Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

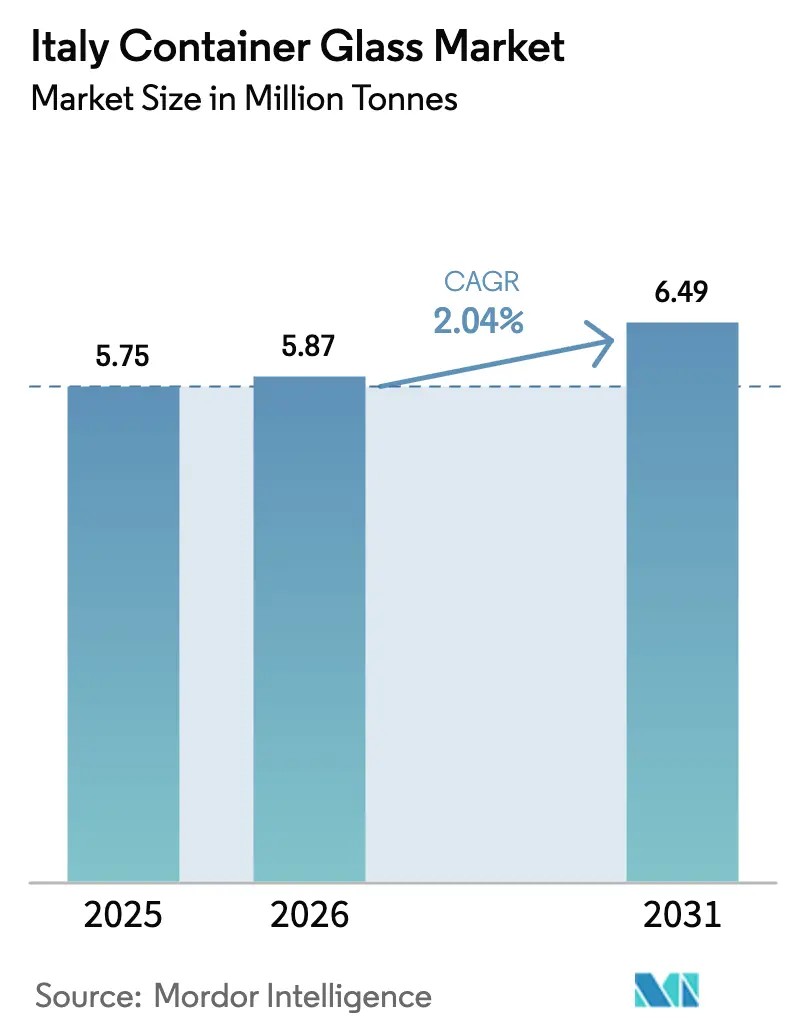

| Base Year Market Size (2025) | 5.75 Million tonnes |

| Market Volume (2026) | 5.87 Million tonnes |

| Market Volume (2031) | 6.49 Million tonnes |

| Growth Rate (2026 - 2031) | 2.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Container Glass Market Analysis by Mordor Intelligence

The Italy Container Glass Market size is expected to grow from 5.75 million tonnes in 2025 to 5.87 million tonnes in 2026 and is forecast to reach 6.49 million tonnes by 2031 at 2.04% CAGR over 2026-2031. This steady trajectory shows how the Italy container glass market benefits from a mature recycling ecosystem, strong premium beverage demand, and supportive circular-economy legislation. The Italy container glass market continues to enjoy favorable consumer sentiment toward recyclable packaging, even as lightweight alternatives compete aggressively on logistics costs. Regulatory incentives for recycled content reinforce the Italy container glass market’s resilience, while glass’s premium image sustains pricing power in wine, spirits, and cosmetics applications. Technology investments in electric and hybrid furnaces, coupled with expanding cullet supplies, further anchor the Italy container glass market on a balanced path of incremental volume gains and rising value per ton.

Key Report Takeaways

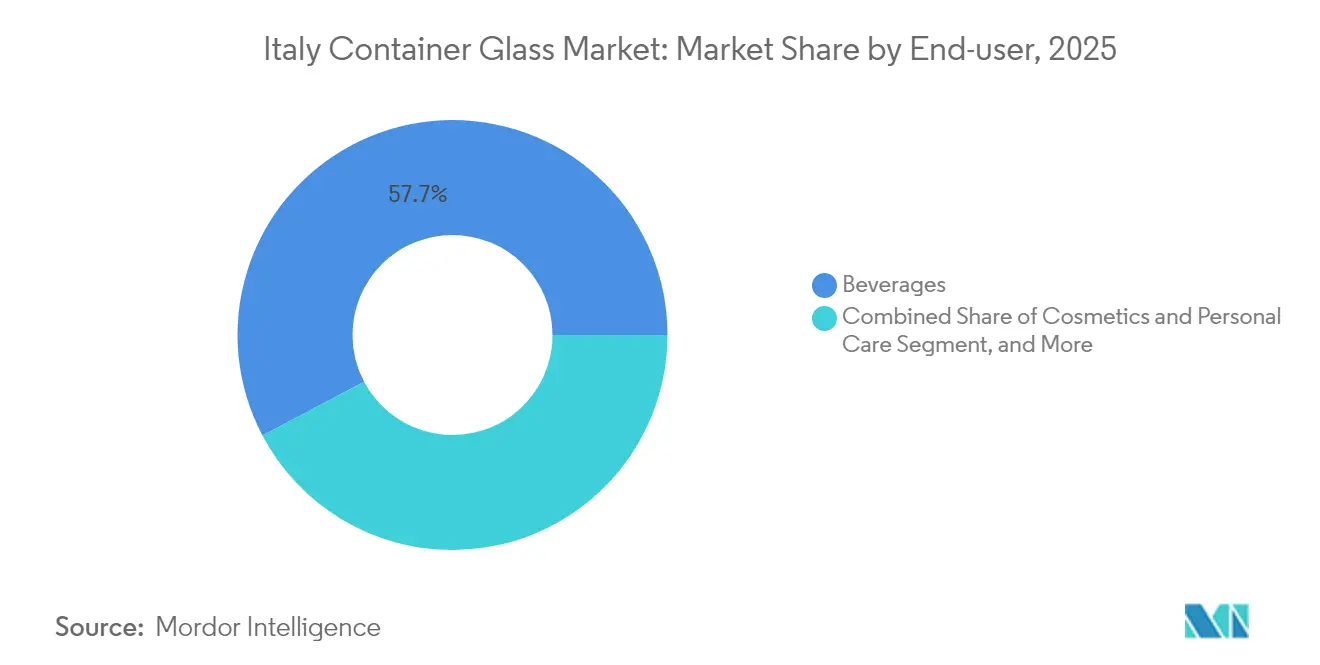

- By end-user, beverages captured 57.74% of the Italy container glass market share in 2025.

- By color, the Italy container glass market size for the amber glass segment is forecast to advance at a 3.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Eco-Friendly and Sustainable Packaging Solutions | +0.8% | Italy, with spillover to EU markets | Medium term (2-4 years) |

| Government Policies and EU Regulations Supporting Circular Economy | +0.6% | Italy and broader EU region | Long term (≥ 4 years) |

| Booming Beverage Industry, Especially Wine, Spirits, and Craft Beer | +0.4% | Northern Italy wine regions, national spirits market | Short term (≤ 2 years) |

| Health and Safety Awareness Among Consumers | +0.3% | Italy, particularly urban centers and premium market segments | Medium term (2-4 years) |

| Technological Innovations in Glass Manufacturing | +0.3% | Italy manufacturing hubs in Veneto and Lombardy | Medium term (2-4 years) |

| Premium Branding and Shelf Appeal of Glass Packaging | +0.2% | Italy, with focus on luxury goods and export markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Eco-Friendly and Sustainable Packaging Solutions

Italian shoppers view endlessly recyclable glass as a tangible response to packaging waste concerns. Supermarkets now prioritize shelf space for products in returnable or high-recycled-content bottles, pushing brand owners toward glass. The PPWR target of 90% collection by 2030 accelerates this shift, and the Italy container glass market gains structural support as CONAI’s reverse-logistics network achieves consistent cullet flows. Brands willing to pay a green premium amplify demand, ensuring that the Italy container glass market remains the default for high-image goods while plastic alternatives face levies and reputational risks.[1]European Commission, “Packaging and Packaging Waste,” ec.europa.eu

Government Policies and EU Regulations Supporting Circular Economy

Italy’s plastic tax of EUR 0.45 (USD 0.48) per kg, introduced in 2024, immediately narrowed the cost gap between PET and glass. Extended producer-responsibility fees now scale with recyclability scores, effectively subsidizing glass because of its high recovery rate. National glass-recycling plants operating under CoReVe process more than 2 million tons of cullet annually, guaranteeing supply stability for producers. These policy levers collectively raise the baseline for the Italy container glass market and discourage substitution in premium segments.[2]Conai, “Nel 2022 Riciclato il 71.5% dei Rifiuti di Imballaggio,” conai.org

Booming Beverage Industry, Especially Wine, Spirits, and Craft Beer

Wine production of 44.5 million hectoliters in 2024 underpins a deep pipeline of bottle demand, and premium labels continue to specify heavier glass for brand distinctiveness. Over 900 craft breweries amplify call-offs for bespoke bottles that symbolize authenticity. Export-oriented spirit makers, enjoying double-digit U.S. sales growth, rely on glass for shelf impact and regulatory acceptance abroad. This cocktail of volume and value protects the Italy container glass market from near-term volume erosion and sustains furnace utilization rates.

Technological Innovations in Glass Manufacturing

Electric and hybrid furnaces installed in northern Italy demonstrate 15% lower energy intensity and quicker color changeovers. Real-time furnace modeling extends campaign life and curbs downtime, while advanced optical sorters elevate cullet purity, allowing recycled content to exceed 50% in some production runs. These technical gains nurture margins and lower carbon footprints, reinforcing competitiveness of the Italy container glass market even as fuel prices fluctuate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Competition from Lightweight and Cost-Effective Alternatives | -0.4% | Italy and broader European markets | Short term (≤ 2 years) |

| Fragility and Risk of Breakage During Handling and Transport | -0.3% | Italy, particularly affecting export and logistics operations | Medium term (2-4 years) |

| Higher Transportation and Storage Costs Due to Weight | -0.3% | Italy, particularly affecting export markets | Medium term (2-4 years) |

| Limited Design Flexibility Compared to Malleable Materials | -0.2% | Italy, with focus on consumer goods and beverage sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense Competition from Lightweight and Cost-Effective Alternatives

Aluminum cans weigh roughly 60% less than equal-volume glass, trimming freight outlays by as much as 25% for long hauls. PET bottles add design freedom and shatter resistance that appeal to on-the-go consumers. Beverage giants seeking quick cost wins can pivot formats rapidly, siphoning shared volume from the Italy container glass market in entry-price segments. Glass producers respond by targeting premium lines where packaging is central to brand heritage rather than a commodity cost.

Higher Transportation and Storage Costs Due to Weight

Each glass bottle’s heft raises per-unit transport spend by EUR 0.15-0.25 (USD 0.16-0.26) on long routes, and warehouse operators allocate 40% more space for safe stacking. As diesel surcharges and impending carbon fees widen logistics expense, exporters face shrinking margins. The Italy container glass market therefore concentrates on domestic and near-field EU flows, accepting a geography-bound opportunity set until greener logistics options scale.[3]Ardagh Group, “Climate Action,” ardaghgroup.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Anchor Premium Positioning

The beverage segment commanded 57.74% of the Italy container glass market in 2025, generating the bulk of furnace throughput and sustaining multi-shift operations. Alcoholic drinks especially wine account for 35% of total volume and remain closely tied to rural viticulture clusters. Craft beer, posting 4.2% annual growth, energizes demand for distinctive bottle molds that smaller glassmakers can supply at attractive margins. Non-alcoholic premium juices and botanical sodas join this momentum, reinforcing the Italy container glass market size uplift.

Cosmetics and personal care exhibits the fastest expansion at a 3.9% CAGR, reflecting consumers’ appetite for refillable glass jars and prestige fragrances. Luxury brands leverage glass’s tactile and visual cues to justify higher price points, lifting revenue density per ton. Food applications form a stable, low-volatility base, while pharmaceutical vials and ampoules gain from Italy’s export-oriented drug sector. Together, these trends keep furnace utilization above 90% and encourage lines dedicated to smaller-batch, higher-margin runs.

By Color: Flint Retains Scale, Amber Accelerates

Flint glass delivered 36.85% of the Italy container glass market size in 2025, leveraging broad applicability across wine, spirits, and upscale waters. Transparent packaging showcases liquid color and clarity, attributes that premium producers exploit for shelf differentiation. Scale economies in flint production keep per-unit costs competitive despite rising energy prices, preserving its backbone role in the Italy container glass market.

Amber glass is advancing at 3.62% CAGR, fueled by pharmaceuticals that require UV shielding and by craft brewers favoring the classic amber look. Higher recycled-content thresholds are easier to achieve in amber, adding a sustainability edge. Green bottles continue to support traditional wine exports, while specialty hues serve niche promotional runs. Color diversity increasingly operates as a brand accessory rather than a technical constraint, widening the design palette available to Italy container glass market participants.

Geography Analysis

Northern Italy houses roughly 65% of container glass capacity, with Veneto and Lombardy offering dense clusters of skilled labor, cullet suppliers, and proximate beverage clients. The regional colocation of glassworks and wineries compresses delivery lead times, a decisive advantage for just-in-time bottling operations. Electric furnace pilots in Verona illustrate how the Italy container glass market can decarbonize while staying anchored in its historical heartland.

Central territories such as Tuscany and Lazio provide growing pockets of demand, propelled by luxury wine estates and Rome’s cosmetics distribution hub. Glassmakers expanding here accept longer cullet supply lines but gain access to premium customers who value bespoke bottle shapes. Recent brownfield expansions in Florence target export-ready wine brands, broadening the Italy container glass market’s mid-peninsula footprint.

Southern Italy contends with higher outbound freight costs to northern buyers yet offers comparative labor savings. Incremental investments in Sicily exploit closeness to Mediterranean shipping lanes, enabling the Italy container glass market to service North African and Middle Eastern beverage fillers. EU infrastructure funding continues to upgrade southern road and port networks, progressively narrowing the logistics gap with the north.

Competitive Landscape

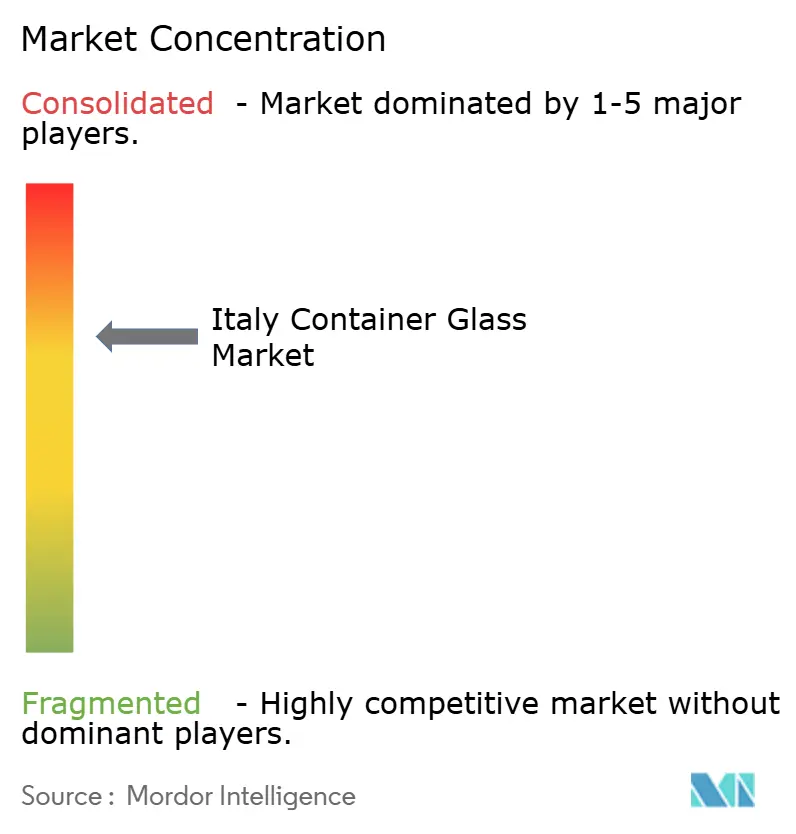

The competitive arena shows moderate concentration, with Verallia Italia, O-I Glass Italy, and Zignago Vetro controlling a material share yet leaving room for mid-tier firms specializing in artisanal runs. Corporate strategies focus on capital efficiency, furnace modernization, and vertically integrated cullet procurement. Verallia’s EUR 1.2 billion (USD 1.29 billion) Allied Glass acquisition widens specialty know-how, bolstering its claim on high-value spirits packaging. Zignago Vetro’s planned EUR 45 million pharmaceutical line demonstrates the pivot to margin-rich segments where certification and traceability act as entry barriers.

Technology differentiation is now central. O-I’s optical-sorting upgrade feeds cleaner cullet, allowing 50% recycled content without compromising bottle clarity. Ardagh’s biofuel trials point to long-range carbon reductions that could insulate the Italy container glass market from escalating ETS charges. Smaller players mitigate scale disadvantages through flexible molding equipment and rapid color-change capability, serving craft beverage labels that require limited production lots.

Customer intimacy remains pivotal. Wineries and cosmetics brands demand collaborative design and just-in-time drops, favoring suppliers located within a day’s drive. This logistics reality preserves a multi-player landscape despite global consolidation trends. Because the top five producers hold around 70% of national volume, the market receives a concentration score of 7, reflecting significant yet not overwhelming dominance.

Italy Container Glass Industry Leaders

Verallia Group

Vetropack Holding Ltd

Vetri Speciali SpA

Vetrobalsamo S.p.A.

O-I Glass Italy S.r.l. (Owens-Illinois)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Stevanato Group posted Q1 2025 revenue of USD 269.93 million, citing strong demand for EZ-Fill ready-to-use vials.

- April 2025: Ardagh Group completed biofuel furnace trials in Italy, recording a 15% carbon-emission cut.

- March 2025: O-I Glass Italy commissioned high-precision optical sorters to raise recycled content potential to 50%.

- February 2025: Zignago Vetro unveiled a EUR 45 million (USD 49.5 million) line dedicated to cosmetics and pharma bottles, set to open in 2026.

Italy Container Glass Market Report Scope

Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents. It is often chosen for products where purity, safety, and environmental sustainability are paramount concerns.

The Italy container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large is the Italy container glass market in 2026?

The market totals 5.87 million tonnes in 2026 and is on track for 2.04% compound growth through 2031 (2026-2031).

Which end-user segment dominates demand?

Beverages account for 57.74% of total volume, driven by wine, spirits, and expanding craft beer lines.

Why is amber glass growing faster than other colors?

Amber’s UV-blocking properties meet pharmaceutical and craft-beer needs, pushing a 3.62% CAGR to 2031.

How do EU regulations influence glass packaging in Italy?

Plastic taxes, higher recycling targets, and extended producer-responsibility fees encourage brand owners to choose glass and raise recycled content mandates.

What technology trends shape competitiveness among Italian glassmakers?

Investments in electric or hybrid furnaces, optical cullet sorting, and rapid color-change lines cut emissions and improve production flexibility.

Page last updated on: