Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

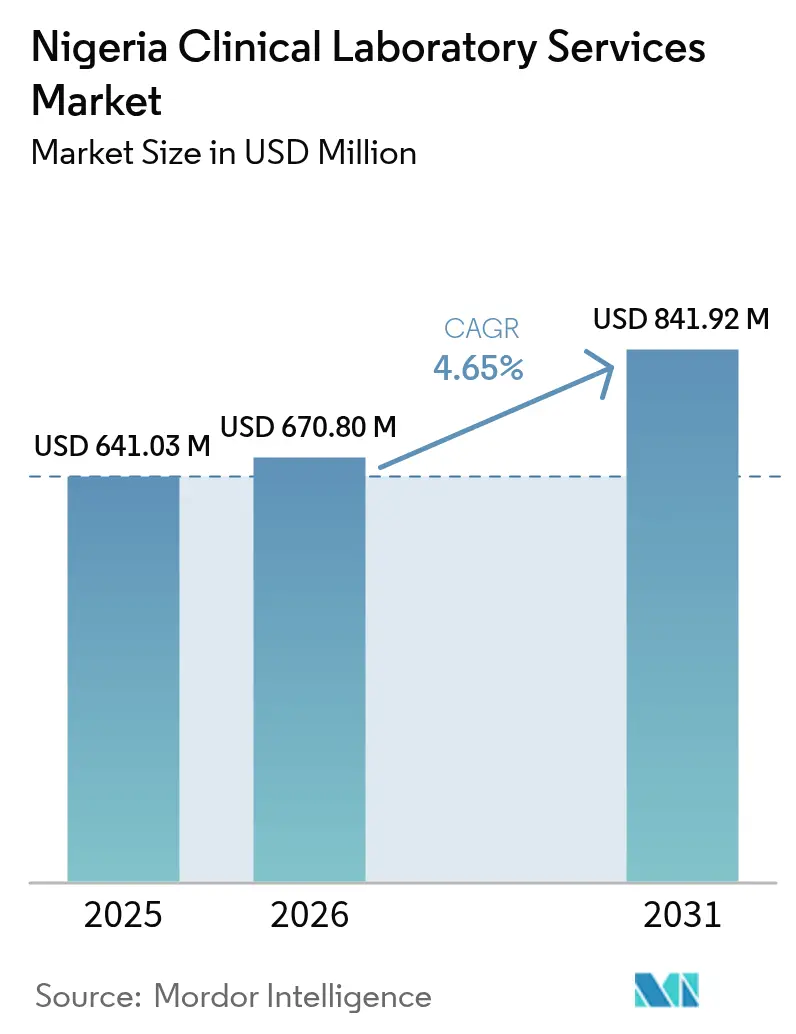

| Base Year Market Size (2025) | USD 641.03 Million |

| Market Size (2026) | USD 670.8 Million |

| Market Size (2031) | USD 841.92 Million |

| Growth Rate (2026 - 2031) | 4.65% CAGR |

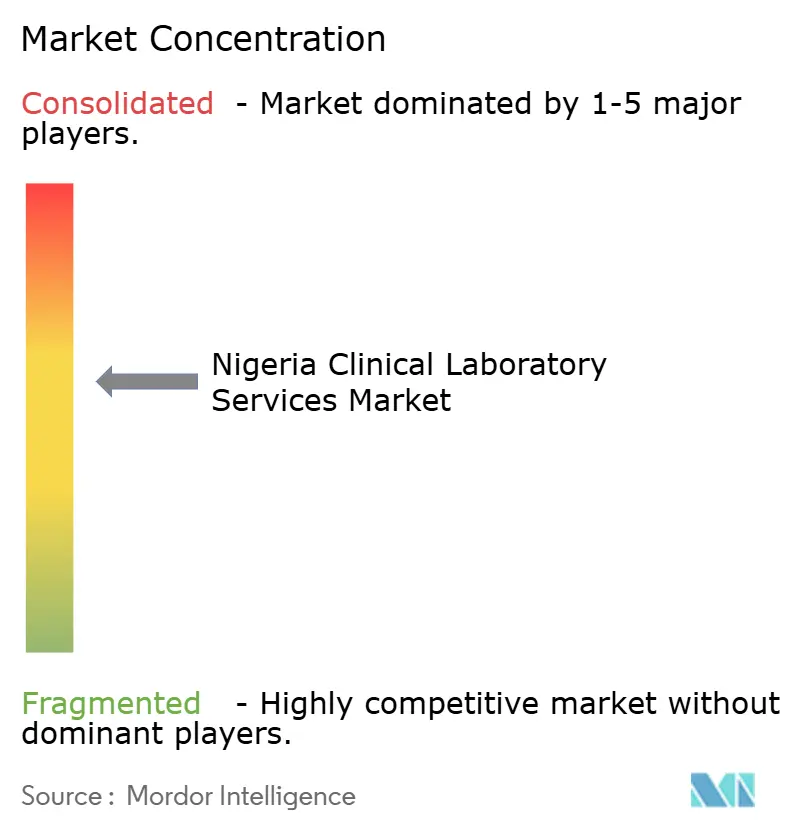

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Clinical Laboratory Services Market Analysis by Mordor Intelligence

The Nigeria clinical laboratory services market size is expected to grow from USD 641.03 million in 2025 to USD 670.8 million in 2026 and is forecast to reach USD 841.92 million by 2031 at 4.65% CAGR over 2026-2031. Sustained demand stems from the dual disease burden, rising health-insurance enrollment, and continuous public–private investment that modernizes diagnostic infrastructure. Currency volatility and a 1,100% jump in antibiotic costs after multinational pharmaceutical exits compressed margins, yet testing volumes rose as clinicians intensified evidence-based care to offset drug shortages. Technology adoption, especially laboratory information systems and point-of-care platforms, improved turnaround times in urban centers while AI-enabled analytics began to penetrate diabetic-retinopathy screening workflows. Despite workforce constraints—Nigeria retains only 55,000 physicians for 220 million citizens—task-sharing, telepathology, and centralized reference networks helped laboratories maintain service continuity.

Key Report Takeaways

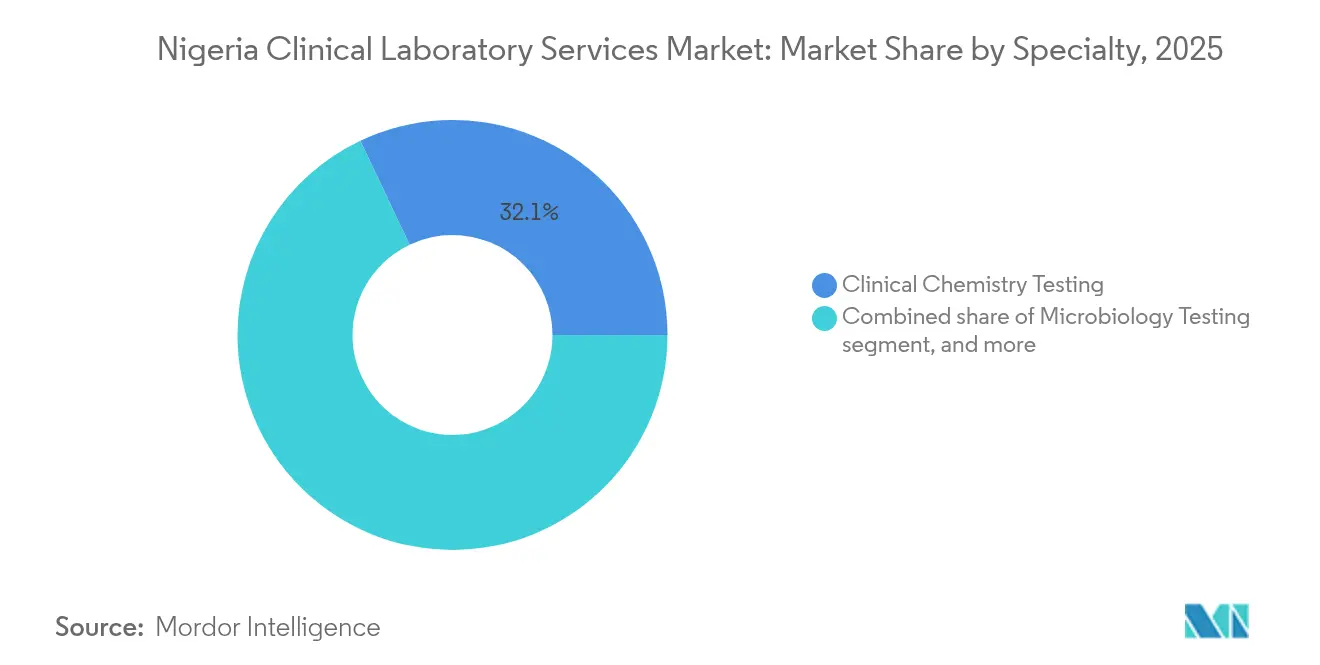

- By specialty, clinical chemistry led with 32.05% revenue share in 2025; genetic and molecular testing is set to advance at a 6.31% CAGR through 2031.

- By provider type, independent and reference laboratories accounted for 59.10% of the Nigeria clinical laboratory services market share in 2025, while hospital-based laboratories are expanding at 6.08% CAGR through 2031.

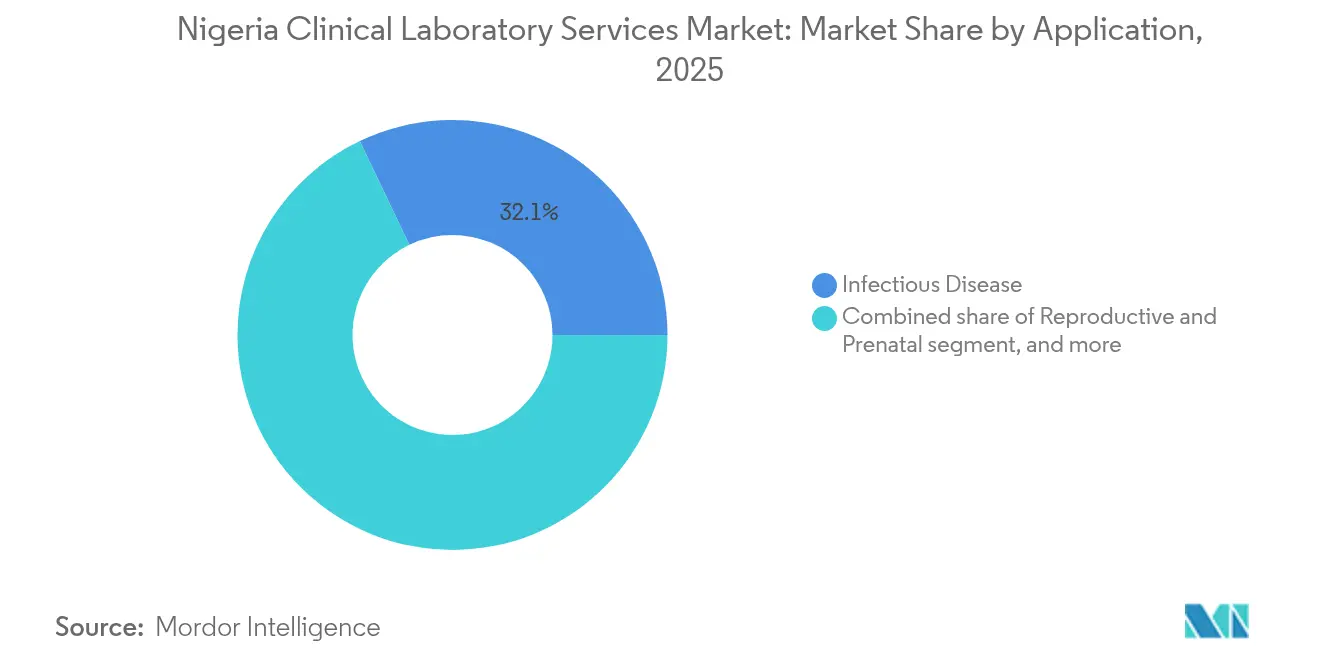

- By application, infectious-disease testing captured 32.10% of the Nigeria clinical laboratory services market size in 2025; non-communicable-disease testing is forecast to post a 7.14% CAGR to 2031.

- By test type, routine tests represented 55.12% share of the Nigeria clinical laboratory services market size in 2025; specialized and esoteric tests are projected to grow at 6.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Clinical Laboratory Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disease Burden and Diagnostic Demand | +1.2% | Lagos, Kano, Rivers | Medium term (2-4 years) |

| Expanding Public–Private Healthcare Investments | +0.9% | Lagos, Abuja, Port Harcourt | Long term (≥ 4 years) |

| Growing Health Insurance Coverage | +0.7% | Nationwide | Long term (≥ 4 years) |

| Adoption of Digital and Point-of-Care Technologies | +0.8% | Urban centers extending to rural areas | Medium term (2-4 years) |

| Diaspora Remittance–Driven Healthcare Spending | +0.5% | Southwest & Southeast | Short term (≤ 2 years) |

| Governmental Quality and Accreditation Initiatives | +0.6% | Tertiary facilities nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disease Burden and Diagnostic Demand

Nigeria’s simultaneous fight against infectious and non-communicable diseases underpins structural growth in the Nigeria clinical laboratory services market. Malaria positivity topped 52.4% in several states during 2024 while tuberculosis GeneXpert coverage soared from 7.4% in 2015 to 66% in 2023, underscoring aggressive case-finding programs. At the same time, cardiovascular-disease prevalence accelerated, yet only 31.6% of tertiary hospitals delivered cardiac-marker results within the recommended one-hour window[1]F. Mbonu et al., “Cardiac Marker Turnaround Study,” African Journal of Health Sciences, ajhsjournal.org. Viral-hepatitis rates—6.9% for hepatitis B and 4.8% for hepatitis C—require continuous viral-load monitoring. Population growth toward 440 million by 2050 compounds pressure on existing laboratories, prompting network expansion and adoption of high-throughput analyzers. Collectively, these epidemiological trends translate into durable multi-specialty test demand that shields the Nigeria clinical laboratory services market from cyclical economic swings.

Expanding Public–Private Healthcare Investments

The National Health Sector Renewal Investment Initiative catalyzes USD 3 billion in blended financing, channeling funds into 3,000 planned primary-care centers equipped with basic laboratories. Federal budget allocation to health rose 41.5% in 2023, including ₦37 billion for facility upgrades. Private capital follows suit: a Lagos-based chain secured USD 2 million for network enlargement, while an international IVD manufacturer established an antimicrobial-stewardship center in 2023, bringing advanced phenotypic-testing capacity to West Africa. Cross-border partnerships lower equipment-procurement costs, enable reagent volume discounts, and accelerate ISO 15189 accreditation pursuits. Such investment momentum underwrites long-term volume growth, even as macro-risks persist.

Growing Health-Insurance Coverage

Implementation of the National Health Insurance Authority Act in 2022 reshapes payment flows across the Nigeria clinical laboratory services market. The Vulnerable Group Fund targets 83 million citizens, potentially doubling the insured base and trimming the current 76% out-of-pocket spending rate. Early deployments of the Basic Healthcare Provision Fund in northern states already lift prenatal-screen uptake and chronic-disease monitoring frequencies. Laboratories are redesigning billing interfaces to integrate claims-management modules, shortening reimbursement cycles and improving cash flow. Wider coverage encourages preventive testing and long-interval disease management panels, supporting steady volume growth over the next decade.

Adoption of Digital and Point-of-Care Technologies

Digitization progresses from isolated laboratory information systems to integrated, cloud-hosted platforms capable of bidirectional EHR connectivity in tertiary hospitals across Lagos and Abuja. A statewide readiness audit identified a 35-point improvement in LIS adoption scores between 2022 and 2024. Mobile diagnostic hubs leverage lightweight analyzers and satellite connectivity, slashing specimen transit times for rural patients. Point-of-care glucose meters and urine dipsticks are now standard in 68% of surveyed facilities, yet less than 56% maintain continuous quality-control logs. AI-enabled analyzers, such as an ophthalmic-screening platform aiming to test 5 million Nigerians by 2027, promise to offset specialist shortages and elevate diagnostic precision. Regulators have updated validation checklists to embed cybersecurity and data-privacy protocols, balancing innovation with patient-safety mandates.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Skilled Workforce and Infrastructure | −0.8% | Rural & northern regions | Long term (≥ 4 years) |

| Supply Chain and Power Reliability Challenges | −0.6% | Nationwide, acute in northern states | Medium term (2-4 years) |

| Currency Fluctuations Increasing Input Costs | −0.5% | Import-dependent facilities nationwide | Short term (≤ 2 years) |

| Fragmented Regulatory and Quality Oversight | −0.4% | Multi-agency nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Skilled Workforce and Infrastructure

Physician density stands at 1:4,000, far below the WHO target of 1:600, as 15,000–16,000 clinicians emigrated in the past five years. Laboratory technologist programs enroll fewer than 2,100 graduates annually, leaving a widening skills gap. Salary differentials—domestic pay ranges from USD 2,000 to USD 4,000 per year compared with USD 60,000 in the United Kingdom—fuel outbound migration. Equipment shortages compound workforce stress: only 55.9% of tertiary hospitals operate functional cardiac-marker analyzers, and 43% lack uninterrupted power supplies critical for cold-chain reagent storage. Rural diagnostic centers face the brunt of shortages, extending sample-to-result times beyond clinically useful windows. Without accelerated training grants and retention incentives, the Nigeria clinical laboratory services industry risks capacity bottlenecks that curb long-range growth.

Supply Chain and Power Reliability Challenges

Laboratories import 79% of analyzers, reagents, and consumables, exposing them to foreign-exchange volatility that ballooned costs when the naira depreciated 55% against the U.S. dollar in 2024[2]Central Bank of Nigeria, “Foreign Exchange Market Statistics 2024,” cbn.gov.ng. The 2024 exit of multinational pharmaceutical distributors disrupted just-in-time reagent delivery pipelines, forcing laboratories to pre-order six-month stockpiles, thereby tying up working capital. National grid reliability hovered at 68% uptime, obliging facilities to rely on diesel generators that raised per-test energy costs by 11%. Cold-chain lapses led to 7.3% reagent wastage in peripheral labs during the 2023 malaria-peak season. NAFDAC has begun piloting a fast-track IVD-import channel aligned with WHO pre-qualification to cut customs delay by half, yet scale-up remains pending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Specialty: Molecular Testing Accelerates Precision Care

Clinical chemistry retained a 32.05% revenue lead within the Nigeria clinical laboratory services market in 2025, underscoring the category’s role in diabetes, renal, and lipid-profile management. The segment’s dominance is fueled by automated analyzers capable of running 400–600 tests per hour, minimizing per-test costs. Molecular diagnostics, however, posted a 6.31% CAGR and is reshaping high-margin growth trajectories. Genetic-screen programs for sickle-cell disease and oncology panels gained policy traction following the launch of the Centre for Human Virology & Genomics in Lagos. Federal procurement agreements cut PCR-reagent prices 18%, triggering adoption in 27 additional tertiary centers. Infectious-disease nucleic-acid testing now covers 66% of TB case detection, while emergent next-generation sequencing facilities produced Nigeria’s first pathogen genomic-surveillance dashboards in 2024. The Nigeria clinical laboratory services market size for molecular diagnostics is therefore expected to climb steadily as capacities expand and cost curves fall.

Parallel growth permeates microbiology, hematology, and immunology. Microbiology revenue ramped after a national TB-molecular expansion that lowered test turnaround to 3 hours. Hematology demand remains tethered to malaria and sickle-cell management; opening of a dedicated hemoglobinopathy lab in Awka extended specialized flow-cytometry testing beyond Lagos. Immunology growth is anchored in HIV viral-load monitoring, with reagent pack prices dropping 12% under pooled-procurement schemes. Cytology and pathology services lag due to a 1:250,000 pathologist-to-population ratio, but remote-slide-reading pilots could unlock latent demand. As disease profiles diversify, multi-disciplinary labs capable of routing samples through chemistry, immunoassay, and molecular lines will capture a premium, deepening competitive differentiation.

By Provider: Independent Networks Maintain Scale Advantage

Independent and reference laboratories commanded 59.10% Nigeria clinical laboratory services market share in 2025, leveraging hub-and-spoke logistics, brand trust, and direct-to-consumer marketing. Leading chains process upward of 2 million tests annually, offering 360-degree menus spanning hematology to high-resolution genomics. Cost efficiency stems from centralized high-throughput analyzers and reagent bulk-purchasing contracts, allowing narrow per-test margins while sustaining profitability. Hospital-based labs, historically restricted by capital budgets, now benefit from earmarked infrastructure funds under the Health-Renewal Initiative, registering a 6.08% CAGR and closing service gaps in peri-urban areas.

Partnership models multiply as private labs sign managed-service agreements with public hospitals, installing analyzers in exchange for guaranteed minimum volumes. Telepathology networks route histo-slides to reference centers, expanding service breadth without full-time on-site pathologists. The Nigeria clinical laboratory services market size attributed to hospital-embedded operations is forecast to rise as tertiary centers upgrade to ISO 15189 to improve transplant-readiness metrics. However, profit-pool migration toward hospital laboratories may remain capped until reimbursement tariffs align with real-time exchange-rate fluctuations. Independent networks counteract by integrating home-collection and digital-results portals, fortifying market position.

By Application: Chronic Disease Panels Outpace Traditional Infectious Focus

Infectious-disease testing still generated 32.10% of 2025 revenue but its share is edging downward as non-communicable-disease (NCD) panels gain traction. Urbanization and dietary shifts pushed adult diabetes prevalence past 6%, swelling HbA1c test orders by 14% in 2024. Cardiovascular-risk panels comprising lipid profiles, hs-CRP, and cardiac-marker assays grew 11% year on year despite reagent price spikes. Consequently, the Nigeria clinical laboratory services market size accruing to NCD applications is forecast to grow fastest at 7.14% CAGR. Prenatal screening volumes also climbed, linked to government-funded maternal-mortality-reduction campaigns that mandate early antenatal bloodwork.

Oncology diagnostics remain nascent but promising. An estimated 125,000 new cancer cases in 2024 spurred demand for tumor-marker panels, HER2 immunohistochemistry, and liquid-biopsy pilots, although specialist shortages continue to constrain capacity. Wellness testing packages broadened amid rising corporate-insurance coverage, embedding vitamin-D, thyroid, and hormonal profiles in routine executive health checks. Infectious-disease sub-segments are themselves evolving: multiplex respiratory-pathogen panels and dengue RT-PCR fill gaps in differential diagnosis as climate change updates vector-borne disease maps. Laboratories that diversify into comprehensive chronic-disease panels while retaining strong infectious-disease capabilities will harvest balanced revenue streams resistant to seasonal swings.

By Test Type: Specialized and Esoteric Tests Unlock Margin Upside

Routine tests made up 55.12% of total volumes in 2025, dominated by complete blood counts, electrolytes, and urinalysis. Automation of these tests reached 85% penetration in urban centers, achieving sub-$1 variable cost per assay. Yet specialized and esoteric tests—cytokine panels, pharmacogenomic assays, and next-generation sequencing—posted a 6.52% CAGR, dwarfing routine expansion. High-complexity tests carry gross margins above 45%, compared with 22% for routine panels, presenting an attractive mix-shift for profit-conscious providers. The Nigeria clinical laboratory services market size attributed to specialized tests is expected to double by 2030 as oncologists and rheumatologists integrate molecular biomarkers into treatment pathways.

Point-of-care (POC) adoption adds nuance: POC devices deliver rapid glucose and troponin readings in emergency units but can erode centralized-lab volumes if not integrated into LIS for data consolidation. Survey data show only 56% of facilities run daily POC-quality checks, risking result variability. Integration of middleware that harmonizes POC and core-lab data remains a priority to avoid diagnostic silos. Demand for specialized testing also spurs logistics evolution; cold-chain requirements and specimen-stability constraints lead reference labs to deploy regional mini-hubs equipped with −80 °C freezers. Consequently, test-type diversification shapes procurement strategies, staffing models, and capital-investment horizons.

Competitive Landscape

Competitive intensity is moderate, with no operator exceeding a 15% volume share nationally. Internationally backed SYNLAB leverages its global network of 600 million annual tests and centralized procurement to offer specialized panels, while Lancet Laboratories maintains strength in microbiology and oncology testing. Indigenous chain MDaaS Global employs a digital-first model that integrates home-collection, teleconsultation, and BeaconOS reporting, strategically positioning 17 hubs within 3-hour drive time for 53 million Nigerians. Independent stand-alone labs compete on convenience and rapid turnaround, but scale disadvantages limit their ability to secure reagent discounts.

Technology serves as a key differentiator. FundusAI’s diabetic-retinopathy solution is embedding retinal-image analytics into partner-lab workflows, reducing ophthalmologist referral burden by 38%. Established players invest in middleware to unify POC, core-lab, and radiology data, thereby improving clinician user experience. Accreditation status influences payer negotiations; ISO 15189-certified labs command tariff premiums of 8% under select corporate-insurance plans. Market entry barriers include MLSCN licensing requirements, NAFDAC import permits, and capital costs for automated chemistry lines, tempering the threat of new entrants.

Strategic alliances proliferate. Hospital chains outsource laboratory operations under reagent-rental agreements, guaranteeing minimum volumes that de-risk supplier investments. Equipment vendors co-locate maintenance engineers within high-volume labs, cutting mean-time-to-repair from 72 to 24 hours. Supply-chain hedging via multi-currency procurement contracts gained traction post-2024 currency swings. Competitive dynamics will likely intensify as telemedicine providers integrate on-demand lab ordering, blurring boundaries between diagnostic and primary-care ecosystems and reinforcing the centrality of data-driven service delivery in the Nigeria clinical laboratory services market.

Nigeria Clinical Laboratory Services Industry Leaders

Mecure Healthcare Limited

AfriGlobal Medicare Limited

Synlab Bondco PLC

Echolab

Union Diagnostic & Clinical Services PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: African Medical Centre of Excellence opened commercial operations, integrating advanced molecular and imaging laboratories in Abuja.

- October 2024: Cinven agreed to acquire a 10% stake in SYNLAB AG, reinforcing capital for sub-Saharan expansion.

- August 2024: HJFMRI inaugurated a modular tuberculosis laboratory in Abuja, boosting national GeneXpert capacity.

- June 2024: eHealth Africa invested USD 2 million and donated USD 112,000 in equipment to EHA Clinics, enhancing laboratory automation.

Nigeria Clinical Laboratory Services Market Report Scope

As per the scope of the report, a clinical laboratory utilizes samples of fluids or tissues from patients to obtain information about the patient's health to aid in the diagnosis, prevention, and treatment of diseases. The space is organized into anatomic pathology, clinical chemistry, hematology, genetics, microbiology, phlebotomy, and the blood bank.

The Nigerian clinical laboratory services market is segmented by specialty and provider. The market is segmented by specialty into clinical chemistry testing, microbiology testing, hematology testing, immunology testing, cytology testing, genetic testing, and other specialties. Provider segments the market into independent, reference, and hospital-based laboratories. The report offers the market size in value terms in USD for all the abovementioned segments.

By Specialty

| Clinical Chemistry Testing |

| Microbiology Testing |

| Hematology Testing |

| Immunology Testing |

| Cytology Testing |

| Genetic & Molecular Testing |

| Other Specialties |

By Provider

| Independent & Reference Laboratories |

| Hospital-Based Laboratories |

By Application

| Infectious Disease |

| Non-Communicable / Chronic Disease |

| Reproductive & Prenatal |

| Oncology |

| Wellness & Preventive Screening |

By Test Type

| Routine Tests |

| Specialized / Esoteric Tests |

| By Specialty | Clinical Chemistry Testing |

| Microbiology Testing | |

| Hematology Testing | |

| Immunology Testing | |

| Cytology Testing | |

| Genetic & Molecular Testing | |

| Other Specialties | |

| By Provider | Independent & Reference Laboratories |

| Hospital-Based Laboratories | |

| By Application | Infectious Disease |

| Non-Communicable / Chronic Disease | |

| Reproductive & Prenatal | |

| Oncology | |

| Wellness & Preventive Screening | |

| By Test Type | Routine Tests |

| Specialized / Esoteric Tests |

Key Questions Answered in the Report

How large is Nigeria’s clinical laboratory services market in 2026?

The Nigeria clinical laboratory services market size is USD 670.8 million in 2026 and is forecast to reach USD 841.92 million by 2031 at a 4.65% CAGR.

Which test segment is expanding fastest nationwide?

Genetic and molecular diagnostics leads growth with a projected 6.31% CAGR as precision-medicine initiatives gain funding and equipment costs fall.

What share do independent laboratories hold?

Independent and reference laboratories captured 59.10% Nigeria clinical laboratory services market share in 2025 by leveraging centralized high-throughput hubs and home-collection services.

Why is health-insurance expansion critical for laboratories?

The National Health Insurance Authority targets coverage for 83 million citizens, which is expected to boost test utilization and stabilize reimbursement flows.

What are the major operational challenges for laboratories?

Key barriers include skilled-worker shortages, power-supply instability, foreign-exchange volatility that inflates reagent costs, and fragmented regulatory oversight.

How are laboratories addressing rural diagnostic gaps?

Providers deploy mobile testing units, adopt point-of-care devices, and integrate telepathology networks to shorten result times and expand menu reach in underserved regions.

Page last updated on: