Immersion Cooling Fluids Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

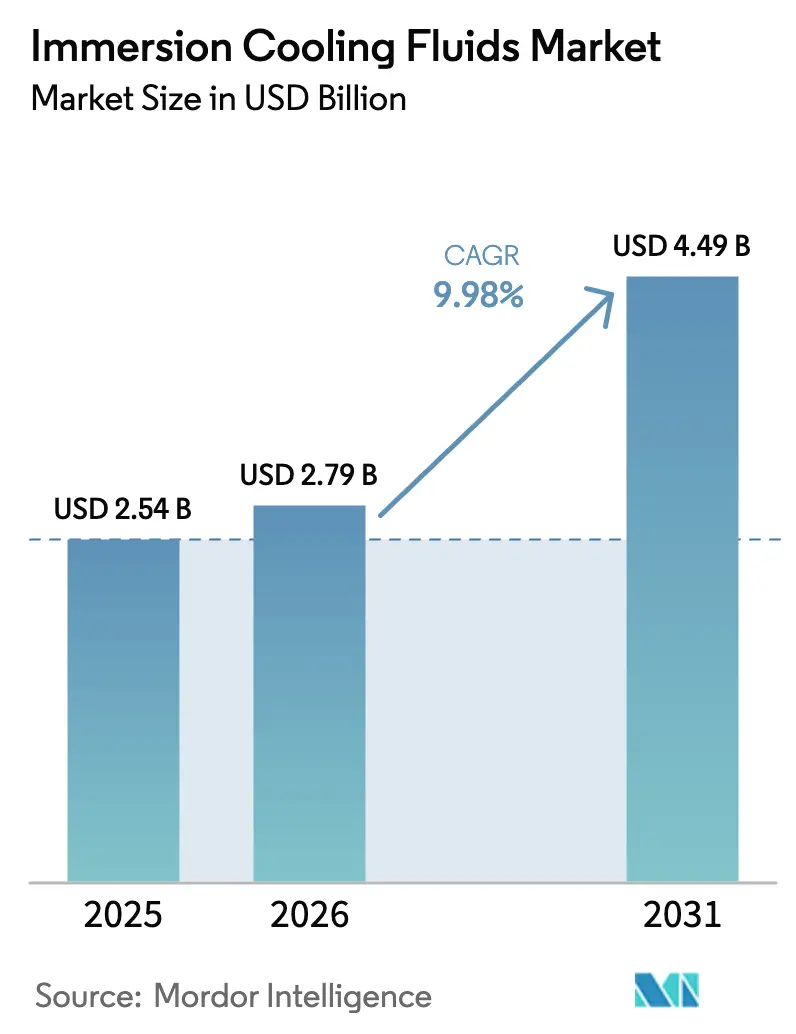

| Market Size (2026) | USD 2.79 Billion |

| Market Size (2031) | USD 4.49 Billion |

| Growth Rate (2026 - 2031) | 9.98% CAGR |

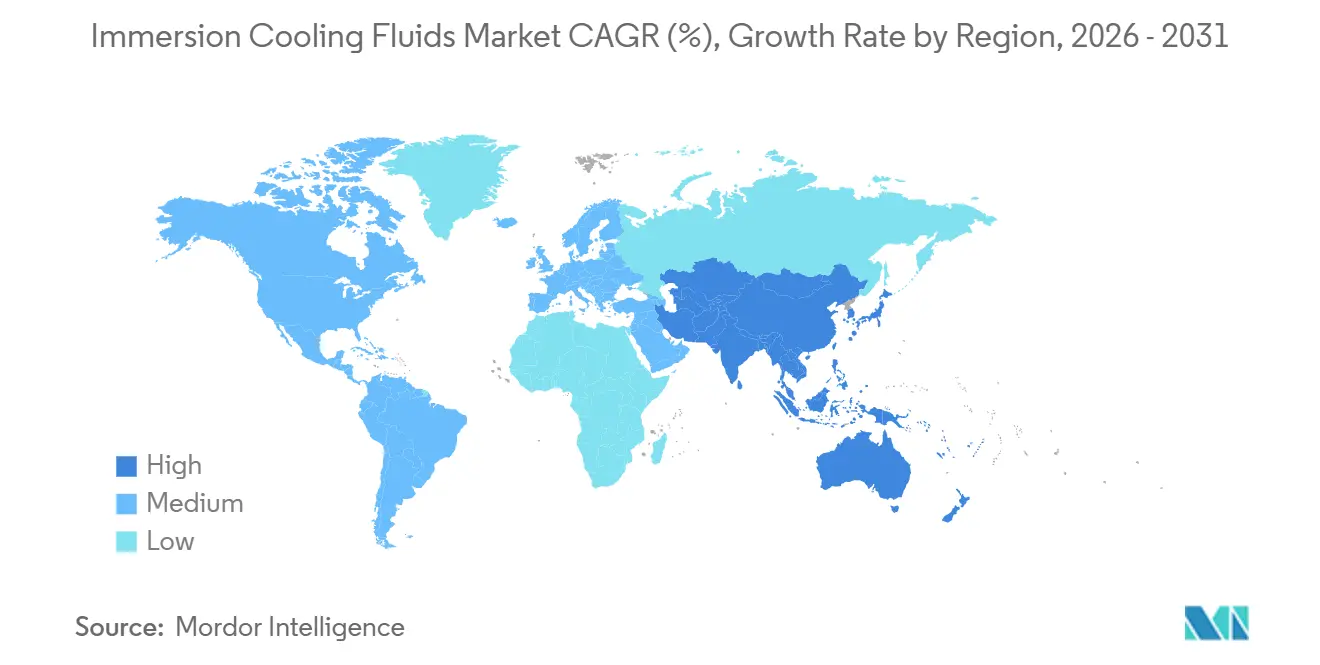

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

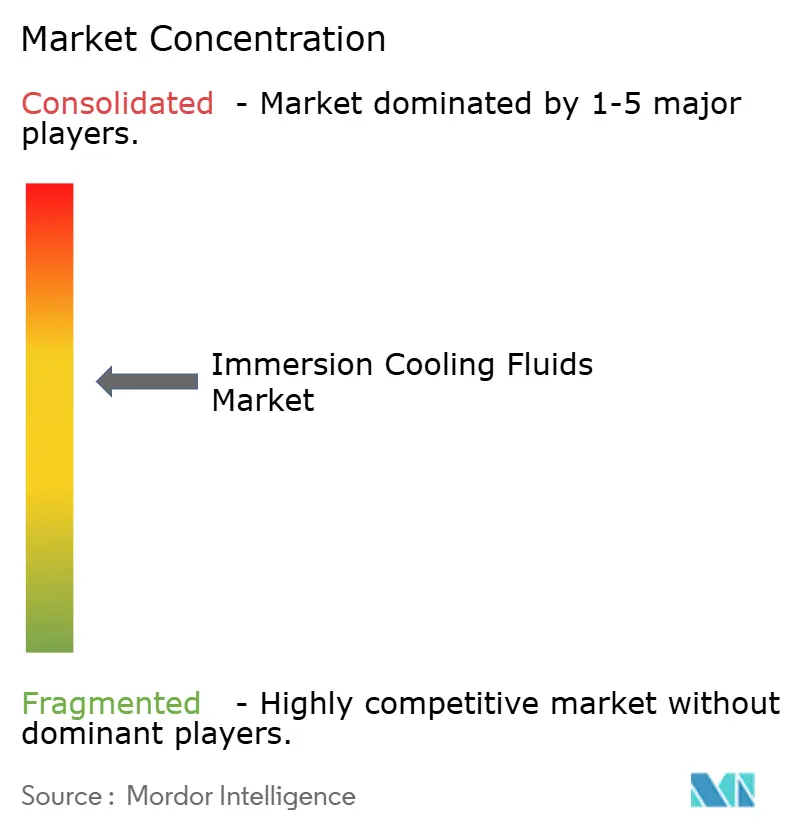

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Immersion Cooling Fluids Market Analysis by Mordor Intelligence

The Immersion Cooling Fluids Market size is projected to expand from USD 2.54 billion in 2025 and USD 2.79 billion in 2026 to USD 4.49 billion by 2031, registering a CAGR of 9.98% between 2026 and 2031. Growing rack densities that exceed 30 kilowatts, hyperscale operators’ shift toward AI clusters above 400 MW per campus, and district-heating programs that monetize waste heat are redefining data-center economics. Regulatory deadlines phasing out PFAS compounds in North America and Europe are steering buyers toward PFAS-free synthetics and esters, while Intel’s 2025 certification of Shell and ExxonMobil fluids removed a key hurdle for hyperscale adoption. As a result, single-phase systems priced at USD 2-5 per liter for mineral oils dominate installed capacity, yet fluorinated alternatives, now PFAS-free, are the fastest-growing chemistry. Competitive intensity remains high because no vendor holds more than 12% share, but suppliers that combine refining scale with chip-maker endorsements are consolidating influence.

Key Report Takeaways

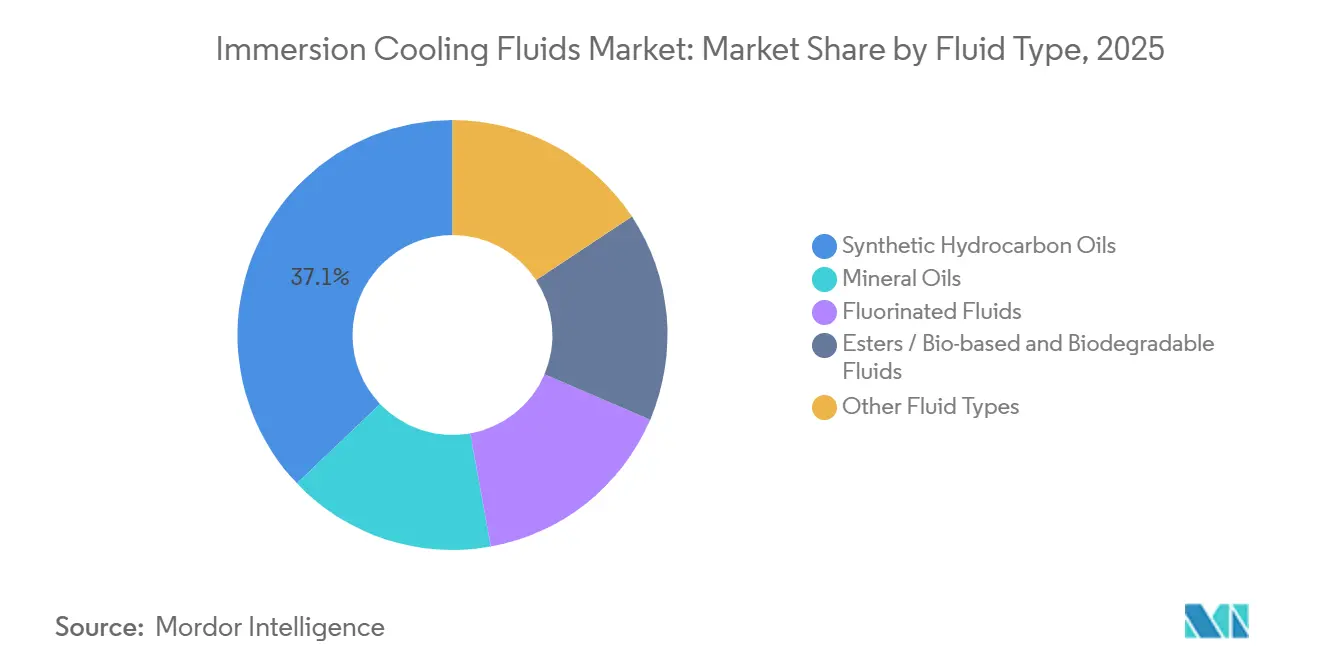

- By fluid type, synthetic hydrocarbons captured 37.12% of the Immersion Cooling Fluids market share in 2025, while fluorinated fluids are growing at a 10.22% CAGR during the forecast period (2026-2031).

- By cooling type, single-phase systems held 64.44% of the Immersion Cooling Fluids market size in 2025 and are advancing at a 10.36% CAGR during the forecast period (2026-2031).

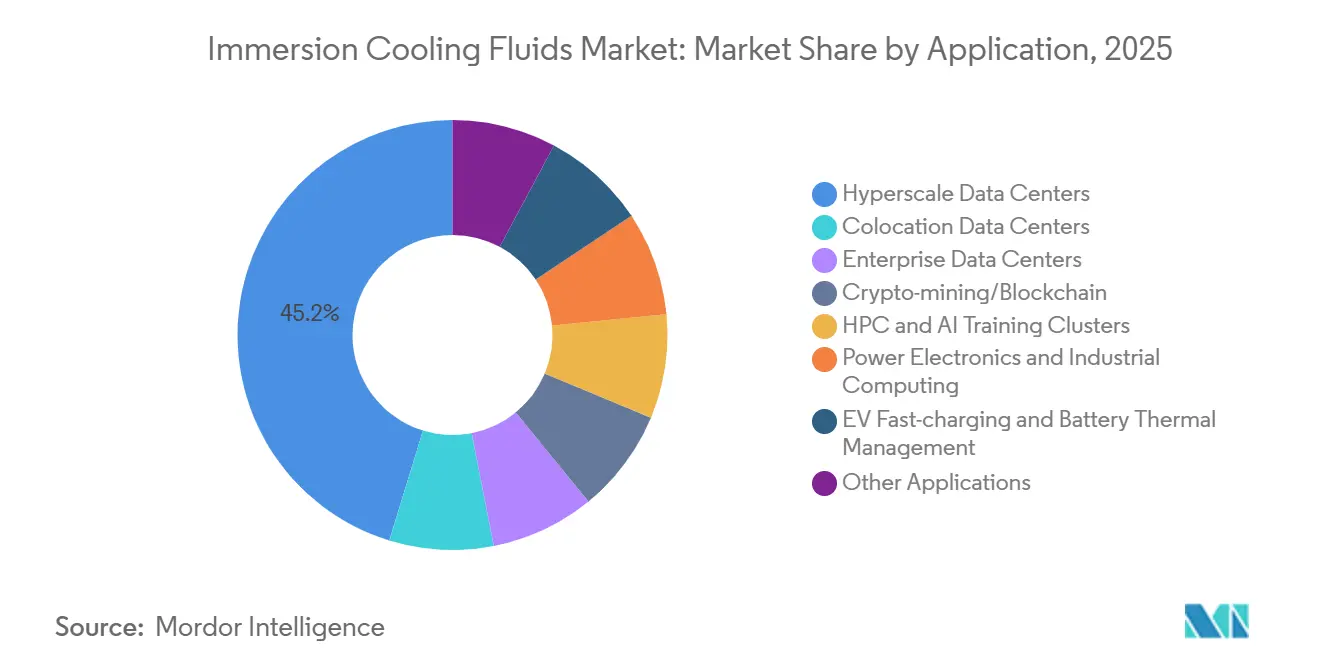

- By application, hyperscale data centers led with 45.23% revenue share in 2025; HPC and AI clusters are projected to expand at an 11.12% CAGR during the forecast period (2026-2031).

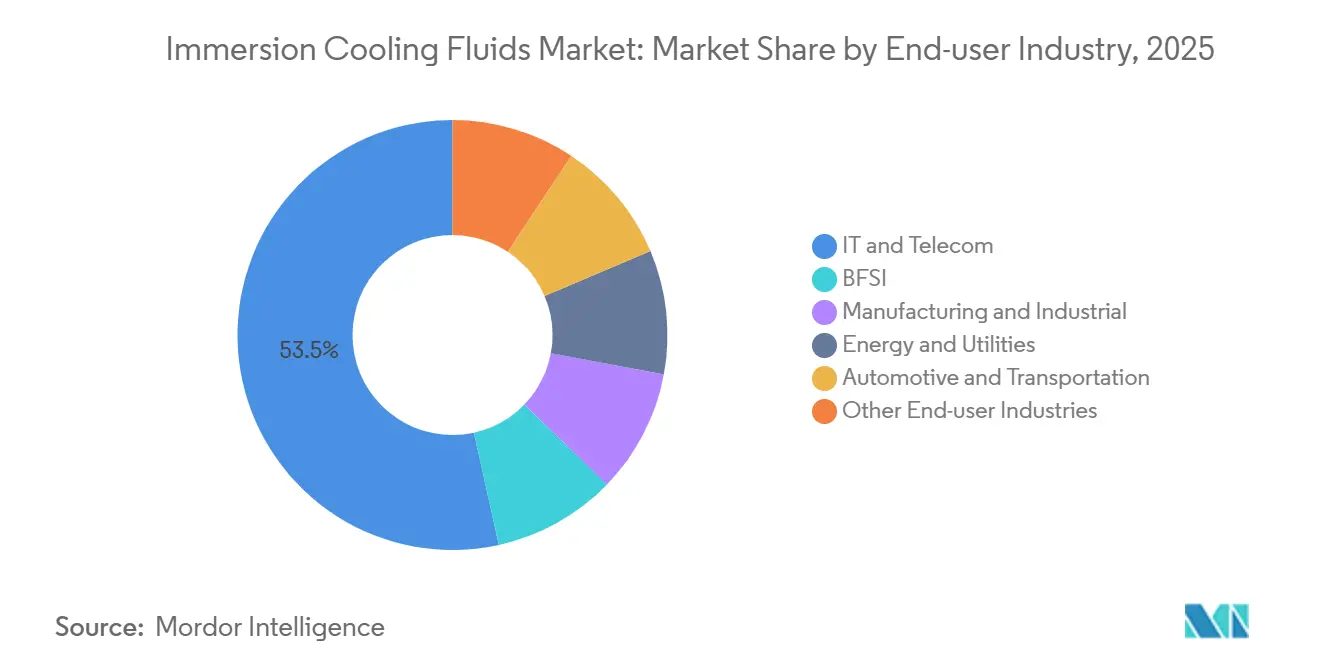

- By end-user industry, IT and telecom accounted for 53.45% share of the Immersion Cooling Fluids market size in 2025, while automotive and transportation are growing at a 10.68% CAGR during the forecast period (2026-2031).

- By geography, North America commanded 41.18% of the Immersion Cooling Fluids market share in 2025; Asia-Pacific is set to register a 10.45% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Immersion Cooling Fluids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising energy-efficiency and PUE optimization pressures | +2.8% | Global, early adoption in North America, Europe, Singapore | Medium term (2-4 years) |

| Sustainability and carbon-neutral targets accelerate adoption | +2.1% | Europe, North America, APAC | Long term (≥ 4 years) |

| Stricter PFAS-phase-out deadlines reshape fluid chemistries | +1.6% | North America, EU, spill-over to APAC | Short term (≤ 2 years) |

| Growing edge–micro-data-centers in emerging markets | +1.4% | APAC, Middle East, Latin America | Medium term (2-4 years) |

| Heat-reuse initiatives driving district-heating integration | +1.2% | Europe, pilots in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Energy-Efficiency and PUE Optimization Pressures

Operators pushing PUE below 1.15 face steep air-cooling penalties once rack densities top 30 kW. Single-phase immersion reduces fan and chiller loads, delivering a PUE of 1.05-1.15, while two-phase achieves 1.02-1.08. Microsoft’s fleetwide rollout of direct liquid cooling in July 2025 and Colovore’s USD 925 million financing for 200 kW-per-rack capacity mark a shift from pilot to baseline engineering. Dell’Oro Group recorded 85% year-over-year liquid-cooling growth in 2025, although immersion still trails direct-to-chip retrofits. The European Data Centre Association measured only 5.6% immersion adoption in 2024, underscoring a five-to-ten-year conversion window. Intel-Shell tests confirmed up to 48% energy savings, 30% CO₂ reduction, and 99% lower water use, aligning with corporate science-based targets.

Sustainability and Carbon-Neutral Targets Accelerate Adoption

District-heating programs price delivered heat at EUR 12–22 per MWh, undercutting gas boilers by roughly 50%. AWS Tallaght supplied 92% of Trinity College Dublin’s heating and cut 704 tons of CO₂ in 2024, proving revenue-positive heat export. Microsoft–Fortum’s Finland scheme will reach 250,000 residents by 2026. Singapore’s moratorium lift now mandates PUE less than 1.3 and renewable sourcing, stimulating liquid cooling at STT GDC. Meta’s USD 65 billion AI build and Google’s USD 40 billion Texas plan both specify liquid cooling, giving colocation operators pricing power premiums of 20-40% per kilowatt.

Stricter PFAS-Phase-Out Deadlines Reshape Fluid Chemistries

3M ended Novec supply on 31 December 2025, eliminating 30-40% of fluorinated capacity. EU Regulation 2025/718 and the U.S. AIM Act push suppliers toward PFAS-free blends. Intel cleared Shell’s S3 X/S5 X and ExxonMobil’s single-phase hydrocarbons in 2025, reducing buyer risk. Hydrocarbons deliver 0.13-0.16 W/m/K thermal conductivity and -40°C to 200°C operating windows, though they lack fluorinated non-flammability. Natural esters such as Cargill FR3 boast over 300°C flash points but run 5-8°C hotter, forcing operators to balance safety and thermal margins.

Growing Edge-Micro-Data-Centers in Untapped Emerging Markets

India’s Vertiv-Netweb racks above 200 kW and Singapore’s growth from 1.4 GW in 2024 to 2 GW by 2029 typify APAC’s capacity wave. UAE expansion to 750 MW by 2029 and Mexico’s 10.2% CAGR show similar patterns. Edge nodes for 5G and industrial IoT need compact, low-overhead cooling; single-phase immersion cuts infrastructure overhead to 2-5%. Yet fluid cost differentials, USD 50-200 per liter for engineered fluids vs USD 2-5 for mineral oils, and fragmented OEM protocols slow scale-out.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Material compatibility and safety concerns amid PFAS regulation | -1.3% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Limited standards / inter-operability across OEM ecosystems | -0.9% | Global, fragmentation in APAC and emerging markets | Medium term (2-4 years) |

| Volatility in synthetic base-oil supply chain post-3M exit | -0.7% | North America, Europe, spill-over to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Material Compatibility and Safety Concerns Amid PFAS Regulation

Hydrocarbon coolants can attack certain elastomers, forcing component-by-component validation[1]Lubrizol, “Compatibility of Hydrocarbon Dielectrics,” lubrizol.com. Cargill FR3 is biodegradable but creates hotter spots, potentially shortening lifecycle in tight-margin designs. Two-phase tanks demand hermetic sealing; micro-leaks slash performance and raise fire risk when fluids are flammable. Absent long-term field data, Shell and ExxonMobil only cleared Intel tests in 2025; risk-averse BFSI users defer conversion. Divergent EU and U.S. rules oblige region-specific blends, inflating SKUs and cost.

Limited Standards / Inter-Operability Across OEM Ecosystems

Intel’s certification covers only Xeon chips; AMD, NVIDIA, and ARM lack equivalent seals, fragmenting approval matrices. Tank designs from Hypertec, Penguin, and Wiwynn are proprietary, so switching vendors entails rack re-engineering. No IEC or IEEE interoperability code yet exists, stretching commissioning to up to 15 months against 3-6 months for air. Emerging-market edge deployments suffer most due to skill gaps and hazmat logistics that add 20-30% cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fluid Type: Synthetic Hydrocarbons Lead, Fluorinated Fluids Accelerate

Synthetic hydrocarbons captured 37.12% of the Immersion Cooling Fluids market share in 2025, buoyed by Intel’s endorsement of Shell and ExxonMobil formulas. Fluorinated fluids, relaunched as PFAS-free hydrofluoroethers by Chemours, Solvay, and DOW, are forecast for a 10.22% CAGR during the forecast period (2026-2031). Mineral oils keep crypto miners loyal thanks to USD 2-5 per-liter pricing and 6-12 month paybacks, while natural-ester blends meet IEC 62770 yet run hotter, curbing HPC uptake. Engineered suppliers such as Dynalene and Engineered Fluids fill customization gaps at premium margins.

By Cooling Type: Single-Phase Dominates, Two-Phase Advances in Ultra-Dense HPC

Single-phase accounted for 64.44% of the Immersion Cooling Fluids market size in 2025 and should grow at a 10.36% CAGR, reflecting their lower capital cost (no hermetic sealing required), simpler fluid management (no evaporation control), and compatibility with district-heating networks that accept 50-60°C inlet temperatures. Two-phase remains essential for racks above 100 kW, demonstrated by Accelsius pipelines and DarkNX’s 300 MW Ontario campus hitting PUE 1.02-1.08. However, hermetic design complexity and refrigerant management keep the two-phase adoption niche today.

By Application: Hyperscale Data Centers Rule, AI Training Clusters Surge

Hyperscale Data Centers delivered 45.23% of 2025 revenue, underpinned by Microsoft Fairwater and Oracle’s 131,000-GPU pod. HPC and AI clusters are expected to post the highest 11.12% CAGR during the forecast period (2026-2031) as tensor processors pass 700 W TDP limits. Colocation space achieves 20-40% price premiums and 94% occupancy for immersion bays, while enterprise sites prefer direct-liquid retrofits.

By End-User Industry: IT & Telecom Dominant, Automotive Fastest

The IT and telecom sector captured 53.45% market share in 2025, driven by hyperscale operators (Microsoft, Google, Meta) and colocation providers (Equinix, Digital Realty) deploying liquid cooling for AI workloads that exceed 400 watts per GPU. Automotive and transportation, driven by fast-charging and battery-storage pilots from Shell-QAES, will expand fastest at 10.68% CAGR. Banking, financial services, and insurance (BFSI), manufacturing, and energy follow with use cases in data localization, semiconductor fab, and grid storage, respectively. Energy and utilities leverage immersion for grid-scale battery-energy-storage systems; Shell-QAES's October 2025 pilot targeted cycle-life extension and thermal-runaway mitigation, addressing fire-safety concerns that constrain lithium-ion deployments near population centers[2]Shell, “S3 X & S5 X Certification with Intel,” shell.com.

Geography Analysis

North America led with 41.18% of 2025 revenue owing to Meta’s USD 65 billion AI build and Google’s USD 40 billion Texas project. Asia-Pacific shows a 10.45% forecast CAGR, catalyzed by Singapore’s green-data-center rules, Japan’s 9.6% market CAGR, and India’s 200 kW-rack deployments. Europe monetizes waste heat, AWS Tallaght cut 704 tons of CO₂ in 2024, and Microsoft-Fortum will heat 250,000 Finns by 2026, creating 15-25% better ROI for operators. Latin America and the Middle East record double-digit growth but struggle with hazmat regulations and skills shortages, slowing immersion ramp.

Competitive Landscape

The Immersion Cooling Fluids market is moderately concentrated. Start-ups such as LiquidStack, ZutaCore, and Submer secure VC funding and OEM alliances to ship turnkey pods. Modine’s 2024 purchase of Green Revolution Cooling signals traditional HVAC players moving downstream. Engine manufacturers’ certifications (Intel in 2025) act as gatekeepers, channeling demand to approved chemistries.

Immersion Cooling Fluids Industry Leaders

3M

Engineered Fluids

ExxonMobil Corporation

Shell plc

The Chemours Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: ExxonMobil received the Intel Data Centre Certified designation for its hydrocarbon-based single-phase immersion fluids, with validation partners including Baltimore Aircoil Company (BAC COBALT system), Hypertec (servers), and Micron (memory modules)

- May 2025: Shell Lubricants’ immersion cooling fluids became the first to receive official certification from Intel, a major chip manufacturer, allowing its products to be used with confidence in data centres worldwide.

Global Immersion Cooling Fluids Market Report Scope

Immersion cooling fluids are specialized, electrically insulating (dielectric) liquids used to submerge IT hardware, such as servers or miners, for highly efficient heat removal. These thermally conductive fluids, which can be single-phase (liquid) or two-phase (liquid-to-vapor), directly absorb heat to enable higher hardware density and reduce energy usage compared to air cooling.

The Immersion Cooling Fluids market is segmented by fluid type, cooling type, application, end-user industry, and geography. By fluid type, the market is segmented into synthetic hydrocarbon oils, mineral oils, fluorinated fluids, esters/bio-based and biodegradable fluids, and other fluid types. By cooling type, the market is segmented into single-phase immersion cooling and two-phase immersion cooling. By application, the market is segmented into data centers – hyperscale, data centers – colocation, data centers – enterprise, crypto-mining/blockchain, HPC and AI training clusters, power electronics and industrial computing, EV fast-charging and battery thermal management, and other applications. By end-user industry, the market is segmented into IT and telecom, BFSI, manufacturing and industrial, energy and utilities, automotive and transportation, and other end-user industries. The report also covers the market size and forecasts for immersion cooling fluids in 17 countries across major regions in value (USD).

| Synthetic Hydrocarbon Oils |

| Mineral Oils |

| Fluorinated Fluids |

| Esters / Bio-based and Biodegradable Fluids |

| Other Fluid Types |

| Single-phase Immersion Cooling |

| Two-phase Immersion Cooling |

| Data Centers – Hyperscale |

| Data Centers – Colocation |

| Data Centers – Enterprise |

| Crypto-mining/Blockchain |

| HPC and AI Training Clusters |

| Power Electronics and Industrial Computing |

| EV Fast-charging and Battery Thermal Management |

| Other Applications |

| IT and Telecom |

| BFSI |

| Manufacturing and Industrial |

| Energy and Utilities |

| Automotive and Transportation |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Netherlands | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Fluid Type | Synthetic Hydrocarbon Oils | |

| Mineral Oils | ||

| Fluorinated Fluids | ||

| Esters / Bio-based and Biodegradable Fluids | ||

| Other Fluid Types | ||

| By Cooling Type | Single-phase Immersion Cooling | |

| Two-phase Immersion Cooling | ||

| By Application | Data Centers – Hyperscale | |

| Data Centers – Colocation | ||

| Data Centers – Enterprise | ||

| Crypto-mining/Blockchain | ||

| HPC and AI Training Clusters | ||

| Power Electronics and Industrial Computing | ||

| EV Fast-charging and Battery Thermal Management | ||

| Other Applications | ||

| By End-user Industry | IT and Telecom | |

| BFSI | ||

| Manufacturing and Industrial | ||

| Energy and Utilities | ||

| Automotive and Transportation | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecast size of the Immersion Cooling Fluids market by 2031?

The Immersion Cooling Fluids market size is projected to reach USD 4.49 billion by 2031 from USD 2.79 billion in 2026.

Which fluid type holds the largest revenue share today?

Synthetic hydrocarbons led with 37.12% market share in 2025 after Intel certified Shell and ExxonMobil formulations.

Why are hyperscale operators moving to immersion cooling?

AI clusters above 400 MW demand rack densities that push air systems past economic limits, and immersion cuts energy use up to 48% while enabling PUE below 1.10.

How will PFAS regulation affect product choices?

With 3M exiting Novec and EU/US rules tightening, buyers are shifting to PFAS-free hydrofluoroethers, synthetic hydrocarbons, and bio-ester alternatives.

Page last updated on: