Cooling Fabrics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

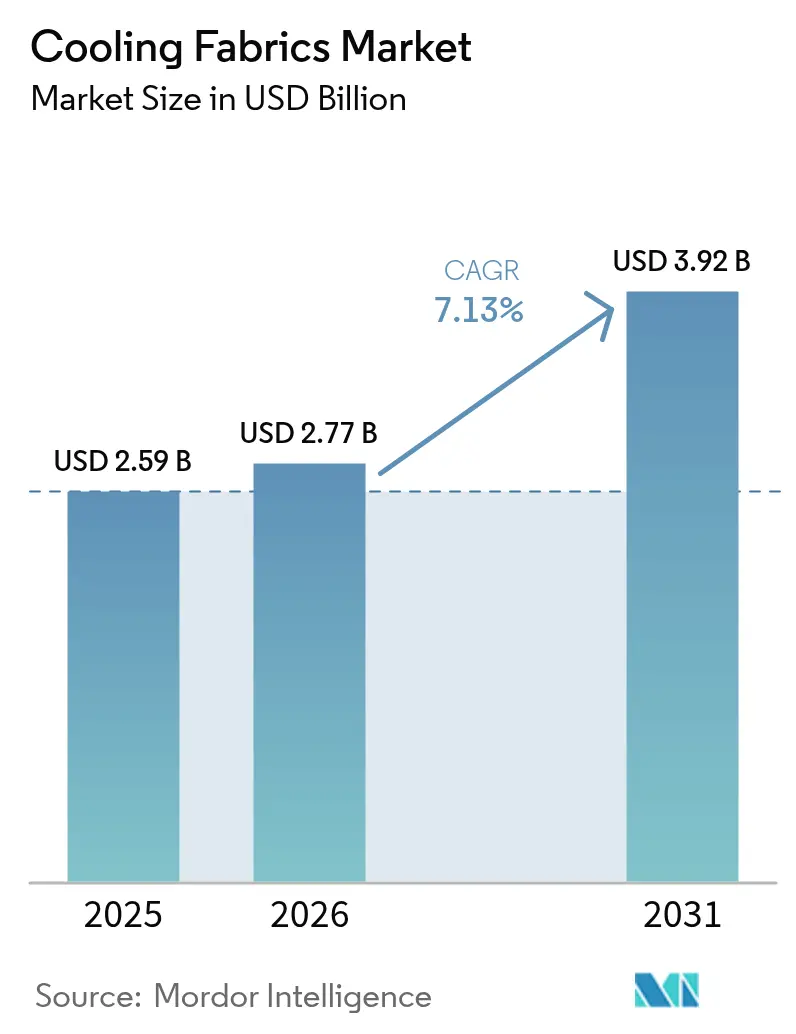

| Market Size (2026) | USD 2.77 Billion |

| Market Size (2031) | USD 3.92 Billion |

| Growth Rate (2026 - 2031) | 7.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

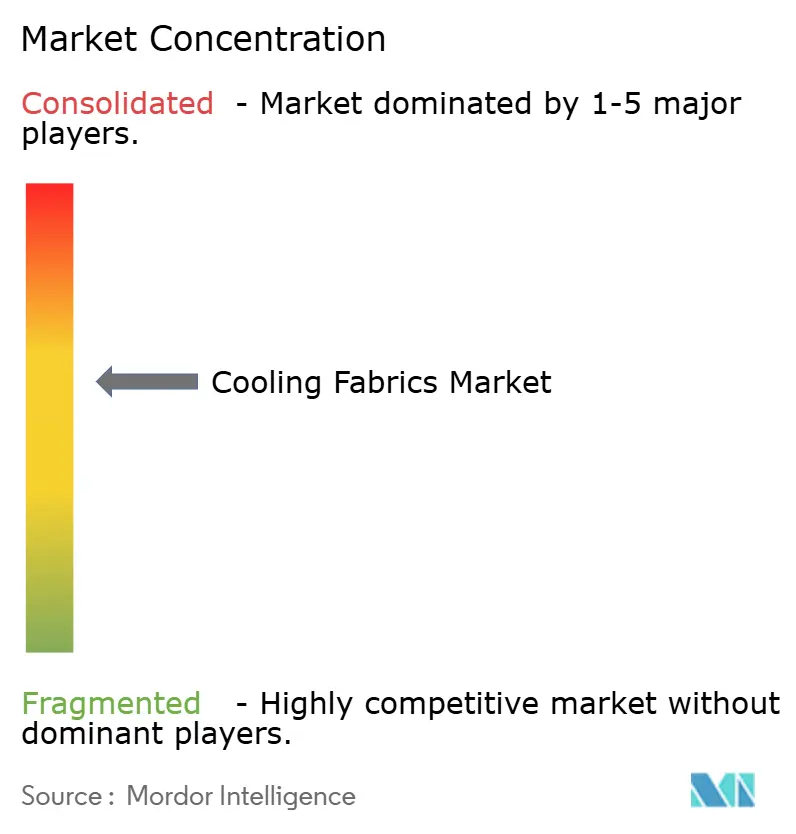

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cooling Fabrics Market Analysis by Mordor Intelligence

Cooling Fabrics market size in 2026 is estimated at USD 2.77 billion, growing from 2025 value of USD 2.59 billion with 2031 projections showing USD 3.92 billion, growing at 7.13% CAGR over 2026-2031. Heightened urban heat island effects, widespread athletic and outdoor lifestyles, and rapid material-science breakthroughs position the cooling fabrics market for sustained expansion. Synthetic moisture-wicking fibers, passive radiative “metafabrics,” and recycled yarn innovations are widening product capabilities while sustainability mandates accelerate natural-fiber adoption. Manufacturers gain scale advantages from woven constructions that accept coatings and hybrid finishes without compromising integrity, and military procurement is stimulating premium product diffusion into civilian segments. Price sensitivity in emerging economies and performance fade after laundering remain headwinds, yet diversified application uptake continues to outweigh these constraints.

Key Report Takeaways

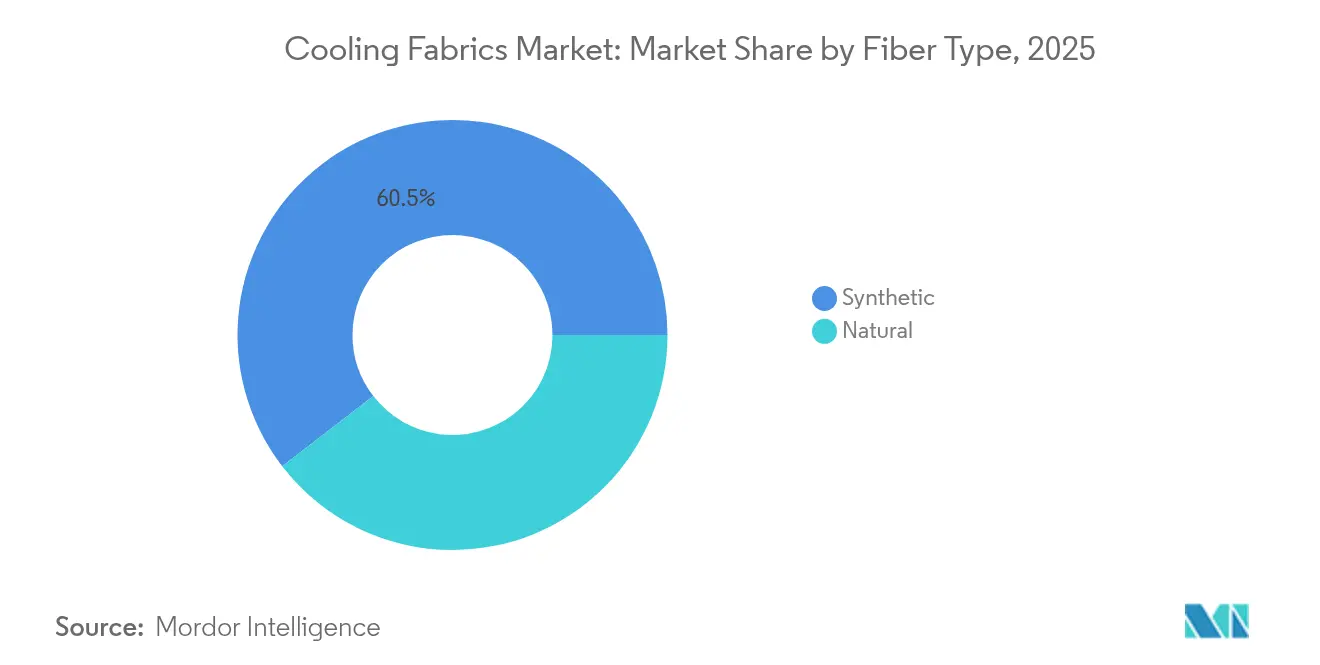

- By fiber type, synthetic fibers led with 60.45% of the cooling fabrics market share in 2025, while natural fibers are projected to grow fastest at an 8.03% CAGR to 2031.

- By fabric construction, woven textiles held 40.12% revenue share in 2025 and are advancing at an 8.25% CAGR through 2031.

- By application, sportswear commanded 46.88% of the cooling fabrics market size in 2025; protective wear is expanding at an 8.12% CAGR through 2031.

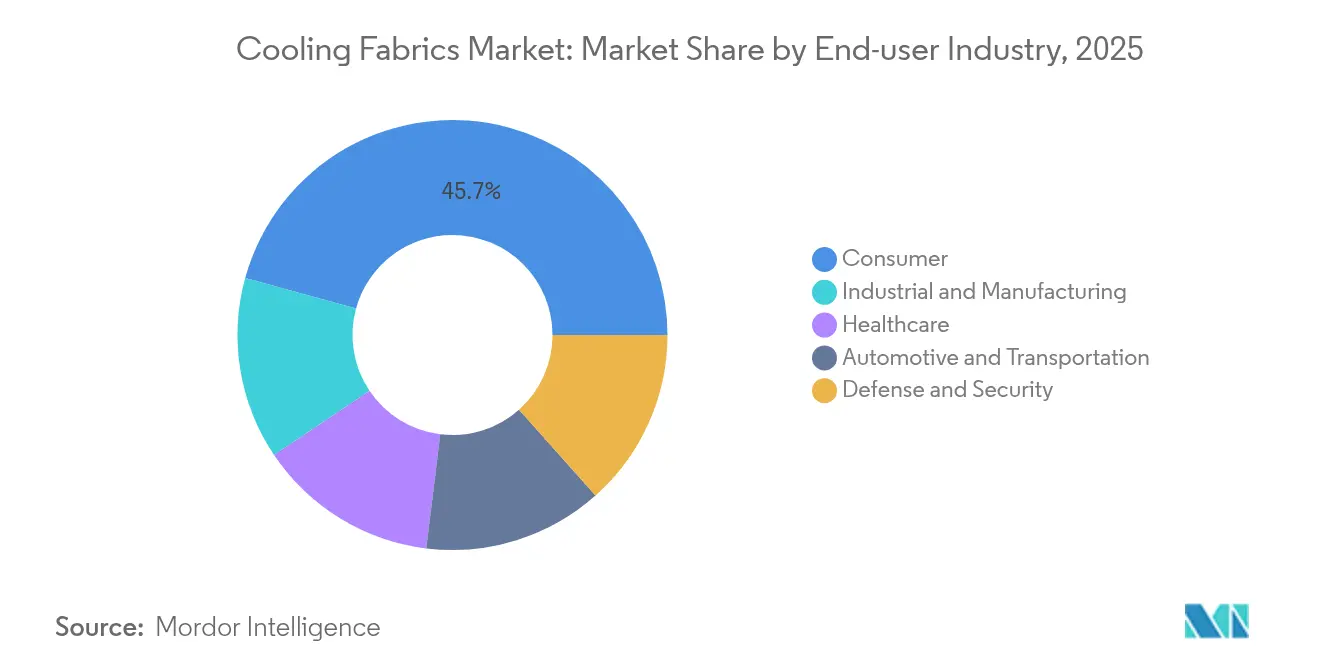

- By end-user industry, consumer products contributed 45.73% of 2025 revenue, whereas defense and security applications are set to register a 7.72% CAGR between 2026-2031.

- By geography, Asia-Pacific accounted for 31.05% of 2025 revenue and is expected to post a 7.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Cooling Fabrics Market*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Synthetic Moisture-wicking Fibers for Sports and Athleisure | +1.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Expansion of Outdoor and Performance Apparel Brands Globally | +1.5% | Global, led by Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Breakthrough Passive Radiative “Metafabrics” for Urban Heat Mitigation | +1.2% | Urban centers worldwide, early adoption in China & US | Long term (≥ 4 years) |

| Military Procurement of Heat-stress Uniforms for Desert Operations | +0.9% | North America, Middle East, select Asia-Pacific | Short term (≤ 2 years) |

| Sustainability Mandates Accelerating Recycled Cooling Fibers Adoption | +1.1% | EU-led, expanding to North America & developed Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Synthetic Moisture-wicking Fibers for Sports and Athleisure

Athleisure and performance sportswear now treat dynamic cooling as a baseline expectation. Brands integrate COOLMAX EcoMade, brrr° and comparable yarns that embed phase-change materials or micro-minerals, providing continuous heat draw-down even under heavy perspiration [1]The LYCRA Company, “COOLMAX EcoMade Expands Sustainable Options,” lycra.com. Market penetration benefits from global participation in fitness and outdoor recreation, and synthetic fibers retain dominance because they deliver repeatable moisture transport, stretch and mechanical durability. Technical-textile advances lift synthetic yarns’ share of global fiber demand above 19%, reinforcing scale economies that underpin the cooling fabrics market. With nanohybrid fillers improving thermal conductivity, engineered synthetics outperform many natural alternatives. In parallel, recycled Polyethylene Terephthalate (PET) streams keep cost bases stable while satisfying tightening eco-design rules.

Expansion of Outdoor and Performance Apparel Brands Globally

Multinational outdoor labels channel proprietary cooling platforms into both back-country and everyday urban lines. Columbia Sportswear’s Omni-Heat Infinity and Omni-Shade technologies exemplify such crossover. Heat-mitigating fabrics combat city temperatures that can sit 8.9°C higher than surrounding rural zones, broadening addressable demand. As brands leverage Asia-Pacific manufacturing clusters, they shorten development cycles and lower per-unit costs, making premium cooling attainable for mainstream consumers. Iterative launches that combine 3D-printed structures with aerodynamic panels demonstrate a migration of elite-sport learnings to lifestyle garments, thus enlarging the cooling fabrics market. Technology transfer across hemispheres further accelerates global uptake.

Breakthrough Passive Radiative “Metafabrics” for Urban Heat Mitigation

Metafabrics redirect solar radiation and emit body heat through atmospheric windows, achieving up to 5°C skin-temperature reduction without external energy. Lab data show emissivity near 94.5% and reflectivity above 92.4%, while silver-nanowire trilayers sustain 2.3°C advantages over incumbent synthetics. Machine-learning-optimized metasurfaces push reductions to 15.4°C under direct sun, pointing to disruptive gains. Commercial sewing techniques can produce these multilayer textiles at roughly a 10% cost premium, keeping price gaps manageable. As global cities target personal cooling to lessen air-conditioning loads, metafabrics can unlock large addressable volumes, underpinning a long-run CAGR boost for the cooling fabrics market.

Military Procurement of Heat-stress Uniforms for Desert Operations

Defense ministries allocate dedicated budgets for next-generation uniforms that stabilize core temperatures beyond 46°C ambient conditions. US Navy SBIR (Small Business Innovation Research) grants explore dynamic thermal suits, while multispectral camouflage fabrics combine infrared suppression with conductive cooling. Procurement cycles create predictable offtake for high-spec textiles, allowing suppliers to scale novel chemistries faster than civilian buyers might tolerate. After battlefield validation, many designs transition to industrial or outdoor segments, widening revenue bases. Military endorsement also affirms performance credibility, de-risking adoption by risk-averse institutional customers in oil, gas and construction domains.

Restraints Impact Analysis of Cooling Fabrics Market*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Cost of Advanced Cooling Textiles | -1.4% | Global, with sharper effect in price-sensitive emerging economies | Short term (≤ 2 years) |

| Performance Degradation After Repeated Laundering Cycles | -0.8% | Global, contingent on washing practices | Medium term (2-4 years) |

| Dye-uptake Limitations on High-reflectance Radiative Fabrics | -0.6% | Global, concentrated in fashion and consumer apparel segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production Cost of Advanced Cooling Textiles

Passive-radiative layers call for titanium dioxide nanoparticles, polymer membranes and silver nanowires that elevate bill-of-materials costs relative to commodity apparel. Specialized coating lines introduce capital outlays, while stringent quality-control protocols add labor intensity. Although process optimization has trimmed the premium to almost 10%, sticker shock persists in lower-income regions, slowing volume. Suppliers must refine continuous-roll deposition and broaden raw-material options to reach mass-price points. Scaling pauses notwithstanding, premium categories such as defense, professional sports and industrial Personal Protective Equipment (PPE) absorb the cost, allowing research and development (R&D) amortization that should eventually spill into value segments.

Performance Degradation After Repeated Laundering Cycles

Cooling finishes can leach or crack under mechanical agitation and detergent chemistry, leading to diminished wicking or emissivity after successive washes. Cotton blends often lose tensile strength faster than synthetics, and coatings relying on microcapsules may rupture. Durability shortfalls erode consumer satisfaction and curb repeat buy rates. Material scientists explore covalent-bonded coatings, plasma treatments and core-sheath filament architectures to raise wash resilience. Progress here is pivotal because expected garment lifespans in mainstream wardrobes extend toward 50 wash cycles. Until robust solutions scale, warranty claims and brand reputation risk will temper the cooling fabrics market growth curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cooling Fabrics Market Segment Analysis

By Fiber Type:

Natural Fibers Drive Sustainability TransitionSynthetic yarns retained 60.45% of cooling fabrics market share in 2025 by delivering uniform moisture transport and stretch at scale. They underpin many patented cooling chemistries that remain cost-optimal for high-volume sportswear. Natural fibers, though, are on an 8.03% CAGR path as regulators and consumers prize biodegradability. Cotton modified with nanodiamonds or chitosan micro-porosity now attains 2–3°C temperature drops, while closed-loop cupro yarns marry plant-based feedstocks with industrial recyclability. Blended constructions pair regenerated cellulose with micro-mineral synthetics, balancing feel and function. Investors therefore finance gin upgrades and enzymatic pre-treatments that elevate natural fiber quality, pointing to broader acceptance within the cooling fabrics market.

Hybrid yarn advances demonstrate that sustainability targets and performance metrics need not be mutually exclusive. Bemberg cupro showcases solvent recovery rates exceeding 99%, illustrating circularity without sacrificing heat-dissipation capacity. Recycled cotton streams also outperform virgin cotton on thermal resistance in pilot trials. As fashion groups publish science-based carbon goals, procurement pivots toward these lower-impact options, translating eco-preference into measurable demand. Over the forecast horizon, natural-fiber cooling lines will likely take incremental share, though synthetics will remain central to rapid-wicking and stretch-critical apparel tiers.

By Fabric Construction:

Woven Dominance Through Manufacturing EfficiencyWoven fabrics supplied 40.12% of 2025 revenue and are growing at an 8.25% CAGR because their tightly-controlled interlacings provide dimensionally stable substrates for nanoparticle coatings, reflective films and phase-change print pastes. Weaving plants already operate at high throughput, minimizing incremental cost to add cooling capability. Knits retain strong footholds in activewear thanks to comfort stretch and breathability, yet their looped structure demands slower machinery and can complicate multilayer coatings. Non-wovens gain relevance in disposable medical or filtration niches where tactile drape is secondary.

Process innovation continues to lift woven productivity, with water-jet looms delivering finer deniers while conserving energy. Multi-phase weaves adjust pore geometry, aiding moisture vapor transport. At the same time, knitting equipment adopts digital control and finer gauges, narrowing the gap in surface regularity. Electrospun membranes layered onto knits or wovens add ultra-thin emissive skins, creating hybrid laminates that fuse each construction’s strengths. Cost and versatility advantages suggest woven textiles will retain top billing in the cooling fabrics market, but rising consumer appetite for stretch will keep knitted shares steady rather than declining.

By Application:

Protective Wear Accelerates Through Safety MandatesSportswear generated 46.88% of 2025 revenue due to widespread adoption in athletic and athleisure apparel, yet protective wear is staging the quickest advance at an 8.12% CAGR. Industrial, firefighting and defense users tolerate higher price points to safeguard personnel performance under extreme heat . Regulatory bodies now classify heat stress alongside chemical hazards, prompting employers to specify cooling Personal Protective Equipment (PPE) under occupational-safety regimes.

Protective garments integrate phase-change liners, infrared-blocking veils and moisture-activated cooling gels without hindering mobility. Firefighter turnout designs merge breathable barriers with non-PFAS (per- and polyfluoroalkyl substances) water repellency, illustrating how cooling functions coexist with flame and chemical resistance. Smart robotic exosuits that adjust vent apertures in response to skin temperature show early promise for foundry and mining roles. Beyond heavy industry, healthcare settings deploy cooling scrubs and patient gowns that stabilize body temperature during long procedures, opening steady institutional demand. These shifts position protective wear as a vibrant revenue engine inside the cooling fabrics market.

By End-user Industry:

Defense Sector Drives Premium AdoptionConsumer apparel occupies 45.73% of 2025 turnover, buoyed by affordable activewear and rising comfort expectations in daily wardrobes. Defense and security clients, however, deliver a 7.72% CAGR owing to mission-critical specifications that prize thermal performance over cost. Military acquisition programs stipulate durability, multispectral concealment and electrolyte balance maintenance, pushing suppliers to exceed civilian benchmarks.

Industrial employers also upgrade uniforms to curb heat-related accidents that erode productivity, particularly in oil platforms, steelmaking and logistics yards. Healthcare institutions embrace cooling bedding and post-surgery wraps to manage patient core temperatures. Automotive Original Equipment Manufacturers (OEMs) test ventilated seat fabrics that cut cabin cooling loads, drawing on the same emissive coatings proven in apparel. Each end-user niche multiplies addressable volume, reinforcing a diversified demand base for the cooling fabrics market.

Geography Analysis

APAC Cooling Fabrics Market

Asia-Pacific held 31.05% of global revenue in 2025 and is moving at a 7.63% CAGR through 2031, anchored by China’s scale in technical-textile exports and its leadership in passive-radiative research that delivers 5°C garment cooling. Government grants support pilot plants for metafabric yardage, while downstream apparel makers in Vietnam, Indonesia, and India integrate these textiles into cost-competitive cut-and-sew lines. Japan’s material-science ecosystem refines polymer blends for Ultraviolet (UV) reflection, and South Korea’s electronics sector pursues smart-textile overlays that feed body-temperature data to mobile devices. Rising middle-class populations confronting humid summers amplify retail pull.

North America Cooling Fabrics Market

North America benefits from defense contracts and an outdoor recreation culture. US Naval Air Systems programs accelerate supplier learning curves and validate ruggedized cooling fabrics. Outdoor labels headquartered in Oregon and Colorado roll new collections each summer, driving steady consumer uptake. Canada’s severe temperature swings prompt multi-season layering concepts that embed cooling on one face and insulation on the other, stretching product utility. Mexico expands role as a near-shore sewing destination, giving brands flexibility amid global logistics disruptions.

Europe Cooling Fabrics Market

Europe’s trajectory intertwines with environmental policy. The European Union (EU) Ecodesign regulation prioritizes textiles, compelling value-chain traceability and recyclate usage. German mills like Outlast adapt NASA-born Phase Change Material (PCM) treatments into eco-certified linings, while Italian spinners push low-impact dyeing of recycled yarns. The United Kingdom (UK) research councils fund university-industry consortia focused on nanostructured emissive films. Higher energy costs in the region reinforce demand for passive personal cooling, stimulating domestic uptake despite premium pricing.

South America and MEA Cooling Fabrics Market

South America and the Middle East & Africa present emerging opportunities tied to rapid urbanization and intense solar exposure. Brazil’s athletic-wear boom spurs local sourcing of phase-change infused polyester, and Gulf states test cooling uniforms for construction crews working in 45°C midday heat. Infrastructure gaps and limited disposable income temper near-term volumes, yet sustained climate warming suggests long-run growth. Global suppliers eye joint ventures and technology-licensing to local partners to overcome tariff and logistics hurdles, ensuring the cooling fabrics market achieves broader geographic balance.

Value Chain Analysis

Upstream inputs span commodity and specialty polymers (polyester, nylon, polyethylene and PLA) plus functional additives, including mineral-based cooling agents, phase change materials and nanoparticle systems (for example TiO2 and SiO2) used to tune emissivity and reflectance. At the chemical-supplier layer, formulation and compliance screening is increasingly linked to restricted-substance expectations in apparel and PPE supply chains (for example REACH-aligned and OEKO-TEX and ZDHC oriented requirements). That is pushing adoption of formaldehyde-free and APEO/NPEO-free finishing chemistries. Intellectual property and materials science also shape feedstock choices, with radiative-cooling architectures moving from lab concepts to textile-compatible stacks that combine polymers with conductive or reflective layers (for example silver-nanowire and multilayer fiber constructs reported in 2026 peer-reviewed studies).

Midstream manufacturing routes split between (i) dope-dyeing or extrusion-level integration, where cooling minerals or functional fillers are embedded in yarn to improve wash durability, and (ii) post-fabric finishing, where padding, exhaust and stenter-based application of cooling agents and coatings is added to woven and knitted greige goods. Converters and mills then supply fabric rolls to brand and uniform program owners, while downstream distribution is led by performance apparel brands, workwear/PPE suppliers, and defense-oriented sourcing channels. Key bottlenecks remain the cost and complexity of multi-material radiative-cooling builds (metal-nanowire/polymer hybrids and hierarchical pore structures) and the consistency of performance retention after laundering, which raises demand for measurable specifications such as Q-max and radiative spectral selectivity during qualification and procurement.

Competitive Landscape

The Cooling Fabrics market features a moderate consolidation, dominated by key players including Coolcore, Columbia Sportswear Company, HeiQ Materials AG, Milliken & Company, and Asahi Kasei Corporation. Leveraging proprietary chemistries and a global distribution network, these industry leaders set performance benchmarks, often emulated by smaller competitors. Notable IP-protected innovations include HeiQ Materials AG’s Smart Temp coating and Columbia Sportswear Company’s Omni-Heat Infinity foil dot patterns. Milliken & Company’s R&D 100-winning Polartec Power Shield Pro highlights the fusion of scale and deep innovation. These established players consistently refresh their offerings, forging collaborations with fiber producers like NILIT and Nan Ya to secure upstream supplies.

Cooling Fabrics Industry Leaders

Asahi Kasei Corporation

Coolcore

Columbia Sportswear Company

HeiQ Materials AG

Milliken & Company

- *Disclaimer: Major Players sorted in no particular order

Cooling Fabrics Market Companies Covered in this Report

- Ahlstrom

- Asahi Kasei Advance Corporation

- Balavigna Mills Pvt. Ltd.

- brrr°

- Cocona Labs

- Columbia Sportswear Company

- Coolcore

- Elevate Textiles, Inc.

- Everest Textile Co., Ltd.

- FORMOSA TAFFETA CO., LTD.

- HeiQ Materials AG

- LunaMicro AB

- Milliken & Company

- NAN YA PLASTICS CORPORATION

- NILIT

- Outlast Technologies GmbH

Market Opportunities and Future Outlook

Heat-stress mitigation is expanding cooling-fabric design briefs beyond sportswear into workwear and protective wear programs that require measurable thermal performance and durability across repeated wash cycles. The International Labour Organization has highlighted the scale of heat exposure at work, reporting that 71% of the global workforce is exposed to excessive heat, which supports white space for employer-procured cooling uniforms, PPE liners and next-to-skin layers where buyers can justify higher unit costs through safety and productivity outcomes. At the same time, defense-driven specifications and industrial safety mandates continue to raise requirements for cooling textiles that also meet antimicrobial/odor-control, flame resistance or chemical barrier needs, favoring suppliers that can deliver multi-function stacks rather than single-claim finishes.

Technology whitespace is concentrated in scalable radiative-cooling and hybrid thermoregulation platforms designed to retain performance under sweat, abrasion and laundering. R&D in this area is converging on directional moisture transport, hierarchical pore engineering, and combined passive radiative plus phase-change buffering. Peer-reviewed 2026 materials work on multilayer spectrally selective radiative-cooling textiles and bioinspired PLA metafabrics illustrates how architectures are being adapted for wearable manufacturing constraints, while brand-facing productization continues to test consumer willingness to trial new form factors (for example Japan-market cooling wear and fan-integrated garments). There is also commercial opportunity in supply-chain simplification, as shifting from post-finish-only approaches toward fiber-level integration can reduce wash-off risk and warranty exposure, improving total delivered cost for brands and institutional buyers even when bills of materials remain elevated for advanced nano-enabled structures.

Recent Industry Developments in Cooling Fabrics Market

- June 2026: Coolcore and Snow Peak, Inc. launched the Peak Shade Evaporative Cooling Poncho in Japan, using Coolcore's Biomimetic Fiber Geometry for heat management alongside UV protection. The tie-up extends cooling-fabric adoption into a premium outdoor lifestyle channel and strengthens Coolcore's downstream pull-through in Asia via a recognized regional brand.

- February 2025: Noble Biomaterials and Coolcore debuted COOLPRO fabric at Performance Days Munich, combining Noble's Ionic+ Pro antimicrobial yarn technology with Coolcore's Biomimetic Fiber Geometry. The launch reflects rising demand for bundled functionality in performance textiles, where cooling and hygiene claims are qualified together for sportswear and workwear programs.

- August 2024: HeiQ Materials AG and GQ Apparel launched GQ Cool Tech Jeans in Thailand featuring HeiQ Cool, a biobased cooling technology integrated into denim. Bringing cooling finishes into everyday denim broadens the addressable apparel base beyond technical athletic categories and highlights Southeast Asia as an active commercialization market for cooling chemistries.

Cooling Fabrics Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the cooling fabrics market covers textile materials engineered to create a cooling feel for the wearer through moisture management, heat transfer, or phase change behavior, and the value is counted at the fabric level in USD.

Scope exclusions: We exclude finished apparel brand revenues, stand-alone cooling devices, and non-textile cooling accessories that are not sold as fabric.

Segments Covered in This Report

- By Fiber Type

- Natural

- Synthetic

- By Fabric Construction

- Woven

- Knitted

- Non-woven

- By Application

- Sportswear

- Protective Wear

- Apparels

- Other Applications (Medical and Healthcare Textiles, etc.)

- By End-user Industry

- Consumer

- Industrial and Manufacturing

- Defense and Security

- Healthcare

- Automotive and Transportation

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map where cooling fabrics are actually used, and to anchor the model with public signals on textile output, trade, and end use demand. We referred to sources such as UN Comtrade for fabric-related trade flows, the International Trade Centre for mirror statistics, and the US International Trade Commission data tools to cross-check tariff lines and import patterns.

To keep assumptions realistic, we also reviewed technical and adoption signals from sources such as the ASTM standards library (for test methods that influence performance claims), the USPTO patent database (to gauge innovation activity around cooling finishes and fibers), and peer-reviewed textile journals that describe cooling mechanisms and durability. Company filings, investor presentations, association websites, and reputed press were used to understand capacity additions and pricing direction. For financial normalization and limited private-company context, we used an approved paid subscription focused on company financials and intelligence. These desk research sources are illustrative, and many other public references were used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work was used to pressure-test the demand pool, the real-world price bands, and how cooling claims translate into repeat orders across regions. We spoke with raw material and fabric-side stakeholders, apparel and PPE buyers, and distribution-side participants so assumptions on penetration and mix could be tightened where public data stays broad. Since this is a global market, inputs were balanced across APAC, EMEA, and the Americas to avoid a single-region view driving the forecast.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 42% |

| Mid tier: 55% | Functional/Unit leaders: 34% | EMEA: 37% |

| Smaller Players: 16% | Managers: 53% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where textile production and trade data are reconstructed into an addressable fabric pool, which is then narrowed using cooling-fabric penetration by end use. The key checks include the share of sportswear and active lifestyle apparel in overall apparel demand, the shift toward synthetic performance textiles, and the adoption rate of cooling finishes or phase change treatments in targeted product lines.

Once the demand pool is formed, values are derived using a blended ASP approach, where price bands differ by fabric construction (woven, knitted, non-woven), treatment intensity, and typical order quantities. Results are then corroborated with selective bottom-up approximations like supplier revenue sampling, channel checks on fabric price per meter or per kilogram, and sanity checks against reported capacity utilization, which helps adjust totals where direct price data is patchy.

For forecasting, scenario analysis was used so the model can respond to variables that change unevenly across years, such as outdoor activity participation, heat stress and workwear compliance demand, and raw material price swings that impact fabric ASPs. Inputs were reviewed with primary experts, and gaps in supplier-side visibility were handled by using conservative penetration ramps and then rechecking the implied volumes against trade and production signals.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, and then reviewed for variance by region, application, and fabric type so outliers are not carried forward. Where the model implies unusual price jumps or volume dips, assumptions are rechecked against trade movement, apparel output trends, and feedback from recent interviews, and respondents are re-contacted when a discrepancy stays unresolved.

Before sign-off, a second analyst reviews the full chain of assumptions, followed by a final consistency check across historical and forecast years. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major capacity additions, regulation-driven PPE demand shifts, or sharp input cost moves. Right before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Cooling Fabrics Market Estimate Compared With Other Published Estimates

Published market values for cooling fabrics can differ because each publisher draws the line differently on what counts as cooling performance, and also because ASP and adoption rates are handled in different ways. Timing also matters, since some figures are tied to a base year, while others point to an estimated year that sits inside a forecast window.

The table shows a noticeable spread around the mid-2020s because cooling claims are not standardized across all textiles, and adjacent categories are sometimes mixed in. In Mordor Intelligence's model, revenues are counted at the fabric level across natural and synthetic cooling fabrics used in sportswear, protective wear, and apparel uses, and the 2026 value is built by linking a demand pool to price bands rather than using a single blended ASP for all regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.77 B (2026) | |

| Industry Publisher A | USD 2.31 B (2025) | Uses a 2025 base year and a longer forecast window, and the scope can tilt toward apparel-led demand framing, which can undercount fabric-level value when fabric pricing is modeled conservatively across regions. |

| Industry Publisher B | USD 2.02 B (2025) | Reports a 2025 base value with regional rollups, and the lower figure is consistent with stricter assumptions on adoption within lifestyle clothing and protective clothing, plus different currency timing and price normalization. |

Overall, the gap is mostly explained by year alignment and the treatment of ASP progression and penetration by application. When the demand pool, conversion into cooling-treated fabric share, and the pricing bands are stated clearly, it becomes easier to reconcile why 2025-based figures can sit below an estimated 2026 value and still be directionally consistent.

Key Questions Answered in the Report

What is the current value of the cooling fabrics market?

The cooling fabrics market size reached USD 2.77 Billion in 2026.

How fast is the cooling fabrics market expected to grow?

It is projected to expand at a 7.13% CAGR from 2026 to 2031.

Which segment is growing quickest within the cooling fabrics market?

Protective wear shows the fastest rise, advancing at an 8.12% CAGR due to safety mandates in industrial and defense sectors.

Why are woven constructions so prominent in cooling fabrics?

Woven textiles provide dimensional stability that supports nanoparticle and phase-change coatings while enabling large-scale, cost-efficient manufacturing.

How do sustainability regulations influence new cooling fabrics?

European Union (EU) Ecodesign and US state Extended Producer Responsibility (EPR) laws push producers toward recycled or bio-based fibers, accelerating the adoption of natural and chemically recycled yarns without compromising cooling performance.

Page last updated on: