Chennai Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

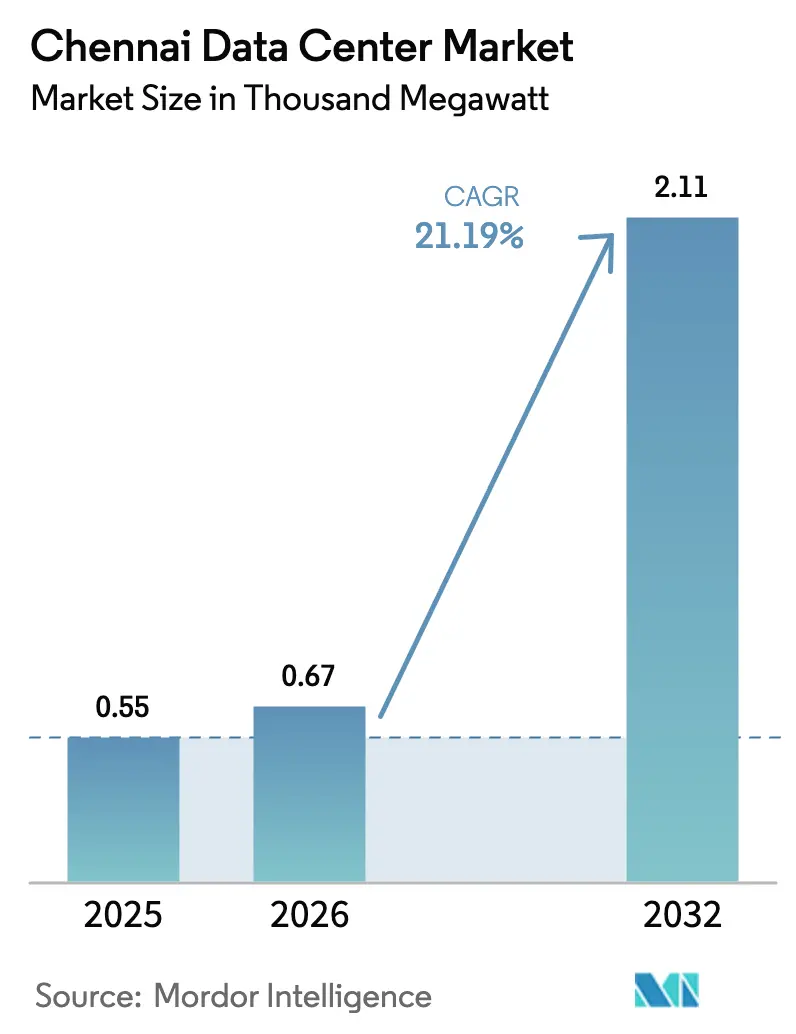

| Base Year Market Size (2025) | 0.55 Thousand megawatt |

| Market Volume (2026) | 0.67 Thousand megawatt |

| Market Volume (2032) | 2.11 Thousand megawatt |

| Growth Rate (2026 - 2032) | 21.19% CAGR |

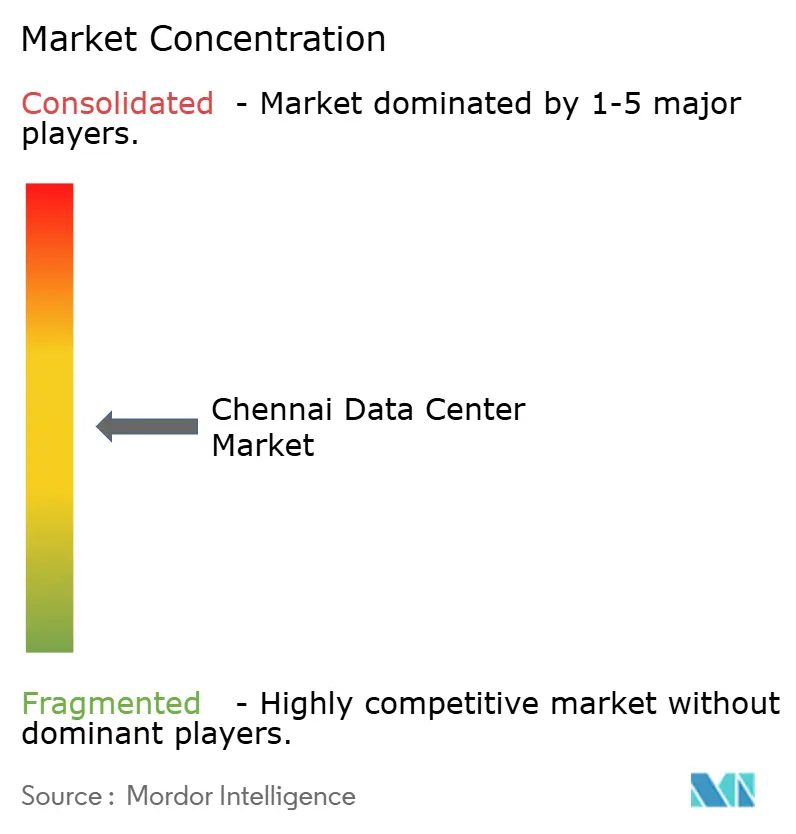

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chennai Data Center Market Analysis by Mordor Intelligence

The Chennai data center market size is expected to grow from 0.55 Thousand MW in 2025 to 0.67 Thousand MW in 2026 and is forecast to reach 2.11 Thousand MW by 2032 at 21.19% CAGR over 2026-2032. Market growth stems from the convergence of new submarine cable landings, state-backed renewable-energy corridors, cloud-first digital transformation, and AI-focused rack-density upgrades. Competitive intensity has deepened as global operators deploy capital toward hyperscale campuses, while local firms pivot to edge and compliance-ready services. Large contiguous parcels near cable landing stations command premium pricing, but operators are pursuing multi-phase builds in inland industrial zones to balance cost and risk. Rapid renewable integration and single-window clearances lower operating costs, yet grid-tie delays, land scarcity, and monsoon-related flood risks remain material constraints.

Key Report Takeaways

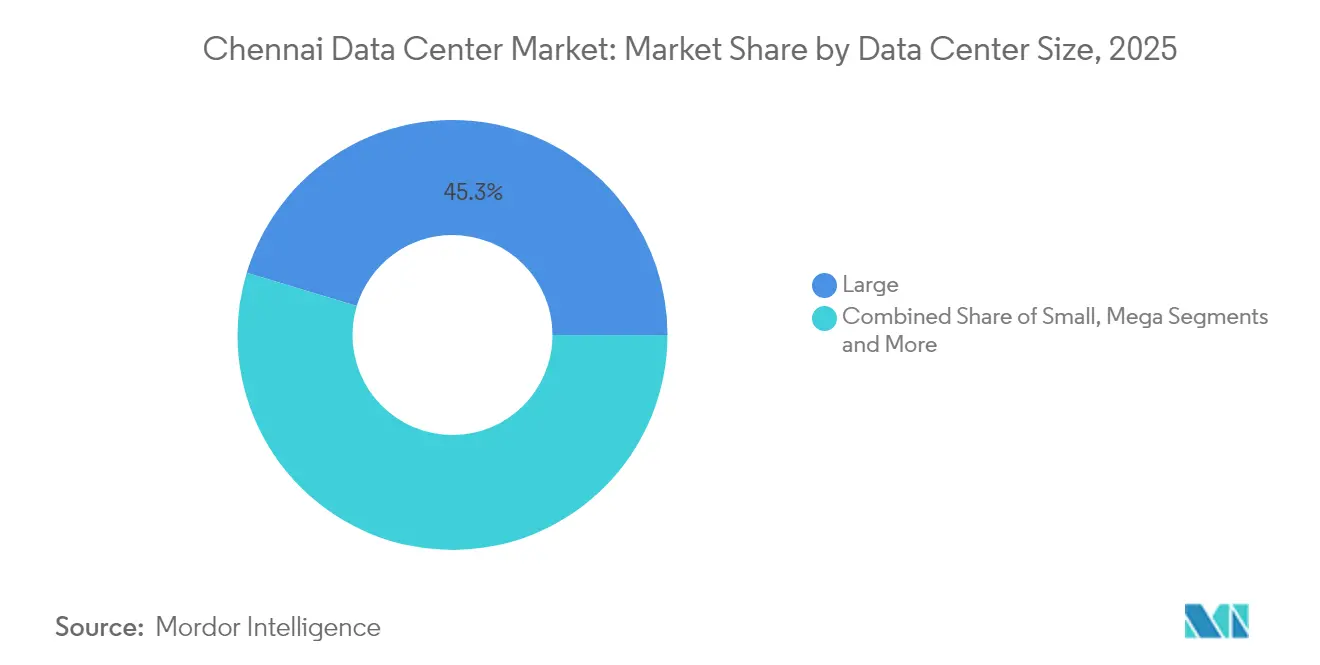

- By data-center size, large facilities led with 45.32% of Chennai data center market share in 2025, while the massive segment is forecast to advance at a 23.12% CAGR through 2032.

- By tier standard, Tier III accounted for a 76.28% share of the Chennai data center market size in 2025, whereas Tier IV is projected to grow at a 21.74% CAGR to 2032.

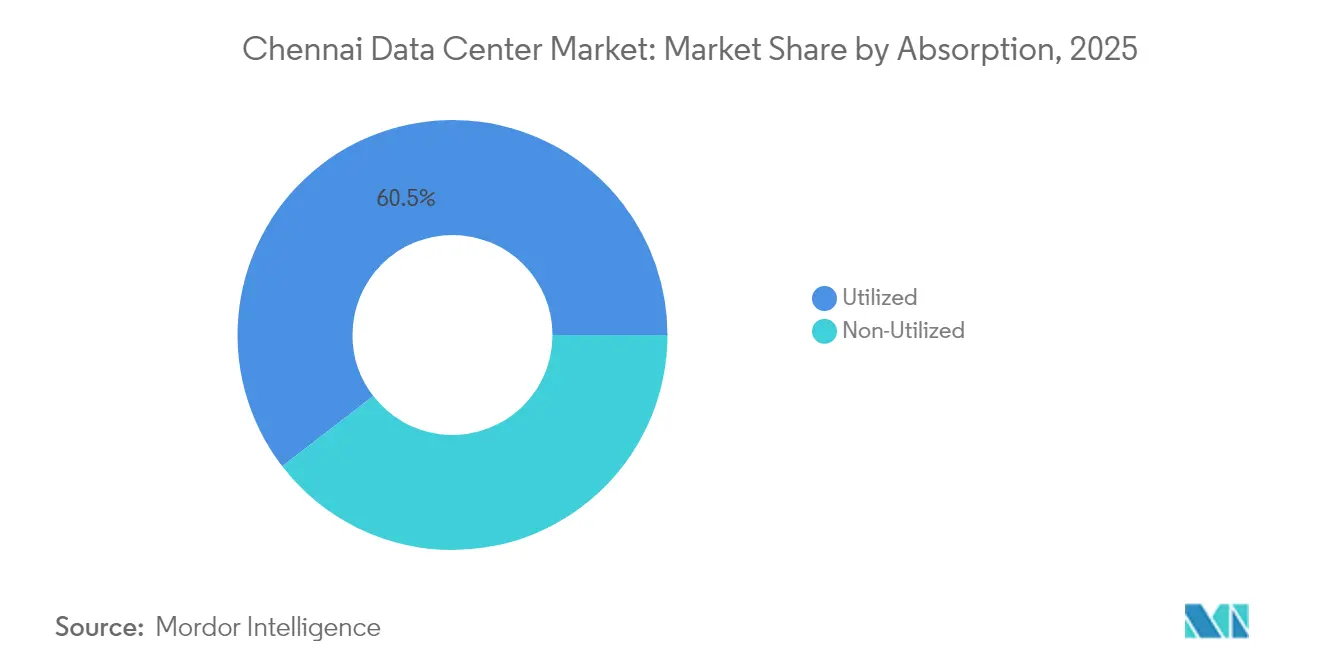

- By absorption, the utilized capacity represented 60.45% of the Chennai data center market in 2025 and is set to expand at a 22.36% CAGR through 2032.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chennai Data Center Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Sub-sea cable landings multiply international bandwidth | +4.2% | Chennai coastal corridor | Medium term (2–4 years) |

| Renewable-energy open-access corridors in Tamil Nadu | +3.8% | State-wide, Chennai hub | Long term (≥4 years) |

| Cloud-first adoption by BFSI, OTT and GCC operators | +5.1% | Chennai metro and tier-2 spillover | Short term (≤2 years) |

| State incentives under Tamil Nadu DC policy | +2.9% | State-wide, Chennai focus | Medium term (2–4 years) |

| ≥30 kW AI/LLM rack densities force white-space retrofits | +3.7% | IT corridor and industrial zones | Short term (≤2 years) |

| Cold-chain logistics pivot to data-powered automation hubs | +1.5% | Port vicinity and manufacturing clusters | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Sub-sea cable landings multiply international bandwidth

Five additional systems, including SEA-ME-WE-6 and MIST, give Chennai direct access to 420 TBPS aggregate capacity, lowering latency to Singapore and Marseille while positioning the city as a regional disaster-recovery hub.[1]Economic Times Telecom, Bharti Airtel lands SEA-ME-WE 6 submarine cable in Chennai, telecom.economictimes.indiatimes.com Cable operators co-locate landing stations with hyperscale campuses, creating vertically integrated connectivity-to-compute clusters that attract OTT and fintech workloads. Bandwidth abundance also underpins the Chennai data center market’s role in AI training, where large data ingests benefit from high-capacity international routes. Combined with India’s nine-fold increase in cable capacity since 2016, Chennai’s share of outbound traffic continues to rise.

Renewable-energy open-access corridors in Tamil Nadu

Tamil Nadu hosts 34.7 GW of renewable assets across wind, solar, and hydro, giving operators a cost-effective path to 100% clean energy targets.[2]The Hindu, A different shade of green: T.N.’s renewable energy initiatives, thehindu.com Data-center power purchase agreements benefit from favorable wheeling charges and banking provisions, cutting operating costs by up to 12%. STT GDC sources more than 60% green power for its Chennai campus, while Equinix targets 100% by 2030. Renewable corridors also de-risk future carbon regulations, making sustainability a competitive differentiator in hyperscale colocation bids.

Cloud-first adoption by BFSI, OTT and GCC operators

Large banks, OTT platforms, and 305 global capability centers rely on low-latency interconnects and local compliance to host critical workloads in Chennai. Mizuho Financial Group quadrupled its headcount to 1,000 and shifted AI and cybersecurity operations to a Chennai data center in 2025.[3]Business Standard, Japan’s Mizuho Finance Group sets up global business centre in Chennai, business-standard.com OTT firms consolidate storage and transcoding nodes locally to serve South India, driving steady utilization in both retail and hyperscale colocation segments.

State incentives under Tamil Nadu DC policy

The policy offers land-cost rebates, electricity-duty waivers, and accelerated depreciation benefits, trimming upfront capex by 6–8% and shortening approval cycles to 90 days. SEZ designation at TN Tech City adds tax holidays and faster customs clearance for imported equipment, further reducing time-to-market. Combined incentives have attracted CapitaLand, Yotta, and AdaniConneX to announce multi-phase campuses near Chennai.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Scarcity of contiguous greater than 25-acre parcels in Greater Chennai | -2.8% | Greater Chennai | Short term (≤2 years) |

| 230 kV grid-tie lead times exceed 24 months | -3.1% | Chennai and suburbs | Medium term (2–4 years) |

| Monsoon-flood and CRZ clearance risk along ECR coastline | -1.9% | Coastal Chennai | Long term (≥4 years) |

| Shortfall of Uptime-Tier-certified commissioning talent | -2.2% | Chennai metro | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Scarcity of contiguous greater than 25-acre parcels in Greater Chennai

Urban expansion has exhausted prime land along the IT corridor, raising acquisition costs by 15–20% and forcing operators toward multi-story vertical builds or suburban campuses. Yotta’s 13-acre facility achieves 20,000-rack capacity through floor-wise modular design, while ESR offers 80 acres in Oragadam to offset coastal land premiums. Land scarcity could slow the Chennai data center market unless satellite clusters emerge.

230 kV grid-tie lead times exceed 24 months

TANGEDCO approvals lag behind demand, prompting developers to install on-site gas generators or secure 110 kV interim feeds, inflating project costs by 8%. Utility restructuring into separate generation and distribution entities promises efficiency gains but remains a medium-term solution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Massive Facilities Drive AI Infrastructure

Large facilities captured 45.32% of Chennai data center market share in 2025, supported by balanced capex and near-shore connectivity advantages. The massive segment is forecast to grow at 23.12% CAGR, contributing 782.6 MW to Chennai data center market size by 2032. Hyperscale clients reserve contiguous halls exceeding 10 MW to deploy liquid-cooled AI clusters, while enterprises lease smaller blocks within large campuses for compliance-ready workloads.

Chennai’s massive campuses integrate on-site substations and direct renewable feeds, reducing power latency and carbon footprints. AdaniConneX’s flagship campus pairs a 400 kV switchyard with an 18 MW solar plant, enabling 30 kW racks without derating. NTT’s Chennai 2 facility prioritizes modular power trains, allowing phased expansion in response to AI demand surges.

By Tier Standard: Tier IV Adoption Accelerates for Mission-Critical Workloads

Tier III remains the backbone of enterprise colocation, holding 76.28% of the Chennai data center market in 2025. Rapidly evolving regulatory mandates in BFSI and telecom segments, however, fuel Tier IV demand, which is expected to expand at 21.74% CAGR. Financial services clients require 99.995% uptime for risk analytics and transaction processing, making concurrently maintainable infrastructure imperative.

Operators differentiate on certification speed and fault‐tolerant design. Equinix CN1 embeds 2(N+1) UPS topology and six-layer security to meet global banking standards. AI training clusters further tilt preference toward Tier IV given the cost of interrupted model builds. As a result, a growing share of new supply enters the market with Tier IV design readiness, even if operators initially certify at Tier III for capex prudence.

By Absorption: Utilized Capacity Reflects Strong Enterprise Demand

Utilized halls accounted for 60.45% of total live IT load in 2025, underscoring Chennai’s status as a mature, demand-aligned region. Hyperscale colocation sub-leases anchor pre-commitments exceeding 18 months, allowing operators to finance rapid expansions at favorable terms. Retail racks serve 305 GCCs and hundreds of fintech start-ups, filling smaller footprints with moderate power densities.

High utilization accelerates return on invested capital and validates forward-purchase land strategies despite scarcity risks. City Union Bank’s full migration to a Chennai colo hall cut latency for payment gateways by 35% while meeting RBI security norms. Empty shell capacity remains essential to capture AI testing surges; operators maintain buffer halls equal to 15–20% of built space, ensuring rapid ramp-up while sustaining market balance.

Geography Analysis

The Chennai data center market commands 22.60% of India’s total installed capacity, driven by proximity to five submarine cable landing stations and a 1,400-acre IT corridor housing 80% of Grade A office supply. Sub-regional clusters have emerged: the OMR-Siruseri stretch focuses on latency-sensitive OTT and fintech clients; Ambattur and Madhavaram cater to hyperscale builds seeking inland elevation and lower land prices. Coastal sites enjoy direct cable interconnects but require CRZ compliance measures that lift capex by 7%.

Industrial suburbs such as Oragadam and Sriperumbudur offer parcels exceeding 50 acres at a 35% discount to OMR. ESR’s 80-acre park showcases a campus-style model combining warehouse and edge data-center pods serving automotive IoT analytics. Government-led TN Tech City in Madhavaram targets mixed-use tech development, integrating data-center zoning with metro connectivity to decongest prime corridors.

Regional interconnect initiatives augment Chennai’s hub status. Space World’s USD 500 million fiber ring links 14 Chennai facilities with 400G wavelengths, reducing cross-connect fees and improving disaster-recovery posture for enterprises spanning Bengaluru and Hyderabad.

Competitive Landscape

The Chennai data center market commands 23% of India’s total installed capacity, driven by proximity to five submarine cable landing stations and a 1,400-acre IT corridor housing 80% of Grade A office supply. Sub-regional clusters have emerged: the OMR-Siruseri stretch focuses on latency-sensitive OTT and fintech clients; Ambattur and Madhavaram cater to hyperscale builds seeking inland elevation and lower land prices. Coastal sites enjoy direct cable interconnects but require CRZ compliance measures that lift capex by 7%.

Industrial suburbs such as Oragadam and Sriperumbudur offer parcels exceeding 50 acres at a 35% discount to OMR. ESR’s 80-acre park showcases a campus-style model combining warehouse and edge data-center pods serving automotive IoT analytics. Government-led TN Tech City in Madhavaram targets mixed-use tech development, integrating data-center zoning with metro connectivity to decongest prime corridors.

Regional interconnect initiatives augment Chennai’s hub status. Space World’s USD 500 million fiber ring links 14 Chennai facilities with 400G wavelengths, reducing cross-connect fees and improving disaster-recovery posture for enterprises spanning Bengaluru and Hyderabad.

Chennai Data Center Industry Leaders

Sify Technologies Limited

STT Telemedia

Reliance industries

NTT Data

Nxtra Data Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Bharti Airtel landed the SEA-ME-WE-6 cable in Chennai, adding 220 TBPS capacity that meshes with Nxtra’s data-center network.

- January 2025: Sify Technologies unveiled a USD 5 billion roadmap for AI-focused expansions, earmarking significant Chennai capacity.

- December 2024: CapitaLand India Trust advanced construction on a 54 MW Ambattur facility, targeting completion by Q2 2026.

- September 2024: STT GDC committed USD 3.2 billion to add 550 MW nationwide, with major Chennai allocations.

Chennai Data Center Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services, as well as store and manage the data connected with those applications and services.

The Chennai data center market is segmented by DC size (small, medium, large, massive, mega), by tier type (tier 1 and 2, Tier 3, Tier 4), by absorption (utilized, colocation type (retail, wholescale, hyperscale), end user (cloud & IT, telecom, media & entertainment, government, BFSI, manufacturing, e-commerce), and non-utilized).

The market sizes and forecasts are provided in terms of value (MW) for all the above segments.

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User Industry | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End Users | ||

| Non-Utilized | ||

| By Data Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Utilized | By Colocation Type | Hyperscale |

| Retail | |||

| Wholesale | |||

| By End-User Industry | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End Users | |||

| Non-Utilized | |||

Key Questions Answered in the Report

How large is the Chennai data center market in 2026?

Installed IT load is 666.55 MW and is forecast to reach 2,110.92 MW by 2032.

Which data-center size segment is growing the fastest?

Massive campuses show the highest growth, projected at a 23.12% CAGR through 2032.

Why are Tier IV facilities gaining traction in Chennai?

Financial services, OTT, and AI workloads demand 99.995% uptime that Tier IV designs assure.

What role do submarine cables play in local growth?

New landings such as SEA-ME-WE-6 and MIST supply 420 TBPS capacity, reducing latency and attracting international workloads.

How are operators addressing renewable-energy goals?

Developers sign open-access PPAs with Tamil Nadu wind and solar farms, achieving up to 100% green power targets.

What is a key bottleneck for rapid expansion?

230 kV grid-tie approvals often exceed 24 months, delaying large-scale power connectivity.

Page last updated on: