Image Guided Therapy System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 5.67 Billion |

| Market Size (2031) | USD 7.27 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Image Guided Therapy System Market Analysis by Mordor Intelligence

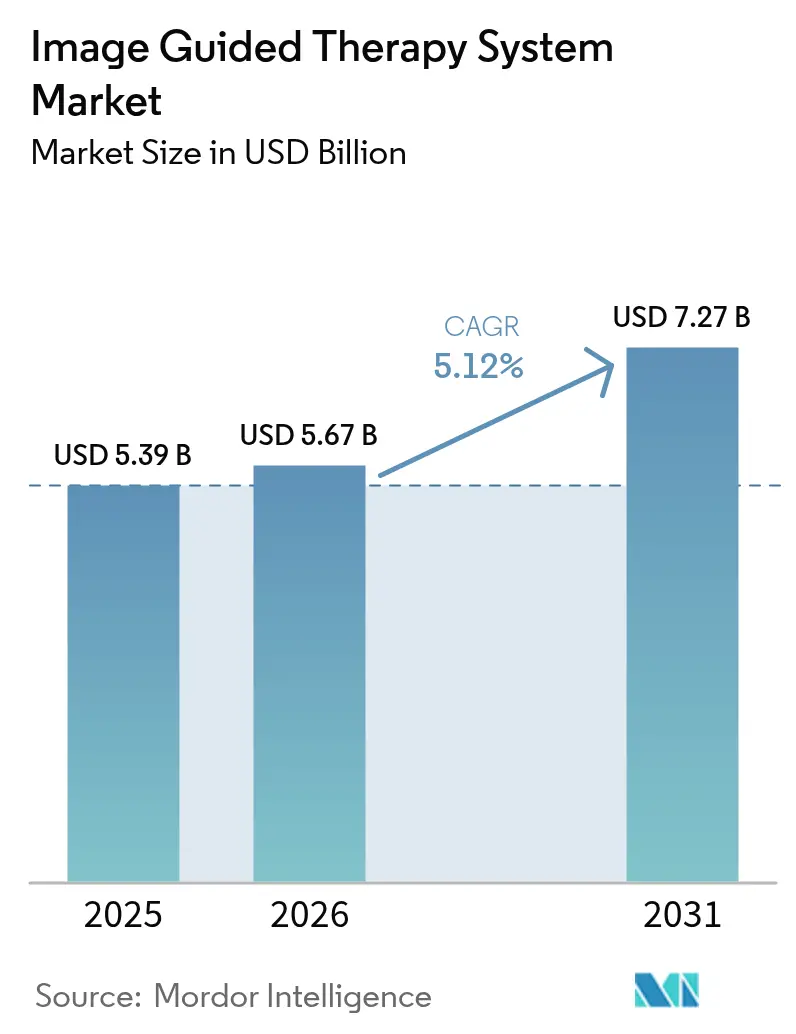

The Image Guided Therapy System market size is expected to grow from USD 5.39 billion in 2025 to USD 5.67 billion in 2026 and is forecast to reach USD 7.27 billion by 2031 at 5.12% CAGR over 2026-2031. Growth now stems from deeper platform integration, where AI-enhanced, multi-modality suites replace stand-alone imaging units. Software-centric innovation sharpens procedural accuracy, while regulatory alignment around interoperability and device cybersecurity lowers switching costs for health systems. Capital flows concentrate on hybrid operating rooms (ORs) that merge electromagnetic navigation, real-time MRI and robotic manipulation. Training bottlenecks for the 14-person teams often required inside hybrid ORs temper near-term growth, yet long-run demand benefits from an aging population, rising chronic-disease incidence and the clinical push toward minimally invasive care.

Key Report Takeaways

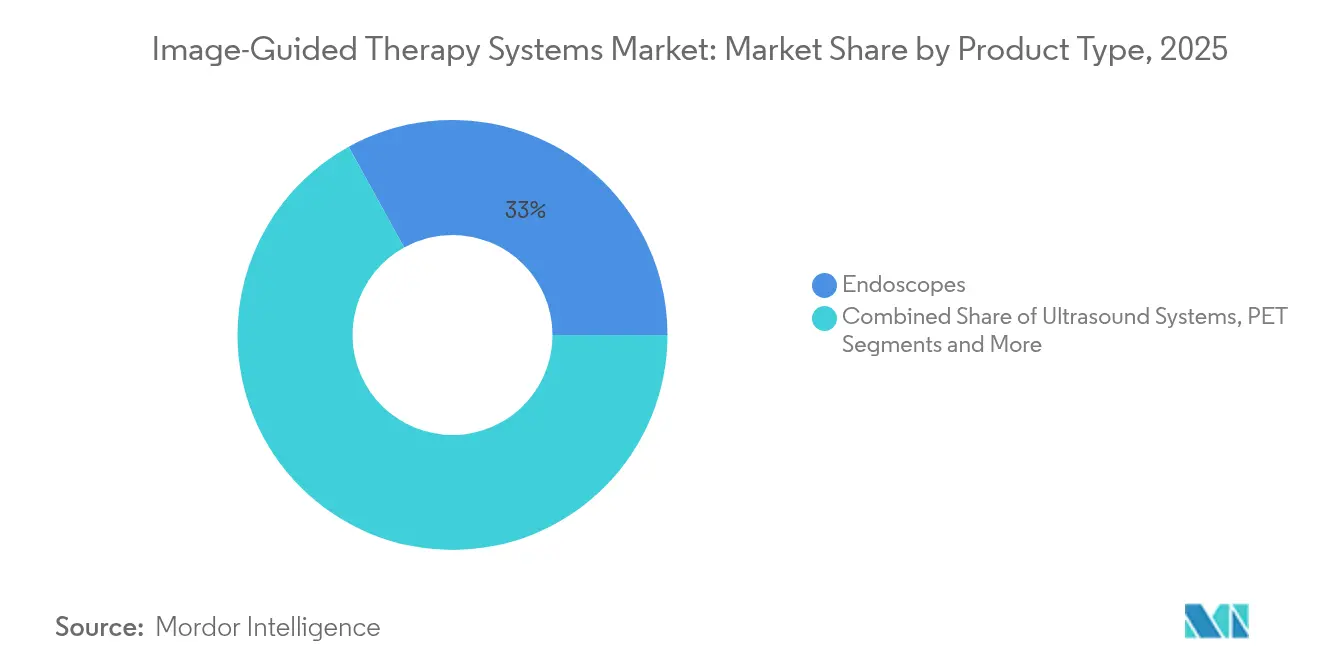

- By product category, endoscopes held 33.02% of the Image Guided Therapy System market share in 2025; MRI systems are projected to grow at 5.60% CAGR through 2031.

- By technology, electromagnetic navigation accounted for 29.94% revenue share in 2025, while robotic-assisted imaging guidance is set to advance at a 6.13% CAGR to 2031.

- By application, cardiac surgery & structural heart dominated with 32.01% share of the Image Guided Therapy System market size in 2025; neurosurgery is poised to rise at a 6.25% CAGR.

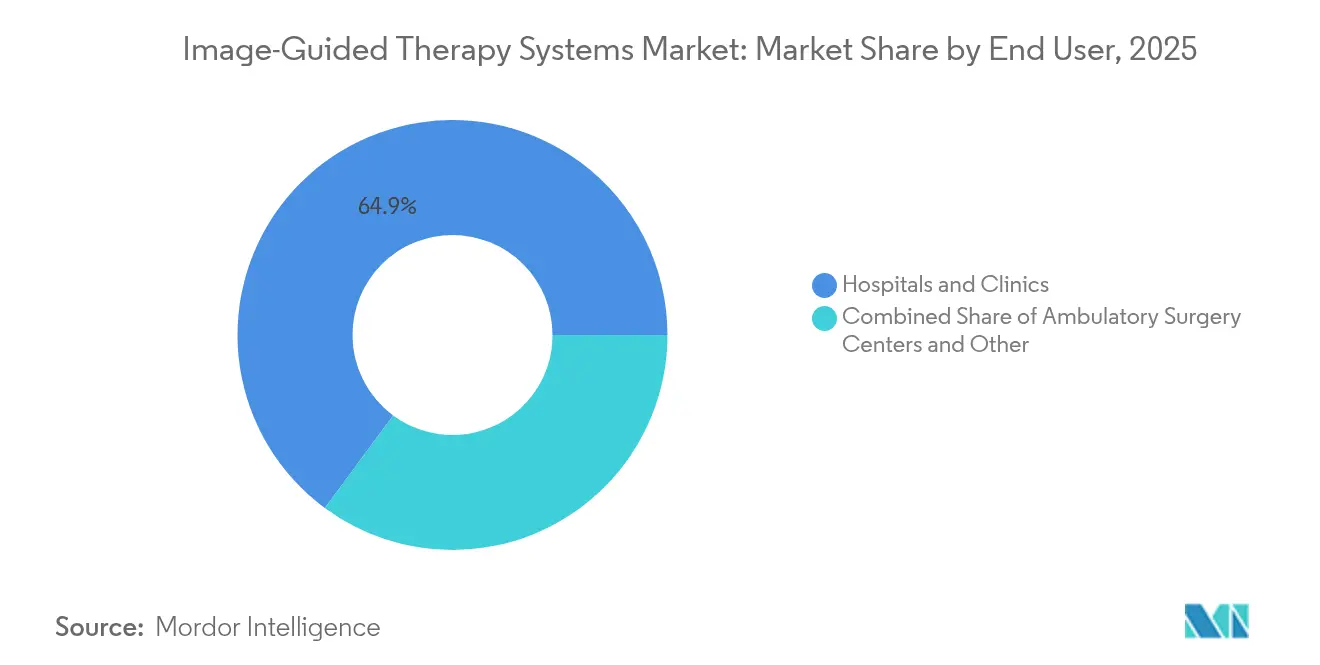

- By end-user, hospitals and clinics captured 64.88% revenue share in 2025 as ambulatory surgery centers expand the fastest at 5.80% CAGR.

- By modality portability, fixed systems held 53.64% of the Image Guided Therapy System market size in 2025, whereas hand-held/portable units lead growth at 5.82% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Image Guided Therapy System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing geriatric population | +1.2% | Global, North America & Europe dense | Long term (≥ 4 years) |

| Rising burden of chronic diseases | +1.1% | Global, faster in Asia-Pacific | Medium term (2-4 years) |

| Shift to minimally invasive, image-guided procedures | +0.9% | North America & EU lead | Short term (≤ 2 years) |

| Expansion of hybrid operating rooms | +0.8% | North America & Europe core | Medium term (2-4 years) |

| Regulatory convergence on interoperability | +0.6% | EU & North America | Long term (≥ 4 years) |

| Venture funding for MRI/US-guided robotics | +0.4% | Global, North America focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing geriatric population

Patients aged 65+ now constitute the fastest-growing surgical cohort, prompting wider adoption of precise electromagnetic navigation that limits tissue trauma and speeds recovery. MRI-guided focused ultrasound lets fragile elders avoid open craniotomy for essential tremor, improving quality-adjusted life years while trimming readmissions. Health-system budget holders recognize that upfront imaging costs offset downstream postoperative expenses.

Rising burden of chronic diseases

Cardiovascular, oncologic and neurologic disorders collectively drive over 70% of deaths worldwide, making repeatable, image-guided interventions essential. Deep-learning ECG analytics reach 95% accuracy in detecting structural heart disease, fueling earlier referrals to catheter-based repair guided by real-time 3D imaging [1]National Institutes of Health, “Deep Learning for Cardiovascular Imaging,” nih.gov . Fiscal strain from chronic illness sharpens the case for technologies that reduce lifelong care volumes.

Rapid shift to minimally invasive, image-guided procedures

Ambulatory centers complete most U.S. surgeries today, cutting costs up to 50% and wait times by 20% while favoring compact imaging units that fit smaller suites. Robotic navigation shortens transforaminal lumbar fusion times and lowers revision rates, and augmented-reality overlays let surgeons track subsurface anatomy without breaking sterility.

Expansion of hybrid operating rooms in tertiary hospitals

A hybrid OR merges angiography, CT or MRI with surgical tables, letting clinicians alternate between diagnosis and therapy in a single session. Each room can demand USD 2-5 million in capital, yet payback arrives in 3-5 years owing to higher case throughput and fewer transfers. Staffing complexity—often 14 specialists—remains the prime constraint.

Regulatory convergence enabling multi-modality interoperability

The U.S. FDA and the EU Medical Device Regulation now accept common DICOM-based cybersecurity test suites, reducing vendor-lock penalties and enabling hospitals to mix best-of-breed components.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of integrated systems | -1.4% | Global, emerging markets acute | Medium term (2-4 years) |

| Radiation & electromagnetic exposure concerns | -0.8% | Global regulatory focus | Long term (≥ 4 years) |

| Shortage of hybrid-OR-trained specialists | -0.7% | North America & Europe | Short term (≤ 2 years) |

| Cyber-security and data-integration hurdles | -0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital cost of integrated systems

Comprehensive suites that blend navigation, robotics and AI imaging cost USD 1-3 million plus 15–20% annual service fees, deterring mid-tier hospitals with thin margins. Leasing and outcome-based contracts soften this barrier but cannot erase scale advantages enjoyed by academic centers.

Radiation & electromagnetic exposure concerns

The U.S. CDC links 2% of annual cancers to medical imaging radiation, prompting stricter dose-tracking mandates and preference for non-ionizing guidance such as MRI and ultrasound [2]Centers for Disease Control and Prevention, “Ionizing Radiation in Medical Imaging,” cdc.gov . Electromagnetic interference fears add shielding expenses and testing delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Endoscopes sustain leadership while MRI accelerates

Endoscopes retained 33.02% of the Image Guided Therapy System market in 2025 as their flexibility spans gastroenterology, urology and pulmonology. Hospitals integrate electromagnetic tracking probes through existing endoscope channels, trimming incremental spend. MRI systems, though smaller in volume, are forecast to expand 5.60% annually as focused ultrasound, laser ablation and deep-brain neuromodulation migrate into real-time MRI suites. Vendors now offer intra-operative 1.5 T magnets with robotic accessories that pivot seamlessly between scan and incision.

Ultrasound platforms gain momentum among ambulatory centers because portable carts need lower room shielding and cost fractions of fixed CT. X-ray C-arms stay vital for high-volume angiography despite radiation scrutiny. Hybrids such as PET-MRI tackle oncology staging in single sessions, blurring lines between diagnostic and therapeutic imaging.

By Technology: Electromagnetic navigation dominance meets robotic challenge

Electromagnetic navigation commanded 29.94% revenue in 2025 owing to line-of-sight independence and sub-millimeter accuracy in spine and cranial work. Segment revenue hit USD 1.61 billion, representing the highest slice of the Image Guided Therapy System market size that year. Robotic-assisted imaging guidance is poised to climb 6.13% CAGR through 2031 as AI route-planning and automated drilling cut operating times.

Real-time 3D/4D AI visualization halves targeting error versus manual fluoroscopy, according to multicenter trials. Augmented reality headsets project CT data onto the surgical field, refining implant alignment. Optical trackers remain economical for orthopedic extremity work yet lose precision in deep cavities.

By Application: Cardiac dominance balances neurosurgical innovation

Cardiac surgery & structural heart held 32.01% of 2025 revenue as TAVR, mitral repair and left-atrial appendage closure demand fused fluoroscopy–echo guidance. At USD 1.73 billion, cardiac uses formed the biggest slice of the Image Guided Therapy System market share in 2025. Neurosurgery grows fastest at 6.25% CAGR atop MRI-guided focused ultrasound for tremor and Parkinson’s.

Orthopedic and spine suites deploy robotic arms with CT navigation to raise screw placement accuracy, lowering revision rates. Oncology embraces microwave and cryo-ablation under CT-US fusion, benefiting frail patients unsuitable for open excision.

By End-user: Hospital consolidation versus ASC agility

Hospitals and clinics absorbed 64.88% of 2025 revenue, favored for complex, capital-intensive caseloads. Their purchasing consortia negotiate fleet upgrades, bundling service and cybersecurity into multiyear contracts. Ambulatory surgery centers expand 5.80% CAGR by focusing on lower-acuity procedures where portable ultrasound or compact CT suffices. Reimbursement parity for outpatient TAVR and complex spine accelerates ASC adoption.

Specialist centers that concentrate on one or two high-volume lines—such as electrophysiology or minimally invasive spine—often secure dedicated image-guided theaters, boosting throughput beyond general hospitals.

By Modality Portability: Fixed system stability meets portable innovation

Fixed suites provided 53.64% of sales in 2025, prized for superior detector size, cooling and image fidelity demanded in neuro-oncology and hybrid ORs. Portable scanners, however, will post 5.82% CAGR. Hand-held ultrasound probes stream AI-enhanced images to tablets, enabling trauma surgeons to place chest drains at the bedside. Mobile C-arms now feature 3D cone-beam and navigation packages once reserved for fixed angiography labs, compressing footprint without sacrificing guidance accuracy.

Geography Analysis

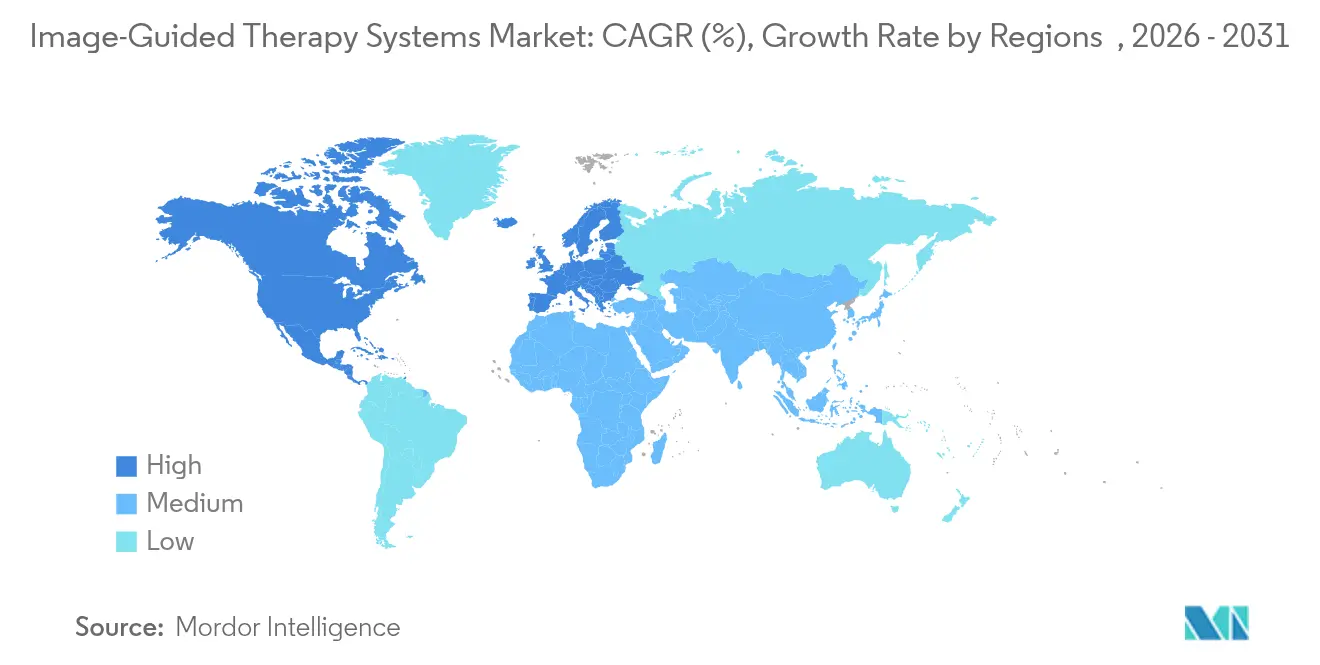

North America led with 45.18% revenue in 2025 as academic health systems, supportive reimbursement and dense vendor presence speed adoption. The FDA’s 2024 cybersecurity final rule clarified premarket requirements, letting suppliers certify multi-modality suites more quickly. U.S. venture investment in surgical robotics surpassed USD 2 billion in 2024, intensifying domestic competition. While payers pressure hospitals to justify capital spend, consolidation affords network-wide rollouts that spread cost over higher procedure volumes.

Asia-Pacific is projected to rise 6.55% CAGR through 2031. China’s public-hospital reform funnels budget toward high-end imaging, and the Healthy China 2030 plan subsidizes minimally invasive cardiology labs. Japan’s super-aged society raises demand for low-trauma therapy; local makers pioneer MRI-compatible robotics that fit small urban hospitals. India’s private chains deploy portable ultrasound and navigation bundles to tap medical tourism, while Korea combines domestic manufacturing strength with heavy R&D tax incentives.

Europe remains a technology proving ground under the Medical Device Regulation. Health-technology assessment agencies such as NICE evaluate cost-utility, nudging suppliers to document outcome gains. Germany hosts clusters of mid-sized imaging OEMs that supply modular components worldwide. EU AI Act rules, effective 2025, require transparent algorithm logs for surgical guidance software, lengthening validation cycles yet offering first-mover advantage for compliant vendors . Elsewhere, Brazil and Saudi Arabia upgrade trauma networks with hybrid cath-lab–OR complexes, opening late-adopter avenues.

Competitive Landscape

The Image Guided Therapy System market shows moderate concentration: the top five firms account for roughly 55% of global revenue. Siemens Healthineers, GE HealthCare and Philips anchor portfolios with CT, MRI and angio labs, adding AI navigation layers via in-house code or partnerships. Stryker and Brainlab focus on orthopedic and cranial navigation, integrating third-party imaging for full-procedure ecosystems. Strategic deals emphasize software: GE’s 2024 buyout of an AI segmentation startup embedded auto-contouring in its Innova platform, while Medtronic teamed with Siemens Healthineers to feed intra-op CBCT into its Mazor spine robots.

Start-ups tackle gaps in portability and cost. Hyperfine’s point-of-care MRI targets neurocritical care beds, and Clarius markets wireless ultrasound probes for ambulatory sites. Cybersecurity has moved from checkbox to differentiator; vendors that achieve FDA’s Secure Product Development Framework earn procurement preference among U.S. hospital groups. Distributors in emerging markets bundle leasing, service and surgeon training to lower entry friction.

Image Guided Therapy System Industry Leaders

Koninklijke Philips N.V.

Brainlab

Siemens Healthineers

General Electric Company (GE Healthcare)

Altaris Capital Partners, LLC (Analogic Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Philips India unveiled Azurion image-guided therapy suite with table-side 3D switching and AI-based remote diagnostics.

- October 2024: Philips and Medtronic Neurovascular partnered with the World Stroke Organization to widen timely stroke-care access using image-guided platforms.

- October 2024: GE HealthCare released Versana Premier ultrasound featuring AI workflow tools across OBGYN and cardiology.

- September 2024: Medtronic expanded the AiBLE spine ecosystem via Siemens Healthineers imaging and AI planning modules.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the image-guided therapy systems market as all purpose-built capital equipment and embedded software that fuse real-time imaging (CT, MRI, ultrasound, fluoroscopy, PET, SPECT, or endoscopy) with navigation workstations to plan, perform, and assess minimally invasive interventions across surgical, interventional radiology, and cardiology suites.

Scope Exclusions: sales of stand-alone diagnostic scanners, conventional external-beam radiotherapy LINACs, and post-processing software sold independent of an interventional platform are outside the study.

Segmentation Overview

- By Product Type

- Ultrasound Systems

- Endoscopes

- Magnetic Resonance Imaging (MRI)

- X-ray Fluoroscopy / C-arms

- Positron Emission Tomography (PET)

- Single-Photon Emission CT (SPECT)

- Others

- By Technology

- Electromagnetic Navigation

- Robotic-assisted Imaging Guidance

- AI-Enhanced Real-time 3D/4D Imaging

- Augmented / Mixed-Reality Visualization

- Optical & Laser-based Tracking

- By Application

- Neurosurgery

- Cardiac Surgery & Structural Heart

- Orthopedic & Spine

- Urology

- Oncology & Ablation

- Others

- By End-user

- Hospitals and Clinics

- Ambulatory Surgery Centers

- Others

- By Modality Portability

- Fixed Systems

- Mobile C-arms

- Hand-held / Portable

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with biomedical engineers, cath-lab managers, interventional radiologists, and procurement heads across North America, Europe, and Asia help validate installed-base life cycles, utilization rates, and average selling prices. Targeted surveys of clinicians confirm emerging use cases such as robotic navigation and mixed-reality overlays, filling gaps left by public data.

Desk Research

Our analysts first map the demand context using publicly available tier-1 sources such as the WHO hospital procedure statistics, OECD Health Data on imaging install base, United States FDA 510(k) device clearances, and Eurostat trade codes for C-arms and endoscopes. Annual reports, Form 10-Ks, and investor slide decks of leading imaging vendors, along with specialty society registries for cardiac and neuro procedures, provide unit trends and typical pricing bands. Subscription datasets from D&B Hoovers (company revenues) and Dow Jones Factiva (deal pipelines) supply additional benchmarks for market share and deal momentum. The sources listed illustrate our approach; a wider body of literature, government tenders, and patent feeds were also consulted to cross-check figures and narratives.

Market-Sizing & Forecasting

A top-down demand pool begins with procedure volumes by specialty, adjusted for imaging-guided adoption rates and average device capacity. Results are cross-checked through selective bottom-up roll-ups of supplier shipments and sampled ASP × units. Key inputs include elective surgery backlogs, aging population growth, hybrid OR penetration, capital budget outlooks, reimbursement trends, and average seven-year replacement cycles. Multivariate regression, with procedure growth and capital expenditure indices as predictors, underpins the 2025-2030 forecast, while scenario analysis tests shocks such as delayed hospital capex or accelerated AI-driven upgrades.

Data Validation & Update Cycle

Outputs pass variance checks against independent install-base audits and trade data. Senior analysts review anomalies before release. Reports refresh every twelve months, with interim updates triggered by major regulatory approvals or material M&A, ensuring clients receive the latest view.

Why Mordor's Image-Guided Therapy Systems Baseline Earns Trust

Published figures frequently diverge because publishers choose different device baskets, price assumptions, and refresh rhythms. By anchoring our base year to verified procedure counts and cross-examined ASPs, Mordor Intelligence delivers a balanced number that planners can replicate.

Key gap drivers include inclusion of diagnostic scanners, blanket CAGR application, and omission of device life-cycle corrections, which are addressed in Mordor's disciplined model.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.39 B (2025) | Mordor Intelligence | |

| USD 5.13 B (2024) | Regional Consultancy A | Considers only upgrade sales, assumes fixed eight-year replacement without procedure growth adjustment |

| USD 5.10 B (2024) | Global Consultancy B | Applies single 7.3% CAGR and blends radiation therapy with therapy systems |

| USD 6.12 B (2024) | Industry Association C | Counts diagnostic imaging scanners as therapy systems, inflating base value |

Taken together, the comparison shows that our scoped device list, dual-path validation, and annual refresh cadence yield a figure that sits between aggressive and conservative extremes, giving decision-makers a dependable, transparent baseline.

Key Questions Answered in the Report

What is the current Global Image Guided Therapy System Market size?

The market stood at USD 5.67 billion in 2026 and is projected to reach USD 7.27 billion by 2031.

Who are the key players in Global Image Guided Therapy System Market?

Koninklijke Philips N.V., Brainlab, Siemens Healthineers, General Electric Company (GE Healthcare) and Altaris Capital Partners, LLC (Analogic Corporation) are the major companies operating in the Global Image Guided Therapy System Market.

Which segment holds the largest Image Guided Therapy System market share?

Endoscopes led with 33.02% revenue share in 2025.

Which region has the biggest share in Global Image Guided Therapy System Market?

In 2025, the North America accounts for the largest market share in Global Image Guided Therapy System Market.

Page last updated on: