Bioactive Wound Dressing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.27 Billion |

| Market Size (2031) | USD 6.99 Billion |

| Growth Rate (2026 - 2031) | 10.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

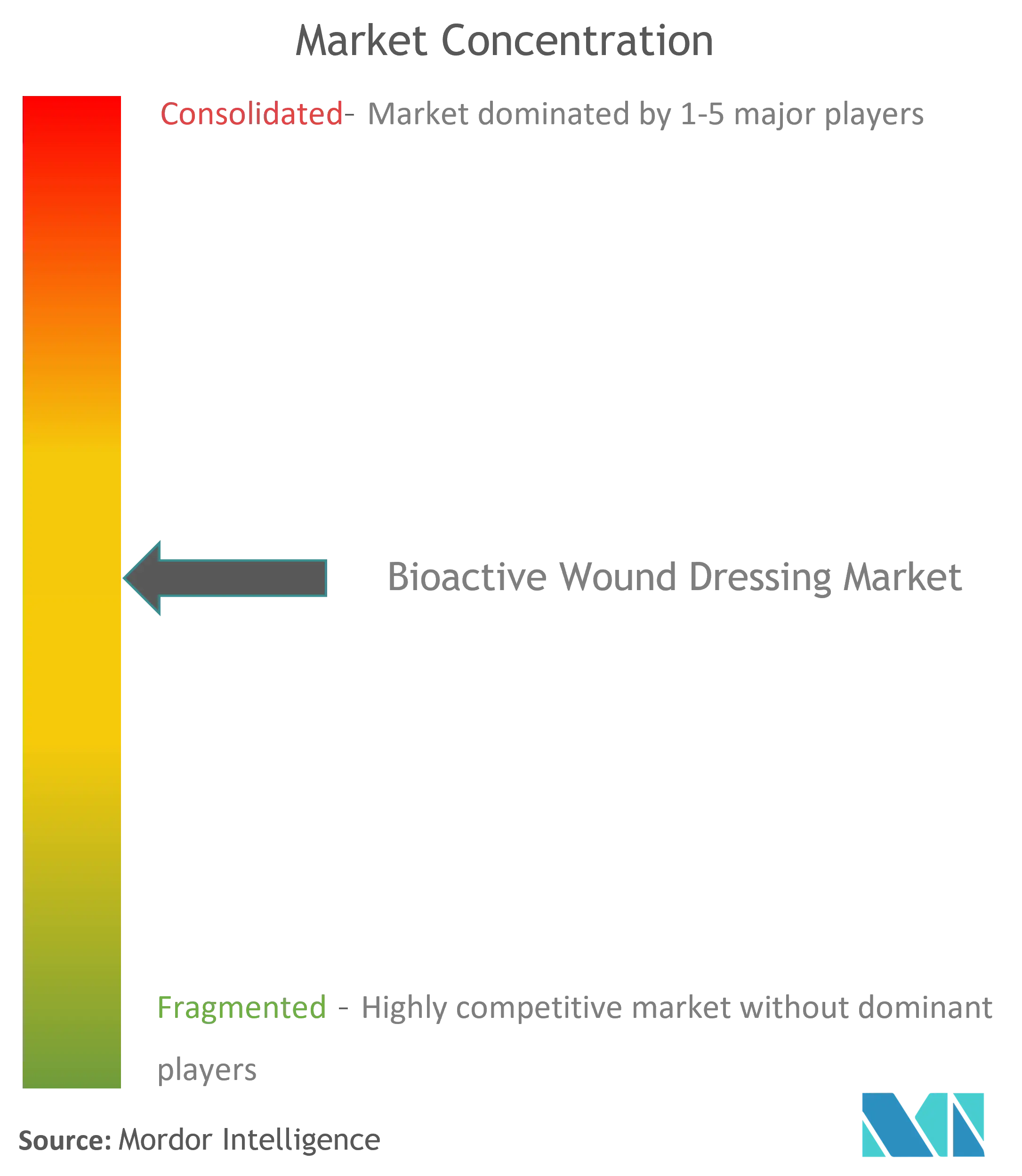

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioactive Wound Dressing Market Analysis by Mordor Intelligence

Bioactive wound dressing market size in 2026 is estimated at USD 4.27 billion, growing from 2025 value of USD 3.87 billion with 2031 projections showing USD 6.99 billion, growing at 10.36% CAGR over 2026-2031. Rapid growth stems from a confluence of aging populations, rising diabetes prevalence, and continuous breakthroughs in biomaterial science that are broadening clinical applications and enhancing healing outcomes. Demand intensifies as traditional hydrocolloid and alginate dressings give way to intelligent sensor-integrated platforms capable of real-time biomarker monitoring, while government payers increasingly reimburse premium solutions that shorten healing time and lower complication rates. Defense and trauma medicine open additional niches through fish-skin grafts, and wider reimbursement in OECD markets reduces cost friction for hospitals adopting advanced therapies. Smart bio-electronic dressings, although a smaller revenue slice today, record the fastest adoption trajectory as Internet-of-Things (IoT) functionality and predictive analytics move from pilot studies into commercial practice.

Key Report Takeaways

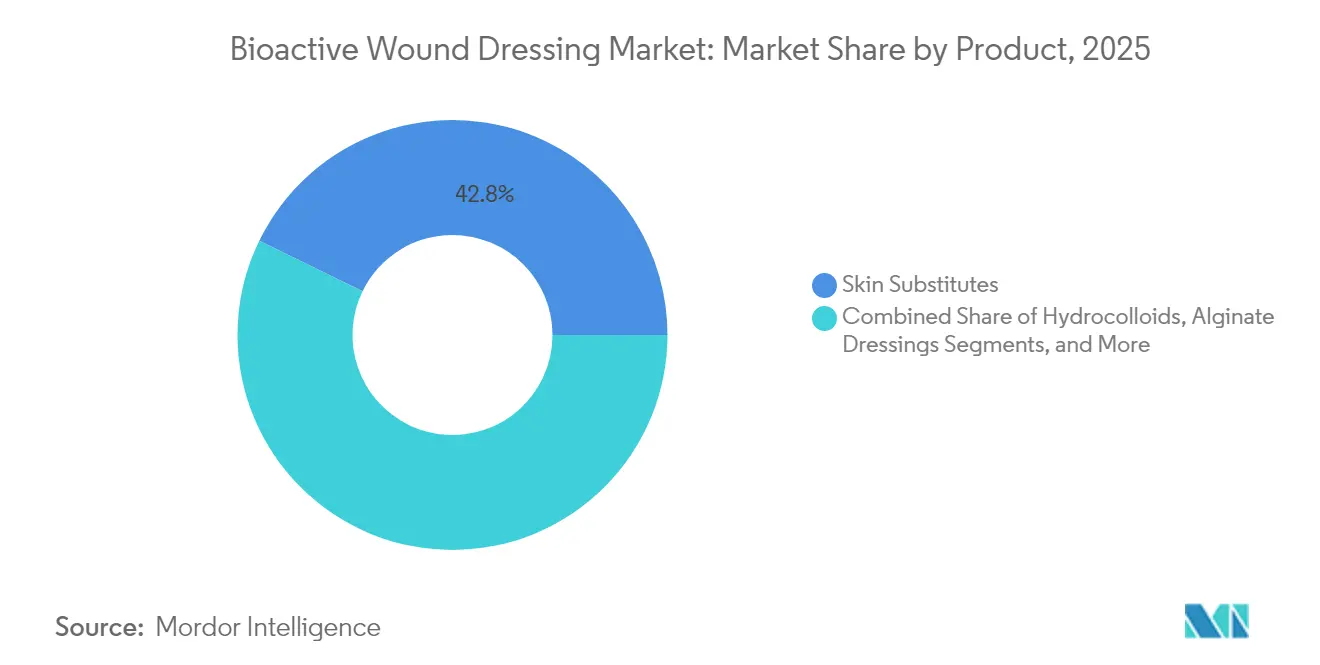

- By product category, skin substitutes led with 42.78% revenue share of the bioactive wound dressing market in 2025; smart bio-electronic dressings are projected to expand at an 10.95% CAGR through 2031.

- By application, surgical and traumatic wounds held 46.05% of bioactive wound dressing market share in 2025, while diabetic foot ulcers are forecast to grow at 11.18% CAGR to 2031.

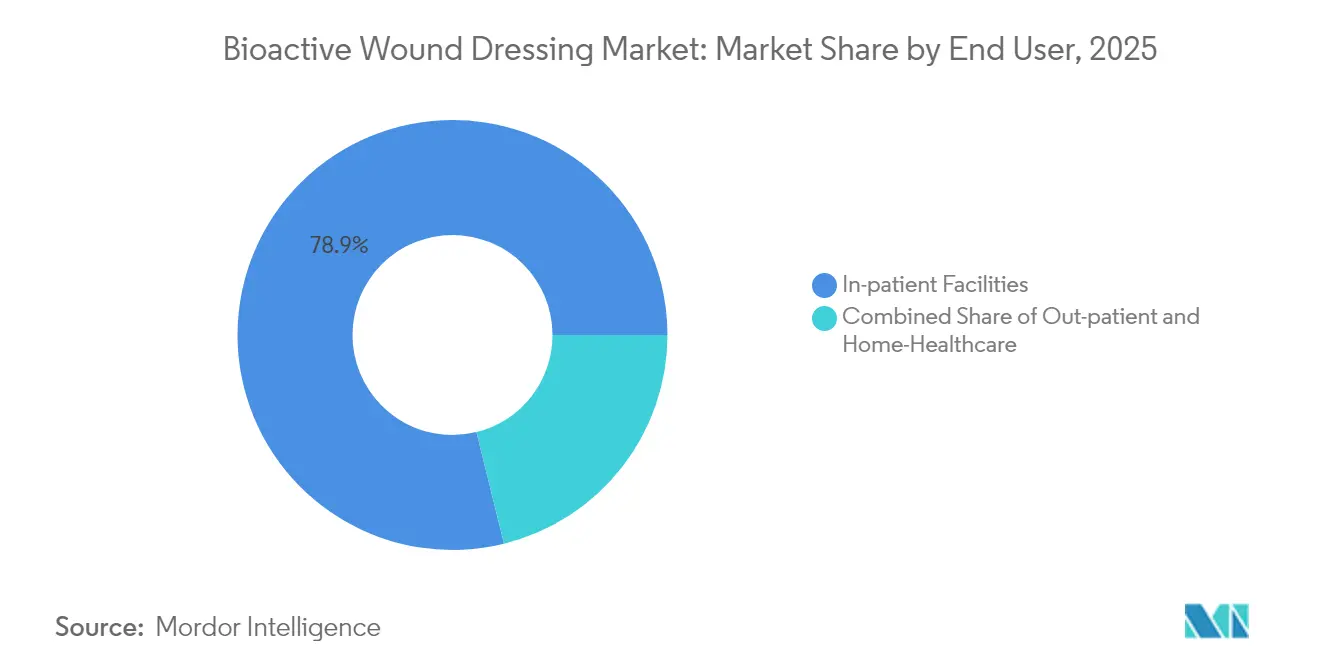

- By end user, inpatient settings held a 78.85% share of the bioactive wound dressing market in 2025; outpatient and ambulatory centers, with an 11.35% CAGR through 2031, represent the fastest-growing setting.

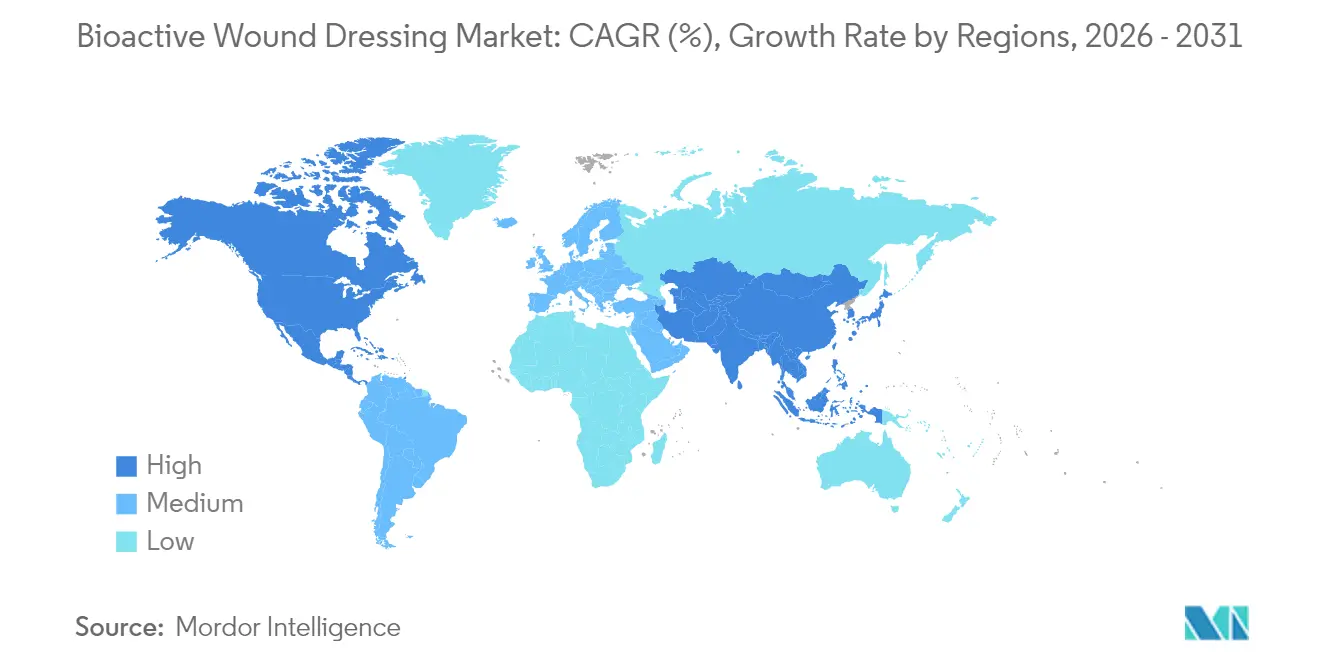

- By geography, North America maintained 42.30% revenue share of the bioactive wound dressing market in 2025, whereas Asia-Pacific is advancing at an 11.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bioactive Wound Dressing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of chronic wounds & diabetes | +2.8% | Global, strongest in North America & Asia-Pacific | Long term (≥ 4 years) |

| Rapid innovation in biomaterial science | +2.1% | Global, led by North America & Europe | Medium term (2-4 years) |

| Rising geriatric population & surgery volumes | +1.9% | Global, focused on developed markets | Long term (≥ 4 years) |

| Wider reimbursement of bioactive dressings | +1.7% | North America & Europe | Medium term (2-4 years) |

| Emergence of smart bio-electronic dressings | +1.4% | North America, expanding in Asia-Pacific | Short term (≤ 2 years) |

| Defense & remote-trauma fish-skin grafts | +0.6% | North America, Nordic countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing burden of chronic wounds & diabetes

Global diabetes now affects more than 537 million adults, and diabetic foot ulcers reach 15-25% of that population, creating persistent demand for advanced solutions that can cut healing time by 30-40% compared with gauze. Chronic wounds afflict 6.7 million Americans and drive USD 50 billion in direct annual treatment costs; evidence shows platelet-rich plasma dressings achieve 65% complete closure in 12 weeks versus 40% with standard care. Clinical superiority supports premium pricing and drives physician adoption, especially among older patients whose healing capacity declines with age.

Rapid innovation in biomaterial science (hydrogels, alginate composites)

Next-generation hydrogels possess self-healing properties that restore up to 90% structural integrity within hours, while high-purity alginate extraction improves biocompatibility and addresses earlier supply bottlenecks. Smart-responsive polymers now adjust moisture, pH, and glucose gradients on the wound bed, accelerating epithelialization by 25% in clinical studies. Antimicrobial nanofibers containing silver or copper mitigate infection without compromising tissue regeneration, and nanodiamond additives add mechanical strength for chronic cases.

Rising geriatric population & surgery volumes

People aged 65+ require wound care at rates three to four times higher than younger cohorts, and global surgical demand rises commensurately. Advanced dressings have lowered hospital stays by more than one day after total knee arthroplasty, generating cost savings and higher patient satisfaction. Minimally invasive procedures, despite smaller incisions, still rely on precision moisture control that bioactive formulations provide.

Wider reimbursement of bioactive dressings in OECD countries

Medicare doubled allowable skin-substitute applications to eight per ulcer over 12 weeks in 2025, reflecting growing recognition of improved outcomes. European health-technology assessors likewise credit these products with up to 50% lower lifetime case costs, propelling physician uptake even at higher unit prices. Disparities remain in emerging economies where out-of-pocket payment slows adoption.

Emergence of smart bio-electronic dressings with in-situ sensors

Sensor-enabled dressings measure temperature, pH, and cytokine levels, warning clinicians of complications early and reducing readmissions; machine-learning algorithms forecast healing trajectories with 98% accuracy in pilot studies. Early adopters among trauma centers report 20% fewer dressing changes and higher nursing efficiency.

Defense & remote-trauma adoption of fish-skin grafts

Cold-water cod-skin matrices rich in omega-3 fatty acids provide natural scaffolding and anti-inflammatory benefits; U.S. military applications cut infection risk in austere settings. Field surgeons value shelf stability and simplified storage compared with human cadaver grafts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High product cost vs. traditional dressings | -1.8% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Reimbursement gaps in emerging markets | -1.5% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Supply-chain fragility for marine/biologic raw materials | -1.2% | Global, affecting alginate and fish-skin products | Short term (≤ 2 years) |

| Regulatory ambiguity around living-cell/IoT combination dressings | -0.9% | Global, most acute in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High product cost vs. traditional dressings

Advanced dressings range from USD 50-200 per unit, while standard gauze costs under USD 5, creating hurdles for cost-sensitive providers. The 2025 Physician Fee Schedule trimmed average reimbursement by 2.93%, pushing hospitals to justify premium selections; adoption rates in low-income countries trail by up to 70% despite documented 30-40% savings over an entire treatment episode.

Supply-chain fragility for marine/biologic raw materials

Seasonal seaweed harvests determine global alginate availability; climate shifts disrupt yields, and logistic costs add 15-20% to landed price. Fish-skin sourcing hinges on sustainable quotas and cross-border clearances that can delay shipments, prompting producers to investigate synthetic biology options likely needing three to five years before commercial scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Smart Dressings Drive Innovation

Smart bio-electronic dressings are the fastest-growing product group, expanding at an 10.95% CAGR and gradually lifting their share of the bioactive wound dressing market . Skin substitutes, however, retained a 42.78% bioactive wound dressing market share in 2025 owing to broad clinical familiarity and reimbursement coverage. The bioactive wound dressing market size for skin substitutes reached USD 1.66 billion in 2025 and continues to advance on the back of favorable clinical trials.

Traditional hydrocolloid and alginate sheets remain workhorses in high-volume surgical cases but face commoditization and margin squeeze. Collagen and chitosan dressings win favor for regenerative outcomes, particularly in reconstructive surgery. Sustainability concerns amplify interest in bacterial-cellulose and plant-based alternatives, while combination products that embed antimicrobials or growth factors secure higher price points because they shorten dressing cycles.

By Application: Diabetic Care Accelerates Growth

Surgical and traumatic wounds generated 46.05% of bioactive wound dressing market revenue in 2025, anchored by predictable procedure volumes and standardized care pathways. In contrast, diabetic foot ulcers post the highest trajectory at 11.18% CAGR, reflecting rising diabetes prevalence and evidence that fish-skin grafts yield 92% closure within 16 days compared with 75% under conventional care. The bioactive wound dressing market size for diabetic foot ulcer care surpassed USD 0.84 billion in 2025 and is climbing rapidly toward parity with surgical indications.

Burns, though lower in incidence, justify premium-priced biologic matrices that reduce scarring and pain. Pressure, venous, and arterial ulcers rely heavily on moisture-balance hydrogels and antimicrobial alginates; platelet-rich plasma and stem-cell impregnated fabrics hold promise for chronic complex sites but require robust cold-chain logistics, limiting uptake in resource-constrained geographies.

By End User: Outpatient Shift Transforms Delivery

Hospitals and inpatient centers commanded 78.85% of global revenue in 2025 as complex wounds necessitated clinician oversight, yet outpatient clinics and ambulatory surgery centers are expanding at 11.35% CAGR. The bioactive wound dressing market size in outpatient settings was USD 0.83 billion in 2025 and is forecast to double by 2031 as payers push lower-cost sites of care.

Telemedicine-enabled home health programs now pair sensor dressings with cloud dashboards, letting nurses monitor healing remotely and reducing travel burden for frail patients. Specialized wound centers act as hybrids, offering high-acuity care without full hospital costs; standardized AI-driven assessment tools ensure consistent treatment quality across sites.

Geography Analysis

North America led with 42.30% of bioactive wound dressing market share in 2025, buoyed by Medicare coverage expansion and robust clinical-evidence demands that reward differentiated technologies. Regional innovations such as Solventum’s V.A.C. Peel and Place Dressing have cut application time by 61% and overall costs by 41%, cementing provider confidence . Despite a 2.93% Medicare payment reduction in 2025, the region’s aging populace and high diabetes incidence sustain long-run demand; Department of Defense contracts worth USD 75 million underscore continued government backing for trauma solutions.

Asia-Pacific is the fastest-growing territory at 11.55% CAGR through 2031, propelled by rising incomes, insurance coverage, and modernizing regulatory frameworks. India’s updated marketing code for medical devices signals tighter compliance and smoother entry for foreign brands, while local manufacturing capacity drives competitive pricing. Clinical studies reveal biodegradable temporizing matrices achieve 94.6% healing rates across Asian cohorts, reinforcing clinician trust .

Europe records steady progress, supported by rigorous health-technology assessments that reward proven efficacy. HARTMANN reported EUR 608.9 million wound-care revenue in 2024, up 4.4% organically, reflecting demand for silicone super-absorbents that manage complex exudate scenarios. Sustainability priorities boost alginate and chitosan uptake, while post-Brexit regulatory alignment remains a moving target but is unlikely to derail continental adoption. Emerging markets in Latin America and Africa present long-term upside yet demand lower-cost variants and infrastructure-friendly supply chains.

Regulatory Landscape

Regulation for bioactive wound dressings is anchored in medical-device frameworks, but classification can shift upward when products include medically important antimicrobials or combine biologics with connected sensing. In the United States, the FDA device framework under 21 CFR Part 878 (General and Plastic Surgery Devices) supports 510(k) pathways for many wound dressings, while certain solid wound dressings, gels, creams, and ointments containing medically important antimicrobials are treated as Class III devices requiring premarket approval (PMA), reflecting heightened scrutiny tied to antimicrobial-resistance risk. This divergence pushes manufacturers to assemble stronger clinical and bench evidence packages early, particularly for antimicrobial and combination products.

In Europe, Regulation (EU) 2017/745 (EU MDR) governs market access and has increased documentation and post-market obligations for higher-risk wound-care technologies through 2026 implementation timelines. For bioactive materials, biocompatibility and chemical characterization are commonly structured around the ISO 10993 series (including ISO 10993-1 for biological evaluation planning, ISO 10993-12 for extraction conditions, and ISO 10993-11 for systemic toxicity), which remains a practical global anchor for material and process changes across collagen, alginate, chitosan, and next-generation hydrogel platforms.

Value Chain Analysis

The value chain starts with bio-derived and synthetic inputs, then moves through purification, formulation, manufacturing, sterilization, regulatory release, and multi-channel distribution into hospitals, outpatient wound centers, and home-health programs. Key upstream materials include bovine or porcine collagen, chitin-derived chitosan (including deep-sea sources), and medical-grade Manuka honey, all of which require clinical-grade purification and consistent lot controls. Midstream manufacturing commonly uses processes such as electrospinning and crosslinking (for example, with genipin or sodium tripolyphosphate) followed by terminal sterilization (often ethylene oxide), with quality systems designed to support material changes without destabilizing biocompatibility and performance.

Downstream, market access depends on regulatory submission strategy and channel execution, with many US products routed through 510(k) substantial-equivalence pathways, while more complex antimicrobial or combination technologies face higher evidentiary burdens. Recent corporate actions show value-chain optimization: AVITA Medical reported a contract manufacturing agreement supporting PermeaDerm Biosynthetic Wound Matrix production at its Ventura, California facility, alongside distribution amendments (March 2025). Mölnlycke announced a joint venture with Zhende Medical to integrate portfolios and expand advanced wound-care access in China, with operations targeted for Q3 2026 (May 2026). Distribution-led expansion also appears in bioactive portfolios, such as BioLab Holdings partnering with SweetBio to extend reach for APIS bioengineered wound products that use collagen and Manuka honey (April 2026).

Competitive Landscape

The bioactive wound dressing market remains moderately concentrated. Smith+Nephew, ConvaTec, and Mölnlycke collectively capture more than 40% of global revenue, leveraging legacy brands, multi-country sales teams, and extensive clinical data libraries. Smith+Nephew’s focused investment in negative-pressure therapy and large-surface biologic matrices positions it to retain hospital contracts, while ConvaTec emphasizes ostomy and wound synergy to cross-sell dressings.

Disruptors press incumbents on two fronts: biologic innovation and digital enablement. Kerecis built a fish-skin graft franchise that earned rapid U.S. and Nordic defense uptake thanks to natural omega-3 profiles linked to anti-inflammatory effects. Vomaris targets infection control with bioelectric micro-current dressings that deactivate pathogens without antibiotics, a strategic advantage as antimicrobial-resistance concerns mount.

Regulatory shifts reshape the field. The FDA proposes to reclassify antimicrobial coatings based on resistance risk, pushing higher-risk categories into premarket approval and favoring well-capitalized firms with deep regulatory capacity. Traditional device firms lacking sensor expertise increasingly partner with digital-health startups to embed analytics, creating blended offerings that deliver both physical healing and data-driven insights.

Bioactive Wound Dressing Industry Leaders

3M

B. Braun SE

Convatec Group PLC

Monlnlycke Health Care AB

Smith & Nephew PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is opening in regulatory-cleared, next-generation matrices and hydrogels that broaden clinician options beyond sheet dressings, particularly for irregular wound geometries and complex chronic sites where application technique and conformability drive outcomes. A visible proof point is the cadence of FDA 510(k) clearances in 2026 across material classes and formats: Medskin Solutions Dr. Suwelack AG received clearance for a modified MatriDerm (K261224) under an animal-derived dressing product code, ECM Therapeutics received 510(k) clearance (K253521) for ECMT-100 WMD as a flowable extracellular matrix hydrogel (June 2026), and Kreate Medical announced two 510(k) clearances for absorbable synthetic matrix lines including an antibacterial version (May 2026). These approvals support portfolio expansion across skin substitutes, extracellular-matrix hydrogels, and synthetic scaffolds, creating room for differentiated claims tied to handling, antimicrobial functionality, and wound-bed interaction.

A second opportunity area sits at the intersection of smart bio-electronic dressings and active microenvironment modulation, where bioelectronics, microfluidics, and stimulus-responsive hydrogels are being demonstrated in peer-reviewed 2026 research. As hospitals and outpatient programs adopt remote monitoring workflows, sensor-enabled dressings that track pH, temperature, or inflammatory markers align with efficiency goals such as fewer dressing changes and earlier complication detection already cited by early adopters in trauma settings within the report scope. Commercialization pathways for these connected products still need clearer regulatory positioning for combination device-software functions and stronger biocompatibility evidence for novel materials, making partnerships between wound-care incumbents and digital-health specialists a practical route to shorten development-to-market cycles.

Recent Industry Developments

- June 2026: ECM Therapeutics received FDA 510(k) clearance (K253521) for ECMT-100 WMD, a flowable extracellular matrix hydrogel designed for wound management. Flowable ECM formats expand the usable footprint of bioactive dressings in irregular anatomies and can strengthen competitive positioning in chronic-wound protocols that need conformability beyond sheets.

- May 2026: Mölnlycke Health Care announced a joint venture with Zhende Medical to integrate wound-care portfolios and accelerate access to advanced wound-care solutions in China, with operations planned to start in Q3 2026. The move adds local execution leverage in Asia-Pacific and supports faster commercialization and channel reach in a high-growth geography.

- July 2024: AVITA Medical expanded its portfolio with PermeaDerm Biosynthetic Wound Matrix as part of its advance wound care offerings. Broadening biosynthetic matrix options helps address hospital demand for regenerative coverings in surgical, traumatic, and complex chronic wounds while supporting bundling with adjacent wound-care products in provider contracts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues from bioactive wound dressings that actively support healing by interacting with the wound bed, such as collagen and alginate based dressings, chitosan or cellulose based materials, and related bio-derived matrices used in acute and chronic wound management.

Scope exclusions: Traditional gauze and basic dressings, negative pressure wound therapy devices, sutures and sealants, and topical pharmaceuticals are excluded from the sizing.

Segmentation Overview

- By Product

- Hydrocolloids

- Alginate Dressings

- Collagen-based Dressings

- Skin Substitutes (Acellular & Living)

- Antimicrobial/Silver Dressings

- Chitosan & Bacterial-Cellulose Dressings

- Growth-Factor / Stem-Cell Impregnated

- Smart Bio-electronic Dressings

- By Application

- Surgical & Traumatic Wounds

- Burns

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous & Arterial Ulcers

- Donor-Site & Other Chronic Wounds

- By End User

- In-patient Facilities

- Out-patient / Ambulatory Settings

- Home-Healthcare

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by matching the demand pool to clinical and utilization signals, then mapping where bioactive dressings sit within advanced wound care pathways. Public sources were used to anchor incidence and treatment patterns, such as CDC diabetes statistics, CMS coverage and payment policies, WHO health indicators, OECD health expenditure series, and peer-reviewed wound care journals that report healing outcomes and product adoption trends.

We also reviewed import and export trade statistics for relevant material categories, and regulator updates on product safety and recalls, such as FDA notices. Company public disclosures, including annual reports and investor presentations, were used to understand portfolio mix and geographic exposure. Where public reporting is limited, we cross-checked revenue splits using a paid subscription for company financials and intelligence. The desk sources referenced here are illustrative only, and additional public and paid references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on testing what share of advanced dressings is actually bioactive, and how usage varies by wound type, care setting, and reimbursement environment. Discussions included manufacturers, distributors, clinicians, and procurement stakeholders across APAC, EMEA, and the Americas. The input was then used to adjust assumptions on average selling prices, switching patterns within dressing classes, and utilization per treated patient.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 46% |

| Mid tier: 48% | Functional/Unit leaders: 39% | EMEA: 32% |

| Smaller Players: 15% | Managers: 47% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where treated wound volumes are reconstructed from epidemiology and procedure indicators, then filtered through the share that receives bioactive dressings in each care setting. To keep totals realistic, selective bottom-up checks were added, including supplier and channel feedback on category revenues, sampled price bands by material type, and sanity checks against typical usage rates per wound episode.

Key model inputs included diabetes prevalence and ulcer burden, aging population trends, surgical procedure volumes, and chronic wound case mix, such as diabetic foot ulcers and pressure ulcers. Reimbursement coverage signals were incorporated since they influence product access. Average selling price movement by dressing class and geography was also modeled. Forecasting relied mainly on scenario analysis supported by expert views on reimbursement tightening or expansion, clinical guideline changes, and capacity or supply constraints for bio-derived materials. Where direct volume signals were weak, we applied conservative adoption ramps and re-tested them in interviews until the assumptions aligned with observed switching and utilization behavior.

Data Validation & Update Cycle

Outputs were checked against independent indicators, including regional spend patterns for advanced wound care, reported growth in chronic wound patient loads, and price movements seen in tenders and hospital procurement.

Any variances were investigated before sign-off. If gaps remained large, assumptions were re-checked and follow-up calls were completed with relevant respondents to confirm channel and care-setting dynamics.

The model also goes through multi-step analyst reviews so that country totals, regional rollups, and global sums reconcile cleanly. Reports are refreshed annually, with interim updates when material events occur, such as reimbursement changes or major regulatory actions. Before delivery, a final pass is done to ensure the latest public data points and market signals are reflected.

Mordor Intelligence's Bioactive Wound Dressing Market Size Compared Against Other Published Estimates

Published values for this market can differ quite a bit, and the reason is usually not one single math error. The spread is often driven by how each study defines what counts as bioactive, which revenue point is captured (manufacturer price versus downstream sales), and which years and currencies are used for normalization.

In this study, the main gap driver is scope. Some estimates fold skin substitutes and broader bioactive wound care therapies into the same total, while this sizing keeps the count limited to bioactive wound dressings and excludes NPWT devices and topical drug treatments. This is why the 2026 starting value lands where it does for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.27 B (2026) | |

| Trade Publisher A | USD 3.32 B (2025) | Uses a different scope that combines bioactive dressings with skin substitutes, and the values are stated at factory gate level, which shifts totals versus end-market revenue capture. The base year and forecast window also differ, which changes how price and mix are carried forward. |

| Industry Report B | USD 3.80 B (2024) | Category labeling appears broader, with a type-based grouping that can include adjacent moist and antimicrobial wound care products that are not always bioactive by mechanism. The lower CAGR assumption and earlier base year reduce the implied ramp in adoption and pricing over time. |

The comparison indicates that scope and revenue capture choices explain most of the differences, followed by base-year timing and growth assumptions. By tying volumes to treated wound pools, checking price logic with practitioners and channels, and keeping inclusions consistent, the final number remains traceable to clear inputs and can be repeated when new data arrives.

Key Questions Answered in the Report

What is the current Bioactive Wound Dressing Market size?

The bioactive wound dressing market size is USD 4.27 billion in 2026 and is projected to reach USD 6.99 billion by 2031 at a 10.36% CAGR.

Who are the key players in Bioactive Wound Dressing Market?

3M, B. Braun SE, Convatec Group PLC, Monlnlycke Health Care AB and Smith & Nephew PLC are the major companies operating in the Bioactive Wound Dressing Market.

Which is the fastest growing region in Bioactive Wound Dressing Market?

Asia-Pacific is advancing at 11.55% CAGR, spurred by regulatory modernization, rising incomes, and expanding healthcare infrastructure.

Why are diabetic foot ulcers a strategic focus?

Diabetic foot ulcers are expanding at 11.18% CAGR because diabetes affects 537 million adults globally, and bioactive solutions significantly improve closure rates.

Page last updated on: