Per Diem Nurse Staffing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

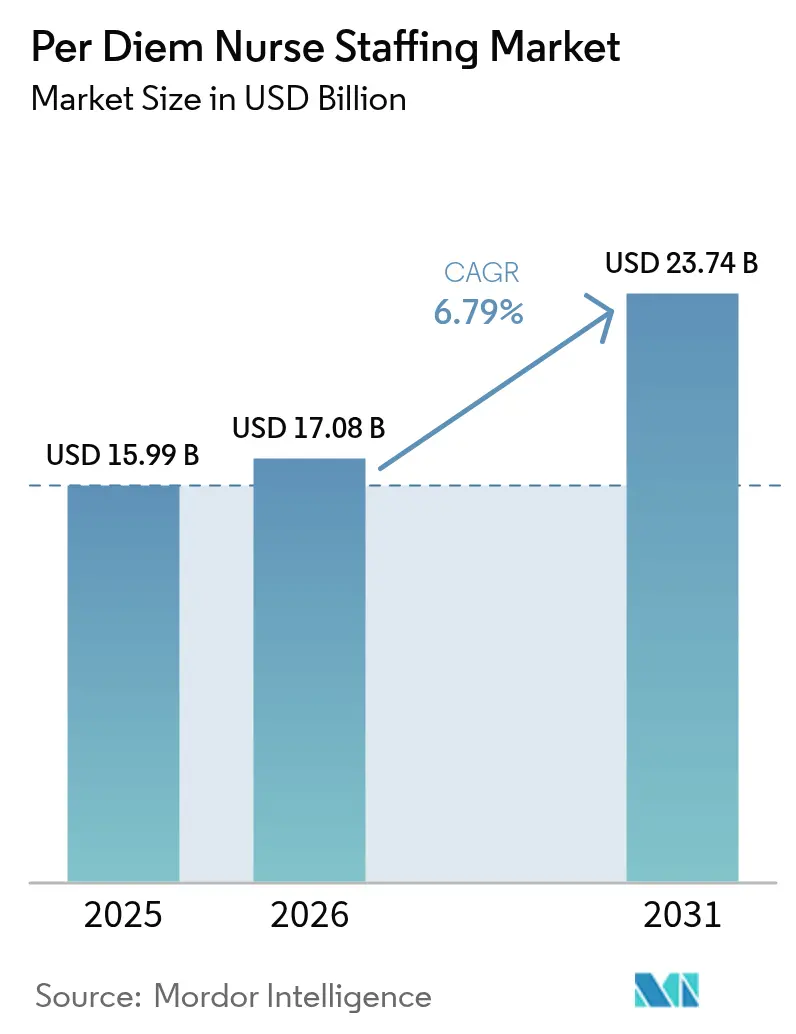

| Market Size (2026) | USD 17.08 Billion |

| Market Size (2031) | USD 23.74 Billion |

| Growth Rate (2026 - 2031) | 6.79% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Per Diem Nurse Staffing Market Analysis by Mordor Intelligence

The per diem nurse staffing market size was valued at USD 15.99 billion in 2025 and estimated to grow from USD 17.08 billion in 2026 to reach USD 23.74 billion by 2031, at a CAGR of 6.79% during the forecast period (2026-2031). Increasing reliance on flexible nurse supply, widening labor-cost pressures that already consume 60% of hospital operating expenses, and the World Health Organization’s forecasted 4.1 million global nurse shortfall are sustaining demand for on-demand coverage. Digital scheduling platforms, hospital census volatility, and value-based reimbursement incentives further reinforce adoption. Provider executives also view contingent staffing as a hedge against burnout-driven turnover, and they are willing to pay premiums for nurses who can step into high-acuity units without lengthy orientation. As technology lowers placement frictions, pricing transparency and real-time credentialing are becoming core competitive factors.

Key Report Takeaways

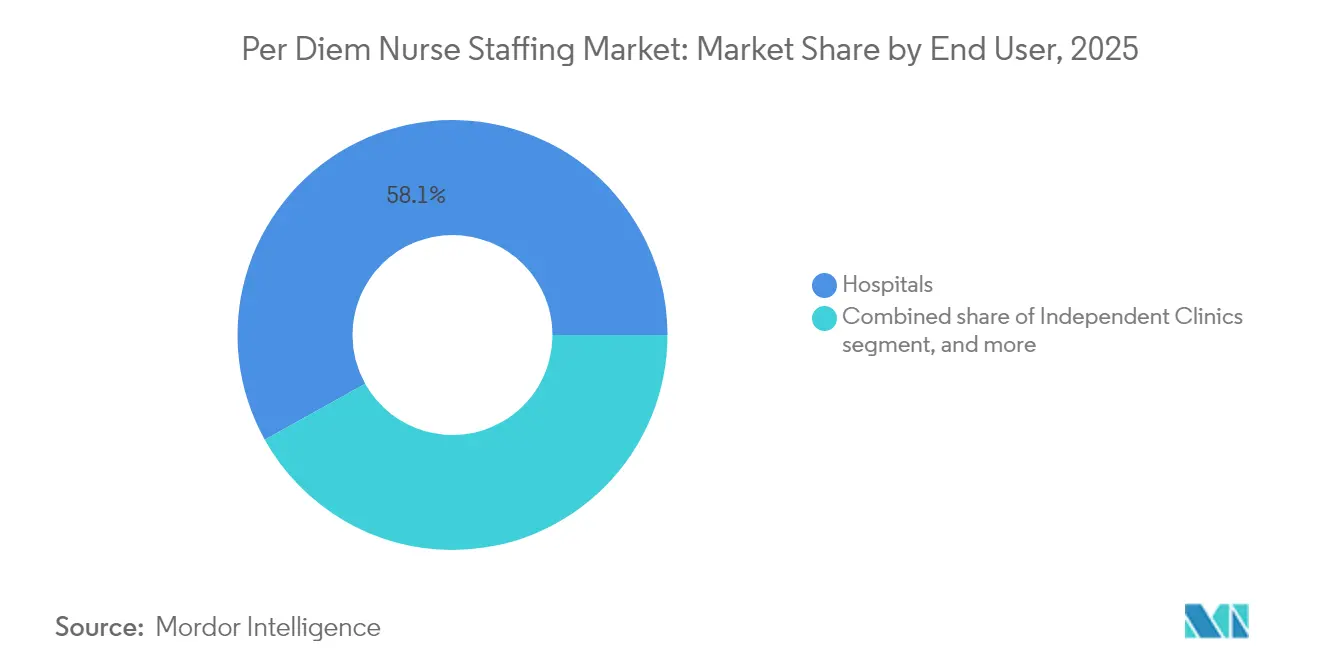

- By end-user, hospitals held 58.10% of the per diem nurse staffing market share in 2025, while home healthcare agencies are forecast to expand at an 8.34% CAGR from 2026 to 2031.

- By nurse type, registered nurses accounted for 61.85% of 2025 billings; advanced practice registered nurses are projected to post the fastest 8.87% CAGR through 2031.

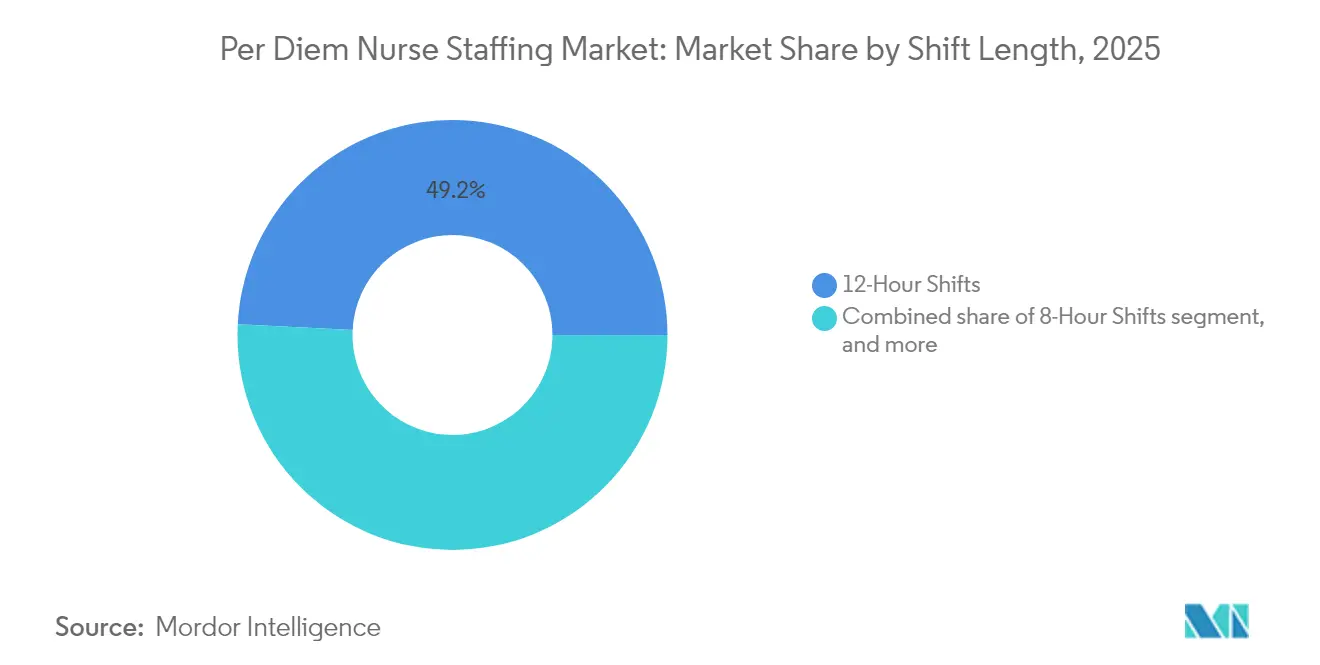

- By shift length, twelve-hour shifts led with 49.20% revenue in 2025, whereas float-pool/on-call arrangements are positioned for an 8.55% CAGR over the forecast horizon.

- By scheduling platform, traditional staffing agencies captured 72.90% of 2025 placements, yet app-based marketplaces are set to record a 8.98% CAGR during 2026-2031.

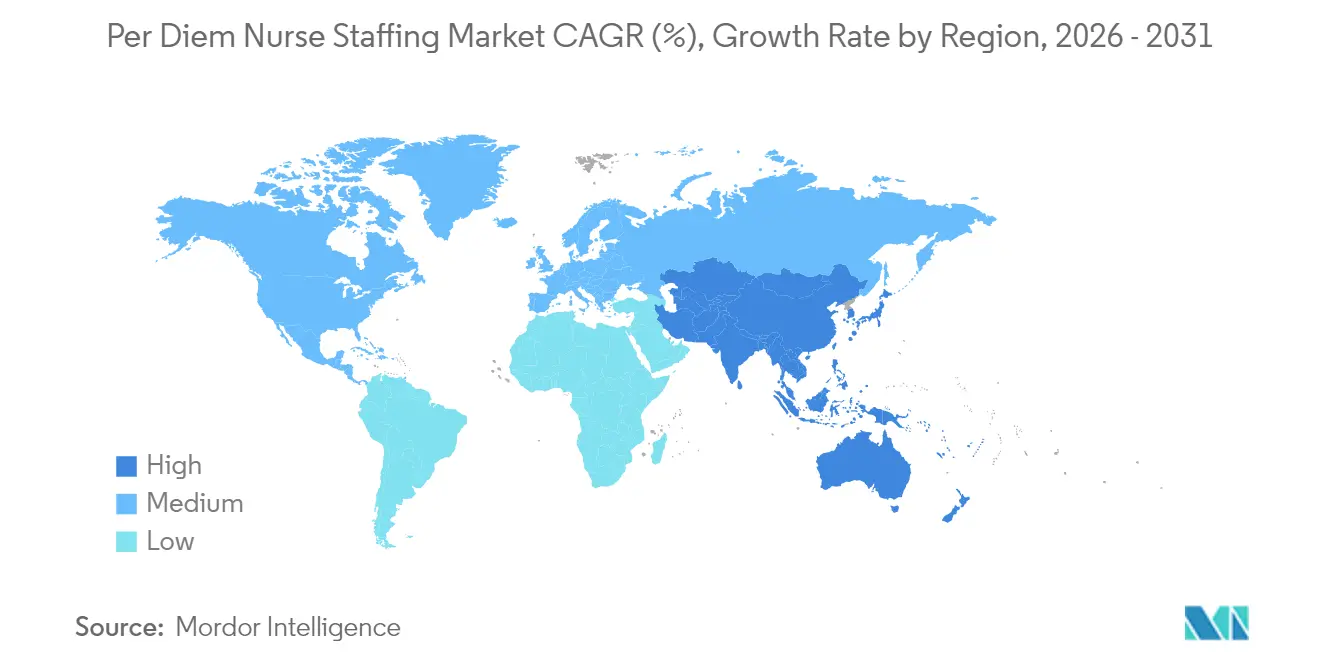

- By geography, North America dominated with 45.10% share in 2025, while Asia-Pacific is expected to deliver the quickest 7.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Per Diem Nurse Staffing Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Nursing Shortage | +2.1% | Global; acute in North America & Europe | Long term (≥ 4 years) |

| Accelerated Hospital Patient Admissions | +1.8% | Global; concentrated in aging populations | Medium term (2-4 years) |

| Cost Optimization Initiatives in Healthcare Facilities | +1.3% | North America & Europe | Short term (≤ 2 years) |

| Shift Toward Flexible Workforce Models | +0.9% | Global; led by developed markets | Medium term (2-4 years) |

| Rapid Adoption of Digital Staffing Platforms | +0.7% | Global; technology-enabled markets | Short term (≤ 2 years) |

| Expansion of Outpatient and Post-Acute Care Networks | +0.6% | North America; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Nursing Shortage

WHO data confirm that the worldwide pool climbed to 29.8 million in 2023, yet 78% of nurses still practice in countries that host just 49% of the global population, exposing severe regional imbalances. In the United States, the Department of Health and Human Services projects registered-nurse gaps approaching 10% by 2027, a level that would leave many hospitals unable to meet legally mandated staffing ratios[1]U.S. Department of Health and Human Services, “National Supply & Demand Projections for Registered Nurses: 2025–2030,” hhs.gov. Europe’s January 2025 “Nursing Action” initiative likewise acknowledges an 18 million-worker deficit across EU health professions. These deficits are making per diem contracts less discretionary and more structural as providers compete for scarce hands. Rate escalation follows naturally, setting a floor under per diem compensation and attracting clinicians who prefer autonomy.

Accelerated Hospital Patient Admissions

Post-pandemic admissions are stabilizing at volumes 15-20% above 2019 baselines as chronic disease prevalence and deferred care converge. Older patients drive longer average lengths of stay, raising nurse-minutes per bed and heightening the call for short-notice coverage. Emergency departments report more complex multimorbidity cases, and administrators cite per diem recruits as the only immediate fix because full-time hires can require months to onboard. The American Association of Nurse Practitioners flags geriatric demand as the most urgent 2025 trend, intensifying specialist placement needs[2]American Association of Nurse Practitioners, “2025 Trends in Geriatric Care,” aanp.org. Acute-care directors consequently view per diem rosters as operational shock absorbers.

Cost-Optimization Initiatives in Healthcare Facilities

Labor already represents 60% of hospital operating outlays, with finance teams under payor-mix pressure to curb fixed wage lines. Variable per diem scheduling converts a slice of those expenses from fixed to flexible, aligning nurse hours with fluctuating census. Internal float initiatives at WellSpan Health and Allegheny Health Network collectively saved USD 6.9 million between 2024 and 2025, yet leadership still relies on external per diem suppliers for highly specialized roles. Hybrid sourcing strategies—internal first, external for niche expertise—are emerging as the dominant cost model.

Shift Toward Flexible Workforce Models

Nurse sentiment surveys reveal that 93% of executives believe staff no longer view permanent employment as advantageous over independent contracting. The 1.7 million clinicians who resigned from health roles in 2022 demonstrate a workforce unafraid to seek schedule autonomy. Travel-nurse demand surged 35% between 2019 and 2020 and is on track for another 40% jump by 2026, a pattern echoed in per diem uptake as caregivers weigh burnout against flexibility. Institutions now target 20-35% of nursing hours from contingent pools, cementing the per diem channel in workforce architecture.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perceived Job and Income Instability | −1.2% | Global; acute in developing markets | Medium term (2-4 years) |

| Regulatory Limitations on Agency Fees | −0.8% | North America & Europe | Short term (≤ 2 years) |

| Growing Use of Internal Staffing Pools | −0.6% | Developed markets with large health systems | Long term (≥ 4 years) |

| Rising Professional Liability Costs | −0.4% | Global; concentrated in litigious markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Perceived Job and Income Instability

Per diem roles typically exclude guaranteed hours, employer-sponsored benefits, and retirement funding. Nurses with fixed financial obligations often favor stable salaries even when per diem premiums are attractive. Liability insurance also weighs heavily: combined ratios for medical professional coverage have stayed above 100% since 2013, translating to rising premiums for independent contractors. During economic slowdowns, facilities trim discretionary shifts first, reinforcing the instability narrative. This hesitancy particularly limits adoption in regions with sparse hospital density, where shift opportunities can be sporadic.

Regulatory Limitations on Agency Fees

State oversight is sharpening. New York’s Article 29-K bans buy-out charges and enforces quarterly contract disclosures, while Connecticut, Iowa, and Oregon mandate fee reporting. The federal Travel Nursing Agency Transparency Study Act tasks the GAO with auditing agency practices, foreshadowing national caps. IntelyCare’s USD 0.5 million Massachusetts settlement demonstrates enforcement teeth. These rules compress margins and force costly compliance systems, prompting smaller brokers to exit or sell and nudging the market toward scale players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Hospitals Retain Scale, Home Care Accelerates

Hospitals captured 58.10% of 2025 billings, anchoring the per diem nurse staffing market through sheer volume and continual census swings that necessitate surge coverage. Most tertiary centers rely on daily scheduling algorithms that book per diem nurses 24–48 hours ahead, sustaining predictable demand. Independent clinics and outpatient specialty centers employ per diem staff to cover procedural peaks, though growth remains incremental. Nursing homes and assisted-living operators face persistent attrition and regulatory scrutiny, making them steady but secondary contributors.

The home-health agency segment, growing at 8.34% CAGR, illustrates how payors’ shift from acute to community settings is redirecting nurse hours. CMS’s 2025 mandate that agencies attest to staffing sufficiency before reimbursement effectively embeds per diem supply into compliance workflows. Agencies often pay 10–15% premiums for nurses skilled in wound vac management, complex medication regimens, and chronic-disease coaching, reinforcing segment attractiveness. As remote-monitoring technology spreads, demand for hybrid virtual-and-in-home per diem roles will rise, broadening recruitment pools beyond local commuting distances.

By Nurse Type: RNs Dominate, APRNs Lead Uptick

Registered nurses held 61.85% share in 2025, forming the operational backbone for floor coverage, step-down units, and emergency departments. The per diem nurse staffing market size for RNs is set to expand steadily as hospitals guard against fixed-cost inflation while preserving mandated ratios. Advanced practice registered nurses, though smaller in absolute count, will expand at 8.87% CAGR through 2031 as states broaden scope-of-practice laws and as primary-care gaps widen. The Bureau of Labor Statistics projects 135,500 net new NP roles from 2023 to 2033, a pipeline that per diem agencies are already tapping.

Licensed practical/vocational nurses fill essential long-term care functions, while certified nursing assistants round out basic ADL support. For these tiers, agency demand spikes during flu seasons and infection outbreaks when isolation protocols intensify staffing needs. Nonetheless, reimbursement ceilings in skilled-nursing facilities constrain rate flexibility, tempering growth compared with higher-acuity categories.

By Shift Length: 12-Hour Rotations Prevail, Float Pools Surge

Twelve-hour patterns represented nearly half of all per diem hours logged in 2025 as nurses valued compressed workweeks and hospitals minimized handoffs. Evidence is mounting, however, that 12-hour fatigue undermines productivity and safety, prompting a gradual pivot toward mixed scheduling. Eight-hour and 10-hour rosters are resurfacing in telemetry and medical-surgical wards aiming to curb burnout. Meanwhile, float pool/on-call frameworks will accelerate at 8.55% CAGR, underpinning internal capacity buffers that can redeploy staff across sister facilities on short notice. Such pools synergize with crisis-response contracts, giving systems an in-house first line before escalating to external bookings.

By Scheduling Platform: Agencies Command, Apps Disrupt

Traditional intermediaries controlled 72.90% of 2025 placements thanks to entrenched procurement contracts, credentialing infrastructure, and liability cover. Their grip is loosening as app-based marketplaces expand at 8.98% CAGR, propelled by intuitive mobile UX, instantaneous shift confirmation, and transparent pay breakdowns. The “Uber for nursing” model delivers speed but must still address regulatory vetting, shift no-shows, and clinical-competency assurance before it can displace legacy incumbents entirely. Hybrid strategies are emerging wherein large agencies white-label platform technology to blend high-touch and self-service channels, preserving margin while adding scale.

Geography Analysis

North America generated 45.10% of global revenue in 2025 driven by chronic workforce deficits, stringent staffing mandates, and established per diem ecosystems. The per diem nurse staffing market share for the United States will remain dominant, supported by rapid digital-platform uptake and continuing retirement-wave attrition that outpaces graduation rates. Canada’s universal coverage model and aging demographic reinforce steady demand, while Mexico’s infrastructure upgrades create cross-border agency opportunities.

Europe presents a mature landscape with universal health systems but escalating nurse shortages as baby-boomer caregivers retire. The EU-funded Nursing Action program funnels resources toward recruitment, retention, and mental-health supports, paving space for per diem solutions that offer workload flexibility. Language diversity and rigid labor protections can slow agency credentialing, yet cross-border recognition frameworks are easing mobility. Nordic countries, where work-life balance is paramount, are piloting flexible shift banks that mirror per diem dynamics within collective-bargaining frameworks.

Asia-Pacific, forecast to expand at 7.41% CAGR, benefits from aggressive hospital construction, burgeoning middle classes, and concerted nurse-education investments. The International Council of Nurses underscores severe ratio gaps, particularly in India and Southeast Asia, opening doors for regional agencies and expatriate programs. Mutual recognition of nursing licenses across ASEAN members further lubricates workforce flows. Challenges remain in uneven regulatory enforcement and cultural preference for permanent employment, but urban megacities are quickly adopting app-based gig staffing to handle patient surges.

Competitive Landscape

The field remains moderately concentrated, with the top five vendors accounting for a combined 38% of 2024 billings. Aya Healthcare’s USD 615 million purchase of Cross Country Healthcare illustrates strategic consolidation that fuses technology, client rosters, and geographic reach. AMN Healthcare leverages its Smart Square software to bundle scheduling SaaS with staffing services, capturing sticky, recurring revenue streams. Maxim Healthcare’s 2024 rebrand to Amergis clarifies its identity as it diversifies into education staffing.

Digital entrants such as ShiftMed and IntelyCare are challenging fee structures through algorithmic pricing, though compliance costs and litigation risks have trimmed headcounts at some platforms. Regional specialists thrive in niche verticals—cardiovascular critical care, dialysis, or rural deployments—where relationship capital outweighs scale. Investors are pouring capital into AI credential-scrubbing, predictive demand analytics, and automated payroll solutions, anticipating margin expansion through operational efficiency. The competitive narrative thus centers on technology adoption, service breadth, and regulatory agility.

Per Diem Nurse Staffing Industry Leaders

Accountable Healthcare Staffing

Cross Country Healthcare

HealthTrust Workforce Solutions (HCA)

Maxim Healthcare Services

AMN Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NPHub secured USD 20 million to modernize nurse-practitioner clinical placements, signaling robust venture appetite for workforce tech.

- February 2025: AMN Healthcare’s Smart Square won Best in KLAS Scheduling for 2025, validating digital workforce management innovations.

- January 2025: WHO launched the EU-funded Nursing Action project to tackle an 18 million-worker gap by 2030.

- December 2024: Aya Healthcare agreed to acquire Cross Country Healthcare for USD 615 million, expanding multichannel staffing reach.

- September 2024: Ingenovis Health consolidated leadership under Catherine Pearson to boost efficiency across specialty brands.

- April 2024: ShiftMed acquired CareerStaff Unlimited, gaining a seven-year contract to staff 1,400 Genesis HealthCare sites.

Global Per Diem Nurse Staffing Market Report Scope

As per the scope of the report, per diem nurse staffing refers to how the nurse is hired, i.e., on a day-to-day basis. Per Diem nurses work on a variety of units and sometimes in a variety of hospitals and other healthcare facilities. The Per Diem Nurse Staffing Market is Segmented by End User (Hospitals, Independent Clinics, and Nursing Homes) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value in USD for the above segments.

| Hospitals |

| Independent Clinics |

| Nursing Homes |

| Home Healthcare Agencies |

| Other Long-Term Care Facilities |

| Registered Nurses (RN) |

| Licensed Practical/Vocational Nurses (LPN/LVN) |

| Certified Nursing Assistants (CNA) |

| Advanced Practice Registered Nurses (APRN) |

| 8-Hour Shifts |

| 10-Hour Shifts |

| 12-Hour Shifts |

| Float Pool / On-Call |

| Traditional Staffing Agencies |

| App-Based Marketplaces |

| Internal Hospital Float Pools |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By End User | Hospitals | |

| Independent Clinics | ||

| Nursing Homes | ||

| Home Healthcare Agencies | ||

| Other Long-Term Care Facilities | ||

| By Nurse Type | Registered Nurses (RN) | |

| Licensed Practical/Vocational Nurses (LPN/LVN) | ||

| Certified Nursing Assistants (CNA) | ||

| Advanced Practice Registered Nurses (APRN) | ||

| By Shift Length | 8-Hour Shifts | |

| 10-Hour Shifts | ||

| 12-Hour Shifts | ||

| Float Pool / On-Call | ||

| By Scheduling Platform | Traditional Staffing Agencies | |

| App-Based Marketplaces | ||

| Internal Hospital Float Pools | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the per diem nurse staffing market?

The per diem nurse staffing market size is USD 17.08 billion in 2026 and is forecast to reach USD 23.74 billion by 2031.

How fast is demand for per diem nurses expected to grow?

Aggregate revenue is projected to expand at a 6.79% CAGR between 2026 and 2031 as providers deepen contingency pools.

Which end-user segment is expanding the quickest?

Home healthcare agencies show the highest growth at an 8.34% CAGR, reflecting the migration of care to community settings.

Why are advanced practice registered nurses in high demand?

APRNs fill primary-care and high-acuity roles amid physician shortages and are forecast to grow at 8.87% CAGR through 2031.

What technology trends are reshaping staffing?

AI-driven scheduling platforms cut fill times, improve credential checks, and are winning industry awards for workforce optimization.

Which region offers the fastest growth potential?

Asia-Pacific leads with a 7.41% CAGR as infrastructure investment and nursing shortages converge to stimulate flexible staffing adoption.

Page last updated on: