Artificial Skin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

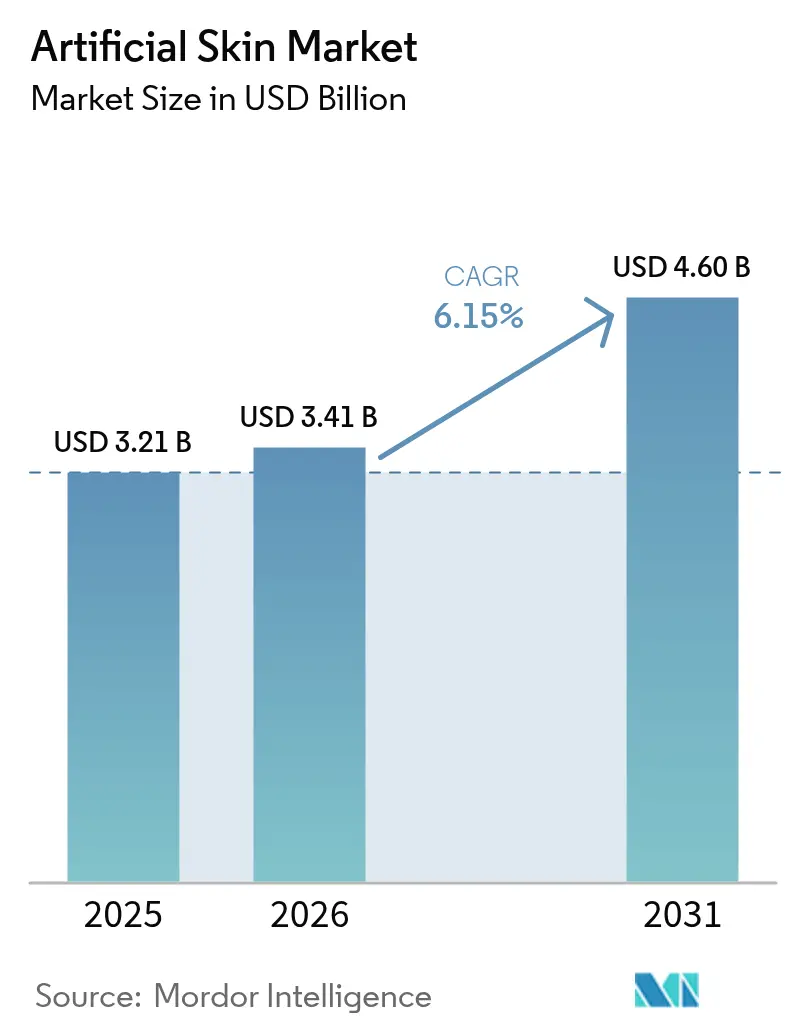

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 4.60 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Skin Market Analysis by Mordor Intelligence

The global artificial skin market size, valued at USD 3.21 billion in 2025 and rising to USD 3.41 billion in 2026, is forecast to reach USD 4.60 billion by 2031, registering a 6.15% CAGR during 2026–2031. Payers and surgeons are pivoting toward solutions that shorten healing time, reduce readmission risk, and integrate monitoring, thereby shifting demand from disposable temporary grafts to composite constructs that offer longer residence and functional restoration. Embedded-sensor substitutes and 3D-bioprinted, patient-specific grafts that entered mid-stage trials in 2025 are expanding revenue streams through newly created remote-monitoring reimbursement codes. Defense and space-agency funding for extreme-environment grafts is accelerating dual-use R&D that incumbents can repurpose for civilian trauma care. Finally, supply-chain fragility in biological raw materials is pushing manufacturers to adopt bio-hybrid polymers that offer reproducible quality and lower cost volatility, further shaping product-mix dynamics inside the artificial skin market.

Key Report Takeaways

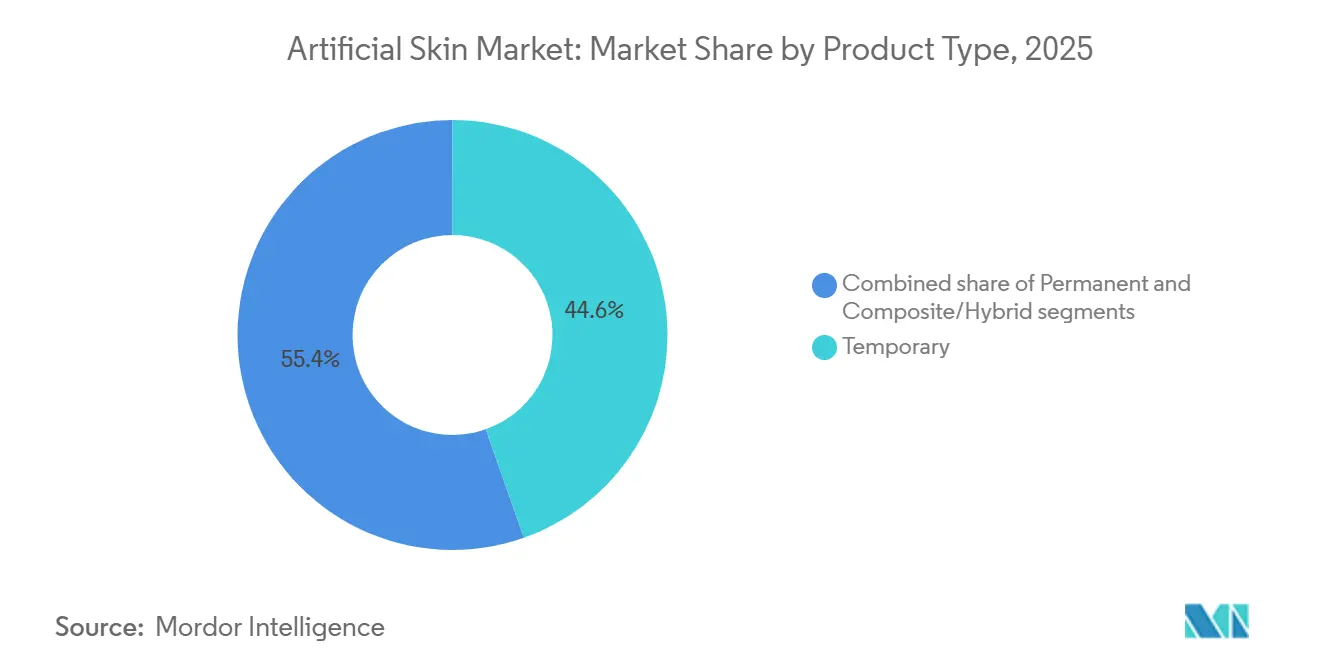

- By product type, temporary grafts led with 44.55% of the artificial skin market share in 2025, while composite/hybrid constructs are forecast to grow at an 8.85% CAGR through 2031.

- By replacement area, dermal replacement held 55.53% share of the artificial skin market size in 2025, and full-thickness composite solutions are advancing at an 8.75% CAGR through 2031.

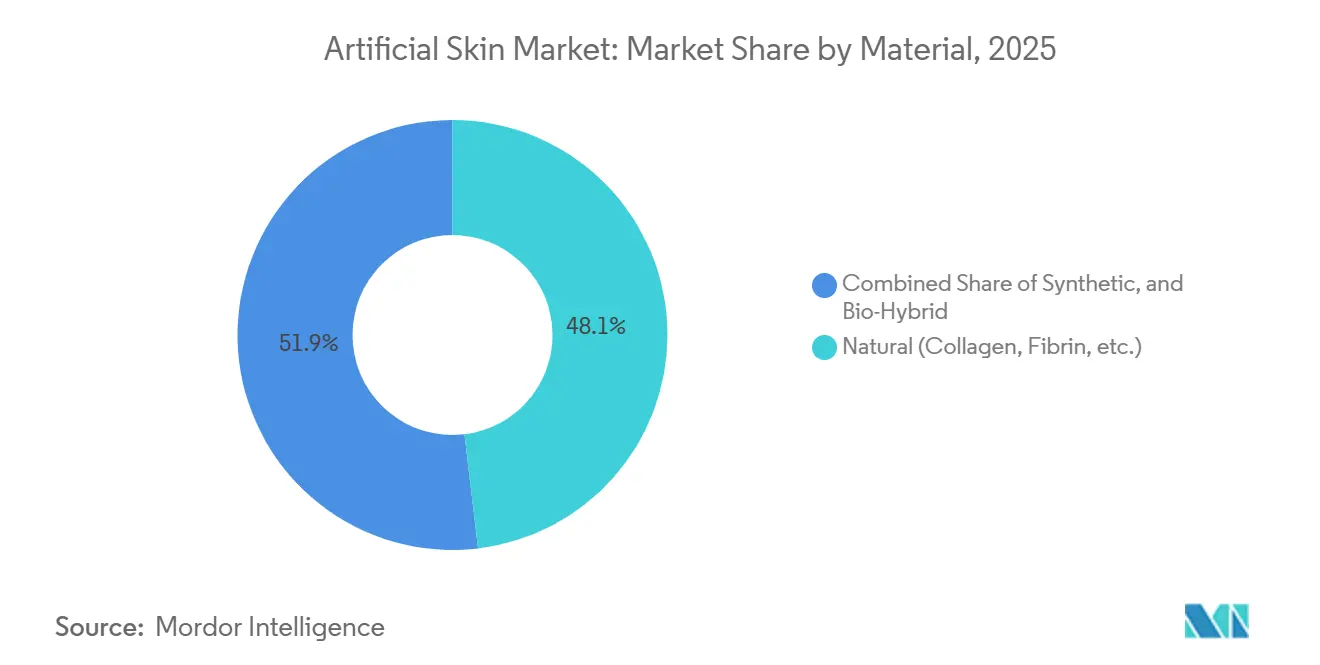

- By material, natural collagen-based scaffolds captured 48.15% of the market in 2025, whereas bio-hybrid constructs are projected to expand at a 9.82% CAGR through 2031.

- By application, acute wounds accounted for 46.52% of revenue share in 2025; chronic wounds are set to grow at a 9.12% CAGR during 2026-2031.

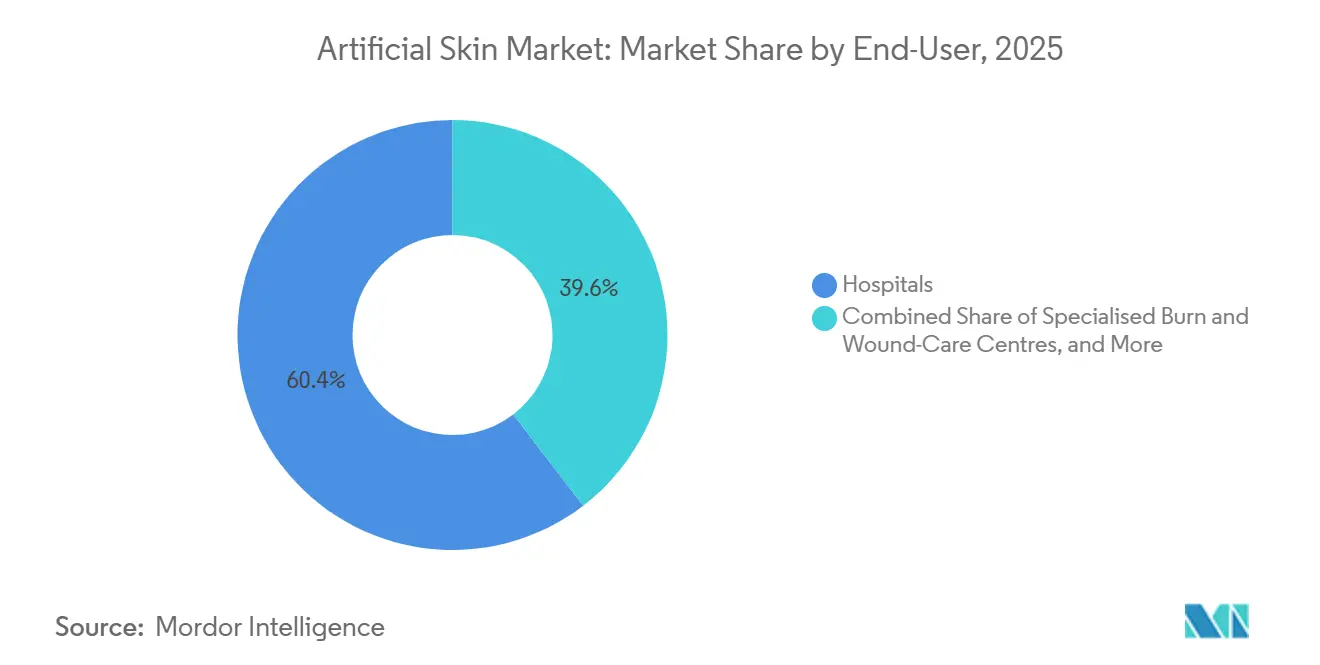

- By end user, hospitals accounted for 60.45% of 2025 revenue, yet ambulatory surgical centers are projected to exhibit the highest 10.62% CAGR to 2031.

- By geography, North America dominated with a 39.55% share in 2025, while Asia-Pacific is on track for an 8.72% CAGR through 2031 as regulatory harmonization accelerates approvals.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Skin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological Innovations in Regenerative Medicine | +1.2% | North America, EU | Medium term (2-4 years) |

| Increasing Incidence of Chronic & Acute Skin Injuries | +1.5% | Global, aging OECD | Long term (≥ 4 years) |

| Rising Geriatric & Diabetic Population | +1.3% | North America, Europe, APAC | Long term (≥ 4 years) |

| 3D-Bioprinted, Patient-Specific Grafts Entering Trials | +0.8% | North America, EU | Medium term (2-4 years) |

| Smart Sensor-Embedded Substitutes Unlocking Remote Reimbursement | +0.7% | North America, selective EU | Short term (≤ 2 years) |

| Defense & Space Grants Accelerating Extreme-Environment Graft R&D | +0.5% | North America, limited EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Technological Innovations in Regenerative Medicine

Electrospun nanofiber scaffolds that mimic extracellular matrix architecture gained FDA clearance in 2024 and cut re-epithelialization time by 40%, enabling outpatient autologous cell seeding and shifting procedures away from hospitals. Japan authorized iPSC-derived keratinocytes for clinical use in 2025, offering an unlimited cell source without donor-site morbidity. Patent activity around self-assembling peptide hydrogels rose 60% year-over-year in 2025, highlighting the push for injectable formulations that harden in situ and remove surgical debridement costs. Collectively, these advances reposition the artificial skin market toward faster, less invasive care settings, underpinned by materials that accelerate healing and widen provider adoption.

Increasing Incidence of Chronic and Acute Skin Injuries

The CDC recorded 6.3 million U.S. adults living with diabetic foot ulcers in 2025, and recurrence exceeds 40% within a year, even with standard care. Although burn admissions fell 8% between 2020 and 2025, average burn surface area per patient climbed 12%, strengthening demand for high-complexity grafts. Pressure ulcer incidence in long-term care facilities rose to 2.8 per 1,000 patient-days in 2025, underscoring the need for durable coverage that withstands extended immobilization. These trends collectively lift baseline demand for artificial skin products that promise durable closure, infection control, and cost-effective repeat use[1]U.S. Centers for Disease Control and Prevention, “National Diabetes Statistics Report 2025,” cdc.gov.

Rising Geriatric and Diabetic Population

Adults aged 65 years and older will represent 16% of the global population by 2030, while global diabetes prevalence reached 537 million in 2025. Geriatric skin fragility and neuropathic ulcers lengthen healing times, creating sustained pull for advanced grafts. Japan bundled artificial skin substitutes with continuous glucose monitoring in its 2025 reimbursement schedule, cementing the link between metabolic control and wound outcomes. Manufacturers are therefore integrating sensors and diagnostics to address chronic-care pathways, locking in higher lifecycle revenues inside the artificial skin market.

3D-Bioprinted, Patient-Specific Grafts Entering Trials

Organovo’s Phase II data, released in 2025, showed autologous bioprinted grafts lowering rejection rates to below 5% versus 18% for allogeneic options, saving USD 15,000-25,000 per year in immunosuppression. Production timelines fell from six weeks in 2023 to 72 hours in 2025, making on-demand grafting feasible for regional burn centers. Yet FDA treats bioprinted constructs as combination products, adding 18-24 months to approval, favoring well-capitalized firms with in-house regulatory scale[2].Organovo Holdings Inc., “Phase II Clinical Trial Results for Bioprinted Skin Grafts,” ir.organovo.com

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Costs & Budget Constraints | −1.1% | Emerging APAC, Latin America | Short term (≤ 2 years) |

| Stringent Multi-Regional Regulatory Frameworks | −0.9% | EU, Japan | Medium term (2-4 years) |

| Supply-Chain Fragility for Biological Raw Materials | −0.6% | Global, collagen dependent | Short term (≤ 2 years) |

| Limited Vascularization & Engraftment >20 Cm² | −0.7% | Global burn centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs & Budget Constraints

Advanced biologic grafts cost USD 1,500-8,000 per 100 cm² while Medicare reimburses USD 12,000-18,000 per burn admission, forcing hospitals to absorb up to 40% of costs. In India, national reimbursement is USD 200-300 per burn procedure, effectively excluding premium grafts. Until synthetic or bio-hybrid alternatives reach parity pricing, cost misalignment will temper adoption in value-sensitive regions.

Stringent Multi-Regional Regulatory Frameworks

U.S. 510(k) clearance can be finalized within nine months, yet EU MDR demands clinical trials that extend approval to 24-36 months and add EUR 2-4 million in costs. Japan’s conditional pathway shortens entry but imposes seven-year surveillance. Divergent rules drain 15-20% of R&D budgets and slow time-to-revenue for small innovators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Composite Constructs Gain Traction

Temporary grafts held a 44.55% share in 2025 for triage-oriented coverage, yet composite constructs are projected to grow at an 8.85% CAGR as clinicians favor single-stage closure. Hybrid matrices combine synthetic durability with biologic cues, lowering application frequency and infection risk, which aligns with bundled-payment incentives inside the artificial skin market.

Permanent grafts remain preferred for full-thickness burns but face supply and reimbursement headwinds, while temporary xenografts remain the preferred option for pediatric use due to their elastic properties. FDA clarified in 2024 that most composites qualify for 510(k) clearance, trimming launch timelines and accelerating category growth.

By Replacement Area: Full-Thickness Solutions Accelerate

Dermal replacements captured a 55.53% share in 2025, yet full-thickness constructs are advancing at an 8.75% CAGR because they collapse two surgical stages into one, reducing anesthesia exposure and infection risk.

Epidermal-only sheets hold a minor share due to fragility, whereas emerging bioprinted constructs deposit epidermal layers directly on dermal scaffolds, boosting take rates to 85% in preclinical tests. Hospitals embracing bundled payments prize the shorter closure time of full-thickness grafts, steering demand toward integrated solutions across the artificial skin market.

By Material: Bio-Hybrids Outpace Pure Biologics

Natural collagen matrices led with a 48.15% revenue share in 2025, but bio-hybrid scaffolds are expected to post a 9.82% CAGR through 2031 as they address batch variability and cost instability. Synthetic backbones functionalized with peptide motifs match natural engraftment speed while cutting rejection to single digits.

Synthetic-only films remain limited to short-term coverage, and newer fish-skin collagen products add competitive variety but still face regional approval hurdles. Functional minimalism design and stable input sourcing underpin the bio-hybrid advance in the artificial skin market.

By Application: Chronic Wounds Gain Momentum

Acute trauma accounted for 46.52% of the 2025 spend, but chronic wound care is on a 9.12% CAGR path because diabetic foot and pressure ulcers are rising faster than burn incidence. Diabetic ulcer recurrence above 40% turns each patient into a multi-episode consumer of grafts, scaling volume far beyond episodic burn needs.

Outpatient reimbursement delays still suppress penetration in diabetic ulcers, but new codes and sensor integration are shortening approval loops. Acute applications retain premium pricing in defense and disaster stockpiles, sustaining a barbell revenue mix within the artificial skin market.

By End-User: Ambulatory Centers Surge

Hospitals accounted for 60.45% of 2025 revenue, yet ambulatory surgical centers (ASCs) are forecast to grow at a 10.62% CAGR after CMS added skin-substitute procedures to the ASC list in 2024. Simplified techniques and room-temperature scaffolds enable office-based application, putting price pressure on hospital outpatient departments.

ASCs favor single-use, ambient-stable packaging that minimizes storage complexity, while hospitals keep high-TBSA cases needing intensive care. Suppliers that optimize for both settings gain broader coverage across the artificial skin market.

Geography Analysis

North America generated 39.55% of 2025 revenue thanks to broad reimbursement and high per-capita spend. Medicare covers advanced biologics at 2-3× European rates, allowing rapid uptake of sensorized grafts and bioprinted trials. Diverse burn center networks support clinical evidence generation, reinforcing regional leadership in the artificial skin market.

Europe follows with robust clinical adoption but fragmented payer rules, which slow penetration in diabetic ulcers despite strong evidence. Germany finances advanced grafts for burns but not chronic wounds, while France demands cost-effectiveness data rarely generated for niche populations.

Asia-Pacific is projected to grow at an 8.72% CAGR as Japan and South Korea harmonize with FDA standards and approve products within six months. China’s first domestically developed bioengineered skin, approved in 2025 at half the Western price, is broadening access in tier-2 cities. India’s reimbursement gap remains a drag, yet private hospitals in metropolitan hubs are adopting bio-hybrids to serve medical tourism flows, gradually expanding the artificial skin market footprint.

Competitive Landscape

The top five companies command a significant share of global revenue, leaving moderate fragmentation that fuels price and innovation competition. Integra LifeSciences and Organogenesis leverage vertically integrated supply chains to secure gross margins of 60-70%, while regional players pursue cost-plus strategies for private-label products. Regulatory speed, reimbursement access and post-market registry data are the main competitive levers.

Emerging bioprinting startups bypass the cold chain, printing grafts on-site within 72 hours and reshaping distribution economics. Synthetic-biology ventures scaling recombinant collagen at 70-80% lower cost threaten natural-matrix incumbents. With ISO 13485 and cGMP compliance costing up to USD 10 million in upgrades, manufacturing remains an entry barrier that consolidates capacity among established firms.

Patent filings show strategic focus: Integra lodged 47 patents on collagen cross-linking for a 36-month shelf life, and Organogenesis filed 34 patents on cryopreservation, extending living-cell storage to 12 months. Sensor integration and pediatric growth-accommodating grafts are underserved niches where fewer than five viable products exist, offering white-space upside inside the artificial skin market.

Artificial Skin Industry Leaders

Integra Lifesciences Corporation

Smith & Nephew Plc

Medtronic

Molnycke Health Care AB

Baxter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Swedish researchers unveiled dual 3D-bioprinting methods that fabricate vascularized skin, marking a potential breakthrough for large-area grafts.

- August 2025: TU Graz and Vellore Institute of Technology began developing a 3D-printed skin model with live cells to test cosmetic nanoparticles without animal studies.

Global Artificial Skin Market Report Scope

As per the scope of the report, artificial skin is a synthetic substitute for human skin that can induce the regeneration of the skin. The skin is the largest organ in the human body and comprises two layers, namely, the epidermis and dermis. Severe burns and wounds make the body more vulnerable to infections and impair healing. Artificial skin helps to overcome this obstacle and quickens the healing of wounds and burns. Artificial skin does not contain any immunogenic cells, so it is not rejected by the body.

The artificial skin market is segmented by product type, replacement area, material, application, end-user, and geography. By product type, the market is segmented into permanent, temporary, and composite. By replacement area, the market is segmented into dermal, epidermal, and full-thickness. By material, the market is segmented into natural, synthetic, and bio-hybrid. By application, the market is segmented into acute wounds, chronic wounds, and cosmetic & aesthetic procedures. By end user, the market is segmented into hospitals, specialised burn & wound-care centres and ambulatory surgical centres. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Permanent |

| Temporary |

| Composite / Hybrid |

| Dermal |

| Epidermal |

| Full-Thickness (Composite) |

| Natural (Collagen, Fibrin, etc.) |

| Synthetic (PGA, PCL, PU, etc.) |

| Bio-Hybrid |

| Acute Wounds (Burns, Trauma) |

| Chronic Wounds (Diabetic, Pressure Ulcers) |

| Cosmetic & Aesthetic Procedures |

| Hospitals |

| Specialised Burn & Wound-Care Centres |

| Ambulatory Surgical Centres |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Permanent | |

| Temporary | ||

| Composite / Hybrid | ||

| By Replacement Area | Dermal | |

| Epidermal | ||

| Full-Thickness (Composite) | ||

| By Material | Natural (Collagen, Fibrin, etc.) | |

| Synthetic (PGA, PCL, PU, etc.) | ||

| Bio-Hybrid | ||

| By Application | Acute Wounds (Burns, Trauma) | |

| Chronic Wounds (Diabetic, Pressure Ulcers) | ||

| Cosmetic & Aesthetic Procedures | ||

| By End-User | Hospitals | |

| Specialised Burn & Wound-Care Centres | ||

| Ambulatory Surgical Centres | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the artificial skin market be by 2031?

It is projected to reach USD 4.60 billion by 2031, growing at a 6.15% CAGR from 2026 to 2031.

Which segment is expanding the fastest in artificial skin products?

Composite/hybrid constructs are forecast to grow at an 8.85% CAGR as clinicians adopt single-stage solutions.

Why are ambulatory surgical centers gaining share in artificial skin procedures?

CMS added skin-substitute applications to the ASC reimbursement list in 2024, enabling lower-cost outpatient treatments that are growing at a 10.62% CAGR.

What is the main driver for growth in chronic-wound applications?

Rising diabetes prevalence and high ulcer recurrence are pushing chronic-wound demand toward advanced grafts with remote monitoring capabilities.

Which region is expected to record the highest CAGR?

Asia-Pacific is set for an 8.72% CAGR as Japan and South Korea harmonize regulations and China approves lower-priced domestic products.

How are smart sensor-embedded grafts changing reimbursement?

They secured dedicated CMS codes in 2025 that pay USD 150 per week for remote monitoring, offsetting their higher unit price and expanding adoption.

Page last updated on: