Dental Bone Void Filler Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

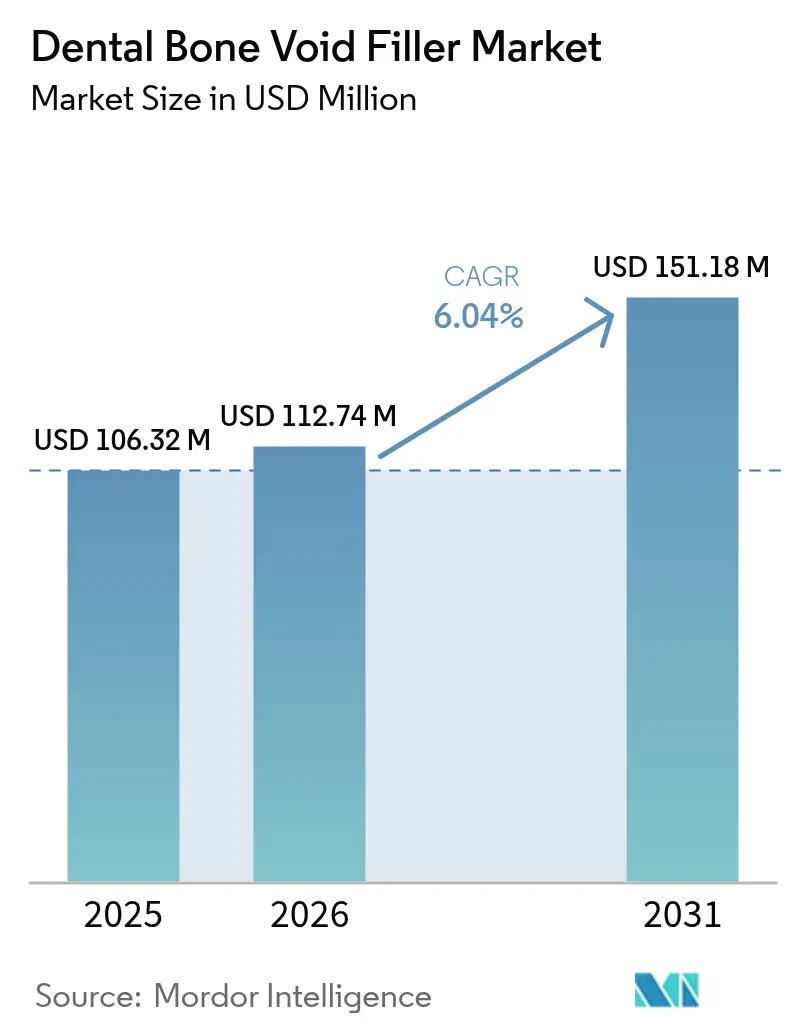

| Market Size (2026) | USD 112.74 Million |

| Market Size (2031) | USD 151.18 Million |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Bone Void Filler Market Analysis by Mordor Intelligence

The dental bone void filler market size was valued at USD 106.32 million in 2025 and estimated to grow from USD 112.74 million in 2026 to reach USD 151.18 million by 2031, at a CAGR of 6.04% during the forecast period (2026-2031). Demand expands as aging populations require complex implant procedures, while next-generation bioceramics improve osteoinduction and address autograft morbidity. North American clinicians adopt premium biomaterials quickly because of robust reimbursement structures and well-defined regulatory pathways. Asia-Pacific registers the fastest growth as dental tourism, rising disposable incomes, and technology transfer accelerate high-value procedure volumes. Moderate industry fragmentation continues to narrow as leading device manufacturers invest heavily in 3D printing and nanotechnology to differentiate product portfolios.

Key Report Takeaways

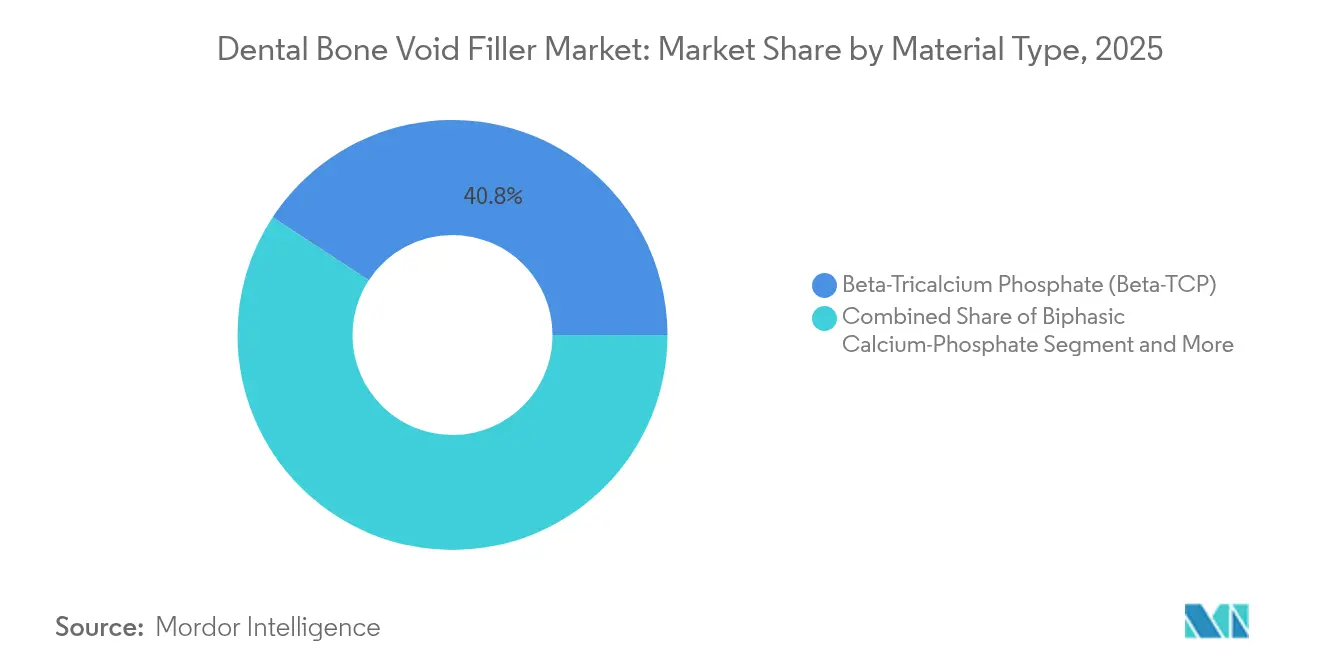

- By material type, β-tricalcium phosphate led with 40.78% of the dental bone void filler market share in 2025, whereas calcium-phosphate cements are projected to grow at a 9.03% CAGR through 2031.

- By form factor, granules accounted for 40.12% of the dental bone void filler market size in 2025; injectable formats are advancing at an 8.12% CAGR to 2031.

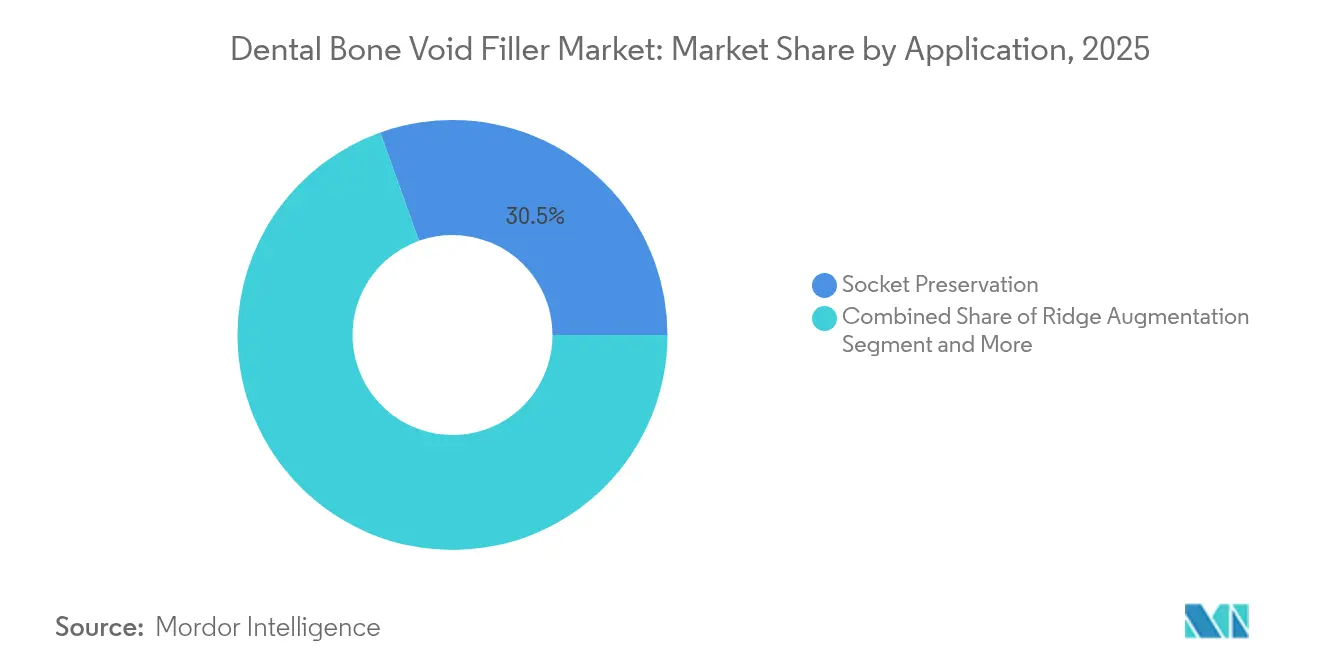

- By application, socket preservation held 30.45% revenue share of the dental bone void filler market size in 2025, while ridge augmentation is forecast to expand at a 9.01% CAGR.

- By end user, dental clinics captured 37.26% of the dental bone void filler market size in 2025, and ambulatory surgical centers record the highest CAGR at 8.37% through 2031.

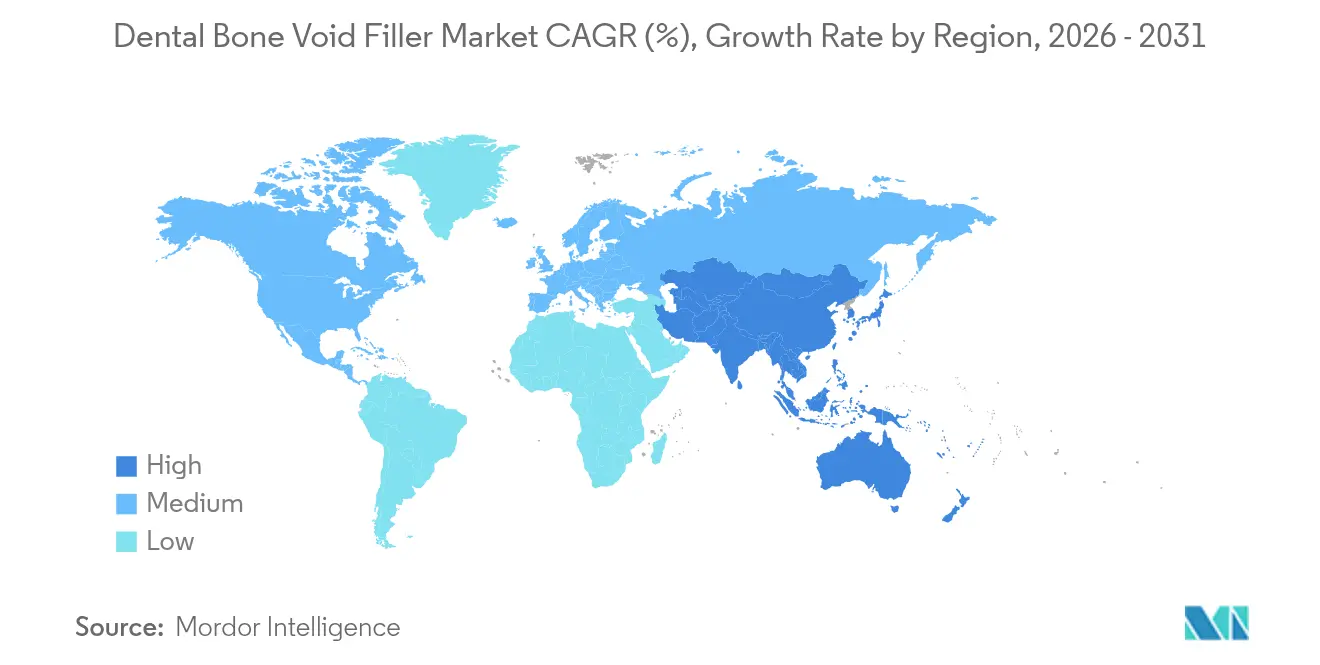

- By geography, North America commanded 35.41% of the dental bone void filler market in 2025, yet Asia-Pacific is growing at a 9.33% CAGR on the back of dental-tourism inflows.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Bone Void Filler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption Of Bioceramics For Dental Reconstruction | +1.8% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Rapid Rise In Dental-Implant Procedures Among Aging Population | +2.1% | North America & Europe core, expanding to APAC | Long term (≥ 4 years) |

| Advances In Synthetic Biomaterials (Nano-HA, β-TCP) Enhancing Osteoinduction | +1.4% | Global, led by R&D centers in US, Germany, Switzerland | Medium term (2-4 years) |

| Chair-Side 3-D Printing Of Custom Graft Scaffolds | +0.9% | North America & Europe, emerging in urban APAC | Short term (≤ 2 years) |

| Dental-Tourism-Led Demand Surge In Cost-Competitive APAC & MEA Hubs | +1.2% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Bioceramics for Dental Reconstruction

Next-generation, ion-doped hydroxyapatite and β-TCP formulations demonstrate superior bone formation and reduced inflammatory response. Fluorine-incorporated hydroxyapatite significantly accelerates socket healing by modulating macrophage activity. Clinicians embrace these synthetic options to avoid donor-site morbidity and achieve predictable outcomes. Broader regulatory acceptance and positive long-term data boost surgeon confidence. As prices stabilize, adoption permeates mid-tier markets, reinforcing the dental bone void filler market growth.

Rapid Rise in Dental-Implant Procedures Among Aging Population

A global cohort of more than 280 million older adults experiences tooth loss yet seeks fixed restorations rather than dentures. Implant success exceeding 95% when supported by quality grafts fuels procedure volumes. Age-related alveolar resorption necessitates bone augmentation, anchoring sustained demand for fillers. Public-health campaigns that emphasize oral health in senior care further lift procedure utilization. Consequently, the dental bone void filler market benefits from demographics that ensure multi-year procedural pipelines.

Advances in Synthetic Biomaterials (Nano-HA, β-TCP) Enhancing Osteoinduction

Nanostructuring increases surface area, improving protein adsorption and cellular attachment. Nano-hydroxyapatite doped with antibacterial ions offers mechanical strength and infection resistance. β-TCP now leverages controlled porosity to activate mesenchymal stem cells and shorten healing times[1]Peramune Kumara, “Bioceramics in Endodontics: Limitations and Future Innovations,” PubMed, pubmed.ncbi.nlm.nih.gov. Tailored degradation rates align scaffold resorption with new bone deposition, elevating clinician confidence. These innovations reduce reliance on allografts, bolstering adoption within the dental bone void filler market.

Chair-Side 3-D Printing of Custom Graft Scaffolds

Point-of-care printing converts CBCT data into patient-specific scaffolds during surgery, eliminating inventory delays. Open-source CAD-CAM software streamlines the workflow, while titanium or polymer meshes are fabricated in minutes. Surgeons achieve precise fit and reduced operative time, enhancing patient comfort. Cost curves decline as printer utilization rises, making personalization accessible beyond flagship centers. This digital shift differentiates forward-leaning providers in the dental bone void filler market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unpredictable Resorption & Clinical Limitations Of Certain Bioceramics | -0.8% | Global, particularly affecting new material adoption | Medium term (2-4 years) |

| High Procedure Cost & Reimbursement Gaps | -1.2% | North America & Europe core, emerging markets affected | Long term (≥ 4 years) |

| Supply-Chain Risk For Xenografts Amid Tighter Zoonotic-Disease Surveillance | -0.6% | Global, with heightened scrutiny in regulated markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Unpredictable Resorption & Clinical Limitations of Certain Bioceramics

Interpatient variability in bioceramic degradation complicates treatment planning and implant stability. Highly porous scaffolds may fracture under load, restricting posterior-jaw usage. Systematic reviews highlight contamination risks that compromise biocompatibility. Regulators demand extensive post-market surveillance, lengthening product approval cycles. These uncertainties temper the dental bone void filler market expansion until next-wave formulations demonstrate consistent performance.

High Procedure Cost & Reimbursement Gaps

Many insurers classify bone grafting as elective, imposing strict clinical criteria and annual caps. Patients shoulder material and surgical fees that can exceed USD 3,000 per site, limiting uptake among middle-income groups. Multi-stage augmentations inflate costs further, creating socioeconomic disparities in care access. Emerging value-based payment models may eventually widen coverage, but near-term growth remains constrained. Affordability challenges particularly affect large-volume emerging markets, where out-of-pocket spending dominates dental expenditures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: β-TCP Dominance Faces Injectable Innovation

β-tricalcium phosphate retains 40.78% share of the dental bone void filler market in 2025 because surgeons trust its resorption profile and osteoconductivity. Calcium-phosphate cements, advancing at a 9.03% CAGR, satisfy demand for injectable solutions that simplify minimally invasive techniques. Biphasic blends combine hydroxyapatite volume stability with β-TCP resorption, winning cases that need balanced remodeling. Recent cement upgrades shorten setting times and improve compressive strength, broadening indications beyond socket preservation. Growth prospects favor materials offering surgeon-friendly handling, predictable integration, and compatibility with digital delivery systems.

Procedural selection now hinges on clinical objective: fast-resorbing powders for sockets, slower materials for ridge augmentation. Regulatory approvals are accelerating as dossier evidence meets stringent safety endpoints. Supply resilience, aided by synthetic production, shields clinicians from xenograft shortages. Consequently, competitive intensity centers on proprietary ion-doping and nanostructuring that enhance bioactivity without escalating cost.

By Form Factor: Granules Lead While Injectables Gain Momentum

Granules commanded 40.12% of the dental bone void filler market in 2025, favored for versatility and straightforward application. Injectable formats rise at an 8.12% CAGR by providing precise placement through specialized cannulas and reducing surgical trauma. Putty and paste options fill irregular defects, while rigid blocks remain essential for non-contained augmentation. Customizable, chair-side printed scaffolds blur the line between traditional form factors and bespoke constructs.

Digitally guided delivery systems synchronize implant drills with graft injection, decreasing material wastage and operative time. Surgeons increasingly value closed syringe packaging that maintains sterility and eases workflow. As printing technologies mature, hybrid approaches—injecting a flowable phase around a printed core—promise enhanced stability and vascularization. Market acceptance will hinge on clinical evidence demonstrating that convenience does not sacrifice long-term structural integrity.

By Application: Socket Preservation Leads Diverse Clinical Needs

Socket preservation represented 30.45% of the dental bone void filler market size in 2025, reflecting its routine adoption immediately after extraction. Ridge augmentation posts the fastest 9.01% CAGR because implant therapy often encounters insufficient native bone. Periodontal defect regeneration benefits from biomaterials that support vertical attachment gain, while peri-implantitis management sparks interest in antibacterial fillers. Sinus lifts and complex reconstructive cases populate the “others” category, each requiring tailored graft characteristics.

Guided tissue regeneration membranes complement grafts by excluding epithelium and stabilizing clot formation. Growth-factor-augmented fillers accelerate vascular ingrowth, shortening healing timelines and supporting early implant loading. Evidence-based protocols advise socket preservation to mitigate future augmentation, saving cost and morbidity. This preventive focus sustains steady material volumes even when implant placement is deferred.

By End User: Dental Clinics Dominate Growing Market

Dental clinics held 37.26% of the dental bone void filler market in 2025 thanks to integrated implant services and patient-centric care models. Ambulatory surgical centers, expanding at an 8.37% CAGR, optimize overheads and scheduling flexibility, attracting complex graft cases traditionally performed in hospitals. Multispecialty hospitals remain indispensable for medically compromised patients needing coordinated anesthesia and postoperative monitoring. Academic and research institutes drive early adoption of novel biomaterials and digital workflows, influencing private-sector standards.

Clinic chains invest in chair-side imaging, CAD-CAM, and on-site sterilization to deliver full-cycle implant rehabilitation. Insurance partnerships that bundle grafting into implant packages aim to soften out-of-pocket shocks. As procedure volumes migrate from hospital to outpatient settings, suppliers tailor product kits to smaller inventories and rapid turnover. Training programs emphasize standardized graft protocols, reinforcing repeatable outcomes and sustaining material pull-through.

Geography Analysis

North America maintained 35.41% of the dental bone void filler market in 2025, driven by sophisticated reimbursement, clinician familiarity with advanced biomaterials, and stringent FDA performance pathways that protect innovation investment. Premium pricing prevails because practitioners prioritize long-term success over material cost. Professional societies disseminate evidence-based protocols, accelerating uptake of ion-doped and nano-structured grafts.

Asia-Pacific records a 9.33% CAGR through 2031 as dental tourism funnels international patients into cost-competitive hubs. Procedure pricing in destinations like Malaysia and Thailand averages 60–80% lower than in Australia or the United States, yet maintains robust quality benchmarks. Rising middle-class incomes and government spending on oral-health infrastructure amplify domestic demand. Multinational manufacturers localize production to benefit from tariff relief and supply-chain resiliency.

Europe exhibits steady expansion supported by an aging populace and payer systems that reimburse evidence-backed biomaterials. Harmonized Medical Device Regulation fosters predictable approvals for synthetic grafts emphasizing sustainability and traceability. Swiss and German R&D centers collaborate with universities to refine calcium-phosphate chemistries, while the region’s cross-border directive facilitates patient mobility, allowing clinics in Spain and Portugal to attract Northern European patients seeking competitive pricing.

Competitive Landscape

The dental bone void filler market is moderately fragmented, yet consolidation intensifies as diversified device companies spin off non-core units to focus on biomaterials. ZimVie’s 2024 restructuring into a pure-play dental firm channelled capital toward 3D-printed scaffolds and sterilization technologies that have processed 11 million implants without infection. Johnson & Johnson earmarked a portion of its USD 50 billion annual R&D pool for nano-ceramic surfaces that promote faster osseointegration[3]Johnson & Johnson, “Q4 2024 Earnings Call,” q4cdn.com.

Strategic acquisitions target startups with proprietary ion-doping and bioactive-glass platforms, improving pipeline diversity. Partnerships with 3D-printer OEMs integrate material cartridges calibrated for dental indications, creating bundled solutions that lock in consumable demand. Supply-chain vigilance heightens after a nationwide tuberculosis outbreak traced to contaminated allografts in 2024 prompted urgent xenograft audits. As a result, synthetic producers highlight pathogen-free manufacturing to win share from biologics.

Competitive differentiation now hinges on digital ecosystems that link imaging, design, and graft delivery. Firms bundle treatment-planning software with chair-side printers and validated materials, creating service-oriented revenue models. Market entrants lacking end-to-end solutions struggle against incumbents that offer full digital workflows, clinical education, and robust post-market surveillance data.

Dental Bone Void Filler Industry Leaders

Curasan Inc

Graftys

Johnson & Johnson

Medtronic plc

Olympus-Terumo Biomaterials

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: UnitedHealthcare updated its dental clinical policy for bone replacement grafts, clarifying criteria while retaining elective-procedure restrictions.

- April 2024: ZimVie divested its spine division for USD 375 million, reallocating resources toward dental biomaterials and implants.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the dental bone void filler market as the sale of synthetic or naturally derived biomaterial products that are implanted to restore small voids in alveolar bone before or during oral procedures such as socket preservation, ridge augmentation, and implant placement. We measure value at factory-gate prices in USD and cover products sold through hospitals, dental clinics, and ambulatory centers across 17 countries.

Scope Exclusion: Orthopedic or spinal uses of bone void fillers and autologous grafts are not considered.

Segmentation Overview

- By Material Type

- Beta-Tricalcium Phosphate (Beta-TCP)

- Biphasic Calcium-Phosphate

- Calcium-Phosphate Cements

- Others

- By Form Factor

- Granules

- Putty/Paste

- Injectable

- Blocks/Molds & Others

- By Application

- Socket Preservation

- Ridge Augmentation

- Periodontal Defect Regeneration

- Implant Bone Regeneration

- Others

- By End User

- Hospitals

- Dental Clinics

- Ambulatory Surgical Centers

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed oral surgeons, periodontists, procurement leads at hospital groups, and material scientists across North America, Europe, and Asia. These conversations validated usage rates per procedure, price discount corridors, and likely adoption curves for newer biphasic ceramics, filling data gaps that literature alone could not close.

Desk Research

We opened our model with public datasets that record the scale of dental need, including WHO Global Oral Health Statistics, CDC National Health and Nutrition Examination Survey, and Eurostat procedural volumes, which supplied baseline incidence numbers. Device clearance files on the US FDA and European MDR portals clarified product taxonomy, while trade flow snapshots from UN Comtrade and Volza helped us track cross-border movements of tricalcium phosphate and DBM kits.

To benchmark pricing and company shares, analysts pulled illustrative filings and investor decks, then triangulated them with news streams in Dow Jones Factiva and company intelligence from D&B Hoovers. Additional clinical insight was drawn from peer-reviewed PubMed articles and American Dental Association white papers. The sources named here are illustrative; many others supported data gathering and verification.

Market-Sizing & Forecasting

We built a top-down model starting with annual dental implant, sinus-lift, and ridge-augmentation procedures, then applied verified penetration and per-procedure filler volume to derive unit demand, which was valued using consensus ASP bands. Supplier roll-ups and channel checks offered a bottom-up reasonableness test. Key variables include implant procedure growth, aging population ratios, elective spending trends, reimbursement adjustments, synthetic material share, and typical granule-to-putty mix. A multivariate regression supported by ARIMA smoothing projects each driver to 2030, while scenario analysis addresses regulatory or pricing shocks. Any data gaps in channel splits were bridged with weighted averages from matched clinics before final reconciliation.

Data Validation & Update Cycle

Outputs pass three analyst reviews, variance checks against independent indicators, and a senior sign-off. We refresh models every 12 months or sooner if material events, such as a major product recall, shift market fundamentals, ensuring clients receive the most current baseline.

Why Mordor's Dental Bone Void Filler Baseline Market Commands Confidence

Published numbers often diverge because firms pick different product mixes, pricing bases, and refresh cadences. Our disciplined scope and annual update rhythm keep the baseline grounded and timely for decision makers.

Key gap drivers include broader inclusion of orthopedic segments by some publishers, reliance on revenue booking rather than factory-gate valuations, and limited validation of ASP drift. Mordor's study, by contrast, centers strictly on dental indications, tests price bands with live clinic feedback, and reconciles model swings before release.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 106.32 million (2025) | Mordor Intelligence | |

| USD 101.4 million (2024) | Global Consultancy A | Excludes putty formats; extrapolates import data without clinical volume cross-checks |

| USD 1,244.45 million (2025) | Regional Trade Journal B | Combines orthopedic, spinal, and dental revenues; uses billed sales rather than factory-gate value |

The comparison shows that when scope creep or unchecked assumptions inflate totals, figures swing wildly. Mordor's transparent variable selection and repeatable steps deliver a balanced, dependable baseline clients can trace and trust.

Key Questions Answered in the Report

What is the current size of the dental bone void filler market?

The market stands at USD 112.74 million in 2026 and is projected to reach USD 151.18 million by 2031.

Which material type holds the largest share?

Β-tricalcium phosphate leads with 40.78% of global revenue in 2025, reflecting strong clinical familiarity.

Why is Asia-Pacific the fastest-growing region?

Dental-tourism inflows, rising middle-class incomes, and localized manufacturing underpin its 9.33% CAGR through 2031.

How are 3D-printed scaffolds influencing the market?

Chair-side printing enables patient-specific grafts, reducing operative time and enhancing fit, thereby accelerating material adoption.

What are the main barriers to wider market uptake?

High procedure costs coupled with limited insurance coverage and variability in bioceramic resorption rates restrain near-term growth.

Page last updated on: