Acupuncture Needles Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

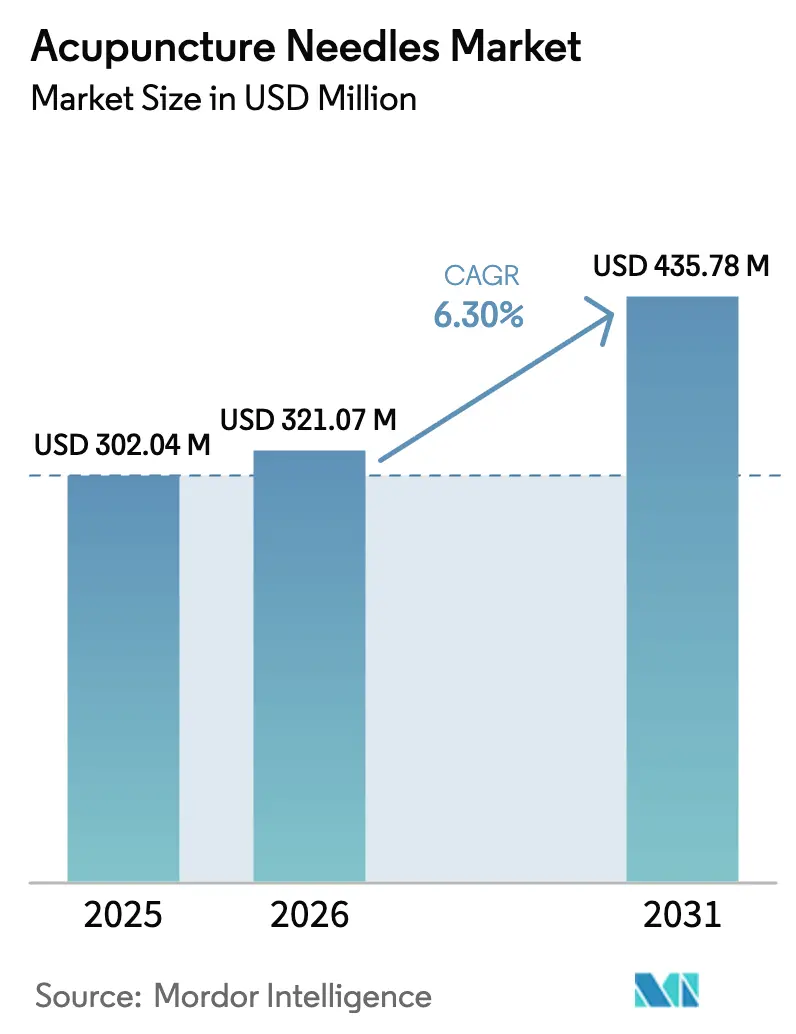

| Market Size (2026) | USD 321.07 Million |

| Market Size (2031) | USD 435.78 Million |

| Growth Rate (2026 - 2031) | 6.30% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acupuncture Needles Market Analysis by Mordor Intelligence

Acupuncture needles market size in 2026 is estimated at USD 321.07 million, growing from 2025 value of USD 302.04 million with 2031 projections showing USD 435.78 million, growing at 6.3% CAGR over 2026-2031. Momentum stems from three converging forces: aging populations that demand non-pharmacological pain relief, clinical evidence that validates acupuncture across musculoskeletal and metabolic conditions, and regulatory moves that embed traditional Chinese medicine into national health systems.[1]Wen-Li Wu et al., “Acupuncture Improves Bone Mineral Density: A Meta-analysis of 2,758 Patients,” Frontiers in Endocrinology, frontiersin.org Rising purchasing power in Asia-Pacific, e-commerce penetration that widens procurement routes, and technological gains in silicone-coated micro-needles also reinforce growth. At the same time, supply-chain hedging by large medical device firms mitigates raw-material volatility and secures volumes against geopolitical shocks. Heightened policy scrutiny of single-use medical waste introduces cost pressure, yet it also encourages R&D in biodegradable or reusable formats, sustaining innovation pipelines within the acupuncture needles market.

Key Report Takeaways

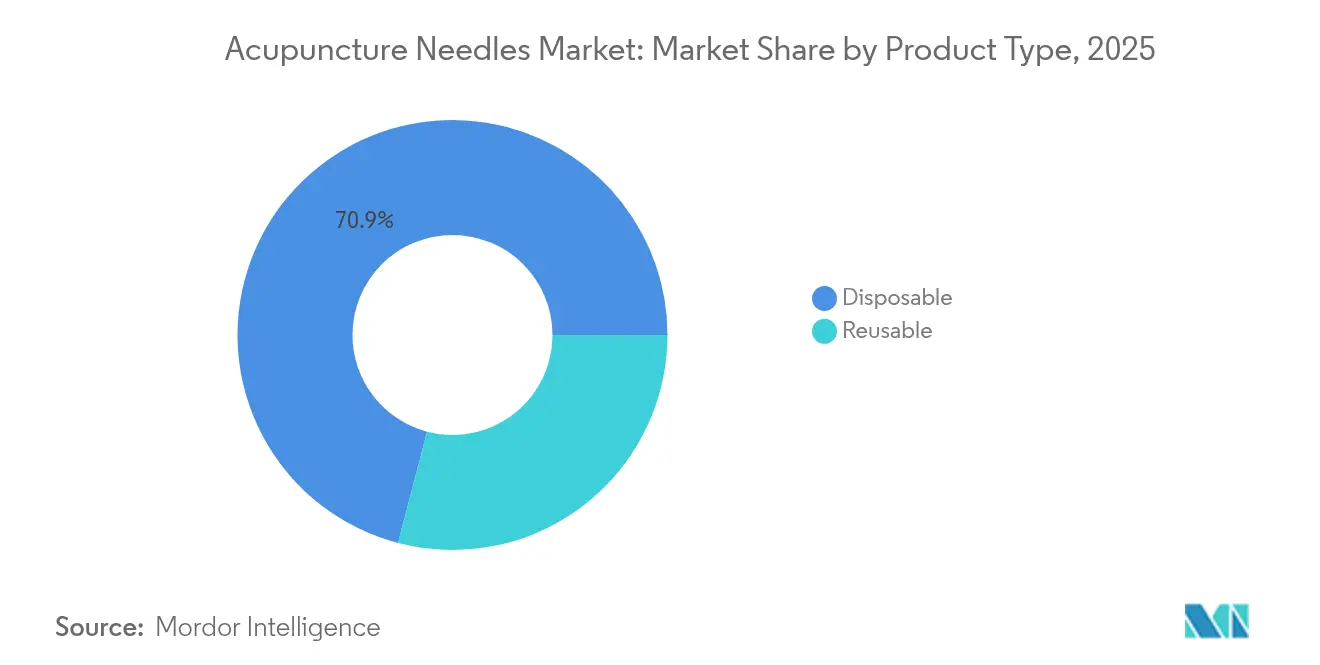

- By product type, disposable needles held 70.92% of acupuncture needles market share in 2025; reusable formats are projected to grow at a 6.79% CAGR through 2031.

- By material, stainless-steel devices commanded 72.96% share of the acupuncture needles market size in 2025, while silver variants are expanding at a 7.05% CAGR.

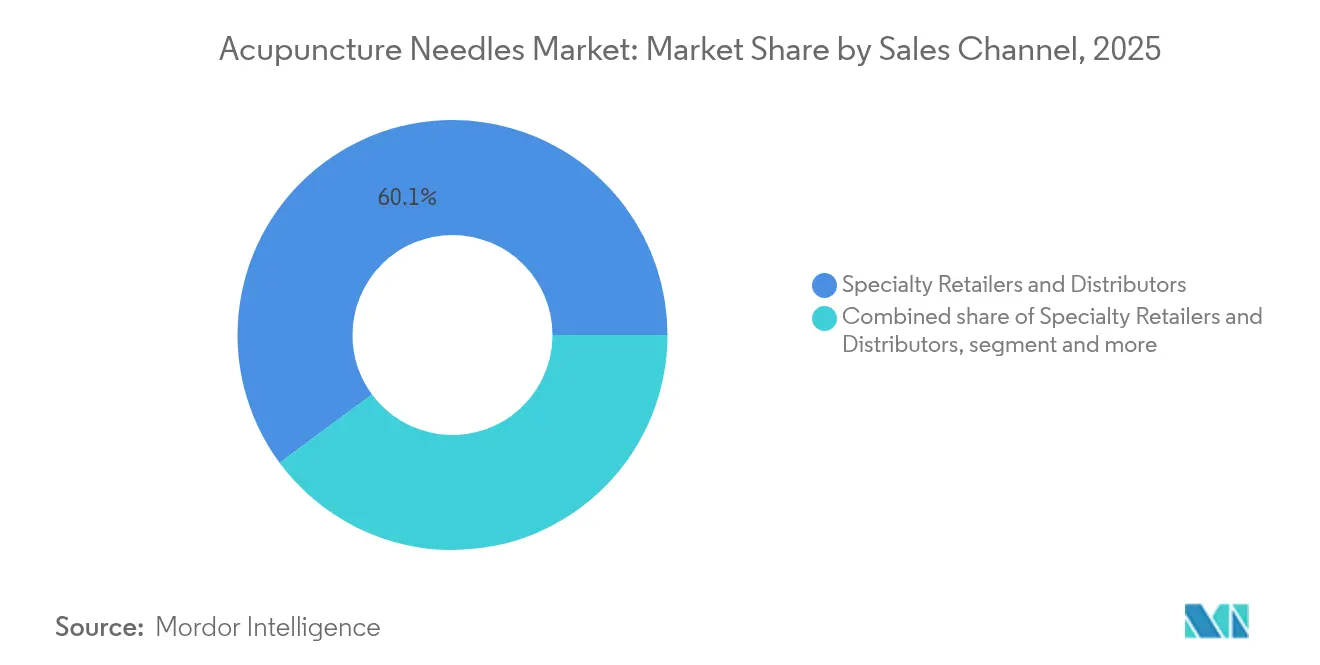

- By sales channel, specialty retailers and distributors controlled 60.12% revenue in 2025, whereas online marketplaces are advancing at an 7.78% CAGR to 2031.

- By end user, specialty and multidisciplinary clinics captured 45.74% of the acupuncture needles market in 2025; the home-care segment is accelerating at a 7.32% CAGR.

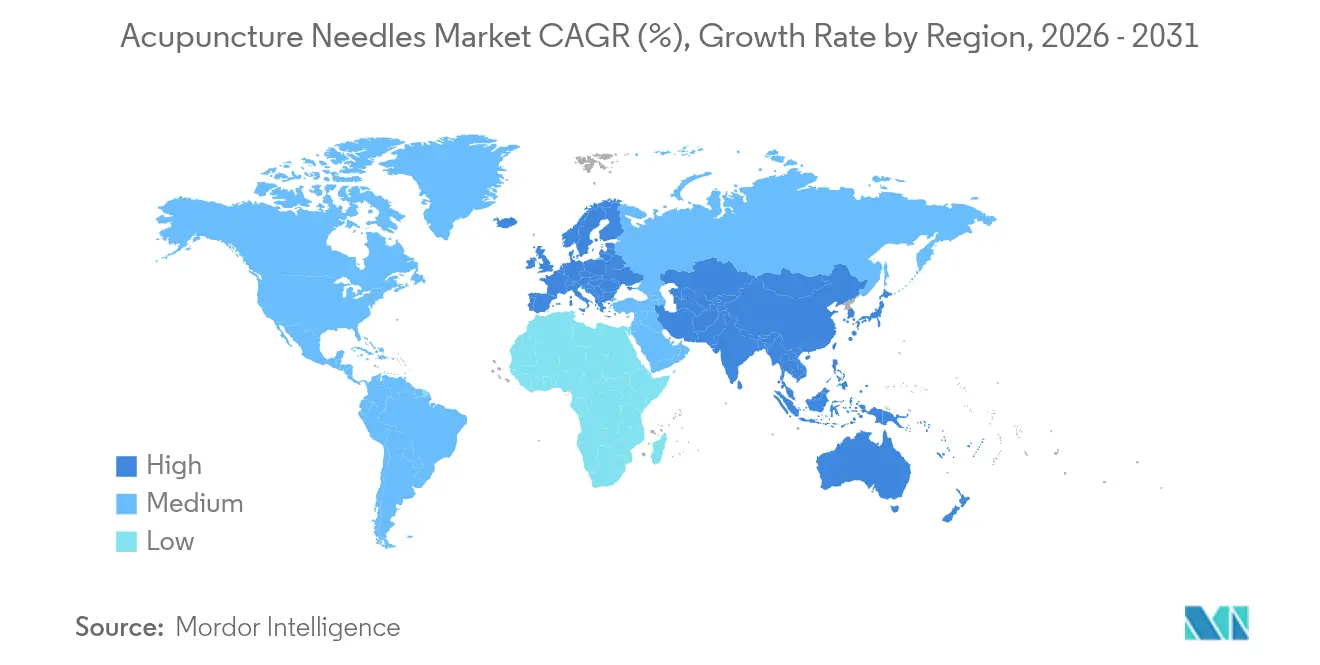

- By geography, Asia-Pacific led with 43.31% market share in 2025; Europe is pacing fastest with a 7.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acupuncture Needles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic pain disorders | +1.5% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Growing geriatric population seeking non-pharmacological therapies | +1.3% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Clinical evidence driving integration into conventional healthcare | +1.2% | North America & EU, with early adoption in urban centers | Medium term (2-4 years) |

| Miniaturised, silicone-coated micro-needles enabling self-treatment | +1.7% | Global, with early gains in developed markets | Short term (≤ 2 years) |

| Surge in cross-border e-commerce of Traditional Chinese Medicine devices | +1.2% | APAC to global, with strong growth in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Pain Disorders

Chronic pain now affects 21.45% of European adults, intensifying demand for non-opioid therapies that the acupuncture needles market readily serves.[2]Nils Georg Niederstrasser et al., “Chronic Pain Prevalence in Europe,” PAIN, journals.lww.comEpidemiological modelling projects a continuing climb in neck and low-back pain through 2044, especially among middle-aged groups in high-income economies. Health authorities respond by issuing guidelines that insert acupuncture into first-line pain pathways, shifting volume toward medical-grade needles. Updated ICD-11 codes sharpen diagnostic accuracy by 63.2%, streamlining reimbursement processes and shortening referral cycles. The 2024 Medicare decision to pay for chronic low-back-pain acupuncture solidified public-insurance precedents that commercial payers increasingly mirror. Collectively, these dynamics underpin recurring procurement budgets for acupuncture needles across hospitals and outpatient clinics.

Growing Geriatric Population Seeking Non-Pharmacological Therapies

Meta-analysis of eight randomized trials involving 469 seniors confirmed that acupuncture improved gastrointestinal motility in functional constipation cases, an outcome that elevates its relevance for aging cohorts. Parallel reviews covering 79 studies linked acupuncture to measurable gains in cerebral blood flow and cognitive performance among patients with vascular cognitive impairment—findings that widen the therapeutic envelope beyond pain. As Japan and South Korea enter super-aged status, national health insurers finance integrative medicine programs that bulk-purchase needles for community clinics. Polypharmacy worries amplify patient preference for non-drug options, positioning the acupuncture needles market as a durable supplier to geriatric-care pathways.

Clinical Evidence Driving Integration into Conventional Healthcare

Peer-reviewed work in 2024 mapped acupuncture’s modulation of neurotransmitter release, synaptic plasticity, and inflammatory cascades, providing molecular clarity that garners acceptance from Western clinicians. Neuroimaging confirmed needle-induced changes in the default-mode and central-executive networks, reinforcing objective validity for chronic-pain and cognitive indications. A meta-analysis of 2,758 patients showed statistically significant bone mineral density improvements versus standard pharmacotherapy, bolstering osteoporosis adjunct protocols. Publication volume from China, the United States, and Korea continues to surge, normalizing acupuncture within evidence-based practice and creating steady demand for single-use, sterile supplies.

Miniaturized, Silicone-Coated Micro-Needles Enabling Self-Treatment

Advances in bidirectional-drawing lithography have yielded hyaluronic-acid microneedles sized in micrometers, improving patient comfort while ensuring precise insertion depth. Metallic micro-needles fabricated from surgical-grade stainless steel or titanium deliver robust mechanical strength essential for home-use devices. FDA classifies acupuncture needles as Class II items; this clear pathway allows innovators to launch consumer-grade kits tethered to telehealth coaching platforms. As wearable health technologies proliferate, self-administration broadens the addressable base beyond clinics, lifting the acupuncture needles market into adjacent wellness channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of alternative pain-management modalities | -0.8% | Global, with highest impact in developed markets | Medium term (2-4 years) |

| Limited insurance reimbursement in many countries | -0.7% | North America & EU, with varying impact by region | Long term (≥ 4 years) |

| Supply-chain volatility of surgical-grade stainless-steel wire | -0.9% | Global, with highest impact on cost-sensitive segments | Short term (≤ 2 years) |

| Escalating regulation on single-use needle waste management | -0.6% | EU & developed markets, expanding to emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Alternative Pain-Management Modalities

Digital therapeutics, wearable transcutaneous-stimulation gadgets, and targeted drug-delivery implants intensify competition. Health systems often gravitate toward technologies with embedded data analytics, an edge that traditional needles lack without digital augmentation. New non-opioid pharmaceuticals with improved safety profiles also compress practitioner mindshare. Despite this competitive field, the ongoing opioid crisis keeps acupuncture relevant as a complement, rather than a casualty, in multimodal pain programs.

Limited Insurance Reimbursement in Many Countries

While US Medicare now pays for chronic low-back-pain acupuncture, coverage elsewhere remains patchy, leading to significant out-of-pocket spending that dampens procedure volumes. Private insurers frequently bundle needle costs inside provider fees rather than reimbursing as separate supply items, capping revenue visibility for manufacturers. Legislation such as HR 1477 aims to broaden federal coverage, yet political timelines remain uncertain. Until reimbursement parity emerges, growth in the acupuncture needles market will lean heavily on self-pay segments and emerging-market clinics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposable Formats Anchor High-Volume Demand

Disposable needles accounted for 70.92% of the acupuncture needles market in 2025, cementing their status as the default option for infection control mandates. FDA single-use labeling removes sterilization complexity for practitioners and curtails liability exposure. Continuous investment in automated line technology lifts unit throughput and dampens per-piece cost, preserving share even amid raw-material shifts.

Reusable formats, though smaller, are set to climb 6.79% annually to 2031. Cost-sensitive clinics in India, Brazil, and parts of Southeast Asia view sterilizable needles as viable under tight reimbursement ceilings. Some specialized segments favour reusable gold or silver variants for premium procedures. These dual trends suggest an enduring two-tier structure within the acupuncture needles market size: high-volume disposables for mainstream care and slower-moving reusables for economic or specialty niches.

Environmental scrutiny introduces an emerging variable. In Europe, directives on single-use plastics are prompting R&D into biodegradable polymer handles and recyclable stainless-steel shafts. If successful, such eco-centric designs could ease regulatory pressure while retaining the convenience of disposability. Reusable advocates, meanwhile, refine autoclave-ready alloys to shorten turnover cycles, indicating technology flowers on both ends of the spectrum within the acupuncture needles market.

By Material: Stainless Steel Retains Scale Advantage

Stainless-steel products represented 72.96% of the acupuncture needles market size in 2025 owing to corrosion resistance, biocompatibility, and vast established supply lines. Suppliers benefit from mature melting and wire-drawing ecosystems concentrated in China, Japan, and Germany, delivering cost leadership that smaller premium-material makers struggle to match. This heft buffers price swings in nickel or chromium, sustaining margin stability.

Silver needles are growing fastest at 7.05% CAGR through 2031. Their intrinsic antimicrobial properties appeal to dermatology and cosmetic indications, where infection avoidance carries premium willingness to pay. Gold and titanium variants serve hypoallergenic or MRI-compatible applications, forming micro-niches within the broader acupuncture needles market.

Supply-chain risk remains a headline issue. Surgical-grade stainless-steel wire prices spiked twice in 2024 following geopolitical trade frictions, exposing over-reliance on a handful of smelters. In response, firms such as BD announced USD 10 million domestic capacity additions to hedge import dependence and assure lead times. Material diversification—coated alloys, polymer composites, or hybrid microneedles—offers product-line resilience and price hedging in the acupuncture needles industry.

By Sales Channel: Digital Platforms Widen Reach

Specialty distributors held 60.12% of global sales in 2025 because they navigate device-registration bureaucracy and maintain just-in-time inventory near clinical customers. Yet online marketplaces are projected to post an 7.78% CAGR, the highest among channels, as practitioners embrace one-click procurement and drop-shipping convenience. Chinese exporters ride this wave, listing factory-direct SKUs on Amazon, Alibaba, and dedicated B2B portals that undercut local middlemen.

Regulatory complexity tempers e-commerce scale, especially in Europe where the new EU Medical Device Regulation requires seller registration and vigilance reporting even for cross-border shipments. Compliance hurdles create an entry moat that well-capitalized platforms can clear faster, potentially tipping share in their favour. Direct-to-physician portals run by manufacturers themselves boost margin capture and feed valuable usage analytics back into R&D cycles, anchoring a virtuous loop within the acupuncture needles market.

By End User: Home-Care Adoption Gains Traction

Clinics—traditional Chinese medicine centers, physiotherapy offices, and integrative pain units—commanded 45.74% of demand in 2025, mirroring their frontline role in therapeutic delivery. Hospitals remain heavy users because inpatient and ambulatory departments integrate acupuncture into standardized post-operative and chronic-pain pathways.

The home-care slice, while smaller, is slated for 7.32% CAGR on the back of telehealth coaching apps and FDA-cleared self-treatment kits. Hyaluronic-acid dissolving microneedles and compact spring-loaded applicators simplify technique-sensitive insertions, cutting learning curves for laypersons. Aging-at-home policies in Europe, plus chronic-pain prevalence among working-age populations in the United States, give this modality a broad user base. Over the forecast horizon, rising home-use volumes will heighten focus on user-friendly packaging and multilingual instructions across the acupuncture needles market.

Geography Analysis

Asia-Pacific held 43.31% of the acupuncture needles market in 2025 thanks to cultural alignment, domestic device production, and state incentives that integrate traditional Chinese medicine into primary care. China alone supplies more than 80% of global stainless-steel acupuncture needle exports, leveraging scale economies and vertically integrated steel mills. Demand also stems from Japan and South Korea, where super-aged societies foster constant need for non-pharmacological therapies.

Europe is pacing at a 7.61% CAGR up to 2031. Harmonized EU regulations now demand supply-interruption notifications, raising quality bars but also shielding incumbents from low-end imports. Germany, France, and the UK anchor hospital-based integrative clinics, while Scandinavian health systems reimburse acupuncture for musculoskeletal and migraine indications. Combined, these policies enlarge the regional acupuncture needles market share despite reimbursement disparities between public and private insurers.

North America retains a sizeable base, buoyed by Medicare’s decision to cover acupuncture for chronic low-back pain. BD’s Nebraska and Connecticut expansions target domestic self-reliance after pandemic-era supply shocks, reinforcing local availability. Canada follows with province-level pilot programs that fold acupuncture into opioid-reduction strategies. Mexico, meanwhile, offers cost-competitive manufacturing that may serve as a near-shore alternative for US distributors, enhancing supply-chain optionality in the acupuncture needles market.

Competitive Landscape

The acupuncture needles market remains moderately fragmented. With the leading manufacturers holding a significant share of global revenues, mid-tier firms find opportunities to establish their own geographic or material-specific niches. Chinese producers dominate volume through cost leadership and government export incentives, supplying private-label needles to Western distributors.

Western incumbents differentiate via premium metals and rigorous post-market surveillance. BD’s USD 10 million capacity investment exemplifies a strategy of vertical integration plus localization to mitigate trade risks. European specialist EUROPIN was bought by private-equity firm Gilde Healthcare in 2024, signaling rising investor appetite for consolidation plays that can stitch together regional footprints.

Innovation focal points include silicone-coated surfaces that lower insertion force, biodegradable handles that address waste regulations, and smart applicators with depth-control sensors. Start-ups utilizing direct-to-consumer e-commerce challenge legacy distributors, offering subscription boxes bundled with tele-coaching. Competitive intensity is therefore shifting from pure price wars to encompassing sustainability credentials, digital integration, and local-for-local supply strategies within the acupuncture needles industry.

Acupuncture Needles Industry Leaders

SEIRIN Corporation

3B Scientific GmbH

Suzhou Hualun Medical Appliance

AcuMedic Ltd.

Lojer Oy (Hegu)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: A Medicine case report documented full lesion resolution in an elderly herpes-zoster patient after four sessions of subcutaneous acupuncture, with no postherpetic neuralgia at 12-month follow-up.

- January 2025: FDA issued a warning letter to Robbins Instruments over the Dermo-Jet needle-less injector marketed without proper clearance, underscoring the agency’s enforcement stance on acupuncture-related devices.

- October 2024: A systematic review in PAIN Reports detailed neurobiological mechanisms that underpin acupuncture analgesia, strengthening its evidence base for acute and chronic indications.

- July 2024: EU Regulation 2024/1860 came into force, requiring device makers to notify authorities of supply interruptions, thereby tightening quality oversight for acupuncture needle suppliers.

Global Acupuncture Needles Market Report Scope

Acupuncture needles are specialized, sterile, thin needles made primarily of stainless steel. They are inserted into the skin at specific acupoints to stimulate healing and balance the body's energy. These needles play a crucial role in acupuncture therapies, which are increasingly recognized for their effectiveness in treating various health conditions.

The acupuncture needles market is segmented by type, material, sales channel, end-user, and geography. By type, the market is segmented as disposable and reusable. By material, the market is segmented as stainless steel, silver, and others. By sales channel, the market is bifurcated into online and retail. By end-user, the market is segmented as hospitals, clinics, and others. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. For each segment, the market sizing and forecasts have been done based on value (in USD).

| Disposable |

| Reusable |

| Stainless-Steel |

| Silver |

| Gold |

| Others |

| Online Marketplaces |

| Specialty Retailers & Distributors |

| Direct-to-Practitioner (B2B) |

| Hospitals |

| Specialty & Multidisciplinary Clinics |

| Home-care & Self-administration |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Disposable | |

| Reusable | ||

| By Material | Stainless-Steel | |

| Silver | ||

| Gold | ||

| Others | ||

| By Sales Channel | Online Marketplaces | |

| Specialty Retailers & Distributors | ||

| Direct-to-Practitioner (B2B) | ||

| By End User | Hospitals | |

| Specialty & Multidisciplinary Clinics | ||

| Home-care & Self-administration | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the acupuncture needles market in 2026?

The market is worth USD 321.07 million in 2026 and is projected to reach USD 435.78 million by 2031.

Which region leads the acupuncture needles market?

Asia-Pacific holds the largest position with 43.31% share in 2025, benefiting from manufacturing scale and cultural acceptance.

What segment is growing fastest by sales channel?

Online marketplaces are expanding at an 7.78% CAGR over 2026-2031 as cross-border e-commerce simplifies global procurement.

Why are stainless-steel needles so dominant?

Stainless steel offers cost efficiency, corrosion resistance, and mature manufacturing infrastructure, giving it 72.96% share in 2025.

How is technology reshaping home-care use of acupuncture needles?

Silicone-coated micro-needles and FDA-cleared self-treatment kits enable safe at-home application, driving a 7.32% CAGR in the home-care segment.

What regulatory changes affect suppliers in Europe?

EU Regulation 2024/1860 mandates supply-interruption notifications, raising compliance requirements but safeguarding against device shortages.

Page last updated on: