Slovakia Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

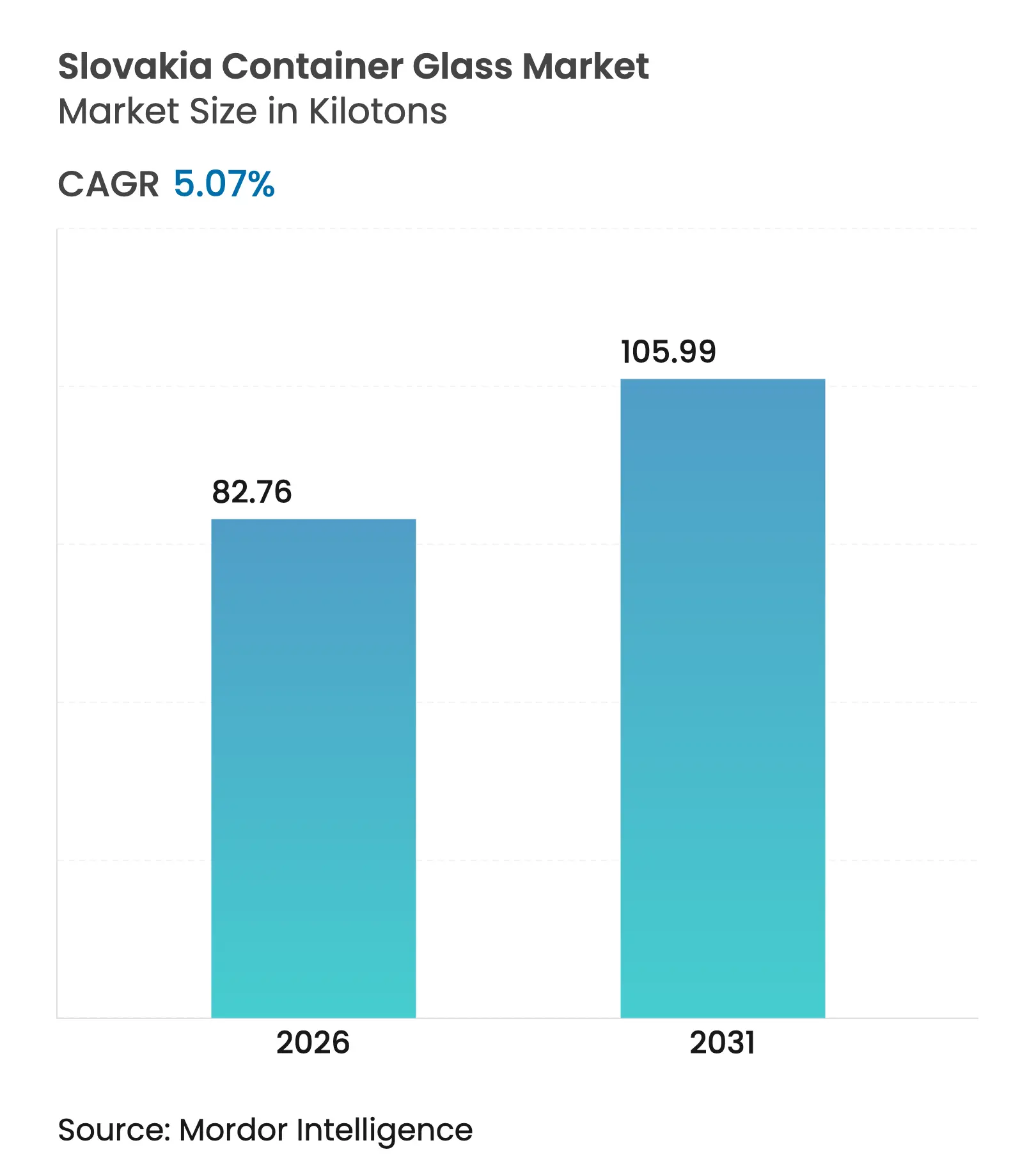

| Market Volume (2026) | 82.76 kilotons |

| Market Volume (2031) | 105.99 kilotons |

| CAGR | 5.07 % |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Slovakia Container Glass Market Analysis by Mordor Intelligence

The Slovakia container glass market size in 2026 is estimated at 82.76 kilotons, growing from 2025 value of 78.77 kilotons with 2031 projections showing 105.99 kilotons, growing at 5.07% CAGR over 2026-2031. Firm integration with regional food, beverage, and pharmaceutical supply chains, combined with a revealed comparative advantage (RCA1 = 1.55) in glass exports, underpins steady output expansion.[1]C. Boumová, “Revealed Comparative Advantage of Slovak Glass Exports,” Studia Commercialia, scb.euba.sk The rising adoption of circular economy targets, proximity to Germany, the Czech Republic, and Poland, and labor costs that remain below Western European averages all reinforce Slovakia’s cost competitiveness. At the same time, EU decarbonization mandates accelerate furnace electrification, pushing producers toward hybrid and hydrogen-ready technologies that can insulate margins from volatile energy pricing. Supply-chain realignment triggered by reduced imports from Russia, Belarus, and Ukraine further redirects order volumes into the Slovakia container glass market, ensuring high asset utilization and encouraging capacity upgrades.

Key Report Takeaways

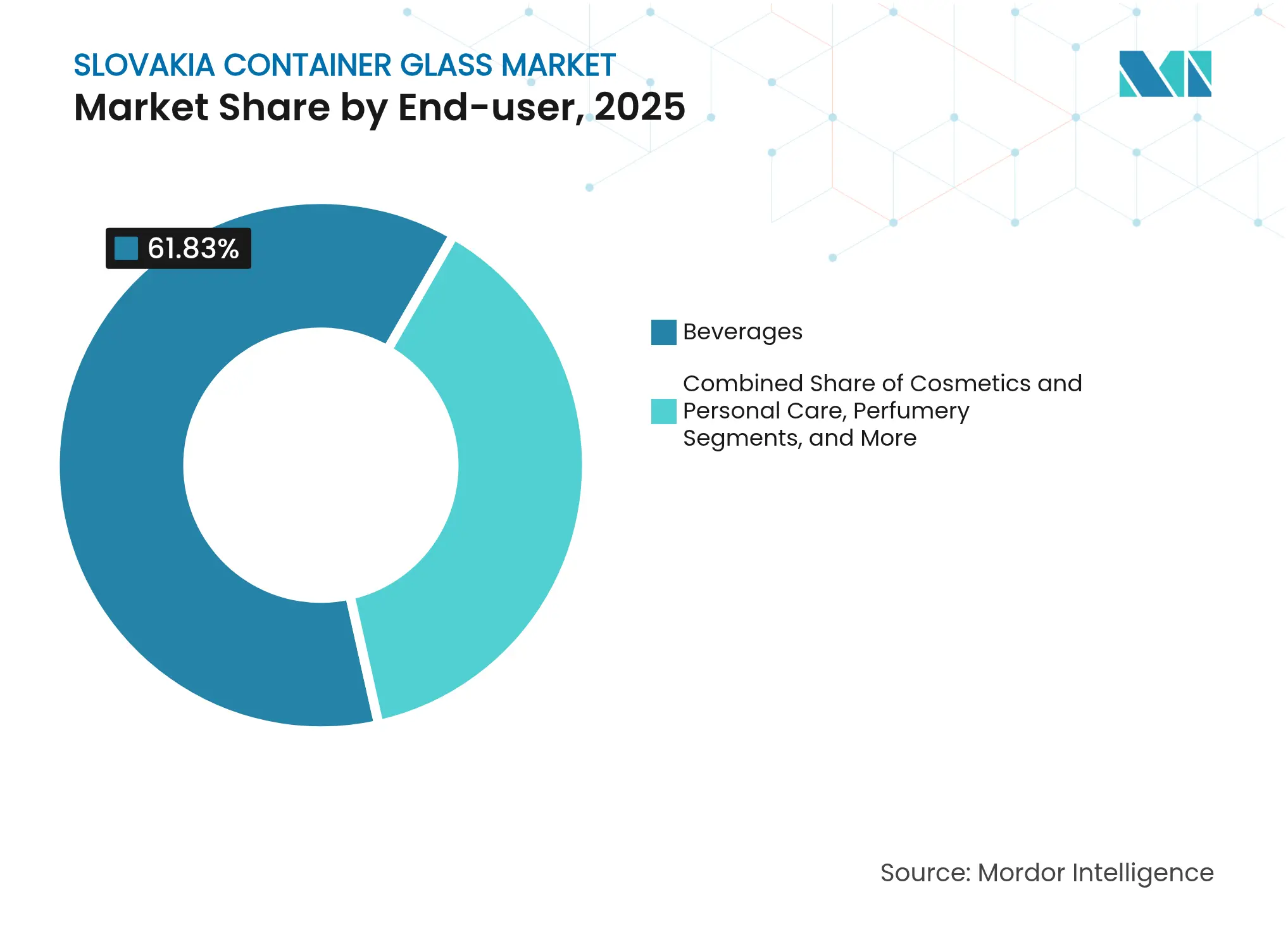

- By end-user, beverages captured 61.83% of the Slovakian container glass market share in 2025.

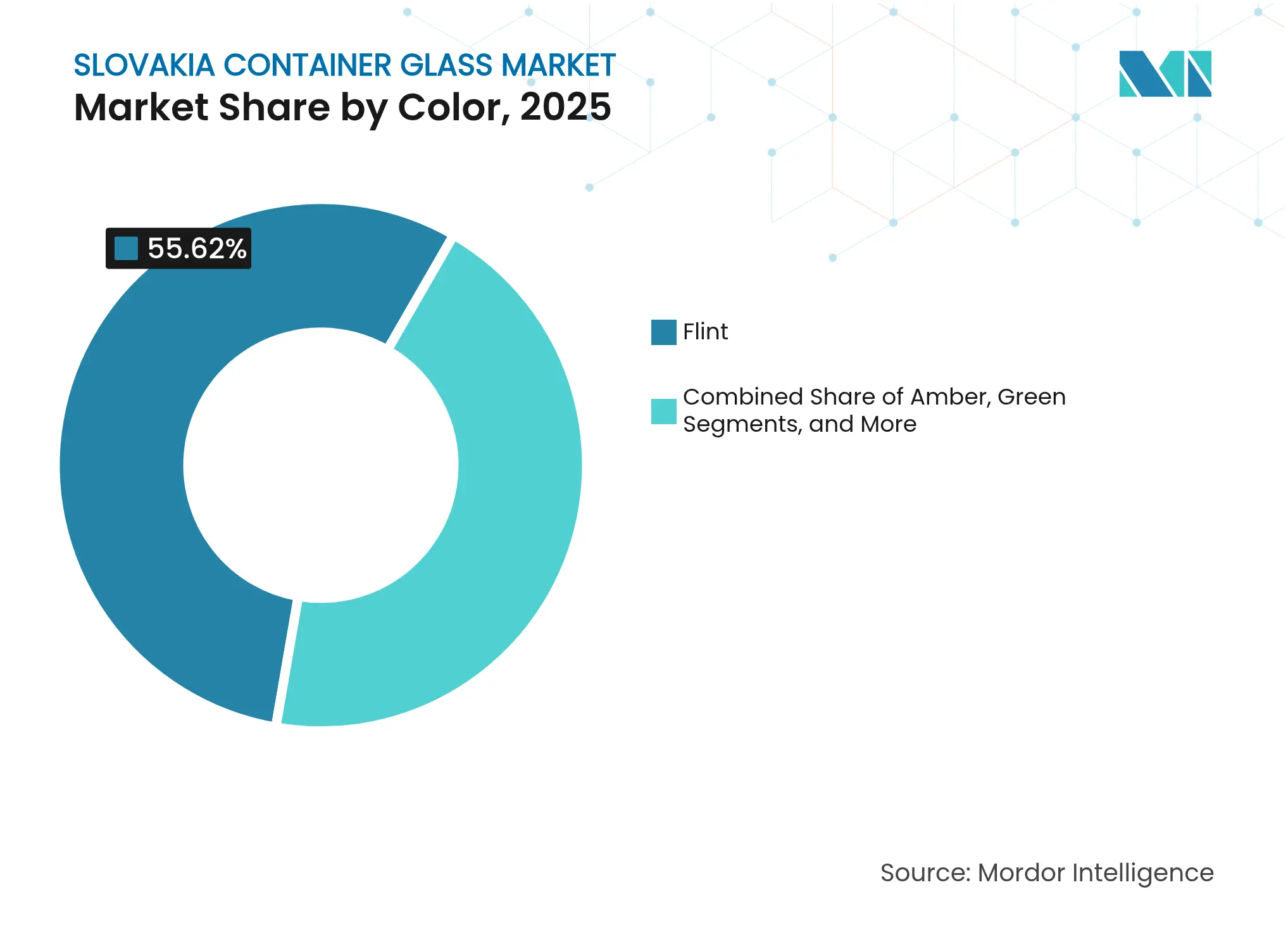

- By color, the Slovakian container glass market size for the amber segment is projected to grow at a 5.74% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Slovakia Container Glass Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Eco-friendly packaging demand acceleration Eco-friendly packaging demand acceleration | +1.2% | EU-wide | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:EU-wide | Impact Timeline:Medium term (2-4 years) |

Food and beverage sector volume growth Food and beverage sector volume growth | +1.8% | National & regional | Short term (≤ 2 years) | |||

EU single-use plastics directive compliance EU single-use plastics directive compliance | +0.9% | EU-wide | Long term (≥ 4 years) | |||

High recycling rates & closed-loop systems High recycling rates & closed-loop systems | +0.7% | National & regional | Medium term (2-4 years) | |||

Craft spirits & microbrewery premiumization Craft spirits & microbrewery premiumization | +0.6% | National & regional | Short term (≤ 2 years) | |||

Pharma near-shoring for vial-size packs Pharma near-shoring for vial-size packs | +0.8% | Central Europe | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Eco-friendly Packaging Demand Acceleration

Consumer and regulatory momentum toward 100% recyclable packaging by 2030 is channeling fresh orders into the Slovakia container glass market. Slovakia’s collection rate exceeds the EU average of 80.1%, ensuring an abundant supply of cullet that reduces raw material usage and energy needs.[2]A. Kuhn, “EU Parliament Imposes Sustainable Wine Packaging,” Meiningers International, meiningers-international.com Global brands operating production lines in Bratislava and Trnava are increasingly specifying glass to align with their corporate net-zero roadmaps. Survey data indicate that 40% of European shoppers actively choose glass for circularity reasons, enabling Slovak producers to negotiate price premiums, particularly in flint and amber formats used for premium foods and beverages. Favorable economics of closed-loop manufacturing, achieved through cullet substitution savings of up to EUR 850 (USD 919) per ton and 322 kWh per ton of energy, deepen the competitive moat for incumbents. With EU lawmakers finalizing the Packaging and Packaging Waste Regulation, the demand curve for glass packaging is set on a steeper trajectory, directly benefiting the Slovakia container glass market.

Food and Beverage Sector Volume Growth

Slovakia’s role as a processing hub for beer, wine, fruit spirits, and specialty foods stimulates the continuous off-take of returnable and one-way bottles within the Slovakian container glass market. Preliminary 2025 trade data highlight the expansion of agri-food exports to Germany, Austria, and the Czech Republic, each relying on standardized glass formats for regulatory compliance and shelf appeal. Breweries and craft distilleries often favor heavier bottles that convey authenticity and allow for hot-fill processes, while premium honey, jam, and condiment brands typically adopt clear flint jars to showcase their product quality. Volume commitments from supermarket private-label contracts ensure baseline furnace loading, while seasonal spikes linked to harvest periods help smooth capacity utilization. Together, these factors reinforce a resilient demand profile through at least 2028.

EU Single-Use Plastics Directive Compliance Push

Directive 2019/904 bans several plastic items and imposes recycled-content thresholds, encouraging beverage fillers to adopt glass alternatives. Hospitality operators face a January 2030 deadline to eliminate single-use plastics, prompting distributors to invest in closed-loop bottle recycling systems. Slovakia’s legislators have synchronized national compliance measures with EU milestones, providing manufacturers with regulatory predictability to justify furnace retrofits. Deposit-return schemes under discussion could further lower effective input costs by boosting cullet inflows and reducing virgin material purchases.

High Recycling Rates and Closed-Loop Infrastructure

Collection networks organized around yellow-bag and bottle-bank systems enable color-sorted cullet streams, raising melt quality and furnace efficiency for Slovakia container glass market producers. Cross-border cullet trading with Austria and the Czech Republic offers flexibility to fine-tune batch chemistry, ensuring consistent optical clarity and tensile strength in flint products. Long-term EU targets mandating 75% recycling of all glass packaging by 2030 incentivize continued capital spending on automated sorting and washing facilities, effectively locking in supply advantages for established Slovak plants.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

PET & aluminium substitution gains PET & aluminium substitution gains | -1.1% | Global | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.1% | Geographic Relevance:Global | Impact Timeline:Medium term (2-4 years) |

Volatile energy prices for furnace operations Volatile energy prices for furnace operations | -0.8% | National & regional | Short term (≤ 2 years) | |||

Skilled furnace operator shortage Skilled furnace operator shortage | -0.6% | National | Medium term (2-4 years) | |||

EU ETS Phase IV CO₂ quota tightening EU ETS Phase IV CO₂ quota tightening | -0.4% | EU-wide | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

PET and Aluminium Substitution Gains

Lightweight PET bottles can reduce freight costs by up to 90% compared to glass equivalents, providing soft-drink makers a strong economic incentive to switch to this format in high-volume, low-margin categories. Aluminium’s improved oxygen-barrier linings attract brewers seeking shelf-life extension, while offering recyclability messaging that narrows the sustainability edge of glass. Commodity beverage segments, therefore, experience gradual glass displacement; however, premium brands continue to favor glass for perceived quality, limiting the overall drag on the Slovakia container glass market.

Volatile Energy Prices for Furnace Operations

Electricity accounts for 15-20% of the total cost for continuous melt furnaces. Slovakia’s tariff path has become less predictable since the reduction of Russian gas imports, exposing glassmakers to margin compression during peak price periods. While hybrid furnaces and waste-heat recovery help mitigate volatility, smaller, independent plants lack the balance-sheet capacity to fund large-scale retrofits, constraining their expansion plans.

Segment Analysis

By End-user: Beverages Dominate, Cosmetics Accelerate

The beverages category accounted for 61.83% of Slovakia's container glass market size in 2025, a share sustained by established beer, wine, and spirits bottling lines that anchor furnace utilization across Bratislava and Trnava. Continuous production schedules enable cost spreading over high volumes, allowing for competitive export pricing in Germany and Austria. Craft distilleries add incremental demand for bespoke bottles, while mainstream brewers maintain large orders for returnable crates, ensuring stability in kiloton throughput. Food applications, spanning jams, honey, and condiments, deliver steady but lower-margin runs, benefiting from Flint’s transparency that signals product purity on retail shelves. Pharmaceutical fillers near-shoring low-volume specialty medicines rely on Type III and Type II containers, creating premium side streams that lift average selling prices without requiring major color change downtime.

Cosmetics and personal care, although representing a smaller base, are projected to grow at a 6.05% CAGR to 2031, the fastest within the Slovakian container glass market. Luxury skin-care brands favor thick-walled flint and specialty tints with high clarity, stimulating investments in advanced IT-controlled forming lines capable of maintaining tight dimensional tolerances. European brand owners increasingly relocate packaging procurement to Central Europe to shorten lead times, and Slovakia’s logistics links make it an attractive node. Perfumery’s decorative frosting and metallization needs spur value-added services, expanding glassmakers’ revenue beyond container supply. As a result, the Slovakian container glass industry captures rising margins while diversifying away from the volume swings of the beverage industry.

Note: Segment shares of all individual segments available upon report purchase

By Color: Flint Retains Scale, Amber Leads Growth

Flint glass held 55.62% of Slovakia's container glass market share in 2025, due to its versatility across the food, beverage, and healthcare domains. Producers benefit from shared cullet pools and simplified furnace color campaigns, which reduce changeover costs and scrap. The segment also capitalizes on consumer preference for product visibility, crucial for premium honey and condiment jars. Continuous R&D in oxygen-enriched combustion lowers flint’s traditionally higher energy needs, reinforcing cost advantages.

Amber glass is forecast to post a 5.74% CAGR, outperforming other colors due to surging demand for UV-protective pharmaceutical bottles and premium beverage lines emphasizing heritage aesthetics. Slovak furnaces have integrated robot-assisted color stacking to execute quicker switchover from flint to amber, minimizing production downtime. Green glass is closely tied to regional wine and certain beer brands, offering stable yet mature demand. Niche blues and custom hues cater to cosmetics and spirits, where unique shades elevate shelf differentiation and justify higher price points, albeit at lower tonnage.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Western Slovakia, which clusters around Bratislava, Trnava, and Nitra, accounts for most furnace capacity, leveraging highway and rail corridors that enable outbound deliveries to Austria in under three hours and to southern Germany in six. These corridors anchor the Slovakia container glass market, enabling just-in-time replenishment for beverage fillers located across Central Europe. Midwestern Žilina and Trenčín add secondary glass output, benefiting from proximity to automotive OEMs that cultivate a skilled industrial labor pool shared with glassmakers.

Cross-border commerce enjoys tariff-free access within the EU single market, driving balanced two-way trade flows, as evidenced by a Grubel-Lloyd index of 1.00 with Ukraine before the conflict and stability with the Czech Republic since 2024. As Eastern European imports declined after 2022, Slovak producers absorbed redirected orders, resulting in furnace load factors exceeding 93% in 2025. Forward-looking investors plan brownfield expansions near the Polish border to shorten lead times for northern markets.

Labor cost advantages persist: the average gross monthly earnings of EUR 1,403 (USD 1,518) in 2023 translate into a double-digit wage gap compared to German and French plants, yet remain compatible with EU quality standards. Although worker shortages threaten ramp-ups, policy incentives for vocational training and regional development funds ameliorate pressure. Combined, these geographic advantages secure Slovakia’s role as a resilient node within the continental glass-packaging value chain.

Competitive Landscape

Market Concentration

The Slovakia container glass market is moderately consolidated: a handful of European majors operate multi-furnace complexes, while smaller local players focus on niche runs. Capital requirements for furnace rebuilds averaging EUR 40 million (USD 43.2 million) every 12-14 years deter new entrants and reinforce incumbent dominance. Strategic emphasis centers on decarbonization, with Verallia’s hydrogen pilot and O-I Glass’s electrified batch melter each targeting a 50% reduction in CO₂ emissions relative to 2020 baselines.

Product innovation scales alongside sustainability drives. Vetropack’s Echovai bottle reduces weight by 30% while preserving returnability, thereby lowering logistics emissions and extending crate life cycles. Competitors respond with internal lightweighting programs and reductions in embossing to trim material use. Furthermore, ISO 15378 certification shields the pharmaceutical sub-segment from new players lacking sterile-manufacturing credentials, enabling established firms to command price premiums.

M&A activity resumed in 2024 with Verallia's acquisition of Vidrala’s Italian assets, thereby expanding southern European capacity and enhancing shipping synergies into Slovakia via rail links. Private equity interest surfaces in cullet-processing startups that feed color-sorted glass into Slovak furnaces, signaling a move toward vertical integration of recycling streams. Overall, strategic playbooks center on carbon-cost mitigation, automation, and portfolio diversification into higher-margin cosmetic and pharmaceutical containers.

Slovakia Container Glass Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vetropack announced leadership transition with Lukas Burkhardt becoming CEO at year-end.

- March 2025: Verallia began hydrogen-powered melting at Essen-Karnap and started hybrid furnace installation at Saint-Romain-Le-Puy.

- September 2024: Hrastnik launched a hybrid regenerative furnace, achieving 60% CO₂ reduction.

- June 2024: Ciner Glass has unveiled a EUR 504 million (USD 545 million) greenfield plant in Belgium, slated for commissioning in 2026.

Table of Contents for Slovakia Container Glass Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Eco-friendly packaging demand acceleration

- 4.2.2Food and beverage sector volume growth

- 4.2.3EU single-use plastics directive compliance push

- 4.2.4High recycling rates and closed-loop infrastructure

- 4.2.5Craft spirits and microbrewery premiumisation boom

- 4.2.6Pharma near-shoring to Central Europe for vial-size packs

- 4.3Market Restraints

- 4.3.1PET and aluminium substitution gains

- 4.3.2Volatile energy prices for furnace operations

- 4.3.3Skilled furnace operator shortage

- 4.3.4EU ETS Phase IV CO2 quota tightening

- 4.4PESTEL Analysis

- 4.5Industry Value Chain Analysis

- 4.6Container Glass Furnace Capacity and Locations in Slovakia

- 4.6.1Plant Locations and Year of Commencement

- 4.6.2Production Capacities

- 4.6.3Types of Furnaces

- 4.6.4Color of Glass Produced

- 4.7Export-Import Data of Container Glass - Covering Key Import and Export Destinations

- 4.7.1Import Volume and Value, 2021-2024

- 4.7.2Export Volume and Value, 2021-2024

- 4.8Porter's Five Forces Analysis

- 4.8.1Threat of New Entrants

- 4.8.2Bargaining Power of Suppliers

- 4.8.3Bargaining Power of Buyers

- 4.8.4Threat of Substitutes

- 4.8.5Competitive Rivalry

- 4.9Raw Material Analysis

- 4.10Recycling Trends for Glass Packaging

- 4.11Demand vs Supply Analysis for Glass Packaging

5. MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1By End-user

- 5.1.1Beverages

- 5.1.1.1Alcoholic

- 5.1.1.1.1Beer

- 5.1.1.1.2Wine

- 5.1.1.1.3Spirits

- 5.1.1.1.4Other Alcoholic Beverages (Cider and Other Fermented Drinks)

- 5.1.1.2Non-Alcoholic

- 5.1.1.2.1Juices

- 5.1.1.2.2Carbonated Drinks (CSDs)

- 5.1.1.2.3Dairy Product Based Drinks

- 5.1.1.2.4Other Non-Alcoholic Beverages

- 5.1.2Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles)

- 5.1.3Cosmetics and Personal Care

- 5.1.4Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.5Perfumery

- 5.2By Color

- 5.2.1Green

- 5.2.2Amber

- 5.2.3Flint

- 5.2.4Other Colors

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves and Developments

- 6.3Company Market Share Analysis, (Based on Latest Production Capacity)

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Vetropack Nemsova a.s.

- 6.4.2O-I Glass, Inc.

- 6.4.3Ardagh Glass Packaging

- 6.4.4Stoelzle Glass Group

- 6.4.5Saverglass SAS

- 6.4.6BA Glass Croatia d.o.o.

- 6.4.7Verallia Packaging Czech s.r.o.

- 6.4.8Heinz-Glas GmbH and Co. KGaA

- 6.4.9Gerresheimer AG

- 6.4.10Vetropack Moravia Glass a.s.

- 6.4.11Huta Szkla Jaslo Sp. z o.o.

- 6.4.12Glassworks Skloplast Trnava s.r.o.

- 6.4.13Vidrala SA

- 6.4.14Pochet du Courval SA

- 6.4.15Bruni Glass S.p.A.

- 6.4.16Stoelzle Masnieres Parfumerie SAS

- 6.4.17Saverglass Polska Sp. z o.o.

- 6.4.18Nampak Glass Europe BV

- 6.4.19Calaso BV

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

Slovakia Container Glass Market Report Scope

Glass containers are vessels made from glass used to store and protect products such as food, beverages, pharmaceuticals, cosmetics, and chemicals. Available in diverse shapes and sizes, such as bottles, jars, and vials, these containers provide airtight seals and protect contents from external contaminants. Glass packaging is valued for its non-reactive nature, preservation of product quality, and high recyclability. These attributes make glass containers a preferred choice for packaging across multiple industries.

The Slovakia container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, and by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.