Hyderabad Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

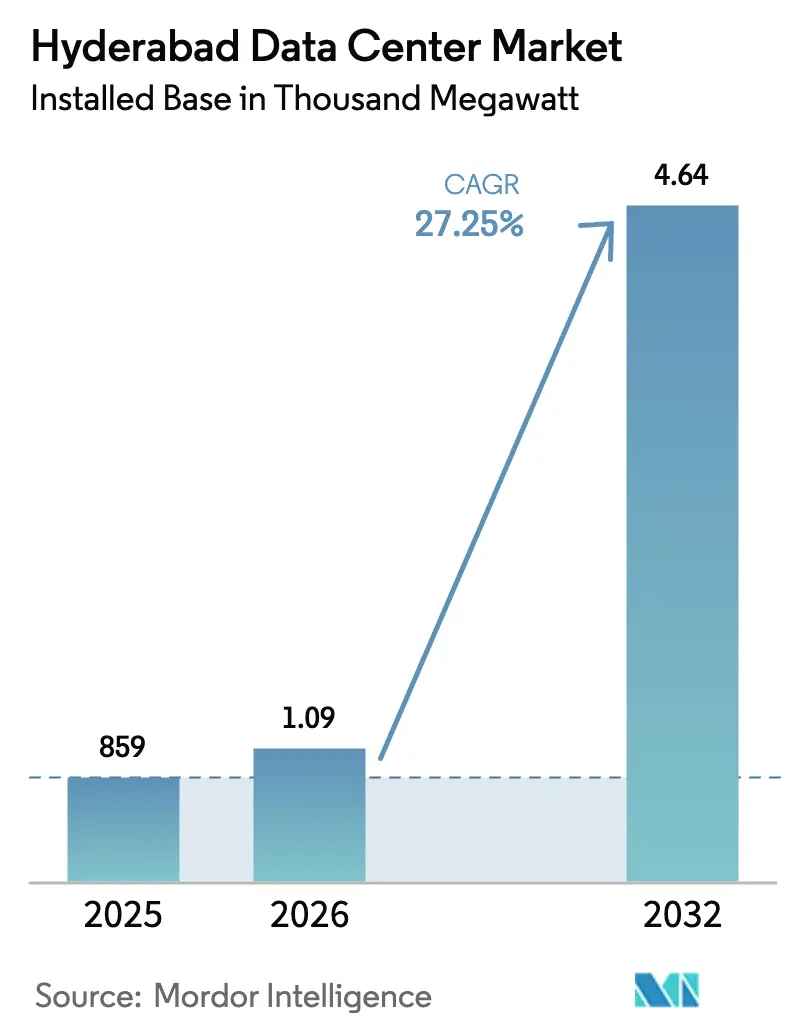

| Base Year Market Size (2025) | 859 Thousand megawatt |

| Market Volume (2026) | 1.09 Thousand megawatt |

| Market Volume (2032) | 4.64 Thousand megawatt |

| Growth Rate (2026 - 2032) | 27.25% CAGR |

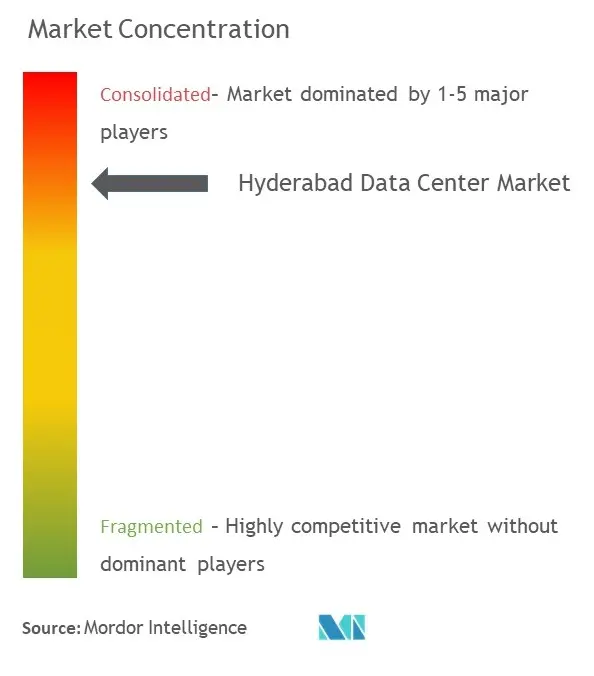

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hyderabad Data Center Market Analysis by Mordor Intelligence

The Hyderabad data center market size is expected to grow from 859 MW of installed IT load in 2025 to 1,093.1 MW of installed IT load in 2026 and is forecast to reach 4,640.8 MW by 2032 at 27.25% CAGR over 2026-2032. Surging hyperscale capital expenditure, Telangana’s single-window incentives, and the Digital Personal Data Protection (DPDP) Act anchor this expansion. Hyperscale operators benefit from land costs that average 40% below Mumbai while enjoying comparable fiber density, a combination that accelerates regionwide capacity planning. Intensifying AI and GPU demand lifts rack power densities to 20–40 kW, steering investment toward liquid-cooled halls and Tier IV redundancy. Meanwhile, 5G backhaul traffic and OTT streaming reinforce edge-node builds that complement hyperscale nodes, sustaining a balanced absorption curve. Execution risks persist around grid reliability and real-estate inflation, but coordinated state subsidies and renewable-power mandates soften these headwinds.

Key Report Takeaways

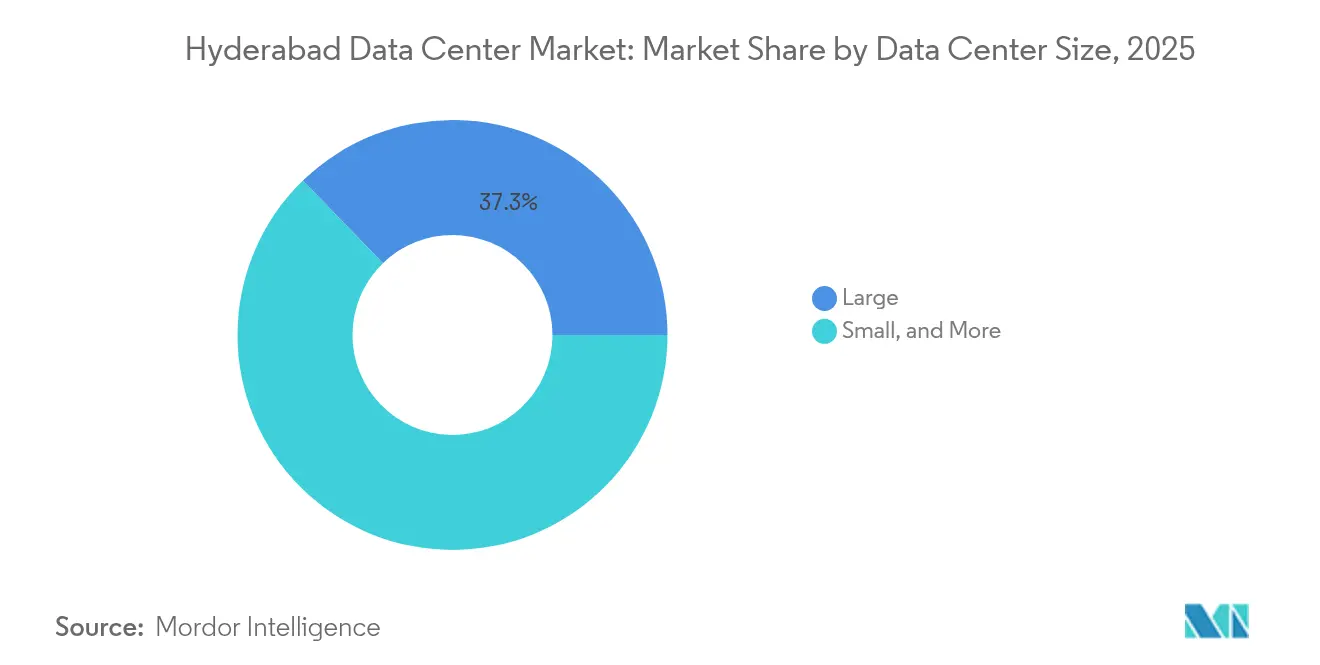

- By data center size, Large facilities held 37.25% of Hyderabad data center market share in 2025, whereas Massive sites are expanding at a 23.07% CAGR through 2032.

- By tier standard, Tier III captured 56.45% revenue share in 2025; Tier IV facilities are forecast to grow at a 20.68% CAGR to 2032.

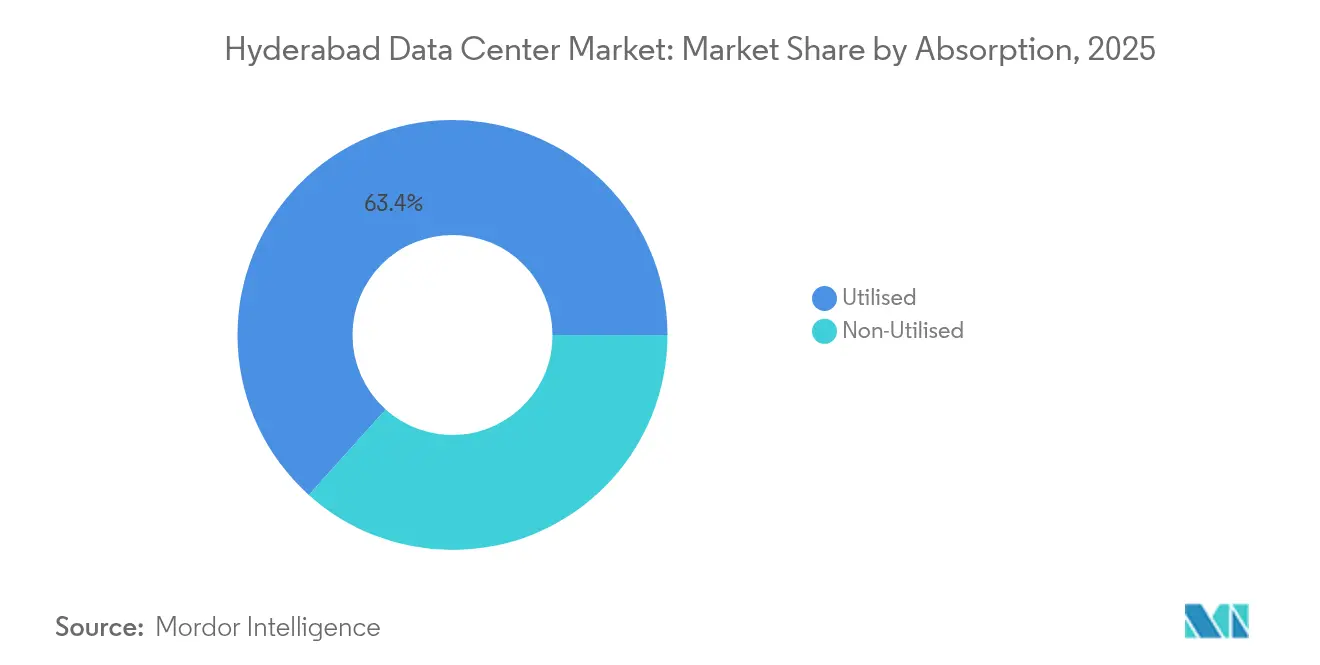

- By absorption, the Utilised category accounted for 63.35% of Hyderabad data center market size in 2025 and is advancing at a 24.41% CAGR through 2032.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hyderabad Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding mobile-data consumption and 5G roll-out | +4.20% | National; Hyderabad, Chennai, Bangalore lead | Medium term (2–4 years) |

| Indian data-localization mandates (DPDP Act) | +3.80% | National; concentrated in metro hubs | Short term (≤2 years) |

| Hyperscale cloud region roll-outs in Hyderabad | +5.10% | Hyderabad-centric; Telangana spillover | Long term (≥4 years) |

| Surge in OTT, gaming and AI workloads | +3.50% | National; Hyderabad as southern hub | Medium term (2–4 years) |

| Single-window clearance and CAPEX subsidies | +2.10% | Telangana specific | Short term (≤2 years) |

| Aerospace and defense R and D corridor demand | +1.50% | Hyderabad aerospace cluster | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Cloud Region Roll-outs Drive Unprecedented Capacity Expansion

Amazon’s USD 4.4 billion commitment and Microsoft’s six-site blueprint create a gravitational pull that redirects capacity away from saturated Mumbai corridors. Each anchor facility targets >100 MW IT load, catalyzing supplier ecosystems and creating roughly 48,000 direct and indirect jobs yearly [1].Data Center Knowledge, “Amazon Commits $4.4B in Data Center Investment in Hyderabad, India,” datacenterknowledge.comIncentives include Telangana’s 10-year power-duty exemptions and fast-track environmental clearances that compress construction timelines by up to six months. Land parcels along the Outer Ring Road (ORR) trade 40% below equivalent plots in Navi Mumbai, lowering per-MW capex even after factoring in redundancy requirements. Network operators respond by extending dark-fiber rings to these greenfield campuses, ensuring sub-2-millisecond latency to Hyderabad’s financial district.

Data Localization Mandates Create Immediate Enterprise Demand

The DPDP Act obliges all entities handling sensitive personal data to localize storage inside India, setting an immediate demand floor [2].Taxmann, “Overview of Digital Personal Data Protection Act 2023,” taxmann.com Financial institutions face even stricter Reserve Bank of India norms, prompting Tier IV preference for core banking workloads. Flipkart’s renewable-powered Tier IV build-out in Hyderabad illustrates how compliance spurs higher-spec deployments that fetch premium rack rates. Multinationals serving Indian consumers now factor Hyderabad colocation costs into global data-sovereignty budgets, ensuring consistent absorption even during macro-slowdowns.

Mobile-Data Explosion and 5G Infrastructure Deployment Accelerate Edge Requirements

Average per-capita mobile data usage crossed 25 GB per month in 2025, and 5G traffic is climbing 60% year on year. Airtel Nxtra alone is investing USD 600 million to triple capacity to 400 MW, with Hyderabad hosting a major slice to backhaul 5G traffic. Sub-10 ms latency thresholds for autonomous-vehicle testbeds and industrial IoT lines demand micro-edge pods within 30 km of users. Operators integrate computational-fluid-dynamics-optimized cooling to dissipate the additional heat generated by 5G radios, cutting PUE by 5–7% relative to legacy sites.

AI and Gaming Workloads Drive Premium Tier IV Adoption

CtrlS’s AI-ready campus showcases 400-GPU clusters and immersion-cooled racks that sustain >40 kW per rack while holding PUE below 1.1. Gaming-platform traffic spikes by as much as 300% during tournaments, requiring deterministic latency under 5 ms. Tier IV redundancy eliminates the revenue risk of mid-game outages, justifying 40–50% higher rental yields. Sustainability is central; the campus sources 70% of its power from off-site solar and feeds waste heat into neighboring commercial complexes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-reliability issues and high diesel backup costs | -2.80% | Hyderabad metro and ORR zones | Short term (≤2 years) |

| Escalating real-estate prices in HITEC and Gachibowli | -1.90% | Core IT corridors | Medium term (2–4 years) |

| Delays in fiber RoW approvals across ORR | -1.20% | ORR expansion areas | Medium term (2–4 years) |

| Seasonal water scarcity limiting liquid cooling | -0.80% | Greater Hyderabad | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Grid Reliability Challenges Elevate Operational Costs

Peak-summer demand forces load-shedding that triggers diesel-genset run-time spikes of 25–30%, inflating OPEX and carbon footprints [3].South First, “Frequent power cuts in Hyderabad raise concerns,” southfirst.com Repetitive fluctuations shorten UPS life cycles, risking availability downgrades below Tier III despite design intent. Operators pilot hydrogen-fuel-cell backups that promise 99.999% availability while slashing scope-1 emissions, but commercial viability hinges on the state’s upcoming green-hydrogen incentive scheme.

Real-Estate Cost Inflation Constrains Expansion in Prime Locations

Land in HITEC City now trades at USD 9 million per acre, nearly doubling since 2022, squeezing IRR for anything under 40 MW builds. Microsoft’s purchase of a 48-acre parcel 40 km out signals a shift to peri-urban zones, but longer fiber runs and right-of-way delays can add 3–5 months to go-live schedules. Smaller operators lacking hyperscale balance sheets are forced into joint-venture models or brownfield retrofits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Massive Facilities Lead Next-Generation Deployments

Massive sites—defined as >80 MW IT load—grow at a 23.07% CAGR through 2032, reflecting hyperscalers’ tilt toward campus-style economics. Amazon’s new campus clusters three 100 MW blocks behind a single 400 kV substation, yielding a 12% capex advantage per MW compared with two separate 50 MW sites. Large facilities still hold 37.25% Hyderabad data center market share in 2025, serving mid-sized cloud regions and BFSI outsourcing nodes. Medium and Small halls focus on edge caching and disaster-recovery needs for local enterprises. Immersion cooling at scale lets Massive campuses hit PUE 1.05, reinforcing their long-run cost leadership.

The capex heft of Massive formats elevates entry barriers, shifting bargaining power toward land aggregators and specialized EPC firms. Renewable-power purchase agreements often exceed 300 MW, stimulating state-level solar-park tenders that bundle power and green credits. Because each new Massive hub anchors multiple availability zones, network carriers race to pre-lay high-strand-count fiber rings, ensuring latency parity with Mumbai for pan-India traffic.

By Tier Standard: Tier IV Acceleration Reflects AI Infrastructure Demands

Tier IV footprints exhibit 20.68% CAGR, outpacing Tier III despite the latter’s 56.45% base-year share. GPU training clusters cannot tolerate mid-job resets that wipe multi-day computational cycles, so 99.995% uptime is economically rational. CtrlS’s Tier IV halls demonstrate integrated dual-active power feeds, 2N+1 cooling, and rack densities exceeding 40 kW. Meanwhile, Tier III remains optimal for SaaS and ERP workloads, balancing reliability and cost. Tier II serves backup-tape vaulting and non-critical archiving.

Higher-tier migration introduces a services layer—continuously monitored electrical switchgear, predictive maintenance using digital twins, and ISO 27017 cloud-security frameworks—to which hyperscalers attach premium SLAs. Capital intensity rises 40–50%, but operators partially offset this through green bonds and sustainability-linked loans like AdaniConneX’s USD 1.44 billion raise.

By Absorption: Utilised Segment Dominance Validates Market Fundamentals

With 63.35% 2025 share, the Utilised category validates supply-demand alignment, and is forecast to log 24.41% CAGR by 2032. Hyperscale colocation occupies the lion’s share; AWS and Microsoft pre-commit 15-year leases, derisking developer balance sheets. Retail colocation thrives on SMB digitalization drives, offering 5-kW half-rack plans with burstable bandwidth. Wholesale colocation appeals to SaaS unicorns needing contiguous cages minus the capex burden. BFSI contributes 35% of active white space, underpinned by real-time payment rails and algorithmic-trading nodes.

Utilisation gains are aided by power-contract innovation—pay-as-you-grow clauses align tenant payments with actual draw, improving cash flow for both sides. Developers also integrate on-site 30 MWh battery farms that provide ride-through and peak-shave grid tariffs, enhancing ROI while supporting state renewable targets.

Geography Analysis

Hyderabad sits at the geographic intersection of southern and central India, yielding latency under 30 ms to 60% of the country’s population centers. Telangana’s single-window clearances compress statutory cycles to <30 days, a distinct advantage over Karnataka’s multi-agency sign-offs that can stretch to 90 days. Renewable-energy sourcing is buoyed by the state’s 5 GW solar roadmap, enabling corporate PPAs priced 15% below grid tariffs, a draw for sustainability-focused operators. Regional Ring Road completion, though delayed, will link peripheral land banks to fiber routes, lowering last-mile trenching costs.

Within Hyderabad, HITEC City and Gachibowli remain preferred nodes for latency-critical BFSI tenants, yet land scarcity nudges new builds toward Shamshabad and Yacharam along the ORR. These peri-urban pockets offer 20–30% cheaper parcels but require greater investment in dual-path fiber to maintain sub-2-ms intra-metro latency. International reach is enabled via Mumbai–Hyderabad–Chennai terrestrial super-routes that interconnect to SEA-ME-WE-6 and IAX subsea systems, giving local tenants onward links to Singapore under 60 ms round-trip. Government plans for India’s first data-analytics park in Gachibowli reinforce the cluster’s talent magnet, supporting 10,000 new analytics jobs and deepening enterprise demand.

Hyderabad’s aerospace-defense corridor adds a secure-cloud niche; OEMs and R&D labs require hybrid colocation meeting ITAR-equivalent controls. This demand boosts higher-margin service revenue—zero-trust architectures, air-gapped backup vaults, and tamper-evident racks. The corridor’s requirements ripple into peripheral zones, spurring micro-edge pods at factory floors where inline quality-inspection AI models reside.

Competitive Landscape

Market structure is moderately fragmented yet tilting toward consolidation. AWS, Microsoft, and Google wield scale leadership, but local champions CtrlS and Pi Datacenters leverage rapid-build expertise and customer-proximity to defend share. NTT’s USD 1.26 billion AI-focused campus signals rising foreign capital appetite, prompting domestic incumbents to accelerate expansion roadmaps.

Strategic moves highlight this arms race. CtrlS signed a January 2025 MoU with Telangana to streamline land and power allotment, aiming to triple local capacity to 200 MW. AdaniConneX raised a record USD 1.44 billion sustainability-linked loan, earmarking a multi-site pipeline that includes a 50 MW liquid-cooled block in Hyderabad. Aurum Equity Partners’ USD 400 million green campus underscores investor confidence in AI-ready, renewables-heavy builds. Market wide, average rack rates rose 7% year on year despite capacity additions, proving demand depth.

Regulatory complexity and technical specialization erect barriers that limit the viable competitor pool, yet white-space niches—secure government cloud, AI test clusters, 5G edge nodes—enable smaller innovators to prosper without head-to-head price wars. Partnerships—carrier-neutral IX points, renewable-energy aggregators, and modular-build specialists—emerge as critical levers for accelerated go-live schedules and differentiated SLAs.

Hyderabad Data Center Industry Leaders

Sify Technologies Limited

STT Telemedia

Reliance industries

CtrlS

Nxtra Data Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Telangana government signed an MoU with CtrlS Datacenters to expedite advanced facility development across the state.

- January 2025: Amazon Web Services committed Rs 60,000 crore to expand Hyderabad capacity, deepening its earlier USD 4.4 billion pledge.

- August 2024: Microsoft acquired 48 acres for Rs 267 crore to add new hyperscale modules in Hyderabad.

- August 2024: Aurum Equity Partners unveiled a USD 400 million next-generation, AI-powered green data-center plan in the city.

- July 2024: Microsoft announced Rs 16,000 crore for three additional data centers, elevating its Hyderabad total to six.

Hyderabad Data Center Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services.

The Hyderabad data center market is segmented by dc size (small, medium, large, massive, mega), by tier type (tier 1&2, tier 3, tier 4), by absorption (utilized (colocation type (retail, wholescale, hyperscale), end user (cloud & IT, telecom, media & entertainment, government, BFSI, manufacturing, e-commerce, and other end-users)), non-utilized).

The market sizes and forecasts are provided in terms of value (MW) for all the above segments.

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User Industry | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End Users | ||

| By Data Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User Industry | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End Users | |||

Key Questions Answered in the Report

How fast is capacity growing in Hyderabad?

The Hyderabad data center market size stands at 1,093.1 MW of installed IT load in 2026 and is projected to reach 4,640.8 MW by 2032, translating into a 27.25% CAGR over 2026-2032.

Which facility size is expanding the quickest?

Massive campuses larger than 80 MW are advancing at a 23.07% CAGR, driven by hyperscale demand for consolidated, AI-ready capacity.

Why are Tier IV builds gaining traction?

AI and gaming workloads cannot tolerate outages, so operators justify Tier IV’s 99.995% uptime despite higher capex, leading to a 20.68% CAGR for this standard.

What role does the DPDP Act play?

The 2023 data-localization law forces enterprises to store personal data in-country, guaranteeing a baseline of demand for compliant Hyderabad facilities.

How severe are grid-reliability issues?

Frequent power cuts increase diesel-genset usage by up to 30%, raising OPEX; operators are piloting hydrogen fuel cells to mitigate this risk.

Which companies are investing the most?

Amazon, Microsoft, and NTT headline with multi-billion-dollar commitments, while local leader CtrlS and new entrant AdaniConneX accelerate expansion through green financing.

Page last updated on: