Biomaterial Wound Dressing Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 7.72 Billion |

| Market Size (2031) | USD 11.04 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

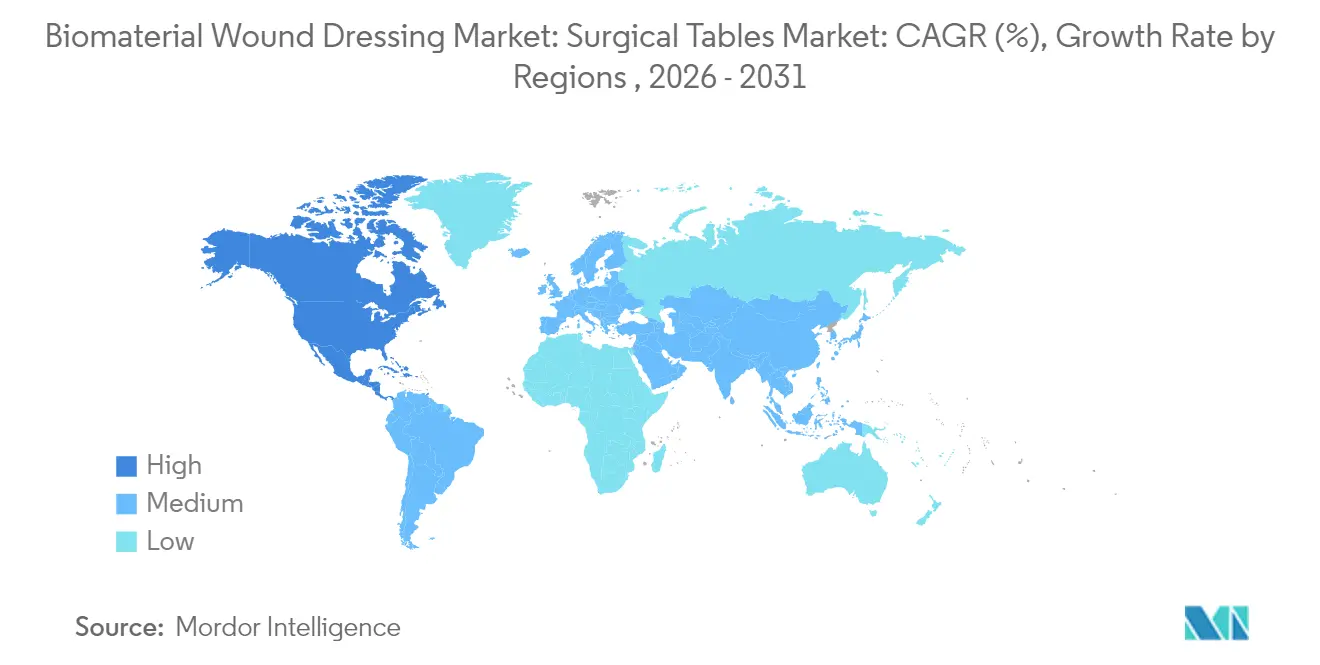

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

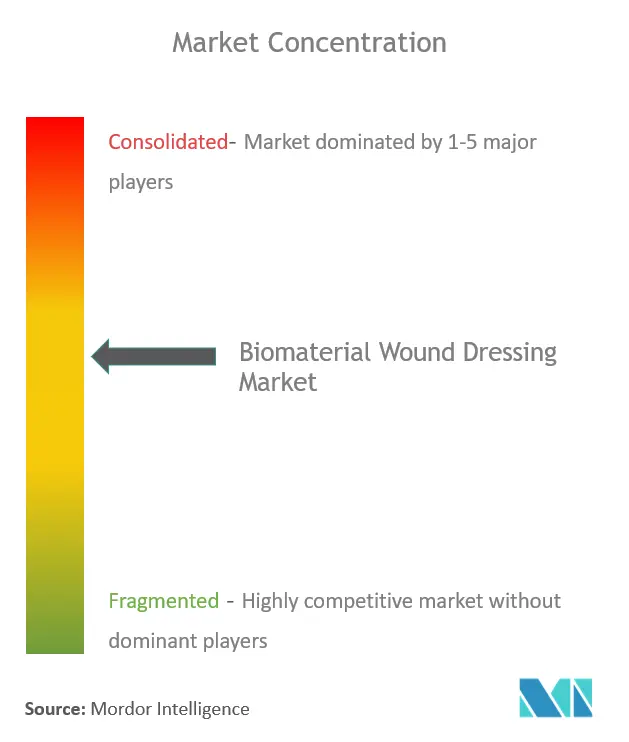

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Biomaterial Wound Dressing Market Analysis by Mordor Intelligence

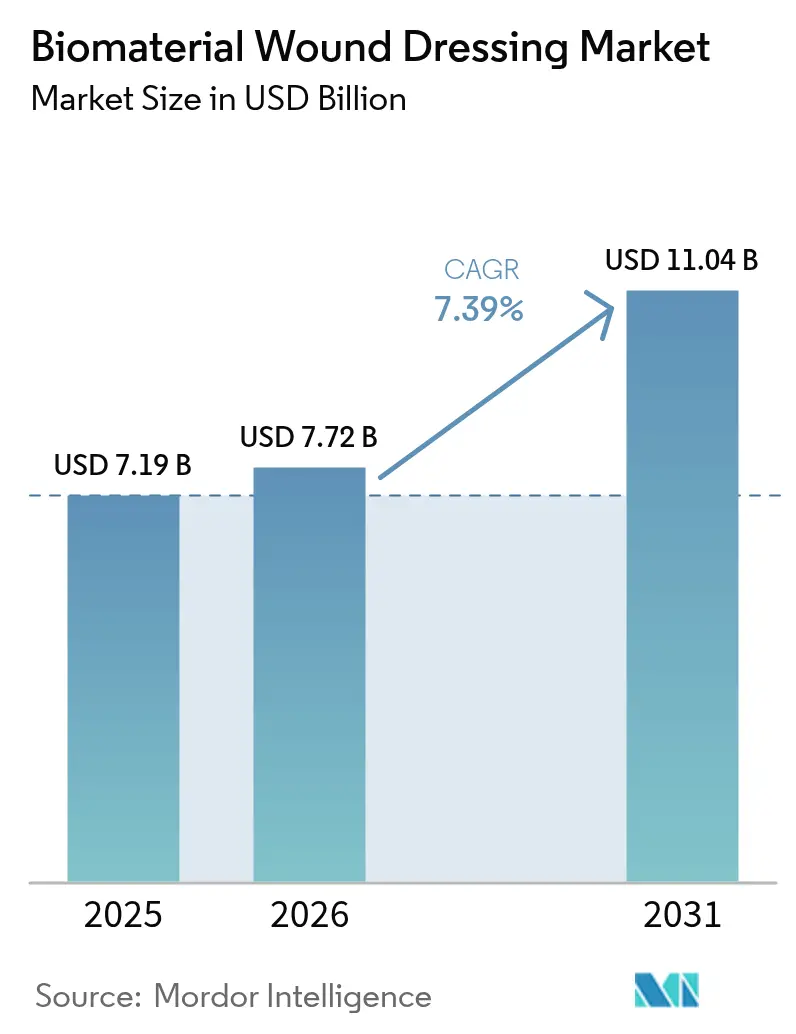

The biomaterial wound dressing market size is expected to grow from USD 7.19 billion in 2025 to USD 7.72 billion in 2026 and is forecast to reach USD 11.04 billion by 2031 at 7.39% CAGR over 2026-2031. Rising incidence of chronic wounds, rules that now demand clinical‐grade evidence for product claims, and hospital-to-home care shifts are reinforcing steady adoption of advanced biomaterial dressings. Military validation of chitosan hemostatic pads, mounting payer support for bioactive products, and new electro-spun nanofiber scaffolds are widening the remedy toolkit while keeping pricing networks resilient. Simultaneously, vertical integration across alginate supply chains and investments in in-house biocompatibility testing are emerging as key risk-mitigation strategies. Overall, the biomaterial wound dressing market is moving into a phase where platform-based dressings that combine moisture control, infection prevention, and real-time monitoring are favored for their ability to shorten healing cycles and curb total treatment costs.

Key Report Takeaways

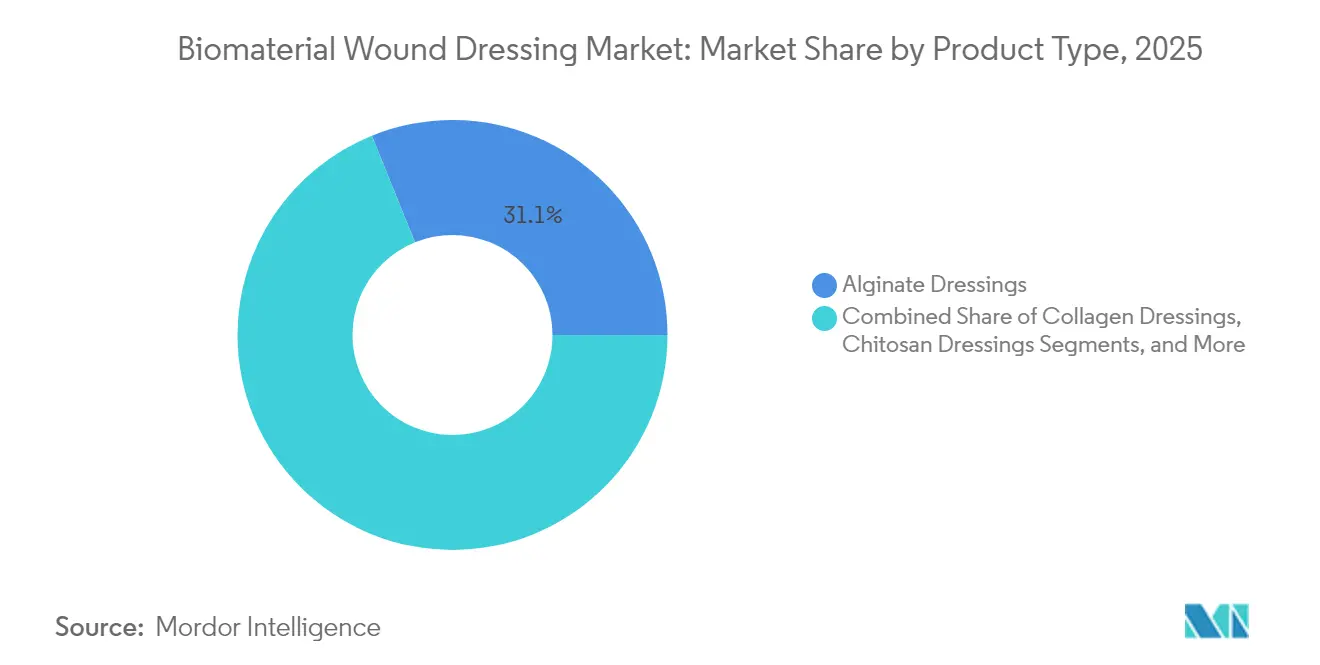

- By product type, alginate dressings led with 31.12% revenue share in 2025, while chitosan dressings are projected to expand at a 7.70% CAGR through 2031.

- By material source, natural biomaterials held 54.88% of the biomaterial wound dressing market share in 2025, whereas composite biomaterials record the highest projected 7.93% CAGR to 2031.

- By mechanism, moisture-retentive dressings commanded 42.96% share of the biomaterial wound dressing market size in 2025, and bioactive/intelligent dressings are slated to grow at an 8.03% CAGR.

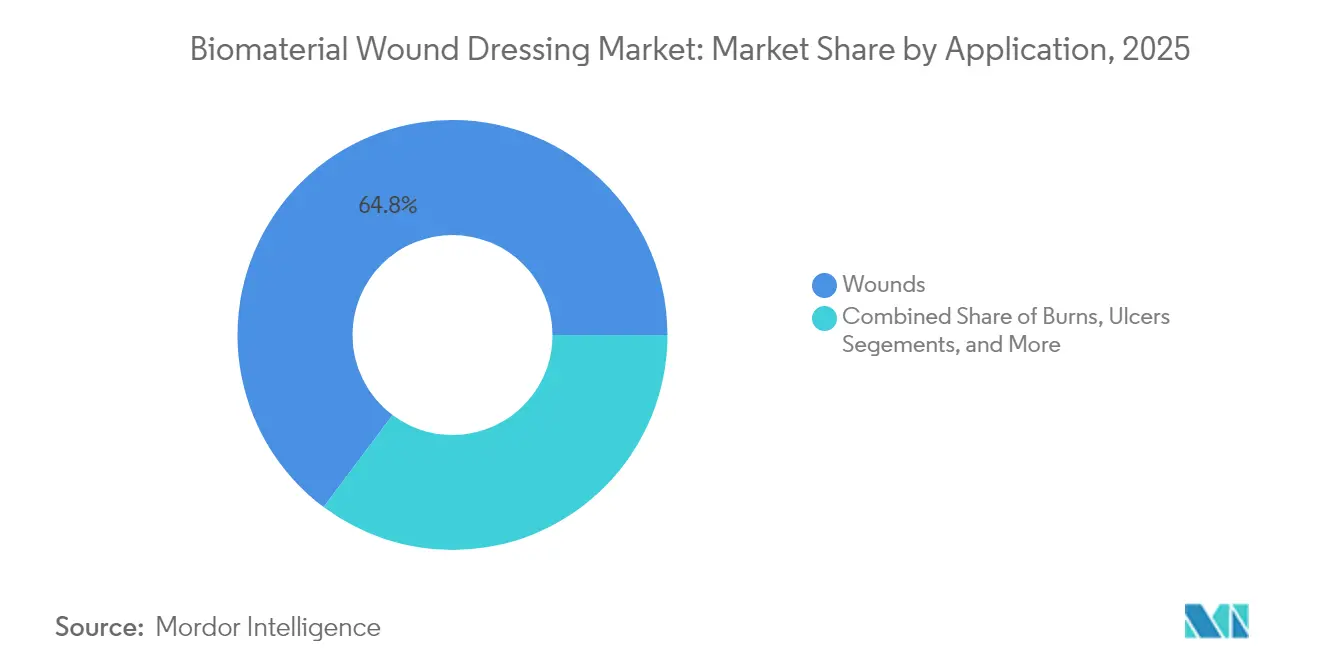

- By application, general wound care accounted for 64.77% share in 2025, while traumatic injury care is advancing at an 8.14% CAGR through 2031.

- By end-user, hospitals held 60.69% share in 2025; home healthcare is the fastest-growing channel at an 7.84% CAGR.

- By geography, North America captured 45.02% of the biomaterial wound dressing market in 2025, yet Asia-Pacific shows the quickest 8.58% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biomaterial Wound Dressing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for evidence-based advanced dressings | +1.2% | Global, early adoption in North America & EU | Medium term (2-4 years) |

| Rising diabetic & geriatric chronic-wound pool | +1.8% | Major impact in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Surge in outpatient surgery & home-based care | +1.1% | North America & EU core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Reimbursement expansion for bioactive dressings | +0.9% | North America & EU, selective Asia-Pacific markets | Medium term (2-4 years) |

| Breakthroughs in electro-spun nanofiber scaffolds | +0.8% | Global, led by North America & Europe R&D hubs | Long term (≥ 4 years) |

| Military adoption of chitosan hemostatic pads | +0.4% | Global, defense procurement cycles | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory push for evidence-based advanced dressings

Regulators are shifting from material-class exemptions to performance-based benchmarks. The FDA’s proposal to reclassify antimicrobial dressings into Class II and III status will compel companies to submit more clinical data, filtering out commodity products that lack safety validation. European rule makers are layering environmental metrics over traditional risk assessments, spurring design teams to favor biodegradable polymers that meet both safety and sustainability tests. Device sponsors with in-house ISO 10993 labs now enjoy shorter approval cycles because third-party queuing delays no longer erode their speed-to-market advantage.

Rising diabetic & geriatric chronic-wound pool

Global diabetes prevalence is expected to reach 643 million adults by 2030, and roughly one-third will face diabetic foot ulcers at some point in their lives. Clinical trials demonstrate that collagen dressings deliver 54.5% mean wound-area reduction in chronic ulcers compared with 38.8% for conventional gauze, tightening payer focus on solutions that cut infection rates and readmissions. As population aging intensifies immune compromise and slows re-epithelialization, demand for bioactive scaffolds that curb inflammation and stimulate angiogenesis will remain durable.

Surge in outpatient surgery & home-based care

Ambulatory surgical centers now perform complex procedures once limited to inpatient beds, transferring post-op wound care burden to patients and family caregivers. An all-in-one negative-pressure dressing launched in 2024 trims application time by 61% and maintains integrity for seven days, aligning with staffing shortages in home care settings [1]Solventum, “Solventum Launches All-In-One, Extended-Wear Wound Dressing for V.A.C. Therapy," solventum.com. Telehealth-enabled bandages equipped with color-change sensors alert remote clinicians when exudate saturation warrants a change, reducing home nurse visits and widening payer enthusiasm for value-based reimbursement.

Reimbursement expansion for bioactive dressings

UnitedHealthcare and other large payers now reimburse skin substitutes such as EpiFix after four weeks of failed standard care, signaling a gradual broadening of coverage criteria. The temporary halt of Local Coverage Determinations (LCDs) on skin substitutes in 2025 prevents uncertainty-driven stocking cuts by hospitals, keeping the biomaterial wound dressing market buffered during policy realignment. As cost-effectiveness dossiers accumulate, formularies are expected to approve additional products that document fewer clinic visits and faster closure times.

Breakthroughs in electro-spun nanofiber scaffolds

Clinicians in multi-center trials reported that 46.6% of chronic-wound patients treated with a nanofiber spray reached full epithelialization without rehospitalization, versus none in control cohorts. Nanofiber-coated cotton integrating lawsone compounds eradicated multidrug-resistant bacteria and accelerated closure in animal models, underscoring the technology’s dual antimicrobial and regenerative merit. Multi-nozzle electro-spinning rigs now balance throughput and fiber uniformity, easing prior bottlenecks that impeded commercial scaling.

Military adoption of chitosan hemostatic pads

Defense health agencies are procuring chitosan dressings to stop arterial bleeding within the “golden five minutes,” validating their use under extreme conditions. Traumagel earned FDA approval in 2025 and is being positioned for civilian trauma rooms and ambulances [2]Bios Scientia Publishers, “Traumagel FDA Approval," bioscientiapublishers.com. A Department of Defense contract worth USD 75 million for advanced wound therapy systems further demonstrates defense sector commitment and de-risks revenue for scaled suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented raw alginate supply chain | -0.7% | Global, concentrated impact on seaweed-dependent regions | Medium term (2-4 years) |

| Stringent biocompatibility validation timelines | -0.5% | Global, particularly affecting new market entrants | Long term (≥ 4 years) |

| Recycling-disposal concerns for silver-laden dressings | -0.4% | EU & North America core, expanding to APAC | Medium term (2-4 years) |

| Price sensitivity in low- & middle-income settings | -0.6% | APAC, MEA, Latin America, with spillover to cost-conscious segments globally | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Fragmented raw alginate supply chain

Most alginate comes from brown seaweed harvested in a narrow seasonal window, exposing dressings makers to raw-material price swings and stock-out risks. Studies show cultivated kelp can match wild-harvest quality when enzyme-based extraction replaces chemical methods, but adoption is still nascent [3]Phys.org, “New Alginate Extraction Method May Help Cultivated Kelp Be as Good as Wild Kelp," phys.org. With alginate demanded by over 600 product categories, vertical integration—either by acquiring seaweed farms or securing offtake contracts—is emerging as a hedge against supply shocks.

Stringent biocompatibility validation timelines

A full ISO 10993 battery can consume 18 months and several million dollars when novel polymers or nanomaterials are involved. Small developers often face financing gaps while waiting for cytotoxicity, sensitization, and chronic-toxicity readouts, allowing incumbents with GLP-certified labs to secure first-mover status. Although risk-based shortcuts exist for well-characterized materials, hybrid composites still trigger exhaustive endpoint panels, elongating time-to-market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Alginate leadership faces chitosan momentum

Alginate dressings captured 31.12% of the biomaterial wound dressing market in 2025 because their gel-forming fibers lock in exudate while maintaining a micro-moist healing climate. Yet the same year saw chitosan pads deliver the fastest 7.70% CAGR trajectory, bolstered by battlefield proof and strong antimicrobial credentials. Collagen dressings continue to win chronic-wound protocols owing to their extracellular-matrix mimicry, whereas composite dressings add super-absorbent layers or antimicrobial nanoparticles to broaden indications.

Over the forecast horizon, alginate incumbents are moving into proprietary blends that combine alginate’s absorptivity with chitosan’s clot-triggering chains, counteracting share erosion. Skin-substitute sheets command premium pricing thanks to tissue-engineering complexity, and spider-silk prototypes with tensile strength rivaling steel are now in pre-clinical programs. Collectively, the biomaterial wound dressing market will likely see a migration toward multi-mechanism sheets that consolidate absorption, hemostasis, and antibacterial effects within a single change interval.

By Material Source: Natural dominance meets composite ingenuity

Natural polymers account for 54.88% of the biomaterial wound dressing market size because clinicians trust their biocompatibility and biodegradability, and governments favor sustainable supply chains. Composite materials, however, lead projected growth at 7.93% CAGR as they unite natural chains like chitosan with electro-spun synthetics that add tensile strength and programmable release kinetics. Pure synthetic options are still viewed warily when microplastic residues are flagged by environmental health agencies, but fully bio-based synthetics are progressing through pilot lines.

In practice, the next wave of composite sheets may integrate plant-derived cellulose nanocrystals with bio-resorbable polyesters to balance mechanical endurance and eco-friendly disposal. Device sponsors that master solvent-free manufacturing will likely benefit from easing regulatory audits and lower carbon disclosures, attributes that payers increasingly embed into procurement scorecards. As such, composite material vendors will gain bargaining power across a biomaterial wound dressing market eager for greener, tougher, and data-rich dressings.

By Mode of Mechanism: Moisture control reigns as intelligence rises

Moisture-retentive dressings held 42.96% share of the biomaterial wound dressing market size in 2025 because fluid balance remains the cornerstone of epithelial cell migration. Nonetheless, bioactive and intelligent dressings hold the top growth slot with an 8.03% CAGR, propelled by smart sensors that flag pH spikes or bacterial load before visual symptoms arise. Hemostatic pads, historically used in field trauma, are entering dialysis centers where anticoagulant patients need fast closure at access sites.

The ecosystem is also seeing electroactive sheets that emit micro-currents to accelerate angiogenesis, pushing efficacy beyond passive moisture management. Early trials record 99.75% closure against 94% for conventional moist therapy, hinting at step-change outcomes. As hospitals ease into remote monitoring, intelligent bandages that transmit data to clinician dashboards can justify higher unit prices by trimming unplanned outpatient visits.

By Application: Chronic wounds anchor volume; trauma care outpaces

Wounds represented 64.77% of 2025 revenue, underpinning the biomaterial wound dressing market with steady patient inflows from pressure ulcers, venous leg ulcers, and post-operative incisions. Yet traumatic injuries—spanning battlefield, road accidents, and industrial mishaps—register the briskest 8.14% CAGR through 2031 as military field kits become civilian EMS staples. Burns remain a high-margin niche where filmic dressings infused with growth factors reduce graft frequency and inpatient days.

Looking forward, trauma centers may embrace chitosan-based foams that halt spurting hemorrhage inside 300 seconds, while diabetic clinics deploy collagen matrices that down-regulate chronic inflammation markers. Each sub-segment will continue to demand tailored absorption rates, conformability profiles, and exchange intervals, driving portfolio diversification across the biomaterial wound dressing market.

By End-User: Hospitals anchor scale; home care accelerates

Hospitals retained 60.69% share in 2025 because complex wounds still rely on surgical debridement, negative-pressure rigs, and multi-disciplinary oversight found primarily in acute facilities. Nevertheless, home healthcare logs the fastest 7.84% CAGR as insurers champion lower-cost settings and self-care friendly dressings. Specialty outpatient wound clinics and long-term care facilities form the “other” cluster that demands extended-wear sheets with intuitive change indicators.

Telemedicine is easing remote oversight; smart bandages now transmit exudate volume trends and detect odor-causing anaerobes, leading to fewer clinic trips. Manufacturers are thus embedding peel-and-place applicators, color cues, and step-by-step QR code tutorials to cut training minutes. The biomaterial wound dressing market will therefore pivot toward patient-centric form factors that don’t sacrifice clinical rigor.

Geography Analysis

North America holds 45.02% of the biomaterial wound dressing market owing to robust reimbursement pathways, dense trauma centers, and early adoption of sensor-embedded sheets. FDA clarity on Class II and III filings sustains a predictable pipeline, encouraging venture capital for start-ups that target unmet diabetic foot ulcer needs. Academic-industry collaborations further shorten ideation-to-trial cycles, making the region a crucible for next-generation scaffolds.

Europe represents a mature but environmentally mindful region where Medical Device Regulation (MDR) compliance now intertwines product safety with life-cycle sustainability. Suppliers with biodegradable substrates and take-back recycling programs are earning procurement points from national health services. Sweden’s appetite for advanced dressings illustrates payer readiness to reimburse premium composites when clinical dossiers show reduced nursing hours.

Asia-Pacific posts the highest 8.58% CAGR as urbanization and lifestyle diseases swell chronic-wound caseloads. China is forming extramural wound-care networks that coordinate outpatient clinics, telehealth, and standardized protocols—expanding the addressable base for intelligent dressings. Japan’s clear but intricate device nomenclature under PMDA slows entry for smaller firms yet rewards those that complete the pathway with strong physician trust. India’s regulatory flux keeps domestic output subdued, but rising imports meet only a fraction of its vast need, opening doors for cost-effective natural polymer solutions.

Competitive Landscape

The biomaterial wound dressing market is moderately fragmented: legacy device multinationals command flagship alginate and collagen lines, while focused innovators disrupt with nanofiber sprays and AI-enabled smart sheets. Platform strategies dominate; firms are bundling moisture-control films, antimicrobial nanoparticles, and biosensor arrays into single SKUs that are coded under unified HCPCS reimbursement lines.

Vertical integration trends continue as alginate shortages prompt buyers to secure kelp farms or ink decade-long supply contracts, buffering them against commodity shocks. Concurrently, companies with ISO 10993 suites in-house shorten product iteration loops and amass broader portfolios without incurring third-party lab delays. Technology alliances—such as polymer chemists pairing with semiconductor sensor teams—are accelerating the intelligence layer atop traditional dressings.

Emerging white space lies in personalized wound-care algorithms: platforms that ingest patient comorbidities, wound geometry, and exudate composition to recommend dressing type, change cadence, and adjunct therapy. FDA’s 2024 clearance of Symvess, an acellular tissue engineered vessel, underlines regulatory willingness to approve novel biomaterial constructs beyond planar sheets, setting precedence for three-dimensional scaffolds in complex trauma scenarios.

Biomaterial Wound Dressing Industry Leaders

-

ConvaTec Group PLC

-

Smith & Nephew PLC

-

Mölnlycke Health Care AB

-

B. Braun Melsungen AG

-

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SolasCure received FDA Fast Track Designation for Aurase Wound Gel to treat calciphylaxis ulcers, a serious condition with high mortality rates. The hydrogel releases Tarumase, a recombinant enzyme targeting fibrin, collagen, and elastin in wounds, currently in Phase II trials for venous leg ulcers.

- May 2025: Smith+Nephew secured a USD 75 million Department of Defense contract to supply advanced wound therapy systems, demonstrating military sector confidence in biomaterial technologies and creating revenue visibility for defense applications.

- June 2022: Collagen Matrix, a United States-based regenerative medicine firm, received 510(k) clearance from the Food and Drug Administration for a new fibrillar collagen wound dressing, an absorbent microfibrillar matrix used to treat wounds.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the biomaterial wound dressing market as all advanced coverings fabricated from naturally sourced or bio-engineered polymers, such as alginate, collagen, chitosan, hyaluronic acid, and multi-layer composites, that maintain moisture, deliver bioactive cues, and actively support tissue regeneration in acute or chronic wounds. The value reflects only factory-built sterile dressings supplied to healthcare or home-care channels at ex-works pricing.

Scope exclusion: Topical antiseptic solutions, traditional cotton or gauze pads, negative-pressure kits, and standalone growth-factor injectables are outside this scope.

Segmentation Overview

-

By Product Type

- Hydrocolloids

- Alginate Dressings

- Collagen Dressings

- Chitosan Dressings

- Skin Substitutes

- Composite / Combination Dressings

- Other Products

-

By Material Source

- Natural Biomaterials

- Synthetic Biomaterials

- Composite Biomaterials

-

By Mode of Mechanism

- Moisture-Retentive

- Antimicrobial

- Haemostatic

- Bioactive / Intelligent

-

By Application

- Wounds

- Burns

- Ulcers

- Surgical Incisions

- Traumatic Injuries

- Other Applications

-

By End-User

- Hospitals

- Home Healthcare

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed clinicians in burns units, diabetic-foot specialists, procurement managers at hospital groups across North America, Europe, and Asia-Pacific, as well as product managers from dressing manufacturers. These discussions validated dressing utilization rates, price dispersion, and the speed at which chitosan and hybrid composites penetrate protocol guidelines, helping us reconcile desk-based assumptions.

Desk Research

We begin by mapping the treated-wound universe through public datasets from the World Health Organization, International Diabetes Federation, OECD Health Statistics, United States HCUP surgical discharge files, and Eurostat hospital activity records. Trade associations such as the European Wound Management Association and Advanced Wound Care Coalition supply prevalence benchmarks, reimbursement shifts, and technology adoption timelines. Company 10-Ks, investor decks, and regulatory filings clarify product mix and average selling prices, which are then supplemented with shipment traces from Volza, news flow captured on Dow Jones Factiva, and patent insights via Questel. This set is illustrative; many additional open and paid sources underpin our desk work.

Market-Sizing & Forecasting

A top-down prevalence-to-treatment model converts chronic-wound patient pools and surgical incidence into dressing-volume demand, followed by selective bottom-up checks using sampled ASP × unit data from major suppliers and distributors. Key variables include diabetic population growth, trauma admissions, average dressing sets per patient episode, reimbursement coverage breadth, composite-material adoption curves, and country-level currency shifts. Forecasts employ multivariate regression blended with scenario analysis to capture regulatory or pricing shocks. Coefficients are stress-tested with expert panels before finalization. Gaps where bottom-up samples are thin are bridged through weighted regional proxies and sensitivity ranges.

Data Validation & Update Cycle

Outputs pass a multi-layer review: automated variance flags, peer analyst cross-checks, and senior sign-off. Reports refresh annually, with interim revisions when material events, such as major reimbursement changes or large recalls, occur. A final validation run is completed just before release so clients receive the latest view.

Why Mordor's Biomaterial Wound Dressing Baseline Commands Reliability

Published estimates often differ because firms vary product scope, price capture points, update cadence, and underlying clinical assumptions. Our disciplined selection of wound types, inclusion of both hospital and home-care channels, and annual refresh ensure a balanced reference point.

Key gap drivers emerge when other publishers exclude composite bio-dressings, freeze ASPs, or rely on sales audits limited to high-income hospitals. Mordor's model, by contrast, layers patient epidemiology with dynamic price ladders confirmed through field interviews, providing consistency across geographies and time.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.19 B (2025) | Mordor Intelligence | - |

| USD 6.63 B (2024) | Global Consultancy A | Counts only top hospital SKUs; omits home-care volumes |

| USD 5.80 B (2023) | Trade Journal B | Excludes composite and nanofiber dressings |

| USD 6.18 B (2025) | Industry Association C | Uses flat global ASP without channel mix adjustment |

Taken together, the comparison shows that when scope breadth and variable rigor tighten, figures converge toward Mordor's benchmark. Clients therefore gain a transparent, reproducible baseline rooted in clearly stated drivers and regular validation.

Key Questions Answered in the Report

What is the current Biomaterial Wound Dressing Market size?

The biomaterial wound dressing market size stands at USD 7.72 billion in 2026 and is tracking toward USD 11.04 billion by 2031 at a 7.39% CAGR.

Who are the key players in Biomaterial Wound Dressing Market?

ConvaTec Group PLC, Smith & Nephew PLC, Mölnlycke Health Care AB, B. Braun Melsungen AG and 3M are the major companies operating in the Biomaterial Wound Dressing Market.

Which is the fastest growing region in Biomaterial Wound Dressing Market?

Asia-Pacific is forecast to expand at an 8.58% CAGR through 2031, driven by rising chronic diseases and broadening healthcare access.

Which region has the biggest share in Biomaterial Wound Dressing Market?

In 2025, the North America accounts for the largest market share in Biomaterial Wound Dressing Market.

Why are composite biomaterials gaining attention?

Composite dressings merge natural polymers with engineered scaffolds, delivering the biocompatibility clinicians demand plus greater mechanical strength and controlled drug release.

Page last updated on: