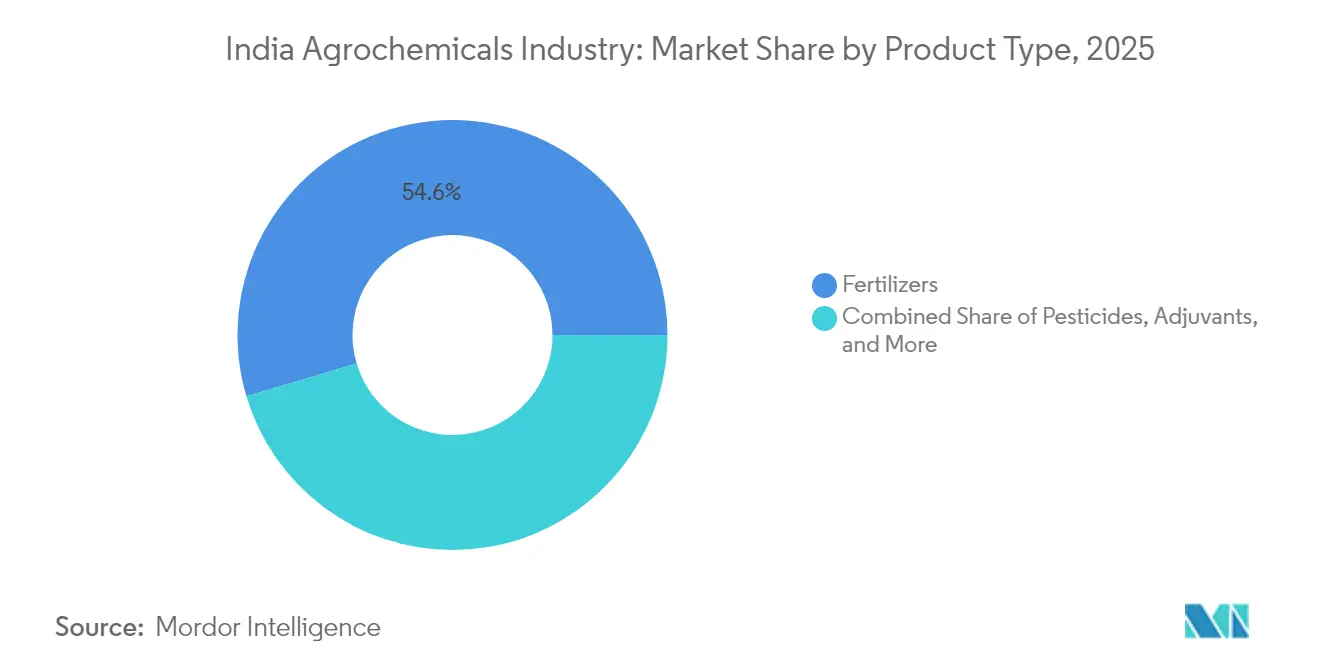

- By product type, fertilizers captured 54.60% of the India agrochemicals market share in 2025, while pesticides are on track to expand at a 10.12% CAGR through 2031.

- By application, grains and cereals accounted for 46.75% of the India agrochemicals market size in 2025, whereas fruits and vegetables are projected to accelerate at a 8.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Agrochemicals Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidy rationalization spurring bio-inputs adoption | +1.8% | National, with early gains in Maharashtra, Punjab, Karnataka | Medium term (2-4 years) |

| Digitized agri-credit and e-commerce platforms expanding chemical reach | +1.2% | National, concentrated in Uttar Pradesh, Bihar, and West Bengal | Short term (≤ 2 years) |

| Drone-based precision spraying is unlocking untapped smallholder demand | +0.9% | North India and Western states, spill-over to South India | Medium term (2-4 years) |

| Off-patent molecule wave enlarges export pipeline | +1.4% | Global export markets, domestic manufacturing hubs in Gujarat, Maharashtra | Long term (≥ 4 years) |

| Climate-linked pest outbreaks are increasing pesticide intensity | +0.7% | National, with acute impact in Punjab, Haryana, Maharashtra | Short term (≤ 2 years) |

| Government schemes boosting domestic manufacturing capacity | +1.1% | National, concentrated in Gujarat, Maharashtra, and Andhra Pradesh | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidy Rationalization Spurring Bio-inputs Adoption

New subsidy frameworks reward states for curbing blanket fertilizer consumption and channel budgetary support toward compost, biofertilizers, and nano-nutrient liquids. The 2025 Union Budget set aside for agriculture and launched the Prime Minister Dhan-Dhanya Krishi Yojana, creating a formal mechanism to reimburse farmers who switch to certified biologicals [2]Source: Staff reporter, “Subsidy Shift to Bio-fertilisers in Union Budget,” pib.gov.in. Parallel programs such as PM-PRANAM link disbursements to chemical reduction targets, encouraging administrators to fast-track training modules and field demonstrations.

Digitized Agri-credit and E-commerce Networks Widening Last-mile Reach

Government-funded digital infrastructure now integrates land records, soil health cards, and Kisan Credit Card limits into a unified farmer registry, allowing input companies to vet credit profiles in minutes and dispatch orders through app-based platforms. In 2024, Indian Farmers Fertiliser Cooperative Limited (IFFCO) e-Bazar, for instance, fulfilled more than 200,000 online transactions in the past fiscal year and delivered to 27,000 pin codes, a scale previously unimaginable for bulk inputs. For the India agrochemicals market, these digital rails translate into higher off-take of premium formulations, especially in tier-II districts where assortment depth had long been a constraint.

Drone-based Precision Spraying Unlocking Smallholder Demand

Government subsidies of up to 40% on drone purchases and service vouchers have lowered entry barriers for custom-hire entrepreneurs. Demonstration drives led by IFFCO covered 3 million acres across 12 states and proved that a single drone can spray one acre of paddy in under six minutes while trimming water use by 90%. As adoption grows, the India agrochemicals market benefits from higher demand for ultra-low-volume concentrates and adjuvants tailored for aerial application.

Off-patent Molecule Wave Expanding Export Pipeline

Three out of every four active ingredients sold globally are no longer under patent, opening a technology corridor for cost-competitive Indian producers. With 60% of sector revenue already export-linked, firms located in Gujarat’s Dahej and Maharashtra’s Tarapur clusters are scaling backward integration to secure intermediaries and cut freight costs. Overall, the driver reinforces the long-term growth arc of the Indian agrochemicals market by widening its global addressable base and incentivizing technology upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Disruptive raw-material dependence on China is raising cost volatility | -1.6% | National manufacturing hubs, particularly Gujarat, Maharashtra | Short term (≤ 2 years) |

| Accelerating state-level bans on high-toxicity actives | -0.8% | National, with early implementation in Kerala, Punjab, Maharashtra | Medium term (2-4 years) |

| The growing counterfeit channel is eroding branded volumes | -0.5% | National, concentrated in Uttar Pradesh, Bihar, Madhya Pradesh | Medium term (2-4 years) |

| Intensifying resistance to legacy insecticides | -0.4% | National, acute in Punjab, Haryana, Maharashtra cotton belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Disruptive Raw-material Dependence on China Raising Cost Volatility

Indian plants import a bulk of technical intermediates such as bismuth, tellurium, and graphite from Chinese suppliers, leaving local formulators exposed to price swings and shipping delays during geopolitical flashpoints. Domestic producers must carry higher safety stocks, locking working capital and eroding margins when global freight rates spike. Government task forces have identified 10 critical minerals where India is 100% import-dependent and are drafting incentive packages to fast-track alternative sources.

Accelerating State-level Bans on High-toxicity Actives

Kerala, Punjab, and Maharashtra are leading a regulatory wave that restricts or phases out molecules flagged by the World Health Organization as highly hazardous. More than one-third of India’s 339 registered pesticides now fall into a watch list that could shrink portfolios if central or additional state authorities follow suit. The result is a mixed demand signal. While legacy sales taper off, safer bio-rational alternatives gain traction, slightly muting overall value growth in the India agrochemicals market during the transition phase.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fertilizers Lead Despite pesticides Surge

Fertilizers captured 54.60% of the India agrochemicals market size, and continue to anchor food security policies for rice, wheat, and sugarcane systems. Di-ammonium phosphate and urea dominate volumes, yet escalating subsidy reforms are nudging growers toward micronutrient blends and nano-liquids that minimize groundwater contamination.

Pesticides, though starting from a smaller base, are projected to add nearly incremental sales by 2031 at a 10.12% CAGR, underpinned by compost incentives, residue-linked export standards, and expanding organic certification acreage. The rising popularity of microbial consortia and seaweed-based stimulants is encouraging conventional fertilizer majors to launch dedicated bio-divisions. Producers that master shelf-life extension, cold-chain independent packaging, and farmer education stand to capture early mover loyalty.

By Application: Grains Drive Volume While Horticulture Accelerates

Grains and cereals commanded 46.75% of the India agrochemicals market size in 2025, reflecting the scale of paddy, wheat, and maize acreage across the Indo-Gangetic plain. Government procurement price floors insulate growers from cyclical dips and sustain input demand even in sub-normal monsoon years. Fruits and vegetables, while contributing a smaller revenue share today, are projected to expand at a 8.78% CAGR as export-class mangoes, grapes, and bananas shift to trellis, fertigation, and climate-controlled environments that lift input intensity.

Demand for residue-compliant fungicides and biorational insecticides is rising in greenhouse clusters around Pune, Bengaluru, and Nashik. Oilseed and pulse acreage are relatively price-sensitive but benefit from national self-sufficiency missions that subsidize sulfur-rich fertilizers and bio-nitrogen fixers.

Geography Analysis

West India plays a significant role in the market, on the back of Maharashtra’s sugarcane mills and Gujarat’s cotton ginners, both of which rely on high nutrient and pesticide loads to protect yields. Proximity to deep-sea ports and chemical parks further shortens supply chains . South India is projected to clock impressive growth as horticulture clusters in Tamil Nadu, Karnataka, and Andhra Pradesh migrate to greenhouse and precision-fertigation systems that multiply per-acre agrochemical spends.

South India is the most dynamic theatre for premium inputs. Greenhouse vegetable acreage around Bengaluru has doubled in five years, stimulating demand for residue-free biofungicides, amino-acid chelates, and drone-calibrated micronutrient cocktails. Andhra Pradesh’s aquaculture boom feeds back into allied crop sectors by augmenting farmer incomes that are reinvested in high-density banana and papaya orchards requiring weekly pest-scouting and corrective sprays. Importantly, logistical corridors through Chennai, Krishnapatnam, and Tuticorin ports support back-haul efficiencies for suppliers, lowering landed costs.

North India’s wheat-rice-mustard rotation keeps baseline volumes high, yet groundwater ordinances in Punjab and Haryana are persuading growers to adopt direct-seeded rice and laser leveling. These practices cut irrigation requirements but also marginally lower pre-emergence herbicide usage. Bihar and Uttar Pradesh remain candidates for rapid growth as the government ramps up rural warehousing and cold-chain funding, thereby upgrading market linkages that reward better quality.

Regulatory Landscape

Crop protection regulation in India continues to be governed by the Insecticides Act, 1968, with pesticide registrations and related oversight handled by the Central Insecticides Board and Registration Committee (CIBRC) under the Directorate of Plant Protection, Quarantine and Storage (PPQS). In practice, market access for new and existing products depends on CIBRC registrations (including pathways under Section 9(3), 9(3B), and 9(4)) and ongoing compliance with licensing and record-keeping requirements through the CROP portal hosted on PPQS systems.

In June 2026, the Ministry of Agriculture and Farmers Welfare notified the Insecticides (Amendment) Rules, 2026 (G.S.R. 493(E), dated 17 June 2026), moving the framework toward mandatory digital-first licensing and compliance, with an implementation timeline triggered from publication. In parallel, the draft Pesticides Management Bill, 2025 has been circulated for public consultation and proposes institutional changes (including a Central Pesticides Board) and stricter penalties, raising compliance stakes around quality, traceability, and spurious products while the 1968 Act remains operative.

Competitive Landscape

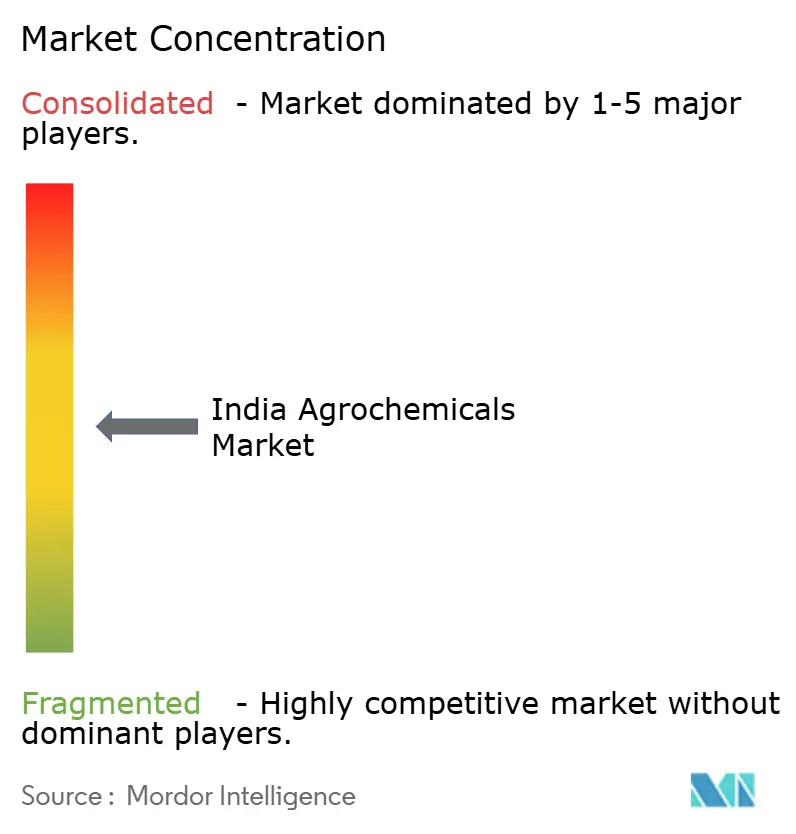

The supply side is moderately fragmented, the top five manufacturers together creating room for niche specialists in biologicals, micronutrients, and drone-compatible ultra-low-volume concentrates. UPL leads and complements its 25,000-dealer footprint with a data-rich Nurture Farm platform that pushes advisory messages to more than 3 million mobile numbers each week.

Strategic collaborations are multiplying. UPL and Aarti Industries have formed a 50:50 joint venture focused on specialty amines and other high-value intermediates, aiming for a USD 60 million annual turnover within three years. Chemplast Sanmar is investing to double its custom-manufacturing capacity for active ingredients near Cuddalore, signaling confidence in the export-linked visibility of its pipeline. Meanwhile, Sharda Cropchem, a formulators-turned-registration specialist, is broadening its European dossiers to hedge against price competition in saturated post-patent molecules.

Technology integration is now a decisive battleground. Crop-scouting AI modules, sachet-sized drone payloads, and SKUs equipped with encrypted QR codes for anti-counterfeit tracking are redefining value propositions. Producers that embed stewardship training for resistance management and safe-handling practices into their sales model are likely to gain regulatory goodwill as well. Over the forecast period, consolidation is projected in commodity herbicides, while differentiated biologicals attract venture-funded startups eager to plug knowledge gaps in rapid field validation protocols. Such cross-currents keep competitive intensity high, yet they collectively elevate product sophistication across the India agrochemicals market.

India Agrochemicals Market Leaders

Bayer AG

IFFCO

Syngenta India Private Limited

UPL Ltd.

PI Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Digital compliance for pesticides is creating room for solution providers and organized manufacturers to operationalize traceability, e-records, and faster regulatory interactions at scale. The June 2026 Insecticides (Amendment) Rules, 2026 reinforces the need for online submissions and structured compliance processes, which supports investment in data systems, QR/serialization workflows, and distributor-level governance. These capabilities also align with efforts to address counterfeit and sub-standard inputs.

On the supply side, India is adding formulation and technical capacity in key chemical clusters, consistent with stronger domestic manufacturing and export pipelines in the report context. In February 2026, Crystal Crop Protection announced an investment of INR 100 crore in a greenfield formulation plant at Jhagadia, Gujarat (stated initial capacity of 50,000 MTPA and expansion potential), while March 2026 announcements such as Advance Agrolife capacity additions in Rajasthan indicate continued build-out in herbicide intermediates and actives. On the demand creation side, the Union Budget 2026-27 proposal for Bharat-VISTAAR, a multilingual AI advisory layer integrating AgriStack and ICAR packages, expands the channel for tailored product-use guidance, which can support adoption of differentiated bio-inputs, nano-nutrient liquids, and precision-application compatible formulations already gaining acceptance in India.

Recent Industry Developments

- July 2026: PI Industries launched Pioxaniliprole, positioned as an India-discovered crop protection molecule. The launch indicates a step-up from formulation and scale manufacturing toward domestic R&D-led innovation, which can broaden differentiated portfolios and improve competitiveness in post-patent markets.

- May 2026: UPL secured Fertilizer Control Order (FCO) registration in India for Bioclassic, a biostimulant from its Natural Plant Protection (NPP) unit. This strengthens UPLs biologicals stack in a regulatory framework that governs many non-pesticide input categories and supports deeper penetration into sustainable input programs and modern trade channels.

- July 2025: The Government of India signed the India-UK Free Trade Agreement, covering tariff elimination on a large share of tariff lines including organic chemicals and agrochemical products. The agreement improves export economics for Indian manufacturers selling into the UK and supports the report theme of expanding export pipelines from domestic production hubs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the India agrochemicals market is defined as the value of products used on farm fields to improve yield and protect crops, covering fertilizers, crop-protection chemicals (synthetic and bio-based), plant growth regulators, adjuvants, and biostimulants.

Scope exclusions: Home-garden packs and upstream bulk chemical intermediates are not counted in the market value.

Segmentation Overview

- By Product Type

- Fertilizers

- Nitrogenous

- Phosphatic

- Potassic

- Other Fertilizers

- Pesticides

- Herbicides

- Insecticides

- Fungicides

- Other Pesticides

- Adjuvants

- Plant Growth Regulators

- Fertilizers

- By Application

- Cereals and Grains

- Pulses and Oilseeds

- Fruits and Vegetables

- Commercial Crops

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for demand, pricing, and the policy environment that shapes agrochemical use in India. We referred to public sources such as the Ministry of Agriculture and Farmers Welfare, the Directorate of Plant Protection, Quarantine and Storage, FAOSTAT, and national statistics for crop area and production, which help anchor usage intensity by crop.

To avoid building the model only from broad averages, the desk work also used supporting sources such as customs trade statistics, peer-reviewed agronomy and pest-pressure literature, and pesticide registration and regulatory notifications that indicate which actives and formulations are in active use. We checked company annual reports, investor decks, association websites, and reputed press for product mix signals and channel changes. A paid subscription for company financials and a shipment-level trade view were also used selectively where public series had gaps. These sources are indicative and not exhaustive, and many other references were used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what farmers actually buy in India, how volumes shift by season, and how pricing moves through distributors and retailers. We spoke with a spread of stakeholders such as manufacturers, formulators, distributors, large farm operators, and agronomy advisors across key growing belts, so desk assumptions could be corrected where on-ground behavior differed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 18% | |

| Mid tier: 46% | Functional/Unit leaders: 31% | |

| Smaller Players: 18% | Managers: 51% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where crop area and cropping intensity are converted into a demand pool using crop-wise application norms and adoption levels for key inputs. That demand pool is then priced using India-appropriate average selling prices, which are adjusted for formulation mix and seasonality, and then carried to a yearly value.

Once that picture is formed, it is checked with selective bottom-up approximations so totals do not drift away from reality. We used sampled company revenue splits, channel checks on traded volumes, and a simple volume times price sanity check for major product groups. For India, inputs were kept practical, such as monsoon and drought patterns, shifts in crop acreage, pest and disease incidence signals, changes in subsidy and regulatory actions, and import and export movements that affect local availability. Where bottom-up coverage is patchy for smaller suppliers, we fill gaps using conservative penetration ranges agreed in interviews, and then re-test the totals against independent indicators.

For forecasting, scenario analysis was used to reflect the way weather variability and policy decisions can change demand quickly. Assumptions were aligned to what experts see for planted area, input intensity, and price movement over the period. The final forecast is therefore a controlled extension of observed drivers rather than a single straight-line growth number.

Data Validation & Update Cycle

Validation is done through repeated cross-checks so that one data series does not dominate the final output. Model totals are compared against independent signals such as crop output trends, trade flows, and known changes in product availability, and then large variances are investigated before sign-off.

A multi-step internal review is followed, where assumptions, conversions, and currency treatments are rechecked, and outliers are traced back to the input line that caused them. If a variance cannot be explained, respondents are re-contacted and the desk sources are revisited until the logic is consistent. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed to reflect the latest developments.

Mordor Intelligence's India Agrochemicals Market Size Versus Other Published Estimates

Published market values for India agrochemicals often do not match, even when the title looks similar, because the product scope and pricing points can shift the total meaningfully. Differences also come from the year chosen as the base, how imports and exports are treated, and whether estimates rely more on supply-side reporting or on-field consumption behavior.

The main gap drivers here are whether fertilizers are included alongside crop-protection products, whether bio-based inputs and adjuvants are counted, and whether values are captured before or after retail mark-ups. Another common difference is the use of aggressive versus conservative price progression. This is especially noticeable when currency timing and inflation assumptions are not stated clearly, and when the refresh cadence is slower than recent regulatory and monsoon-driven swings.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.59 B (2026) | |

| Industry Publisher A | USD 9.00 B (2025) | Uses an earlier base year and a different forecast window, and the product mix treatment across fertilizers, pesticides, and biostimulants is not fully transparent, which can shift totals when adoption rates change by season. |

| Global Consultancy B | USD 33.16 B (2023) | Appears to use a broader value pool that can fold in wider agriculture input categories and pricing layers, which inflates the number versus a farm-field application view that prices before retailer mark-ups. |

The table shows that the spread is mostly explained by what is counted as agrochemicals and where the price is captured in the chain. When fertilizers, bio-based inputs, and related categories are treated differently, the total can move by multiples, and this is why a clear farm-field use scope and consistent pricing point were enforced. This is a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current size of the India agrochemicals market?

The market stands at USD 9.59 billion in 2026 and is projected to reach USD 13.25 billion by 2031.

Which product category holds the largest share?

Fertilizers lead with 54.60% of revenue in 2025, reflecting continued reliance on conventional nutrients.

How fast are fruits and vegetables segment is growing?

Fruits and vegetables are forecast to advance at a 8.78% CAGR through 2031, the fastest rate among all product types.

Which region shows the strongest growth outlook?

South India is projected to grow at an 7.95% CAGR between 2026 and 2031, driven by high-value horticulture expansion.

How are government policies shaping market demand?

Subsidy reforms favor bio-inputs, while drone and digitization incentives broaden access to precision application technologies.

Page last updated on: