Hydraulic Fluid Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

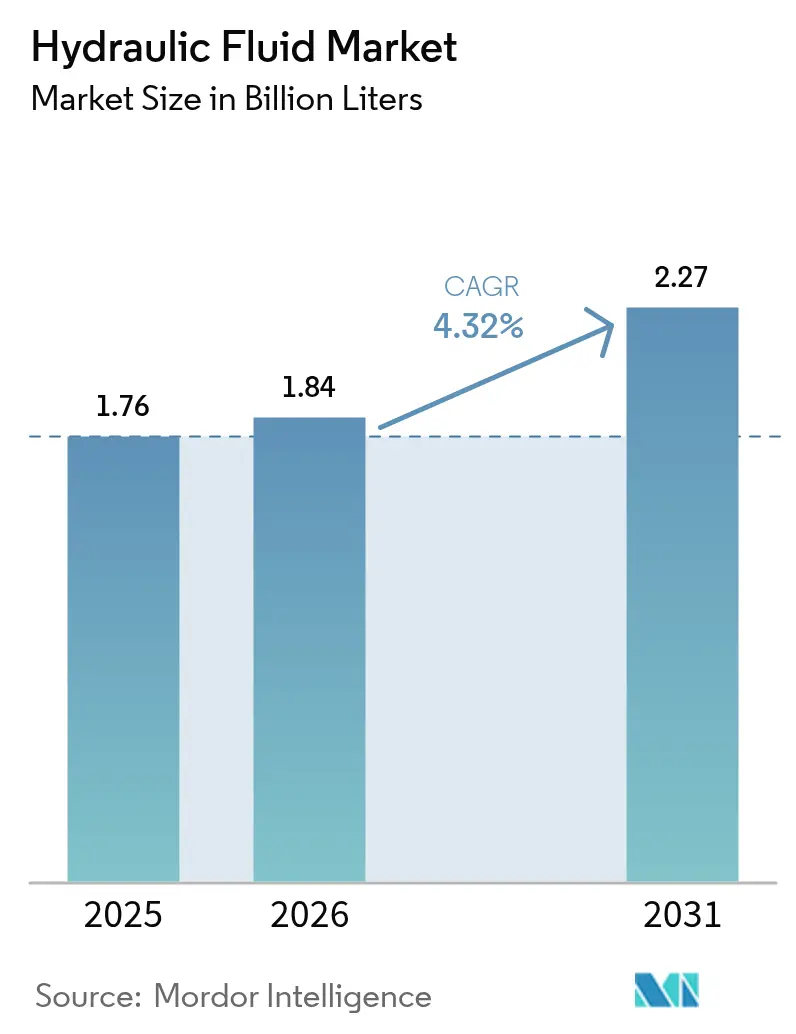

| Market Volume (2026) | 1.84 Billion liters |

| Market Volume (2031) | 2.27 Billion liters |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

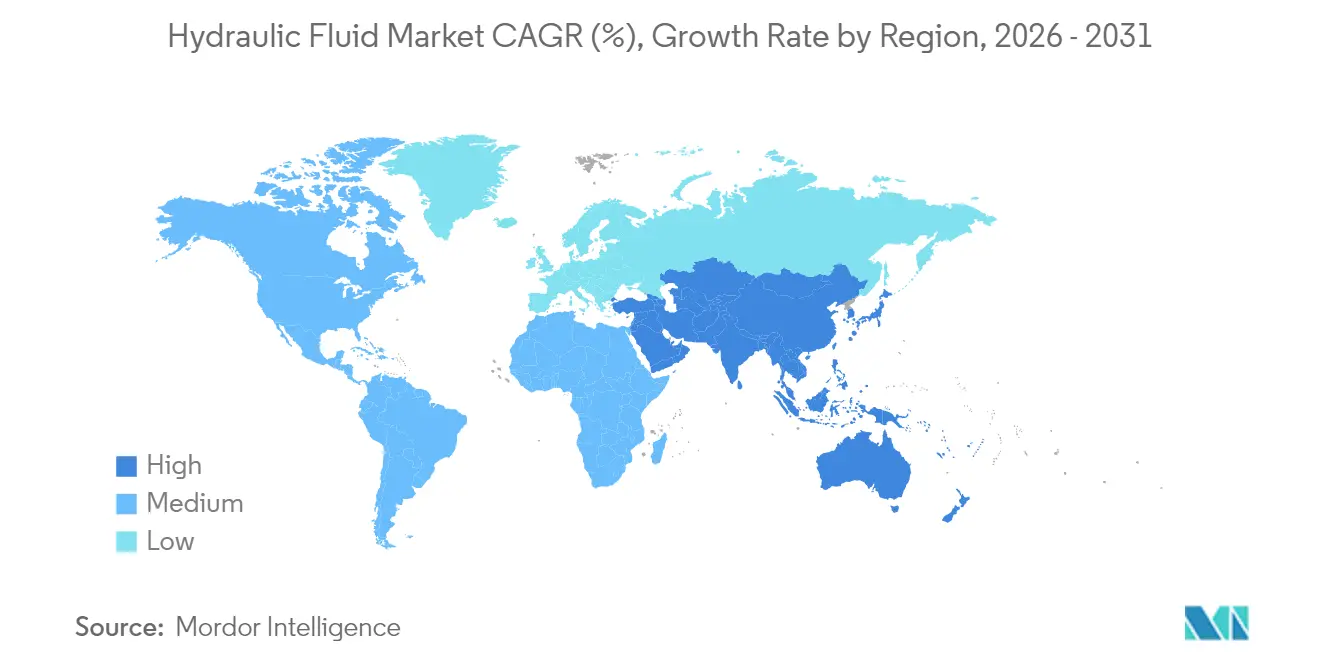

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydraulic Fluid Market Analysis by Mordor Intelligence

The Hydraulic Fluid Market size was valued at 1.76 billion liters in 2025 and estimated to grow from 1.84 billion liters in 2026 to reach 2.27 billion liters by 2031, at a CAGR of 4.32% during the forecast period (2026-2031). This sustained growth trajectory stems from steady infrastructure spending, a broad wave of equipment modernization, and the unmatched power density that fluid power offers in construction, mining, and agricultural machinery. Capital outlays for new earth-moving equipment, rising automation in factories, and the mechanization of large farms underpin recurring demand for high-quality fluids. Regulatory pushes for cleaner operations are encouraging end users to shift from legacy formulations toward low-viscosity and biodegradable blends, yet cost-effective mineral oils continue to dominate high-volume applications. Competitive intensity remains moderate: major lubricant suppliers leverage wide distribution footprints and technical service networks to lock in long-term service contracts, while regional specialists focus on niche applications such as fire-resistant aerospace fluids.

Key Report Takeaways

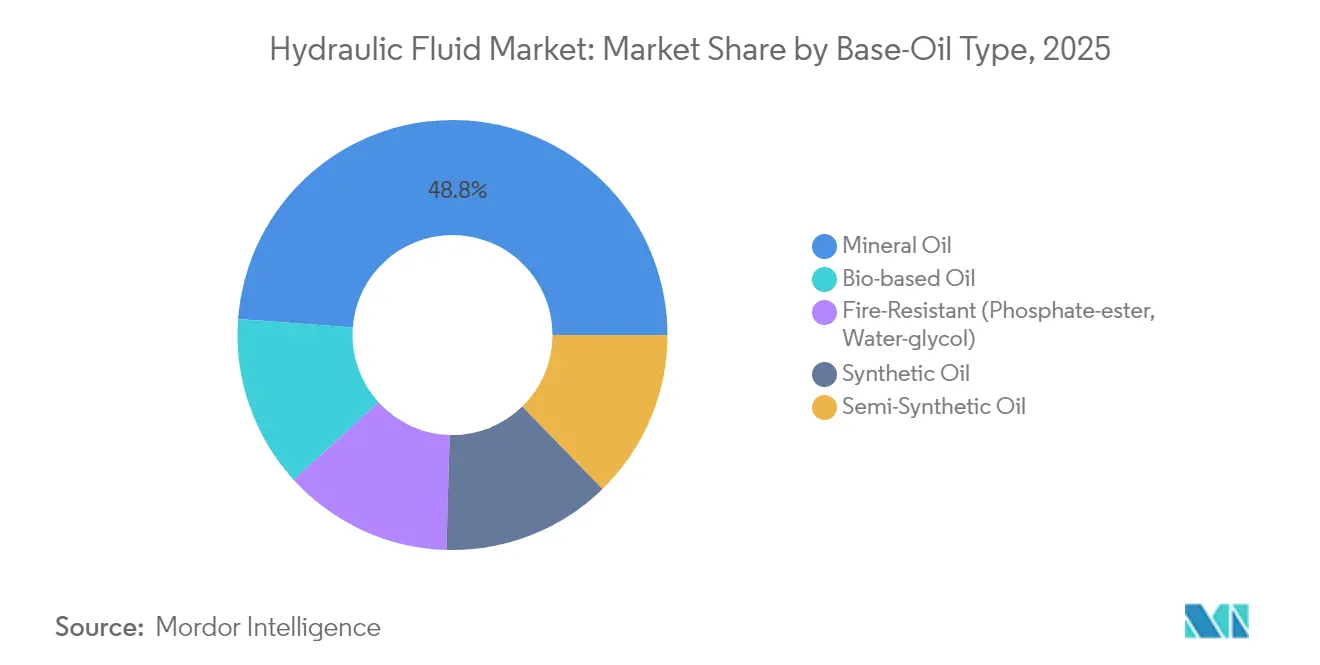

- By base-oil type, mineral oils led with 48.81% of hydraulic fluid market share in 2025, while bio-based products are forecast to expand at a 5.03% CAGR through 2031.

- By application, mobile hydraulic systems captured 54.76% of the hydraulic fluid market share in 2025; industrial stationary systems are projected to grow at a 4.26% CAGR through 2031.

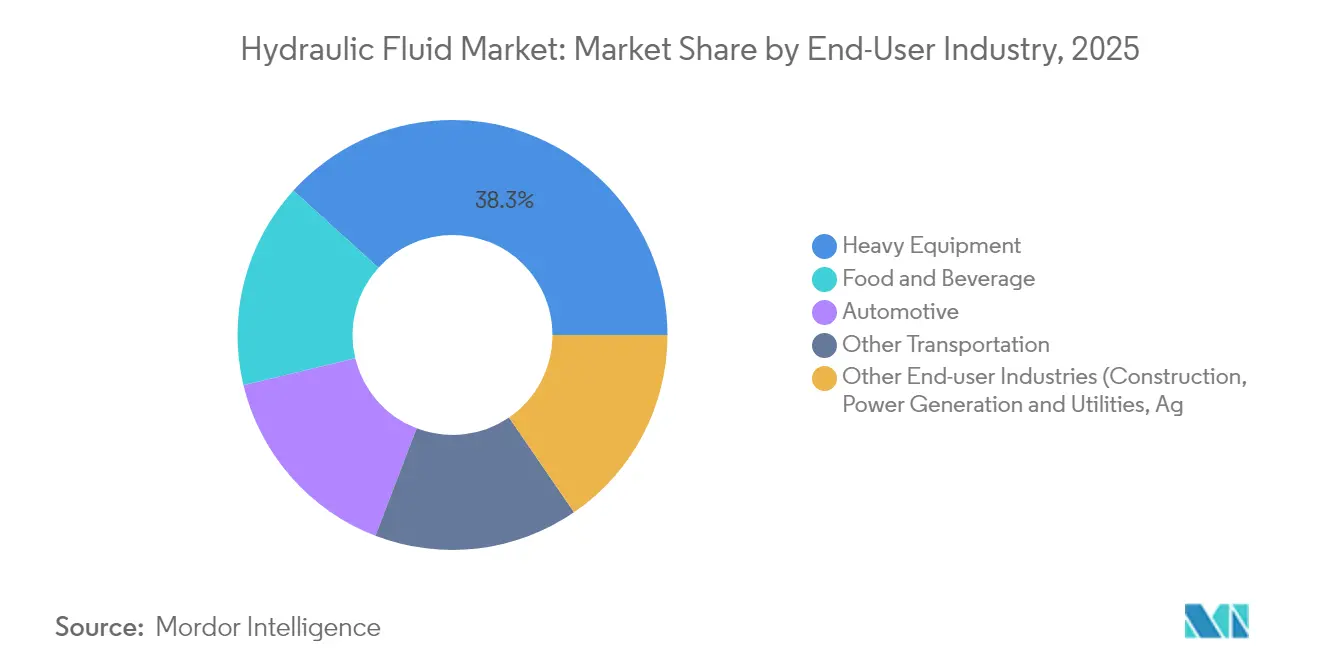

- By end-user industry, heavy equipment held 38.26% of the hydraulic fluid market size in 2025, whereas the “Other End-Industries” category is set to advance at a 5.94% CAGR between 2026 and 2031.

- By geography, Asia-Pacific commanded 40.75% revenue share in 2025, and the region is positioned to post the fastest 5.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydraulic Fluid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding construction and mining activities | +1.2% | Global with emphasis on Asia-Pacific and Middle East | Medium term (2-4 years) |

| Automotive and EV production growth | +0.8% | Global, led by Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Shift toward energy-efficient hydraulics | +0.6% | North America and Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Agricultural mechanization surge | +0.9% | Asia-Pacific core, spill-over to Latin America and Africa | Long term (≥ 4 years) |

| Adoption of fire-resistant aerospace fluids | +0.3% | Global, concentrated in aerospace manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Construction and Mining Activities

Construction equipment accounts for 76% of hydraulic equipment usage and therefore dominates fluid consumption. Robust infrastructure pipelines under China’s Belt and Road framework and India’s National Infrastructure Pipeline translate into sustained purchases of excavators, loaders, and cranes that demand premium fluids capable of coping with heat, dust, and extended duty cycles. Safety regulations in U.S. underground mining stipulate MSHA-approved fire-resistant fluids, boosting demand for phosphate-ester and water-glycol blends[1]U.S. Department of Labor, “MSHA hydraulic fluid fire safety regulations,” dol.gov. The post-pandemic rebound in mega-projects, alongside urbanization and resource extraction, creates a durable tailwind for the hydraulic fluid market.

Automotive and EV Production Growth Boosting Demand for Advanced Hydraulics

Electric-vehicle assembly lines still rely on high-force hydraulic presses and battery-pack lifting rigs. These stations require fluids with superior electrical insulation and thermal stability, prompting formulation innovation such as water-based and low-conduction esters. TotalEnergies recently debuted water-based lubricants aimed at EV cooling loops, underscoring how fluid suppliers are repositioning around new drivetrain architectures[2]TotalEnergies, “Launch of water-based lubricant for EV,” totalenergies.com . While steer-by-wire and brake-by-wire cut conventional automotive fluid volumes, incremental opportunities in EV battery production, giga-presses, and body-in-white operations offset volume losses.

Shift Toward Energy-Efficient Hydraulic Equipment in Manufacturing

Plant operators target lower total cost of ownership, so interest in low-traction, low-viscosity hydraulic fluids is rising. Laboratory testing shows torque losses fall by up to 30% when systems are filled with advanced, friction-optimized blends. U.S. Department of Energy efficiency standards for pumps and compressors amplify this shift by nudging OEMs and users to combine variable-speed drives with ultra-shear stability fluids. ISO 4413 design guidelines also highlight energy considerations, encouraging the adoption of fluids that cut internal leakage and heat generation.

Agricultural Mechanization Surge in Emerging Economies

India produced more than 1 million tractors in 2024 and now shows wheat mechanization at 69% and rice at 50%. Subsidy schemes like the Sub-Mission on Agricultural Mechanization reduce up-front equipment costs, accelerating fluid demand from pump, harvester, and planter hydraulics. OEMs such as Kubota are expanding in-house hydraulic component output to secure supply for precision farming machines, further enlarging the installed base that consumes biodegradable fluids acceptable for sensitive soil environments. Similar trends in Southeast Asia and Africa strengthen the growth outlook.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil price volatility | -0.7% | Global, greater effect in price-sensitive markets | Short term (≤ 2 years) |

| High cost and limited supply of bio and synthetics | -0.5% | Global, stronger in emerging economies | Medium term (2-4 years) |

| Rapid electrification of mobile machinery | -0.4% | Developed markets leading, gradual spread elsewhere | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Crude-Oil Prices Impacting Mineral-Oil Fluid Costs

Base-oil prices track crude swings. OPEC+ production adjustments ripple through Group II and Group III feedstocks, creating budgeting headaches for end users that rely on large hydraulic fluid inventories. Supply upsets caused by refinery outages or geopolitical tensions can rapidly squeeze margins for blenders who operate under fixed-price supply contracts. Because mineral oil accounts for nearly half of all liters sold, price spikes ripple across the hydraulic fluid market and may prompt short-term demand deferral.

High Cost and Limited Supply of Synthetic and Bio-Based Fluids

Vegetable-oil esters can cost up to three times more than mineral oils, primarily due to tight supply of high-oleic feedstocks and specialized additive packages. Storage stability remains a concern; lab data reveal oxidative degradation after prolonged warehousing, pushing users to shorter change intervals. Performance additives required for extreme-temperature service raise blending costs, limiting uptake to applications where spill risk or fire safety outweighs price sensitivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Base-Oil Type: Bio-Based Innovation Challenges Mineral Dominance

Mineral oils controlled 48.81% of the hydraulic fluid market in 2025, a position underpinned by favorable cost-performance ratios and broad OEM approvals. Bio-based products, while only mid-single-digit share, are forecast to register the quickest 5.03% CAGR as end users pursue sustainability certifications and regulators tighten spill-prevention rules. The hydraulic fluid market size for bio-based grades is expected to widen noticeably in agriculture and marine sectors as biodegradable features align with environmental mandates. Bio-ester oxidation risks once limited adoption, yet modern antioxidant packages now extend fluid life, as shown by Chevron’s Clarity Bio EliteSyn AW launch that uses a renewable synthetic base to tackle sludge formation. Synthetic esters remain entrenched in aerospace flight-control systems where phosphate-ester performance cannot be compromised.

Growth prospects differ across regions. Europe pushes maritime operators toward EU Ecolabel-approved fluids, propelling demand for FUCHS PLANTOHYD series that meets rapid biodegradability criteria. North America focuses on high-performance Group III blends aimed at energy savings. Asia-Pacific blends cost advantage with rising green requirements, so regional blenders balance mineral and vegetable-oil inputs to maintain competitiveness. Despite upward momentum, price differentials will slow wholesale substitution, ensuring mineral oil remains the volume backbone of the hydraulic fluid market through 2031.

By Application: Mobile Systems Drive Growth Despite Electrification

Mobile hydraulic systems held 54.76% of 2025 volume and are projected to climb at a 5.98% CAGR, reflecting brisk construction equipment turnover and an expanding fleet of mechanized farm machinery. In value terms, this segment commands premium margins because OEMs specify tighter cleanliness and oxidation standards to lengthen service intervals. The hydraulic fluid market size for mobile systems could surpass 1.35 billion liters by 2031 if replacement cycles in Asia’s rental fleets stay on course. Electro-hydraulic integration remains a key transition point; Caterpillar’s Cat 651 Scraper pairs electric control with high-pressure pumps, requiring fluids that resist micro-dieseling under dynamic load.

Stationary industrial systems exhibit slower unit growth but stable per-machine consumption. Factory automation, die-casting, and injection-molding machines depend on precise pressure control, so fluid suppliers promote zinc-free anti-wear chemistries to safeguard servo valves. Predictive maintenance projects use in-line sensors to monitor viscosity and contamination, enabling proactive top-ups and longer drains. Hybrid drive concepts may curb aggregate liters in some presses, yet high-force operations such as steel mills will continue to rely on fluid power. Overall, the application mix reinforces the critical role of hydraulics where electric motors alone cannot deliver comparable power density.

By End-User Industry: Heavy Equipment Dominance Faces Diversification

Heavy equipment, spanning earth-moving and mining fleets, contributed 38.26% of total liters in 2025. Large excavators, bulldozers, and dump trucks rely on multiple high-capacity circuits, so they remain the single largest consumer group in the hydraulic fluid market. OEM renewal programs emphasize low-viscosity fluids that can cut idle-time fuel burn and meet Tier 4 final emission rules. Concurrently, “Other End-Industries” such as food processing, marine, and renewable energy display the fastest 5.94% CAGR, underpinned by automation and stringent safety codes. The hydraulic fluid market share for these emerging segments is modest today, yet their double-digit adoption of biodegradable and H1 food-grade fluids lifts unit revenues.

Automotive factories represent a swing sector. Traditional platforms phase out hydro-boost steering and hydraulic brakes, but giga-press investments for EV bodies increase demand for heavy-duty hydraulic presses. Food and beverage plants swap mineral oils for NSF-H1 approved synthetic esters to eliminate contamination risks, opening niche premium opportunities. Rail and marine operators likewise shift toward specialized fire-resistant blends to comply with stricter environmental regulations in coastal zones. The expanding end-industry canvas illustrates how fluid suppliers diversify to insulate against cyclical swings in heavy equipment demand.

Geography Analysis

Asia-Pacific remained the epicenter of hydraulic fluid consumption, holding 40.75% of global volume in 2025 and maintaining the quickest 5.36% CAGR outlook. China’s leadership in construction machinery and India’s tractor boom underpin regional dominance. ExxonMobil reinforced its local supply chain by completing the Singapore Resid Upgrade Project in 2025, adding 20,000 barrels per day of EHC 340 MAX basestock that supports broader adoption of high-performance fluids. Kawasaki Heavy Industries doubled hydraulic component capacity in India to service domestic demand and reduce import reliance. Policy-driven infrastructure expansion paired with large-scale agricultural mechanization cements Asia-Pacific’s pre-eminence in the hydraulic fluid market.

North America remains technologically influential despite slower unit growth. The continent leads trials of sensor-integrated fluids that enable predictive analytics, and major blenders like Chevron are debuting renewable base oils to align with ESG targets. Manufacturing reshoring sparks incremental lubrication demand for machine tools and robotic cells, partially offsetting losses from electric-only light vehicles that use fewer hydraulic components. Canada’s co-hosting role at Hannover Messe 2025 spotlights cross-border initiatives around clean technologies requiring specialty fluids. Europe prioritizes environmental compliance, thus favoring biodegradable formulations in forestry, offshore, and civil-works projects. Germany’s advanced forging and die-casting hubs rely on premium zinc-free blends that withstand ultra-high pressures. France and Italy, both strong in aerospace, drive demand for fire-resistant phosphate-esters. Meanwhile, South America and the Middle East & Africa, though smaller today, show high upside as mining ventures accelerate and governments commit to road and rail corridors. Local supply chains remain underdeveloped, so imports dominate, making currency fluctuations a strategic concern for purchasers in these regions. Overall, geography-specific drivers add nuance to the global hydraulic fluid market growth narrative, yet the common denominator across continents is the indispensable role of fluid power in heavy-duty tasks.

Competitive Landscape

The hydraulic fluids market exhibits moderate fragmentation. BP’s recent strategic review of its Castrol business hints at portfolio realignment that could reshape competitive dynamics. ExxonMobil, Chevron, and TotalEnergies round out the top tier by coupling base-oil self-sufficiency with co-engineered OEM approvals, while regional champions such as FUCHS, Sinopec, and CNPC focus on localized blends that match specific climate and duty-cycle conditions.

Product differentiation gravitates toward sustainability and performance. TotalEnergies’ water-based lubricant for EV cooling loops stands out as a radical chemistry pivot addressing electrical conductivity limits in next-generation factories. FUCHS advances its PLANTOHYD biodegradable range to satisfy stricter European spill regulations. Digitalization provides a secondary competitive lever: suppliers embed condition-monitoring sensors into fill ports, bundling data dashboards with fluid contracts to lock in customer loyalty. Such service-based models raise switching costs and blur the line between product and after-sales analytics.

Hydraulic Fluid Industry Leaders

Chevron Corporation

Exxon Mobil Corporation

BP p.l.c

Shell plc

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: TotalEnergies Lubrifiants acquired fire-resistant hydraulic fluid product lines from the German niche manufacturer, Fluid Competence. This acquisition bolsters TotalEnergies' sustainability objectives, enhancing its portfolio with a mineral oil-free fluid.

- September 2024: Chevron has unveiled Clarity Bio EliteSyn AW, a cutting-edge hydraulic fluid tailored for the marine and construction sectors, underscoring the company's commitment to environmental stewardship.

Global Hydraulic Fluid Market Report Scope

Hydraulic fluids are commonly made of mineral oil and water. They act as a medium for transmitting power in hydraulic machinery. Some of the properties of hydraulic fluids include wear resistance, thermal stability, viscosity, compressibility, and oxidation stability.

The market is segmented on the basis of end-user industry and geography. By end-user industry, the market is segmented into automotive, other transportation, heavy equipment, food and beverage, and other end-user industries. The report also covers the market size and forecasts for the hydraulic fluid market in 15 countries around the world. For each segment, the market sizing and forecasts are done on the basis of volume (liters).

| Mineral Oil |

| Synthetic Oil |

| Semi-Synthetic Oil |

| Bio-based Oil |

| Fire-Resistant (Phosphate-ester, Water-glycol) |

| Mobile Hydraulic Systems |

| Industrial/Stationary Hydraulic Systems |

| Automotive |

| Other Transportation |

| Heavy Equipment |

| Food and Beverage |

| Other End-user Industries (Construction, Power Generation and Utilities, Agriculture, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Base-Oil Type | Mineral Oil | |

| Synthetic Oil | ||

| Semi-Synthetic Oil | ||

| Bio-based Oil | ||

| Fire-Resistant (Phosphate-ester, Water-glycol) | ||

| By Application | Mobile Hydraulic Systems | |

| Industrial/Stationary Hydraulic Systems | ||

| By End-user Industry | Automotive | |

| Other Transportation | ||

| Heavy Equipment | ||

| Food and Beverage | ||

| Other End-user Industries (Construction, Power Generation and Utilities, Agriculture, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Hydraulic Fluid Market?

The Hydraulic Fluid Market size is expected to reach 1.84 billion liters in 2026 and grow at a CAGR of 4.32% to reach 2.27 billion liters by 2031.

What is the current Hydraulic Fluid Market size?

In 2026, the Hydraulic Fluid Market size is expected to reach 1.84 billion liters.

How is machinery electrification influencing hydraulic fluid consumption?

Electrification trims fluid volumes in some mobile equipment, yet high-force tasks still require hydraulics, keeping demand resilient.

Which is the fastest growing region in Hydraulic Fluid Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Page last updated on: