Market Overview

| Study Period | 2020 - 2031 |

|---|---|

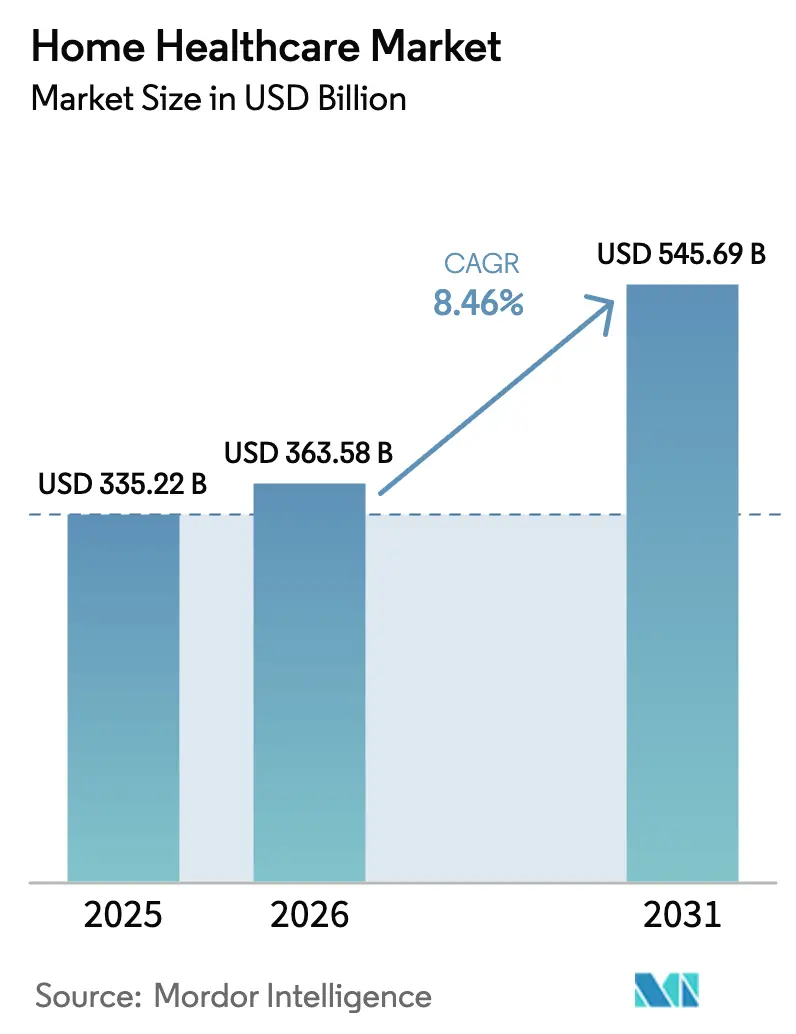

| Market Size (2026) | USD 363.58 Billion |

| Market Size (2031) | USD 545.69 Billion |

| Growth Rate (2026 - 2031) | 8.46% CAGR |

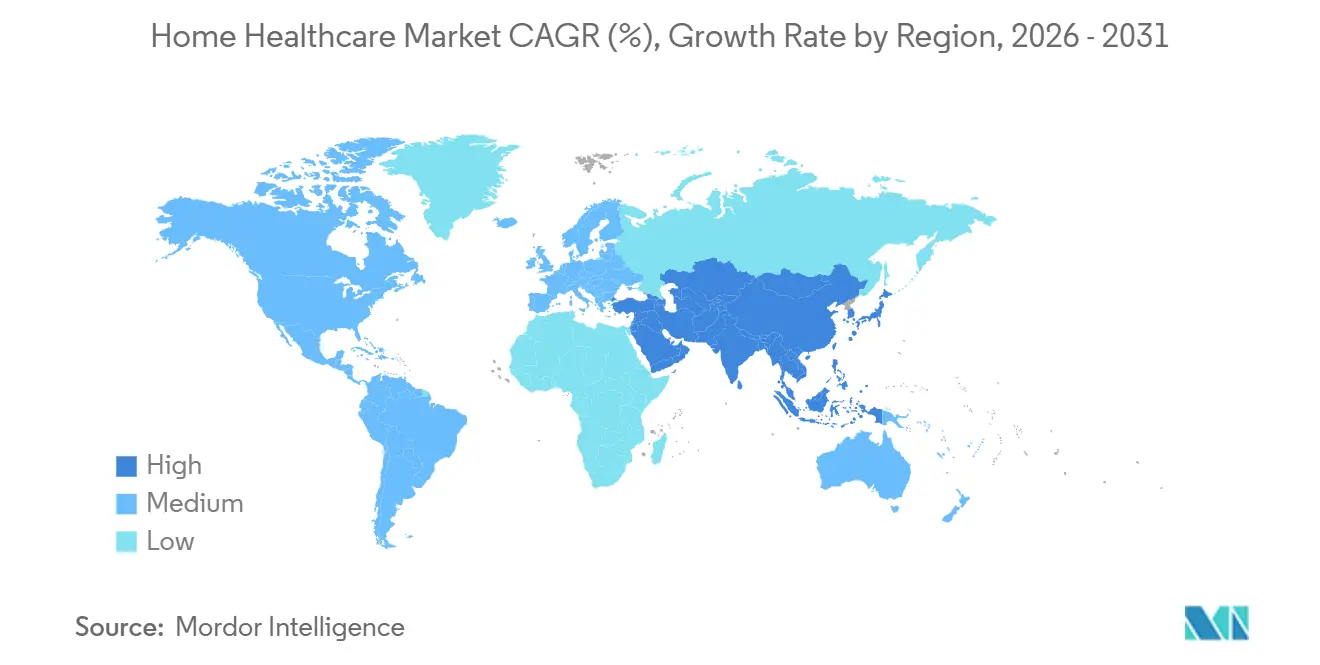

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

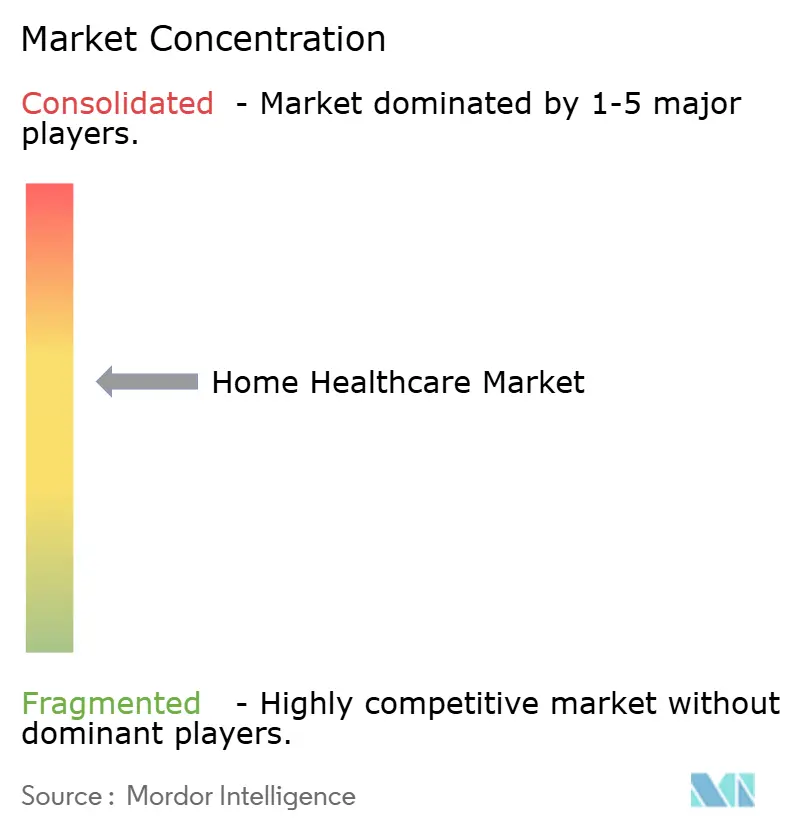

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Healthcare Market Analysis by Mordor Intelligence

The Home Healthcare Market size was valued at USD 335.22 billion in 2025 and is estimated to grow from USD 363.58 billion in 2026 to reach USD 545.69 billion by 2031, at a CAGR of 8.46% during the forecast period (2026-2031).

This growth profile reflects a convergence of aging populations, favorable reimbursement reforms, and reliable connected-device ecosystems that shift acute and chronic care into residential settings. Equipment continues to anchor revenues, yet an accelerating mix shift toward software platforms and data subscriptions signals a maturing digital layer that agencies and payers increasingly view as essential infrastructure for value-based contracting. Device miniaturization and edge computing lower the cost of in-home diagnostics, widening access in emerging economies while easing bandwidth constraints in rural North America and Europe. At the same time, hospital-at-home programs allow hospitals to bill inpatient rates for care delivered in living rooms, creating a direct incentive for integrated delivery networks to bundle devices, skilled nursing, and telehealth into single episodes of care. Competitive intensity remains moderate to high as incumbents defend share with FDA-cleared algorithms, while venture-backed entrants exploit open APIs and modular sensors to undercut on price without compromising clinical accuracy.

Key Report Takeaways

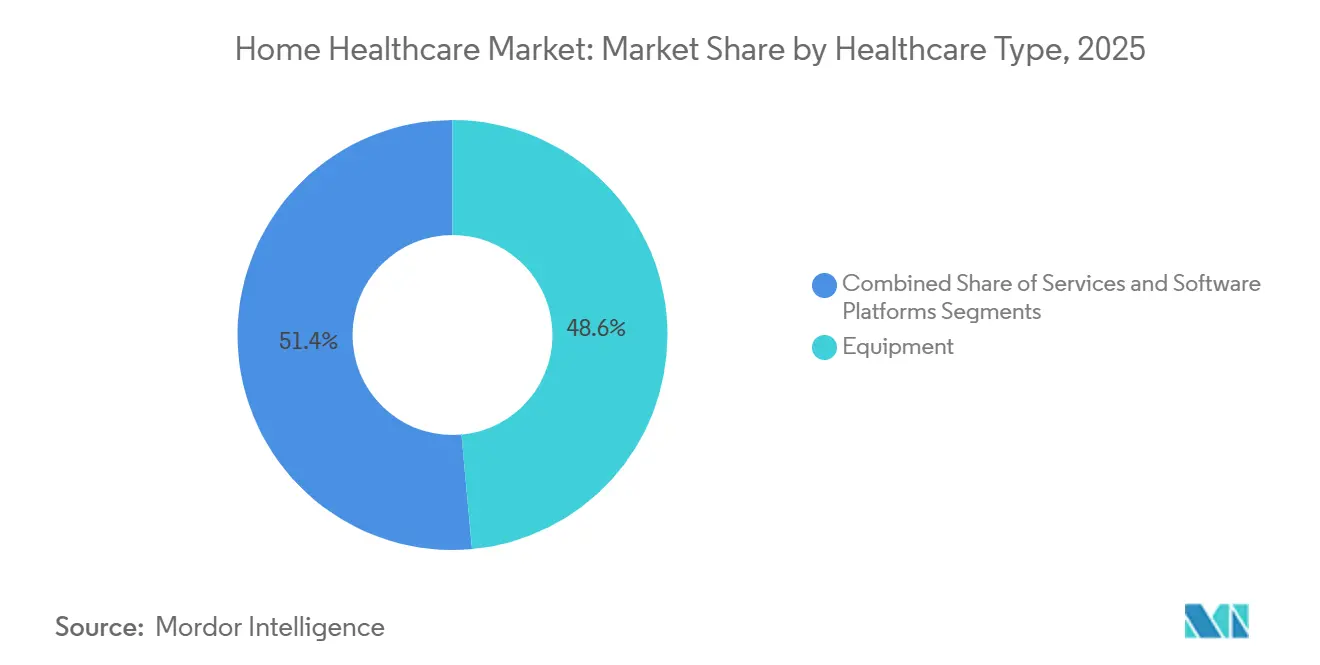

- By healthcare type, Equipment led with 48.56% of home healthcare market share in 2025. Software Platforms are forecast to deliver the fastest segment expansion, advancing at a 12.25% CAGR to 2031.

- By indication, Cardiovascular conditions commanded 26.53% of the 2025 revenue mix, whereas Diabetes is projected to grow at a 10.85% CAGR through 2031.

- By geography, North America retained a 42.13% revenue share in 2025, while Asia-Pacific is on track for a 9.51% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Home Healthcare Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Aging populations driving chronic-care demand | +2.1% | Global, concentrated in Japan, Germany, Italy, South Korea | Long term (≥ 4 years) |

| Reimbursement expansion for remote monitoring | +1.8% | North America & EU | Medium term (2-4 years) |

| AI-enabled devices boost proactive home care | +1.5% | North America, Western Europe, APAC urban hubs | Medium term (2-4 years) |

| Shift to "hospital-at-home" models | +1.3% | United States, United Kingdom, Australia | Short term (≤ 2 years) |

| Edge-computing IoT lowers in-home device costs | +0.9% | Global, early adoption in China, India, Southeast Asia | Long term (≥ 4 years) |

| Miniaturized lab-on-chip diagnostics enter home | +0.7% | North America, EU, APAC advanced economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Populations Driving Chronic-Care Demand

The World Health Organization estimates that 1.4 billion people will be aged 60 plus by 2030, with 80% residing in low- and middle-income nations where institutional long-term care remains limited. Each added year of life expectancy beyond 75 correlates with three to five additional years of chronic-disease management that is less costly when delivered at home than in skilled-nursing facilities. Japan already spends heavily on community-based integrated care under its long-term care insurance scheme, providing a template for other super-aged societies. In China, the 14th Five-Year Plan mandates a 15-minute radius for elderly community services in urban areas, driving local demand for portable diagnostics and telemedicine that link township clinics to tertiary centers. As similar demographic pivots unfold across Europe and North America, the home healthcare market benefits directly from scaled, policy-backed patient migration out of acute settings.

Reimbursement Expansion for Remote Monitoring

The Centers for Medicare & Medicaid Services permanently added CPT codes 99453, 99454, 99457, and 99458, reimbursing providers for device setup, data transmission, and monthly physiologic review, thus normalizing remote-patient monitoring across urban and rural settings alike[1]“Calendar Year 2025 Medicare Physician Fee Schedule Final Rule,” Centers for Medicare & Medicaid Services, cms.gov. Commercial insurers such as UnitedHealthcare and Humana now pay 85-90% of in-office rates for similar services, closing the margin gap that once hindered physician adoption. The shift converts hardware into a recurring revenue model whereby manufacturers subsidize devices and earn subscription fees, mirroring consumer-wearable economics yet underpinned by clinical-grade accuracy and FDA oversight.

AI-Enabled Devices Boost Proactive Home Care

Between 2024 and 2025, the FDA cleared eight algorithms embedded in home-use devices, including Apple Watch atrial fibrillation detection, Eko low-ejection-fraction screening, and Insulet’s Omnipod 5 for automated insulin delivery. Edge processors now let devices run inference locally, trimming latency from seconds to milliseconds and addressing privacy concerns inherent in cloud transmissions. Early results are compelling: ResMed’s Smart Comfort AI cut apnea events and raised therapy adherence by 18 percentage points after its December 2025 clearance.

Shift to Hospital-at-Home Models

CMS’s Acute Hospital Care at Home waiver allows more than 300 hospitals to bill full DRG rates for services delivered in residences, producing 20% lower 30-day readmissions and higher patient satisfaction than traditional admissions. The United Kingdom’s National Health Service similarly targets a 15% reduction in emergency-department crowding through virtual wards that monitor 10,000 concurrent patients. The model blurs equipment and service boundaries, pressuring standalone agencies to integrate vertically or accept subcontractor status.

Restraints Impact Analysis of Home Healthcare Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Shortage of skilled home-care clinicians | -1.4% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Cyber-security & privacy threats to medical IoT | -0.9% | Global, acute in North America & EU | Medium term (2-4 years) |

| Reimbursement rate uncertainty for agencies | -0.7% | United States, fragmented in emerging markets | Short term (≤ 2 years) |

| Lithium-battery supply risk for critical devices | -0.5% | Global, supply-chain bottlenecks in APAC manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Home-Care Clinicians

The United States faces a projected 78,000-nurse deficit by 2026, and home-health-aide turnover tops 65% in several states, limiting agencies’ capacity to accept new patients even as demand rises. Median aide pay of USD 13.50 per hour lags other service sectors, forcing agencies to raise wages 12-18% since 2024, compressing margins that averaged 3-5% pre-pandemic.

Cyber-Security & Privacy Threats to Medical IoT

In 2024 the FDA required software bills of materials and vulnerability management plans for all networked devices after researchers cataloged 127 exploitable flaws across common insulin pumps and glucose monitors[2]“Cybersecurity in Medical Devices,” U.S. Food and Drug Administration, fda.gov. HIPAA penalties reach USD 1.5 million per breach, pushing smaller manufacturers toward partnerships or exits as compliance costs consume up to 12% of R&D budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Home Healthcare Market Segment Analysis

By Healthcare Type:

Equipment Anchors Revenue, Software AcceleratesEquipment represented 48.56% of the home healthcare market in 2025, spotlighting the capital intensity of therapeutic gear such as ventilators, dialysis systems, and insulin pumps. Therapeutic equipment revenues gain from Medicare’s policy that reimburses home dialysis at 80-90% of in-center rates, enlarging the home healthcare market size for renal-care technology by routing high-acuity procedures into domestic environments. Diagnostic and monitoring devices become more affordable; fingerstick glucometer average selling prices fell 25% between 2023 and 2025 as continuous glucose monitors captured share, compressing margins for legacy products. Mobility assist equipment faces direct-to-consumer pressure that widens geographic reach but thins distributor profits.

Services constitute the second-largest 2025 slice, yet staffing deficits force agencies to triage high-acuity cases while technology offsets some labor gaps through remote vitals monitoring and tele-therapy. Hospice and palliative care expand steadily as Medicare’s hospice benefit lowers financial barriers, and tele-homecare volumes stay elevated under permanent billing codes. Software platforms, though starting from a smaller base, are forecast to post a 12.25% CAGR through 2031 as electronic visit verification and open FHIR APIs become prerequisites for payer contracts. The FDA’s Software as a Medical Device framework adds regulatory hurdles yet confers clinical credibility that hastens commercial adoption.

By Indication:

Cardiovascular Leads, Diabetes SurgesCardiovascular conditions held 26.53% of home healthcare market share in 2025, aided by validated home blood-pressure cuffs, implantable loop recorders, and AI-enabled electrocardiogram patches that let clinicians titrate therapy remotely. Remote heart-failure monitoring programs reduce 30-day readmissions by up to 30%, making value-based bundles financially attractive for insurers. Meanwhile, diabetes is on track for a 10.85% CAGR, the fastest among tracked indications, thanks to continuous glucose monitors and closed-loop pumps whose mean absolute relative differences now sit below 10%, meeting replacement thresholds for fingerstick calibration. The FDA’s 2025 clearance of Omnipod 5 for Type 2 diabetes enlarged the addressable user base by an order of magnitude, intensifying competition among pump manufacturers.

Respiratory disorders, including sleep apnea, gain from cloud-connected CPAP machines that upload adherence data to satisfy Medicare’s usage rules, while oncology infusion at home reduces hospital facility fees by 40-60% and limits immunocompromised patients’ exposure to pathogens. Wound-care revenue grows with rental models for negative-pressure systems, and neurology is emerging as smartphone-based digital therapeutics prove effective as adjuncts to physical therapy.

Geography Analysis

North America Home Healthcare Market

North America commanded 42.13% of 2025 revenue, powered by 52% Medicare Advantage penetration and CMS waivers that reimburse inpatient-level services rendered at home. Yet clinician shortages constrain capacity: certified-aide turnover exceeds 65%, and agencies often cap referrals, slowing potential expansion despite payer demand. Canada’s funding for home care remains under 4% of total health expenditure, and Mexico’s telemedicine pilots are creating incremental device demand as coverage extends into rural states.

APAC Home Healthcare Market

Asia-Pacific is forecast to lead growth at 9.51% CAGR through 2031, propelled by Japan’s super-aged demographic profile and Kaigo Hoken reforms that fund comprehensive in-home services[3]“Long-Term Care Insurance System,” Ministry of Health, Labour and Welfare, Japan, mhlw.go.jp. China mandates proximal community care, while India’s Production Linked Incentive scheme subsidizes local device manufacturing, slicing retail prices for basic monitors by up to 30%. South Korea and Australia experiment with outcome-tied payment models that reward agencies for avoiding readmissions rather than maximizing visit counts.

Europe Home Healthcare Market

Europe sustains meaningful share, with the United Kingdom’s virtual wards and Germany’s fast-track reimbursements for digital therapeutics broadening access. France’s hospitalisation à domicile handled 120,000 patients in 2024, predominantly for intravenous antibiotics and chemotherapy, underscoring the region’s advanced policy backing. Italy and Spain offer limited public reimbursement, producing a two-tier landscape in which affluent households fund private care while others rely on informal caregivers.

MEA and South America Home Healthcare Market

Smaller yet accelerating markets include the Gulf Cooperation Council states, which invest sovereign capital into smart-home monitoring, and South Africa, where private insurers pilot remote monitoring for HIV adherence. Brazil’s Programa Melhor em Casa treated 200,000 patients in 2024 but remains unevenly distributed, indicating latent demand for devices and software in underserved northern regions.

Competitive Landscape

The home healthcare market features moderate-to-high fragmentation. Global device manufacturers, Abbott, Medtronic, Philips, ResMed, Fresenius Medical Care, command high-margin therapeutic niches by coupling proprietary sensors to subscription analytics and consumable supply chains. Integrated payers such as Optum and Humana accelerate vertical consolidation, acquiring agencies to lock in referral flows and expand value-based care footprints. Software start-ups exploit the 21st Century Cures Act’s interoperability mandate to unbundle legacy electronic health records, offering lightweight scheduling, billing, and electronic visit verification modules that sync through FHIR APIs.

Patent filings cluster around AI-driven prediction, energy harvesting for battery life extension, and modular sensor boards that support multi-analyte testing, indicating a transition from single-purpose devices to diagnostic hubs. Compliance overhead becomes a competitive moat; the FDA’s cybersecurity guidance elevates cost structures, favoring incumbents able to amortize spending across broad portfolios. Digital adoption remains uneven: North American and European agencies integrate remote monitoring to satisfy payer metrics, whereas many Asia-Pacific and Latin American operators still depend on manual workflows, yielding a two-speed market where tech-forward players capture value-based contracts and laggards compete mainly on price.

Home Healthcare Industry Leaders

Abbott Laboratories

Medtronic plc

Koninklijke Philips N.V.

ResMed Inc.

Fresenius Medical Care AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Home Healthcare Market Companies Covered in this Report

- Abbott Laboratories

- Amedisys Inc.

- Bayada Home Health Care

- Beijing Jiuzhou Tongbang

- Cardinal Health

- CareCentrix Inc.

- Coloplast

- Drive DeVilbiss Healthcare

- Fresenius

- GE HealthCare Technologies Inc.

- Homage Pte Ltd.

- Home Instead Inc.

- Honor Technology

- Invacare

- Kindred at Home (Humana)

- Koninklijke Philips

- LHC Group Inc.

- Linde plc

- Mckesson

- Medtronic

- Omron Healthcare Co., Ltd.

- Resmed

- Sunrise Medical

Recent Industry Developments in Home Healthcare Market

- May 2025: Air Liquide boosted its home healthcare reach by acquiring intensivLeben GmbH and AP-Sachsen GmbH in Germany, strengthening outpatient intensive-care offerings.

- February 2025: Star Health Insurance expanded its home health-care initiative to 100 Indian locations, becoming the country’s largest organized provider.

Home Healthcare Market Report Scope and Research Methodology

Market Definition and Coverage

Our study views the home healthcare market as the total value of medical devices, digital tools, and face-to-face or technology-enabled clinical services delivered in a patient's residence, including skilled nursing, rehabilitation therapy, palliative care, remote monitoring hardware, and related consumables.

Scope exclusion: Short-stay hospital-at-home pilot programs funded as inpatient episodes are outside this count.

Segments Covered in This Report

- By Healthcare Type

- Equipment

- Therapeutic Equipment

- Insulin Delivery Devices

- Home IV Equipment

- Home Dialysis Equipment

- Ventilators & Nebulizers

- CPAP & BiPAP Devices

- Diagnostic & Monitoring Equipment

- Blood-glucose Monitors

- BP Monitors

- Pulse-oximeters

- ECG & Holter Monitors

- Digital Thermometers

- Mobility Assist Equipment

- Wheelchairs

- Walkers & Rollators

- Mobility Scooters

- Therapeutic Equipment

- Services

- Skilled Nursing

- Physical Therapy

- Occupational Therapy

- Speech Therapy

- Hospice & Palliative

- Personal (Unskilled) Care

- Respiratory Therapy

- Tele-homecare & Telehealth

- Software Platforms

- Agency Administration

- Clinical/EHR Platforms

- Remote-patient Monitoring SaaS

- Equipment

- By Indication

- Cardiovascular

- Diabetes

- Respiratory

- Cancer

- Wound-care

- Neurological Disorders

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Our team held structured calls with home-health agency directors, infusion nurses, RPM platform vendors, and regional reimbursement officers across North America, Europe, and key Asian countries. These conversations validated service-mix shifts, price dispersion, and realistic adoption curves that were not obvious in public data.

Desk Research

We gathered baseline numbers from freely available datasets such as OECD health expenditure tables, WHO Global Health Observatory home-care indicators, U.S. CMS Home Health PPS files, Eurostat long-term-care activity, and Japan's MHLW LTCI statistics. Annual reports, 10-Ks, and investor decks from diversified med-tech and home-care operators enriched average selling price and visit-volume inputs. Mordor analysts also extracted shipment leads from D&B Hoovers and filtered topical news on Dow Jones Factiva to monitor capacity expansions and payor rule changes. Patent trends from Questel and import data on respiratory kits via Volza helped us judge technology diffusion and cross-border trade. The secondary list is illustrative; many additional open publications supported data cleaning and variable checks.

Market-Sizing & Forecasting

We started with a top-down reconstruction that scales public and private home-care spending to the study's product and service scope, using age-cohort prevalence, chronic-disease incidence, and average episode cost as anchors. Supplier roll-ups of glucose meters, portable ventilators, and wound-care kits, plus sampled visit counts multiplied by blended reimbursement, offered bottom-up guardrails. Core drivers in the model include 65+ population growth, home infusion episode volume, RPM device unit shipments, nurse-hour wage inflation, and CMS rebasing updates, each forecast through multivariate regression with scenario checks. Where country data were patchy, ratios from matched economies filled gaps and were re-tested with our interview panel.

Data Validation & Update Cycle

Outputs pass variance thresholds, peer review, and anomaly sweeps before sign-off. Mordor refreshes every twelve months and issues mid-cycle tweaks when reimbursement or technology shocks emerge.

How Mordor Intelligence's Home Healthcare Market Size Compares to Other Published Estimates

Published estimates often diverge because firms choose different product baskets, price references, and refresh rhythms. We clarify scope first, then align every variable to in-home clinical delivery, which is why our 2024 base of USD 305.6 billion remains consistent.

Key gap drivers include competitors mixing hospital-at-home spends, applying flat ASP escalators, or projecting growth from single-region pilots without global adjustment. Our cadence and variable cross-checks limit such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 305.6 bn (2024) | Mordor Intelligence | - |

| USD 309.9 bn (2025) | Global Consultancy A | Includes diabetes test-strip retail sales and assumes uniform RPM penetration |

| USD 351.5 bn (2024) | Industry Publisher B | Adds hospital-at-home episode spend and uses headline device MSRP rather than realized prices |

Taken together, the comparison shows that our carefully bounded scope, dual-path modeling, and annual refresh give decision-makers the steadier baseline they need for budgeting and strategic planning.

Key Questions Answered in the Report

What is the projected value of the home healthcare market by 2031?

The market is forecast to reach USD 545.69 billion by 2031, reflecting an 8.46% CAGR over the period.

Which segment is expanding fastest within home-based care offerings?

Software platforms, used for administration, EHR integration, and remote monitoring, are projected to grow at a 12.25% CAGR through 2031.

Why is Asia-Pacific the quickest-growing region?

Policy reforms in Japan and China, coupled with India's device manufacturing incentives, are driving a 9.51% CAGR for the region from 2026 to 2031.

What primary factor restrains service capacity in North America?

A projected shortage of 78,000 registered nurses by 2026 and high home-health-aide turnover restrict agency expansion despite rising demand.

How do hospital-at-home programs affect acute care delivery costs?

Early U.S. pilots show 20% fewer 30-day readmissions and higher patient satisfaction, signaling potential cost savings and quality gains for payers and providers.

Page last updated on: