Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.21 Billion |

| Market Size (2031) | USD 14.71 Billion |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermic Fluid Market Analysis by Mordor Intelligence

The Thermic Fluid Market size was valued at USD 11.76 billion in 2025 and estimated to grow from USD 12.21 billion in 2026 to reach USD 14.71 billion by 2031, at a CAGR of 3.79% during the forecast period (2026-2031). Medium-temperature applications (150-300 °C) continue to anchor demand by serving diverse industries, while high-temperature uses (greater than 300 °C) record the briskest 4.84% CAGR as concentrated solar power (CSP) and advanced chemical processing scale up. Asia-Pacific retains leadership through robust refining throughput, new petrochemical complexes and accelerating renewable projects. Mineral oils still command the largest slice, yet synthetics and glycols gain rapid traction where regulatory pressure, safety needs and energy efficiency outweigh cost. Integrated oil majors and specialty chemical firms expand capacity, pursue acquisitions and release differentiated fluids that answer data-center, food-grade and CSP specifications. Supply-chain resilience programs and stricter emissions standards reshape sourcing strategies, but the thermic fluids market continues to diversify, limiting exposure to cyclical downturns in legacy oil and gas.

Key Report Takeaways

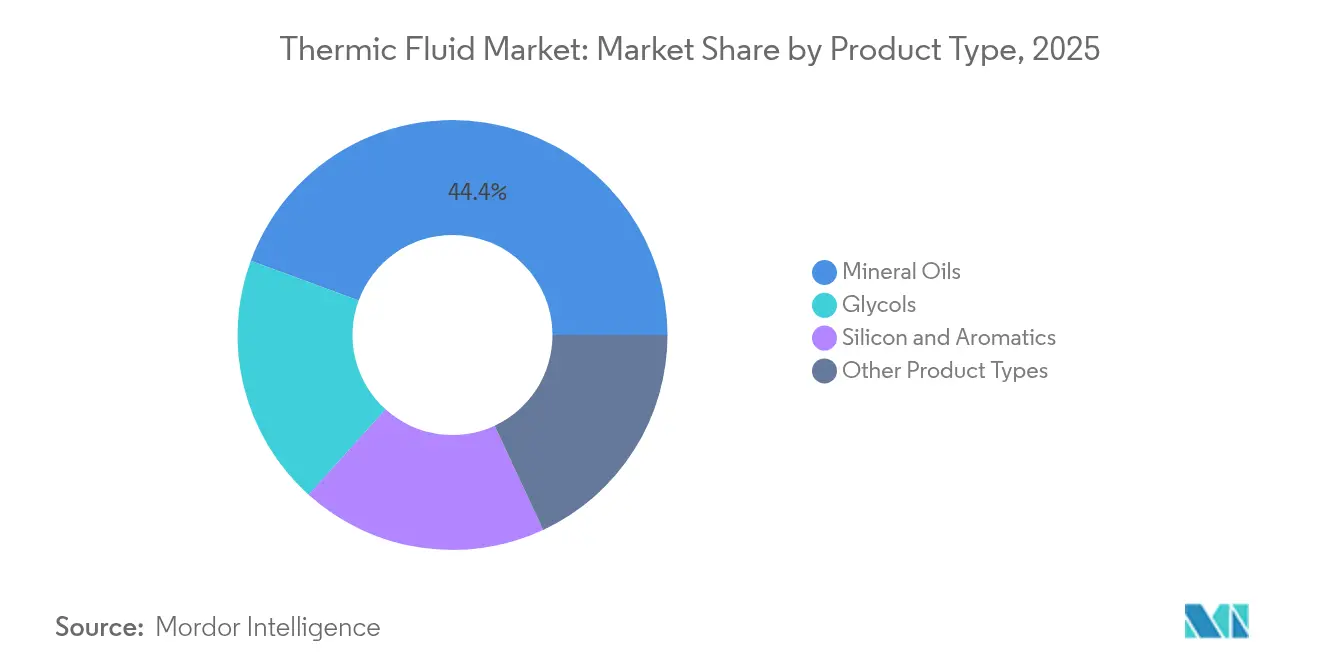

- By product type, mineral oils held 44.38% share of the thermic fluids market size in 2025; glycols are forecast to post the fastest 4.05% CAGR through 2031.

- By temperature range, medium-temperature applications captured 51.88% of the thermic fluids market share in 2025. High-temperature applications are projected to advance at a 4.67% CAGR to 2031.

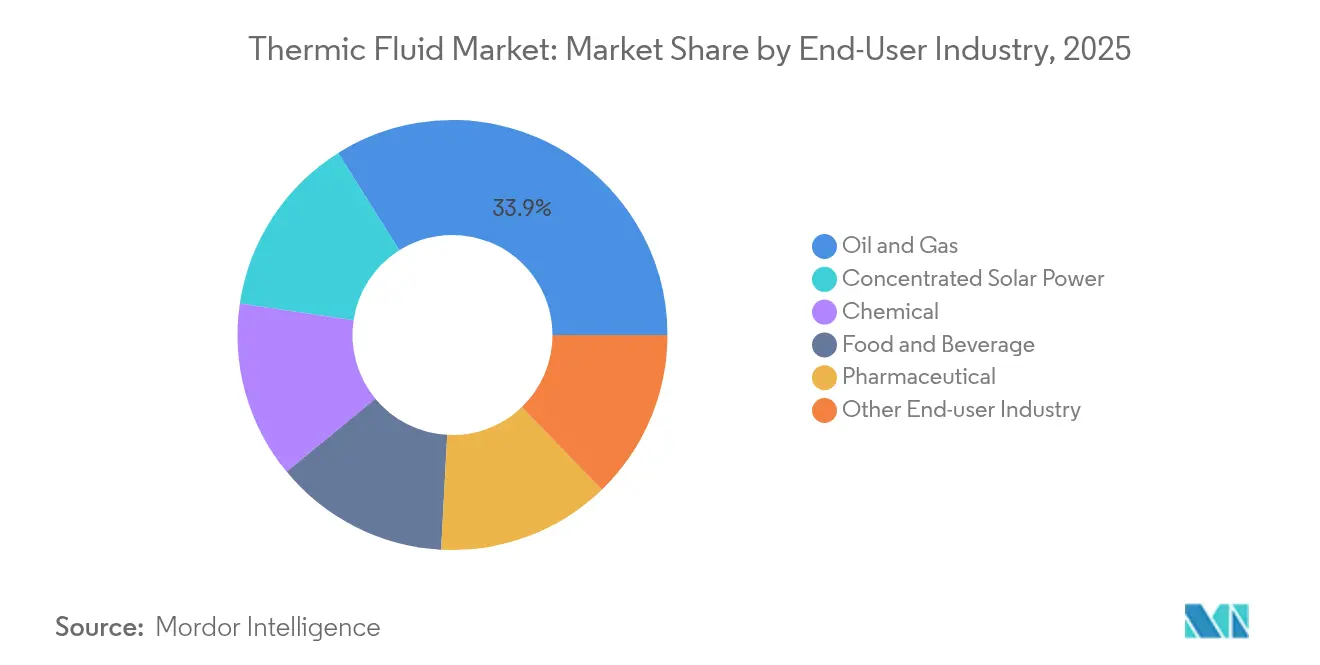

- By end-user industry, oil and gas accounted for 33.92% of the thermic fluids market size in 2025; concentrated solar power is set to grow at a 5.05% CAGR between 2026-2031.

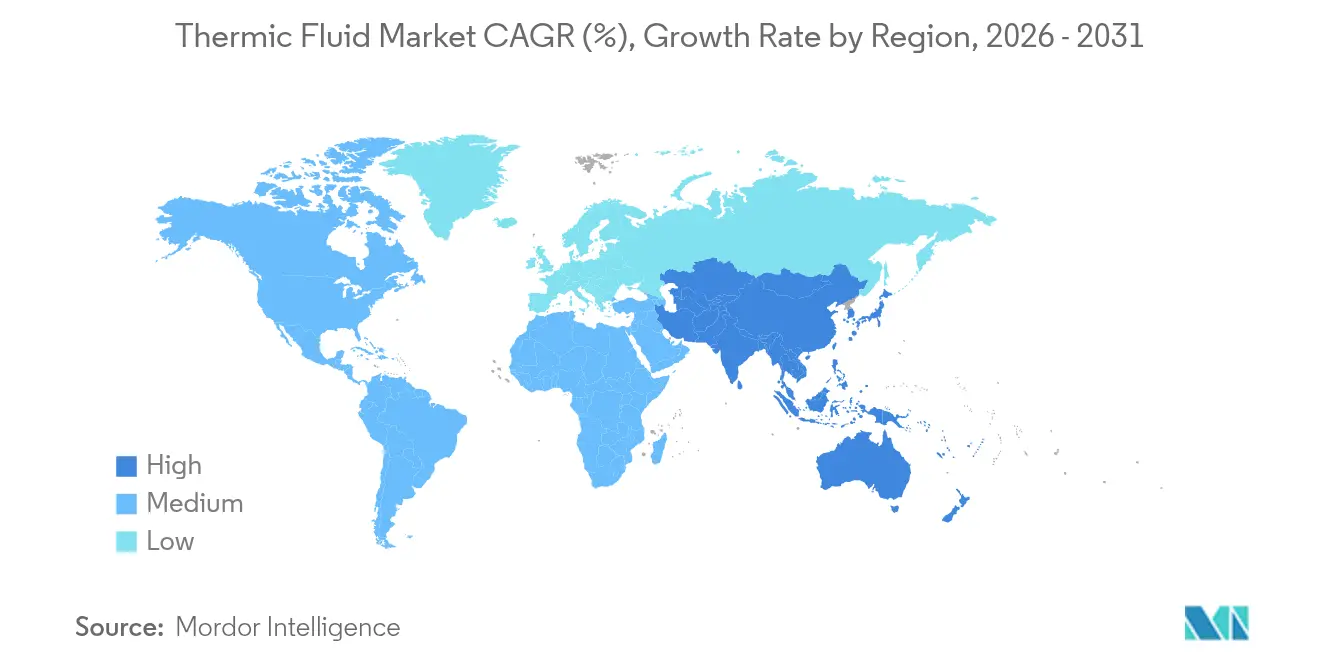

- By geography, Asia-Pacific led with a 37.40% thermic fluids market share in 2025 and is expanding at a 4.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermic Fluid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extensive demand from oil & gas | +1.20% | Global, with concentration in North America, Middle East, and Asia-Pacific | Medium term (2-4 years) |

| Growing adoption in concentrated solar power | +0.80% | Global, with early gains in India, Algeria, and southwestern United States | Long term (≥ 4 years) |

| Expansion in chemical & petrochemical processing | +0.90% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Food-grade formulations gain traction | +0.40% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Data-center immersion cooling uptake | +0.60% | Global, with concentration in North America, Europe, and Asia-Pacific tech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Extensive demand from oil & gas

Heat-transfer duties in modern refineries have grown more complex as operators chase higher conversion rates and lower emissions. China’s throughput of 14.8 million bpd in 2023 illustrates sustained appetite for high-temperature synthetic fluids capable of stable service beyond 380 °C. ExxonMobil’s Singapore resid-upgrade project, due in 2025, will add 20,000 bpd of base stocks tuned for premium thermic fluids, targeting stringent Asian specifications. EPA Subpart OOOOb, enforced from May 2024, mandates zero-emission pneumatic equipment, nudging operators toward low-volatility, longer-life formulations that curb fugitive leaks. These shifts reinforce a two-tier market where synthetic blends command premium pricing while mineral oils retain price-sensitive niches.

Growing adoption in concentrated solar power

CSP plants see thermic fluids as a core storage medium enabling 24-hour renewable power. India’s 500 GW non-fossil goal underlines this outlook, and long-duration storage via molten salt or advanced silicone fluids is now integral to project economics. Laboratory work shows platinum-nanoparticle silicone fluids boosting plant efficiency by 44% at 425 °C without the toxicity concerns linked to legacy aromatics. Algeria’s CSP tower plants record levelized costs of USD 0.097/kWh, validating commercial feasibility and driving demand for high-temperature, low-degradation fluids. Thermal energy storage capacity is forecast to triple this decade, widening the downstream pull on innovative heat-transfer media[1]IRENA, “Innovation Outlook: Thermal Energy Storage,” irena.org .

Expansion in chemical & petrochemical processing

Regionalized supply chains and specialty-chemical focus demand tighter temperature control and cleaner operations. BASF’s USD 10 billion Zhanjiang complex, operational from late 2025, relies on renewable electricity and circular feedstocks, creating a premium for environmentally compatible fluids able to cycle between diverse reactors and exchangers. Chevron Oronite’s Ningbo expansion, finishing in 2026, mirrors the push to locate additive production near Asian OEMs while meeting strict purity standards. Specialty-chemical output favors synthetic fluids with wider thermal windows and lower vapor pressure, driving substitution away from commodity mineral oils.

Food-grade formulations gain traction

In food and pharmaceutical processes, incidental-contact rules supersede cost concerns. NSF HT-1 certification has become non-negotiable, prompting suppliers like Caldera to release purified white-oil blends for bakery ovens and extruders. Eastman’s Therminol XP offers FDA-compliant purity and stable operation to 315 °C, bridging the gap between mineral and synthetic options in edible-oil frying and aseptic packaging. Pharmaceutical plants adopt the same fluids for -115 °C lyophilization to 230 °C reaction steps, enlarging the customer base. Competitive advantage hinges on documented traceability and rapid supply as global processors internalize hygiene and energy mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw material pricing | -0.70% | Global, with acute impact in Asia-Pacific manufacturing centers | Short term (≤ 2 years) |

| Safety & environmental concerns over aromatics | -0.50% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Strict VOC regulations on mineral oils | -0.30% | North America and Europe, with emerging impact in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile raw material pricing

Rapid capacity additions outpaced demand after 2022, squeezing petrochemical margins and swinging base-oil prices. Clean-tech spending topping USD 2.8 trillion diverts naphtha feedstocks toward polymers for batteries and solar panels, tightening supply for thermic fluid producers. Caustic-soda shortages complicate de-acidification steps critical to fluid stability. Firms hedge exposure through vertical integration—Chevron’s pursuit of Phillips 66’s chemical stake exemplifies efforts to secure in-house feed—notwithstanding steep capital commitments.

Safety & environmental concerns over aromatics

EU REACH amendments effective September 2025 expand bans on CMR aromatics, forcing reformulation away from legacy heat-transfer blends. California’s PFAS rule AB 347 will require manufacturer registration by 2029, signaling broader scrutiny of fluorinated additives. OSHA’s July 2024 Hazard Communication update pushes clearer labeling, increasing compliance overhead[2]OSHA, “Hazard Communication Standard; Final Rule,” osha.gov . Eastman’s Therminol FF synthetic flush with higher flash point addresses aromatics-phaseout needs while ensuring system cleanliness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Synthetics challenge mineral-oil dominance

Mineral oils remained the volume leader with 44.38% share in 2025, yet tightening VOC caps shrink their cost edge. Glycols, propelled by food-grade and server-farm demand, are growing 4.05% CAGR, narrowing the gap with hydrocarbons. Eastman’s Therminol FF and Dow’s SYLTHERM silicone line evidence a shift toward broad-temperature synthetics able to run from -40 °C to 400 °C, lengthening service life and boosting uptime. Nanoparticle-infused silicone prototypes raise conductivity by 24% at 200 °C, underscoring how R&D differentiates suppliers. As a result, the thermic fluids market sees larger customers specify synthetic alternatives during turnaround cycles, even when upfront prices rise.

Premium synthetics widen addressable niches in CSP, specialty chemicals and immersion cooling. Silicon and aromatic blends occupy high-temperature or narrow-boiling-range duties where mineral oils break down. New categories, such as platinum-doped silicone oils for 425 °C service, illustrate rapid progress.

By Temperature Range: High-temperature applications drive innovation

Medium-temperature systems supplied 51.88% of the thermic fluids market size in 2025, reflecting adoption across fryers, press-lines and batch reactors. Mineral-oil incumbency keeps cost low, maintaining preference where duty cycles and regulations permit. Conversely, greater than 300 °C loops exhibit the fastest 4.67% CAGR as CSP towers, residue hydrocrackers and high-severity polymer units proliferate. Eastman’s Therminol VP-1 operates vapor-phase to 400 °C, showing how synthetics displace costly molten salts in moderate ranges.

Research into polydimethylsiloxane carriers proves viability at 425 °C with lower toxicity, pointing to future crossover into industrial furnaces. The low-temperature less than 150 °C niche stays small but essential for pharma freeze-drying and environmental test chambers. Suppliers bundle glycol-water premixes with corrosion inhibitors to address condensation and biological fouling. Each cluster sharpens the segmentation of the thermic fluids market, fostering specialized supply contracts that mitigate commoditization.

By End-User Industry: Energy transition reshapes demand

Oil and gas processes held 33.92% thermic fluids market share in 2025, notching replacement-driven volume but muted growth as refineries streamline energy intensity. CSP plants gain fastest at 5.05% CAGR, helped by policy targets and grid-storage economics that favor molten-salt or silicone thermal reservoirs. Chemical complexes sustain mid-single-digit growth tied to specialty chemical output, whereas food and beverage processors lift demand for NSF-certified fluids.

Data centers, though classified within industrial utilities, constitute an emergent vector as immersion cooling adoption rises from 10% in 2024 toward 20% in 2025. Chemours’ partnership with Navin Fluorine to produce two-phase liquids from 2026 underlines cross-industry talent sharing. Taken together, newer verticals fragment demand and lessen reliance on fossil-fuel cycles, supporting balanced expansion of the thermic fluids market.

Geography Analysis

Asia-Pacific owned 37.40% thermic fluids market share in 2025 and is advancing at a 4.42% CAGR through 2031, underpinned by China’s 14.8 million bpd crude runs, BASF’s Zhanjiang megasite and India’s CSP rollout. Policy incentives and local supply chains reinforce regional sales, although reshoring trends encourage multi-country diversification.

North America and Europe rely on technology leadership and tight regulations to pull in higher-margin synthetics. EPA methane rules and EU REACH updates accelerate substitution away from aromatic mineral oils. ExxonMobil’s Singapore base-stock addition illustrates North American firms manufacturing in Asia yet retaining IP dominance.

South America, Middle East and Africa present emerging possibilities as energy infrastructure scales. Algeria’s CSP economics validate demand for 400 °C fluids, while Gulf refiners invest in residue conversion that needs stable heat carriers. Political risk and logistics gaps temper uptake, but governmental supply-chain resilience programs, such as Australia’s critical-minerals initiative, highlight a pivot toward diversified sourcing.

Competitive Landscape

The competitive field is moderately fragmented. BASF, Eastman and Dow maintain global networks and invest heavily in R&D; BASF earmarked USD 19.5 billion for 2024-2027 projects to protect share. ExxonMobil and Chevron deploy integration advantages, with the Singapore resid project and the bid for Phillips 66’s chemical arm showcasing feedstock control. Mid-tier players launch niche solutions: Castrol’s PG 25 for direct-to-chip loops and Sulzer’s molten-salt thermal storage partnership diversify product scopes.

Technology and compliance rather than raw price dictate differentiation. Eastman’s flush fluid introduces a new maintenance category, while Dow’s tie-up with Carbice addresses thermal interface materials for electronics. Partnerships between chemical suppliers and equipment OEMs shorten qualification cycles and lock in long-term volumes across the thermic fluids market.

Start-ups attract venture capital for modular thermal storage, signaling fresh competitive pressure at system level. Nevertheless, barriers remain steep: certifications, plant audits and after-sales engineering favor incumbents. Overall, competition coalesces around integrated value-chain control, environmental compliance and lifecycle performance guarantees.

Thermic Fluid Industry Leaders

BP plc

Dow

Eastman Chemical Company

Exxon Mobil Corporation

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Castrol, a part of BP plc has introduced Castrol ON Direct Liquid Cooling PG 25, a propylene glycol-based cooling fluid specifically engineered for direct-to-chip cooling in high-performance data centers. This launch aims to drive innovation in the thermic fluid market by meeting the demand for efficient cooling in advanced computing.

- October 2023: ExxonMobil introduced a comprehensive portfolio of immersion fluid products for data centers, designed to enhance performance across various industries and global regions. This development is expected to drive innovation and growth in the thermic fluid market by addressing the increasing demand for efficient cooling solutions.

Global Thermic Fluid Market Report Scope

Thermic fluids, also known as heat transfer fluids, are chemicals that can be in liquid or vapor form and used for transferring heat from one system to another. These fluids are mainly used in the reboiler, condenser, regenerator, and other heat-exchanging systems in the processing facilities of various end-user industries, including oil and gas, chemical, and pharmaceutical. Thermic fluids can be based on synthetic oils, molten salts, silicone fluids, glycols, etc. The thermic fluid market is segmented by type, end-user industry, and geography. By type, the market is segmented into mineral oils, silicon and aromatics, glycols, and other types. By end-user industry, the market is segmented into food and beverage, chemical, pharmaceutical, oil and gas, concentrated solar power, and other end-user industries. The report also covers the market size and forecasts for the thermic fluid market in 16 countries across major regions. Market sizing and forecasts are based on each segment's value (USD million).

By Product Type

| Mineral Oils |

| Silicon and Aromatics |

| Glycols |

| Other Product Types |

By Temperature Range

| Low Temperature (less than 150 °C) |

| Medium Temperature (150-300 °C) |

| High Temperature (greater than 300 °C) |

By End-user Industry

| Chemical |

| Oil and Gas |

| Food and Beverage |

| Pharmaceutical |

| Concentrated Solar Power |

| Other End-user Industry |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Mineral Oils | |

| Silicon and Aromatics | ||

| Glycols | ||

| Other Product Types | ||

| By Temperature Range | Low Temperature (less than 150 °C) | |

| Medium Temperature (150-300 °C) | ||

| High Temperature (greater than 300 °C) | ||

| By End-user Industry | Chemical | |

| Oil and Gas | ||

| Food and Beverage | ||

| Pharmaceutical | ||

| Concentrated Solar Power | ||

| Other End-user Industry | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the thermic fluids market?

The thermic fluids market size is USD 12.21 billion in 2026.

Which temperature range segment is growing fastest?

High-temperature applications above 300 °C show the highest 4.67% CAGR through 2031.

Why are synthetics gaining on mineral oils?

Stricter emission rules, higher operating temperatures and demands for longer fluid life are pushing users toward synthetic formulations that outperform mineral oils despite higher upfront costs.

Which end-user industry will add the most new demand?

Concentrated solar power is forecast to expand at 5.05% CAGR and will add the most incremental demand by 2031.

How does Asia-Pacific maintain its lead in the market?

Large-scale refining, massive petrochemical investments and aggressive renewable-energy targets give Asia-Pacific the largest 37.40% share and sustain 4.42% CAGR growth.

What role do data centers play in future demand?

Rising adoption of immersion cooling fluids for AI and high-performance computing racks positions data centers as an important emerging application that can diversify overall market growth.

Page last updated on: