Deicing Fluid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 2.83 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

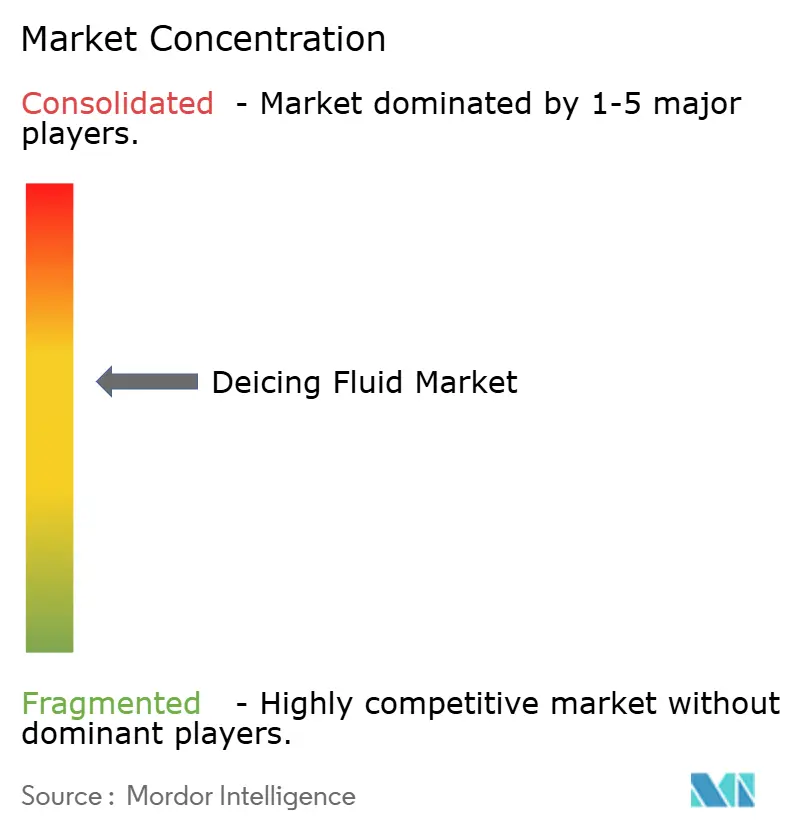

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Deicing Fluid Market Analysis by Mordor Intelligence

The Deicing Fluid Market size is expected to grow from USD 2.16 billion in 2025 to USD 2.26 billion in 2026 and is forecast to reach USD 2.83 billion by 2031 at 4.63% CAGR over 2026-2031. Cold-region airport expansions in Asia, stricter FAA and ICAO runoff caps, and the phased commercialization of Arctic shipping lanes are reinforcing year-round demand for propylene glycol and potassium acetate formulations. North America dominates consumption because of FAA Engineering Brief 108 compliance, while Asia-Pacific provides the fastest incremental lift as India, Japan, and China add high-altitude infrastructure. Suppliers that control bio-based feedstock and bundle modular glycol-recovery systems with fluid contracts are best placed to capture margin upside as environmental mandates drive premium pricing.

Key Report Takeaways

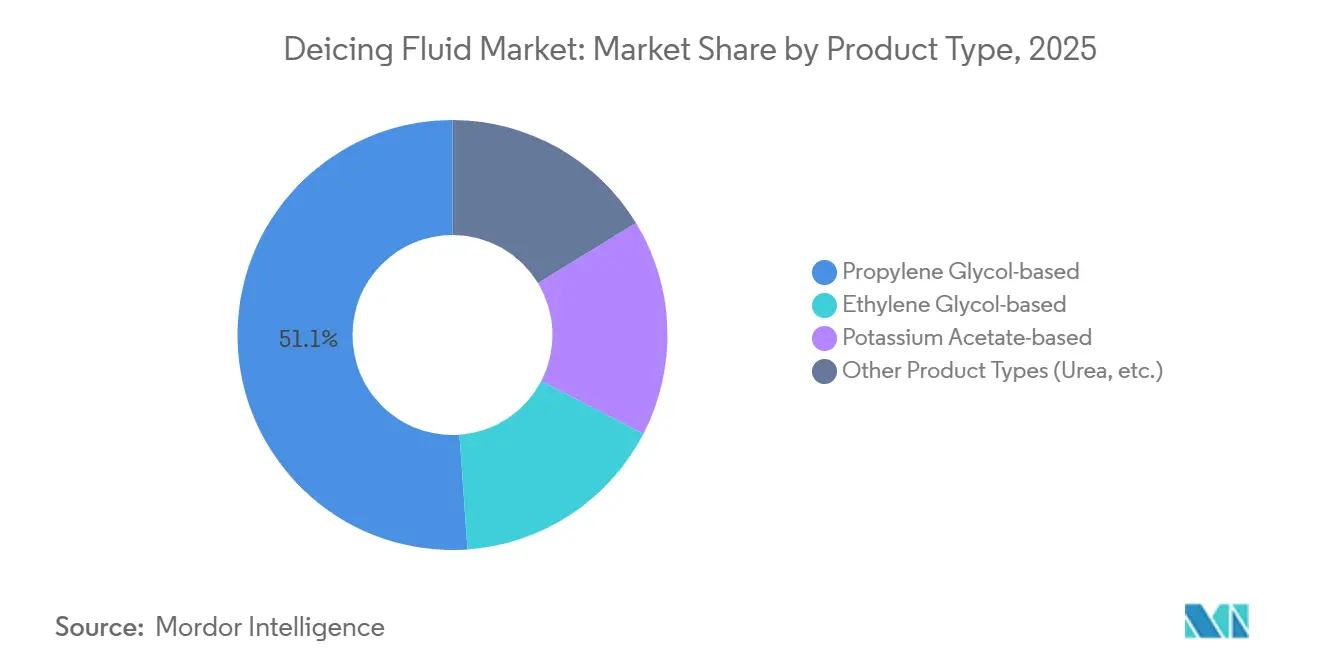

- By product type, propylene glycol-based led with 51.11% of the deicing fluid market share in 2025; potassium acetate-based is forecast to expand at a 5.15% CAGR through 2031.

- By fluid type, Type I accounted for 40.11% of the deicing fluid market share in 2025, while Type IV is advancing at a 5.55% CAGR through 2031.

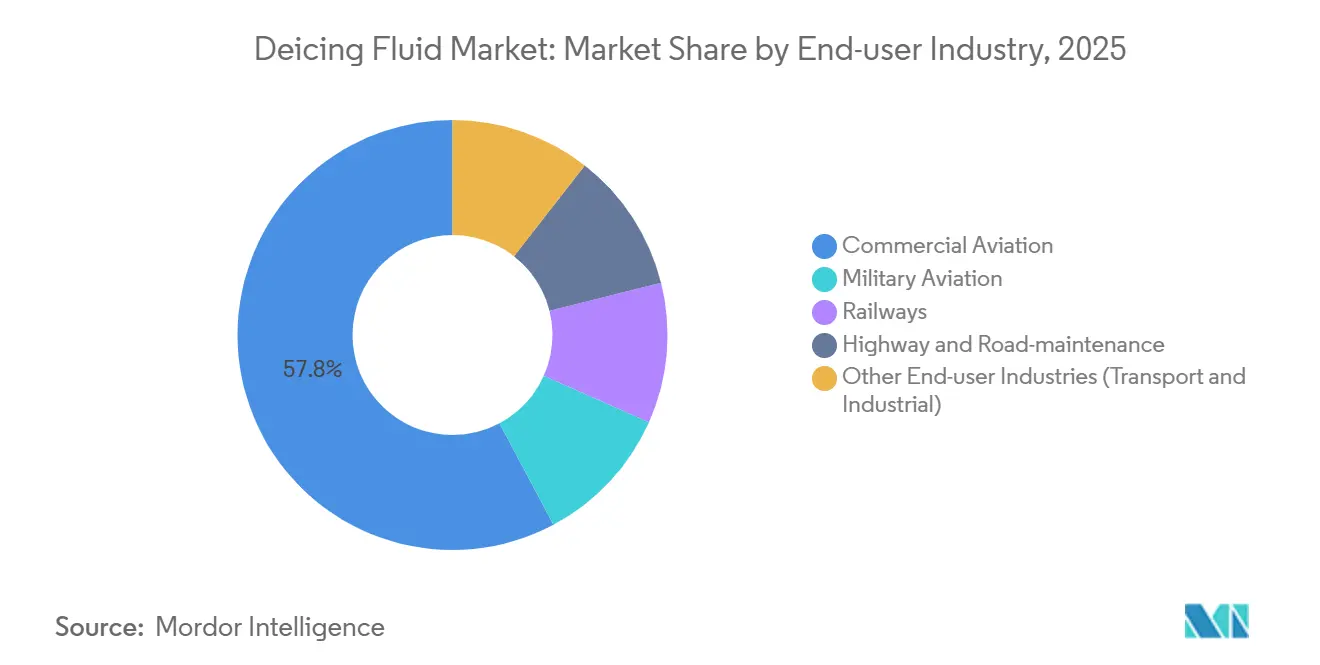

- By end-user industry, commercial aviation held 57.78% of the deicing fluid market share in 2025, whereas military aviation is forecast to expand at a 5.87% CAGR through 2031.

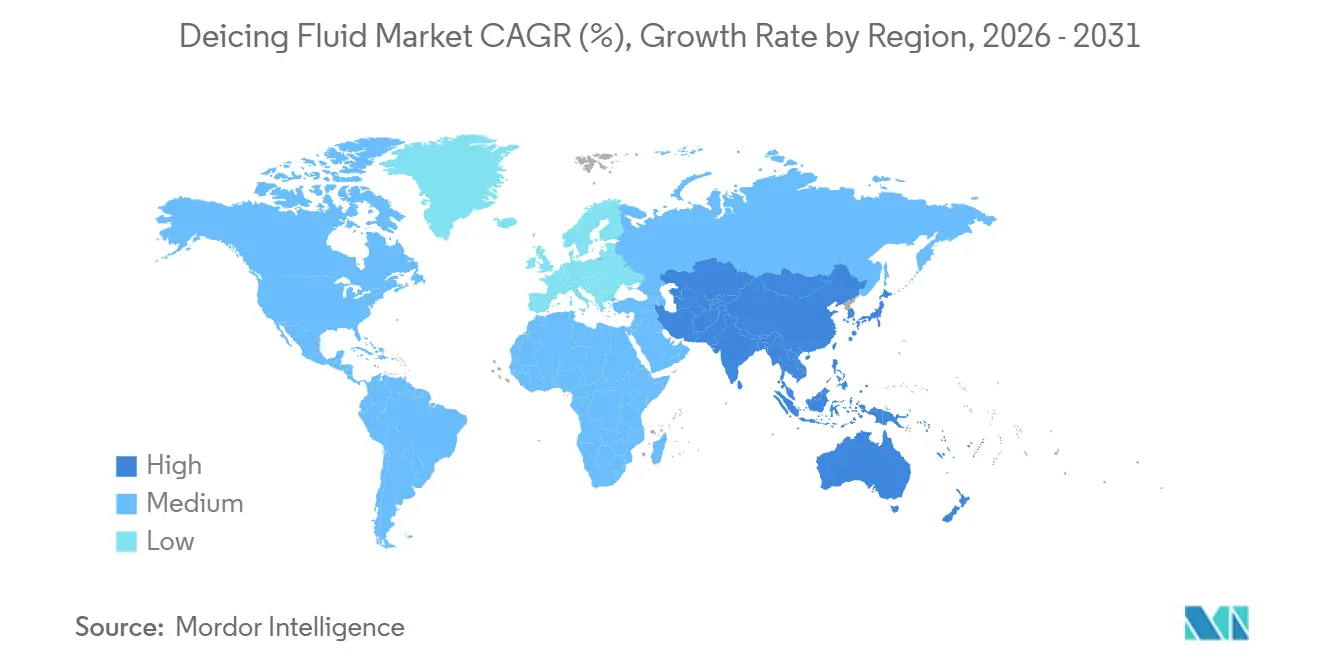

- By geography, North America commanded a 35.46% of the deicing fluid market share in 2025, while Asia-Pacific is set to post a 5.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Deicing Fluid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-region airport and rail expansion in Asia | +1.2% | Asia-Pacific core (India, Japan, China), spill-over to ASEAN highlands | Medium term (2–4 years) |

| Stricter ICAO and FAA glycol run-off caps | +0.9% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Transition to potassium-acetate for PFAS-free compliance | +0.8% | Europe primary, North America secondary | Medium term (2–4 years) |

| Arctic shipping route commercialization | +0.5% | Arctic coastal airports (Russia, Norway, Canada, Alaska) | Long term (≥ 4 years) |

| On-wing electro-thermal anti-ice lowering fluid dosage | +0.3% | Global, early adoption in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cold-Region Airport and Rail Expansion in Asia

India’s Nyoma airbase upgrade and Japan’s runway extension at Okadama exemplify how high-altitude facilities are lengthening winter operations and enlarging the deicing fluid market[1]Ministry of Defense India, “Nyoma Airbase Upgrade,” mod.gov.in. Rail networks from Poland to Japan mirror aviation’s shift from reactive snow removal toward scheduled anti-icing, using propylene-glycol sprays that cut energy costs and delays. Larger regional jets operating into secondary airports demand Type I removal followed by Type IV protection, increasing two-step cycles per turn. Freight corridors built for cold-chain fresh produce in northern India are adding switch-point heaters pre-wetted with glycol blends, expanding cross-modal consumption. Collectively, these projects embed multi-year fluid baseloads outside traditional North American and European hubs.

Stricter ICAO and FAA Glycol Run-Off Caps

FAA Engineering Brief 108 and EPA effluent standards oblige even mid-size Part 139 airports to capture or reclaim spent glycol, driving closed-loop investment that stabilizes annual liftings despite price volatility. Montreal Trudeau’s 99.5%-pure distillation model lowered purchase costs 30% and is now replicated at Syracuse and Columbia Regional, creating predictable take-or-pay contracts with formulators. Tighter biochemical-oxygen-demand limits reduce urea and chloride use, pushing operators toward SAE-compliant propylene-glycol fluids with documented biodegradability. As compliance audits tighten, demand shifts from price-led tenders to multi-year supply agreements bundled with recovery technology support.

Transition to Potassium Acetate for PFAS-Free Compliance

ECHA’s impending blanket PFAS ban has accelerated trials of potassium-acetate fluids that eliminate trace fluorinated surfactants[2]European Chemicals Agency, “PFAS Restriction Proposal,” echa.europa.eu. European hubs already require supplier certification, setting a procurement precedent expected in North America by 2028. Although acetate shows higher aquatic toxicity than chloride, pre-wetting hybrids can discharge loads while delivering holdover performance. Suppliers are reformulating to meet the June 2025 SAE AMS biodegradability thresholds, which boosts demand for premium acetate concentrates in the deicing fluid market.

Arctic Shipping Route Commercialization

Year-round cargo growth along the Northern Sea Route is forcing coastal airports from Tromsø to Deadhorse to stockpile extra Type I inventories for feeder flights that operate in -35 °C conditions. Fixed deicing stations with underground containment are now standard in permafrost zones, adding capital depth that locks in fluid offtake. As Arctic tonnage heads for 100 million tons by 2030, seasonal demand spikes will become structural, lifting baseline revenues of the deicing fluid market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising glycol reclamation and storm-water costs | -0.7% | North America and Europe (high-throughput hubs) | Short term (≤ 2 years) |

| Pending EU-wide PFAS restrictions disrupting legacy blends | -0.5% | Europe primary, spillover to North America | Medium term (2–4 years) |

| Volatility in bio-based feedstock supply | -0.4% | Global, concentrated in Europe and North America bio-based adopters | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Glycol Reclamation and Storm-Water Costs

Vilokan-technology plants cost USD 19.3 million at Syracuse and more than USD 1.5 million in annual opex at Minneapolis-St. Paul is elevating the lifecycle cost of every reclaimed gallon. Smaller airports face per-event capital costs above USD 20,000, squeezing budgets and slowing adoption in low-traffic regions. Municipal wastewater surcharges for excess biochemical demand raise the fully loaded price per gallon, nudging buyers to negotiate bundled supply-and-recovery contracts that temper the deicing fluid market growth rate.

Pending EU-Wide PFAS Restrictions Disrupting Legacy Blends

Testing every batch for sub-25 ppm fluorinated additives adds USD 500-800 per 1,000 liters, while dual inventories for EU and non-EU customers tie up more working capital. Airports with stockpiled legacy ethylene-glycol fluids must either dispose of them or fund reformulation before the projected Q4 2026 transition, creating temporary shortages that unsettle scheduling. Although compliant products command a sustainability premium, the switchover introduces operational friction that weighs on the deicing fluid market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Propylene Glycol Anchors, Potassium Acetate Accelerates

The propylene glycol-based segment held 51.11% of the deicing fluid market share in 2025. Stable demand reflects universal Type I and Type IV compatibility, plus recycling economics that recover 30-40% of spent fluid. LyondellBasell’s Texas expansion adds 400,000 metric tonnes per annum of propylene, buffering oxide feedstock volatility and fortifying supply security. Ethylene glycol is losing favor as the U.S. Air Force enforces propylene-only specifications, but retains a niche at Russian and Chinese hubs with temperatures below -50 °C.

The potassium acetate-based segment is growing at a 5.15% CAGR through 2031. Demand is concentrated in Europe, where PFAS bans accelerate switch-overs, and among U.S. state DOTs blending acetate with chloride to cut freeze points without breaching BOD limits. Cost premiums of USD 1,100-1,800 tons dampen highway penetration, yet airports value holdover reliability and PFAS-free status. Suppliers that master cost-effective hybrid acetate-glycol blends stand to widen margins across the deicing fluid market.

By Fluid Type: Type IV Gains on Holdover-Time Demands

Type I commanded 40.11% of 2025 sales. One-step heated removal keeps them indispensable for quick turnarounds, especially at regional carriers with 20-minute gate windows. Type IV is projected to outpace peers at a 5.55% CAGR through 2031. The June 2025 SAE AMS1428M update extended holdover tables, letting aircraft depart up to 90 minutes after application under defined weather bands, a key advantage during taxi queues at JFK or Heathrow.

Combined Type II/III faces consolidation as airlines migrate to a simplified Type I plus Type IV pairing that eases training and inventory. Nordic operators illustrate the pivot: more than 65% of Aviator Airport Alliance’s fleet handles two-step protocols, and recycled Type IV with 30% reclaimed PG passed Finavia’s holdover verification. Investments in pseudoplastic rheology testing laboratories give top formulators a moat, ensuring rapid qualification when specifications tighten further and cementing their role in the deicing fluid market.

By End-user Industry: Military Aviation Outpaces Commercial Aviation

Commercial aviation drew 57.78% of 2025 global revenue as load factors hit record highs and aging narrow-bodies required additional cycles. Airlines squeezed by USD 11 billion of supply-chain costs retained legacy aircraft longer, deepening fuel consumption. However, military aviation will climb faster, at a 5.87% CAGR through 2031, as NATO training in Norway and U.S. Arctic strategies raise sortie counts that each need full Type I applications at -30 °C.

Railways, telecom towers, and wind turbines contribute a small but quickening baseline. Chicago Transit Authority trials of glycol-based switch sprays trimmed weather delays by up to 80% last winter, signaling how urban transit can diversify the deicing fluid market. Road-maintenance agencies apply acetate only on bridge decks where chloride-induced rebar corrosion is costly, keeping highway revenues modest. End-user expansion beyond airports, however, cushions volatility from any single sector and broadens the deicing fluid market opportunity set.

Geography Analysis

North America generated 35.46% of 2025 revenue, bolstered by FAA runoff rules and 90%+ deicing rates at hubs from Minneapolis to Toronto. Syracuse’s USD 19.3 million reclamation plant and Columbia’s FAA-funded system illustrate the capital commitment underpinning steady liftings. Canada’s Pearson Airport fielded hybrid-electric deicers that cut diesel by 40%, yet depend on high-purity fluids reclaimed on-site, reinforcing closed-loop sourcing across the deicing fluid market.

Asia-Pacific will grow at a 5.78% CAGR through 2031, led by India’s expansion in Ladakh and Japan’s new dedicated apron at New Chitose. ANA’s color-coded fluids improve pre-flight coverage checks, standardizing two-step operations across five major airports. Korean operators import propylene glycol from Singapore and China, exposing them to shipping spikes but securing a reliable supply. High-elevation ASEAN airports use Type I sporadically, but limited local inventory necessitates costly airfreight, nudging carriers to pool regional stockpiles as the deicing fluid market deepens.

Europe will pivot quickly once PFAS restrictions crystallize. Clariant’s Swedish recycled-glycol expansion and Finavia’s closed-loop model underscore the circular-economy ethos that now shapes procurement. Russia’s Sheremetyevo, with 1,000 m³ of storage and 40 specialized vehicles, remains glycol-heavy owing to sub-Arctic winters, while Nordic airports log the world’s highest per-capita fluid use. Electrification of ground assets is complicated by battery performance below -20 °C, creating supplemental demand for heated garages and embedded power systems that indirectly raise deicing fluid market throughput.

Competitive Landscape

The market exhibits moderate concentration. Vertically integrated majors like LyondellBasell anchor feedstock security with propylene expansions that buffer cost swings. Clariant differentiates on sustainability, embedding recycled mono-propylene glycol in SAFEWING Type I with a 25% lower carbon footprint. Airports are bundling fluid orders with modular reclamation units; Columbia Regional reached payback in under ten years through BOD credits, signaling a template for sub-500-event hubs.

Bio-based challengers aggregate glycerin that bypasses conventional propylene-oxide crackers. Argent Energy’s Amsterdam plant trims emissions but wrestles with biodiesel mandate variability that causes feedstock gluts or shortages. Niche formulators lacking in-house labs struggle to re-qualify under new SAE toxicity thresholds, pushing them toward licensing or outright sale to larger peers. Long lead-times for electro-thermal anti-ice systems give chemical suppliers a multi-year runway to refine low-viscosity Type IV blends optimized for hybrid wings. Players able to wrap fluids, testing, and recovery into turnkey deals will secure the stickiest margins through the forecast horizon.

Deicing Fluid Industry Leaders

Clariant

Dow

General Atomics (Cryotech)

Kilfrost Ltd.

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Researchers in the UK developed new deicing fluids that utilized supramolecular polymers to prevent ice formation on aircraft wings for more than twice the duration of existing products. The team incorporated derivatives of a gelling agent, 1,3:2,4-dibenzylidene sorbitol (DBS), into current deicing fluids composed of a 50:50 mixture of water and propylene glycol, along with other additives.

- November 2024: Clariant expanded its storage capacity in Scandinavia to support recycled mono propylene glycol (MPG), an essential component in aircraft deicing fluids. The company installed two new storage tanks and a truck unloading station at its Uddevalla facility in Sweden.

Global Deicing Fluid Market Report Scope

Deicing fluid is a chemical mixture, commonly composed of propylene glycol or ethylene glycol, designed to remove ice, snow, and frost from surfaces such as aircraft wings, vehicles, and runways by reducing the freezing point of water. It incorporates corrosion inhibitors and surfactants to enhance safety by preventing ice accumulation that could interfere with aircraft lift.

The Deicing Fluid Market is segmented into product type, fluid type, end-user industry, and geography. By product type, the market is segmented into propylene glycol-based, ethylene glycol-based, potassium acetate-based, and other product types (e.g., urea). By fluid type, the market is segmented into type I, type II, type III, and type IV. By end-user industry, the market is segmented into commercial aviation, military aviation, railways, highway and road maintenance, and other end-user industries (e.g., transport and industrial). The report also covers the market size and forecasts for deicing fluid in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Propylene Glycol-based |

| Ethylene Glycol-based |

| Potassium Acetate-based |

| Other Product Types (Urea, etc.) |

| Type I |

| Type II |

| Type III |

| Type IV |

| Commercial Aviation |

| Military Aviation |

| Railways |

| Highway and Road-maintenance |

| Other End-user Industries (Transport and Industrial) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Propylene Glycol-based | |

| Ethylene Glycol-based | ||

| Potassium Acetate-based | ||

| Other Product Types (Urea, etc.) | ||

| By Fluid Type | Type I | |

| Type II | ||

| Type III | ||

| Type IV | ||

| By End-user Industry | Commercial Aviation | |

| Military Aviation | ||

| Railways | ||

| Highway and Road-maintenance | ||

| Other End-user Industries (Transport and Industrial) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the deicing fluid market?

The deicing fluid market stands at USD 2.26 billion in 2026 and is forecast to reach USD 2.83 billion by 2031.

Which product type is gaining share fastest through 2031?

Potassium acetate-based is projected to grow at a 5.15% CAGR through 2031, because of PFAS-free compliance.

Why is Type IV demand accelerating through 2031?

The 2025 SAE AMS1428M revision lengthened holdover times for Type IV, giving airlines more departure flexibility and driving a 5.55% CAGR through 2031.

Which region offers the strongest growth potential through 2031?

Asia-Pacific is expected to post a 5.78% CAGR through 2031, fueled by new high-altitude airports in India and expanded winter operations in Japan.

Page last updated on: