Hungary Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

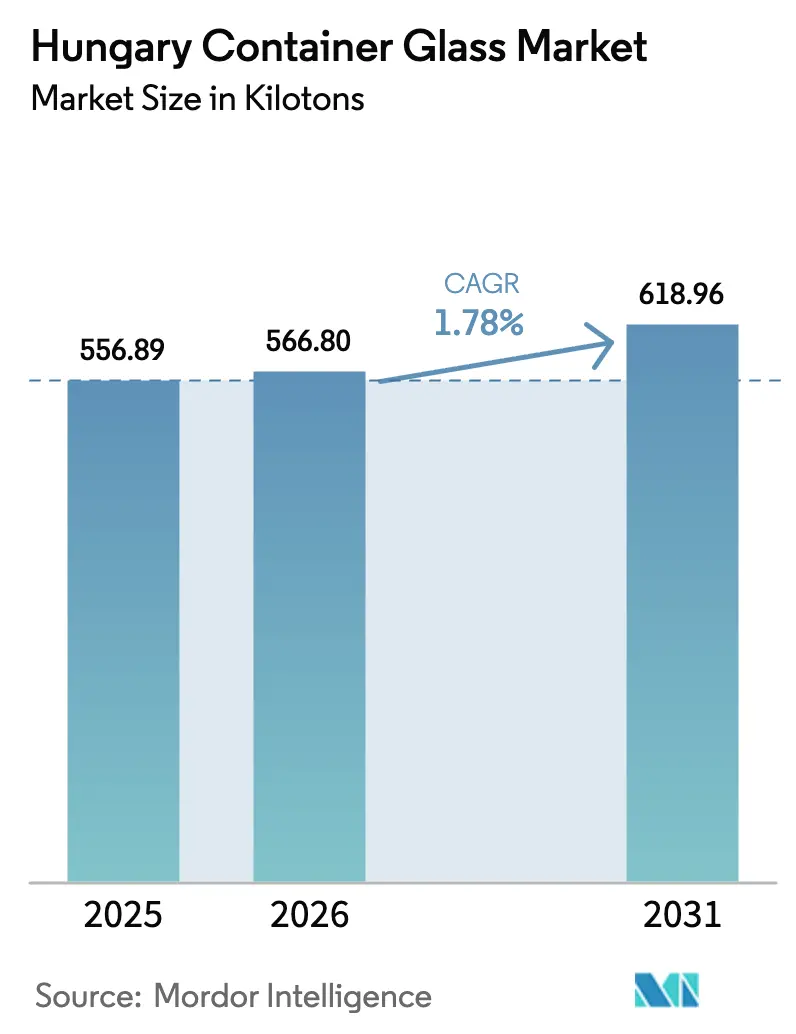

| Base Year Market Size (2025) | 556.89 kilotons |

| Market Volume (2026) | 566.8 kilotons |

| Market Volume (2031) | 618.96 kilotons |

| Growth Rate (2026 - 2031) | 1.78% CAGR |

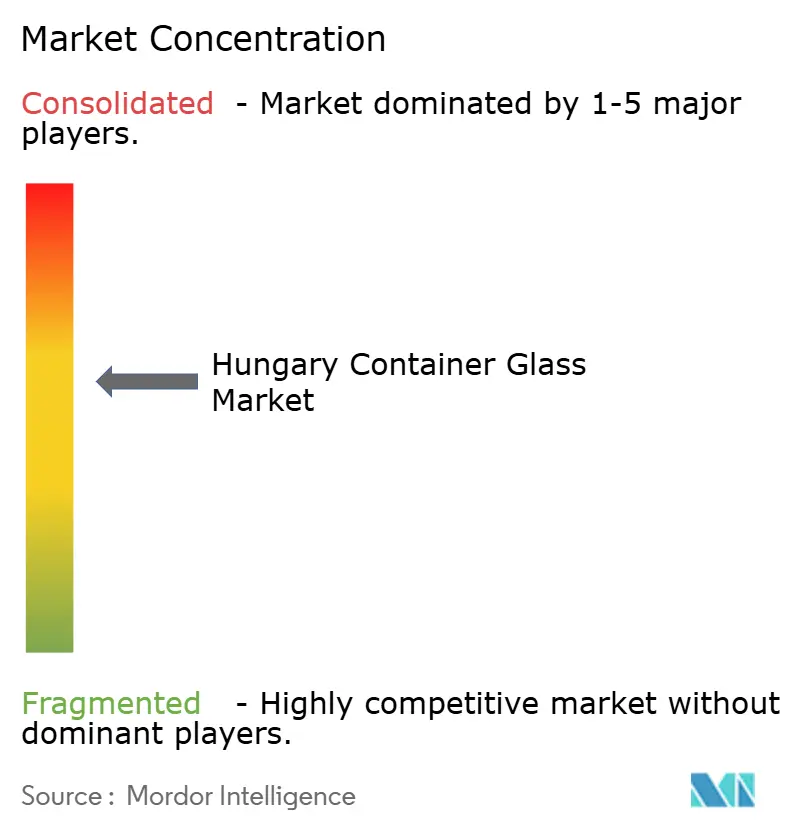

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hungary Container Glass Market Analysis by Mordor Intelligence

The Hungary container glass market size was valued at 556.89 kilotons in 2025 and estimated to grow from 566.8 kilotons in 2026 to reach 618.96 kilotons by 2031, at a CAGR of 1.78% during the forecast period (2026-2031). Hungary’s strategic position in Central Europe enables the efficient servicing of both domestic and export beverage brands, particularly in the premium beer and spirits segments, which rely on glass for shelf differentiation. Continuous investment in energy-efficient furnaces, higher cullet utilization, and lightweighting keeps domestic production competitive despite fluctuations in natural-gas prices. Demand is reinforced by the national deposit return system, which has returned more than 1 billion containers within six months, thereby lowering raw material costs and aligning with EU circular economy mandates.[1]European Commission Press Office, “Commission Welcomes Political Agreement on Revised Packaging and Packaging Waste Regulation,” European Commission, ec.europa.eu Competitive intensity is driving the need for technology upgrades as multinationals strengthen their Hungarian plants to serve regional craft, cosmetics, and pharmaceutical customers.

Key Report Takeaways

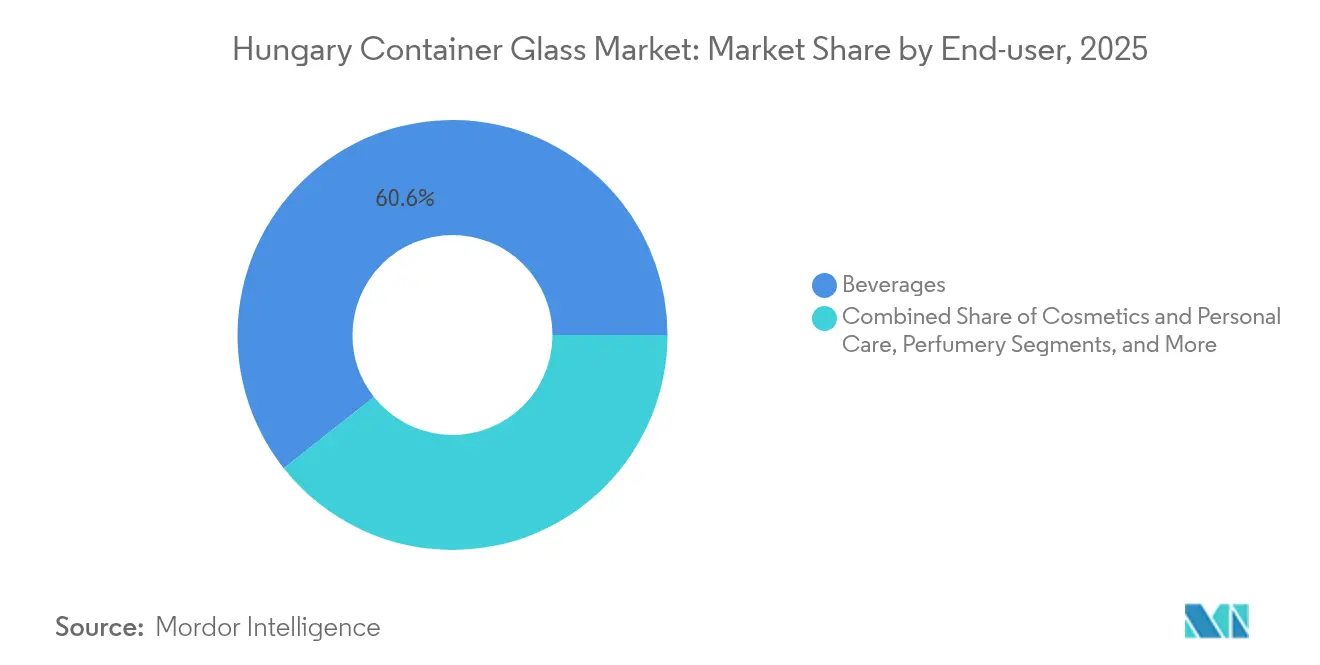

- By end-user, beverages captured 60.63% of the Hungary container glass market share in 2025.

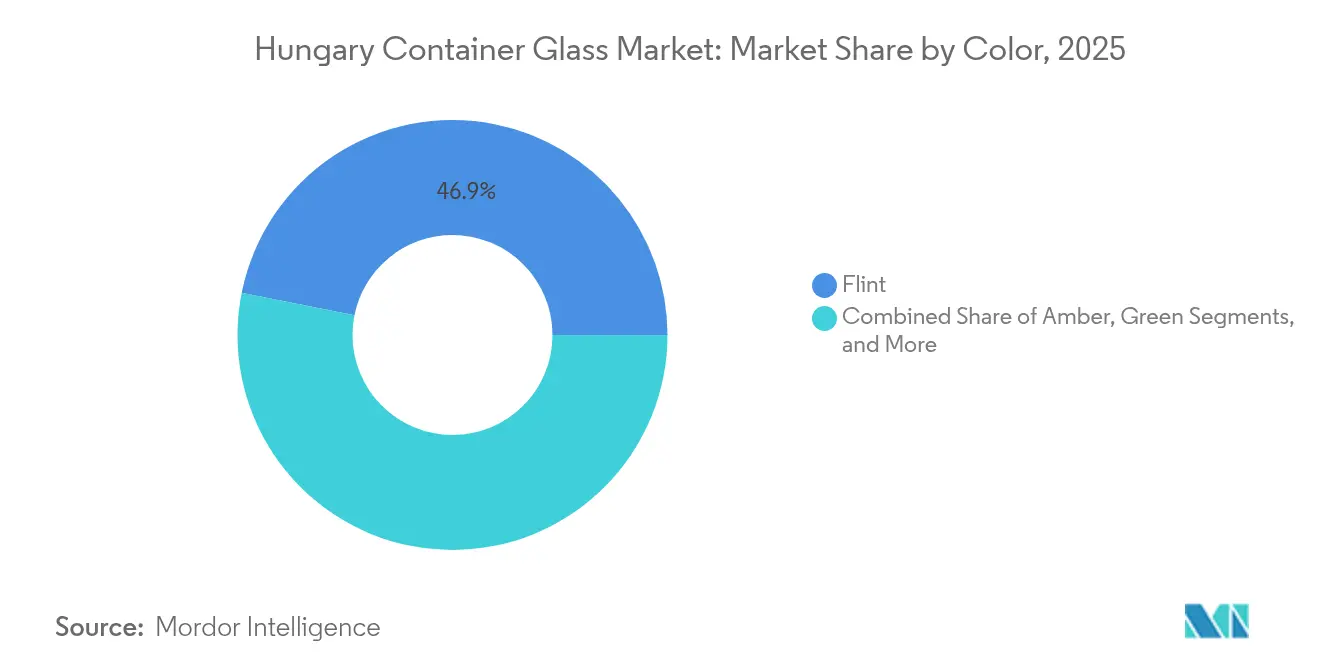

- By color, the Hungary container glass market size for the amber segment is projected to grow at a 3.05% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hungary Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Constant focus on reducing packaging waste and boost eco-friendly packaging | +0.4% | National, with spillover to EU export markets | Medium term (2-4 years) |

| Robust demand for carbonated and other non-alcoholic beverages | +0.3% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Rising beer exports from Hungary to EU neighbours | +0.2% | National production, EU market focus | Medium term (2-4 years) |

| Premiumisation trend in spirits and craft beverages | +0.3% | National, with premium export segments | Long term (≥ 4 years) |

| EU funding for energy-efficient furnace upgrades | +0.2% | National, aligned with EU Industrial Strategy | Long term (≥ 4 years) |

| Emergence of deposit return system for single-use glass | +0.3% | National implementation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Constant Focus on Reducing Packaging Waste and Boost Eco-Friendly Packaging

EU targets that require a 70% glass-recycling rate by 2025 have moved packaging decisions decisively toward glass. Producers that miss Extended Producer Responsibility thresholds risk fines of HUF 50 million, so brand owners favor containers that slot seamlessly into an expanding return-and-recycle loop. Furnace operators respond by increasing cullet ratios, which are already trending toward 66%, and by lightweighting bottles by up to 30% while preserving strength.[2]SaverGlass CSR Team, “CSR Report 2022–2023,” Saverglass, saverglass.com Source: Industry Intelligence Staff, “Mattoni 1873 Installs KHS Canning Line,” Industry Intelligence, industryintel.com The shift benefits flint and amber formats whose clarity or UV-blocking properties are difficult to replicate in plastics. Combined, these measures enhance circularity credentials and lower specific energy consumption, reinforcing the long-term competitiveness of the Hungary container glass market.

Robust Demand for Carbonated and Other Non-Alcoholic Beverages

Urban consumers and multinational fillers drive the uptake of glass in premium soft drinks, functional waters, and energy beverages. Plants in and around Budapest operate multispeed lines that can switch between returnable beer bottles and sleek flint water formats demanded by hotel and restaurant channels. Mattoni’s 1873 EUR 8.2 million (USD 8.9 million) line upgrade illustrates corporate willingness to invest locally for glass differentiation. Rising unit prices in non-alcoholic categories compensate for modest volume growth, thereby sustaining furnace throughput and ensuring adequate cullet availability.

Rising Beer Exports from Hungary to EU Neighbours

Proximity to Germany and Austria underpins robust bottled-beer flows, with Hungarian breweries capitalizing on competitive labor and logistics costs. Amber glass dominates export volumes because its UV barrier preserves flavor stability over longer distribution chains. Custom embossing and proprietary bottle shapes add brand value while stabilizing medium-run production campaigns at O-I’s Oroshaza facility. Export-driven demand thus offsets any softness in domestic consumption, reinforcing the growth profile of the Hungarian container glass market.

Premiumisation Trend in Spirits and Craft Beverages

Premium spirits and small-batch distillers specify heavier, intricately shaped containers that signal authenticity. Ajka Crystal leverages a 146-year glassmaking heritage to deliver bespoke solutions for ultra-premium lines, commanding price points that cushion energy and material cost inflation. Decorative techniques acid etching, hot-foil stamping, and sculpted punt bases require precise furnace control and smaller batch runs, steering investment toward flexible manufacturing cells. This high-margin niche supports CAGR expansion for the Hungary container glass industry, even as mass-market volumes grow more slowly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy costs and volatile natural gas prices | -0.5% | National, affecting all production facilities | Short term (≤ 2 years) |

| Rising inflation squeezing consumer spending on packaged foods | -0.3% | National, concentrated in price-sensitive segments | Medium term (2-4 years) |

| Competition from lightweight PET in CSD and juice segments | -0.2% | National, affecting beverage packaging | Medium term (2-4 years) |

| Limited cullet collection infrastructure outside major cities | -0.2% | Rural and semi-urban areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Energy Costs and Volatile Natural Gas Prices

Natural gas and power account for approximately 27% of container glass operating expenses, exposing producers to fluctuations in global commodity prices. The 2024 energy crisis forced several European furnaces offline and prompted Hungarian sites to accelerate investments in hybrid furnaces, which can lower fuel use by up to 60%.[3]Marco Ferraris, “Reducing the Environmental Footprint of Glass Manufacturing,” Ceramics International, ceramics.onlinelibrary.wiley.com Capital outlays lengthen payback horizons, challenging smaller independents and encouraging industry consolidation.

Rising Inflation Squeezing Consumer Spending on Packaged Foods

Real wages lagging behind headline inflation have curbed household spending on premium jarred foods and beverages. Retailers respond with private-label offerings in larger SKUs, which slightly reduces glass-unit demand even as tonnage remains steady due to the bigger formats. Furnace operators compensate through lightweighting and flexible batch sequencing, but margin pressure persists until consumer confidence improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Drive Volume, Cosmetics Lead Growth

Beverages accounted for 60.63% of Hungary's container glass market share in 2025, reflecting the enduring demand for beer, wine, and spirits. Export-oriented breweries specify amber bottles that mitigate lightstrike, while premium spirit labels favor custom flint decanters. Non-alcoholic brands adopt sleek, clear bottles to differentiate functional beverages. Cosmetics and personal care, although smaller, are forecast to expand at a 2.06% CAGR, buoyed by luxury skincare in refillable jars and perfumes that prize design innovation. The Hungary container glass market size for cosmetics is projected to reach 18.66 kilotons by 2031, underscoring the sector’s strategic value. Local fillers benefit from tight EU supply chains that shorten lead times and reduce carbon footprints, supporting incremental share gains within the Hungary container glass industry.

Food, pharmaceutical, and perfumery segments provide demand diversification. Heat-resistant jars for high-acid foods occupy off-peak furnace capacity, while SCHOTT Pharma’s syringe investment signals rising medical-grade volumes. These applications stabilize throughput and boost value per ton, shielding the Hungary container glass market from cyclical swings in any single category.

By Color: Flint Dominates, Amber Accelerates

Flint glass maintained a leading 46.85% share of Hungary container glass market in 2025. Its growth stems from spirits, premium waters, and cosmetics that rely on transparency to showcase product purity. Volume gains also arise from food jars where visibility is a purchase driver. Amber glass is forecast to post a 3.05% CAGR, supported by pharmaceuticals and craft beverages whose formulations require UV protection. The Hungary container glass market share for amber could surpass 30.25% in pharmaceuticals by 2031 as regulatory emphasis on light-sensitive preparations intensifies.

Green glass maintains its position in the wine and specialty beer niches, where heritage cues are valued. Specialty colors, such as cobalt and black, and custom tints serve marketing campaigns but remain niche. Furnace operators deploy flexible coloring forehearths to capture these higher-margin orders without sacrificing baseline throughput, sharpening competitiveness within the Hungary container glass market.

Geography Analysis

Hungary’s land-linked position offers same-day truck access to Vienna, Bratislava, and parts of southern Germany, lowering delivered cost for export-grade bottles. Germany absorbed 25.16% of Hungary’s glass exports in 2024, demonstrating a significant level of trade integration. Domestic demand clusters around Budapest, Győr, and Debrecen, where beverage fillers and cosmetics plants are concentrated. Cullet flows mirror population density, making metropolitan areas the backbone of the deposit return system that supplies furnaces with high-quality recycled feedstock.

Regional disparities persist. Rural western counties still lack dense collection networks, which limits cullet uptake and increases virgin raw material needs. EU cohesion funds earmarked for waste-management upgrades aim to narrow the gap by 2027, which would enhance supply security for the Hungary container glass market.

Energy infrastructure presents both risks and opportunities. Interconnectors with Slovakia and Croatia diversify gas sources, yet price spikes can erode margins quickly. In response, producers fast-track electric-boosted furnaces and invest in photovoltaic parks to stabilize costs. These initiatives, combined with favorable logistics, enhance Hungary’s credibility as a sustainable hub for glass production in Central Europe.

Competitive Landscape

Three multinational groups O-I, Verallia, and Vetropack command the bulk of installed capacity, giving the Hungary container glass market a moderate concentration profile. Their presence ensures access to leading furnace technologies, design studios, and global procurement channels. Verallia confirmed that no further furnace shutdowns are planned after idling 10% of its European capacity in 2024, signaling confidence in a near-term volume rebound.

Technological differentiation is widening. Hybrid electric and oxy-fuel furnaces, advanced inspection systems, and AI-driven batch optimizers cut energy intensity and defect rates. Early adopters gain cost and sustainability advantages that resonate with brand owners committed to science-based emission targets. Emerging specialists Ajka Crystal and niche decorators thrill luxury brands with hand-finished touches, carving out profitable micro-segments within the broader Hungary container glass market.

Acquisition activity underscores strategic realignment. TricorBraun’s deal for Euroglas and Glaspack adds regional distribution muscle, while Gerresheimer’s integration of Bormioli Pharma creates a global molded-glass champion. These moves consolidate bargaining power with cullet suppliers and freight providers, reinforcing resilience against external shocks and shaping competitive dynamics through 2030.

Hungary Container Glass Industry Leaders

O-I Hungary Kft

Észak Üvért Kft.

PLASTRADE Packaging Ltd.

Şişecam

Feemio Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vetropack named Lukas Burkhardt as incoming CEO, signaling strategic continuity.

- April 2025: Saint-Gobain reported rising Q1 2025 sales, expecting European stabilization in H2 2025.

- January 2025: TricorBraun acquired Euroglas and Glaspack, enlarging its DACH-region glass-packaging network.

- December 2024: Gerresheimer completed the acquisition of Bormioli Pharma, creating a global molded-glass leader.

Hungary Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents. The Hungary glass containers market tracks the shipment volume of different types of glass containers across end-user industries in the market.

Hungary Container Glass Market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, and by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What growth rate is expected for the Hungary container glass market through 2031?

The market is projected to post a 1.78% CAGR, rising from 566.8 kilotons in 2026 to 618.96 kilotons in 2031.

Which end-user segment is growing fastest in Hungary?

Cosmetics and personal care packaging is expanding at a 2.06% CAGR due to premium and eco-friendly positioning.

Why is amber glass demand increasing?

Its UV-blocking properties suit pharmaceuticals and craft beverages, supporting a 3.05% CAGR forecast.

How does Hungary secure cullet for recycled glass?

A nationwide deposit return system collected over 1 billion containers in six months, ensuring a reliable cullet stream.

What is the main operational challenge for Hungarian glassmakers?

High and volatile natural-gas costs, which make up around 27% of production expenses, remain the primary headwind.

Which technologies are glass plants adopting to cut emissions?

Hybrid electric and oxy-fuel furnaces can lower CO₂ emissions by up to 60% while improving thermal efficiency.

Page last updated on: