Cold Flow Improver Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.95 Billion |

| Market Size (2031) | USD 1.23 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

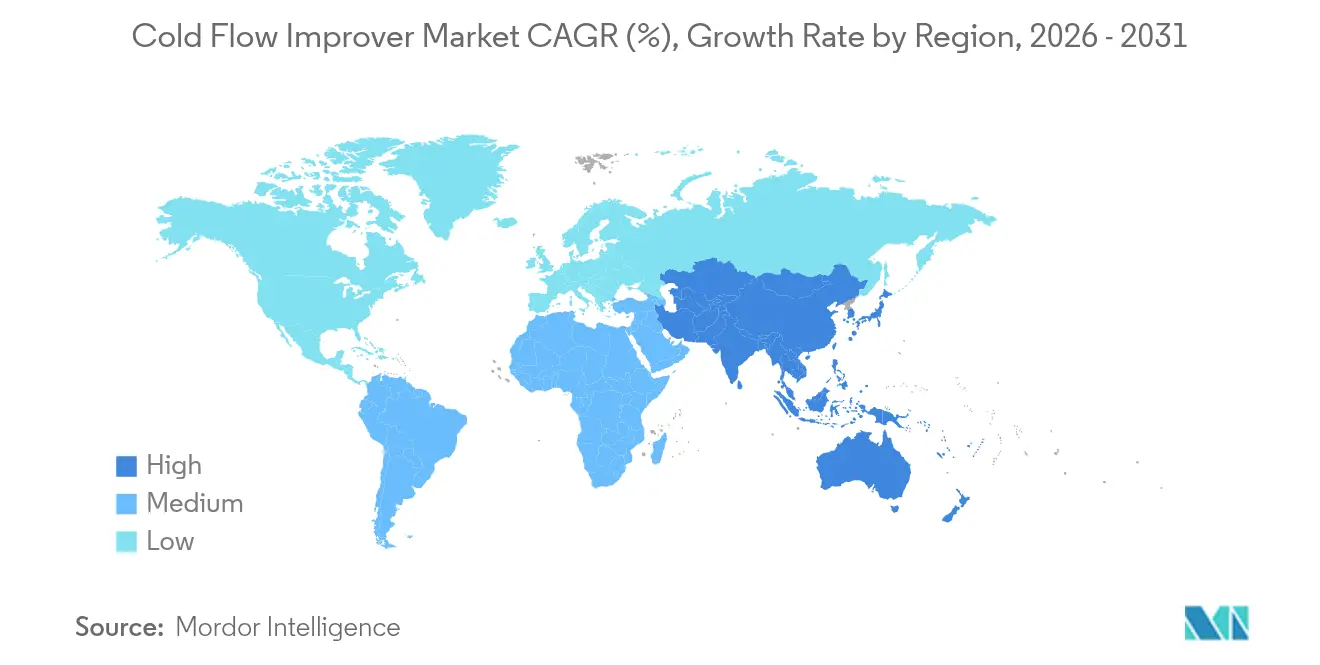

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cold Flow Improver Market Analysis by Mordor Intelligence

Cold Flow Improver market size in 2026 is estimated at USD 0.95 billion, growing from 2025 value of USD 0.9 billion with 2031 projections showing USD 1.23 billion, growing at 5.36% CAGR over 2026-2031. Growing reliance on winter-grade ultra-low-sulfur diesel, rapid biofuel adoption, and stricter standards such as European Norm (EN) 590 and American Society for Testing and Materials (ASTM) D975 are pushing additive demand upward. Rising Arctic and sub-Arctic logistics, together with remote data-center backup power needs, add further momentum. Suppliers are scaling capacity in Asia-Pacific, where local regulations and cold-climate industrial activity are most intense. At the same time, electric vehicle proliferation and solid-state battery research represent long-range headwinds that could gradually temper volume growth.

Key Report Takeaways

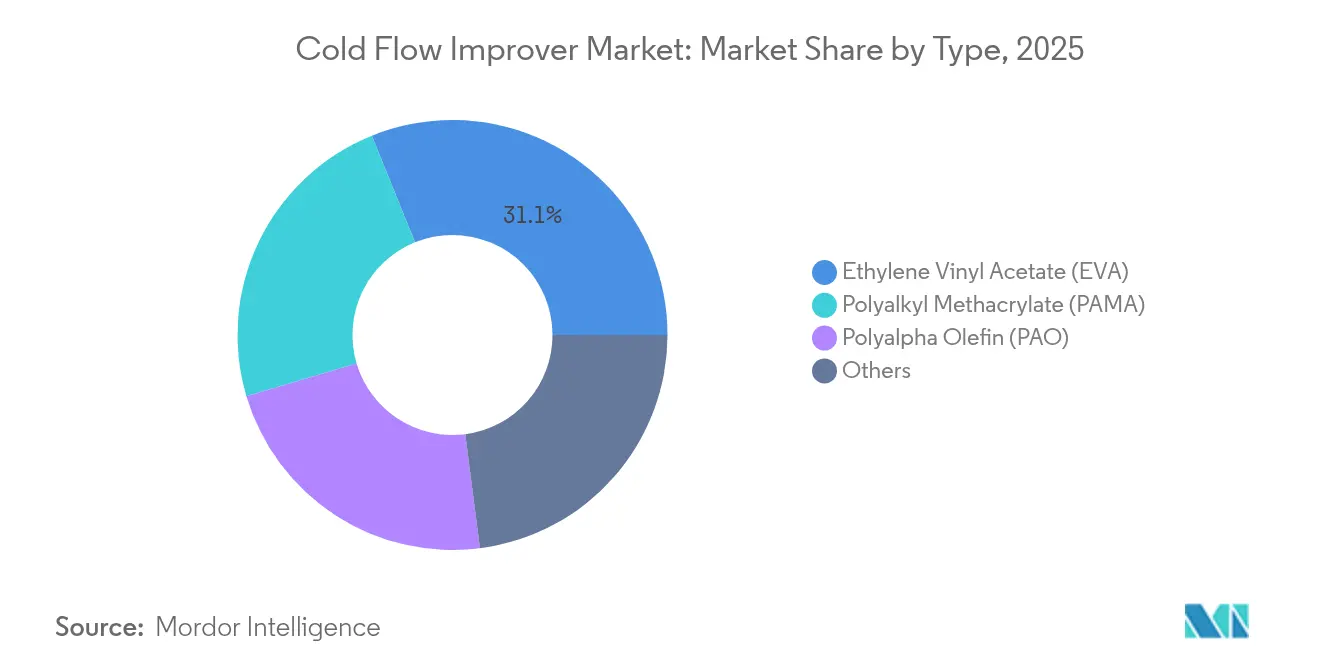

- By type, ethylene vinyl acetate led with 31.12% of the Cold Flow Improver market share in 2025; polyalkyl methacrylate is projected to post the fastest 5.63% CAGR to 2031.

- By end-user industry, the automotive segment accounted for 63.62% of revenue in 2025, while aerospace and defense is set to grow at a 5.45% CAGR through 2031.

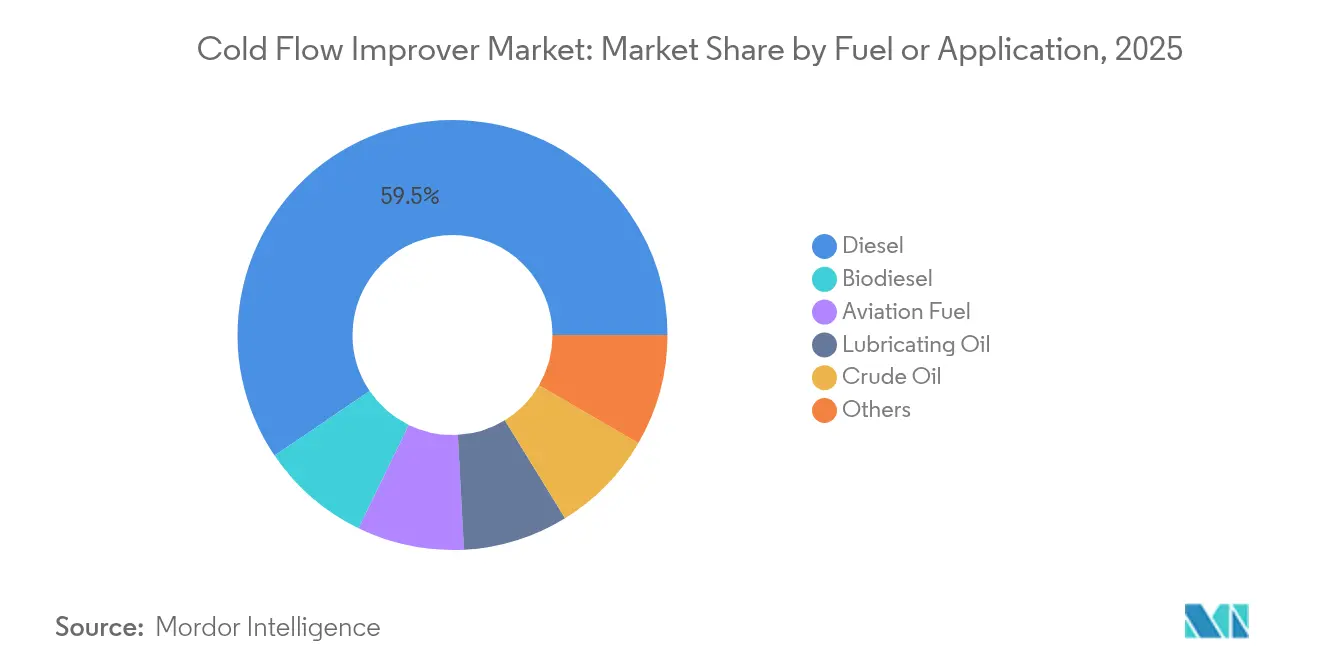

- By fuel/application, diesel commanded 59.48% of the Cold Flow Improver market size in 2025, but biodiesel is advancing at an 8.04% CAGR over the forecast horizon.

- By geography, Asia-Pacific captured 35.33% of 2025 revenue and is forecast to expand at a region-leading 6.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cold Flow Improver Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Ultra-low-sulfur Diesel & Winter-grade Fuels | 1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid Adoption of Biofuels Requiring Advanced Carbon Farming Initiatives (CFIs) | 0.8% | APAC core, spill-over to North America & EU | Long term (≥ 4 years) |

| Stricter Global Cold-flow Fuel Standards (EN 590, ASTM D975) | 0.6% | Global, led by EU & North America | Short term (≤ 2 years) |

| Rising Investment in Arctic & Sub-arctic Oil Logistics | 0.4% | North America (Alaska, Canada), Russia, Nordic regions | Long term (≥ 4 years) |

| Growth of Remote Data-center Backup Gensets in Cold Regions | 0.3% | North America, Nordic regions, Russia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Ultra-low-sulfur Diesel & Winter-grade Fuels

Ultra-low-sulfur diesel at 15 parts per million (ppm) in the United States and 10 mg/kg in China removes sulfur-based natural lubricants, worsening wax crystallization at low temperatures. Winter-grade diesel therefore relies on polymeric pour-point depressants to hold cloud points below regional specifications. Field research in rural Alaska shows annual household fuel costs rising by USD 209 following the Ultra-Low Sulfur Diesel (ULSD) shift, underlining the economic value of effective cold flow improver adoption [1]Alaska Department of Environmental Conservation, “ULSD Transition Cost Study,” dec.alaska.gov. The Arctic Council’s 2024 low-sulfur fuel initiative further signals that future logistics contracts will specify additive-enhanced fuel blends.

Rapid Adoption of Biofuels Requiring Advanced Carbon Farming Initiatives (CFIs)

Higher cloud points from saturated fatty acids in biodiesel force refiners to tailor cold flow improver chemistry. Laboratory work demonstrates that polymethyl acrylate can drop biodiesel pour points by 8°C and cold-filter-plugging points by 6°C, though results vary by feedstock. China’s 230,000 t/y sustainable aviation fuel venture by TotalEnergies and SINOPEC exemplifies the growing scale at which additive-ready biofuels will circulate. The California Low Carbon Fuel Standard’s 2024 amendments oblige fuel suppliers to preserve winter performance while lifting bio-blend ratios, intensifying the need for specialty Carbon Farming Initiatives (CFIs).

Stricter Global Cold-flow Fuel Standards (EN 590, ASTM D975)

Europe’s 2024 revision of EN 590 raises allowable Fatty Acid Methyl Ester (FAME) from 7% to 10%, complicating cold-weather operability and locking in demand for next-generation additives. Canada’s CAN/CGSB-3.517 upgrade follows a similar path, while ASTM D6371-24 provides a unified test for cold-filter-plugging point that dictates additive formulation targets. Harmonized protocols enable multinational suppliers to commercialize common polymer platforms for multiple jurisdictions.

Rising Investment in Arctic & Sub-arctic Oil Logistics

Longer navigation windows and new pipelines in Canada, Russia, and Alaska accelerate demand for reliable pour-point depressants. Field trials on paraffinic crude confirmed that targeted Ethylene-vinyl acetate (EVA)-based packages kept pipelines restartable after three-week shutdowns at (–30)°C. The U.S. Antarctic Program specifies (–58)°C freeze points for Aviation Navy (AN)8 jet fuel, a threshold reachable only with premium cold flow improvers. Such specifications validate the commercial upside of high-performance additives in remote energy projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Popularity of Electric & Fuel-cell Vehicles | -0.7% | Global, led by China, EU, and North America | Long term (≥ 4 years) |

| Volatility in Crude Oil & Additive Raw-material Prices | -0.5% | Global | Short term (≤ 2 years) |

| Emerging Solid-state Battery Backup Systems for Telecom & Data Centers | -0.3% | North America, EU, APAC developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Popularity of Electric & Fuel-cell Vehicles

Electric vehicle adoption represents the most significant long-term threat to cold flow improver demand. The International Energy Agency projects passenger electric vehicle (EV) registrations nearing 30 million units by 2027, eroding diesel demand in urban fleets [2]International Energy Agency, “Global EV Outlook 2025,” iea.org. Heavy-duty sectors lag but remain on an electrification path that could reach 18% of global truck sales by 2030. While cold climates delay adoption, every percent shift away from internal combustion vehicles trims the long-run volume base for the cold flow improver market.

Volatility in Crude Oil and Additive Raw-material Prices

Raw material price volatility creates significant margin pressure for cold flow improver manufacturers, with petroleum-derived base chemicals subject to crude oil price fluctuations that can rapidly alter product economics. The International Energy Agency's World Energy Outlook 2024 highlights continued geopolitical risks affecting energy security, with conflicts in the Middle East and Ukraine creating sustained price volatility. BASF modeled 2025 budgets at USD 75 per-barrel but flagged wide uncertainty. Specialty chemical makers face margin squeeze because cold flow improvers form a tiny cost share of finished fuel yet must pass stringent validation for any formulation change. Price swings in monomers and specialty solvents can therefore stall expansion projects and compress profitability until costs normalize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ethylene Vinyl Acetate (EVA) dominance, Polyalkyl Methacrylate (PAMA) Innovation

Ethylene Vinyl Acetate (EVA) retained 31.12% of the Cold Flow Improver market share in 2025, owing to proven compatibility with both petroleum diesel and biodiesel blends. However, Polyalkyl Methacrylate (PAMA) is accelerating at a 5.63% CAGR as research confirms up to 8°C reductions in biodiesel pour points, an advantage that lifts its penetration in renewable fuel markets. Polyalpha olefin and emerging nanocomposite additives occupy niche roles where pour-point targets drop below (–40)°C, including aviation and Arctic crude streams. Rising blend ratios of biodiesel and sustainable aviation fuel ensure ongoing substitution potential that could erode EVA’s lead beyond 2030.

PAMA suppliers are developing modular polymer chains to fine-tune crystallization inhibition across mixed-feedstock Fatty Acid Methyl Ester (FAME), while EVA producers focus on copolymer architecture to regain low-temperature efficiency. Competitive differentiation now hinges on performance in multi-fuel systems, filterability retention after long storage, and additive-additive synergy with lubricity improvers.

By End-user Industry: Automotive Leads Amid Aerospace Growth

Automotive applications accounted for 63.62% of revenue in 2025, a dominance sustained by the size of the global diesel vehicle parc and the ubiquity of winter fuel blending mandates. Bus and truck fleets in Canada and Northern Europe mandate cloud points below (–20)°C, locking in baseline additive volumes each winter season. Meanwhile, aerospace and defense, although much smaller in absolute terms, is forecast to expand at 5.45% CAGR as military deployments and commercial polar routes grow. Federal Aviation Administration (FAA) rules require 0.07%–0.15% diethylene glycol monomethyl ether as FSII in jet fuel, and additive packages increasingly incorporate proprietary cold flow polymers to widen freeze-point safety margins.

Industrial, marine, and power-generation users round out demand, often leveraging learnings from automotive formulations. Cross-segment technology transfer quickens product cycles and keeps mid-size chemical firms competitive against integrated majors.

By Fuel/Application: Diesel Dominance Challenged by Biodiesel Growth

Diesel retained 59.48% of the Cold Flow Improver market size in 2025, anchored by commercial transport and remote power gensets. Researchers found that combining methacrylate-acrylamide copolymers with EVA cut diesel cold-filter-plugging points by 23°C, a margin critical for Arctic pipelines. Yet biodiesel is pacing ahead at an 8.04% CAGR as mandates rise worldwide. Europe’s EN 590 now permits 10% FAME, and these blends rely heavily on PAMA-based chemistries for field operability. Aviation fuel, lubricating oil, and crude oil present specialized but lucrative opportunities where pour-point or freeze-point gains translate directly to safety and cost savings.

Geography Analysis

The Cold Flow Improver market in Asia-Pacific commands the largest share at 35.33% in 2025, driven by cold-season diesel demand in Northern China and industrial expansion across India, South Korea, and Japan. Regional standards cut sulfur and extend bio-blend ceilings, prompting refiners to specify higher treat rates. Investments by BASF and Lubrizol support local formulation and faster lead times for fuel marketers.

North America remains the archetype of winter operability challenges, from Canadian prairie provinces to Alaskan North Slope fields where temperatures fall below (–40)°C. Revised Canadian biodiesel guidelines add complexity, while the United States’ Arctic science stations specify jet fuel freeze-points near (–60)°C. These extremes underpin a stable premium segment for high-load pour-point depressants.

Europe’s adoption of 10% FAME diesel and policy focus on renewable fuels sustains additive growth even as total diesel consumption plateaus. NORDIC countries push the technological envelope, demanding pour-point solutions that keep military and civil fleets mobile. Southern Europe’s milder climate offers limited seasonal uplift, but supply chains still standardize winter-grade diesel across the continent, ensuring baseline additive volumes.

Regulatory Landscape

Cold flow improver demand is closely tied to diesel and blendstock specifications that embed low-temperature operability requirements. In Europe, EN 590:2025 (published July 30, 2025 by CEN) defines current automotive diesel requirements, with parameters that become more challenging as permitted FAME content rises. This reinforces the role of additives in meeting seasonal CFPP and related limits. In the United States, ASTM International published ASTM D975-26B on March 15, 2026, keeping diesel quality requirements current and maintaining a common reference point for refiners, terminals, and additive suppliers.

Regulatory oversight and compliance mechanisms also shape product registration and validation pathways. EU Member States monitor fuel quality annually under the Fuel Quality Directive (Directive 98/70/EC), with 2024 monitoring results reported through EEA/Eionet in 2026. This sustains attention on sulfur and bio-component parameters that influence cold-flow behavior. In parallel, the US EPA maintains a registered diesel additives framework, and industry criteria catalogues such as DGMK Report 787 are used by refineries to qualify additive use. That approach encourages suppliers to document performance against standardized tests and regional diesel specifications.

Value Chain Analysis

The cold flow improver value chain starts with upstream petrochemical and oleochemical feedstocks (for example, vinyl acetate, maleic anhydride, and fatty-acid-derived monomers). These inputs are polymerized into chemistries such as EVA- and methacrylate-based packages. Major formulators and marketers, including Afton Chemical, Infineum, Innospec, Clariant, Evonik, BASF, and Lubrizol, then rely on application labs to translate these inputs into finished additive concentrates, with treat-rate guidance aligned to diesel, biodiesel, and other distillate streams.

In the midstream, performance qualification is a key value-adding step. Additive suppliers frequently request base-fuel samples from refiners or terminals to tailor formulations to local crude slates, blending practices, and biofuel variability, and then validate results using standardized cold-flow test methods before commercial deployment. Downstream, distribution flows through refinery additive injection points, terminals, and fuel marketers, where technical service and troubleshooting are central during winter operations. Increasing biofuel penetration, including HVO and higher-FAME blends, adds complexity to the blend matrix, raising the importance of rapid reformulation capability, local inventory, and close coordination between additive suppliers and fuel producers to avoid off-spec cold performance.

Competitive Landscape

The Cold Flow Improver market is moderately fragmented with major players, including BASF, Evonik Industries AG, Infineum International Limited, Afton Chemical, and the Lubrizol Corporation that possess integrated supply chains, global application labs, and recent capacity investments. BASF’s 2024 Basoflux upgrade positions it to serve new mining and pipeline projects. Technology differentiation is sharpening as Evonik Industries AG introduces VISCOPLEX biodiesel additives and academic labs publish breakthroughs in montmorillonite nanocomposites that deliver pour-point cuts to (–33)°C. Smaller regional players remain competitive by customizing polymer blends to local fuel chemistries and offering quick technical support.

Cold Flow Improver Industry Leaders

BASF

The Lubrizol Corporation

Afton Chemical

Infineum International Limited

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity area is compliance-assurance packages that help refiners and terminals meet cold-flow targets as fuel specifications evolve. EN 590:2025 in Europe and ASTM D975-26B in the United States keep diesel quality frameworks current, while annual EU fuel-quality monitoring under Directive 98/70/EC (with 2024 data reported in 2026 via EEA/Eionet) sustains visibility on parameters such as sulfur and bio-component content that can shift low-temperature behavior. This supports demand for additive solutions that are validated against standardized test methods and can be tuned to local fuel chemistries.

Another whitespace is feedstock-specific biodiesel cold-flow performance. Crystallization behavior differs across soybean- and palm-oil-derived FAME and other blends, increasing the need for tailored polymer architectures and formulation support. Technology development is also extending upstream into fuel production: Evonik and Zeopore introduced high-performance isodewaxing catalysts in April 2026 aimed at improving cold-flow properties during fuels and lubricants processing. This creates a pathway for combined catalyst-plus-additive strategies that widen operability windows for winter-grade fuels. On the supply side, the market continues to reward suppliers that pair regional manufacturing and stocking with fast technical service, particularly in Asia-Pacific, where scale, policy alignment on lower sulfur, and higher bio-blend activity increase the value of local formulation and shorter lead times.

Recent Industry Developments

- May 2026: SANYO CHEMICAL INDUSTRIES, LTD. announced development of NEOPROVER HBF-201 and NEOPROVER HBF-301 cold flow improver formulations tailored for soybean- and palm-oil-derived biodiesel fuels. The updates target feedstock-specific crystallization behavior that can limit winter operability at higher bio-blend ratios, expanding treatability options for biodiesel producers and fuel blenders.

- September 2025: BASF launched the Keropur Gasoline Performance Additive Series, including Keropur AP 225-20, positioned to meet the revised U.S. TOP TIER+ detergent gasoline standard, with initial deliveries planned for the first half of 2026. While focused on gasoline detergency, the move signals continued investment in regulated performance additive platforms and strengthens BASF's positioning with fuel marketers that typically source multiple additive functionalities from a smaller set of suppliers.

- December 2024: SANYO CHEMICAL INDUSTRIES, LTD. launched NEOPROVER HBF-101, a cold flow improver designed to enhance the low-temperature flowability of biodiesel fuels and reduce engine malfunctions in cold climates. The product addition reinforced the companys biodiesel-focused portfolio depth as winter operability becomes a decisive constraint on higher biodiesel blend usage.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cold flow improver market covers specialty additive chemistries that are blended into fuels and related fluids to improve low-temperature operability, such as pour point and filterability, and then sold across key consuming industries.

Scope exclusions: Excludes non-additive mechanical heating solutions and winter handling equipment that do not involve additive consumption.

Segmentation Overview

- By Type

- Polyalkyl Methacrylate (PAMA)

- Ethylene Vinyl Acetate (EVA)

- Polyalpha Olefin (PAO)

- Others

- By End-user Industry

- Automotive

- Aerospace and Defense

- Other End-user Industry

- By Fuel / Application

- Diesel

- Biodiesel

- Aviation Fuel

- Lubricating Oil

- Crude Oil

- Others

- Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a simple demand map for fuels and fluids that typically need cold flow support in winter conditions. Public sources were used to anchor volumes and policy context, such as the US Energy Information Administration, Eurostat energy statistics, International Energy Agency fuel outlooks, ASTM published test method references (for diesel cold flow properties), and the European Commission's public pages on fuel quality and blending.

To keep assumptions realistic, we also reviewed company annual reports, technical product literature, and credible trade and refining press for blending trends, winter-grade diesel timing, and biodiesel mix impacts. A paid subscription covering company financials and intelligence, plus patent databases, was referenced selectively to cross-check product positioning and innovation activity. These sources are illustrative only, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with additive value chain participants, including producers, distributors, fuel blenders, and end users that manage winter operability programs. We used these discussions to confirm typical treat rates, seasonal purchasing patterns, and how biodiesel mandates change additive needs, and then to sanity-check regional splits across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 48% |

| Mid tier: 45% | Functional/Unit leaders: 32% | EMEA: 32% |

| Smaller Players: 18% | Managers: 55% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where fuel demand and blending trends are reconstructed by region and then translated into additive consumption through practical conversion steps. Our model links the demand pool to a few clear drivers, including diesel consumption levels, biodiesel blending penetration, the share of cold-climate operations that trigger winter-grade programs, typical cold flow improver treat rates, and average selling price progression by chemistry mix.

After the top-down totals are shaped, selective bottom-up approximations are used as a check, such as supplier and distributor revenue reasonability, channel checks on seasonality, and sampled pricing ranges applied to implied volumes. Where company disclosures do not separate cold flow improvers cleanly from broader additive lines, gaps are handled through conservative allocation rules agreed with interview inputs and then tested for sensitivity.

For forecasting, scenario analysis is used because winter severity, diesel versus biodiesel mix, and regulatory changes can move volumes in uneven ways year to year. The forward view is then adjusted using expert consensus on factors like regional diesel outlooks, renewable fuel policy direction, and expected shifts in additive chemistry preference.

Data Validation & Update Cycle

Validation is done through cross-checks between the market model and independent signals, including fuel demand direction, biodiesel blend shifts, and observed seasonality in winter-grade fuel preparations. Outliers are investigated at region and application level, and then the assumptions are reviewed again before sign-off, especially around treat rates and pricing that can drift with crude-linked feedstocks.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory changes, sharp changes in diesel demand, or meaningful pricing swings in additive raw materials. Before delivery, a final analyst pass is completed so clients receive the latest updated view that still remains traceable to the same set of inputs.

Mordor Intelligence's Cold Flow Improver Market Size Compared Against Other Published Estimates

Published values for cold flow improvers can vary even when they talk about the same broad topic, because the market boundary is not always set the same way. Differences usually come from the chosen base year, which fuel and fluid applications are counted, and how treat rates and price averages are translated into a single USD number.

In our checks, winter-grade diesel timing, biodiesel blending penetration, and region-level diesel demand direction are the evidence used to keep the sizing tied to realistic additive consumption, and that alignment is why Mordor Intelligence reports USD 0.95 B for 2026. Other estimates can move up or down when they use a different base year, apply aggressive winterization assumptions across warmer geographies, or blend in adjacent additive functions that are not strictly cold flow improvement.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.95 B (2026) | |

| Global Consultancy A | USD 0.85 B (2024) | Uses an earlier base year and can understate the later-cycle uplift from biodiesel blend increases and post-2024 diesel volume normalization in key regions, which shifts the implied demand pool. |

| Industry Publisher B | USD 0.87 B (2024) | Often applies broad average treat rates without clearly separating diesel versus non-diesel applications and seasonal buying patterns, which can compress the value when winter-driven volumes are smoothed across the year. |

The spread in the table mainly comes down to base-year selection and how clearly the demand pool is connected to diesel and biodiesel winter operability needs. By keeping the steps visible, from fuel indicators to treat-rate and price logic, we get a balanced number that can be repeated and audited as those inputs change.

Key Questions Answered in the Report

What is the current value of the Cold Flow Improver market?

The Cold Flow Improver market size stands at USD 0.95 Billion in 2026.

Which region leads the Cold Flow Improver market?

Asia-Pacific holds 35.33% of global revenue and is also the fastest-growing region at 6.12% CAGR through 2031.

Which fuel application creates the highest demand for cold flow improvers?

Diesel accounts for 59.48% of market revenue, although biodiesel is the fastest-growing segment at 8.04% CAGR.

How does biofuel adoption influence cold flow improver demand?

Higher biodiesel blends raise cloud and pour points, necessitating advanced additives such as PAMA-based polymers to ensure winter operability.

Page last updated on: