Hypertrophic Cardiomyopathy Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

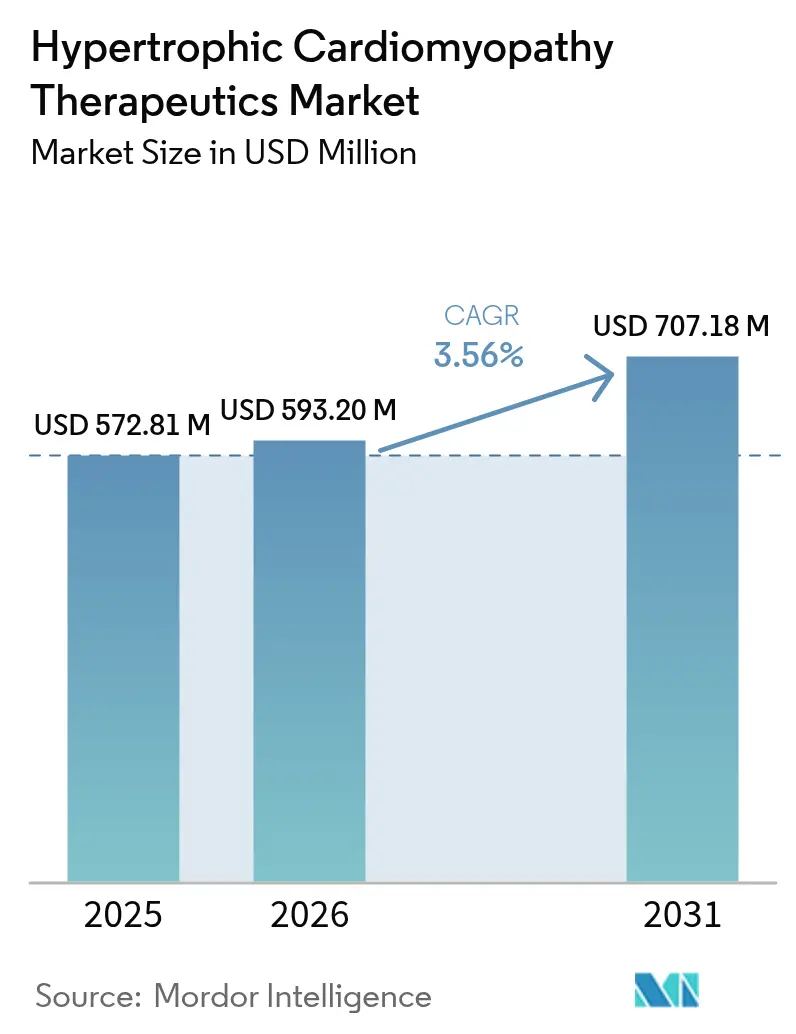

| Market Size (2026) | USD 593.2 Million |

| Market Size (2031) | USD 707.18 Million |

| Growth Rate (2026 - 2031) | 3.56% CAGR |

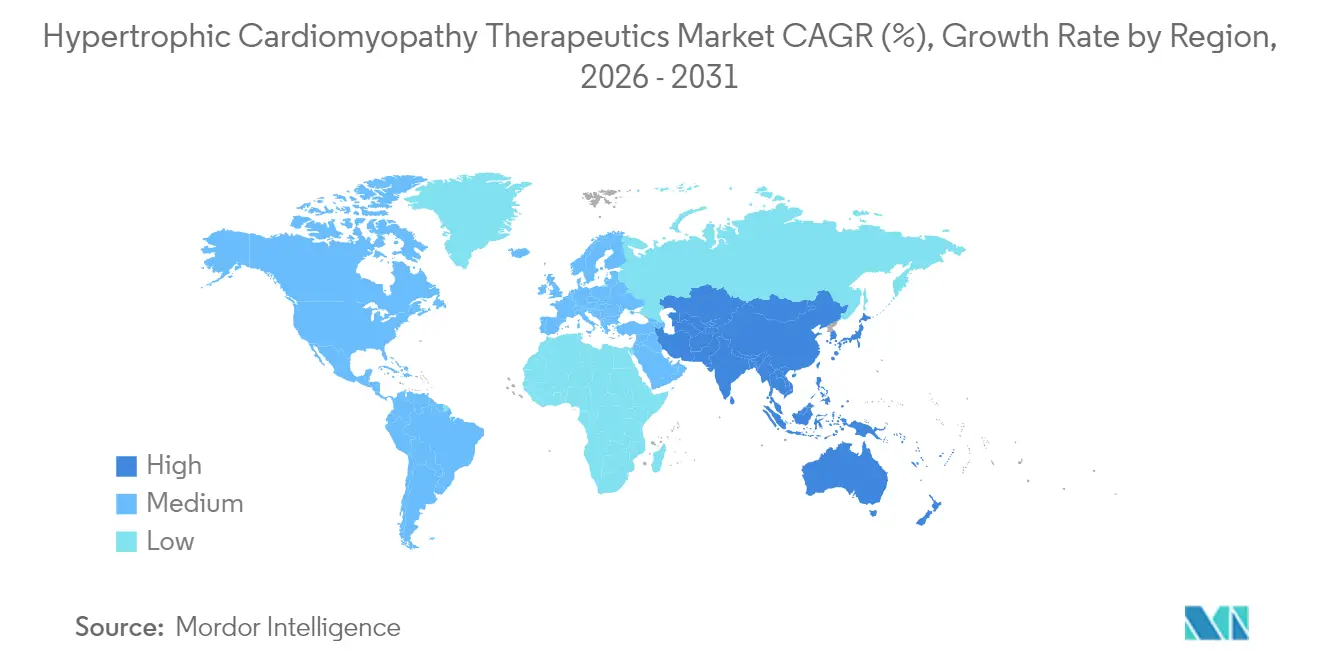

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hypertrophic Cardiomyopathy Therapeutics Market Analysis by Mordor Intelligence

The hypertrophic cardiomyopathy therapeutics market size in 2026 is estimated at USD 593.2 million, growing from 2025 value of USD 572.81 million with 2031 projections showing USD 707.18 million, growing at 3.56% CAGR over 2026-2031. A measured growth profile masks strong value creation as premium-priced cardiac myosin inhibitors replace decades-old beta-blockers, shifting treatment from symptomatic relief toward sarcomere-directed disease modification. Competitive activity is shaped by stringent regulatory oversight, orphan-drug exclusivity, and the clinical need for long-term safety data, all of which encourage disciplined launch strategies and tiered reimbursement models. Geographic momentum diverges; mature North American demand is stable but slowing, while Asia-Pacific benefits from expanding diagnostic infrastructure, national genetic testing programs, and multinational licensing alliances that collectively widen the pool of treatable patients. Digital distribution is also altering the channel mix as US REMS requirements funnel prescriptions to specialty pharmacies, accelerating online volume growth amid broader consolidation.

Key Report Takeaways

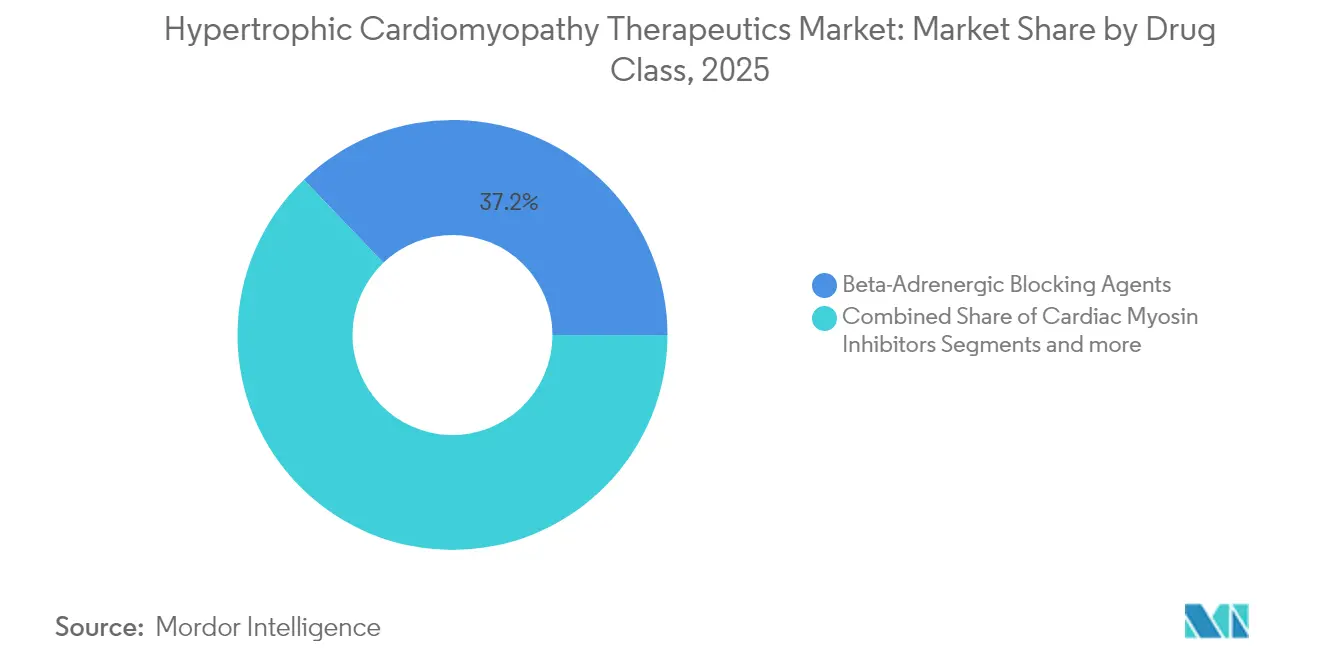

- By drug class, beta-adrenergic blocking agents held 37.15% of hypertrophic cardiomyopathy therapeutics market share in 2025, while cardiac myosin inhibitors are projected to grow at a 4.12% CAGR to 2031.

- By disease phenotype, obstructive HCM dominated with 59.85% revenue share in 2025; non-obstructive HCM is advancing at a 4.18% CAGR through 2031.

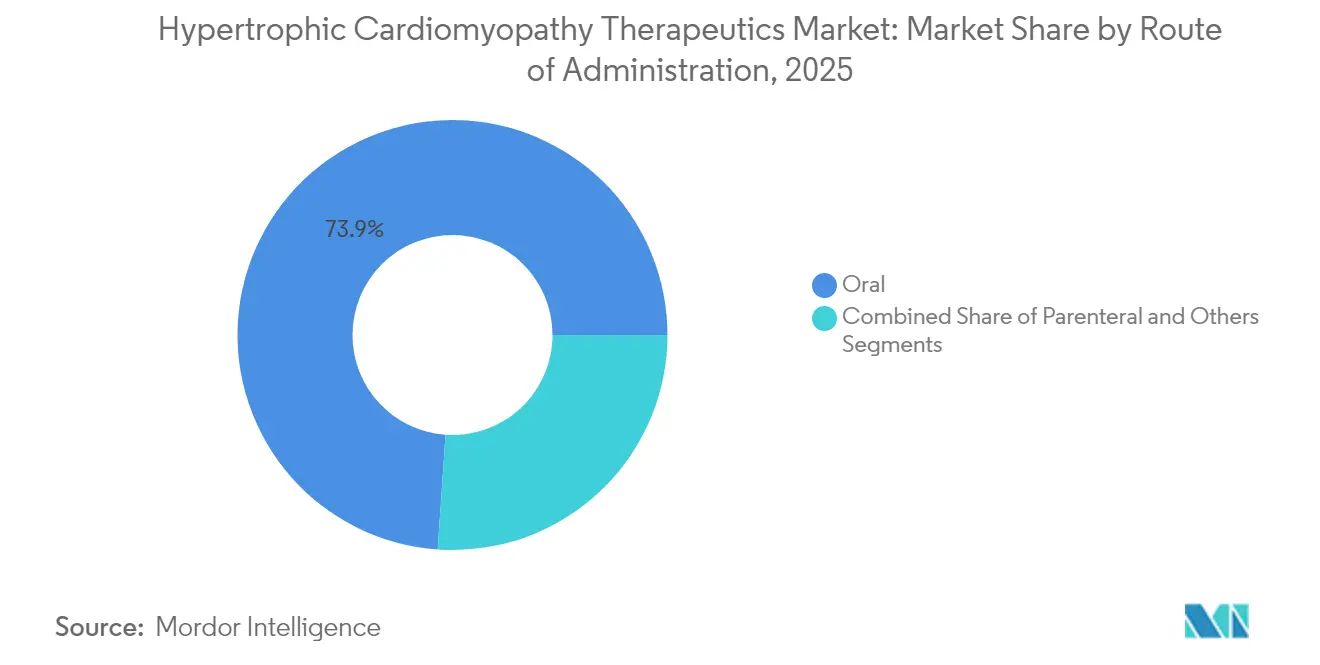

- By route of administration, oral formulations accounted for 73.90% of the hypertrophic cardiomyopathy therapeutics market size in 2025, but parenteral products are expanding at a 4.29% CAGR.

- By distribution channel, hospital pharmacies commanded 47.10% share in 2025, whereas online pharmacies lead growth at a 4.40% CAGR.

- By geography, North America led with a 40.55% share in 2025; Asia-Pacific records the highest regional CAGR at 4.09% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hypertrophic Cardiomyopathy Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA approvals for first-in-class cardiac myosin inhibitors | +1.2% | Global, led by North America & Europe | Medium term (2-4 years) |

| Rising genetic screening and cascade testing of at-risk relatives | +0.8% | North America & EU, expanding to APAC | Long term (≥4 years) |

| Growing prevalence of obesity and sedentary lifestyle | +0.6% | Global, concentrated in developed markets | Long term (≥4 years) |

| Orphan-drug incentives accelerating late-stage pipelines | +0.7% | North America & EU regulatory frameworks | Medium term (2-4 years) |

| AI-enabled echocardiography improving diagnosis rates | +0.5% | Global, early adoption in developed markets | Short term (≤2 years) |

| Payer shift toward outcomes-based contracting | +0.4% | North America & select EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FDA approvals for first-in-class cardiac-myosin inhibitors

Accelerated endorsements for mavacamten and label refinements that cut mandatory echocardiography monitoring from quarterly to biannual intervals improve prescriber confidence and patient convenience [1]Bristol Myers Squibb, “CAMZYOS Label Update,” bristolmyerssquibb.com . Community cardiologists now feel more comfortable initiating therapy outside specialized centers, broadening access beyond academic hubs. The upcoming aficamten decision, expected in December 2025, may establish a duopoly that tempers price escalation while encouraging evidence-based switching. Such regulatory momentum signals a maturation phase in which mechanistic precision, not symptom palliation, determines standard of care. Nevertheless, the non-obstructive trial miss underscores phenotype-specific complexity that could slow expansive label gambits.

Rising genetic screening and cascade testing of at-risk relatives

Nationwide programs integrating next-generation sequencing with cardiology referral pathways enlarge the diagnosed population and reposition HCM from a late-stage discovery to a proactively managed hereditary condition. Family cascade testing detects asymptomatic carriers earlier, and AI-enhanced ECG tools boasting 94% sensitivity shorten diagnostic odysseys. Asian cohorts, historically underdiagnosed, show rising identification rates as regional payors reimburse panel tests and governments subsidize counseling, reinforcing Asia-Pacific’s outsized growth trajectory. Economic ramifications extend to productivity gains when early intervention delays morbidity, supporting payer willingness to finance premium drugs.

AI-enabled echocardiography improving diagnosis rates

Machine-learning algorithms that automatically flag subtle hypertrophy during routine scans improve detection in primary care settings where specialist sonographers are scarce. Standardized gradient measurements reduce inter-observer variability, aiding therapy selection and streamlining REMS compliance. Wider adoption generates a virtuous cycle: higher case capture justifies specialty-clinic expansion, which in turn fuels demand for advanced treatments, further enlarging the hypertrophic cardiomyopathy therapeutics market. Such digital tools also underpin outcomes-based contracts by furnishing real-time metrics on ventricular remodeling.

Orphan-drug incentives accelerating late-stage pipelines

Seven-year US exclusivity, priority review vouchers, and reduced filing fees entice novel entrants despite a relatively small patient base. Mavacamten enjoys exclusivity through 2029, while aficamten could secure similar protection, anchoring commercial forecasts that underpin venture financing rounds for second-generation agents [2]Cytokinetics, “Aficamten Regulatory Status,” cytokinetics.com . Smaller study sizes, permissible under orphan regulations, compress development timelines and lower capital intensity, reinforcing a pipeline dense with gene-therapy, metabolic-modulator, and small-molecule assets. Yet payers increasingly demand risk-sharing contracts that tie reimbursements to functional improvements, tempering revenue certainty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing and REMS program limiting uptake | -0.9% | Global, acute in price-sensitive markets | Short term (≤2 years) |

| Generic beta-blocker competition | -0.6% | Global, concentrated in cost-conscious segments | Medium term (2-4 years) |

| Uncertain long-term safety data for myosin inhibitors | -0.4% | Global, regulatory focus in North America & EU | Medium term (2-4 years) |

| Limited specialist prescriber base for rare cardiomyopathies | -0.3% | Global, acute in emerging markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Premium pricing and REMS program limiting uptake

An annual therapy cost near USD 90,000 positions mavacamten among the most expensive chronic cardiovascular drugs, restricting adoption in health systems with high patient cost-share burdens. REMS enrollment layers logistical hurdles—specialty pharmacy use, baseline and follow-up echocardiograms, and prescriber certification—that dissuade community physicians. Out-of-pocket costs can exceed USD 10,000 for patients in high-deductible plans, generating a two-tier access dynamic tied to geography and insurance. Even where assistance programs exist, administrative complexity prolongs time-to-therapy, dampening early revenue ramp. Price renegotiations or the arrival of aficamten-driven competition may temper this headwind over the medium term.

Generic beta-blocker competition

Long-patent-expired agents such as metoprolol and propranolol cost pennies per day, carry decades of safety familiarity, and require no special monitoring, securing first-line status for mildly symptomatic patients worldwide. Physicians in emerging markets default to these options due to budget constraints, and guidelines still recommend beta-blockers as initial therapy. Consequently, premium mechanisms must demonstrate clear superiority before guideline committees endorse earlier-line use. While disease-modifying advantages drive eventual switch-over, widespread generics keep price pressure high and extend the adoption curve for innovative classes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Myosin Inhibitors Challenge Beta-Blocker Dominance

In 2025, beta-adrenergic blocking agents commanded 37.15% of the hypertrophic cardiomyopathy therapeutics market, reflecting decades of clinical familiarity and broad formulary inclusion. The cardiac myosin inhibitor cohort, although nascent, is set to record a 4.12% CAGR through 2031 as growing physician comfort, guideline integration, and real-world safety validation propel uptake. Premium positioning will likely persist despite competitive entry because mechanistic differentiation supports measurable symptom relief and ventricular remodeling. The hypertrophic cardiomyopathy therapeutics market size for myosin inhibitors is forecast to capture an incremental USD 112.8 million by 2031, offsetting generic erosion in traditional classes.

Second-line classes retain niche relevance. Calcium channel blockers provide an alternative for beta-blocker-intolerant patients, particularly where bradycardia risk is high. Antiarrhythmic use centers on atrial fibrillation management, while anticoagulants expand as physicians increasingly recognize embolic stroke risk in HCM. Gene-therapy and metabolic-modulator pipelines housed within the “Others” segment promise step-change innovation, potentially resetting class hierarchies after 2030. Overall, competitive repositioning around disease modification solidifies the hypertrophic cardiomyopathy therapeutics industry’s transition away from purely symptomatic care.

By Disease Phenotype: Non-Obstructive Gains Despite Setbacks

Obstructive HCM retained 59.85% share in 2025, benefiting from well-defined gradients that clearly warrant pharmacologic or surgical intervention. Yet non-obstructive disease is expanding faster, with a projected 4.18% CAGR, fueled by greater awareness, genetic identification, and the clinical void exposed by a pivotal trial miss. The hypertrophic cardiomyopathy therapeutics market size for non-obstructive candidates is small today but represents an attractive white space for next-generation approaches.

The ODYSSEY-HCM setback underscores the need for phenotype-tailored pathways, inviting metabolic or gene-editing interventions that correct distinct molecular drivers . As registries capture richer longitudinal data, precise end-points for non-obstructive efficacy should become clearer, enabling targeted development and premium reimbursement. In the interim, symptomatic control relies on traditional agents, maintaining a dual-tier structure until mechanism-specific efficacy is proven.

By Route of Administration: Parenteral Momentum Builds

Oral drugs dominated with 73.90% share in 2025 thanks to established prescribing habits and convenience. Nonetheless, parenteral formulations are projected to grow at 4.29% CAGR as innovators pursue monthly or quarterly depot injections that ease adherence burdens for patients juggling polypharmacy. Long-acting injectables offer consistent plasma exposure, potentially smoothing hemodynamic control and reducing monitoring variability.

Immuno-oncology’s success with extended-interval dosing has primed both payers and providers to value convenience premiums, a trend cardiovascular developers hope to replicate. Early-stage gene-therapy vectors delivered intravenously aim at one-time cures, representing the ultimate parenteral extension. Should safety concerns be mitigated, market adoption could accelerate late in the decade, bringing step-wise gains to the hypertrophic cardiomyopathy therapeutics market share for injectable modalities.

By Distribution Channel: Online Specialty Growth Accelerates

Hospital pharmacies accounted for 47.10% of 2025 revenue, reflecting REMS mandates that centralize dispensing in accredited centers. Online specialty platforms, however, are forecast to expand at 4.40% CAGR as digital workflows integrate prior authorization support, educational modules, and automatic refill reminders. The hypertrophic cardiomyopathy therapeutics market size distributed through online channels is small today but increasing steadily as tele-cardiology normalizes.

Specialty pharmacy consolidation-spearheaded by players such as CVS Specialty and Accredo-creates scale economies that manufacturers leverage for patient-support programs and data capture. Retail chains lacking specialty certifications struggle to participate, but collaborative models could emerge where community outlets partner with cloud-based service layers to meet REMS obligations while retaining local dispensing.

Geography Analysis

North America led the hypertrophic cardiomyopathy therapeutics market with a 40.55% share in 2025, supported by early drug approvals, robust insurance coverage, and a dense network of accredited HCM centers. Adoption, however, is moderating as payers intensify scrutiny of list prices and demand post-marketing evidence linking ventricular remodeling to reduced surgical interventions and hospitalizations. Tele-echocardiography programs are extending specialist oversight to rural areas, mitigating some access disparities, yet overall growth will decelerate relative to emerging regions.

Asia-Pacific is tracking a 4.09% CAGR to 2031, the fastest worldwide, thanks to government-backed genetic testing consortia, expanding echocardiography capacity, and cross-border licensing deals such as LianBio’s partnership for mavacamten commercialization. China’s tiered hospital reforms, coupled with Japan’s early adoption of myosin inhibitors, provide dual growth pillars. Meanwhile, India and Southeast Asia concentrate on upgrading diagnostic hardware, creating a sizeable funnel for future drug uptake once affordability programs mature.

Europe sits between these poles: regulatory alignment through the EMA accelerates multi-country launches, but reimbursement is conditional on country-level cost-effectiveness reviews. Health-technology-assessment agencies in Germany and the United Kingdom demand real-world data, stretching time-to-peak sales yet ultimately reinforcing value-based positioning. Pan-European HCM registries facilitate post-approval commitments, bolstering pharmacovigilance and informing iterative guideline updates.

Competitive Landscape

The hypertrophic cardiomyopathy therapeutics market is moderately concentrated, anchored by Bristol Myers Squibb’s mavacamten but poised for disruption as Cytokinetics’ aficamten approaches a December 2025 PDUFA deadline. Should approval occur, a two-player myosin inhibitor segment may ignite competitive rebate structures that expand access while sustaining innovation funding. Patent-term extension proceedings—CAMZYOS received a 2,723-day review period—illustrate the intricate intellectual-property dance that shapes life-cycle management.

Pipeline breadth is widening beyond sarcomere targets. Tenaya Therapeutics is advancing gene-replacement vectors aiming for one-time correction of pathogenic variants, while Edgewise Therapeutics explores small molecules that enhance energetic efficiency, each promising modality-based differentiation rather than incremental same-class variation. Market entrants must surmount high trial-design complexity given the need for precise hemodynamic endpoints and extensive cardiac safety monitoring. Consequently, collaboration with academic HCM centers remains a strategic imperative for both clinical execution and real-world-evidence generation.

Strategically, incumbents focus on label expansion into pediatric populations, perioperative management, and potential combination regimens that address arrhythmic complications. White-space opportunities in non-obstructive disease and long-acting injectable formulations offer new revenue terrain. Alliances with specialty pharmacies and digital platform partners provide data streams necessary for outcomes-based reimbursement, embedding service-layer capabilities into the traditional product model.

Hypertrophic Cardiomyopathy Therapeutics Industry Leaders

AstraZeneca Plc

Bayer AG

Sanofi S.A.

Merck & Co., Inc

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Eli Lilly announced a USD 1.3 billion acquisition of Verve Therapeutics, advancing gene-editing programs relevant to cardiovascular disorders that share pathogenic pathways with HCM.

- May 2025: The FDA extended the PDUFA date for Cytokinetics’ aficamten to December 26, 2025, requesting additional REMS details without new clinical data.

- April 2025: Bristol Myers Squibb reported that the Phase 3 ODYSSEY-HCM study in non-obstructive patients failed to meet primary endpoints, halting its planned label expansion.

Global Hypertrophic Cardiomyopathy Therapeutics Market Report Scope

As per the scope of this report, hypertrophic cardiomyopathy (HCM) is a genetic heart muscle disease caused by a mutation in sarcomere protein genes that encodes for the contractile machinery of the heart. The Hypertrophic Cardiomyopathy Therapeutics Market is segmented by Drug Class (Antiarrhythmic Agents, Anticoagulants, Beta Adrenergic Blocking Agents, Calcium Channel Blockers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Beta-Adrenergic Blocking Agents |

| Calcium Channel Blockers |

| Cardiac Myosin Inhibitors |

| Antiarrhythmic Agents |

| Anticoagulants |

| Others |

| Obstructive HCM (oHCM) |

| Non-Obstructive HCM (nHCM) |

| Oral |

| Parenteral |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Beta-Adrenergic Blocking Agents | |

| Calcium Channel Blockers | ||

| Cardiac Myosin Inhibitors | ||

| Antiarrhythmic Agents | ||

| Anticoagulants | ||

| Others | ||

| By Disease Phenotype | Obstructive HCM (oHCM) | |

| Non-Obstructive HCM (nHCM) | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hypertrophic cardiomyopathy therapeutics market?

The market stands at USD 593.2 million in 2026 and is projected to reach USD 707.18 million by 2031.

Which drug class is growing fastest?

Cardiac myosin inhibitors are forecast to expand at a 4.12% CAGR, the quickest among all classes.

Why is Asia-Pacific the fastest-growing region?

Broader genetic testing, improved echocardiography access, and strategic licensing deals drive a regional CAGR of 4.09%.

How do REMS programs affect drug adoption?

REMS requirements centralize dispensing in specialty channels, elevate monitoring costs, and slow uptake, especially in community settings.

What competitive changes are expected by 2026?

Approval of Cytokinetics’ aficamten may create a duopoly, while gene-therapy candidates begin late-stage trials, diversifying future options.

Are generic beta-blockers still relevant?

Yes, their low cost and widespread familiarity keep them first-line for mild symptoms, although they provide only symptomatic relief.

Page last updated on: