Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

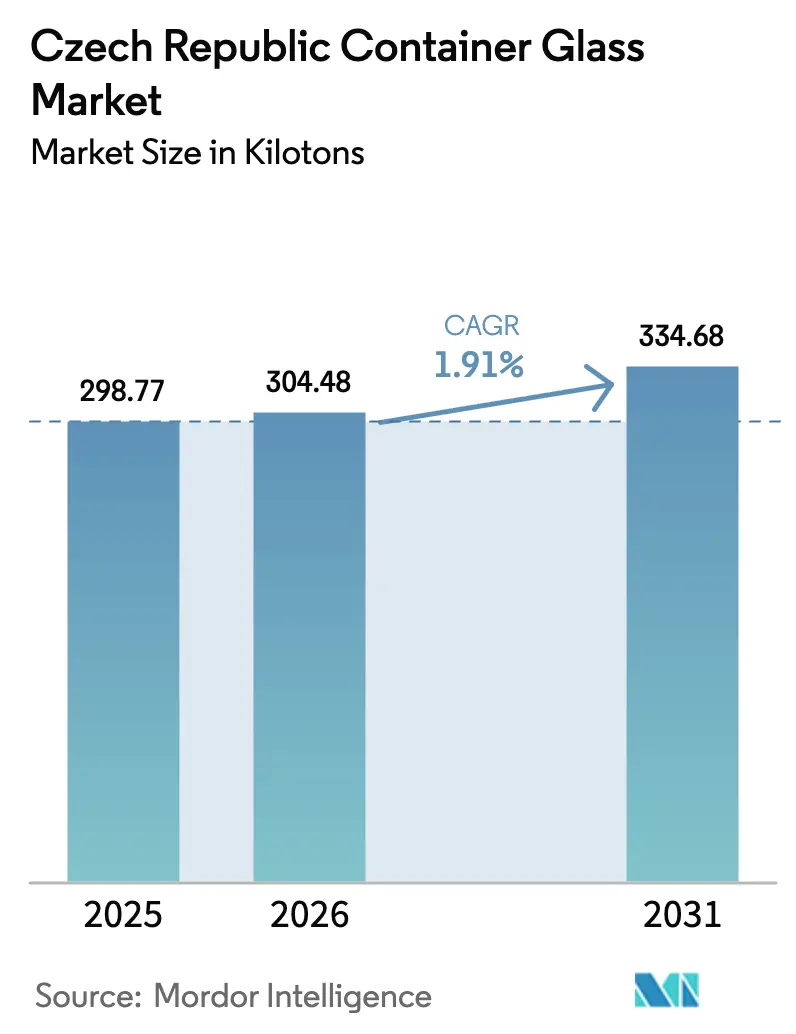

| Base Year Market Size (2025) | 298.77 kilotons |

| Market Volume (2026) | 304.48 kilotons |

| Market Volume (2031) | 334.68 kilotons |

| Growth Rate (2026 - 2031) | 1.91% CAGR |

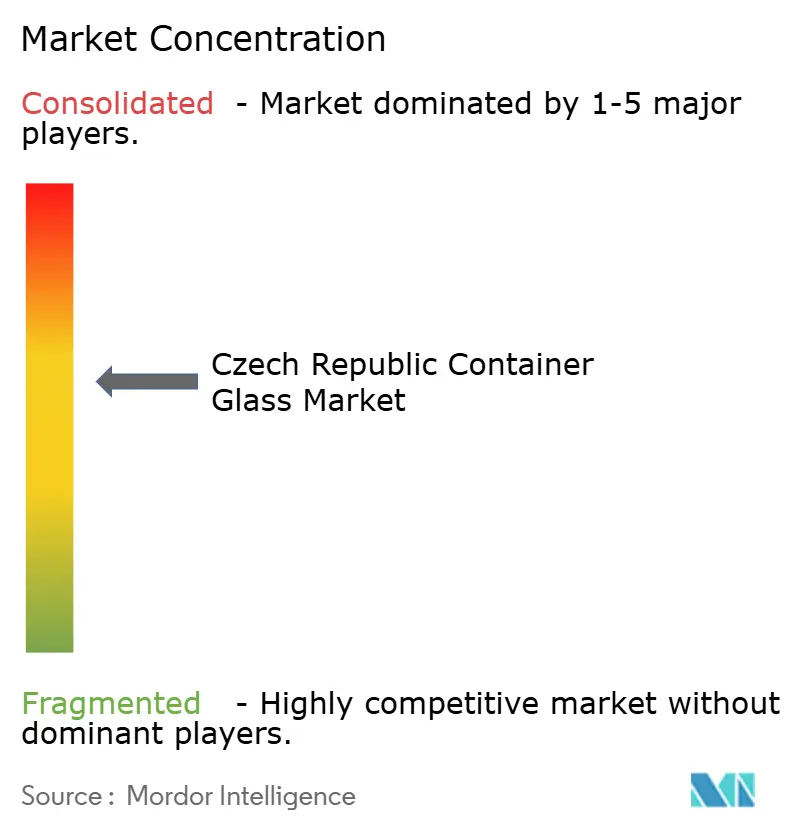

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Czech Republic Container Glass Market Analysis by Mordor Intelligence

The Czech Republic container glass market size is expected to grow from 298.77 kilotons in 2025 to 304.48 kilotons in 2026 and is forecast to reach 334.68 kilotons by 2031 at 1.91% CAGR over 2026-2031. Consistent domestic beverage demand, a recycling rate of 97.5% for glass packaging, and new premium-product opportunities together anchor the market’s steady trajectory. Brand owners keep favoring glass for its circularity and shelf appeal, while energy-efficiency investments are beginning to lower operating costs for large local producers.[1]Ministry of the Environment, “Ekonomická analýza Plánu odpadového hospodářství 2025–2035,” mzp.gov.cz Even so, competition from lighter metal and plastic formats continues to squeeze margins, motivating manufacturers to differentiate through lightweighting, custom molds, and pharma-grade quality systems. The upcoming deposit return system (DRS) and phased ban on single-use plastics are expected to tilt the packaging mix further toward glass in condiments, food, and niche beverage lines. Competitive pressure intensifies as Western European capacity additions come online, yet Czech plants hold an advantage in proximity to Central European customers and established export channels.

Key Report Takeaways

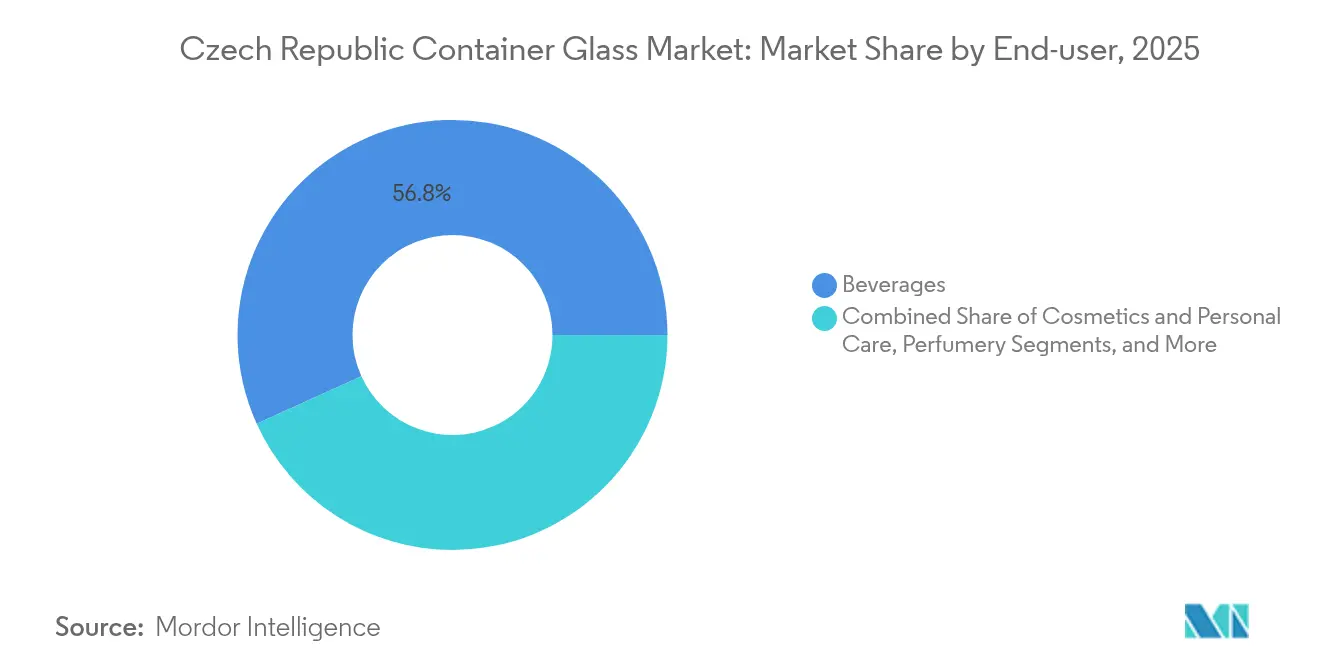

- By end-user, beverages captured 56.77% of the Czech Republic container glass market share in 2025.

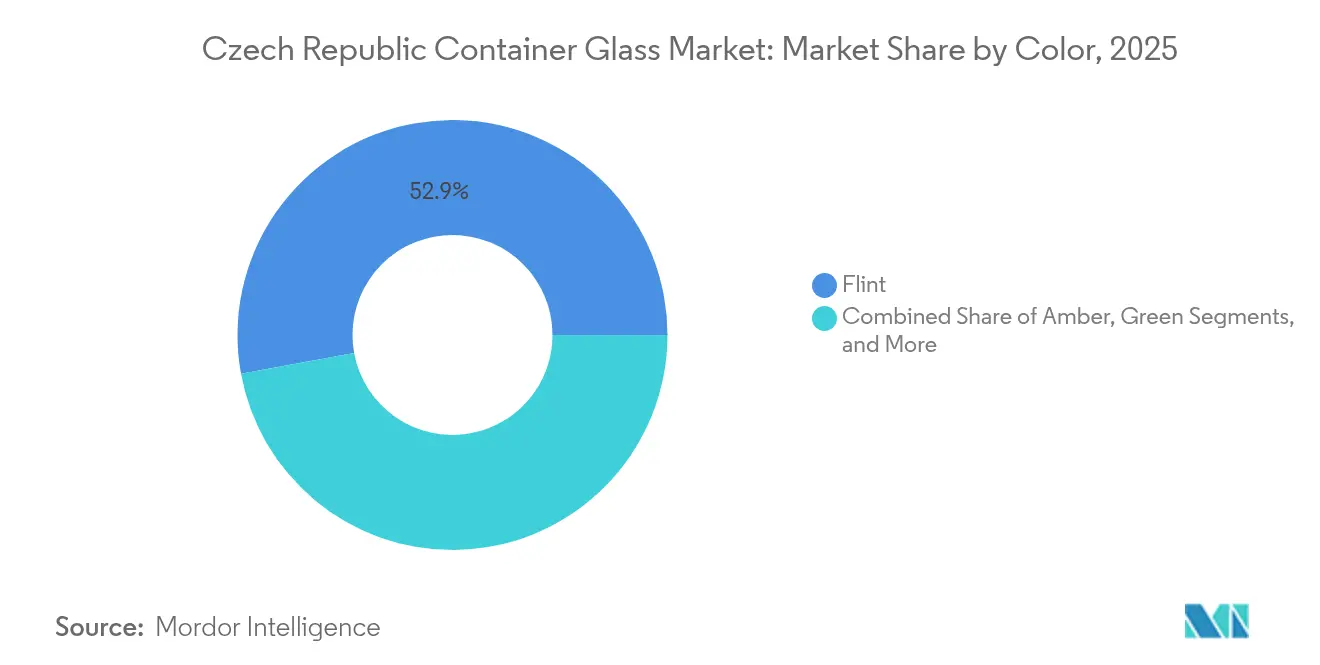

- By color, the Czech Republic container glass market size for the amber segment is projected to grow at a 2.92% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Czech Republic Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Eco-Friendly Packaging Demand Rising Rapidly | +0.8% | Global, with strong EU regulatory push | Medium term (2-4 years) |

| Premium Brands Prefer Glass Over Plastic | +0.6% | Czech Republic, Central Europe | Short term (≤ 2 years) |

| Supportive Government Packaging Regulations Help | +0.4% | National, EU-wide influence | Long term (≥ 4 years) |

| Strong Beverage Industry Fuels Glass Demand | +0.5% | Czech Republic, regional export markets | Medium term (2-4 years) |

| Health-Conscious Consumers Choose Safer Glass | +0.3% | Global, urban centers first | Medium term (2-4 years) |

| Custom Designs Boost Brand Shelf Appeal | +0.2% | Czech Republic, premium segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Eco-Friendly Packaging Demand Rising Rapidly

EU circular-economy directives banning single-use plastics by 2030 are pushing Czech brand owners to substitute toward glass in food and condiment lines, where producers like ADPACK are scaling output. Municipal waste audits show glass collection costs at CZK 2,018 (USD 97.5) per ton, compared with CZK 9,422 (USD 455.2) for plastics, reinforcing economic incentives for local governments. The Czech Republic’s 97.5% glass material recycling rate underscores infrastructure readiness, and nationwide campaigns targeting plastic-free retail aisles are nudging retailers toward returnable or refillable glass formats. Beverage fillers now run multi-trip glass bottle lines to exploit deposit-loop advantages, and winery cooperatives have begun pooling bottle returns through regional hubs to cut logistics costs. As the DRS takes effect in 2027, glass is poised to retain its position as the most circular rigid-packaging medium in the market.

Premium Brands Prefer Glass Over Plastic

Rising disposable incomes average wages grew 6.7% year over year in Q1 2025 allow Czech shoppers to pay premiums for upscale glass-packaged goods.[2]Czech Statistical Office, “Vývoj ekonomiky České republiky – 1. čtvrtletí 2025,” csu.gov.cz Craft breweries leverage bespoke bottle shapes and deep-colored flint variants to signal authenticity, while cosmetics labels such as Dermacol rely on heavy-base flacons to connote quality in export markets. Retail data shows premium SKUs in 330 ml and 500 ml beer bottles gaining shelf share even as mainstream brands trial lighter PET or can options. On-premise channels further amplify glass positioning, with bars highlighting returnable bottle programs as a sustainability badge. Collectively, these product-upgrade dynamics encourage manufacturers to invest in engraved molds, colored frits, and flexible short-run lines that capture higher margins.

Supportive Government Packaging Regulations Help

Prague’s adoption of EU Packaging and Packaging Waste Regulation standards incorporates mandatory recycled-content targets and eco-modulated fees favoring infinitely recyclable substrates. Glass’s chemical inertness and unlimited recyclability qualify it for lower eco-fee tiers, giving bottlers measurable input-cost advantages versus virgin PET. The National Recovery Plan earmarks funding for furnace electrification and waste-heat recovery, allowing incumbent plants to claim emissions credits while cutting utility bills. These policy levers reinforce a virtuous cycle in which higher recycling quotas secure stable cullet supply and manufacturers monetize energy savings from lower melting temperatures.

Strong Beverage Industry Fuels Glass Demand

The Czech Republic retained its title as Europe’s highest per-capita beer consumer in 2024, exporting USD 385.3 million in beer, up 16.48% year over year, while domestic brewers commissioned additional glass bottling lines for premium lagers. Wine volumes remain lower but are climbing as vintners pursue protected-designation status that favors glass bottle provenance cues. Spirits distillers, buoyed by cocktail-bar culture, increasingly specify engraved flint or matte-black bottles to stand out on back bars. Beverage stability during economic slowdowns, plus export growth to non-EU Asia–Pacific markets, assures base-load demand for Czech glass plants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic and Metal Compete with Glass | -0.7% | Global, cost-sensitive segments | Medium term (2-4 years) |

| Fragility Increases Transport and Handling Costs | -0.4% | Czech Republic, export markets | Short term (≤ 2 years) |

| High Energy Costs Limit New Entrants | -0.5% | Czech Republic, Central Europe | Medium term (2-4 years) |

| Recycling Infrastructure Still Needs Improvement | -0.2% | Regional, rural areas primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic and Metal Compete with Glass

Aluminum cans offer 360-degree decoration, rapid chill, and 76% European recycling rates, capturing share among convenience-driven consumers.[3]Ardagh Metal Packaging, “Annual and Transition Report 20-F,” ardaghmetalpackaging.com Promet SK’s launch of 330 ml and 500 ml can sizes caters directly to craft brewers that once relied solely on glass. PET traction remains in value-priced sauces and ready-to-drink tea, where low bottle weight slashes freight expenses. With several multipack beverage formats migrating to slim cans, glass producers must counter by lightweighting, adopting nucleation technologies for strength, and promoting refillable loops.

High Energy Costs Limit New Entrants

Electricity spot rates eased to EUR 0.17/kWh in December 2024 but remain triple pre-2020 averages, locking in high melt costs for soda-lime glass. Czech corporate income-tax hikes to 21% in 2024 further constrict margins, and forward contracts price in gradual gas-network decarbonization levies. While incumbents tap EU decarbonization grants for oxygen-fueled furnaces and photovoltaic arrays, green-field investors face capex that exceeds regional benchmark returns. Resultant barriers to entry preserve today’s producer roster but slow capacity expansions, thereby tempering supply–side responses to demand spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverage Stability and an Accelerating Cosmetics Upswing

The beverages segment held 56.77% of 2025 volumes, underpinning 1.74% forecast growth as the Czech Republic container glass market size for beer alone stretches alongside rising export orders. Robust volumes from lager bottlings cushion cyclical swings, and the Czech Republic container glass market share for beverage formats remains well above 50% through 2031. Wine bottlers add incremental gains from terroir-driven marketing that mandates clear provenance, while spirits adopt heavier bottles and embossing to project premium cues in duty-free channels.

Cosmetics and personal care, expanding at a 2.58% CAGR, inject fresh dynamism through glass droppers, jars, and airless pumps. Local labels exploit glass to emphasize clean-beauty claims, and pan-European e-commerce channels broaden addressable audiences. As consumers pivot toward refillable fragrance bottles, specialty flacons with threaded necks attract contract fillers, sharpening volume gains. Food packaging and specialty preserves fill steady niche orders, supported by farmhouse jam and honey artisans who rely on glass for authenticity and extended shelf life. Pharmaceutical uptake, though smaller, secures double-digit growth in injectable vials and Type II bottles as drugmakers qualify Czech lines for EU stainless-steel ampoule replacement programs.

By Color: Flint Versatility Prevails While Amber Surges

Flint commanded 52.88% of 2025 shipments and is forecast to keep its dominant position thanks to its universal fit across beer, spirits, and condiment shelves. Premium lagers tout the crystal-clear aesthetic to showcase product hue, and cosmetics brands invest in UV-coating additives to mitigate light spoilage without sacrificing transparency. Consequently, the Czech Republic container glass market size tied to flint formulations will remain the core revenue driver for most factories.

Amber glass is on track for a 2.92% CAGR, propelled by pharma’s need for UV-blocking containers and craft brews that seek an artisanal look. Pharmaceutical exports are climbing 10.2% annually, anchoring predictable amber demand, and brewer adoption of retro-style stubby bottles stimulates additional color production runs. Smaller but still relevant, green glass maintains a presence in regional wine lines, while blue and black specialty tones cater to limited-edition cosmetics, essential oils, and liqueurs that command higher average selling prices.

Geography Analysis

The Czech Republic's container glass market is deeply integrated within Central Europe’s packaging network, exporting flint bottles and wide-mouth jars to Germany, Slovakia, and Austria through cost-effective overland routes. In 2024, exports to the United States alone generated USD 64.12 million, underscoring reach beyond the EU’s single market. Domestic volume optimization revolves around two industrial clusters, Moravia in the east and Bohemia in the west, where producers benefit from co-located cullet processors and engineering vendors.

Competition from Western European plants is heating up as Ciner Glass’s EUR 504 million (USD 569.5 million) Belgian facility comes online in 2026, adding 1,300 tons per day to regional supply. Yet Czech makers retain freight-cost edges when serving Central and Eastern Europe, and comparatively lower labor expenses moderate total delivered costs. Government forecasts see GDP growth accelerating to 2.7% in 2025 and holding steady through 2028, fueling domestic demand across food, beverage, and pharma applications.

Cross-border corporate activity signals ongoing consolidation: CANPACK’s sale of Polish glass assets to BA Glass in April 2024 and its planned merger with Giorgi International point to scale-driven strategies. Such transactions can redirect bottle flows and force Czech factories to streamline logistics partnerships. The forthcoming Czech DRS at CZK 4 (USD 0.19) per unit may prompt multinational beverage fillers to harmonize packaging formats across markets, altering regional demand patterns for both one-way and refillable glass.

Competitive Landscape

The Czech Republic container glass market consists of a moderate concentration of established manufacturers: Vetropack Moravia Glass, Stoelzle Union, and O-I Czech Republic collectively supply the bulk of domestic demand, while smaller firms such as ADPACK and Galapack serve agile niche orders. Vetropack’s 800 million CZK share capital backs furnace upgrades and lightweighting R&D aimed at shaving glass per bottle without compromising mechanical strength. Stoelzle Union pushes custom embossing and short production runs to secure premium spirits contracts, whereas O-I leverages its global design library for regional brand extensions.

Strategic emphasis centers on energy and emission cuts. Firms invest in oxy-fuel furnace retrofits, batch pre-heaters, and high-recycled-cullet ratios to shrink kilowatt-hour consumption per ton. Sklostroj Turnov’s IS machine controls allow automatic gob weight adjustments, reducing defect rates and easing mold changeovers. Meanwhile, amber and pharma-grade capacity additions safeguard margins in segments less vulnerable to metal and plastic substitution.

Competitive pressure also originates from substitute packaging suppliers. Ardagh Metal Packaging’s 2024 revenue of USD 4.908 billion spotlights the scale of can producers vying for beverage accounts. Glass makers therefore collaborate with brewers and cosmetics firms to develop storytelling around heritage and recyclability, securing brand loyalty despite higher tare weight.

Czech Republic Container Glass Industry Leaders

SKLÁRNY MORAVIA, a.s.

OI Czech Republic as

ADPACK group, s.r.o.

Vetropack Moravia Glass, a. s.

Stoelzle Union s.r.o

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Ciner Glass signed EUR 504 million (USD 545 million) financing to construct a 1,300 tons-per-day facility in Lommel, Belgium, to be operational by Q2 2026.

- June 2025: WACKER announced a specialty-silicones plant in Karlovy Vary, scheduled for end-2025 start-up, expanding local coatings supply for glass finishing.

- May 2025: Vetropack appointed Lukas Burkhardt as CEO, emphasizing cost optimization and furnace modernization.

- March 2025: Ardagh Metal Packaging reported USD 4.9 billion 2024 revenue, highlighting rising can-format competition.

Czech Republic Container Glass Market Report Scope

Glass containers are vessels made from glass used to store and protect products such as food, beverages, pharmaceuticals, cosmetics, and chemicals. Available in diverse shapes and sizes, such as bottles, jars, and vials, these containers provide airtight seals and protect contents from external contaminants. Glass packaging is valued for its non-reactive nature, preservation of product quality, and high recyclability. These attributes make glass containers a preferred choice for packaging across multiple industries.

The Czech Republic container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, and by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How fast is the Czech Republic container glass market expected to grow between 2026 and 2031?

Volume is projected to rise from 304.48 kilotons to 334.68 kilotons at a 1.91% CAGR.

Which end-user category contributes the most glass demand?

Beverages account for 56.77% of 2025 shipments, supported by strong beer and growing wine volumes.

Why is amber glass gaining popularity?

Pharma and craft beverage producers value amber’s UV protection, driving a 2.92% CAGR for the color segment.

What upcoming regulation could boost glass packaging adoption?

The deposit return system scheduled for 2027 and the ongoing phase-out of single-use plastics both favor reusable or recyclable glass.

How are energy costs influencing production strategies?

High electricity prices encourage incumbents to retrofit furnaces with oxy-fuel or electric melting technology to reduce kilowatt-hour consumption per ton.

Which new capacity addition will affect regional supply?

Ciner Glass’s 1,300 tons-per-day Belgian plant, scheduled for Q2 2026, will increase competition in Western and Central Europe.

Page last updated on: