Human Recombinant Insulin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

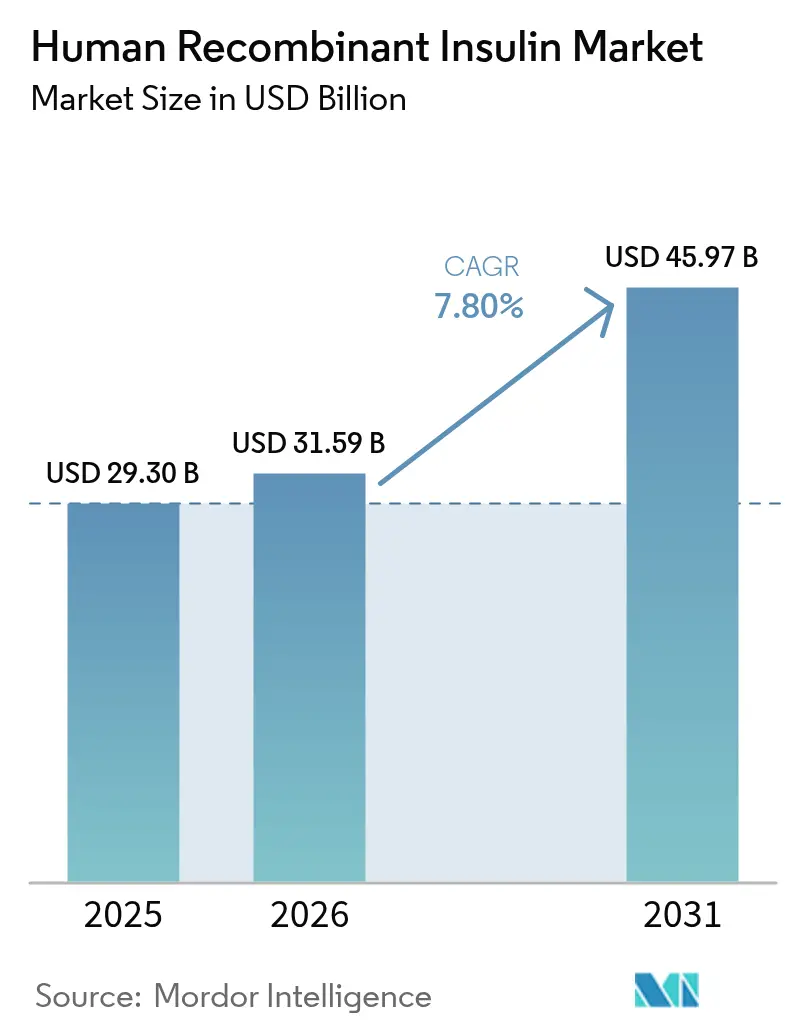

| Market Size (2026) | USD 31.59 Billion |

| Market Size (2031) | USD 45.97 Billion |

| Growth Rate (2026 - 2031) | 7.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Human Recombinant Insulin Market Analysis by Mordor Intelligence

The human recombinant insulin market size in 2026 is estimated at USD 31.59 billion, growing from 2025 value of USD 29.30 billion with 2031 projections showing USD 45.97 billion, growing at 7.80% CAGR over 2026-2031. Uptake continues even as GLP-1 receptor agonists and biosimilars alter therapy choices, because insulin remains the backbone of glycemic control for hundreds of millions of people. Demand growth largely traces back to the accelerating diabetes burden: the World Health Organization reports more than 800 million cases worldwide, quadruple the 1990 base. Capacity expansion has therefore eclipsed discovery research as the primary strategic lever; Novo Nordisk and Eli Lilly together committed over USD 13 billion to U.S. plants slated to enter service before 2030. Meanwhile, widening reimbursement programs, the arrival of new biosimilars, and device innovations such as connected pens and automated pumps keep the competitive field fluid.

Key Report Takeaways

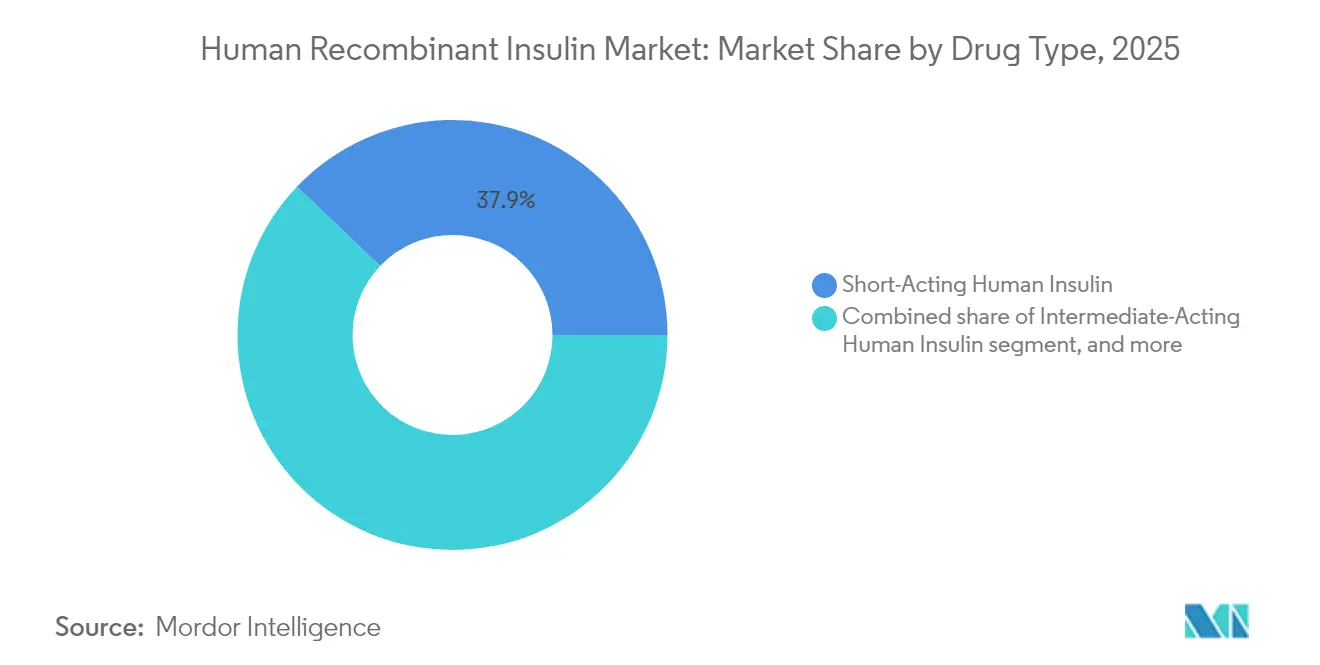

- By product category, Short-Acting Human Insulin led with 37.88% revenue share in 2025, while Premixed Human Insulin is projected to post a 9.22% CAGR to 2031.

- By brand, Humulin held 31.02% of the human recombinant insulin market share in 2025; Insuman is expected to expand at a 9.51% CAGR through 2031.

- By delivery device, Insulin Pens accounted for 42.80% of the human recombinant insulin market size in 2025, whereas Insulin Pumps and Patch Pumps are set to grow at 9.05% CAGR over 2026-2031.

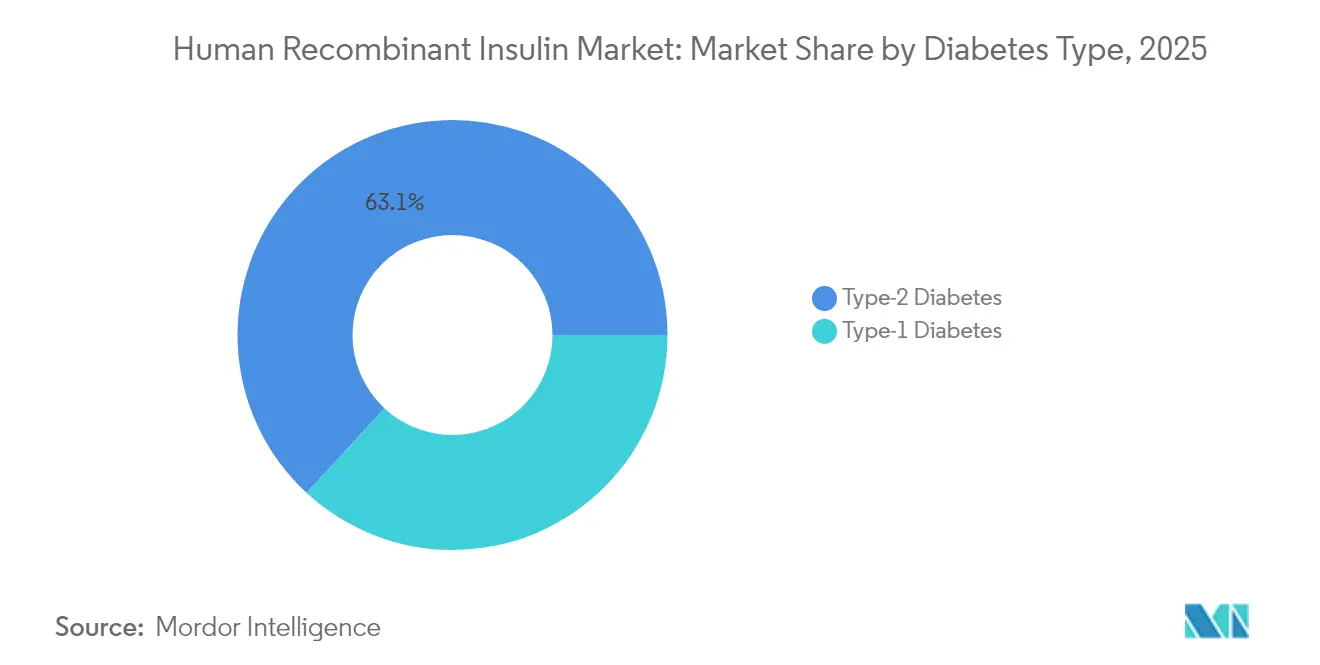

- By diabetes type, Type-2 Diabetes dominated with 63.12% share in 2025, but Type-1 Diabetes therapies are advancing at a 10.24% CAGR.

- By end user, Hospitals and Clinics commanded 50.92% of revenue in 2025, yet Homecare & Self-Administration is forecast to rise at a 10.64% CAGR.

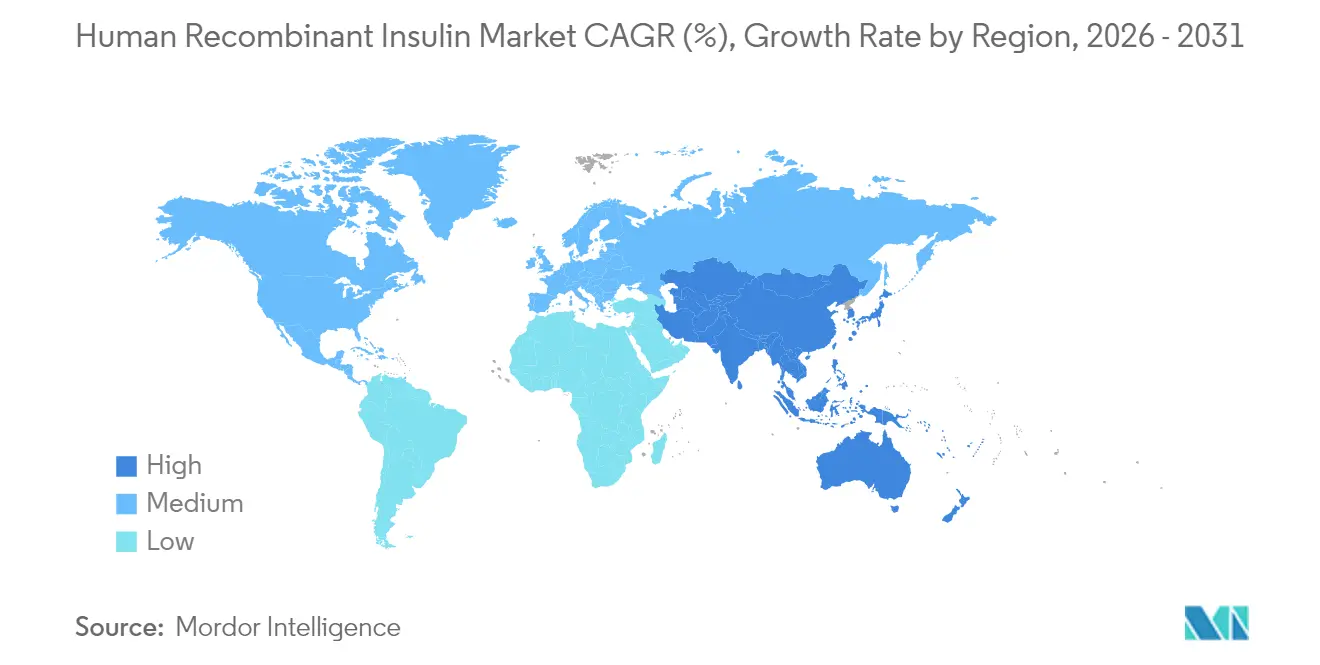

- By geography, North America led with 41.98% share in 2025; Asia-Pacific is the fastest-growing region at 8.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Human Recombinant Insulin Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global diabetes prevalence | +2.1% | Global – highest in Asia-Pacific & Middle East | Long term (≥ 4 years) |

| Expanding national reimbursement programs | +1.8% | North America & EU; expanding to emerging markets | Medium term (2-4 years) |

| Growing adoption of biosimilar insulins | +1.4% | Europe leading, followed by Asia-Pacific | Medium term (2-4 years) |

| Localization of biomanufacturing facilities | +1.2% | Asia-Pacific core; spill-over to MEA & South America | Long term (≥ 4 years) |

| Technological advances in yeast fermentation efficiency | +0.9% | Global manufacturing hubs | Long term (≥ 4 years) |

| Strategic pooled procurement in emerging economies | +0.7% | Africa, South America, select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Diabetes Prevalence

Diabetes incidence has surged to more than 800 million patients, fundamentally stretching health-system capacity and cementing long-duration demand for insulin. Type-2 Diabetes prevalence is rising fastest in urbanizing Asian and Middle-Eastern economies where sedentary lifestyles and dietary shifts converge. As treatment adherence improves, unit volumes climb because insulin therapy typically starts earlier in the disease continuum. The predictable lifetime-use nature of insulin supports the multibillion-dollar factory investments now underway. That manufacturing build-out, in turn, strengthens supply security and positions leaders to meet the expanding patient base.

Expanding National Reimbursement Programs

Affordability initiatives directly translate into higher script volumes. In the United States, the Medicare Part D USD 35 monthly cap takes effect in 2026, neutralizing price as a barrier for millions of seniors. European payers are tightening cost-effectiveness thresholds yet still broaden access by giving biosimilars preferred formulary slots. India’s production-linked incentive scheme, scheduled for 2026, mixes industrial policy with patient-access goals by rewarding local output of diabetes medicines. These actions collectively enlarge the treated population and change brand-choice dynamics inside formularies.

Growing Adoption of Biosimilar Insulins

Regulators now present streamlined approval routes that lower entry costs for biosimilar makers. The U.S. FDA cleared the rapid-acting biosimilar Merilog in February 2025[1]U.S. Food & Drug Administration, “FDA Approves First Rapid-Acting Insulin Biosimilar,” fda.gov, broadening options beyond long-acting glargine copies. Europe remains the reference case: originator glargine list prices fell 21.6% after biosimilar launch, illustrating the deflationary pull. However, entrenched rebate structures still tilt some U.S. purchasing toward premium brands, slowing penetration. Originator firms are countering with dual-price strategies and unbranded biologics to preserve volume even while headline prices drop.

Localization of Biomanufacturing Facilities

COVID-19 supply shocks and geopolitical tensions triggered a pivot to regional production. Sanofi’s USD 1.05 billion insulin complex in Beijing anchors its China strategy. Similar projects dot Southeast Asia and Latin America, reflecting policy incentives to ensure domestic supply. Beyond resilience, localization trims freight costs and can shorten regulatory review when authorities prefer local dossiers. The approach also helps multinational producers secure tender bids that favor in-country value creation.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global price controls | -1.9% | Global – most severe in Europe & emerging markets | Short term (≤ 2 years) |

| Supply-chain vulnerabilities in cold storage | -1.1% | Global; acute in tropical & developing regions | Medium term (2-4 years) |

| High entry barriers due to biologics manufacturing complexity | -0.9% | Global – particularly affects new entrants in Asia-Pacific and MEA | Long term (≥ 4 years) |

| Persistent plasmid DNA production bottlenecks | -0.6% | Global manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Price Controls

Affordability mandates compress margins and can redirect R&D budgets. The Inflation Reduction Act capped U.S. Medicare insulin prices and catalyzed a voluntary 70% list-price cut for Tresiba and Fiasp effective January 2026[2]Drugs.com, “Novo Nordisk Slashes U.S. List Prices for Several Insulins,” drugs.com. Europe now assesses all diabetes therapies against cost-effectiveness benchmarks, putting premium analogues under budget-holder scrutiny. China’s volume-based procurement scheme forces deep discounts for tender winners. Collectively, these policies push manufacturers to find savings in production efficiency and portfolio mix rather than price increases.

Supply Chain Vulnerabilities in Cold Storage

Insulin must move and remain within 2-8 °C. Any deviation can degrade potency, spurring recalls and public-health crises. Outages during South Africa’s 2024 pen shortage illustrate the human toll when temperature-controlled logistics fail. Regulatory agencies now demand real-time temperature monitoring and full audit trails, raising compliance costs. Investment in insulated packaging, data loggers, and regional distribution centers is therefore escalating, especially in tropical markets where last-mile temperatures routinely exceed 30 °C.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Premixed Formulations Extend Convenience

Premixed Human Insulin is the breakout growth story, tracking a 9.22% CAGR for 2026-2031 on the promise of fewer daily injections. Short-Acting formulations still hold the largest slice at 37.88% in 2025, anchoring the human recombinant insulin market through their critical role in mealtime glucose control. Intermediate-Acting products, although clinically valuable, face substitution risk from newer co-formulations that combine basal and bolus action in a single pen.

The human recombinant insulin market responds to patients’ desire for simple regimens, pushing firms to refine biphasic ratios that better mimic physiologic profiles. Capacity allocation also shapes growth: Novo Nordisk’s choice to cease Levemir production frees tanks for higher-value analogues, hinting that legacy segments may contract faster than demand alone would dictate. Weekly basal candidates remain in limbo after a U.S. filing setback, yet China’s nod to insulin icodec displays regional divergence in benefit-risk tolerance.

By Brand: Humulin’s Scale Confronts Agile Challengers

Humulin commanded 31.02% revenue in 2025, reflecting decades-deep formulary entrenchment. Still, Sanofi’s Insuman is on a faster trajectory with a 9.51% CAGR, buoyed by targeted pricing in emerging markets and expanding biosimilar lines. Novolin leverages wide retail distribution but lags on innovation hooks that resonate with payers.

Biosimilar pressure accelerates as patents sunset. Originators adopt “umbrella” strategies: Eli Lilly released an unbranded lispro at half list price to blunt share erosion while protecting rebate flows on the branded SKU. Europe supplies an early look at end-game dynamics, where multiple glargine biosimilars coexist and originator list prices fell yet net prices, after rebates, remain opaque. The human recombinant insulin market thus illustrates how list-price optics diverge from actual transaction economics.

By Delivery Device: Smart Systems Recast Adherence

Insulin Pens held 42.80% share in 2025 thanks to convenience, dose accuracy, and low per-unit cost. However, Insulin Pumps and Patch Pumps post the steepest curve at 9.05% CAGR as algorithm-driven closed-loop systems inch toward mainstream use. Vials and Syringes retain relevance in low-resource settings and among hospitals using centralized infusion pumps for critical care.

Digital integration propels growth. The FDA cleared the first automated dosing system for Type-2 patients in August 2024, broadening pump addressable markets. Patch platforms aim to cut upfront device costs while allowing discreet wear. In parallel, smart pens log dose data and transmit to mobile apps, aiding clinician feedback loops. Manufacturers view hardware as a sticky ecosystem that can bundle proprietary cartridges, reinforcing brand loyalty inside the human recombinant insulin market.

By Diabetes Type: Type-1 Segment Catalyzes Premium Innovation

Type-2 Diabetes dominates volume with 63.12% share, but Type-1 Diabetes will expand faster at 10.24% CAGR because each patient uses higher daily doses and adopts advanced delivery devices first. Technological leaps, such as connected pumps and hybrid closed loops, emerge initially in Type-1 cohorts before cascading to broader groups, anchoring premium ASPs.

Curative approaches inch forward. Vertex’s islet-cell therapy enabled insulin independence in early participants, portending structural demand shifts if scalability hurdles fall. Until then, intensive insulin regimens remain indispensable. Consequently, the human recombinant insulin market sees Type-1 care driving R&D partnerships that marry biologics with wearables, positioning manufacturers for value-based reimbursement that rewards time-in-range metrics.

By End User: Homecare Gains Traction

Hospitals and Clinics absorbed 50.92% of 2025 sales, yet Homecare & Self-Administration registers an anticipated 10.64% CAGR as healthcare shifts to decentralized models. Payers push routine management out of costlier acute settings, and remote-monitoring technologies give clinicians confidence to oversee therapy at a distance.

Device makers capitalize: Tandem Diabetes Care, for example, topped USD 2 billion revenue in 2024 on pump sales married to cloud analytics. At-home use also drives demand for cartridge-based pens that minimize user error. For the human recombinant insulin industry, the migration underscores the strategic need to bundle drug, device, and data services into a cohesive value proposition.

Geography Analysis

North America led with 41.98% of 2025 revenue, fueled by comprehensive insurance coverage and rapid adoption of next-generation delivery systems. The Medicare USD 35 cap, effective 2026, will further secure demand continuity for the human recombinant insulin market. Manufacturers cement local supply: Novo Nordisk’s North Carolina site and Eli Lilly’s Indiana complex collectively add more than 7 million square feet of formulation and fill-finish capacity.

Asia-Pacific is set to deliver the fastest 8.63% CAGR through 2031. China holds the world’s largest diabetic population and has recently accelerated regulatory review timelines for priority drugs. Domestic manufacturing incentives encourage both multinationals and homegrown firms to build plants, tightening cost competition. India’s incentive program will similarly foster local output and could position the country as a regional export hub, deepening the human recombinant insulin market reach.

Europe exhibits a mature yet evolving environment. Health Technology Assessment bodies scrutinize relative cost-effectiveness, giving biosimilars a tailwind and restraining price inflation. EMA guideline updates in 2024 integrated economic considerations into therapy selection, nudging prescribers toward lower-priced options without compromising clinical efficacy. Price-volume contracts remain common, with originator discounting strategies keeping some biosimilar advantages in check.

Middle East & Africa and South America together account for a modest but rising slice. Recent pooled procurement pilots in Africa lowered per-vial costs by double digits, albeit straining supplier margins. Infrastructure investments in refrigerated warehousing are pivotal, as cold-chain lapses currently drive intermittent stock-outs that cap growth potential. Success in these regions will depend on adaptable distribution models and localized value-add services that ensure consistent supply.

Regulatory Landscape

Regulation for human recombinant insulin and follow-on biologics is overseen by agencies including the US FDA and the European Medicines Agency (EMA). Compliance generally centers on comparability packages (PK/PD, immunogenicity, and analytical similarity) and cGMP expectations. In April 2026, the FDA approved Langlara as an interchangeable insulin biosimilar, which underscores how interchangeability designations can affect pharmacy-level substitution where that status is available.

In Europe, EMA continues to publish product-specific biosimilar assessments and scientific guidance for recombinant human insulin and insulin analogues, while also updating manufacturing oversight through revisions to quality and validation expectations. In parallel, the WHO prequalification program for human insulin and its biosimilar pathways, including abridged options for products already authorized by SRAs, provides a practical route for expanding access in low- and middle-income markets where tenders and public procurement often reference WHO-listed products.

Value Chain Analysis

The value chain starts with upstream inputs such as cell banks, media and fermentation feedstocks, buffers, chromatography resins, and single-use or stainless equipment. It then moves through recombinant fermentation (commonly E. coli or yeast), recovery and purification, formulation, and aseptic fill-finish into vials or cartridges for pens. Dominant integrated manufacturers, including Novo Nordisk, Eli Lilly, and Sanofi, concentrate high-capital steps such as fermentation and fill-finish in a limited set of global hubs, while newer entrants and regional suppliers typically participate via localized finishing, technology transfer, and tender-driven supply models.

Downstream, distribution depends on qualified cold-chain partners and compliant storage to maintain 2-8 C conditions from factory to point of care. This places packaging, temperature monitoring, and regional warehousing among the key cost and risk nodes. Regulatory requirements also shape operations across the chain, including ICH Q11-aligned process control expectations and WHO prequalification tools such as the Insulin Master File (IMF) procedure, which was reinforced by WHO final guidance issued in March 2026 and influences how manufacturers structure dossiers for multi-country public procurement.

Competitive Landscape

The three incumbents—Novo Nordisk, Eli Lilly, and Sanofi—control near 90% of global volume, underscoring pronounced concentration in the human recombinant insulin market. Scale affords manufacturing learning-curve advantages and global regulatory muscle. Novo Nordisk leads with 33.7% share across diabetes care and 45.4% within human insulin, helped by deep Nordic production expertise and a broad analog portfolio.

Strategic emphasis has tilted toward brick-and-mortar assets: collective capital outlays surpassed USD 15 billion across 2024-2025 as firms race to lock in fermentation and fill-finish slots. Lilly’s purchase of a Wisconsin injectables facility reflects vertical integration designed to de-risk external supply. Sanofi’s dual sites in Beijing and Frankfurt modernize lines while embedding sustainability features such as closed-loop water systems.

Competitive pressure also stems from biosimilar developers in India and China, whose cost bases undercut Western peers. Companies such as Gan & Lee expand via co-manufacturing deals that offer tender authorities a locally made alternative. Simultaneously, device specialists—Insulet, Tandem, Embecta—forge partnerships with glucose-sensor firms to create full-stack ecosystems that can influence drug choice. Originators thus face a two-front contest: price-oriented biosimilars and technology-driven adjuncts that shift value toward integrated solutions.

Regulatory science is evolving to accommodate this complexity. The FDA’s 2024 release of in-vitro cell-based assays standardizes potency testing, cutting time and animal-study costs for follow-on biologics. Harmonized global standards may accelerate biosimilar approvals and widen therapeutic interchange, intensifying price competition in the human recombinant insulin market.

Human Recombinant Insulin Industry Leaders

Novo Nordisk A/S

Eli Lilly and Company

Sanofi S.A.

Zhuhai United Laboratories Co., Ltd.

Biocon Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Biosimilar and interchangeability momentum creates more room for bids and formulary placements across tender, retail, and institutional channels, where payers target lower net costs and dependable supply while still requiring high confidence in switching. The FDA approval of Langlara as an interchangeable insulin biosimilar in April 2026 indicates a mechanism that can accelerate pharmacy substitution dynamics, giving companies with analytical and manufacturing scale a clearer route to compete beyond traditional long-acting copies.

Localization programs and public procurement contracts are also expanding addressable volumes for manufacturers that can combine capacity with compliant supply chains and local partnerships. In Malaysia, Biocon, through Biocon Sdn. Bhd. and partner Duopharma Biotech, secured Ministry of Health insulin supply contracts valued at over MYR 225 million in June 2026, and the company received EMA approval in July 2026 for a new insulin production line at its Johor facility. Together, these actions point to opportunity for players that can align regional manufacturing footprints with SRA and WHO pathways, while meeting cold-chain performance and tender reliability requirements in emerging markets.

Recent Industry Developments

- April 2026: Novo Nordisk and Eskayef Pharmaceuticals announced the start of local production of modern insulin cartridges (Penfill) in Bangladesh following a technology transfer. The step strengthens regional supply resilience and supports national access goals by shifting part of the supply chain closer to patients.

- May 2025: A major insulin biosimilar program announced a multi-country manufacturing expansion to boost supply availability in Asia, Africa, and Latin America. The move aims to reduce lead times and improve tender competitiveness in LMICs through diversified regional hubs.

- December 2024: Lupin Limited acquired Eli Lillys Huminsulin brand in India, covering insulin human formats including Huminsulin R, NPH, and premixed variants. The transaction reshapes commercial control in a high-volume market and aligns with global manufacturers using portfolio transfers to maintain access while reallocating focus and capacity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of finished human recombinant insulin medicines used to manage diabetes, where the insulin molecule is biologically identical to human insulin and produced using recombinant DNA processes. It includes products sold through retail and hospital channels across major geographies.

Scope exclusions: We exclude insulin analogs (such as long acting and rapid acting analog molecules) and bulk insulin active ingredient sales that are not sold as finished patient medicines.

Segmentation Overview

- By Drug Type

- Short-Acting Human Insulin

- Intermediate-Acting Human Insulin

- Premixed Human Insulin

- By Brand

- Humulin

- Insuman

- Novolin

- Other Brands

- By Delivery Device

- Vials & Syringes

- Insulin Pens (Reusable & Disposable)

- Insulin Pumps & Patch Pumps

- By Diabetes Type

- Type-1 Diabetes

- Type-2 Diabetes

- By End User

- Hospitals & Clinics

- Homecare / Self-Administration

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with public health and utilization signals, and then it is translated into an addressable demand pool for human recombinant insulin only. We used sources such as the International Diabetes Federation for diabetes prevalence, the World Health Organization for treatment guidelines and health system context, and the World Bank and OECD for macro and health expenditure indicators.

To avoid over counting, we reviewed country medicine price and reimbursement references where available, along with regulator and public payer publications that clarify insulin categories and substitution rules. Where customs or trade releases separate insulin products, we used those releases to sanity check usage patterns by therapy type. We also checked peer-reviewed clinical journals for therapy mix context, and used company annual reports and investor materials to confirm portfolio mix and geographic exposure. For parts of the model where public financial splits are limited, we supplemented with paid subscriptions for company financials and intelligence, patent databases, and shipment level import export data to cross check directionally. The sources listed here are illustrative, and many other public documents were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on how prescribing and tendering choices shift between recombinant human insulin and analog options, since that decision changes the real addressable value. We spoke with a mix of manufacturers, distributors, hospital buyers, and diabetes care clinicians across the Americas, EMEA, and APAC. This coverage let us test pricing logic, channel mix assumptions, and access constraints against what buyers and clinicians described.

Insights from these discussions were used to validate assumptions on dose intensity, switching rates, public procurement share, and expected price movement, and then the model was adjusted where consistent gaps showed up across multiple regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | APAC: 49% |

| Mid tier: 55% | Functional/Unit leaders: 28% | EMEA: 32% |

| Smaller Players: 15% | Managers: 58% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool, where the diagnosed diabetes population and insulin treated share are combined with average daily dose and therapy mix. We then translate this into annual units and value by applying region-specific pricing and channel weights. Because insulin is a reimbursed therapy in many markets, we also track public tender share and reference pricing practices, which materially influence average selling price progression over time.

The totals are corroborated with selective bottom-up approximations, including sampled country roll ups of recombinant human insulin consumption, channel checks on hospital versus retail split, and a limited supplier and portfolio mix reconciliation using publicly visible financial disclosures. When a country has sparse pricing visibility, we handle gaps using nearest comparable markets after adjusting for income level, reimbursement intensity, and procurement structure.

Forecasts rely on scenario analysis supported by expert consensus on the same drivers that shape demand and pricing, including diabetes prevalence growth, uptake of analogs versus recombinant human insulin, dosing trends in type 1 and type 2 populations, tender cycle timing, and expected policy shifts around affordability.

Data Validation & Update Cycle

Outputs are checked against independent signals such as diabetes treatment rates, insulin volume movement where visible, and directional pricing changes captured in public payer and regulator updates. If a variance falls outside an expected range, we revisit underlying assumptions, recheck unit conversions, and then recontact relevant respondents when the mismatch is linked to access rules or channel mix shifts.

Before sign-off, a second analyst reviews the model logic and the key inputs. A final pass is then used to confirm that recent regulatory, pricing, or tender events are reflected. The study is refreshed annually, and interim updates are triggered when major policy changes, supply disruptions, or large pricing actions materially alter the market direction.

Mordor Intelligence's Human Recombinant Insulin Market Sizing Compared With Other Published Estimates

Published market sizes for human recombinant insulin can look far apart because the product definition is easy to blur with adjacent insulin categories, and because some estimates embed different price assumptions for public tenders and retail channels. Variation also appears when one publisher uses an older base year or fixes currency conversion to a different timing.

The main gap comes from whether insulin analogs and non-finished insulin sales are included. In Mordor Intelligence's model, only short acting, intermediate acting, and premixed human recombinant insulin finished medicines are counted, with analog molecules and bulk API value left out. Differences also show up when an estimate assumes a uniform global ASP trend, since real price movement is uneven across tender driven markets and commercial pharmacy markets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 31.59 B (2026) | |

| Global Consultancy A | USD 42.30 B (2024) | Uses a broader product lens that includes long acting and rapid acting insulin categories under the same heading, and it anchors to an earlier base year where average prices and mix can be higher in some regions. |

| Industry Publisher B | USD 29.90 B (2024) | Defines the market with a different year and may blend formulation revenue across insulin classes, and it can also apply generalized pricing growth without separating tender heavy markets from retail led markets. |

The spread in the table is mostly explained by what is counted as recombinant human insulin versus adjacent insulin classes, and by the year used for converting volumes into USD value. By tying the sizing to treated population signals, therapy mix, and channel specific pricing behavior, the final number stays traceable to inputs that can be checked and repeated.

Key Questions Answered in the Report

What is the current value of the human recombinant insulin market?

The market is valued at USD 31.59 billion in 2026 and is projected to grow to USD 45.97 billion by 2031 at a 7.80% CAGR.

Which product category leads the human recombinant insulin market?

Short-Acting Human Insulin held the top position, accounting for 37.88% of 2025 revenue.

How are biosimilars affecting insulin pricing?

Biosimilar entry has driven originator price cuts—for example, European glargine prices dropped 21.6% after biosimilars launched—thereby pressuring margins while expanding patient access.

Why is Asia-Pacific the fastest-growing region for recombinant insulin?

Rapidly rising diabetes prevalence, regulatory modernization, and increased healthcare access push regional growth at an 8.63% CAGR.

Which delivery devices are expanding fastest?

Insulin Pumps and Patch Pumps are advancing at a 9.05% CAGR due to automated dosing features and improved user convenience.

What role do reimbursement policies play in market growth?

Policies such as the U.S. Medicare USD 35 monthly cap and European formulary preferences remove affordability barriers, directly boosting insulin volumes and shaping brand competition.

Page last updated on: