Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

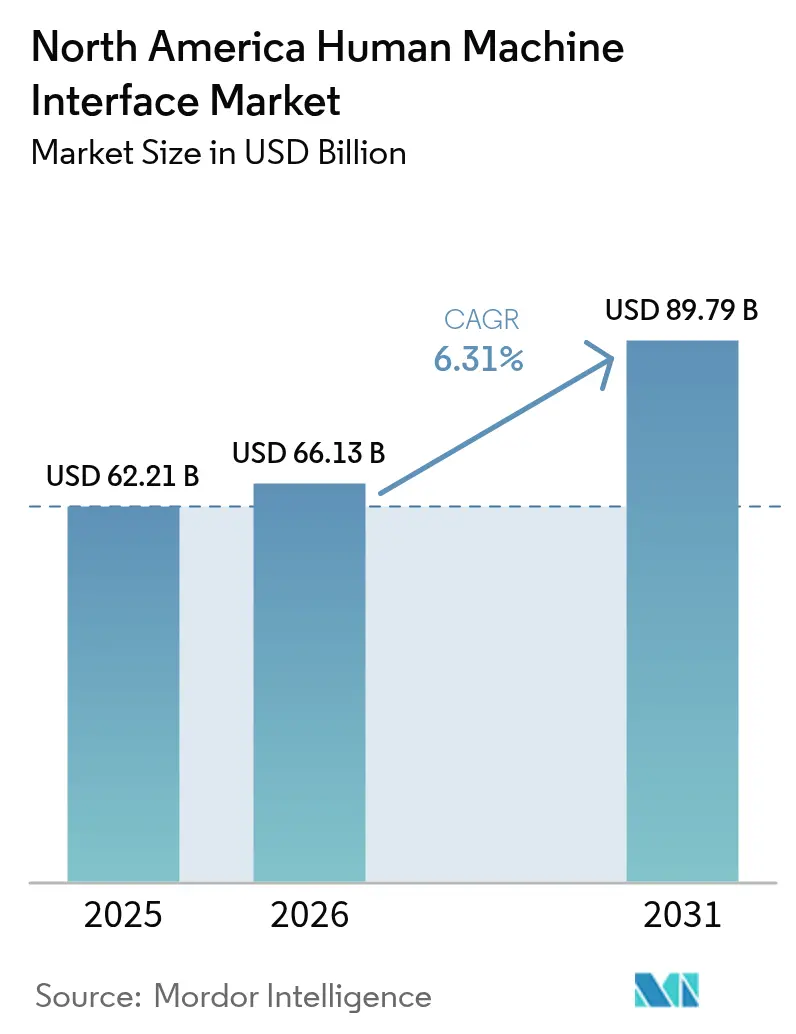

| Base Year Market Size (2025) | USD 62.21 Billion |

| Market Size (2026) | USD 66.13 Billion |

| Market Size (2031) | USD 89.79 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Human Machine Interface Market Analysis by Mordor Intelligence

The North America human machine interface market size in 2026 is estimated at USD 66.13 billion, growing from 2025 value of USD 62.21 billion with 2031 projections showing USD 89.79 billion, growing at 6.31% CAGR over 2026-2031. Demand scales with the region’s push toward Industry 4.0, private 5G roll-outs, and stricter OSHA–NIST cyber-physical rules that force manufacturers to replace legacy operator panels with secure, data-centric systems. Modern plants now expect an HMI to stream real-time production data into cloud analytics rather than simply relay machine status, and this expectation is changing procurement strategies across discrete and process industries. Semiconductor shortages and the lack of OT-IT integration talent form a near-term drag, yet fresh capacity build-outs—especially EV battery gigafactories—continue to anchor multi-year project pipelines. Consequently, vendors that blend hardware, software, and cybersecurity functions occupy a premium competitive position in the North America human machine interface market.

Key Report Takeaways

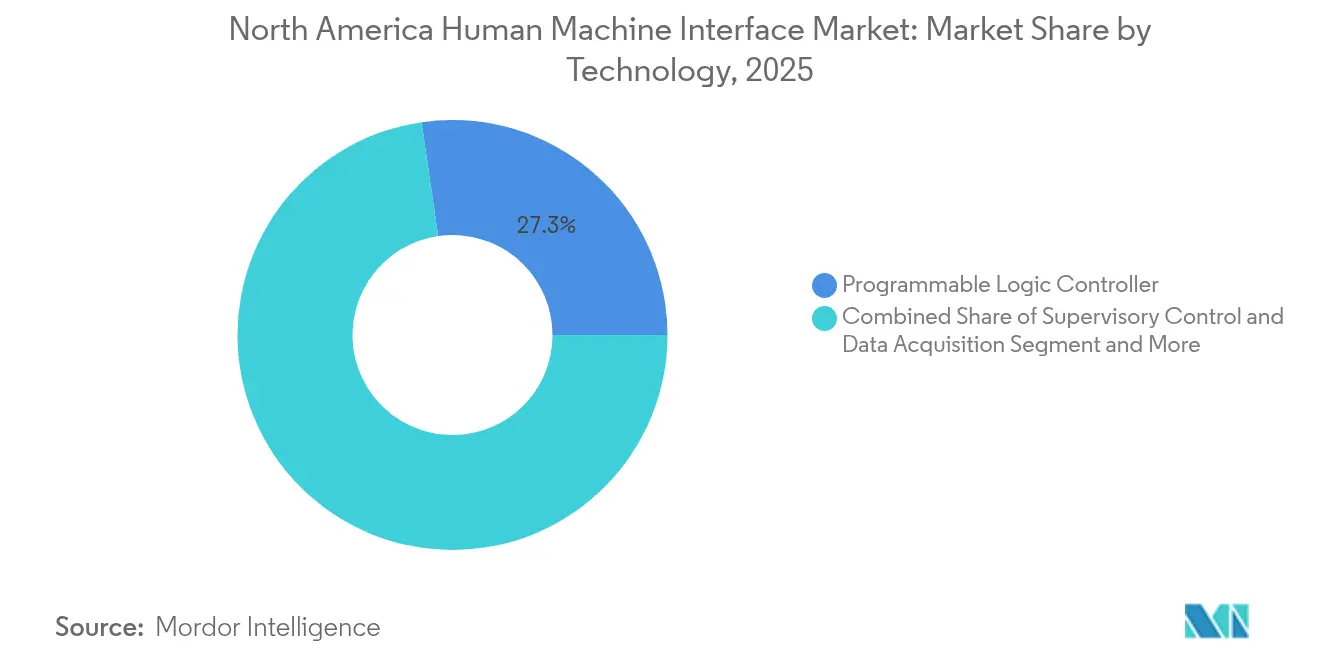

- By technology, Programmable Logic Controllers (PLCs) led with 27.30% of the North America human machine interface market share in 2025, while Manufacturing Execution Systems (MES) are projected to expand at a 9.12% CAGR to 2031.

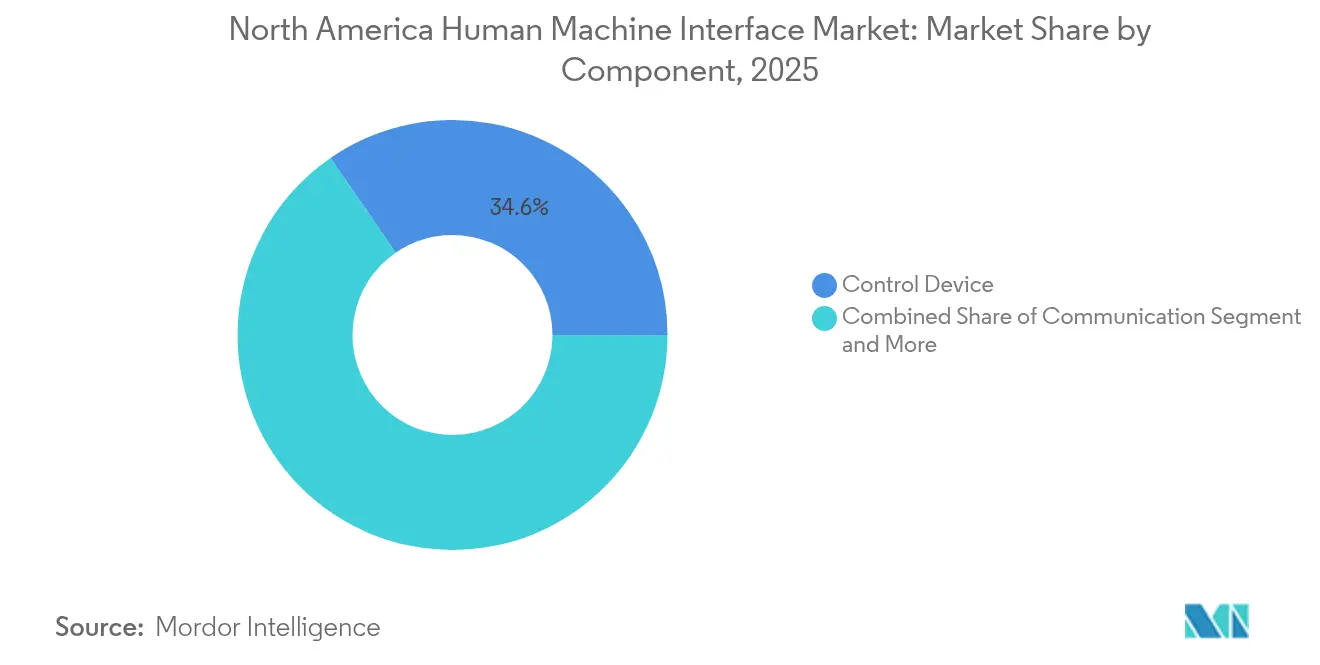

- By component, Control Devices accounted for 34.60% share of the North America human machine interface market size in 2025; Machine Vision Systems are growing at a 9.96% CAGR through 2031.

- By interface type, Touch-Screen Operator Panels commanded 25.50% share of the North America human machine interface market in 2025, whereas Mobile and Wearable HMIs are forecast to rise at a 8.97% CAGR.

- By end-user, automotive manufacturing held 25.80% of the North America human machine interface market share in 2025; pharmaceutical plants record the fastest CAGR at 8.71% up to 2031.

- By geography, the United States dominated with 80.40% share of the North America human machine interface market size in 2025, while Canada is set to grow at 7.22% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Human Machine Interface Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing Industry 4.0 adoption in U.S. discrete manufacturing driving demand for connected machine interfaces | +1.8% | United States, with spillover to Canadian automotive sector | Medium term (2-4 years) |

| OSHA and NIST cyber-physical compliance mandates boosting HMI upgrades | +1.2% | North America-wide, concentrated in regulated industries | Short term (≤ 2 years) |

| Retrofitting ageing process plants in U.S. Gulf Coast and Alberta oil sands | +0.9% | Gulf Coast Texas/Louisiana, Alberta oil sands region | Long term (≥ 4 years) |

| Deployment of private 5G networks enabling real-time HMI in smart factories | +1.1% | U.S. manufacturing corridors, Ontario industrial zones | Medium term (2-4 years) |

| Multilingual workforce requirements accelerating bilingual HMI panel adoption | +0.4% | Border states, Quebec, multicultural manufacturing hubs | Short term (≤ 2 years) |

| Expansion of North American EV battery gigafactories requiring advanced interface solutions | +1.0% | Michigan, Tennessee, Georgia, Ontario battery corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Industry 4.0 adoption in U.S. discrete manufacturing driving demand for connected machine interfaces

Plant managers in automotive, electronics, and packaged-goods lines now pursue single data fabric strategies that unify PLC logic, MES transactions, and quality analytics under one HMI umbrella. Siemens’ Industrial Copilot, honored with the 2025 Hermes Award, embeds generative AI that cuts engineering hours while boosting code robustness.[1]Siemens AG, “Industrial Copilot Wins Hermes Award,” siemens.com Ford integrated the software-defined SIMATIC Automation Workstation across Louisville assembly to reconfigure production cells within hours, not days. Similar deployments across mid-sized contract manufacturers indicate a structural shift from fixed-function panels to scalable, software-centric HMIs that support predictive maintenance and energy optimization. These upgrades directly enlarge the addressable base of the North America human machine interface market.

OSHA and NIST cyber-physical compliance mandates boosting HMI upgrades

Regulators now treat unsecured HMIs as safety risks. OSHA citations reference NIST SP 800-82 controls, compelling pharmaceutical and chemical operators to harden remote-access points and implement multi-factor authentication.[2]National Institute of Standards and Technology, “Framework for Cyber-Physical Systems,” nist.gov CISA advisories in 2024 flagged SQL injection flaws in widely deployed operator stations, pushing firms to retire unsupported versions. The cost of non-compliance dwarfs modernization budgets, shunting capital toward encrypted protocols and role-based access. Vendors that pre-certify panels to IEC 62443 standards report above-market growth across the North America human machine interface market.

Retrofitting aging process plants in U.S. Gulf Coast and Alberta oil sands

Energy majors view advanced HMIs as linchpins for unmanned operations on corrosive and extreme-temperature assets. ExxonMobil’s USD 230 million Baton Rouge upgrade replaced relay logic with open-process architecture capable of digital twin integration.[3]ExxonMobil Corporation, “Baton Rouge Refinery Modernization,” corporate.exxonmobil.com Imperial Oil’s Kearl mine in Alberta adopted autonomous haulage monitored through ruggedized, explosion-proof panels, achieving production records while trimming headcount. With over 50 refineries older than 40 years along the Gulf Coast, retrofit momentum guarantees long-cycle demand for high-specification HMIs.

Deployment of private 5G networks enabling real-time HMI in smart factories

Ericsson’s mid-band 5G deployments deliver sub-10 millisecond latency, letting mobile tablets and AR headsets issue safety-critical commands once reserved for hard-wired terminals. Aerospace integrators now run torque-tool verification and vision inspection directly over 5G links. The resulting flexibility accelerates changeovers and supports labor-augmentation schemes, widening the customer base for mobile HMI software subscriptions and stimulating further growth of the North America human machine interface market.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Persistent vulnerabilities in legacy HMI communication protocols raising cybersecurity concerns | -1.3% | North America-wide, acute in critical infrastructure | Short term (≤ 2 years) |

| Acute shortage of OT-IT integration talent inflating implementation timelines | -0.8% | United States manufacturing belt, Canadian industrial centers | Medium term (2-4 years) |

| Semiconductor supply disruptions causing controller and display lead-time spikes | -0.7% | Global impact, concentrated in North American assembly operations | Short term (≤ 2 years) |

| Stringent FDA re-validation costs discouraging frequent upgrades in pharma plants | -0.4% | U.S. pharmaceutical manufacturing corridors, Canadian biotech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent vulnerabilities in legacy HMI communication protocols

CISA’s 2025 catalog highlights modbus-TCP and DNP3 weaknesses that permit remote code execution on unpatched terminals, intensifying board-level scrutiny of plant OT risk. Because many North American facilities still rely on air-gap illusions, each newly disclosed exploit accelerates plans to replace aging panels. However, complexity of brown-field wiring, combined with the need to stage line outages, slows full migration.

Acute shortage of OT-IT integration talent inflating implementation timelines

Consultancies report that HMI projects now quote average lead times five months longer than in 2023 because certified engineers are scarce. Sourceability forecasts a 67,000-engineer shortfall in U.S. semiconductor and automation disciplines by 2030. Smaller tier-2 suppliers must queue for systems integrators, occasionally deferring upgrades until next capital-expenditure window, dragging the CAGR of the North America human machine interface market below its potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Shift from controller logic to holistic intelligence

The North America human machine interface market size for Programmable Logic Controllers stood at USD 16.98 billion in 2025 and retained a 27.30% share of total spending. MES platforms, although smaller, will grow 9.12% annually to 2031, reflecting a pivot toward closed-loop quality and real-time costing. Vendors integrate motion, safety, and edge analytics into new PLC generations, compressing cabinet footprint while expanding data throughput to enterprise clouds. Early adopters in electronics witness scrap reductions above 12% after unifying PLC tags with MES dashboards. While SCADA and DCS solutions maintain strongholds in process industries, cloud-hosted HMI software outsells perpetual licenses as CFOs prioritize subscription models that convert capex to opex. This technology convergence keeps technologies interoperating rather than cannibalizing, sustaining incremental growth in every layer of the North America human machine interface market.

A growing subset of projects now marries PLM data with operator interfaces so that engineering changes flow instantly to the shop floor. Automotive OEMs cite reductions of two days per engineering change roll-out when CAD revisions automatically populate HMI work instructions. Open-source OPC UA over TSN gains traction as common protocol, trimming custom middleware costs by 18%. Collectively, these advances underline how manufacturers judge the North America human machine interface market not simply on panel counts but on the capacity to convert data into actionable financial outcomes.

By Interface Type: Mobility gains momentum alongside resilient touch panels

Touch-screen panels preserved 25.50% of the North America human machine interface market in 2025 due to their proven IP-65 housings and universal spare-parts ecosystems. Yet mobile and wearable interfaces will compound 8.97% per year as private 5G matures. Early roll-outs at aerospace assembly plants indicate 30% faster first-piece approvals when inspectors use AR-enabled smart glasses that overlay torque specs and tolerances. Industrial PCs now ship with NVIDIA GPUs, letting vision apps run directly on-device and eliminating separate servers. Keypad models stay relevant in explosive or gloved-hand zones, where tactile affirmations prevent mis-clicks. Voice-controlled HMIs inch forward, although background noise remains a barrier in metal-forming lines.

Hybrid deployments become common: a central panel governs safety interlocks while operators carry tablets for non-critical adjustments. The resulting interface mesh boosts uptime through redundancy; if a panel fails, the line can still be jogged from a certified mobile unit. Such configurations widen procurement scope and elevate the profile of cybersecurity certifications that span device families, reinforcing vendor differentiation across the North America human machine interface market.

By Component: Control devices dominate, vision accelerates analytics

Control devices—spanning industrial PCs, PLC racks, and distributed I/O—captured 34.60% of spending in 2025, mirroring their pivotal role in machinery architecture. Machine vision, however, will outrun every other component at 9.96% CAGR by 2031. Automotive paint shops now rely on AI-trained cameras to flag micron-scale defects, freeing skilled inspectors for higher-value tasks and reducing rework by 15%. Communication modules embracing OPC UA and MQTT grow handsomely as plants pursue plug-and-play sensor fabrics. Collaborative robot makers bundle drag-and-drop HMIs that let technicians teach paths within minutes, democratizing automation for mid-market manufacturers.

Edge compute cards embedded in displays now preprocess vibration or thermal imagery, transmitting only anomalies upstream, which cuts bandwidth consumed by vision data by 40%. Sensor prices fall but volumes surge, leading to terabytes of daily shop-floor data that necessitate user-friendly dashboards. These integrated stacks underscore the expanding definition of an HMI, enlarging the total pie of the North America human machine interface market.

By End-User Industry: Automotive still rules; pharma outpaces all

Automotive plants represented 25.80% of the North America human machine interface market share in 2025, reflecting capital-intensive retooling for EV drivetrains and battery pack assembly. Flexible body shops deploy software-defined HMIs to toggle between internal-combustion and electric variants without shutting welding lines. Meanwhile, pharmaceutical facilities will grow fastest at 8.71% CAGR because FDA’s Computer Software Assurance draft elevates computerized controls to inspection priority number 1. Validation 4.0 guidelines encourage modular, low-code interfaces that shorten re-qualification cycles and support digital batch records.

Oil and gas operators continue modernizing control rooms for pipeline integrity and emissions reporting, adopting redundant, high-brightness panels suitable for 24/7 use. Food and beverage processors increase automation to offset labor scarcity and enforce HACCP logging; nearly half of new capex targets robotics paired with hygienic HMIs. Metals and mining companies deploy autonomous drills governed through ruggedized, sunlight-readable displays, cutting downtime from operator fatigue. Each sector articulates different pain points, yet all converge on cybersecurity and data transparency requisites, expanding customer diversity inside the North America human machine interface market.

Geography Analysis

The United States commanded 80.40% of the North America human machine interface market size in 2025, propelled by the country’s dense manufacturing base and stringent safety-cyber regulations that oblige periodic panel replacement. Federal tax incentives under CHIPS and IRA legislation accelerate semiconductor fab and battery cell investments, each specifying open-architecture HMIs to future-proof production lines. Private-sector alliances between telecom operators and automation vendors pioneer 5G campus networks across Illinois, Texas, and South Carolina, enabling latency-free mobile interfaces that raise overall equipment effectiveness.

Canadian demand, while smaller in absolute dollars, will compound at 7.22% annually. Alberta oil-sands projects retrofit control rooms to monitor autonomous haulage fleets where harsh winters require wide-temperature-range displays. Ontario’s auto corridor synchronizes with U.S. Tier-1 supply chains; bilingual touch panels uphold compliance with Canadian language laws and support metric-imperial toggling. Federal manufacturing investment tax credits covering automation assets further sweeten return-on-investment calculations, funneling mid-market firms into the procurement funnel of the North America human machine interface market.

Mexico, although outside the numeric scope of this study, influences supplier logistics and technology spillovers as near-shoring trends shift subassembly operations south. Multinationals operating tri-national plants insist on homogeneous HMIs to maintain operator skills across borders. Consequently, U.S. and Canadian integrators increasingly preload Spanish language packs and remote-access gateways, showcasing how geographic considerations mold product roadmaps even when most revenue still originates north of the Rio Grande.

Regulatory Landscape

North American HMI deployments sit within layered expectations for safety, cybersecurity, and functional safety, and they increasingly reference consensus standards rather than HMI-only prescriptive regulation. In process industries, ISA-101 (Human-Machine Interfaces for Process Automation Systems) is commonly used as a design anchor for usability and situational awareness. OSHA enforcement actions and interpretations can also pull cybersecurity and remote-access hardening into safety-critical expectations when HMIs are treated as part of industrial control systems.

Standardization updates are tightening compliance requirements for HMI-adjacent automation cells. IEC published IEC 63303:2024 to define general structures and functions for HMIs in process automation systems, with a stability date noted for 2026. North American robotics safety updates add requirements that cascade into HMI design for interlocks, safeguarding, and operator prompts, including ANSI/A3 R15.06-2025 and CSA Z434-2026 (adopting ISO 10218-1:2025 and ISO 10218-2:2025 with Canadian deviations). On the procurement side, evolving US federal policy discussions around advanced robotics, including Senate bill S. 3275 on contracting restrictions for certain humanoid-robot suppliers, can shape approved vendor lists and the cybersecurity documentation expected for control-room and operator-station deployments.

Value Chain Analysis

The HMI value chain in North America begins with component and platform inputs, including industrial displays, computing hardware, communication modules, and PLC/DCS/SCADA runtime layers. It then moves into OEM panel builders and automation majors that package terminals together with control software suites. Systems integrators and OT service providers have an outsized role in brownfield environments, where protocol bridging, alarm rationalization, and validation documentation are required, especially for regulated end users such as pharmaceuticals and chemicals, where HMI software changes can trigger re-qualification.

Downstream, distribution and lifecycle services, including installation, cybersecurity patching, remote access governance, and spare-part logistics, increasingly influence total cost of ownership. The evidence from the period points to a software and services tilt: Emerson has emphasized modernizing HMIs around alarm flood reduction and ISA-101-aligned operator performance, and Honeywell introduced Experion Cognition (announced June 2026, with commercial availability scheduled for Q3 2026). The AI-enabled platform is aimed at optimizing production and safety, reinforcing that the value pool is shifting toward software-defined capabilities on top of installed control infrastructure. Key constraints in the chain include OT-IT integration skill gaps and the friction of legacy systems that lack modern API interfaces, which can extend commissioning cycles and increase reliance on specialist partners.

Competitive Landscape

The vendor arena tilts toward moderate consolidation. Siemens, Rockwell Automation, and ABB jointly cover a majority of brown-field installed bases, yet fast-growing software pure-plays erode hardware lock-in. Siemens’ Industrial Copilot stitches large-language-model assistance into code editors, trimming PLC deployment times by 30%. Rockwell folds anomaly-detection AI into FactoryTalk Optix, while ABB leverages its 2025 wiring accessory acquisition to cross-sell building-automation HMIs into industrial campuses.

Start-ups like RealWear and PTC Vuforia anchor AR-based field-service niches, integrating secure WebRTC streams to OT dashboards. Partnerships between cybersecurity firms and automation majors, exemplified by Siemens and ServiceNow’s 2024 alliance, bundle vulnerability management with panel configuration, easing audit compliance. Vendors able to supply UL-listed, edge-enabled panels with pre-integrated zero-trust frameworks command higher margins in the North America human machine interface market.

Pricing remains value-based rather than cost-based; a rugged panel certified to IECEx can list at multiples of a standard IP-54 device. Nevertheless, white-box PC suppliers inch upward, tempting price-sensitive buyers with commodity hardware layered by third-party SCADA. Overall, differentiation now orbits software extensibility, AI co-pilots, and cybersecurity accreditation more than screen resolution or CPU speed.

North America Human Machine Interface Industry Leaders

ABB

Schneider Electric Ltd

Siemens

Rockwell Automation, Inc.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Modernization programs that avoid full rip-and-replace create a whitespace for vendors that can layer secure, data-centric HMIs onto legacy PLC/DCS/SCADA estates while meeting audit demands. There is also visible buyer funding for modernization at scale: Schneider Electric announced Industrial Automation Modernization as a Service in June 2026, built on EcoStruxure Automation Expert with HPE SimpliVity infrastructure. The offering positions subscription-led upgrades for plants that need faster refresh cycles and standardized cyber controls across sites.

Localization of manufacturing capacity and supply resilience further expands room for North American HMI hardware and industrial-PC ecosystems, particularly alongside reindustrialization and new-facility buildouts. In April 2026, Rockwell Automation filed zoning applications for a new 1 million-square-foot manufacturing facility in New Berlin, Wisconsin, as part of a USD 2 billion investment plan. Siemens also highlighted a USD 1 billion cumulative milestone in US manufacturing investments over five years (May 2026), alongside a completed Siemens Canada facility expansion in Drummondville, Quebec (June 2026, CAD 14 million, +40,000 square feet). These steps support opportunities for shorter lead times and region-for-region product variants, including bilingual HMI requirements in Canada, and they reinforce tighter coupling between HMI software, edge compute, and cybersecurity services tied to Industry 4.0 and private 5G factory programs.

Recent Industry Developments

- July 2026: ABB made a strategic minority investment in Gridcog to scale digital modeling for distributed energy resources and industrial microgrids. The move connects ABBs automation stack with energy-optimization software workflows that increasingly surface through operator dashboards. It supports HMI demand that spans production control plus on-site power, emissions, and microgrid operations.

- June 2026: Schneider Electric announced Industrial Automation Modernization as a Service in partnership with HPE, combining EcoStruxure Automation Expert with HPE SimpliVity infrastructure. This commercial packaging shifts plant upgrades toward standardized, repeatable modernization projects rather than bespoke migrations. It also reinforces subscription and lifecycle-service models for HMI and control environments across multi-site manufacturers.

- February 2024: Rockwell Automation released FactoryTalk Optix as part of its software-defined HMI approach, targeting more flexible visualization and modern application workflows. The launch broadened the addressable base beyond traditional panel HMIs by aligning HMI development with contemporary software practices. It also strengthened Rockwells ability to connect visualization with analytics and OT cybersecurity within the FactoryTalk ecosystem.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the North America human machine interface (HMI) market is defined as revenues earned from HMI hardware, HMI software, and related services that enable people to monitor, control, and visualize machines and industrial processes across North America.

Scope exclusions: We exclude general-purpose consumer UI software and devices that are not used for industrial or enterprise equipment monitoring and control.

Segmentation Overview

- By Technology

- Programmable Logic Controller (PLC)

- Supervisory Control and Data Acquisition (SCADA)

- Enterprise Resource Planning (ERP)

- Distributed Control System (DCS)

- Human Machine Interface (HMI) Software

- Product Lifecycle Management (PLM)

- Manufacturing Execution System (MES)

- Other Technologies

- By Interface Type

- Touch-Screen Operator Panels

- Industrial PCs (Panel and Box)

- Keypad / Function-Key HMIs

- Mobile and Wearable HMIs

- Voice- and AR-Enabled HMIs

- By Component

- Communication Segment

- Control Device

- Machine Vision Systems

- Robotics

- Sensors

- Other Components

- By End-User Industry

- Automotive

- Oil and Gas

- Chemical and Petrochemical

- Pharmaceutical

- Food and Beverage

- Metals and Mining

- Other Industries

- By Country

- United States

- Canada

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the foundation for the model and to map what is actually being counted as HMI in North America, before assumptions were taken into interviews. We referred to public and official sources such as US Census Bureau datasets, US International Trade Commission trade statistics, Bureau of Labor Statistics series, National Institute of Standards and Technology publications, and IEEE journal papers to understand production, industrial activity, and technology direction.

To translate those signals into a market number, we also reviewed company annual reports and investor presentations, product catalogs, and industry association websites to identify offering mix and adoption cues. In parallel, we used paid subscriptions for company financials and intelligence, plus patent databases and shipment-level trade datasets where relevant, so revenue splits and import trends could be cross-checked consistently. These desk research sources are illustrative only, and other public references were also used to collect data, validate assumptions, and clarify points that were not straightforward from primary sources.

Primary Interviews and Surveys

Primary work was used to validate the offering scope, typical pricing logic, and the split of demand across end-user industries in the United States and Canada. We spoke with a mix of HMI ecosystem participants, including product and sales leaders, system integration and engineering roles, and operations managers on the buyer side, so desk assumptions could be corrected where buying patterns differed in practice.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | |

| Mid tier: 49% | Functional/Unit leaders: 30% | |

| Smaller Players: 20% | Managers: 56% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where industrial production signals and automation investment proxies are used to reconstruct the addressable demand pool for HMI across North America, then the spend is split into hardware, software, and services using observed mix patterns. The totals are corroborated with selective bottom-up approximations, such as sampled vendor revenue disclosures, channel checks for typical unit volumes, and average selling price ranges by HMI class, with adjustments made when the two views diverge.

A few practical model inputs include manufacturing output momentum, automation and control system adoption in plants, the installed base refresh cycle for operator interfaces, typical pricing differences between basic and advanced HMI setups, and the rate of migration toward connected or cloud-enabled configurations where applicable. For forecasting, scenario analysis is used so growth can flex with industrial capex cycles, supply chain normalization, and end-user backlog conditions. The final path is anchored to what interviewees view as realistic for the next five years. When bottom-up evidence is incomplete, gaps are handled through conservative interpolation using nearest comparable product groups and country-level demand indicators, and the assumptions are re-checked in follow-up calls.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, followed by variance checks at the country and offering level so outliers are not carried into the final tables. If a number implies an unusual price jump, an adoption shift that does not align with observed plant rollouts, or a growth rate that conflicts with industrial indicators, the inputs are revisited, and respondents are re-contacted when the change needs confirmation.

Before sign-off, the model goes through a multi-step internal review so calculations, unit consistency, and currency timing are checked by another analyst. Reports are refreshed annually, with interim updates when material events occur that can move demand or pricing. Right before delivery, a fresh pass is completed to ensure the latest public data releases and news signals are reflected.

Mordor Intelligence's North America Human Machine Interface Market Market Size Measured Against Other Published Estimates

Published market sizes for North America HMI often differ because each publisher draws the line differently on what counts as HMI revenue, and because the base year, currency timing, and pricing progression methods do not match. Differences also show up when one estimate leans heavily on one end-use industry, while another spreads demand across a wider set of industrial and enterprise applications.

The main gap comes from scope mixing, where Mordor Intelligence counts HMI as a combined hardware, software, and services revenue pool in North America, while some other estimates narrow the definition to only HMI software or only industrial control screens, which pushes totals down or up depending on what gets bundled.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 66.13 B (2026) | |

| Trade Publisher A | USD 2.30 B (2024) | Uses an HMI software-only scope, with a longer forecast window, so hardware and services revenues that are material in North America are not captured in the headline number. |

| Research Firm B | USD 62.21 B (2025) | Pins the estimate to a different base year and applies a slightly different growth window, which can shift totals when industrial capex and pricing assumptions are rolled forward. |

The spread in the table is largely explained by what gets included and by timing choices, rather than by a dispute that the category is expanding. By keeping the scope rules explicit and tying inputs to observable demand signals, the final number stays traceable to clear steps that can be repeated when new data is released.

Key Questions Answered in the Report

What is the current value of the North America human machine interface market?

The market stands at USD 66.13 billion in 2026 and is forecast to reach USD 89.79 billion by 2031.

Which technology segment is growing fastest in the North America human machine interface industry?

Manufacturing Execution Systems lead growth at a 9.12% CAGR through 2031.

How do federal regulations influence HMI investments?

OSHA and NIST cyber-physical rules mandate secure, updated panels, driving accelerated replacement cycles.

Why are private 5G networks important for HMI adoption?

They deliver ultra-low latency that lets mobile and wearable HMIs perform real-time control tasks once limited to wired panels.

Which end-user industry is expected to outpace others by 2031?

Pharmaceutical manufacturing, projected to expand at an 8.71% CAGR due to FDA Validation 4.0 requirements.

What limits faster growth of the North America human machine interface market?

Key restraints include legacy protocol vulnerabilities, a shortage of OT-IT engineers, and semiconductor supply disruptions.

Page last updated on: