Insulin Syringes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

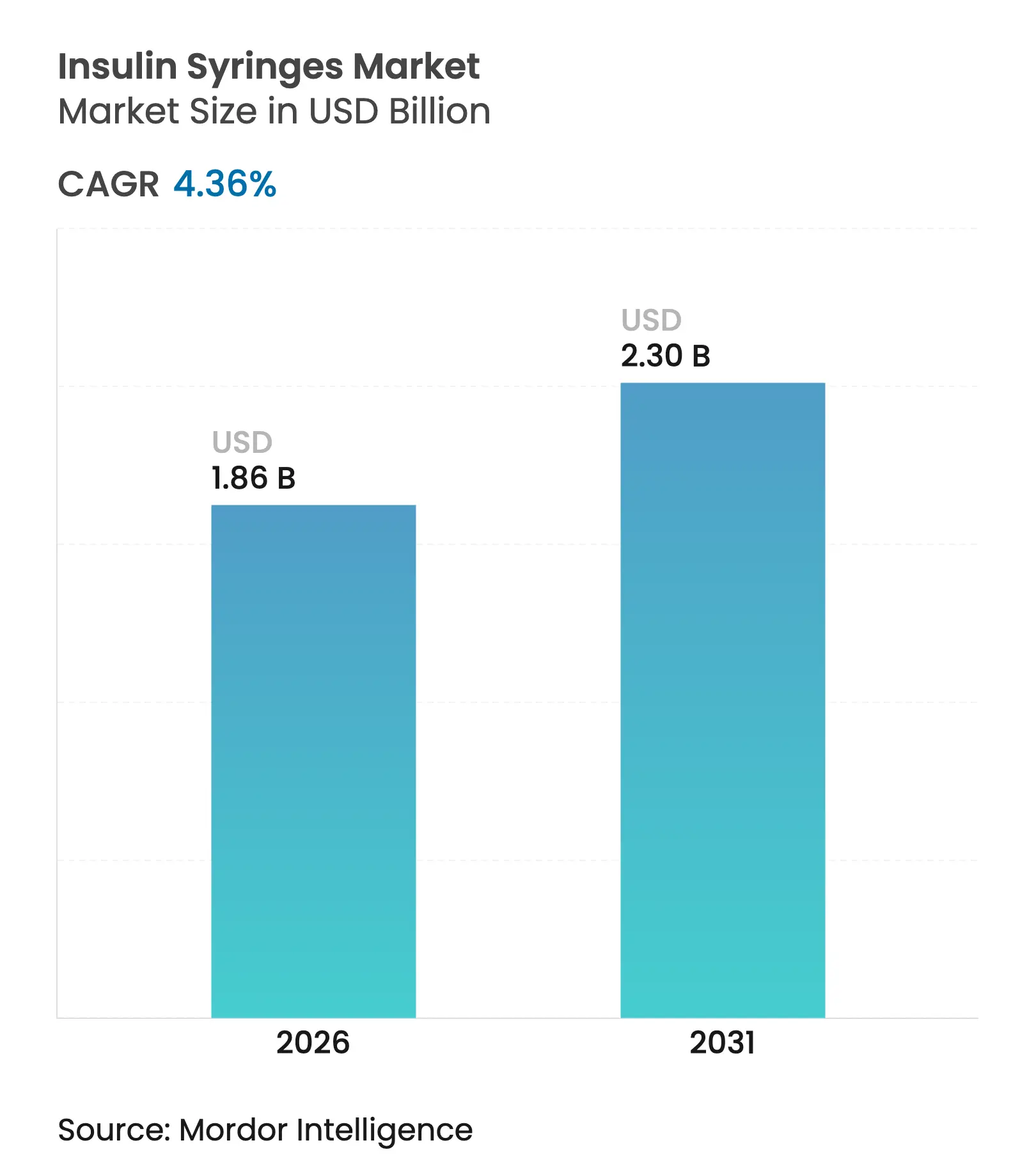

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 2.3 Billion |

| Growth Rate (2026 - 2031) | 4.36 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

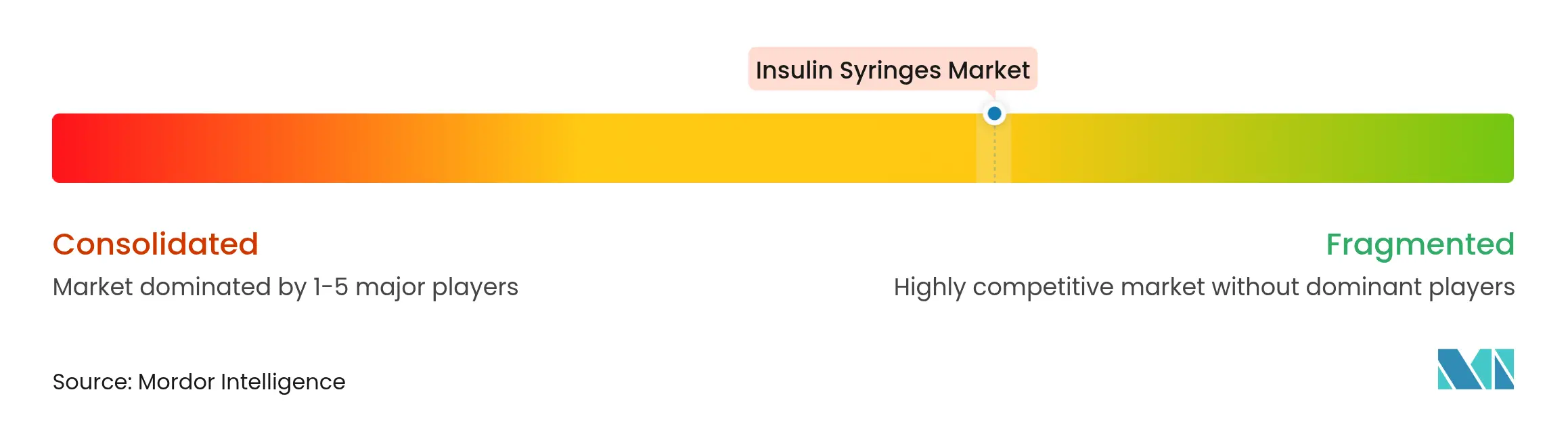

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Insulin Syringes Market Analysis by Mordor Intelligence

Insulin syringes market size in 2026 is estimated at USD 1.86 billion, growing from 2025 value of USD 1.78 billion with 2031 projections showing USD 2.3 billion, growing at 4.36% CAGR over 2026-2031. Heightened diabetes prevalence, cost advantages over advanced devices, and dependable reimbursement programs keep the insulin syringes market resilient despite technology disruption. Safety-engineered designs, concentrated insulin formulations, and domestic manufacturing initiatives further strengthen product demand across developed and emerging economies. Meanwhile, sustainability regulations and escalating competition from pens and pumps temper growth. The insulin syringes market nonetheless benefits from entrenched clinical familiarity, large installed bases, and continuous new-patient inflows that ensure steady replacement cycles.

Key Report Takeaways

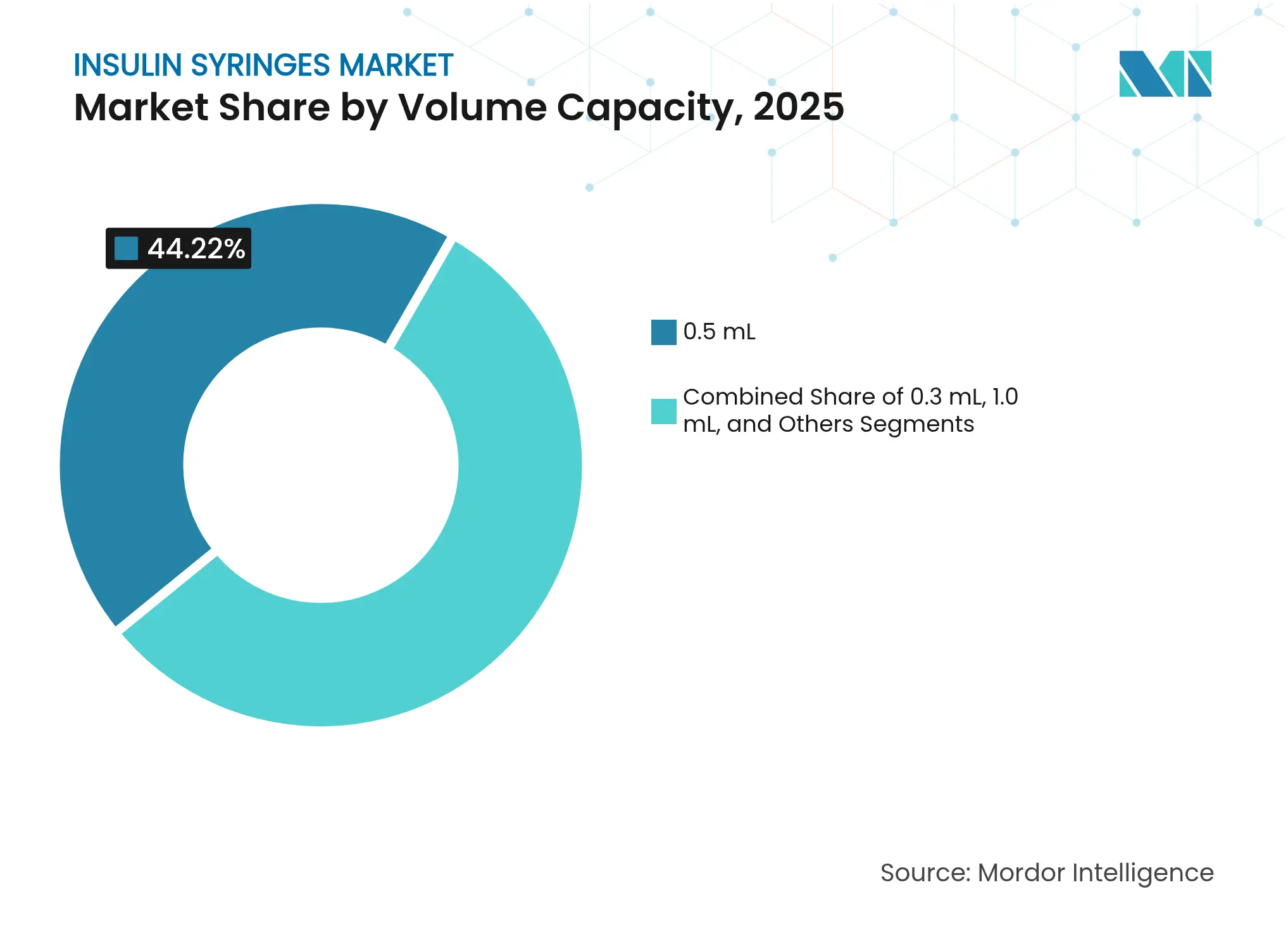

- By volume capacity, the 0.5 mL segment led with 44.22% of insulin syringes market share in 2025, while 1.0 mL units are forecast to expand at a 5.09% CAGR to 2031

- By insulin concentration, U-100 formulations accounted for 69.65% share of the insulin syringes market size in 2025 and U-500 is set to grow at a 5.08% CAGR through 2031

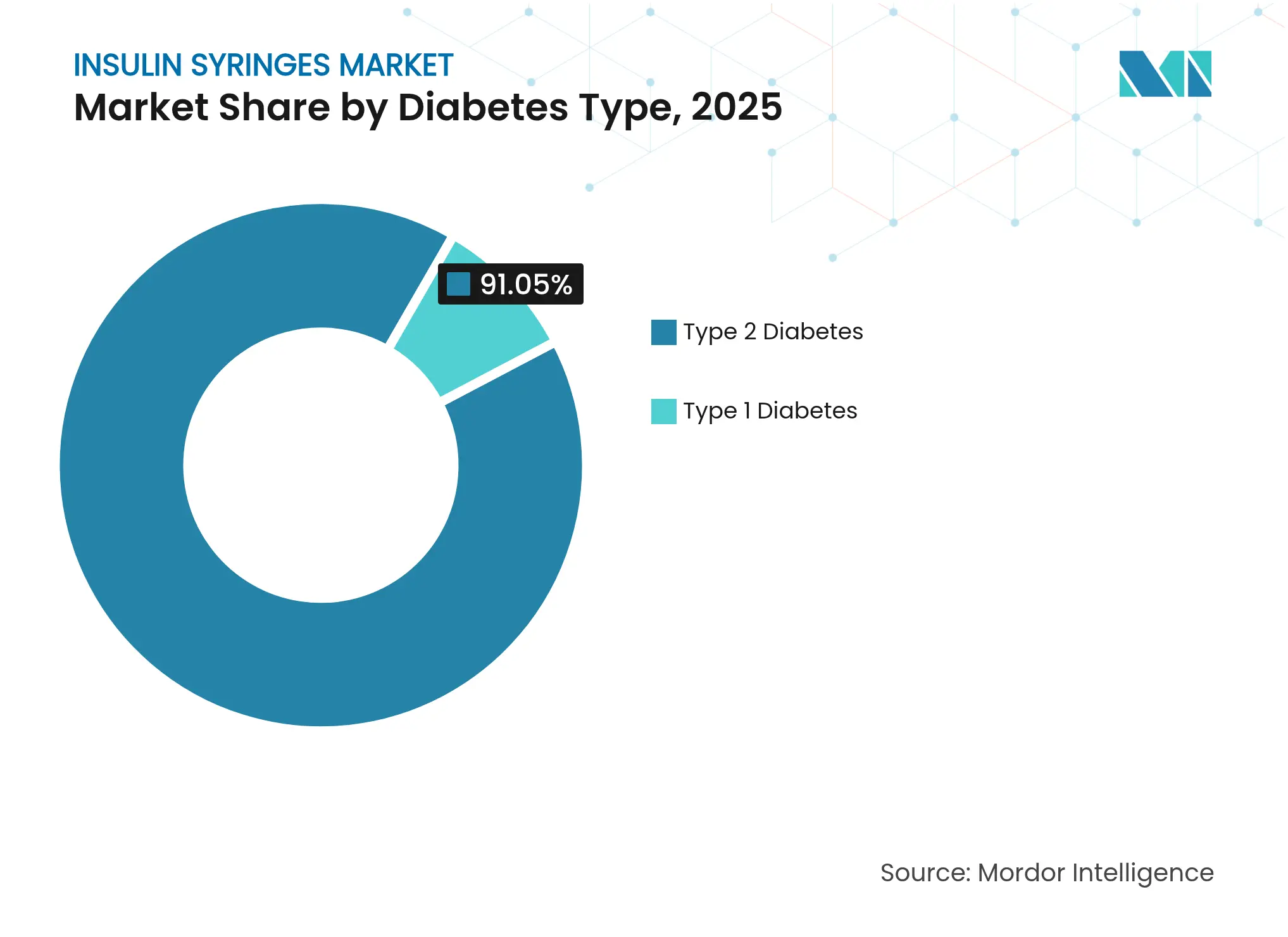

- By diabetes type, Type 2 applications dominated with 91.05% share of the insulin syringes market size in 2025; Type 1 shows the fastest 5.15% CAGR between 2026-2031

- By end user, hospitals and clinics held 47.25% of the insulin syringes market share in 2025, whereas home-care settings will rise at a 5.21% CAGR to 2031

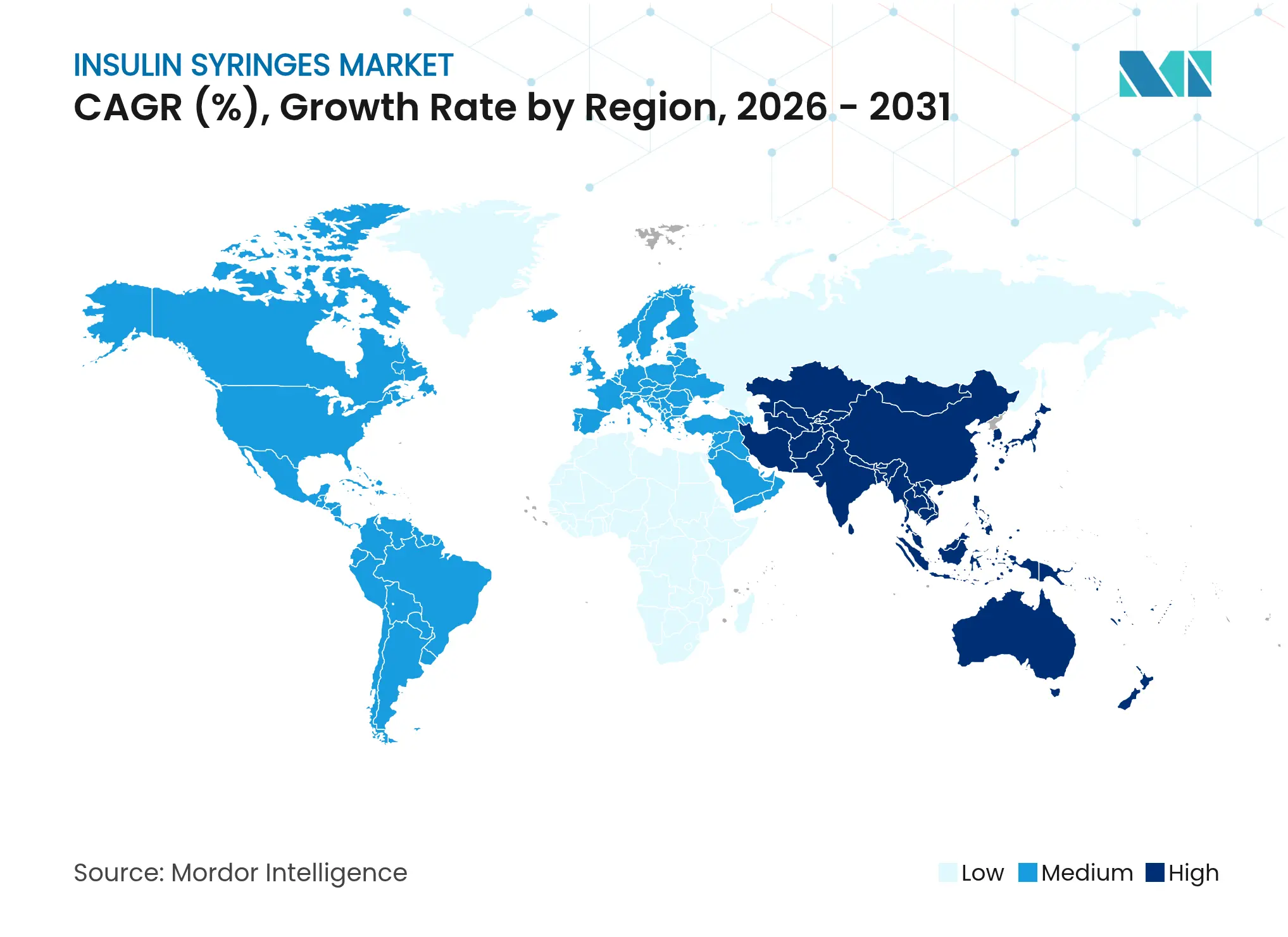

- By geography, North America commanded 39.85% revenue share in 2025 and Asia-Pacific is poised for a 5.19% CAGR over the forecast period

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insulin Syringes Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising global diabetes prevalence

Rising global diabetes prevalence

| +1.8% | Global, with highest impact in APAC and MEA | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.8%

|

Geographic Relevance

:

Global, with highest impact in APAC and MEA

|

Impact Timeline

:

Long term (≥ 4 years)

|

Low-cost preference in LMICs

Low-cost preference in LMICs

| +1.2% | APAC core, MEA, Latin America | Medium term (2-4 years) | |||

Reimbursement & procurement programs

Reimbursement & procurement programs

| +0.8% | North America, Europe, select APAC markets | Medium term (2-4 years) | |||

Safety-engineered syringe innovations

Safety-engineered syringe innovations

| +0.4% | North America, Europe, developed APAC | Short term (≤ 2 years) | |||

Veterinary diabetes demand surge

Veterinary diabetes demand surge

| +0.2% | North America, Europe, urban APAC | Long term (≥ 4 years) | |||

Open-source / 3-D printed auto-injectors

Open-source / 3-D printed auto-injectors

| +0.1% | Global, early adoption in developed markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising global diabetes prevalence

More than 800 million adults live with diabetes, quadrupling 1990 levels and underpinning sustained demand for insulin delivery devices [1]World Health Organization, "Urgent action needed as global diabetes cases increase four-fold over past decades," who.int. Diabetes mortality among 15-49-year-olds in low- and middle-income countries is projected to climb over 30% by 2030 compared with 2019, locking in decades-long insulin needs. In India, cases could surge from 77 million to 134.2 million by 2045, with 57% currently undiagnosed, signaling vast untapped patient pools. Younger onset means longer treatment horizons, strengthening the insulin syringes market worldwide. Aging populations in developed economies add another layer of stable, long-term consumption.

Low-cost preference in LMICs

Traditional syringes remain the most affordable insulin option as pen devices often retail far above estimated production costs [2]MSF Access Campaign, "Estimated Sustainable Cost-Based Prices for Diabetes Medicines," msfaccess.org. China’s volume-based procurement lowered median insulin prices by 42% and saved USD 2.85 billion in its first year, demonstrating how policy drives cost efficiency that favors syringes. Studies in Ethiopia show only 53.8% of patients view diabetes care as affordable, underscoring persistent cost barriers. Competitive tendering and generic production lock price-sensitive markets into syringe-centric care pathways.

Reimbursement & procurement programs

Medicare caps patient insulin outlays at USD 35 per month under the Inflation Reduction Act, guaranteeing predictable expenditure for US beneficiaries. The 2026 CMS rule extends similar protections across Part D plans, sustaining volume demand for covered syringes [3]Centers for Medicare & Medicaid Services, "Medicare Coverage of Diabetes Supplies," cms.gov. India’s price‐control measures on off-patent antidiabetics reinforce this policy trend. Standard HCPCS codes A4252-A4259 ease claims processing, ensuring swift reimbursement flows that preserve provider preference for syringes.

Safety-engineered syringe innovations

Insulin injections account for roughly 20% of needlestick injuries among healthcare workers. Devices with retractable needles and protective shields reduce occupational hazards and command premium pricing. Becton Dickinson is expanding US capacity for safety-engineered units by 40% after a USD 10 million investment in 2024. Asia-Pacific regulators are tightening injury-prevention standards, further accelerating uptake of advanced syringes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shift toward pens & pumps

Shift toward pens & pumps

| -1.4% | North America, Europe, developed APAC | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.4%

|

Geographic Relevance

:

North America, Europe, developed APAC

|

Impact Timeline

:

Medium term (2-4 years)

|

Single-use plastic & waste regulations

Single-use plastic & waste regulations

| -0.6% | Europe, select North American states | Long term (≥ 4 years) | |||

Price pressure from bulk tenders

Price pressure from bulk tenders

| -0.4% | Global, highest impact in LMIC procurement | Short term (≤ 2 years) | |||

Resin supply-chain vulnerability

Resin supply-chain vulnerability

| -0.3% | Global manufacturing, concentrated in Asia | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Shift toward pens & pumps

Automated delivery platforms generated notable gains in 2024, with Insulet recording USD 2 billion revenue and a 22% annual rise, reflecting strong consumer preference for convenience and connectivity. Tandem Diabetes Care shipped 25% more pumps year-on-year, evidencing accelerating migration away from manual syringes. Embecta’s syringe sales fell 7.8%, quantifying share erosion. The technology divide widens as affluent users upgrade, trimming syringe demand in advanced economies.

Single-use plastic & waste regulations

Healthcare generates roughly 34 lb of waste per day, one-quarter being plastic, spurring regulators to impose recycling and reduction mandates. Sweden’s circular-economy rules require on-site microwave disinfection and pyrolysis recycling for medical plastics, raising compliance costs. Early-stage biodegradable polymers such as polylactic acid show promise, yet sterilization and mechanical hurdles delay mass deployment. These policies may compress margins and accelerate product redesign toward eco-friendlier materials.

Segment Analysis

By Volume Capacity: Precision Dosing Drives Differentiation

The 0.5 mL format captured 44.22% of insulin syringes market share in 2025, reflecting clinical preference for balanced capacity and dosing accuracy. The 1.0 mL variant is advancing at a 5.09% CAGR and will increasingly anchor high-dose regimens built around concentrated insulin. Manufacturers benefit from economies of scale in these two mainstream sizes, enabling competitive pricing and global availability. The 0.3 mL format remains vital for pediatric care where precise micro-dosing reduces hypoglycemia risk. Emerging 2.0 mL and 3.0 mL options cater to veterinary and specialty therapies, adding incremental revenue but limited volume.

Rising uptake of U-500 insulin intensifies demand for larger barrel sizes that maintain accuracy at smaller unit gradations. Terumo’s Rika platform, slated to reach 20-25% US share by mid-2025, underscores the strategy of leveraging capacity specialization to gain competitive edge. As healthcare pivots toward personalized medicine, dosing precision becomes paramount, reinforcing the centrality of volume-calibrated syringes in treatment protocols. The insulin syringes market therefore balances high-volume standardization with targeted innovation to meet niche clinical needs.

Note: Segment shares of all individual segments available upon report purchase

By Insulin Concentration: U-500 Emergence Challenges Dominance

U-100 formulations retained 69.65% share of the insulin syringes market size in 2025, cementing their status as the global therapeutic default. Nonetheless, U-500 volumes are expanding at a 5.08% CAGR as clinicians treat severe insulin resistance with higher concentration regimens that reduce injection burden. The shift requires syringes calibrated for finer measurement increments to avoid dosing errors, encouraging production of specialty devices. Intermediate concentrations such as U-200 and U-300 occupy a transitional role, providing flexibility for patients scaling therapy intensity.

Regulatory support for broader insulin choice, evidenced by the February 2025 approval of Merilog insulin-aspart-szjj, enriches the clinical toolkit and stimulates demand for compatible syringes. As physicians adopt concentrated formulations, manufacturers gain an opportunity to command premium pricing for precision-engineered equipment. Nonetheless, entrenched U-100 volumes ensure lasting economies of scale that will continue to anchor the insulin syringes market across all care settings.

By Diabetes Type: Type 1 Growth Outpaces Prevalence

Type 2 diabetes accounted for 91.05% of the insulin syringes market size in 2025 owing to sheer prevalence and the disease’s gradual shift toward insulin therapy. However, Type 1 applications will register a 5.15% CAGR to 2031, outpacing total market expansion. Improved diagnostic protocols, earlier intervention, and longer life expectancy elevate per-capita syringe consumption among Type 1 patients who require lifelong multiple daily injections. Emerging evidence supports intensive insulin therapy for pediatric cohorts, locking in decades of product replacement cycles.

In emerging markets, the vast reservoir of undiagnosed Type 2 cases represents a future demand catalyst once health systems scale screening programs. Conversely, robust Type 1 management infrastructure in developed regions secures recurring revenues through sophisticated dosing regimens. This dual-engine dynamic underpins steady growth across diverse economic environments, sustaining the insulin syringes market even as technology alternatives gain share at the premium end.

Note: Segment shares of all individual segments available upon report purchase

By End User: Home-Care Transformation Accelerates

Hospitals and clinics still represented 47.25% of insulin syringes market share in 2025, anchoring sales in institutional channels. Yet home-care is projected to climb by 5.21% CAGR, driven by patient self-management, insurer cost-containment goals, and remote monitoring technologies. Medicare’s USD 35 monthly cap makes at-home therapy financially predictable, enhancing adherence and favoring standard syringe purchases. Telehealth, continuous glucose monitors, and app-based coaching fortify clinical oversight without requiring in-person visits.

Long-term care facilities and specialty diabetes centers complete the end-user mix, addressing elderly and complex-case populations. As healthcare systems pivot toward value-based models, syringes remain integral thanks to low acquisition costs, familiar workflows, and straightforward supply logistics. The insulin syringes market therefore evolves alongside digital health, preserving relevance by aligning with decentralization trends and supporting patient empowerment.

Geography Analysis

North America commanded 39.85% revenue in 2025, propelled by comprehensive Medicare benefits, robust private insurance coverage, and continuous product innovation. Becton Dickinson’s USD 10 million US capacity expansion reflects confidence in resilient regional demand and the strategic imperative for domestic production after FDA advisories on certain foreign-made syringes. Canada’s publicly funded healthcare and Mexico’s growing middle class further buttress continental uptake.

Asia-Pacific is the fastest-growing region with a 5.19% CAGR, catalyzed by India’s escalating diabetes burden and China’s procurement reforms that slash prices and widen access. Japan’s long-standing insurance coverage for self-injection therapy ensures stable baseline consumption. Expanding local manufacturing, evidenced by Nipro’s North Carolina plant, illustrates how regional diversification strategies cut freight costs and enhance supply security for Asia-linked players. Europe maintains steady momentum through universal health systems but faces mounting pressure from single-use-plastic directives that may spur material innovation or product redesign. Sweden’s circular-economy pilot underscores the continent’s leadership on sustainable healthcare procurement. South America and Middle East & Africa trail but hold substantial upside as diabetes awareness campaigns, donor programs, and economic development gradually raise therapy penetration. The geographic spread thus balances mature, high-value markets with emerging, high-growth territories that collectively propel the insulin syringes market forward.

Competitive Landscape

Market Concentration

The insulin syringes industry is moderately fragmented. Market leaders leverage manufacturing scale, regulatory expertise, and distribution reach to defend share. Becton Dickinson increased US output of safety-engineered syringes by 40% in 2024, safeguarding supply chain resilience and speeding delivery to healthcare systems. FDA scrutiny of certain Chinese plastic syringes prompted renewed domestic sourcing, which can confer quality-assurance advantages to North American and European producers.

Technology differentiation centers on retractable needles, low dead-space barrels, and ergonomic designs that minimize dosing errors. Firms are also eyeing the veterinary segment after canine insulin degludec trials achieved 76% excellent glycemic control, broadening addressable demand.

Nipro’s forthcoming Greenville facility underpins a dual-region strategy serving both North American and Asian markets while cutting transit emissions. Competitive positioning increasingly rewards firms that align product portfolios with safety mandates, sustainability goals, and integration with digital diabetes ecosystems.

Insulin Syringes Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: FDA cleared Merilog (insulin-aspart-szjj), the first rapid-acting insulin biosimilar, in 3 mL pen and 10 mL vial formats to broaden patient access.

- February 2025: Nipro announced its first North American manufacturing site in Greenville, North Carolina, targeting advanced devices for diabetes and kidney care.

- January 2025: BD committed USD 10 million to add syringe production lines in Connecticut and Nebraska, boosting safety-engineered capacity by over 40%.

- September 2024: BD commercially launched Neopak XtraFlow glass prefillable syringes and expanded French manufacturing capacity sevenfold for premium injection solutions.

Table of Contents for Insulin Syringes Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising global diabetes prevalence

- 4.2.2Low-cost preference in LMICs

- 4.2.3Reimbursement & procurement programs

- 4.2.4Safety-engineered syringe innovations

- 4.2.5Veterinary diabetes demand surge

- 4.2.6Open-source / 3-D printed auto-injectors

- 4.3Market Restraints

- 4.3.1Shift toward pens & pumps

- 4.3.2Single-use plastic & waste regulations

- 4.3.3Price pressure from bulk tenders

- 4.3.4Resin supply-chain vulnerability

- 4.4Regulatory Landscape

- 4.5Porters Five Forces Anaysis

- 4.5.1Bargaining Power of Suppliers

- 4.5.2Bargaining Power of Consumers

- 4.5.3Threat of New Entrants

- 4.5.4Threat of Substitute Products

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Volume Capacity

- 5.1.10.3 mL

- 5.1.20.5 mL

- 5.1.31.0 mL

- 5.1.4Others

- 5.2By Insulin Concentration

- 5.2.1U-100

- 5.2.2U-500

- 5.2.3Others

- 5.3By Diabetes Type

- 5.3.1Type 1 Diabetes

- 5.3.2Type 2 Diabetes

- 5.4By End User

- 5.4.1Hospitals and Clinics

- 5.4.2Home-care Settings

- 5.4.3Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Becton, Dickinson and Company

- 6.3.2Nipro Corporation

- 6.3.3Hindustan Syringes & Medical Devices

- 6.3.4Terumo Corporation

- 6.3.5Cardinal Health

- 6.3.6Ultimed, Inc.

- 6.3.7Arkray, Inc.

- 6.3.8Owen Mumford

- 6.3.9Retractable Technologies

- 6.3.10Sol-Millennium Medical

- 6.3.11Ypsomed AG

- 6.3.12B. Braun Melsungen AG

- 6.3.13Exelint International

- 6.3.14Allison Medical

- 6.3.15Smiths Medical

- 6.3.16Medline Industries

- 6.3.17Poly Medicure Ltd.

- 6.3.18Gerresheimer AG

- 6.3.19AdvaCare Pharma

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Volume Capacity

- 0.3 mL

- 0.5 mL

- 1.0 mL

- Others

- 0.3 mL

- By Insulin Concentration

- U-100

- U-500

- Others

- U-100

- By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

- Type 1 Diabetes

- By End User

- Hospitals and Clinics

- Home-care Settings

- Others

- Hospitals and Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Insulin Syringes Baseline Inspires Confidence

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 1.78 B | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 1.92 B | Global Consultancy A | Includes pens and needle-free injectors, applies higher ASP drawn from blended device category | ||

USD 1.66 B | Industry Journal B | Assumes universal single-use behavior, omits online pharmacy channel, uses 2024 average FX rate |