India Agricultural Tractor Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2025) | USD 7.92 Billion |

| Market Size (2030) | USD 10.95 Billion |

| Growth Rate (2025 - 2030) | 6.70% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Agricultural Tractor Market Analysis by Mordor Intelligence

The India agricultural tractor market size stands at USD 7.92 billion in 2025 and is forecast to reach USD 10.95 billion by 2030, advancing at a 6.70% CAGR. This growth is tied to direct‐benefit transfer programs, emission compliance deadlines, and state-backed mechanization funds that shape procurement cycles. Expanding solar pump coverage, the rapid digitalization of used-equipment platforms, and the adoption of precision agriculture are widening the customer base, while a gradually tightening credit environment tempers momentum. Regional demand is highly concentrated in the northern plains, and western states have recently registered the quickest expansion as diversified crop portfolios justify premium equipment.

Key Report Takeaways

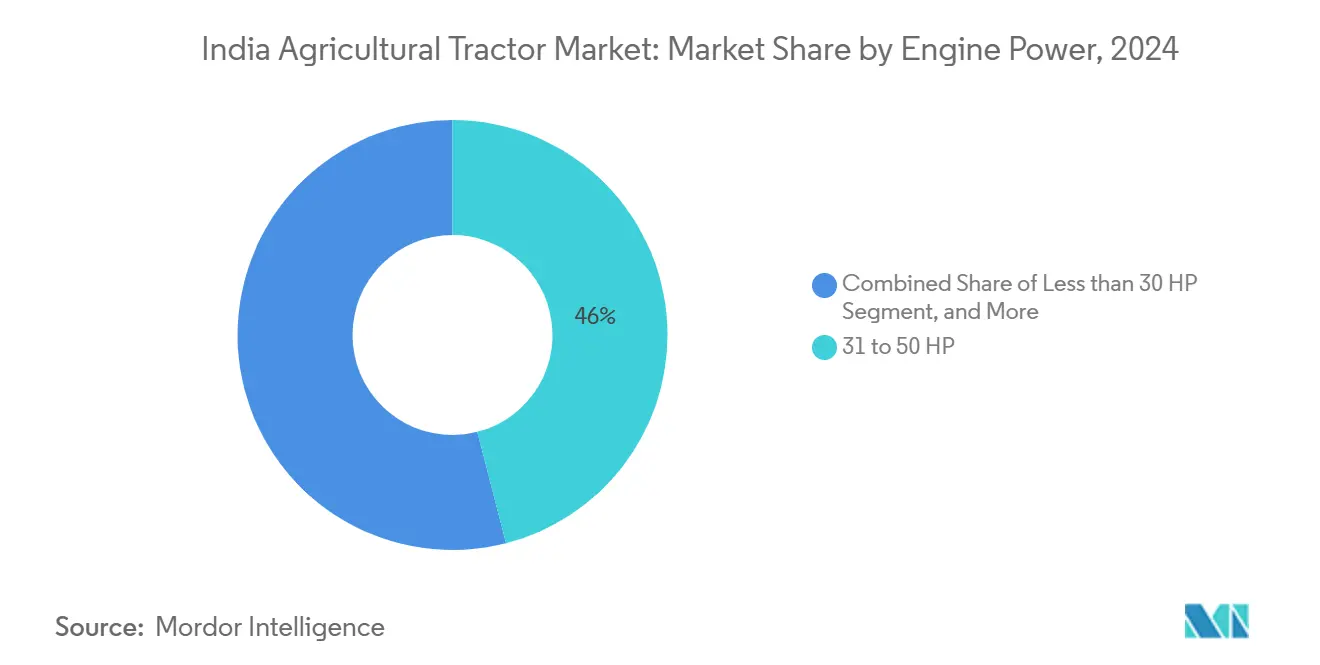

- By engine power, the 31 to 50 HP category led the India agricultural tractor market in 2024, accounting for 46% of the market size, while the 51 to 80 HP segment is projected to post a 9.3% CAGR through 2030.

- By drive type, two-wheel drive units accounted for 87% of the India agricultural tractor market size in 2024, whereas the four-wheel drive units are projected to grow at a 11.1% CAGR to 2030.

- By application, row-crop tractors accounted for 58% of the India agricultural tractor market share in 2024, while the orchard tractors are growing at an 8.4% CAGR through 2030.

- The India agricultural tractor market exhibits high concentration, with Mahindra & Mahindra Ltd., Escorts Kubota Limited, Tractors and Farm Equipment Limited (TAFE), Deere & Company, and Sonalika Group contributing a substantial share of the market revenue.

India Agricultural Tractor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy-linked demand spikes after PM-Kisan Direct Benefit transfers | +1.8% | National, highest in Uttar Pradesh, Bihar, West Bengal | Medium term (2–4 years) |

| Rapid tractor fleet electrification pilots in sugar-cane belts | +0.7% | Maharashtra, Uttar Pradesh, Karnataka | Long term (≥ 4 years) |

| Formalization of used-tractor marketplaces improving upgrade cycles | +1.2% | National, early gains in Punjab, Haryana, Gujarat | Short term (≤ 2 years) |

| Minimum Support Price (MSP) indexation favoring mid-HP tractor sales | +1.5% | Punjab, Haryana, Uttar Pradesh, Madhya Pradesh | Medium term (2–4 years) |

| Drone-ready hitching systems boosting cross-selling | +0.6% | Gujarat, Maharashtra, Karnataka, Tamil Nadu | Long term (≥ 4 years) |

| On-farm solar-pump schemes raising tractor PTO (Power Take-Off) utilization | +0.9% | Gujarat, Rajasthan, Maharashtra, Andhra Pradesh | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Subsidy-Linked Demand Spikes After PM-Kisan Direct Benefit Transfers

Quarterly PM-Kisan disbursements of USD 2.5 billion in August 2025 infused liquidity, resulting in a surge in tractor finance applications within six weeks [1]Source: Press Information Bureau, “Benefits Transferred to Farmers under PM-Kisan Crosses Rs 3 Lakh Crores,” pib.gov.in. Beneficiary farmers recently covered up to 20% of a down payment on 31–50 HP models, reinforcing cyclical surges that producers synchronize with payment calendars. The tractor industry in the Indian market, therefore, tracks fiscal flows more closely than crop-seasonality alone. Manufacturers hedge volatility by splitting production runs between mid-range volumes and premium variants, while dealers preload inventory before each installment release. Digital payment rails shrink leakages and make sales forecasting more reliable. As long as the annual USD 72 benefit stays intact, the India agricultural tractor market is likely to ride predictable liquidity waves.

Rapid Tractor Fleet Electrification Pilots in Sugar-Cane Belts

Subsidies covering up to 40% of e-tractor acquisition costs under the PM E-DRIVE (PM Electric Drive Revolution in Innovative Vehicle Enhancement) program have triggered pilots, where cane cooperatives have measured 60 to 70% fuel-cost savings per hour. Maharashtra and Uttar Pradesh utilize dense cane clusters, ensuring high utilization and boosting payback prospects. Early adopters retrofit sheds with 30 kW chargers linked to off-peak tariffs. Component makers report a nascent domestic ecosystem for traction batteries, thermal management, and compact inverters. The India agricultural tractor market views electrification as a means to circumvent emission penalties and attract ESG-minded buyers. While current pilot numbers are in the low hundreds, projected declines in battery costs for 2027 could unlock mainstream uptake in the 25 to 35 HP range, especially where solar pumps already improve rural load factors.

Formalization of Used-Tractor Marketplaces Improving Upgrade Cycles

The FARMS (Farm Machinery Solutions) mobile app and similar portals certify listings, which raises resale values by approximately 18% compared to traditional dealers. Better valuations shorten replacement cycles from 12 years to nearer 9, expanding new-tractor addressable demand. Banks recently accept digital service histories as collateral proxies, reducing interest spreads on used-equipment loans. The tractor industry in the Indian market, therefore, benefits from a virtuous loop where orderly second-hand liquidity underwrites first-hand purchases. Platform operators are experimenting with buy-back guarantees that could embed subscription-style business models within five years.

Minimum Support Price (MSP) indexation favoring mid-HP tractor sales

A 1.4–12.5% hike in MSP (Minimum Support Price) for 14 kharif crops is set to inject USD 4.2 billion into farm incomes in 2025. Grain-heavy states like Punjab and Haryana thus renew demand for 31 to 50 HP tractors that pair with harvesters, balers, and choppers suited to rice-wheat rotations. Original Equipment Manufacturers (OEMs) upsell power-take-off kits and telematics bundles that optimize mid-range engine loads. The India agricultural tractor market adapts pricing menus to absorb MSP-induced cash inflows without undermining value perception.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening non-road emission standards (TREM-V) inflating price tags | −1.4% | National, strongest on >50 HP units | Short term (≤ 2 years) |

| Persistent land-holding fragmentation below 1 hectare | −2.1% | Nationwide, severe in Bihar, West Bengal, Kerala | Long term (≥ 4 years) |

| Low telematics adoption limiting financing innovation | −0.8% | Rural zones with poor connectivity | Medium term (2–4 years) |

| Stagnant rural credit growth post-NBFC (Non-Banking Financial Company) liquidity crunch | −1.2% | National, higher impact in Maharashtra, Karnataka, Tamil Nadu | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Tightening Non-Road Emission Standards (TREM-V) Inflating Price Tags

Stage V limits for engines exceeding 37 kW require the addition of emission after-treatment systems, which increase factory costs by 8–12%. Larger Original Equipment Manufacturers (OEMs) localize DOC-DPF modules at new lines such as FPT’s F28 plant in Noida. Smaller brands risk market exit or seeking contract manufacturing. Farmers front-load purchases of pre-stage tractors, causing a demand pull-forward in 2024–25 and a potential trough thereafter. Credit financiers adjust loan tenors to ensure residual values align with regulatory obsolescence. Over time, cost pass-through will normalize as suppliers scale up filter substrates and sensors, but an interim affordability gap dampens the tractor industry's growth in the Indian market.

Low Telematics Adoption is Limiting Financing Innovation

Fewer than 15% of Indian tractors are equipped with telematics, which restricts the usage of usage-based lending and predictive maintenance services [2]Source: World Development, “Opportunities and Challenges of Digital Tools for Tractor Hire,” doi.org . Sparse rural connectivity hinders real-time data transfer, while farmers are concerned about data privacy. Without utilization records, lenders price loans conservatively, which can lead to inflated EMIs. Original Equipment Manufacturers (OEMs) struggle to bundle extended warranties because failure prediction models remain data-starved. Government digital-agriculture missions promise USD 339 million to improve connectivity, still tangible gains hinge on telecom rollouts and farmer training. Until adoption scales, innovative finance that could boost the India agricultural tractor market will remain muted.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Power: Mid-Range Dominance Amid Premiumization

The 31 to 50 HP band holds 46% India agricultural tractors market size in 2024, anchored in plots of 1–3 hectares where versatility outweighs specialized power. Farmers tend to gravitate towards engines that strike a balance between purchase price and fuel efficiency, especially after diesel prices spike. The 51 to 80 HP segment is anticipated to expand at a 9.3% CAGR through 2030, driven by demand for higher torque from multi-crop rotations and increased adoption of balers. Premiumization is gathering pace because TREM-V compliance is pushing base-model prices closer to those of feature-rich trims. GPS guidance, CAN-enabled implement control, and longer service intervals are becoming standard above 50 HP. Mahindra’s thrust into sub-30 HP niches illustrates residual demand for micro-plots, yet financing hurdles temper growth. Above 80 HP units cater to contractors and export crop estates, but remain niche until consolidation advances.

Mid-range tractors are increasingly equipped with telematics that capture hours, load, and fuel, enabling lenders to perform risk scoring. As used-tractor portals mature, residual values for 31 to 50 HP units strengthen, further validating ownership economics. Field trials have demonstrated a 12% increase in productivity when mid-HP tractors are paired with minimal-tillage implements, particularly in rice-wheat systems across the Indo-Gangetic Plain. High-HP modules utilize robotic shift transmissions and electro-hydraulic steering to reduce operator fatigue, but their adoption depends on wage inflation and custom hiring density. The tractor industry in the Indian market thus sees power-band stratification, value retention in the mid-range, innovation in the upper tiers, and affordability pressure in the sub-compact classes.

By Drive Type: Two-Wheel Dominance Faces Four-Wheel Challenge

Two-wheel drive models account for 87% of the India agricultural tractors market share in 2024, making them well-suited for light soils and shallow seedbeds. Price sensitivity, labor scarcity, and the use of heavier implements, as well as the adoption of conservation-tillage, drive a robust 11.1% CAGR for four-wheel drive units through 2030. Gujarat leads the adoption of cotton–groundnut rotations, which benefit from deeper traction. Original Equipment Manufacturers (OEMs) narrow the price delta by modularizing differentials and offering field-convertible kits that allow for switching between modes. Farmers note 8–10% fuel savings in wet soils when four-wheel drive optimizes slippage. Utility gains are magnified in hilly orchards, where maneuverability and stability justify premiums.

As crop diversification accelerates, many farmers seek a single tractor that can manage plowing, spraying, and transportation. Four-wheel configurations handle larger sprayer booms and mid-mount mowers that two-wheel units struggle with under heavy load. Leasing firms also prefer four-wheel drive for the longevity of their assets. Still, dealership penetration and maintenance skills lag in eastern India, constraining uptake. The tractor industry in the Indian market, therefore, evolves toward segmented value propositions, two-wheel reliability for staple crops, four-wheel productivity for high-value zones.

By Application: Row-Crop Leadership Amid Orchard Acceleration

Row-crop tractors command 58% of India agricultural tractor market in 2024, mirroring cereal dominance in acreage. Their chassis accommodates mid-width implements, which are essential for cultivating rice, wheat, and maize. Orchard tractors, although smaller in sales, are growing at an 8.4% CAGR through 2030, as horticulture gains policy focus under the Mission for Integrated Development of Horticulture (MIDH) schemes. Narrow track widths and low canopy profiles are suitable for mango and grape orchards in the states of Maharashtra and Karnataka. Original Equipment Manufacturers (OEMs) integrate reversible fans and under-hood insulation to prevent damage to foliage. Specialty sprayer pairings raise per-acre yield while cutting chemical use by nearly 30%[3]Source: IBEF, “Making India a Global Powerhouse in the Farm Machinery Industry,” ibef.org .

Utility tractors serving haulage, rural construction, and municipal duties diversify revenue. They employ PTO (Power Take-Off) -driven concrete mixers or loaders for Pradhan Mantri Gram Sadak Yojana road works. The tractor industry in India increasingly competes with mini-trucks in this utility space. Meanwhile, drone-compatible row-crop units attract tech-savvy growers, while orchard variants embrace electro-hydraulic lift controls for platform harvesters. Application-driven spec sheets nowadays headline marketing brochures more than raw horsepower counts.

Geography Analysis

Uttar Pradesh dominates tractor sales due to its consistent Minimum Support Price (MSP) procurement, which stabilizes cash flows, and state grants subsidize the purchase of implements. The PM-Kisan pipeline ensures liquidity spikes every quarter, aligning with dealer promotions timed for the rabi and kharif seasons. Although plot fragmentation persists, village-level custom hiring centers mitigate utilization constraints.

Punjab and Haryana continue to invest in residue-management kits, following burn-ban regulations, which boosts accessory turnover. Their well-developed workshop networks minimize downtime, thereby reinforcing brand loyalty to incumbent Original Equipment Manufacturers (OEMs). Water scarcity prompts experimentation with conservation tillage that requires higher torque and precision equipment.

Maharashtra’s profile is shaped by sugar-cane cooperatives that operate 24-hour crushing cycles, where tractors haul cane and power PTO (Power Take-Off)-driven choppers. Solar-pump penetration cuts irrigation diesel bills, freeing up funds for mechanization upgrades. Cotton farmers embrace four-wheel drive to navigate black-cotton soils, especially during delayed monsoons. Gujarat’s cooperative credit model, akin to its dairy success, bundles tractor loans with crop procurement contracts, lowering default risk.

Competitive Landscape

Market concentration is high, with manufacturers such as Mahindra & Mahindra Ltd., Escorts Kubota Limited, Tractors and Farm Equipment Limited (TAFE), Deere & Company, and the Sonalika Group capturing a significant share of the market revenue. Mahindra & Mahindra Ltd.'s share stems from a 1,200-plus dealer network, a broad model lineup, and a captive finance arm that approved 228,000 loans in FY25. Tractors and Farm Equipment Limited (TAFE) leverages Massey Ferguson technology and African export volume to amortize R&D across markets. Escorts Kubota Limited blends Japanese hydraulics with local cost engineering to penetrate high-margin orchard niches. Deere & Company focuses on 55 HP and above, bundling telematics and precision packages.

Strategic pivots emphasize digital ecosystems. Firms launch app-based service bookings, subscription maintenance, and parts e-stores. Mahindra & Mahindra Ltd.'s Krish-e platform utilizes sensor data to recommend agronomic practices, thereby creating cross-sell opportunities for implements and inputs. Tractors and Farm Equipment Limited's (TAFE) JFarm Services app aggregates custom hiring demand, accelerating fleet utilization. Emission-compliance deadlines drive alliances with component suppliers, including CNH Industrial N.V. partners with Bosch Limited for after-treatment, while Escorts Limited taps Kubota Corporation for stage-V-ready combustion systems. Electric tractor prototypes surface, but commercialization timelines depend on battery localization.

Traditional incumbents hedge by investing in ventures or launching in-house incubators. Used-tractor portals disrupt dealers’ residual pricing. As technology, regulation, and credit dynamics evolve, competitive advantage will hinge less on metal and more on data, finance, and service depth within the tractor industry in India.

India Agricultural Tractor Industry Leaders

Mahindra & Mahindra Ltd.

Tractors and Farm Equipment Limited (TAFE)

Escorts Kubota Limited.

Sonalika Group (International Tractors Limited (ITL)

Deere & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mahindra & Mahindra Ltd.'s Farm Equipment Sector announced record-high annual domestic tractor sales of 407,094 units for fiscal year 2025, a 12% increase over the previous year. In March 2025, the company sold 32,582 tractors in the domestic market, totaling 34,934 units, including exports, marking a 34% year-over-year growth for the month.

- September 2024: The Union Cabinet of India cleared the Digital Agriculture Mission, which has a budget of USD 339 million. The mission aims to transform India's agriculture sector through the creation of a robust Digital Public Infrastructure (DPI).

- May 2024: Mahindra announced a USD 4.5 billion investment plan for FY25–27, including USD 602 million for farm equipment. The investment is strategically distributed across its various sectors to fund new product development, capacity expansion, and technological advancements.

India Agricultural Tractor Market Report Scope

The India Agricultural Tractor Market Report is Segmented by Engine Power (Less Than 30 HP, 31-50 HP, and More), by Drive Type (Two-Wheel Drive and Four-Wheel Drive), and by Application (Row Crop Tractors, Orchard Tractors, and Other Applications). The Market Forecasts are Provided in Terms of Value (USD).

| Less than 30 HP |

| 31-50 HP |

| 51-80 HP |

| Above 80 HP |

| Two-wheel Drive |

| Four-wheel Drive |

| Row-Crop Tractors |

| Orchard Tractors |

| Other Applications |

| By Engine Power | Less than 30 HP |

| 31-50 HP | |

| 51-80 HP | |

| Above 80 HP | |

| By Drive Type | Two-wheel Drive |

| Four-wheel Drive | |

| By Application | Row-Crop Tractors |

| Orchard Tractors | |

| Other Applications |

Key Questions Answered in the Report

What is the current value of the agricultural tractor industry in India?

The agricultural tractor industry in India is valued at USD 7.92 billion in 2025.

Which engine power band dominates tractor sales across Indian farms?

Models in the 31–50 HP range hold 46% market share in 2024.

Why are four-wheel drive tractors gaining popularity?

States with intensive cotton, sugarcane, and horticulture report an 11.1% CAGR for four-wheel drive units owing to better traction, heavier implement handling, and narrowing price gaps.

Which drive type dominates tractor sales across Indian farms?

By drive type, two-wheel drive units held a maximum market share of 87.0% of the tractor industry in India in 2024.

Page last updated on: