Social Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.4 Billion |

| Market Size (2031) | USD 40.23 Billion |

| Growth Rate (2026 - 2031) | 31.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Social Robots Market Analysis by Mordor Intelligence

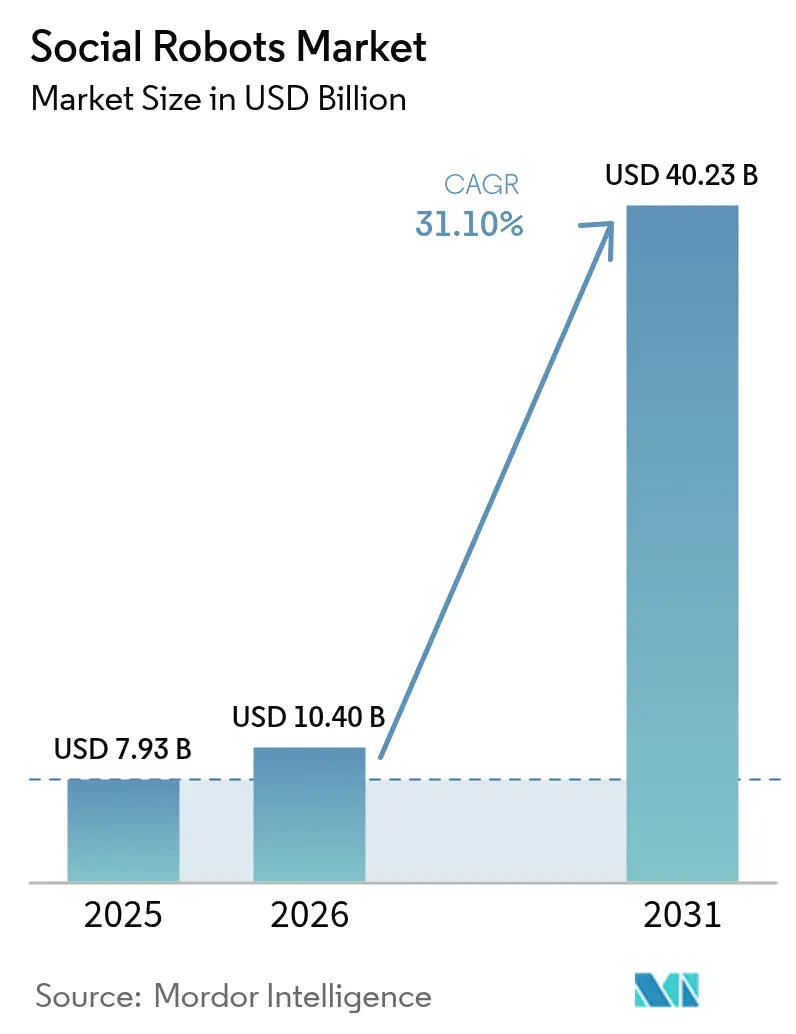

The social robots market size is expected to grow from USD 7.93 billion in 2025 to USD 10.4 billion in 2026 and is forecast to reach USD 40.23 billion by 2031 at 31.1% CAGR over 2026-2031. Steep gains stem from the pairing of large-language-model (LLM) software layers with ever-cheaper sensing and actuation hardware, which together make empathetic, conversational machines commercially viable. Institutional buyers in elder-care, hospitality, and education are choosing turnkey robot-as-a-service contracts that flatten upfront costs and shorten payback periods. Rapid progress in multimodal sentiment analysis enables robots to read facial micro-expressions and voice tone, improving therapeutic outcomes in dementia, autism, and post-acute rehabilitation. Companies are redirecting R&D budgets from form-factor innovation to software frameworks so that a single hardware platform can serve multiple use cases through downloadable skill sets. Large public-sector procurement schemes in Japan, France, and several U.S. states add further momentum, widening the addressable base beyond early adopters.

Key Report Takeaways

- By product type, humanoid robots led with 48.30% revenue share of the social robots market in 2025, while animal-like and companion robots are projected to expand at a 33.55% CAGR through 2031.

- By component, hardware accounted for 57.10% of the social robots market size in 2025; software is forecast to record the fastest growth at 33.08% CAGR to 2031.

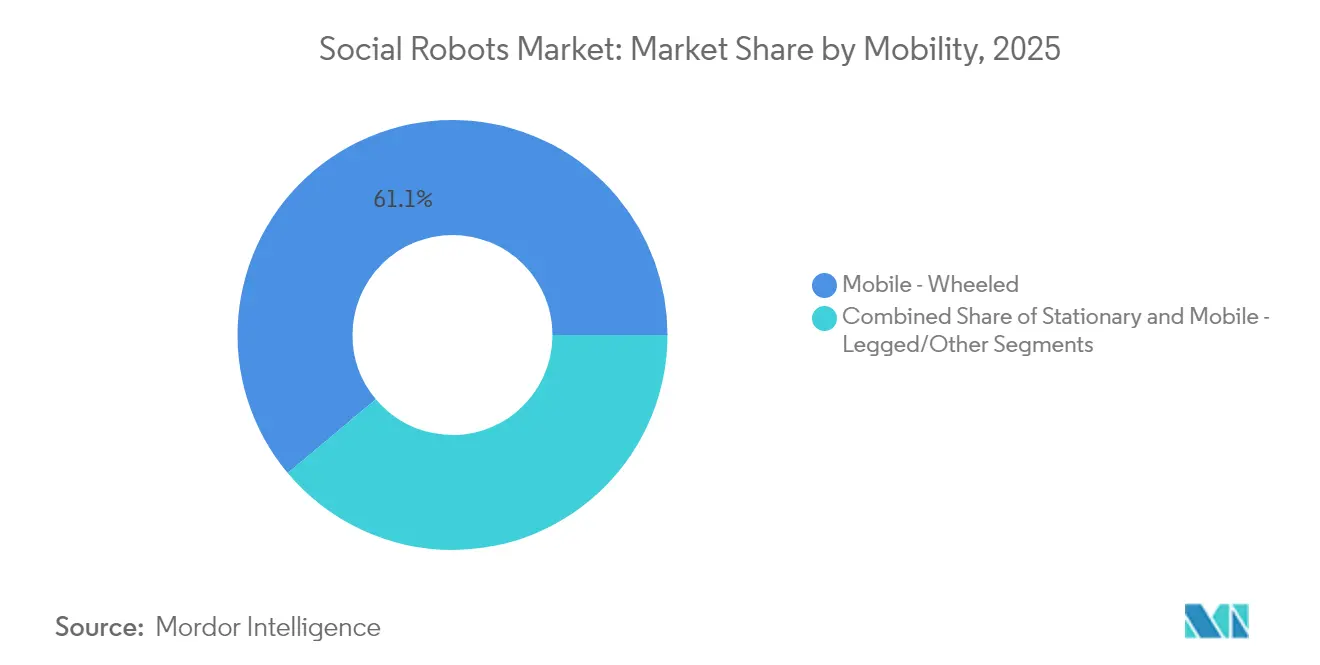

- By mobility, mobile-wheeled platforms held 61.10% share of the social robots market size in 2025, whereas mobile-legged and other advanced solutions are predicted to rise at a 33.30% CAGR.

- By end-user vertical, healthcare commanded 37.85% of the social robots market share in 2025; retail and hospitality applications are advancing at a 33.95% CAGR through 2031.

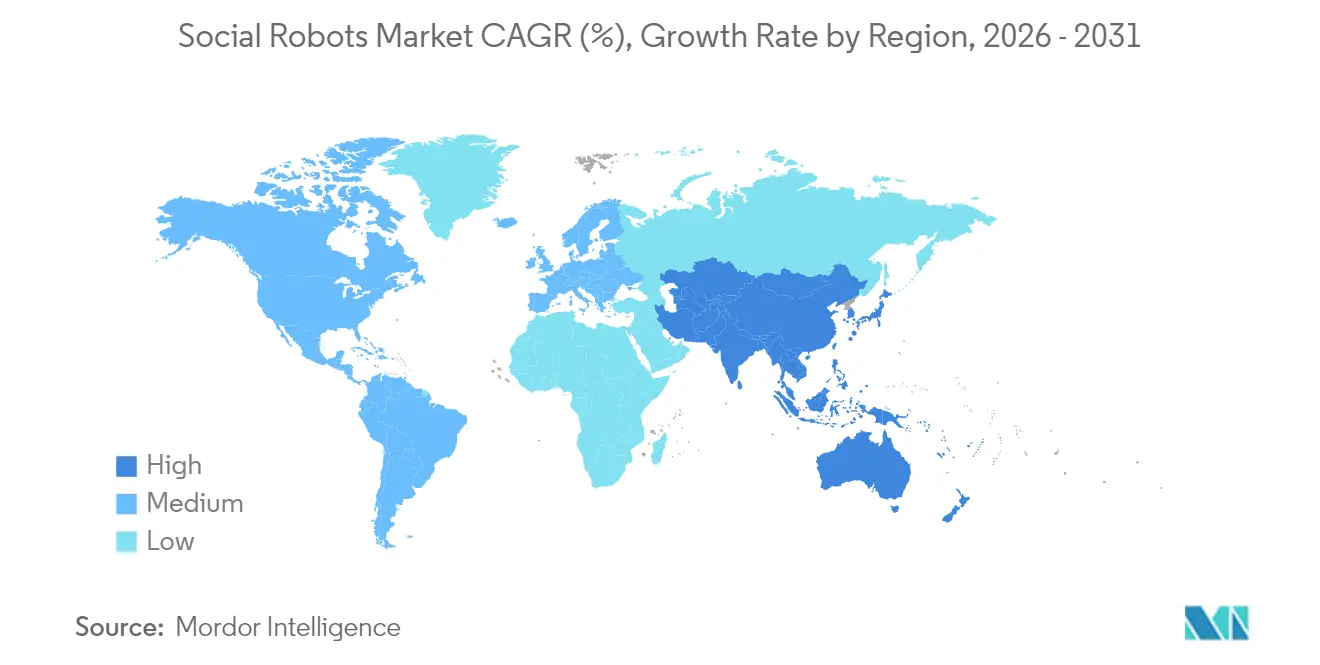

- By geography, North America captured 38.20% share of the social robots market in 2025; Asia-Pacific is the fastest-growing region, progressing at a 33.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Social Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI and NLP breakthroughs | +8.2% | Global, early uptake in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising elder-care demand | +7.8% | Japan, Germany, South Korea | Long term (≥ 4 years) |

| Service-sector labor shortages | +6.4% | North America, Europe, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Government innovation grants | +4.1% | Asia-Pacific, North America, selective EU states | Medium term (2-4 years) |

| Mental-health therapy integration | +3.7% | North America, Europe, emerging urban Asia-Pacific | Medium term (2-4 years) |

| Corporate ESG spending | +2.3% | Developed markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating AI and NLP Breakthroughs Enhancing Human-Robot Interaction

Transformer-based language models now sit on-device or on secure edge servers, allowing sub-400 millisecond response times that make conversation feel fluid and spontaneous. Multi-modal fusion engines combine verbal content with facial-action-coding data to gauge user sentiment, driving context-appropriate gestures, lighting cues, or posture adjustments. Field pilots of Intuition Robotics’ ElliQ platform average more than 30 daily interactions per user, demonstrating sustained engagement in older-adult populations.[1]Intuition Robotics, “The Impact of the State-Funded Program on Older New Yorkers’ Quality of Life,” intuitionrobotics.com Software-defined behaviour also slashes localization costs because new languages can be added through cloud-deployed speech-to-text modules rather than hardware swaps. These capabilities enlarge the social robots market by unlocking billable features such as real-time emotional coaching, fall-risk alerts, and family-caregiver dashboards.

Growing Elder-Care Demand Amid Global Ageing Demographics

Japan’s population aged 65 and older reached 36.25 million in 2024.[2]Statistics Bureau of Japan, “Population Estimates Time Series,” stat.go.jp Similar demographic curves unfold across Germany, Italy, and South Korea, stretching human caregiver supply and public health budgets. Government agencies now frame socially assistive robots as core infrastructure for “aging in place” programs that reduce skilled-nursing-facility admissions. A multi-prefecture initiative in Japan offers capital subsidies of up to JPY 500,000 (USD 3,350) per unit for approved elder-care robots, accelerating deployments in residential facilities. Pilot data show 95% of participants report lower loneliness scores after three months of robot companionship. These results reinforce policymakers' confidence and trigger follow-on orders, broadening the social robots market beyond urban centers to rural clinics and home-care networks.

Rising Labor Shortages and Wage Inflation in Service Sectors

Post-pandemic attrition pushed vacancy rates for U.S. front-of-house hospitality roles above 12%, making automation financially attractive. SoftBank Robotics and Sushimatic now co-package a wheeled greeting robot with sushi-making machinery, cutting guest-wait times during peak hours by 25% and trimming staffing costs.[3]SoftBank Robotics, “SoftBank Robotics Announces Its Partnership with Sushimatic,” softbankrobotics.com Blue Frog Robotics’ Buddy concierge platform at CIC Hospitality’s Aiden hotels manages check-in queues and local recommendations, improving Net Promoter Scores by 14 points over baseline. As wage inflation outpaces productivity, payback periods for subscription robots fall under 24 months, widening uptake among independent restaurants, malls, and amusement venues.

Government Innovation Grants and Subsidies for Robotics Adoption

France’s Ministry of National Education deployed 1,750 Buddy telepresence units under the TED-i program to connect homebound students with classrooms, covering hardware and service fees for three-year terms. U.S. state governments fund companion robots for Medicaid beneficiaries through technology-assistance line items, moving robots from pilot status to reimbursable durable-medical-equipment codes. Similar grant schemes in Singapore and South Korea offer 20%–40% capital rebates for certified social robots. These policies lower adoption risk, generate real-world performance data, and cultivate local integrator networks, collectively lifting demand across the social robots market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Algorithmic bias and ethical risk | –4.6% | Global, strictest in Europe under GDPR | Short term (≤ 2 years) |

| High capital cost vs uncertain ROI | –3.8% | Developing markets worldwide | Medium term (2-4 years) |

| Privacy and data-protection hurdles | –2.7% | Europe, North America, emerging APAC | Short term (≤ 2 years) |

| Limited long-term user engagement | –1.9% | Application-dependent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Algorithmic Bias and Ethical Concerns Surrounding Anthropomorphic Interaction

Regulators note that speech-recognition accuracy can drop when robots engage users with accented English, potentially curbing access to health-advice modules. The European Commission’s AI Act adds risk-classification rules requiring proven safeguards for robots performing social-assistance roles. Developers now embed on-device differential-privacy filters and bias-auditing pipelines, but certification costs lengthen time-to-market. In healthcare settings, informed-consent directives mandate clear disclosures about data use and emotional profiling, leading hospitals to adopt opt-in interaction modes and periodic transparency reports. Compliance overhead tempers near-term expansion, though robust governance models may ultimately boost public trust.

High Capital Cost Versus Uncertain ROI for Small Enterprises

A ready-to-deploy Buddy Pro+ system lists at EUR 3,425.51 (USD 3,664), while multi-site hospitality rollouts add software seats, charging docks, and support packages that double the total cost of ownership. Subscription models help, yet small clinics still weigh monthly fees against unpredictable reimbursement flows. Industry associations now publish ROI calculators covering foot-traffic uplift, reduction in staff overtime, and falls-prevention savings. Transparent metrics will be central to sustained growth, pushing vendors to bundle impact dashboards with every deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Companion Designs Accelerate on Emotional Engagement Advantages

Humanoid platforms hold a 48.30% slice of the social robots market size, but the emotional resonance of pet-like form factors is steering demand toward companion designs growing at a 33.55% CAGR. Interaction studies in dementia care show animal-inspired robots elicit higher sustained attention, reducing agitation episodes by nearly 15%. Vendors exploit this finding by coupling soft-touch skins with adaptive voice-tone modulation, achieving richer affective cues without expensive servo-actuated facial arrays. Telepresence units fill remote-learning and corporate-collaboration niches where visual embodiment, not physical assistance, is the core value. The widening diversity of form factors lets integrators match robot personality to context, supporting wider penetration of the social robots market across customer-experience touchpoints.

Human-centric design shifts also influence procurement criteria. Elder-care administrators report easier resident acceptance of small, non-bipedal robots that pose no fall hazard. This acceptance reduces staff supervision time and drives repeat orders, while the open-source Buddy SDK encourages local app developers to add culturally relevant content. Collectively, these trends favor agile manufacturers whose design pipelines pivot quickly, underscoring how software modularity and cloud-update pathways now outweigh anthropomorphic fidelity when buyers evaluate options in the social robots market.

By Component: Software and Services Outpace Hardware in Value Capture

Hardware continues to generate 57.10% of the social robots market share, yet commoditized sensors and single-board computers compress margins annually. Vendors counter by introducing tiered software licenses that unlock higher-order cognitive skills such as memory-anchored conversations or autonomous navigation in crowded retail aisles. The social robots market size attributable to software subscriptions is forecast to swell rapidly, fueled by recurring revenue from syntax-update packs, language expansions, and specialized therapy modules. Meanwhile, professional services covering workflow mapping, cloud-security audits, and staff training gain prominence as mainstream customers require turnkey integration.

The migration resembles past shifts in the smartphone and industrial-robot fields: once standardized hardware stabilizes, differentiation moves to operating-system ecosystems and service wrappers. Pepper for Home 2.0 exemplifies this paradigm, embedding generative-AI chat functions behind safety guardrails to moderate content, then charging users a monthly fee for premium skill packs because software updates deliver visible functionality without physical retrofits, customer lifetime value rises, reinforcing vendor incentives to prioritize AI research over mechanical innovation.

By Mobility: Wheeled Dominance Persists While Legged Platforms Extend Reach

Wheeled robots own 61.10% of the social robots market size because smooth indoor flooring dominates healthcare, education, and retail spaces. These platforms balance energy efficiency with maintenance simplicity, ensuring 99% uptime in multi-shift service environments. Yet legged locomotion is gathering speed at a 33.30% CAGR as torque-dense actuators and real-time balance algorithms mature. Hospitals exploring in-room patient lifts or ward-round accompaniment require stair-climbing ability, an area where legged units excel. Early prototypes demonstrate sub-2-centimeter foot-placement accuracy, meeting safety norms for patient-interactive devices.

Stationary kiosks remain relevant in high-traffic transit hubs where physical mobility adds little value. For example, a fixed Buddy attendant at Paris-Orly Airport answers 600 daily passenger queries with 92% satisfaction ratings. Each mobility archetype, therefore, targets distinct situational needs, but advanced locomotion will broaden total addressable deployments and raise the technological entry bar for new entrants seeking to penetrate the social robots market.

By End-User Vertical: Healthcare Still Leads but Commercial Segments Race Ahead

Healthcare contributes 37.85% of 2025 revenue as insurers approve reimbursements for fall-detection alerts and medication-reminder conversations. Robots help clinicians run cognitive-stimulation sessions, freeing 8–10 minutes per patient per day. However, retail and hospitality deployments are rising at a 33.95% CAGR as managers automate greeting, shelf-stock inquiries, and queue management. A mid-sized supermarket chain in South Korea reported that customer-interaction robots cut wait times by 18% and boosted basket size by 5%, driving chain-wide rollouts.

Educational institutions leverage telepresence variants to include long-term sick students in classroom life, while entertainment venues use interactive dance and trivia features to deepen visitor immersion. Corporate lobbies adopt mobile guides that escort guests to meeting rooms, slashing manual reception workload by 40%. This diversification signals that commercial volumes may soon eclipse medical units, realigning competitive dynamics inside the social robots market.

Geography Analysis

North America controls 38.20% of current revenue thanks to venture-capital depth, state innovation grants, and fast-track FDA pathways for wellness devices. New York’s statewide companionship program recorded an average of 33 daily interactions per senior and a 95% satisfaction rate, prompting other U.S. states to issue similar RFPs. The region’s privacy statutes are less stringent than GDPR, letting vendors iterate software features more rapidly, though HIPAA obligations keep medical-record modules under strict encryption and audit trails. Canada mirrors U.S. demand drivers, with provincial health ministries funding pilot fleets in remote First Nations communities to counter caregiver scarcity.

Asia-Pacific is the growth engine with a 33.78% CAGR. The Tokyo metropolitan government funds caregiver-assistant pilots that bundle robot leases with caregiver-training curricula, aiming to cut institutional staffing gaps by 10% within five years. China’s robotics clusters in Shenzhen and Suzhou deliver cost-optimized components, enabling domestic brands to price units 25% below global averages without compromising AI capabilities. South Korean telecom carriers integrate 5G edge computing into mall and airport robots, offering robot-as-a-service bundles that include data analytics dashboards.

Europe shows steady uptake balanced by a rigorous compliance culture. Hospitals in Germany deploy companion units only after passing ethical committee reviews and data protection impact assessments, extending procurement cycles but ensuring robust governance. France’s TED-i education initiative, the largest publicly funded telepresence rollout to date, validates the cost-effectiveness of remote-presence robots in mainstream schooling. Nordic elder-care systems test mobile-legged robots for winter-terrain home visits, indicating climatic factors also shape regional adoption patterns.

Competitive Landscape

No single vendor holds more than 10% share, leaving the social robots market moderately fragmented. Incumbents such as SoftBank Robotics focus on open-source ROS2 compatibility, inviting independent developers to add hospitality or retail skill sets that widen addressable use cases. Blue Frog Robotics cultivates a partner marketplace where agencies can resell Buddy-based concierge solutions under white-label agreements, expanding geographic reach without direct capital outlay. Intuition Robotics positions itself squarely in healthcare, layering HIPAA-compliant dashboards and predictive analytics modules that generate subscription revenue well after initial installation.

Start-ups that specialize in clinical therapy, speech-language rehabilitation, autism intervention, or post-stroke motor-skills retraining gain traction by securing peer-reviewed evidence and CE marks, raising entry barriers around domain knowledge. Hardware commoditization pressures pure-play manufacturers; success hinges on proprietary AI stacks, developer ecosystems, and service portfolios rather than electromechanical novelty. Strategic alliances between robotics firms and telecom carriers, cloud-service providers, or medical-device channels are multiplying as each participant seeks bundle economics and data-monetization upside.

Social Robots Industry Leaders

SoftBank Robotics Group Corp.

Blue Frog Robotics SAS

Intuition Robotics Ltd.

Furhat Robotics AB

Amy Robotics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Aldebaran Robotics, creator of the widely deployed Pepper and NAO social robots, was placed in receivership, marking a significant consolidation event that creates uncertainty for existing deployments while potentially opening market opportunities for competitors to acquire technology assets or customer relationships.

- April 2025: SoftBank Robotics began public trials of Pepper for Home 2.0 at its Tokyo flagship café, showcasing ChatGPT-powered conversational upgrades and flexible one-month rental plans.

- February 2025: Reuters reported Japan's accelerated deployment of AI-powered caregiving robots to address severe eldercare worker shortages, with government-funded initiatives targeting practical deployment by 2030 and initial unit costs estimated at JPY 10 million (USD 67,000) for advanced humanoid systems.

- January 2025: Intuition Robotics unveiled the ElliQ Caregiver Solution at CES, combining the companion robot with a new monitoring app that enables caregivers to receive AI-driven health updates and behavioral alerts, priced at USD 249.99 enrollment plus USD 59.99 monthly subscription.

Global Social Robots Market Report Scope

The social robots market is segmented by End-user Vertical (Healthcare, Education, Entertainment, Retail, and Other End-user Verticals) and by Geography (North America, Europe, Asia-Pacific, and the Rest of the World). The social robots for the market study are defined as interactive and assistive autonomous mobile robots and remote-controlled robots, majorly aimed at uplifting an individual's engagement/societal capabilities.

The study is structured to include social robots types, such as rehabilitation robots (physical and emotional therapy), elderly and handicapped assistive devices and telecare and telepresence robots, guidance, information, and telepresence robots for commercial and public space applications, robot toys that move, dances, roves about or generally interacts with the environment. Education purposes of social robots include both types of robots, which offers a platform for experimenting with the robot technology and facilitate interactive teaching to humans.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Humanoid Robots |

| Animal-like/Companion Robots |

| Telepresence Robots |

| Other Product Types |

| Hardware |

| Software |

| Services |

| Stationary |

| Mobile – Wheeled |

| Mobile – Legged/Other |

| Healthcare |

| Education |

| Entertainment and Media |

| Retail and Hospitality |

| Corporate and Public Sector |

| Other End-User Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Humanoid Robots | ||

| Animal-like/Companion Robots | |||

| Telepresence Robots | |||

| Other Product Types | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Mobility | Stationary | ||

| Mobile – Wheeled | |||

| Mobile – Legged/Other | |||

| By End-User Vertical | Healthcare | ||

| Education | |||

| Entertainment and Media | |||

| Retail and Hospitality | |||

| Corporate and Public Sector | |||

| Other End-User Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Singapore | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What revenue level does the social robots market reach by 2031?

Published forecasts show the social robots market size climbing to USD 40.23 billion by 2031 at a 31.1% CAGR.

Which region grows fastest in social robot deployments?

Asia-Pacific records the highest CAGR at 33.78% through 2031, propelled by Japan’s aging population and large public subsidies.

Which end-use segment currently generates the largest robot demand?

Healthcare leads with 37.85% of 2025 revenue thanks to wide uptake in elder-care, rehabilitation and mental-health programs.

How are vendors shifting their revenue models?

Providers now emphasize software subscriptions and professional services that add recurring income beyond the initial hardware sale.

What primary barrier slows adoption among small enterprises?

High total cost of ownership versus uncertain ROI remains the strongest deterrent, especially where upfront capital subsidies are absent.

Page last updated on: