Cups And Lids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.34 Billion |

| Market Size (2031) | USD 21.64 Billion |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cups And Lids Market Analysis by Mordor Intelligence

The cups and lids market size in 2026 is estimated at USD 18.34 billion, growing from 2025 value of USD 17.74 billion with 2031 projections showing USD 21.64 billion, growing at 3.37% CAGR over 2026-2031. Moderate yet steady growth reflects post-pandemic foodservice recovery, rising e-commerce volumes, and the spread of on-the-go consumption habits that rely on single-use beverage packaging. Material trends show plastics retaining a 61.35% share in 2024, while paper and paperboard post the fastest 4.63% CAGR, helped by sustainability mandates and molded-fiber innovations. Drinking cups command 52.21% of global revenue, though lids register the quickest 4.49% CAGR as spill-proof and tamper-evident formats gain traction. Foodservice stays the largest end-user at 49.65% share, yet retail and e-commerce outlets expand at 4.86% CAGR as private-label beverages and meal-kit operators raise demand for branded take-home containers. Regionally, North America leads with 39.42% share, but Asia-Pacific delivers the highest 4.51% CAGR, powered by expanding QSR chains and urban coffee culture in China and India..

Key Report Takeaways

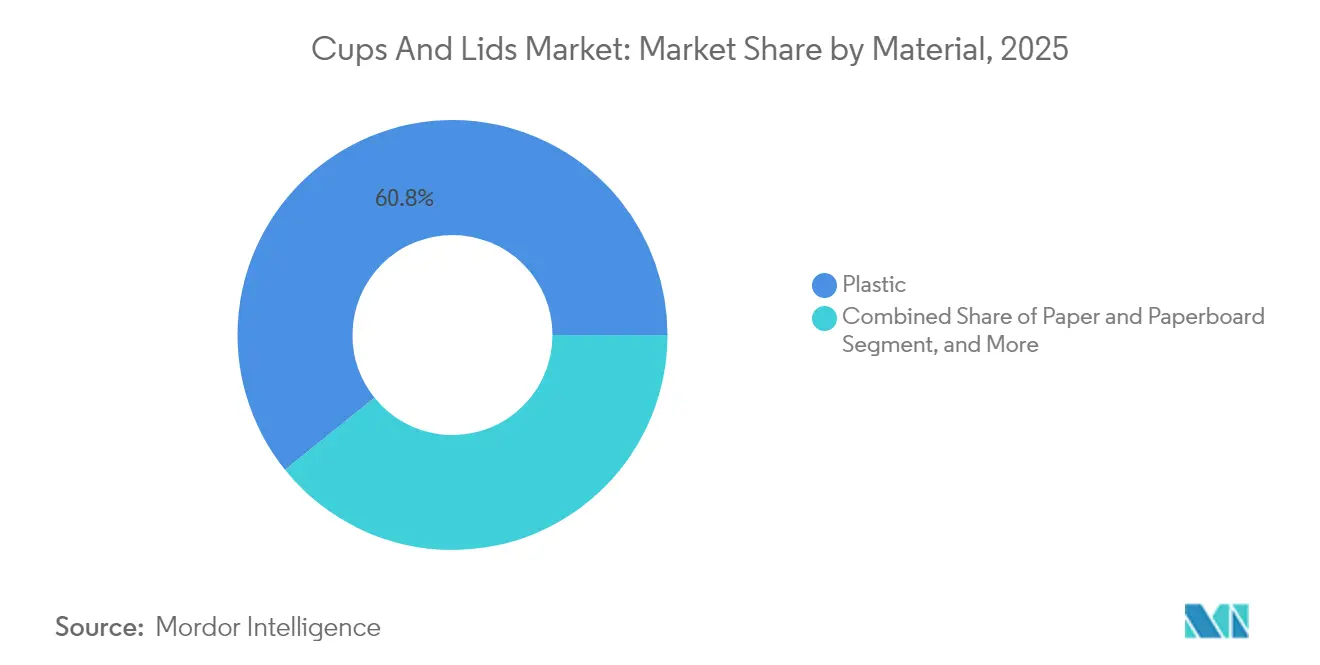

- By material, plastics held a 60.78% of the cups and lids market share in 2025.

- By product type, the cups and lids market for lids is projected to grow at a 4.41% CAGR between 2026-2031.

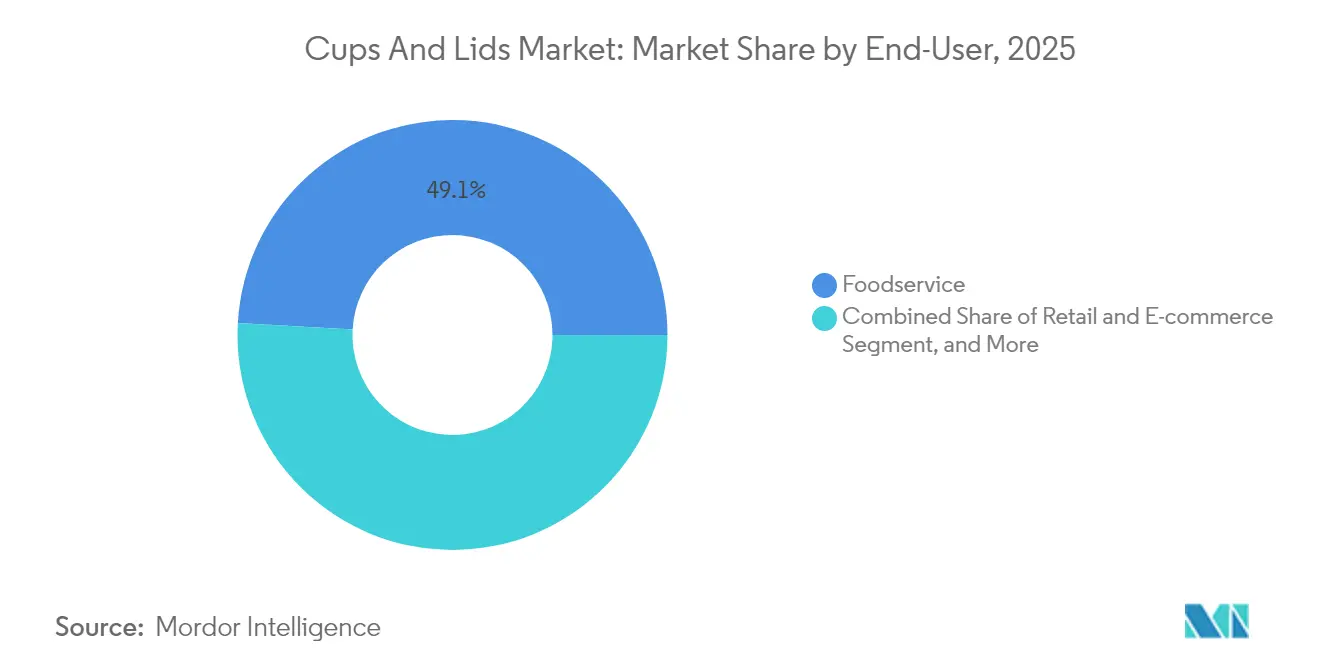

- By end-user, foodservice accounted for a 49.12% share of the cups and lids market size in 2025.

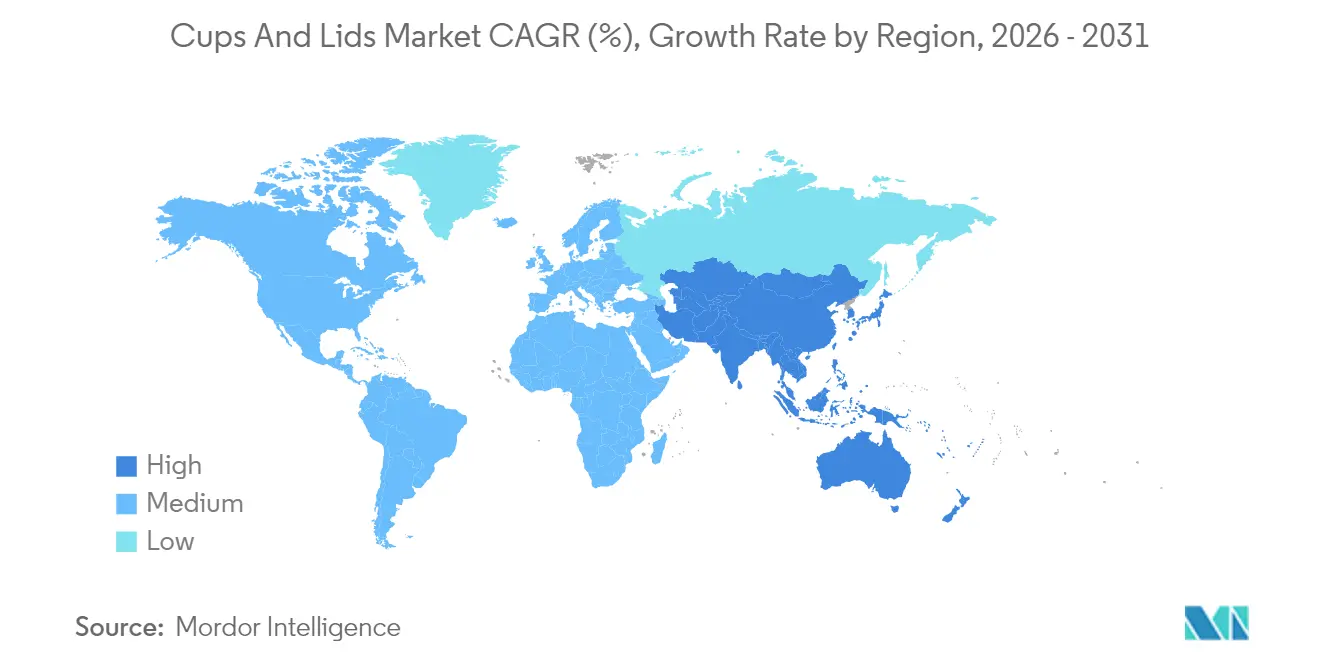

- By geography, the cups and lids market in the Asia-Pacific region is projected to grow at a 4.44% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cups And Lids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| QSR and Food-delivery Boom | +0.8% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in On-the-go Drinks | +0.6% | Global, particularly urban centers in developed markets | Short term (≤ 2 years) |

| Shift from Glass to Plastic | +0.4% | North America and Europe, spill-over to APAC | Long term (≥ 4 years) |

| Rise of Private-label SKUs | +0.5% | North America and Europe core, expanding to emerging markets | Medium term (2-4 years) |

| Dry-molded-fiber Technology | +0.3% | Europe and North America early adoption, global expansion | Long term (≥ 4 years) |

| AI-optimised Inventory | +0.2% | Developed markets initially, gradual emerging market penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

QSR and Food-delivery Boom

Rapid expansion of quick-service restaurants and double-digit growth in delivery orders heighten the need for single-serve packaging. McDonald’s opened over 1,100 new outlets in 2024, while DoorDash posted an 18% year-over-year rise in gross order value to USD 18.7 billion in Q1 2025.[1]McDonald’s Corporation, “Fourth Quarter and Full Year 2024 Results,” corporate.mcdonalds.com Each delivery meal typically contains multiple beverages, requiring leak-proof cups and tamper-evident lids that protect food safety during transit. The surge encourages converters to add integrated venting, QR code tracking, and multi-compartment formats. Asian markets gain strongly because QSR penetration remains below Western levels yet grows in double digits, creating incremental demand for disposables.

Growth in On-the-go Drinks

Global coffee shop visits increased by 12% in 2024 as urban commuters sought takeaway beverages. The trend extends to cold brews, protein shakes, and fresh juices, each requiring distinct barrier properties and temperature resilience. Starbucks removed plastic straws by converting to sipper lids across 30,000 locations, eliminating 1 billion straws annually and illustrating how consumer behavior drives lid redesign. Manufacturers respond with polypropylene-free lids and paper-based vents that pass hot-fill tests, leveraging ESG messaging to capture premium shelf space.

Rise of Private-label SKUs

Store brands increased their retail sales share to 20.2% in 2024, up 110 basis points year-over-year. Retailers want cost-effective packaging that still signals quality, prompting suppliers to standardize cup dimensions and lid thread sizes. Regional converters with shorter lead times and flexible print runs gain orders from supermarket chains launching exclusive beverage lines. Walmart sourced more than 500 million cups for its Great Value drinks in 2024, illustrating scale benefits for agile suppliers. The shift promotes bulk procurement contracts that stabilize converter capacity utilization.

Dry-molded-fiber Technology

PulPac’s dry-molded-fiber process removes water from the forming stage, cutting energy use and reducing unit costs by 30% compared to wet molding. Dart Container invested alongside PulPac in 2025 to commercialize fiber-based cups that target cost parity with plastic in the takeaway coffee market. The technology supports deeper draw profiles and embossed logos, allowing brand owners to swap resin without losing functionality. Huhtamäki’s USD 27.3 million expansion in Germany will raise molded-fiber output by 40% and signals accelerating scale-up across Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastics Regulations | -0.7% | Europe and select US states leading, global expansion | Short term (≤ 2 years) |

| Volatile Resin Prices | -0.5% | Global, with highest impact in cost-sensitive segments | Short term (≤ 2 years) |

| Growing Reusable Culture | -0.4% | Developed markets initially, gradual global adoption | Long term (≥ 4 years) |

| PFAS Barrier Bans | -0.3% | North America and Europe core, regulatory expansion expected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plastics Regulations

The European Single-Use Plastics Directive and California’s SB 54 mandate require producers to pay new fees of EUR 0.05-0.15 per cup and mandate a 25% reduction in plastic use by 2032. Compliance adds capital costs for material conversion and encourages region-specific product portfolios. Smaller converters face disproportionate burdens and may exit the cups and lids market, leading to higher consolidation.

Volatile Resin Prices

Polyethylene prices swung 35% during 2024, and polystyrene jumped 28% in Q1 2025 before sliding 15% in Q2, squeezing converter margins. Frequent price resets strain restaurant chains on fixed menu pricing and create inventory risks for just-in-time operations. Converters adopt hedging and increased recycled-content use, yet smaller players without access to financial derivatives remain exposed to sharp cost spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Paper Gains Ground as Sustainability Push Deepens

Paper and paperboard recorded a 4.55% CAGR through 2031, outpacing plastics, even though the latter still held a 60.78% market share in cups and lids in 2025. The cups and lids market size for fiber-based formats is projected to expand steadily as coffee chains trial molded-fiber lids that pass hot-fill requirements. Foam polystyrene continues to decline as municipal bans expand, while bioplastics remain a niche market due to high feedstock costs.

Converters must dual-source to serve mixed regulatory regimes, so capital allocation pivots toward flexible lines that switch between PET, rPET, and coated paperboard. Dart Container’s USD 180 million paper cup line enables rapid order changes, highlighting how leading producers diversify material risk while pursuing eco-label demand. Brands demand chemical-free barrier coatings to avoid PFAS restrictions, prompting investment in water-based dispersions that still withstand temperatures of 100 °C for beverages.

By Product Type: Lids Lead Innovation Curve

Lids posted the highest 4.41% CAGR and now attract R&D funding for sipper geometry, tamper bands, and smart QR seals. Drinking cups still generate 51.62% of revenue, but customers order matched cup-lid kits to simplify recycling streams, so suppliers integrate design and sales. Portion cups serve fast-growing meal-kit firms that require leak-proof formats for sauces and condiments during their two-day shipping process.

Starbucks' adoption of the strawless lid shows how a single retailer can reset design norms and spur broader adoption. E-commerce grocers prefer stackable cup profiles that reduce voxel height in shipping cartons, thereby saving on freight costs. Leading converters file multiple patents around hinge-free vents and lid stock with post-consumer recycled content, locking in switching costs for buyers.

By End-User: Retail and E-commerce Outpace Foodservice

Foodservice keeps 49.12% global revenue share, yet retail and e-commerce channels enjoy a 4.79% CAGR as supermarket chains and direct-to-consumer brands proliferate. The cups and lids market size associated with online grocery shipments is expected to double by 2030 as fresh juice, smoothie kits, and ready-to-drink coffees scale.

Omnichannel brands require packaging that travels well yet opens cleanly during social media-driven unboxing moments. Amazon cut packaging weight by 38% in 2024, requiring suppliers to validate stress performance under automated test regimes. Converters that can ship MOQ-flexible orders and offer co-packed multipacks gain share with emerging food startups.

Geography Analysis

North America retained a 38.96% market share of cups and lids in 2025, supported by a well-established drive-thru culture and consumers willing to pay for sustainable packaging upgrades. Canada’s single-use plastic ban in 2024 fueled migration to coated paperboard, while Mexico’s growing QSR footprint supplied volume growth for low-cost PET cups. FDA food-contact regulations raise barriers for new entrants yet protect incumbents with strong compliance teams.

Asia-Pacific delivered the highest 4.44% CAGR and remains the focal point for capacity expansions. China experienced a 20% increase in coffee consumption in 2024, which heightened demand for specialty lids that preserve the crema texture during takeaway service. India’s USD 70 billion organized retail sector now specifies standardized volume markers on cups, supporting large production runs and thin-wall designs that cut resin use. Regional wage advantages also attract multinational converters, who are building export hubs that ship to buyers in the Middle East.

Europe grew modestly yet remains the innovation leader, largely due to stringent Extended Producer Responsibility fees that favor recyclable mono-material systems. Germany’s 70% recycling rate target for 2025 encourages brand owners to adopt clear PET cups with matching PET lids, thereby enhancing single-stream collection. The European Commission’s Circular Economy Action Plan layers deposit schemes that add EUR 0.05-0.15 per unit, creating demand for lightweight formats that defend total cost. Suppliers with traceable recycled content certification receive procurement preference from large beverage chains.

Regulatory Landscape

Regulation continues to tighten around single-use beverage packaging, which is driving redesign of cups and lids and accelerating material and chemistry substitutions. In Europe, the Single-Use Plastics Directive (Directive (EU) 2019/904) includes requirements affecting beverage cups and lids, including tethered-cap style rules applied to certain plastic beverage containers and related design-for-recycling priorities that influence lid geometry and attachment concepts across foodservice packs.

Food-contact compliance is also a key gating factor for market access. The EU is updating authorized substance lists and restrictions for plastic food-contact materials through amendments to Regulation (EU) No 10/2011 (positive list updates), and introduced new BPA-related requirements under Regulation (EU) 2026/250, including a sell-off deadline of July 20, 2026 for existing non-compliant single-use food-contact items. In the United States, the FDA Food Contact Notification (FCN) pathway remains central for new resins, additives, and coatings used in cups and lids, with multiple new FCNs recorded during March to May 2026. This reinforces the need for continuous formulation review and documentation among converters and brand owners.

Competitive Landscape

Global competition is moderately fragmented. The top five players held approximately a 35% revenue share in 2024, with Amcor, Dart Container, and Huhtamäki leading the way. Consolidation rose when Amcor acquired Berry Global’s consumer packaging arm for USD 8.43 billion in 2025 and Novolex purchased Pactiv Evergreen for USD 2.3 billion, creating entities with broader portfolios and better raw material bargaining power.[3]Amcor plc, “Completes Berry Global Acquisition,” amcor.com

Strategy increasingly hinges on sustainability. Huhtamäki allocates 65% of capex to molded-fiber projects that qualify for EU green financing. Dart Container installs AI inventory tools that reduce finished-goods stocks by 18%, freeing up cash to fund next-generation coating lines. Regional challengers leverage proximity and lower freight costs to secure private-label contracts, though they risk margin erosion when resin prices spike.

Technology adoption is rapid. PulPac’s dry-molded-fiber partnership with Dart aims for commercial output by 2026, targeting hot beverages currently served in PE-lined paper cups. Novolex integrates predictive maintenance sensors that reduce unplanned downtime by 12%. Intellectual property related to plant-based coatings and vent geometry becomes a tradable currency in joint-development deals with beverage brands seeking exclusive drinking experiences.

Cups And Lids Industry Leaders

Huhtamäki Oyj

Amcor plc

Mondi plc

Graphic Packaging Holding Company

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace sits in scalable, food-contact-compliant alternatives to conventional PE-lined paper cups and polystyrene, as well as other hard-to-recycle lid formats, particularly for hot beverages and delivery use cases where leak resistance and heat stability are non-negotiable. Activity during 2026 also shows where buyers are placing near-term demand: Huhtamaki and Hesburger began transitioning to fiber-based beverage lids in selected markets, framing the switch around removal of plastic lids at restaurant scale, while Amcor brought polypropylene dip cups and lidding solutions to market, positioned around recycle-ready mono-material formats.

Barrier and recycled-content technologies also open incremental opportunities for suppliers that can meet both performance and regulatory constraints. Lecta introduced EraCup Natural Pure with a plant sugar-based barrier intended to be repulpable for paper cup applications, and Perstorp with Goncay Plastik introduced hot cup lids using rPET enabled by heat-resistant additive technology, citing up to 80% post-consumer recycled content. These launches, alongside large retailers and QSRs pushing strawless and redesign initiatives, support additional SKU proliferation in tethered/tamper-evident lids, certified recycled-content cup-lid kits, and coatings that avoid substances under tighter scrutiny in EU and US food-contact frameworks.

Recent Industry Developments

- June 2026: Huhtamaki confirmed a collaboration with Hesburger to supply fiber-based lids for hot and cold beverage cups as a replacement for plastic lids. The collaboration operationalizes fiber lid adoption in high-volume QSR settings and strengthens the supplier position in molded-fiber and plastic-substitution portfolios.

- May 2026: Amcor announced the commercial availability of its PP Revolution portfolio of polypropylene dip cups and lidding solutions for condiments and sauces. The launch expands Amcor's offering in mono-material formats aligned with recycling narratives across foodservice and retail packs.

- September 2024: Huhtamaki became Slush's official sustainability partner and provided recyclable cups for drinks served at the event. The deployment functions as a visible proving ground for recyclable cup formats in high-throughput venues, supporting broader foodservice qualification and customer adoption.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the cups and lids market covers the value of cups and matching lids sold for beverage and foodservice uses, across common materials like paper-based, plastic, foam, and molded fiber. The sizing reflects products supplied into channels such as quick service, institutional, and retail packs.

Scope exclusions: Excludes durable drinkware and long-life reusable containers that are typically sold as consumer goods rather than as packaging or foodservice disposables.

Segmentation Overview

- By Material

- Plastic

- Paper and Paperboard

- Foam (EPS)

- Molded-fiber / Bagasse

- Other Material Types

- By Product Type

- Drinking Cups

- Portion and Packaging Cups

- Lids

- By End-User

- Food and Beverage

- Foodservice

- Retail and E-commerce

- Other End-User

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the demand pool for beverages and away-from-home consumption, and then linking it back to the packaging formats used most often. We referenced public sources such as the US Census Bureau and Bureau of Labor Statistics, the US Food and Drug Administration for food-contact and labeling context, and US International Trade Commission data for trade direction checks on packaging materials and finished articles.

To keep assumptions practical, we also used sources such as UN Comtrade, association websites covering packaging and foodservice topics, peer-reviewed papers on fiber-based and plastic packaging performance, and company annual reports and investor presentations for product mix signals. Where useful, we pulled a paid subscription for company financials and intelligence, and used an import-export shipment-level database to sanity-check scale and flow trends. These sources are illustrative only, and many other public references were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is counted as a cup or lid sale in practice, and how volume shifts between paper-based, plastic, foam, and molded fiber formats across key end users. We spoke with manufacturers, converters, distributors, and large buyers across APAC, EMEA, and the Americas, so the assumptions used in pricing, adoption, and substitution matched what is seen in orders and product specifications.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 41% |

| Mid tier: 48% | Functional/Unit leaders: 43% | EMEA: 34% |

| Smaller Players: 21% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where beverage and foodservice consumption indicators are converted into cup and lid demand by applying format penetration and typical usage rates, then translating that output into value using region- and material-specific pricing. To keep the totals realistic, we corroborate with selective bottom-up approximations, such as sampled average selling price ranges from channel checks multiplied by observed volume bands in key countries.

Inputs used in the model include away-from-home beverage servings, quick-service outlet counts and throughput, material substitution trends (for example, shifts from foam and conventional plastics into paper-based and molded fiber options), average cup size mix, and resin and paper input cost direction as a proxy for pricing movement. When gaps appear for smaller countries or informal channels, we apply proxy ratios from comparable markets and adjust them based on interview feedback.

For forecasting, scenario analysis is used around two common swing factors, the pace of fiber adoption and the impact of regulations on specific single-use formats. We then blend those scenarios into a base case using expert views gathered during primary discussions, and apply final growth rates by region and product type.

Data Validation & Update Cycle

Validation is done in steps, so no single assumption drives the final number. We compare the model output against independent signals such as foodservice spending trends, trade flows for relevant packaging categories, and directional pricing movement, and then investigate any large variances before sign-off.

If an anomaly is found, we re-open the relevant assumptions and re-contact select respondents, especially when the issue is tied to material shifts or sudden pricing changes. Reports are refreshed annually, and interim updates are triggered when a material event occurs, for example a major regulatory change or a sharp input-cost shock. Right before delivery, we run one more pass so clients receive the most up-to-date view available.

Mordor Intelligence's Cups and Lids Market Size Measured Against Other Published Estimates

Published market sizes for cups and lids can vary a lot, even when they appear to cover the same topic. The gaps usually come from differences in what is counted, the year chosen as the starting point, and how pricing is carried forward during the forecast.

In this market, the largest differences are typically driven by whether reusable drinkware and broader rigid packaging items are included, and whether value is reported at the manufacturer level or at a later point in the chain. Some estimates also apply faster price growth or assume a quicker shift to premium fiber formats, which can lift the value even when unit demand grows steadily. The 2026 to 2031 sizing shown here is tied to disposable cups and lids used in food and beverage applications, with pricing and material shifts re-checked during updates, which keeps the scope tighter than broader packaging totals used by some publishers, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 18.34 B (2026) | |

| Global Publisher A | USD 22.09 B (2024) | Uses an earlier base year and a longer forecast window, and the scope is stated broadly as cups and lids packaging, which can pull in adjacent rigid packaging and mixed-use items that are not always counted as foodservice disposables. |

| Packaging Publisher B | USD 27.10 B (2024) | Defines the market as cups and lids packaging and notes disposable and reusable coverage, which can lift the value versus a disposable-focused scope. The higher starting value can also reflect different price points and channel level (later-stage) valuation. |

Taken together, the spread is mainly explained by scope width, the base year used, and how pricing and material mix are handled over time. When definitions are kept consistent and checked against observable demand signals, the market total becomes easier to trace and repeat across updates. This helps users compare growth paths without mixing unlike product pools.

Key Questions Answered in the Report

How large is the cups and lids market in 2026?

The cups and lids market size stood at USD 18.34 billion in 2026 with a 3.37% CAGR outlook to 2031.

Which material is growing fastest?

Paper and paperboard post a 4.55% CAGR due to sustainability regulations and molded-fiber innovations.

Why are lids growing faster than cups?

Spill-proof and tamper-evident designs needed for delivery and strawless formats push lids to a 4.41% CAGR.

Which region offers the best growth prospects?

Asia-Pacific leads with a 4.44% CAGR as QSR chains and coffee culture expand in China and India.

How are regulations affecting plastic cups?

EU and U.S. state bans introduce per-unit fees and reduction targets that lift costs and accelerate material shifts to fiber or recycled PET.

Page last updated on: