Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

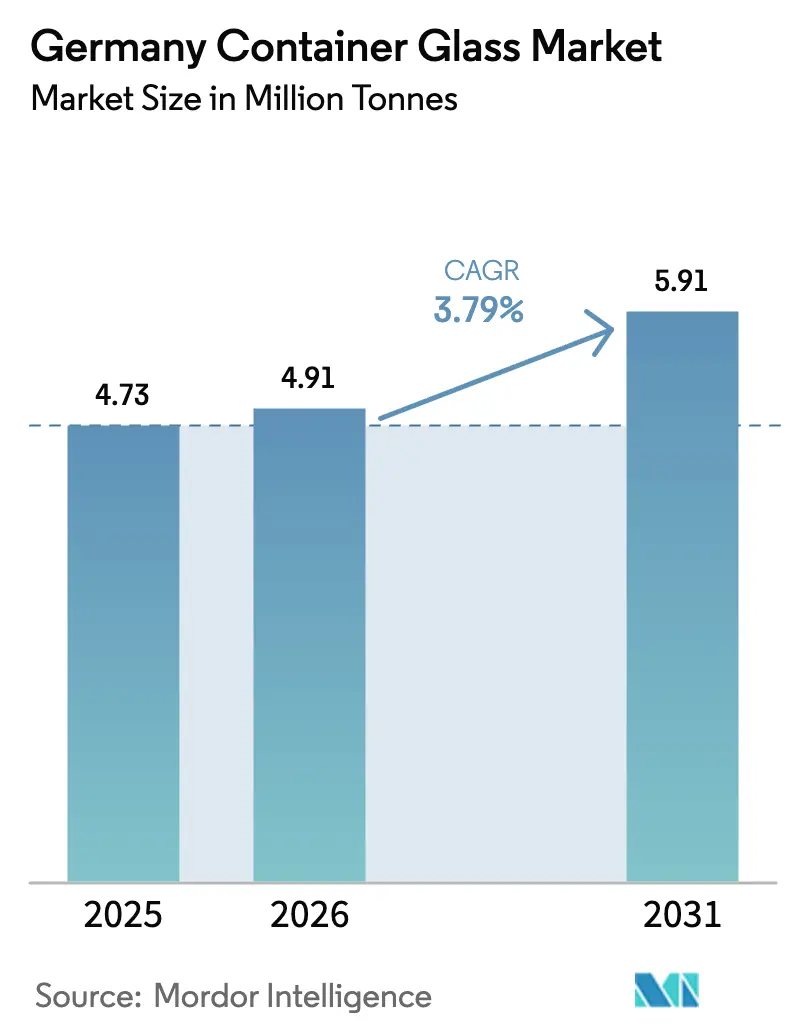

| Base Year Market Size (2025) | 4.73 Million tonnes |

| Market Volume (2026) | 4.91 Million tonnes |

| Market Volume (2031) | 5.91 Million tonnes |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Container Glass Market Analysis by Mordor Intelligence

The Germany container glass market size is projected to be 4.73 million tonnes in 2025, 4.91 million tonnes in 2026, and reach 5.91 million tonnes by 2031, growing at a CAGR of 3.79% from 2026 to 2031. Downward pressure in mainstream beer, higher energy prices, and competition from polyethylene terephthalate have curbed volume growth, yet strategic pivots toward pharmaceuticals and premium beverages are lifting value realisation. Manufacturers are accelerating furnace electrification and hydrogen-ready retrofits to secure decarbonised capacity that meets customer Scope 3 targets. Strict circular-economy rules, including a 70% Mehrweg requirement and a 90% glass recycling goal, are pushing scale players to invest in closed-loop logistics and high-purity cullet sorting. As a result, consolidation around technology leadership rather than raw volume is reshaping competitive dynamics and unlocking margin expansion opportunities across high-specification vial, flint, and decorated formats.

Key Report Takeaways

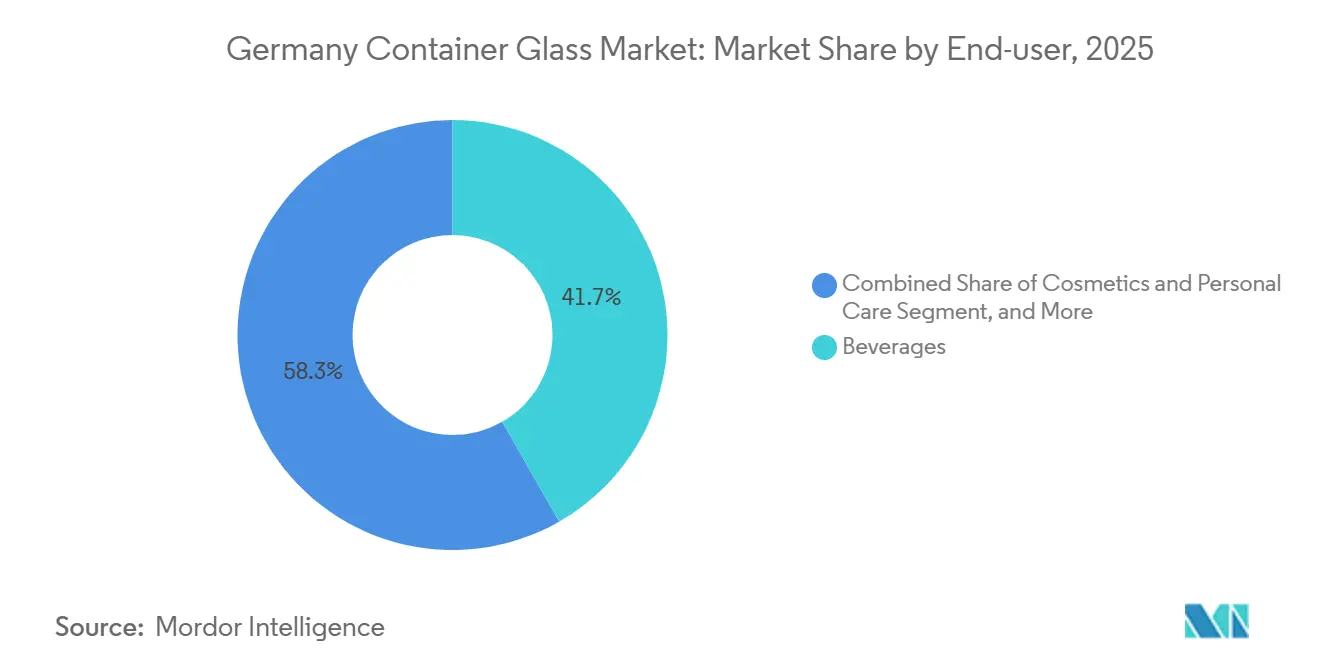

- By end-user, beverages led with 41.73% of volume in 2025, while pharmaceuticals are forecast to expand at a 4.78% CAGR through 2031, the fastest across all segments.

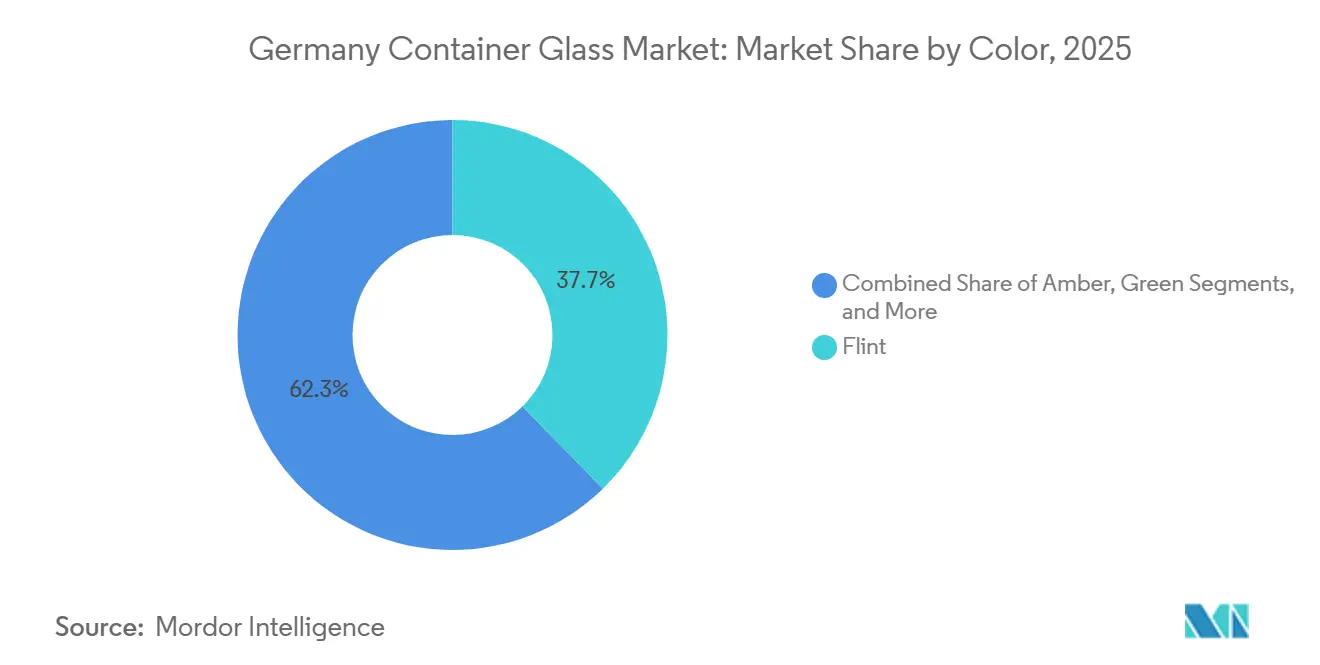

- By color, flint held a 37.67% container glass market share in 2025 and is projected to advance at a 5.52% CAGR between 2026 and 2031, the quickest among color families.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Recyclable Packaging in Germany | +0.8% | Baden-Württemberg, North Rhine-Westphalia | Medium term (2-4 years) |

| Growing Pharmaceutical Sector Boosts High-Quality Glass Packaging | +1.2% | Hesse, Bavaria | Long term (≥ 4 years) |

| Premium Beverages Drive Customized Bottle Requirements | +0.6% | Rhineland-Palatinate, Hamburg | Medium term (2-4 years) |

| Circular Economy Policies Strengthen Glass Recycling Systems | +0.7% | National | Long term (≥ 4 years) |

| Hydrogen-Fired Furnaces Advance Decarbonisation of German Glass Plants | +0.4% | Bavaria, Saxony | Long term (≥ 4 years) |

| Refillable Indie Cosmetic Brands Expand Niche Glass Packaging Demand | +0.2% | Berlin, Munich, Cologne | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing for Recyclable Packaging in Germany

Germany’s Verpackungsgesetz mandates a 90% glass recycling rate by 2025, creating compliance pressure that draws brand owners toward the container glass market rather than alternative substrates. The Federal Environment Agency reinforced a separate 70% target for reusable beverage formats in May 2025, aligning national rules with the European Union’s 2030 objective for at least 10% reusable packaging across member states. Deposit-return systems achieved a 98% collection rate in 2025, yet variable cullet purity prompted operators to invest EUR 2 million to EUR 5 million (USD 2.2 million to USD 5.5 million) per plant in optical-sorting lines. Lifecycle studies show reusable glass outperforms single-use polyethylene terephthalate when deliveries stay within 300 kilometres, a radius that covers most regional beverage flows. Collectively, these measures lock the container glass market into long-run contracts for standardised returnable bottles that stabilise capacity utilisation.

Growing Pharmaceutical Sector Boosts High-Quality Glass Packaging

SCHOTT Pharma’s 2025 report highlighted rising demand for ready-to-fill borosilicate vials serving biologics, oncology drugs, and gene-therapy pipelines.[1]SCHOTT AG, “SCHOTT breaks ground for new electric melting tank,” schott.com Gerresheimer commenced a EUR 30 million (USD 33 million) Wertheim expansion in October 2025 to meet sterile-barrier demands for high-margin cartridges and syringes. In February 2026, Gerresheimer, Stevanato Group, and SCHOTT Pharma formed the Alliance for Ready-to-Use systems, signalling tighter supplier consolidation around integrated washing, sterilisation, and filling services.[2]Gerresheimer AG, “Gerresheimer breaks ground for new Gx RTF vial plant,” gerresheimer.com Germany’s proximity to Basel and Zurich biotech hubs anchors a resilient orderbook, even as lower-cost Eastern European capacity grows. Technical requirements for Type I glass, dimensional precision, and low extractables restrict viable suppliers, giving incumbents pricing leverage within the container glass industry.

Premium Beverages Drive Customized Bottle Requirements

The ProSpirits Report 2025 ranked Germany as Central Europe’s most attractive premium-spirits destination, with craft distillers adopting embossed, coloured flint, and non-standard neck finishes that differentiate on crowded shelves.[3]ProSpirits, “ProSpirits Report 2025,” prospirits.com HEINZ-GLAS invested EUR 4 million (USD 4.4 million) in a Spechtsbrunn decoration centre to capture short-run orders for such bespoke moulds. Although total beer output fell from 87,832 thousand hectolitres in 2022 to 84,885 thousand hectolitres in 2023, craft brewers increased demand for 330-millilitre and 500-millilitre proprietary bottles that support brand storytelling. Premiumisation allows glassmakers to charge 15%-20% price uplifts, offsetting commodity beer weakness and sustaining profitability across the container glass market.

Circular Economy Policies Strengthen Glass Recycling Systems

The Verpackungsgesetz’s 70% Mehrweg mandate plus the European Union’s 10% reusable-packaging rule are altering investment priorities. Reiling commissioned a Lünen cullet plant in October 2025 to upgrade colour-sorting capability for North Rhine-Westphalia’s dense furnace cluster. The Umweltbundesamt’s 2025 report identified contamination from mixed-colour curbside streams that degrade flint batch quality, pushing operators toward advanced sorting optics. Minimum recyclability standards now penalise composite closures and multi-layer labels, creating specification pull-through for monomaterial designs that maximise circular-economy performance. Vertically integrated producers with washing and logistics infrastructure benefit most, reinforcing consolidation trends in the container glass market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Energy Costs Elevate Glass Production Expenses | -0.9% | Saxony, Brandenburg | Short term (≤ 2 years) |

| Competition from PET and Imported Glass Packaging | -0.7% | National | Medium term (2-4 years) |

| Skilled Labor Shortage in Furnace Maintenance and Operation | -0.3% | National | Long term (≥ 4 years) |

| Cullet Quality Variability from Deposit-Return System Expansion | -0.2% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Energy Costs Elevate Glass Production Expenses

Natural-gas melting consumes 4-6 gigajoules per tonne, making energy 25%-35% of production cost and exposing the container glass market to geopolitical shocks. Industrial electricity prices rank among Europe’s highest, undermining the economics of electric furnaces unless supported by renewable power-purchase agreements below EUR 60 per megawatt-hour. The 2024 liquefied-natural-gas spike squeezed margins for commodity beer bottles and accelerated consolidation as hedged groups acquired distressed plants. Green hydrogen offers a decarbonisation path, but at EUR 4 per kilogram it remains twice the energy-equivalent cost of natural gas, requiring carbon prices above EUR 150 per tonne for parity.

Competition from PET and Imported Glass Packaging

Polyethylene terephthalate accounted for 60% of mineral-water packaging in 2022 versus 21% for reusable glass, reflecting retailer preference for lightweight formats that lower transport costs. Imported bottles from Poland and the Czech Republic undercut domestic prices by 8%-12% on commodity wine formats, leveraging lower labour and energy inputs. Although Mehrweg rules favour domestic supply, enforcement gaps allow non-compliant imports to erode share, especially in cost-sensitive juices and table wines, pressuring the container glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Pharma Demand Offsets Beverage Weakness

Beverages represented 41.73% of Germany’s container glass market share in 2025, yet pharmaceuticals are expanding at a 4.78% CAGR through 2031 as biologics pipelines adopt Type I borosilicate vials that earn 3-5 times the revenue per kilogram of soda-lime beer bottles. The Alliance for Ready-to-Use systems underlines the technical moat that incumbents enjoy in high-spec applications. Beer packaging contracted 3.4% between 2022 and 2023, but premium wine and spirits grew mid-single digits, lifting value even as volume stagnated. Non-alcoholic categories remain the most vulnerable to polyethylene terephthalate substitution, especially in functional beverages that face weaker Mehrweg enforcement.

The container glass market size for pharmaceuticals is projected to widen steadily as sterile-injectable demand, prefilled syringes, and gene-therapy cartridges proliferate. Food applications hold a mid-teens share, buoyed by glass’s inertness, while cosmetics and perfumery supply small but lucrative niches where refillable fragrances command 40%-60% gross margins. The shifting mix means capacity planning now hinges on securing vial contracts and value-added decoration lines rather than chasing commodity beer orders.

By Color: Flint Captures Growth From Premiumisation

Flint captured 37.67% of volume in 2025, the largest slice among colour families, and is set to grow fastest at a 5.52% CAGR thanks to pharmaceutical inspection needs and transparent premium-beverage aesthetics. Amber remains vital for beer and photosensitive drugs but loses share to flint coated with ultraviolet-blocking films that maintain clarity while protecting contents. Green holds steady in Riesling and export wines, yet lightweight polyethylene terephthalate eats into entry-level segments where glass’s cost premium is hardest to justify.

Flint’s advance supports a wider container glass market size uplift because its margins exceed those of amber beer bottles. However, mixed-colour cullet threatens furnace yield, prompting investment in high-resolution optics and dedicated bunkers that only large players can afford. Specialty tints such as blue and black address ultra-premium spirits, adding diversity but limited tonnage.

Geography Analysis

Germany maintained its rank as the European Union’s largest container glass producer in 2024 despite a 4.8% contraction in EU27 plus United Kingdom output. First-half 2025 domestic sales slipped 1% to 1.92 million tonnes, underscoring sluggish commodity demand even as pharma and premium orders climbed. Production clusters in North Rhine-Westphalia, Bavaria, Saxony, and Baden-Württemberg benefit from proximity to beverage, automotive, and life-science customers that favour just-in-time delivery.

Decarbonisation is realigning investment geographies. SCHOTT’s EUR 40 million (USD 44 million) electric furnace in Mitterteich and Ardagh’s hybrid hydrogen facility in Obernkirchen demonstrate early-mover readiness, but future builds could gravitate toward Lusatia where stranded renewable capacity lowers power costs. The container glass market size anchored in those emerging clusters will depend on substation upgrades that handle 30-50 megawatt baseloads per 200-tonne-per-day melter.

Germany’s 98% deposit-return collection furnishes abundant cullet, yet quality variance forces EUR 2 million-EUR 5 million optical-sorting retrofits. Export flows are bifurcating; premium pharma and spirits glass moves to North America and Asia, whereas low-spec wine bottles face import competition from Poland and Czech Republic producers. Harmonised EU rules mandating 10% reusable packaging by 2030 may curtail such arbitrage, supporting a more regionalised container glass market.

Competitive Landscape

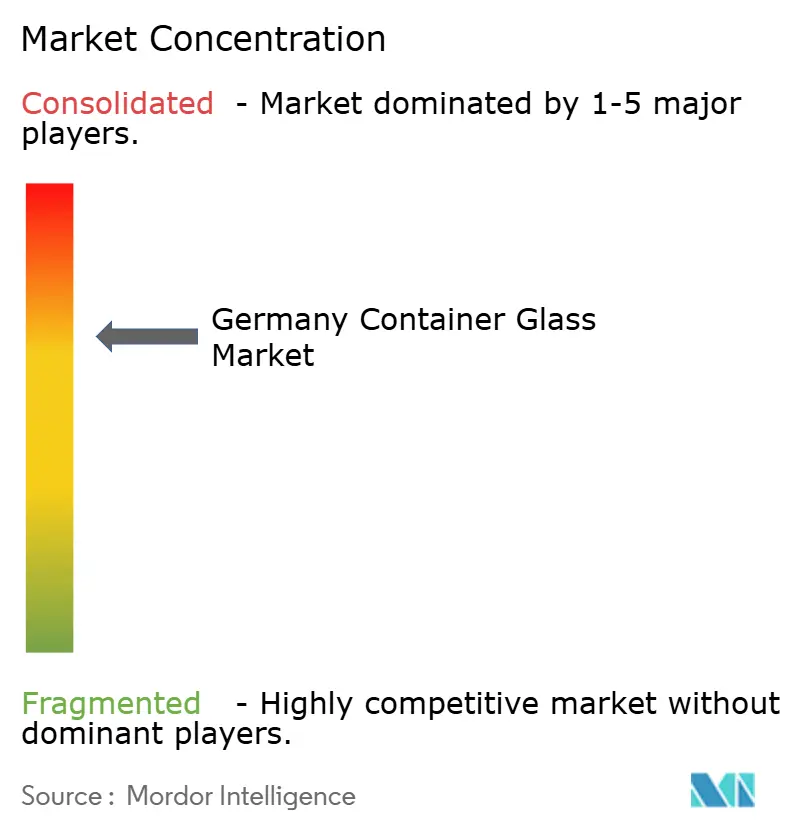

Five multinationals—Ardagh, Verallia, O-I Glass, Gerresheimer, and SCHOTT—control most furnace capacity, though niche specialists such as HEINZ-GLAS, Wiegand-Glas, and Rixius occupy profitable premium and pharma sub-markets. Competition now revolves around decarbonisation timelines and integrated service capability, not raw tonnage. Ardagh’s NextGen hybrid furnace achieved a 64% carbon-dioxide reduction, establishing technical leadership. Gerresheimer’s divestiture of its moulded-glass division in 2025 freed capital for ready-to-use pharma systems, while Verallia’s Northern and Eastern Europe revenues fell in 2024 due to beer softness and high energy costs.

Scale enables early adoption of electric boosting, hydrogen firing, and colour-sorting technology that smaller rivals cannot match. The container glass industry sees white-space opportunities in carbon-neutral toll manufacturing, refillable cosmetic formats, and standardised Mehrweg bottles that slash reverse-logistics complexity. Enforcement gaps in import compliance remain a pricing threat, yet regulatory tightening and customer Scope 3 audits are likely to consolidate share further among technology leaders.

Germany Container Glass Industry Leaders

Gerresheimer AG

O-I Germany GmbH & Co. KG

Wiegand-Glas GmBH

Verallia Deutschland AG

Ardagh Glass GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Gerresheimer, Stevanato Group, and SCHOTT Pharma formed the Alliance for Ready-to-Use systems to streamline washing, sterilisation, and filling for prefilled containers.

- October 2025: Gerresheimer broke ground on a EUR 30 million (USD 33 million) ready-to-use vial plant in Wertheim scheduled for mid-2027 start-up.

- October 2025: Reiling commissioned a cullet-processing facility in Lünen to improve colour separation for North Rhine-Westphalia furnaces.

- August 2025: SCHOTT began building a EUR 40 million (USD 44 million) electric furnace at Mitterteich targeting 2027 production.

Germany Container Glass Market Report Scope

Container glass is a type of glass specifically manufactured to produce bottles, jars, and other containers used for packaging products such as food, beverages, pharmaceuticals, cosmetics, and chemicals. It is designed for strength, chemical resistance, and preservation of contents.

The Germany Container Glass Market Report is Segmented by End-user (Beverages including Alcoholic and Non-Alcoholic, Food, Cosmetics and Personal Care, Pharmaceuticals excluding Vials and Ampoules, Perfumery) and Color (Flint, Amber, Green, Other Colors). The Market Forecasts are Provided in Terms of Volume (Million Tonnes).

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages, Cider and Other Fermented Drinks | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSD) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food, Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals, excluding Vials and Ampoules | ||

| Perfumery | ||

By Color

| Flint |

| Amber |

| Green |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages, Cider and Other Fermented Drinks | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSD) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food, Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals, excluding Vials and Ampoules | |||

| Perfumery | |||

| By Color | Flint | ||

| Amber | |||

| Green | |||

| Other Colors | |||

Key Questions Answered in the Report

What is Germany’s expected container glass volume in 2031?

Demand is forecast to reach 5.91 million tonnes by 2031, reflecting a 3.79% CAGR over 2026-2031.

Which end-user segment is expanding the quickest?

Pharmaceutical packaging leads, advancing at a 4.78% CAGR as biologics, gene-therapy vials, and prefilled syringes gain share.

How will hydrogen and electric furnaces change emissions?

Early hybrid and all-electric retrofits cut carbon dioxide by up to 64%, moving producers toward the 2045 net-zero goal.

Which regulations most influence reusable glass adoption in Germany?

Verpackungsgesetz enforces a 90% glass recycling rate by 2025 and a 70% Mehrweg share for beverages, while the European Union requires 10% reusable packaging by 2030.

Which color segment offers the strongest growth outlook?

Flint glass shows the highest upside, with a 5.52% CAGR driven by pharmaceutical inspection needs and premium-beverage aesthetics.

How do rising energy prices shape production strategy?

Energy accounts for 25%-35% of glass costs, prompting long-term renewable PPAs, hydrogen trials, and furnace electrification to secure cost stability.

Page last updated on: