Mumbai Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

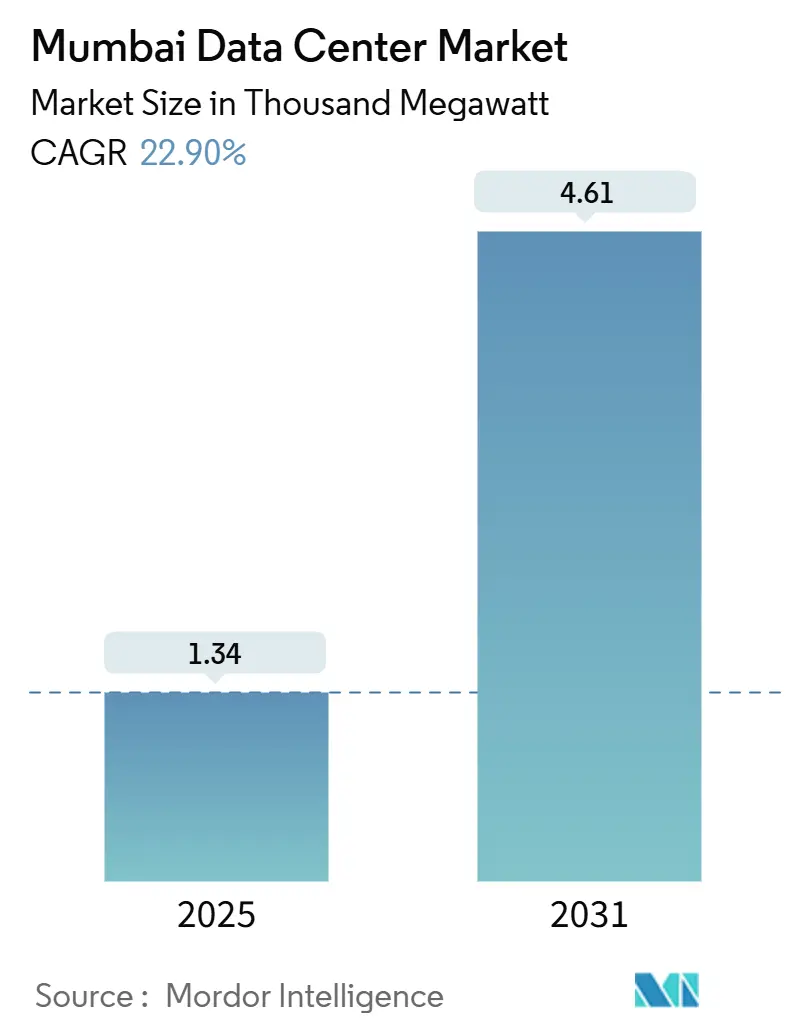

| Market Volume (2025) | 1.34 Thousand megawatt |

| Market Volume (2031) | 4.61 Thousand megawatt |

| Growth Rate (2025 - 2031) | 22.90% CAGR |

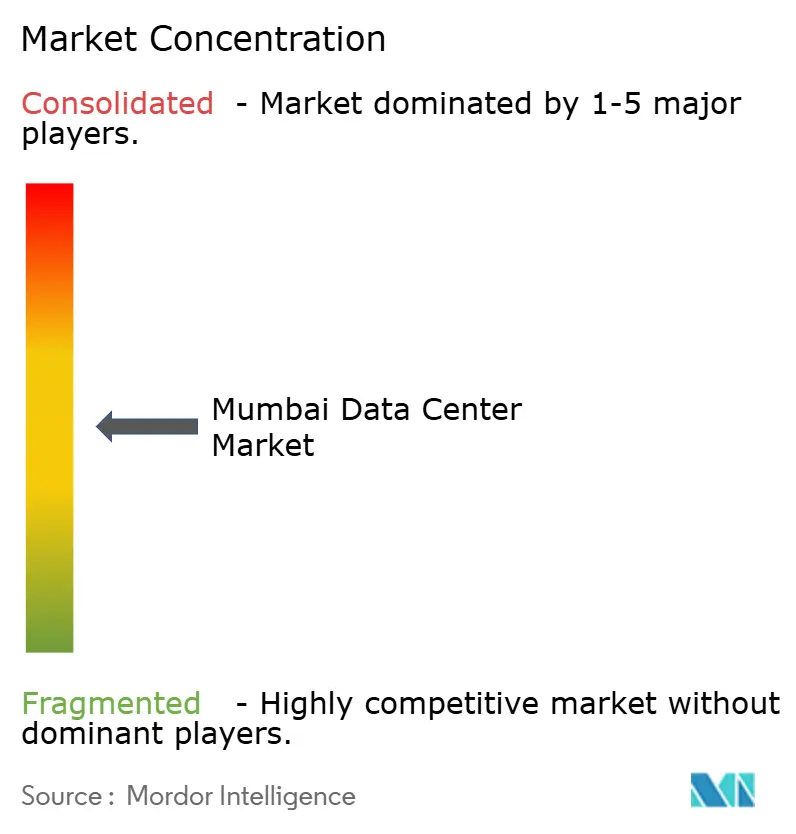

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mumbai Data Center Market Analysis by Mordor Intelligence

The Mumbai data center market reached 1,337.09 MW in 2025 and is forecast to rise to 4,606.91 MW by 2031, translating into a 22.9% CAGR over the period. Expansive infrastructure spending, hyperscale cloud deployments, and aggressive renewable-energy initiatives are the three most powerful drivers pushing the Mumbai data center market to the next tier in the Asia-Pacific hierarchy. Power-availability bottlenecks and premium land prices continue to shape site-selection economics, but developers are responding with brownfield mill conversions, vertical designs, and captive renewable projects. Strategic alliances among construction firms, global investment managers, and cloud providers are accelerating construction timelines, while metro-fiber densification is supporting edge computing and AI workloads. Competitive intensity is gradually increasing, yet the top players still control a sizable share, keeping pricing rational and allowing operators to maintain healthy utilization rates.

Key Report Takeaways

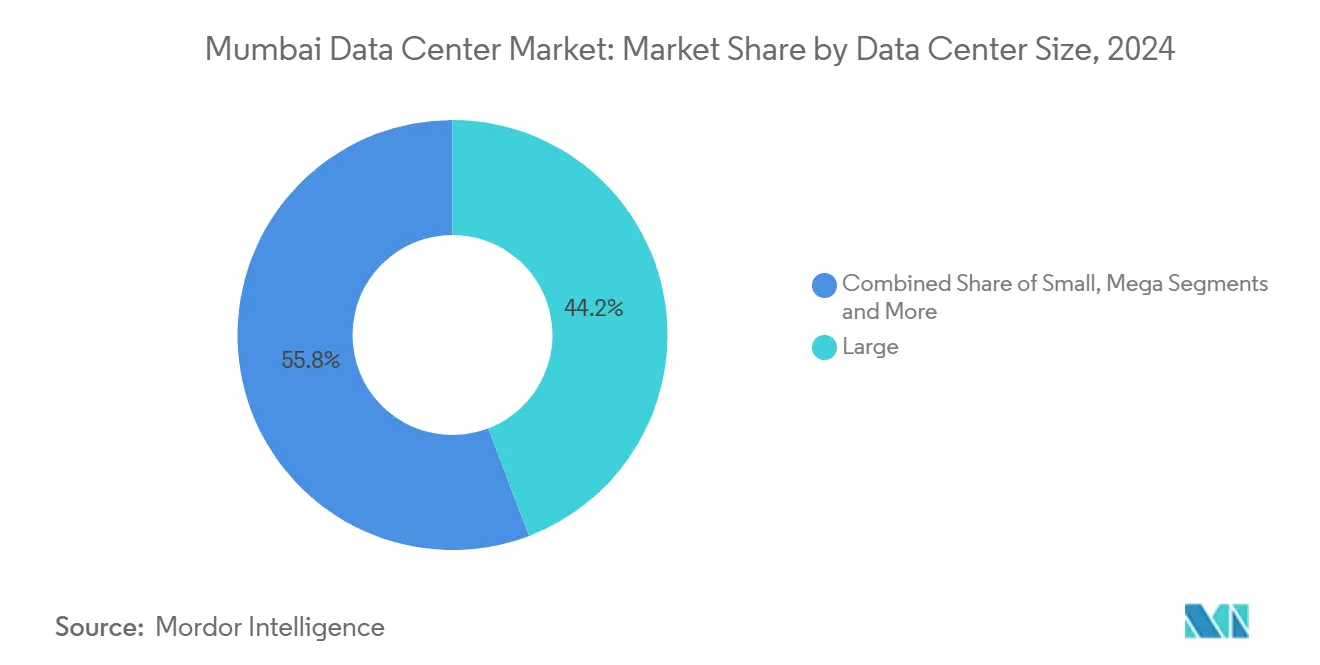

- By data center size, Large facilities secured 44.2% of the Mumbai data center market share in 2024.

- By tier standard, Tier III accounted for 66.7% of the Mumbai data center market size in 2024, while Tier IV is set to grow at 24.5% CAGR to 2031.

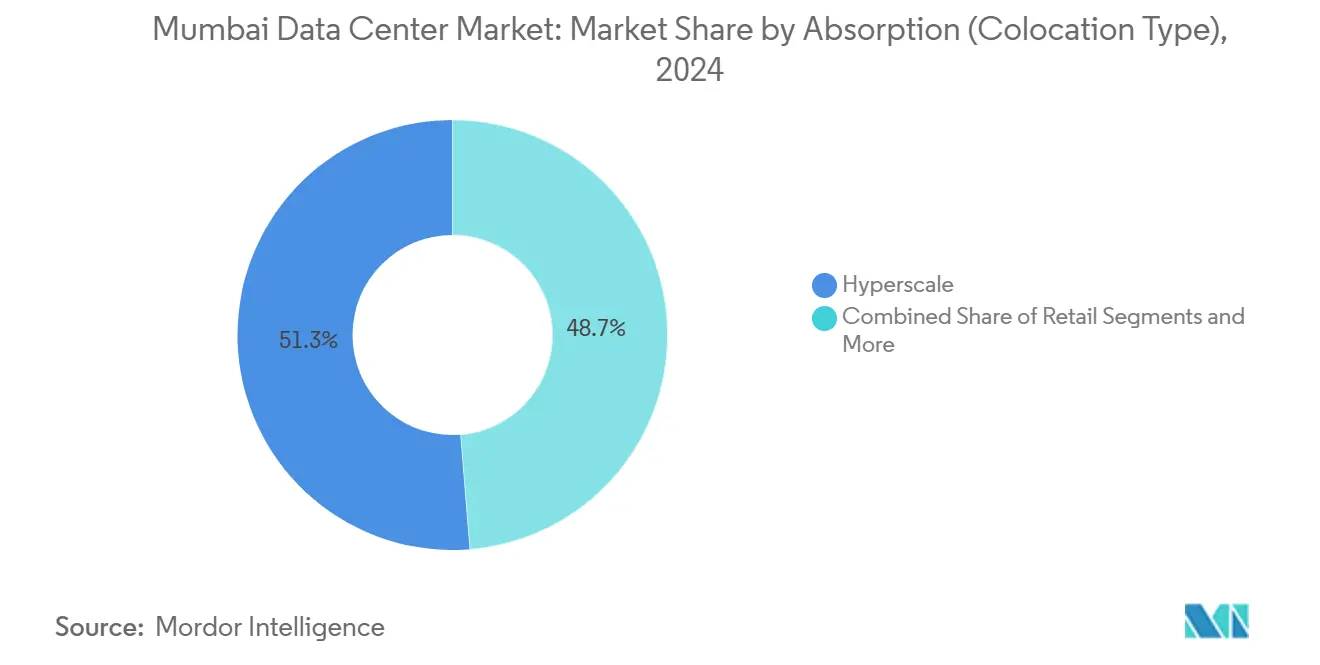

- By absorption type, the Utilized-Hyperscale category captured 51.3% of the Mumbai data center market size in 2024 and will expand at 23.0% CAGR through 2031.

- By end-user industry, cloud service providers led with 48.8% market share in 2024; AI/ML cloud workloads are progressing at a 24.5% CAGR through 2031.

Mumbai Data Center Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising cloud-first demand from BFSI, media and OTT players | +4.2% | Mumbai Metropolitan Region, with spillover to Pune corridor | Short term (≤ 2 years) |

| Aggressive renewable-power targets by Maharashtra DISCOMs | +3.8% | Maharashtra state-wide, concentrated in MMR industrial zones | Medium term (2-4 years) |

| Edge-ready metro fibre densification across MMR | +3.1% | Mumbai city, Navi Mumbai, Thane, extending to satellite towns | Medium term (2-4 years) |

| Incentives under Maharashtra IT/ITeS policy 2024 | +2.9% | Maharashtra state boundaries, enhanced benefits in designated IT townships | Long term (≥ 4 years) |

| Redevelopment of brown-field textile mills into DC campuses | +2.4% | Central Mumbai, Lower Parel, Worli micro-markets | Short term (≤ 2 years) |

| Availability of high-TDS brine for liquid immersion cooling | +1.8% | Coastal Mumbai, Navi Mumbai industrial belt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cloud-First Demand From BFSI, Media and OTT Players

Financial institutions are shifting core workloads to engineered cloud platforms that demand near-zero downtime. HDFC Bank migrated its core banking stack in 2024 to increase throughput for 93 million customers. Media outlets and OTT providers require low-latency infrastructure during live-streaming peaks, adding new racks in Colocation zones inside the Mumbai data center market. Community cloud templates offered by ESDS help more than 280 cooperative banks comply with Reserve Bank norms while reducing deployment costs. Flipkart’s decision to move production servers in-house demonstrates how e-commerce operators are increasing wholesale absorption in Mumbai data centers. Together, BFSI, media, and digital-commerce demand flows are expected to anchor the next wave of capacity additions in the Mumbai data center market.

Aggressive Renewable-Power Targets by Maharashtra DISCOMs

Maharashtra aims to reach 40% renewable power by 2030, creating incentives for operators to sign green PPAs and pursue captive solar farms.[2]Lyla Bavadam, “Maharashtra aims to achieve 40% electricity generation through renewable sources by 2030,” Frontline, frontline.thehindu.com. Equinix already sources wind-solar hybrids for its Mumbai sites, while CtrlS commissioned a 125 MW solar array to cut grid dependency. Yotta Infrastructure targets 80% renewable coverage within three years, up from 30% now. Green energy credentials are now a key selection criterion for hyperscale tenants, pushing every major developer to integrate renewables into the Mumbai data center market.

Edge-Ready Metro-Fiber Densification Across MMR

Fiber investments are projected to triple by 2030 as AI and 5G drive fourfold data traffic per rack.[1]Lightstorm Staff, “AI and 5G power India’s optical fiber boom,” Light Reading, lightreading.com Lightstorm alone connected 60 data centers with 30,000 km of cable, slicing latency to single-digit milliseconds. The upcoming Navi Mumbai airport and six metro lines create fresh ducts for fiber pulls, enabling operators to place micro-edge nodes along mobility corridors. Project Waterworth, Meta’s new subsea system landing in Mumbai in 2026, will widen international bandwidth and consolidate the city’s status as a gateway. Fiber density is therefore a critical enabler of distributed architectures in the evolving Mumbai data center market.

Incentives Under Maharashtra IT/ITeS Policy 2024

The 2024 policy grants 100% stamp-duty waiver, permanent electricity-duty exemption, and preferential power tariffs for qualifying data centers. Infrastructure status designation lowers borrowing costs and removes land-use hurdles. Recent regulatory tweaks also eliminated the need to convert agricultural land for industrial use, shortening approval cycles. Together these measures cut capex by 8-10 percentage points and should keep the Mumbai data center market attractive for global investors across the forecast horizon.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Scarcity of contiguous 50-acre parcels inside MMR | -3.4% | Mumbai Metropolitan Region core areas, acute in island city | Short term (≤ 2 years) |

| 220 kV grid interconnection queues greater than 24 months | -2.8% | Maharashtra state grid, concentrated bottlenecks in MMR industrial zones | Medium term (2-4 years) |

| Monsoon-driven flooding risk and mandatory CRZ clearances | -2.1% | Coastal Mumbai, low-lying areas in Navi Mumbai, Thane creek vicinity | Long term (≥ 4 years) |

| Shortfall of Uptime-Tier-certified commissioning engineers | -1.9% | Pan-India shortage, acute impact in Mumbai due to project concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Contiguous 50-Acre Parcels Inside MMR

Mumbai’s dense urban morphology constrains new hyperscale campuses. Suitable tracts in the island city command rentals of ₹200-500 per square foot, pushing developers to recycle decaying mills into multistory facilities. Nirlon IT Park is an early success story that converted a textile compound into an 8-building IT campus, signaling the viability of adaptive reuse. Large greenfield parcels are now concentrated in Navi Mumbai and Taloja, but added transport time elevates latency for ultra-low-delay use cases. Land scarcity therefore forces a hybrid strategy of vertical densification downtown and horizontal expansion on the periphery across the Mumbai data center market.

220 kV Grid Interconnection Queues Exceeding 24 Months

Maharashtra’s transmission approval pipeline is struggling to keep pace with hyperscale demand, leading to two-year waits for bulk connections.[3]Umesh Saini, “Maharashtra Electricity Regulatory Commission (Multi-Year Tariff) Regulations, 2024,” MERC, merc.gov.in Load-despatch centers must now vet renewable-heavy portfolios, adding complexity. Developers hedge by funding captive solar farms or deploying temporary diesel-gas turbines. CtrlS, for example, allocated land for a 125 MW solar plant to guarantee timeline certainty. Persistent interconnection delays remain a gating factor for the Mumbai data center market in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Mega Facilities Anchor Hyperscale Growth

Large sites maintained 44.2% of the Mumbai data center market share in 2024, showing enterprises still favor mid-range footprints near downtown hubs. Mega facilities, however, are scaling fastest at 23.5% CAGR because hyperscale tenants need contiguous 50-100 MW blocks. The average capex for a 1 MW build in Mumbai is INR 46.5 crore, with electrical systems consuming the largest slice. NTT’s Navi Mumbai campus demonstrates how liquid immersion cooling can lift rack density and shorten ROI cycles.

High-density cooling enables developers to fit more capacity per acre, mitigating land scarcity. Mega campuses in Navi Mumbai leverage cheaper greenfield parcels and proximity to submarine cable landing stations, unlocking economies of scale and positioning the Mumbai data center market for global AI workloads.

By Tier Standard: Tier IV Deployment Momentum Builds

Tier III configurations commanded 66.7% of the Mumbai data center market size in 2024, satisfying mainstream enterprise uptime needs. Tier IV facilities, though fewer in number today, are projected to grow at 24.5% CAGR as financial institutions and cloud giants demand full fault-tolerance. Yotta’s NM1 hub achieved Tier IV certification for 7,200 racks and 50 MW, setting a benchmark for Mumbai resilience. Certification costs are rising because India has fewer than 90 commissioning professionals qualified for Tier IV audits, creating execution risk.

Clients are willing to pay a 15-20% premium for ultra-high availability when storing regulated workloads, so developers see Tier IV as an important differentiation lever within the Mumbai data center market.

By Absorption (Colocation Type): Hyperscale Utilization Dominates

Utilized-Hyperscale absorption held 51.3% of the Mumbai data center market size in 2024 and is tracking a robust 23.0% CAGR. AWS’s USD 8.3 billion state pledge and Microsoft’s multi-site land banking explain why wholesale space is contracting rapidly. Retail colocation continues to serve enterprises requiring 200-500 kW pods, while non-utilized capacity has dipped below 6%, indicating a sellers’ market.

Wholesale contracts lock in 10-15 year revenue streams, giving build-to-suit developers predictable cashflows and supporting the high leverage structures common in the Mumbai data center market.

By Absorption (End-User Industry): AI/ML Workloads Accelerate Uptake

Cloud service providers own 48.8% of installed capacity and remain the anchor tenant group for new builds. AI/ML cloud services represent the fastest-growing workload vertical at 24.5% CAGR as enterprises adopt generative AI for customer analytics and supply-chain optimization. Yotta’s GPU-dense Shakti Cloud, built in partnership with NVIDIA, already supports large-language-model training workloads.

The BFSI sector is a steady second-tier customer. ICICI Lombard, for instance, shaved 45% off cloud operating costs after modernizing its data-management platform, reinforcing Mumbai’s position as India’s financial data nerve center. Manufacturing and media companies follow closely, with e-commerce intermediaries scaling cache nodes to meet next-day delivery expectations. The blend of tenants across industries underscores the resilience of demand for the Mumbai data center market.

Geography Analysis

Development is clustering along four corridors: Central Mumbai, Navi Mumbai, Thane-Kalyan, and the future “Third Mumbai City” zone. Navi Mumbai leads capacity additions, hosting Google’s 22.5-acre acquisition and AdaniConneX’s USD 1.44 billion financing for 250 MW of new builds. The new international airport will compress travel time to South Mumbai, encouraging more hyperscale investments.

Central Mumbai remains essential for low-latency BFSI workloads; STT GDC’s Bandra-Kurla facility continues to attract banks requiring proximity to server colocation. Thane and Kalyan are emerging with metro lines 4 and 5, offering cheaper land and power. The Mumbai Trans Harbour Link stitched South Mumbai to Navi Mumbai in 20 minutes, enabling active-active configurations across the harbor

“Third Mumbai City” aims to allocate a dedicated Data Centre Zone powered entirely by renewable energy, targeting 65% of India’s future storage demand. These geographic forces create a multi-node topology that balances latency, land cost, and disaster-recovery separation within the broader Mumbai data center market.

Competitive Landscape

The construction segment shows moderate concentration, with the top five players controlling roughly two-thirds of capacity under development. Larsen & Toubro leads turnkey EPC work, booking ₹116,036 crore orders in Q3 FY’25 and rebranding its cloud services arm as Cloudfiniti. Sterling & Wilson leverages MEP depth to bundle solar-plus-data-center EPC, while Shapoorji Pallonji focuses on hybrid office-IT parks housing colocation halls.

Specialists such as Princeton Digital Group partner with land owners like Mindspace to build technology campuses, enhancing amenity value for tenants. Yotta and AdaniConneX compete on scale and renewable integration, setting PUE benchmarks below 1.3. Technology differentiation centers on advanced cooling; NTT’s liquid-immersion pods cut energy draw by 30% and will be replicated across future halls.

Investment capital is flowing from global players. Blackstone paired with Panchshil Realty for India’s first 500 MW campus, validating Navi Mumbai’s large-parcel economics. Microsoft, Temasek, and BlackRock launched the USD 30 billion Project MGX, nominating Mumbai as an AI-specific cluster. Competitive pressure is therefore intensifying, yet the Mumbai data center market still rewards scale, permitting margins above global averages.

Mumbai Data Center Industry Leaders

NTT Global Data Centers

STT GDC India

CtrlS Datacenters

Yotta Infrastructure

Equinix India

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- Jan 2025: Project MGX, backed by Temasek, Microsoft, and BlackRock, earmarked 200-500 MW liquid-cooled campuses in Mumbai and other APAC hubs.

- February 2025: Blackstone–Panchshil announced a ₹20,000 crore, 500 MW hyperscale project in Navi Mumbai.

- March 2025: AWS reaffirmed a USD 8.3 billion Maharashtra commitment lasting through 2030.

- November 2024: Equinix signed a renewable PPA with CleanMax covering all Mumbai sites.

Mumbai Data Center Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services.

The mumbai data center market is segmented by DC size (small, medium, large, massive, and mega), tier type (tier 1 and 2, tier 3, and tier 4), and absorption (utilized (colocation type (retail, wholescale, and hyperscale), end user (cloud and IT, telecom, media and entertainment, government, BFSI, manufacturing, and e-commerce)), and non-utilized). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User Industry | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| Non-Utilized | ||

| By Data Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Utilized | By Colocation Type | Hyperscale |

| Retail | |||

| Wholesale | |||

| By End-User Industry | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

| Non-Utilized | |||

Key Questions Answered in the Report

How large will the Mumbai data center market be by 2031?

Installed capacity is projected to reach 4,606.91 MW, growing at a 22.9% CAGR from 2025.

Which size category leads demand?

Large facilities (10-25 MW) held 44.2% share in 2024, but Mega sites are expanding fastest at 23.5% CAGR.

Why are Tier IV data centers gaining traction?

Financial services and hyperscalers demand 99.995% uptime, prompting a 24.5% CAGR in Tier IV deployments.

What is the main challenge for developers?

Two-year waits for 220 kV grid interconnections lengthen project timelines and elevate costs.

How is renewable energy influencing site selection?

Maharashtras 40% renewables target incentivizes developers to secure green PPAs and build captive solar farms, lowering power costs.

Page last updated on: