Hyperphosphatemia Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

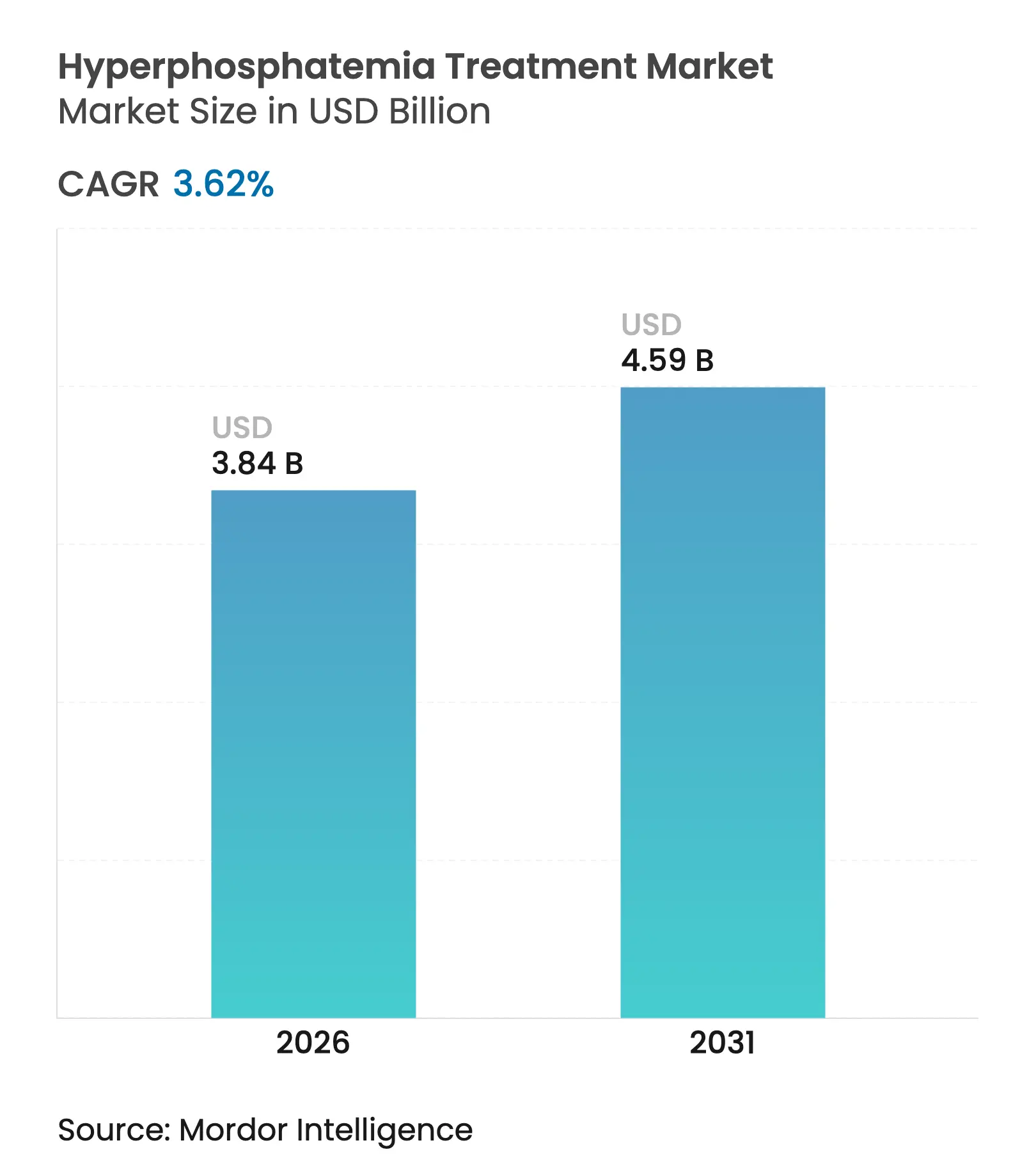

| Market Size (2026) | USD 3.84 Billion |

| Market Size (2031) | USD 4.59 Billion |

| Growth Rate (2026 - 2031) | 3.62 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Hyperphosphatemia Treatment Market Analysis by Mordor Intelligence

The hyperphosphatemia treatment market size is expected to grow from USD 3.71 billion in 2025 to USD 3.84 billion in 2026 and is forecast to reach USD 4.59 billion by 2031 at 3.62% CAGR over 2026-2031. Growing dialysis prevalence, Medicare’s bundled-payment overhaul, and rising early-stage chronic kidney disease (CKD) detection continue to expand the addressable patient base. Innovation momentum is shifting from traditional binders toward absorption-inhibition and microbiome modulation, helped by regulatory frameworks that now reward clinical outcomes rather than pill volume. Manufacturers are redesigning product portfolios to align with lower pill-burden preferences and to integrate digital adherence support. Simultaneously, regional procurement policies, especially in Asia Pacific, are opening procurement channels for cost-effective iron and synbiotic options that meet both phosphate and anemia targets. Competitive differentiation is therefore converging on dual-indication efficacy, ease of administration, and the ability to thrive under facility-level cost controls.

Key Report Takeaways

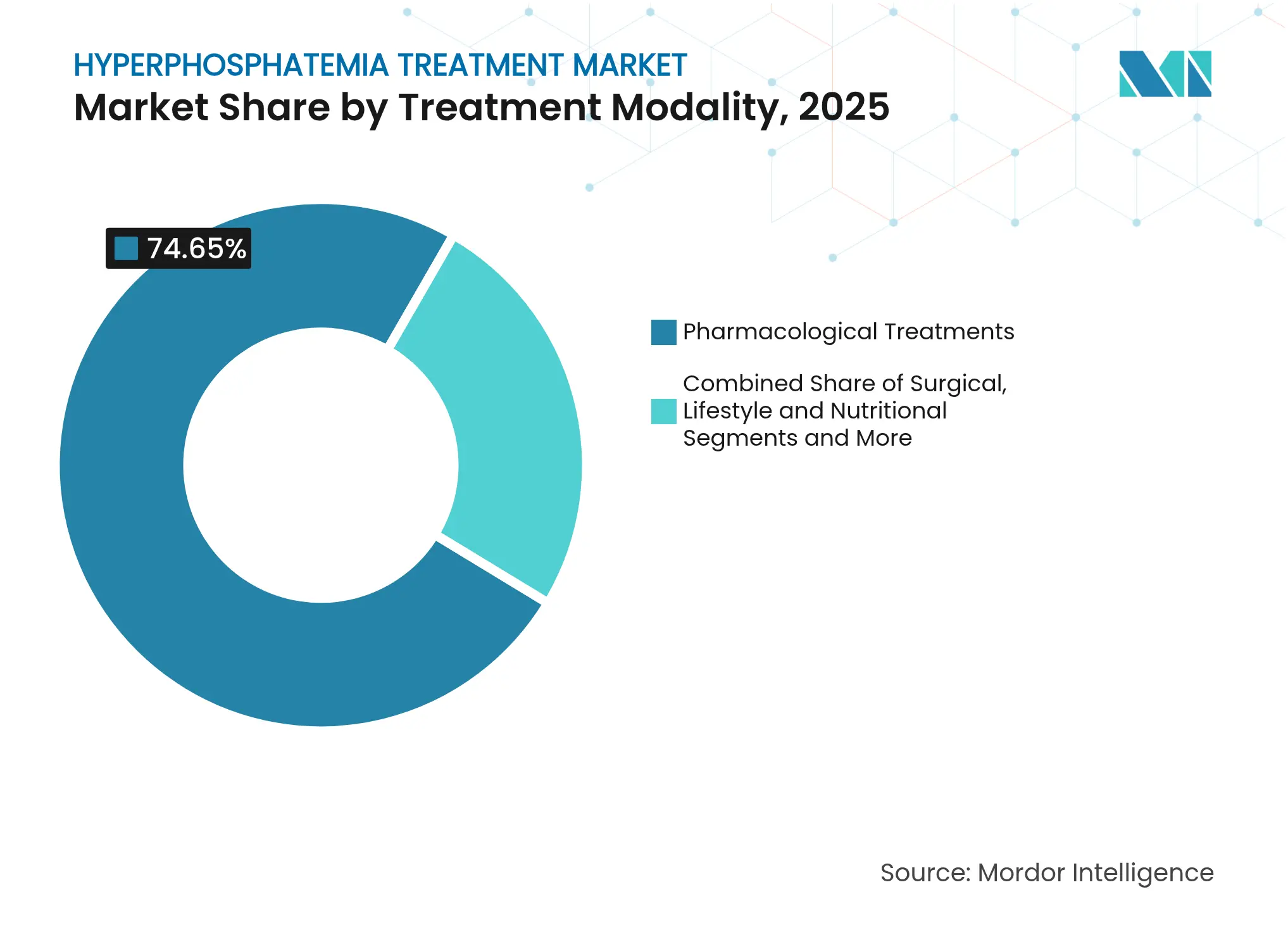

- By treatment modality, pharmacological products led with 74.65% hyperphosphatemia treatment market share in 2025, while biologic & microbiome-based therapies are projected to grow at a 6.93% CAGR through 2031.

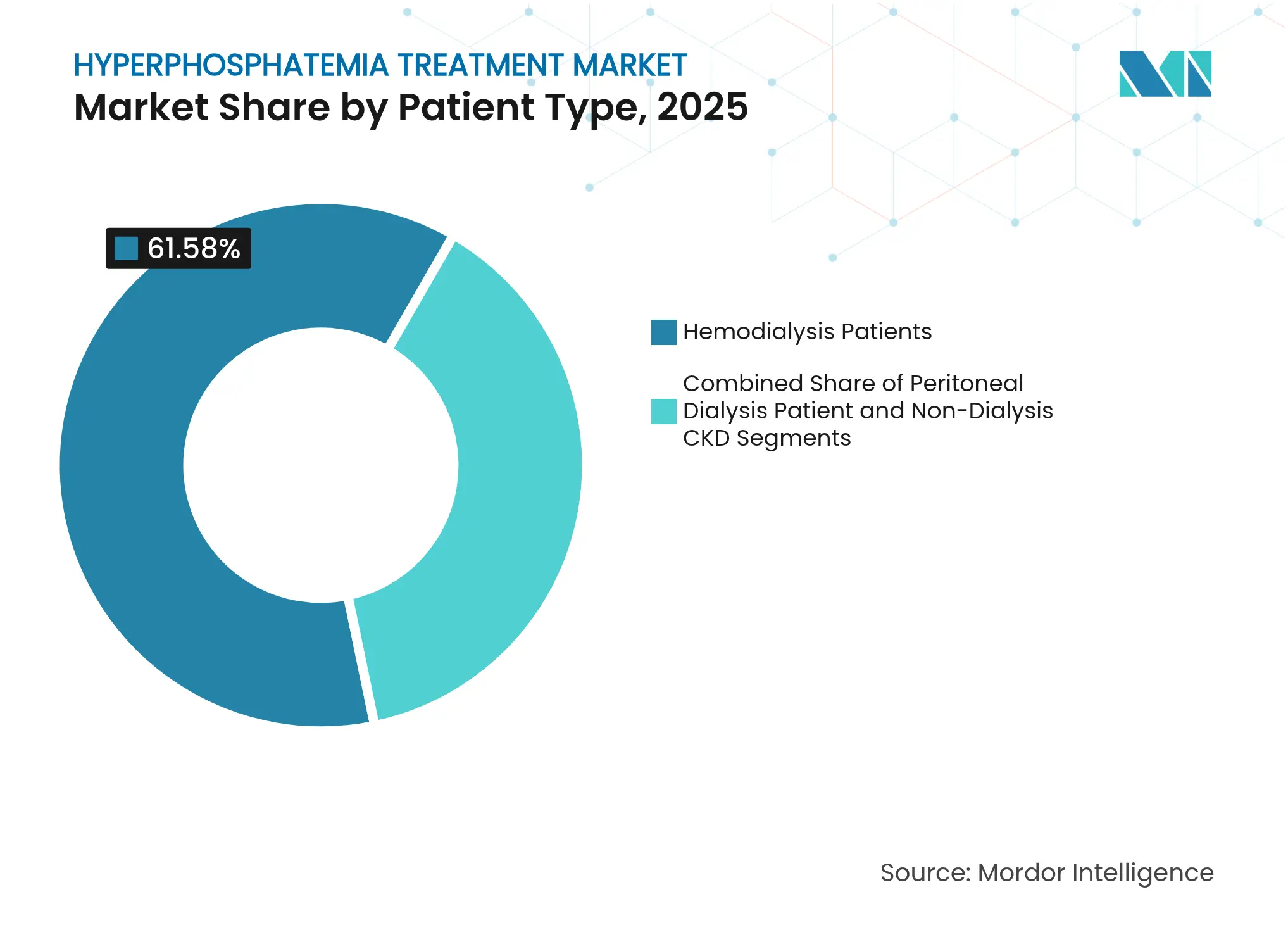

- By patient type, hemodialysis accounted for 61.58% of the hyperphosphatemia treatment market size in 2025; non-dialysis CKD is forecast to expand at 6.58% CAGR to 2031.

- By end user, hospitals & specialty clinics held 44.02% revenue share in 2025, whereas home-care settings are advancing at a 6.22% CAGR through 2031.

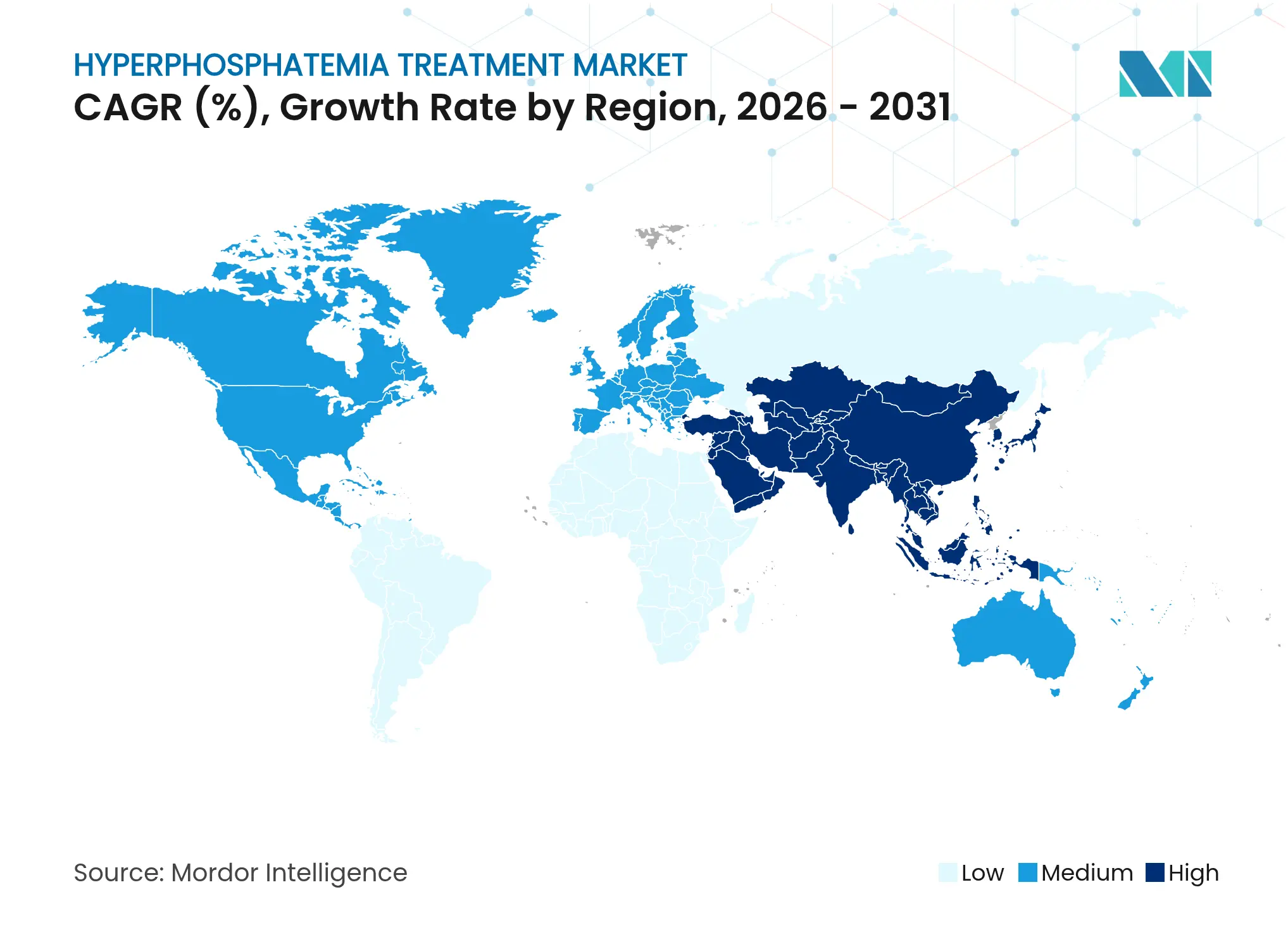

- By geography, North America captured 33.12% of the hyperphosphatemia treatment market size in 2025, while Asia Pacific records the highest projected CAGR at 5.37% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hyperphosphatemia Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of CKD & ESRD

Rising prevalence of CKD & ESRD

| +0.8% | Global with concentration in North America & APAC | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+0.8%

|

Geographic Relevance

:

Global with concentration in North

America & APAC

|

Impact Timeline

:

Long term (≥ 4 years)

|

Growing dialysis population &

aging demographics

Growing dialysis population &

aging demographics

| +0.6% | Global; most acute in developed markets | Long term (≥ 4 years) | |||

Regulatory push for serum-phosphate

targets

Regulatory push for serum-phosphate

targets

| +0.4% | North America & EU; extending to APAC | Medium term (2-4 years) | |||

Launch of low-pill-burden iron

binders

Launch of low-pill-burden iron

binders

| +0.3% | Global; early uptake in North America | Short term (≤ 2 years) | |||

Home-dialysis growth driving

convenient treatments

Home-dialysis growth driving

convenient treatments

| +0.2% | North America & EU; emerging in APAC | Medium term (2-4 years) | |||

Digital diet-tracking apps improving

adherence

Digital diet-tracking apps improving

adherence

| +0.1% | Technology-enabled markets worldwide | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of CKD & ESRD

Incident CKD cases rose at a 1.82% annual rate to 18.9 million in 2019 and have accelerated through 2025 as hypertension and diabetes continue to climb in emerging economies.[1]Yafeng Li, “Epidemiological Shifts in Chronic Kidney Disease: A 30-Year Global and Regional Assessment,” BMC Public Health, bmcpublichealth.biomedcentral.comWider diagnostic coverage means more patients reach nephrology clinics earlier, increasing demand for phosphate control therapies that prevent cardiovascular morbidity. Serum phosphorus levels among U.S. hemodialysis patients also trended upward over the last decade, underscoring an urgent need for better-performing products.[2]Murilo Guedes, “Serum Phosphorus Level Rises in US Hemodialysis Patients Over the Past Decade,” Kidney Medicine Journal, kidneymedicinejournal.org

Growing Dialysis Population & Aging Demographics

Longer survival on dialysis platforms enlarges the chronic user base, and a higher average patient age complicates adherence because polypharmacy and frailty reduce tolerance for multi-tablet regimens. European assisted peritoneal programs illustrate how home modalities cater to older patients who need simplified treatment routines.[3]Simon J. Davies, “Addressing the Inequity of Access to Home Dialysis in Europe,” BMC Nephrology, bmcnephrol.biomedcentral.com

Regulatory Push for Serum-Phosphate Targets

The 2025 U.S. End-Stage Renal Disease Prospective Payment System bundles oral binders into a facility payment and awards a USD 36.41 Transitional Drug Add-on Payment Adjustment, pivoting incentives toward target achievement rather than script volume. Parallel FDA guidance funnels all therapies through prescription channels, sidestepping the unregulated OTC space.[4]U.S. Food & Drug Administration, “21 CFR 310.542—OTC Drug Products Containing Active Ingredients for Hyperphosphatemia,” ecfr.gov

Launch of Low-Pill-Burden Iron Binders

Iron-based agents such as sucroferric oxyhydroxide achieve 80% compliance versus 53.3% for lanthanum carbonate while simultaneously correcting anemia, enabling single-product management of two CKD sequelae. Early U.S. uptake reflects the immediate benefit under value-based reimbursement.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

GI side-effects & pill burden

GI side-effects & pill burden

| −0.5% | Global; intensified in elderly groups | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

−0.5%

|

Geographic Relevance

:

Global; intensified in elderly

groups

|

Impact Timeline

:

Long term (≥ 4 years)

|

Reimbursement gaps for novel binders

Reimbursement gaps for novel binders

| −0.3% | Emerging markets and cost-sensitive regions | Medium term (2-4 years) | |||

Limited patient adherence to diet

restrictions

Limited patient adherence to diet

restrictions

| −0.2% | Global with cultural variation | Long term (≥ 4 years) | |||

Lanthanum ore supply volatility

Lanthanum ore supply volatility

| −0.1% | Products using lanthanum worldwide | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

GI Side-Effects & Pill Burden

Tenapanor triggers gastrointestinal events in up to 53% of users, and traditional binders require multiple meal-time doses, leaving 70% of dialysis patients outside target phosphate thresholds. Patient surveys show 79% favor reduced-pill options even at equivalent efficacy.

Reimbursement Gaps for Novel Binders

Shifting payment responsibility from Medicare Part D to facility budgets constrains access to branded agents in many U.S. programs, and similar funding gaps across developing markets perpetuate the use of low-cost calcium binders despite inferior control.

Segment Analysis

By Treatment Modality: Pharmacological Dominance Faces Microbiome Disruption

Pharmacological options controlled 74.65% of 2025 revenue. Within this category, iron-based and absorption-inhibitor classes are eroding the share of bulky calcium binders. Biologic & microbiome candidates expand at 6.93% CAGR, backed by pre-clinical data showing synbiotics reduce both serum phosphate and parathyroid hormone levels. The hyperphosphatemia treatment market size for biologic & microbiome agents is set to reach meaningful commercial thresholds as the first products exit late-phase trials after 2027.

Tenapanor’s 2023 approval confirmed that targeting intestinal sodium-phosphate co-transporters can supplant binding models. Iron binders, namely ferric citrate, pair phosphate control with anemia correction, appealing to payers seeking bundled clinical benefits. Pipeline small-molecule inhibitors and nutrition-formulated low-phosphate meals add further competitive layers, suggesting that the hyperphosphatemia treatment market will diversify beyond binders before 2030.

Note: Segment shares of all individual segments available upon report purchase

By Patient Type: Non-Dialysis CKD Emerges as Growth Catalyst

Hemodialysis patients represented 61.58% revenue in 2025, supported by well-reimbursed in-clinic protocols. Yet non-dialysis CKD shows the highest CAGR at 6.58%, indicating an emerging shift toward prophylactic intervention before mineral imbalance manifests. The hyperphosphatemia treatment market share in hemodialysis will slowly dilute as earlier-stage therapy adoption widens.

Preventive prescribing hinges on diet education and once-daily agents that minimize burden, a fit for primary-care management. In dialysis cohorts, aging demographics heighten adherence challenges, accelerating the move to low-pill iron or absorption-inhibitor options. Home-dialysis expansion further aligns with this pattern by empowering patients to self-administer regimens suitable for remote monitoring.

Note: Segment shares of all individual segments available upon report purchase

By End User: Home-Care Settings Drive Treatment Innovation

Hospitals & specialty clinics owned 44.02% revenue in 2025, but home-care settings grow fastest at 6.22% CAGR. Digital connectivity tools such as Baxter’s Sharesource cut technique failure risk by 77%, enabling safe phosphate management outside clinics. As a result, the hyperphosphatemia treatment market size attributed to home-care will expand steadily through 2031.

Remote monitoring platforms auto-capture adherence data, allowing clinicians to adjust dosing without physical visits. This ecosystem favors formulations stable at room temperature, available in blister packs, and endorsed by bundled reimbursement policies that reward lower facility utilization.

Geography Analysis

North America maintained leadership with 33.12% of 2025 revenue, driven by Medicare coverage and an active clinical-trial environment. The region supports rapid uptake of novel mechanisms, evident from tenapanor’s commercial rollout that generated USD 15.2 million in Q1 2024 sales. Strong pay-for-performance models incentivize adoption of agents capable of tighter control, positioning the hyperphosphatemia treatment market in the United States as a bellwether for pricing strategies elsewhere.

Europe follows a patient-centric path, emphasizing home modalities to curb long-term system costs. Assisted peritoneal dialysis initiatives are narrowing access disparities, and cost-effectiveness assessments favor dual-benefit iron binders when they demonstrate reduced hospitalization. The hyperphosphatemia treatment market size for European home programs is set to outpace hospital channels as national procurement frameworks emphasize total-care budgets.

Asia Pacific records the fastest CAGR at 5.37% through 2031, propelled by expanding dialysis capacity and escalating CKD prevalence. Direct treatment cost per renal-replacement patient averages USD 23,358, highlighting the financial weight of disease management. Governments are therefore piloting bundled purchasing of iron and generic binders, creating volume-driven opportunities for manufacturers. Digital adherence tools are also penetrating select urban markets to mitigate physician-shortage constraints and reinforce treatment compliance.

Competitive Landscape

Market Concentration

Market concentration is moderate. Established binder suppliers defend share through broad portfolios but face price compressions under the new U.S. payment bundle. Ardelyx demonstrated how first-in-class absorption inhibitors can capture traction despite entrenched incumbents. Meanwhile, Unicycive’s June 2025 Complete Response Letter shows that manufacturing robustness is a non-negotiable gatekeeper for market entry.

Strategic moves increasingly marry pharmaceuticals with service layers. Baxter’s plan to spin off its kidney care unit into Vantive signals a push toward vertically integrated renal ecosystems that bundle devices, drugs, and digital oversight. Start-ups in microbiome or synbiotic niches seek out manufacturing alliances early to navigate quality requirements and to access the scale necessary for bundled-payment economics. In parallel, group-purchasing organizations such as Premier are locking in multi-year supply contracts to secure price stability for high-volume facilities.

Hyperphosphatemia Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA issued a Complete Response Letter to Unicycive Therapeutics for oxylanthanum carbonate citing third-party manufacturing deficiencies, prompting a shift to a secondary site for corrective action.

- June 2025: Alebund Pharmaceuticals completed database lock on a pivotal phase 3 trial of AP301, an oral iron binder that met its primary endpoint in dialysis patients.

- May 2025: Unicycive Therapeutics confirmed an upcoming FDA decision date for oxylanthanum carbonate in dialysis-dependent CKD.

- November 2024: CMS finalized inclusion of oral-only phosphate binders in the ESRD bundled payment, adding a USD 36.41 per-member-per-month Transitional Drug Add-on Payment.

Table of Contents for Hyperphosphatemia Treatment Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of CKD & ESRD

- 4.2.2Growing Dialysis Population & Aging Demographics

- 4.2.3Regulatory Push For Serum-Phosphate Targets

- 4.2.4Launch Of Low-Pill-Burden Iron Binders

- 4.2.5Home-Dialysis Growth Driving Convenient Treatments

- 4.2.6Digital Diet-Tracking Apps Improving Adherence

- 4.3Market Restraints

- 4.3.1GI Side-Effects & Pill Burden

- 4.3.2Reimbursement Gaps For Novel Binders

- 4.3.3Limited Patient Adherence To Diet Restrictions

- 4.3.4Lanthanum Ore Supply Volatility

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Treatment Modality

- 5.1.1Pharmacological Treatments

- 5.1.1.1Phosphate Binders

- 5.1.1.1.1Calcium-Based Binders

- 5.1.1.1.2Non-Calcium Binders

- 5.1.1.2NHE3 Inhibitors (Tenapanor)

- 5.1.1.3Nicotinamide & Emerging Small-Molecules

- 5.1.2Interventional & Device-Based

- 5.1.2.1Conventional In-Center Hemodialysis

- 5.1.2.2Home Hemodialysis Systems

- 5.1.2.3Peritoneal Dialysis Solutions & Kits

- 5.1.2.4Adsorptive/Column-Based Phosphate Removal Devices

- 5.1.3Surgical / Procedural

- 5.1.3.1Parathyroidectomy

- 5.1.3.2Combined Parathyroid–Thyroid Procedures

- 5.1.4Lifestyle & Nutritional

- 5.1.4.1Phosphate-Restriction Diet Programs & Meal Services

- 5.1.4.2Medical Nutrition (Low-P Formulas, Enteral)

- 5.1.4.3Digital Diet-Tracking & Tele-nutrition Platforms

- 5.1.5Biologic & Microbiome-Based

- 5.1.5.1Synbiotic / Probiotic PAO Therapy

- 5.1.5.2Engineered Microbes / Enzyme Capsules

- 5.2By Patient Type

- 5.2.1Hemodialysis Patients

- 5.2.2Peritoneal Dialysis Patients

- 5.2.3Non-Dialysis CKD (Stages 3–4)

- 5.3By End User

- 5.3.1Hospitals & Specialty Clinics

- 5.3.2Dialysis Centers (Chains & Independent)

- 5.3.3Home-Care Settings & Home Hemodialysis Users

- 5.3.4Research & Academic Institutes

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Sanofi

- 6.3.2Fresenius Medical Care

- 6.3.3Akebia Therapeutics

- 6.3.4Ardelyx

- 6.3.5Baxter International

- 6.3.6B. Braun Melsungen

- 6.3.7Kyowa Kirin

- 6.3.8Takeda Pharmaceutical

- 6.3.9Astellas Pharma

- 6.3.10Mitsubishi Tanabe Pharma

- 6.3.11Kissei Pharmaceutical

- 6.3.12Lupin

- 6.3.13Unicycive Therapeutics

- 6.3.14Amgen

- 6.3.15Bayer AG

- 6.3.16Panion & BF Biotech

- 6.3.17Danone Nutricia

- 6.3.18Sun Pharma

- 6.3.19Zydus Lifesciences

- 6.3.20Dr. Reddy’s Laboratories

- 6.3.21Alebund Pharmaceuticals

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Hyperphosphatemia Treatment Market Report Scope

As per the scope, hyperphosphatemia, characterized by elevated phosphate levels in the blood, can arise from various factors, including advanced chronic kidney disease, hypothyroidism, and both metabolic and respiratory acidosis. Effective management of hyperphosphatemia typically involves a combination of dietary phosphate restrictions, appropriate dialysis, and medications.

The hyperphosphatemia treatment market is segmented into drug class, distribution channel, and geography. By drug class, the market is segmented into phosphate binders, non-phosphate binders, and others. The phosphate binders drug class includes calcium-based phosphate binders and non-calcium phosphate binders. The non-calcium-based phosphate binders are divided into sevelamer, lanthanum carbonate, iron-based phosphate binders, and others. The others include aluminum hydroxide, magnesium carbonate, and others. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for all the above segments.