Tele Intensive Care Unit Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 5.52 Billion |

| Market Size (2031) | USD 11.01 Billion |

| Growth Rate (2026 - 2031) | 14.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

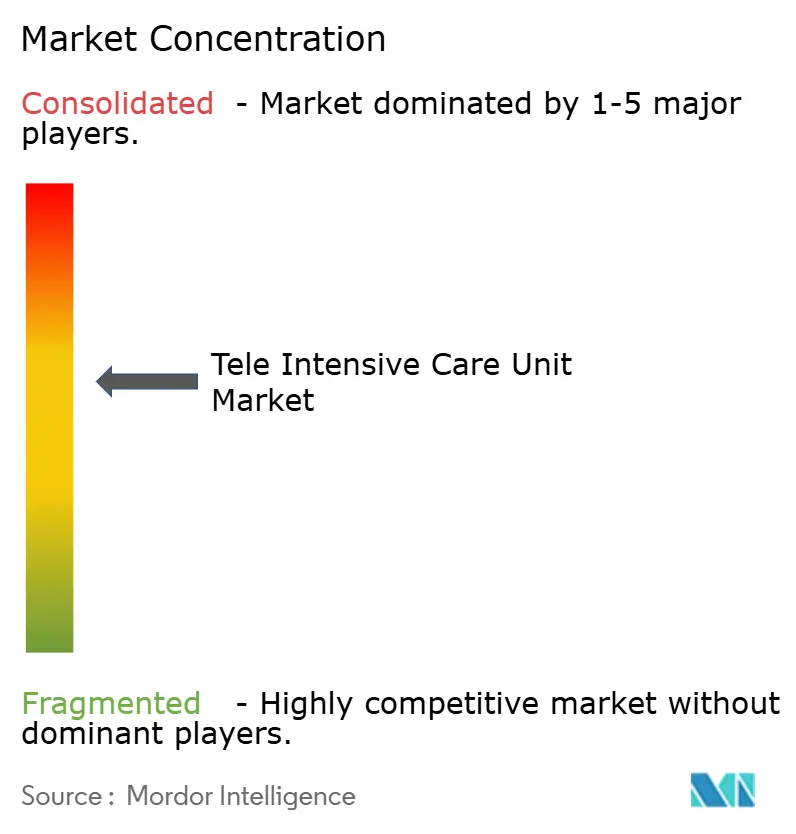

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tele Intensive Care Unit Market Analysis by Mordor Intelligence

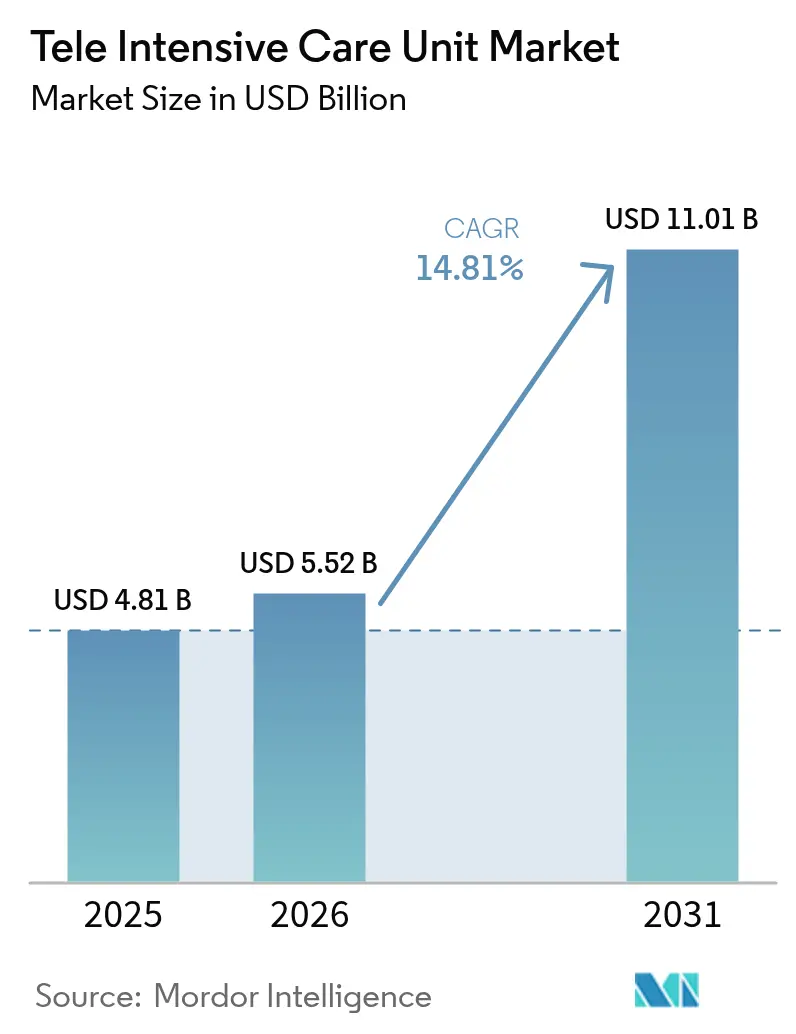

The Tele Intensive Care Unit Market size was valued at USD 4.81 billion in 2025 and estimated to grow from USD 5.52 billion in 2026 to reach USD 11.01 billion by 2031, at a CAGR of 14.81% during the forecast period (2026-2031).

Growth is fueled by persistent intensivist shortages, the need to extend critical-care expertise into underserved regions, and rapid progress in real-time connectivity technologies. North America retains its leadership position by combining mature hospital networks with payer policies that reimburse virtual critical-care encounters, while Asia-Pacific records the quickest uptake as health-system investors back5G-ready facilities and remote-monitoring pilots. Hybrid command-center models gain support because they couple centralized specialists with on-site clinical teams, moderating cost while lifting clinical performance. New5G deployments inside hospitals have lowered round-trip latency to under10ms, which is enabling high-definition imaging review, robot-assisted ultrasound, and continuous video analytics during admissions. Although reimbursement cliffs and high start-up costs temper near-term adoption, public grants and the permanence of post-pandemic telehealth waivers continue to widen the business case for virtual critical care across hospital sizes.

Key Report Takeaways

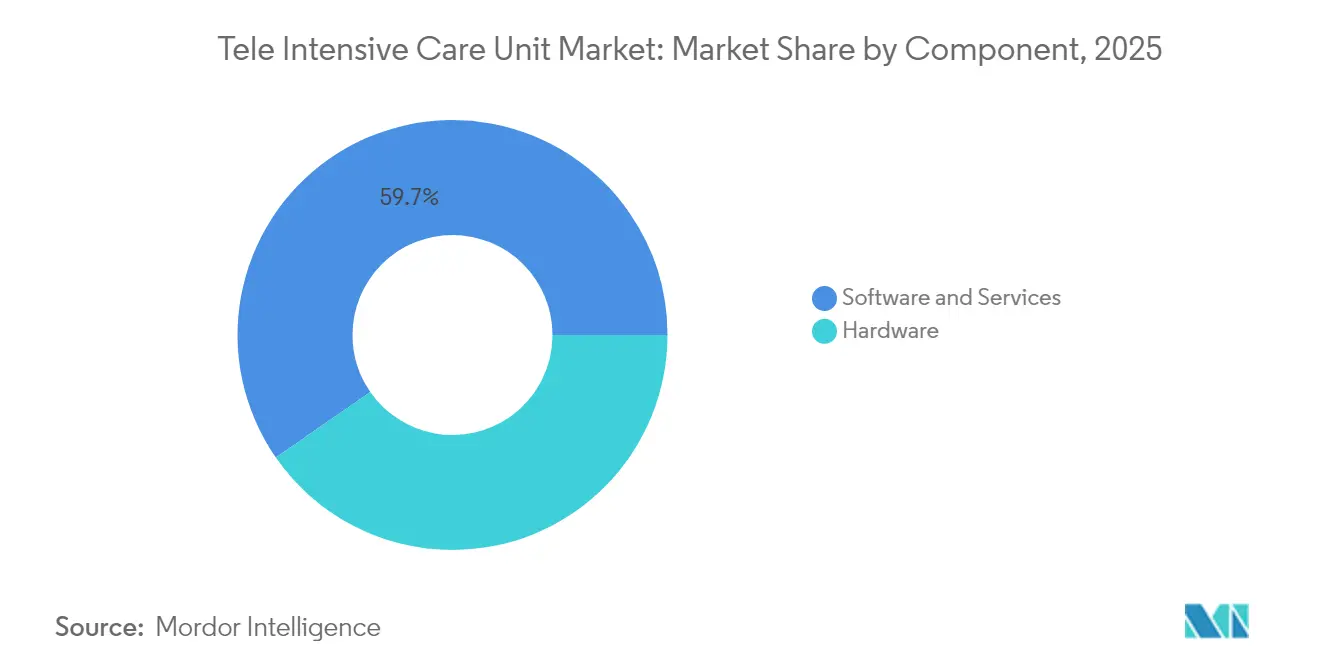

- By component, software & services held 59.65% of the tele-intensive care unit market share in 2025, while smart cameras are projected to expand at a 13.92% CAGR through 2031.

- By model type, centralized model commanded 50.30% revenue share in 2025; hybrid configurations are expected to post the fastest 15.24% CAGR to 2031.

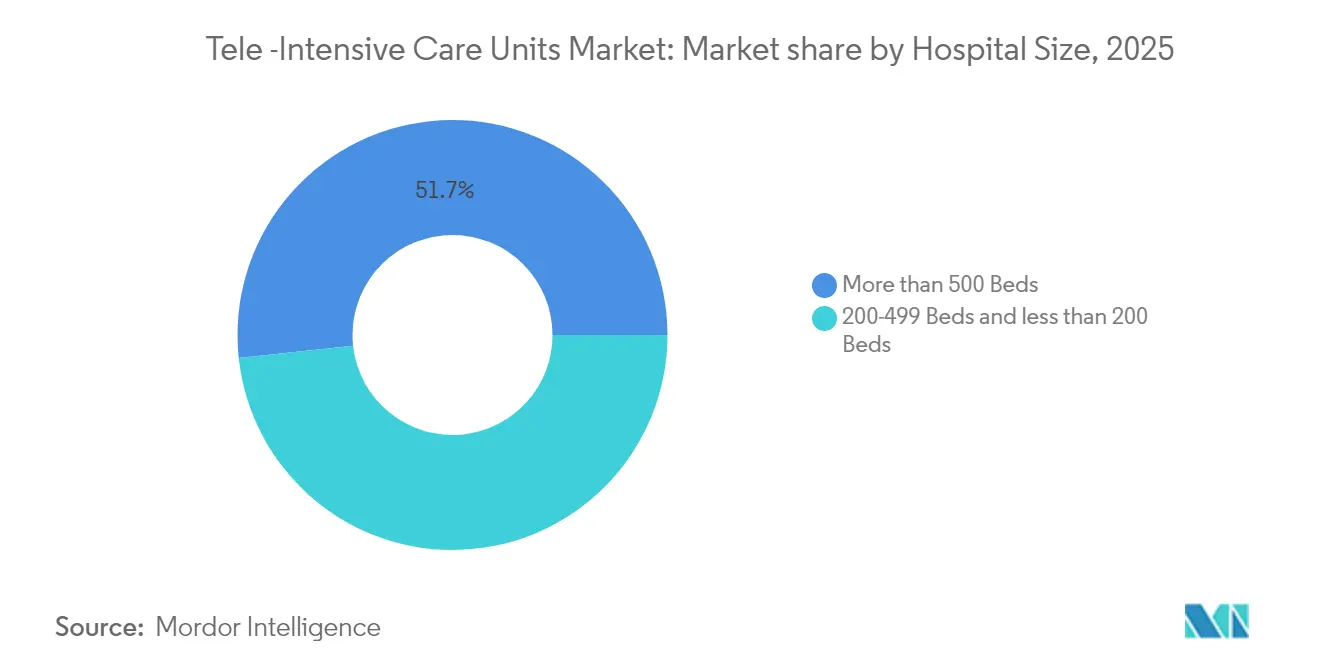

- By hospital size, facilities with more than 500 beds controlled 51.70% share of the tele-intensive care unit market size in 2025, yet 200-499 bed hospitals are forecast to grow at 14.12% CAGR to 2031.

- By geography, North America led with 43.10% revenue share in 2025, and Asia-Pacific is projected to register a 15.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tele Intensive Care Unit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Analysis |

|---|---|---|---|

| Aging Population Driven Critical Care Demand Surge | +3.2 | Global, with highest impact in North America and Europe | Long term (≥5 yrs) |

| Accelerated Adoption of 5G-Ready Hospital Networks | +2.1 | North America, Europe, and developed APAC | Medium term (≈3-4 yrs) |

| Increasing Demand for Remote Patient Monitoring | +3.5 | Global | Short term (≤2 yrs) |

| Large-Scale Public Tele-ICU Grants | +1.8 | North America and Europe | Medium term (≈3-4 yrs) |

| Post-COVID Remote Monitoring Policies Becoming Permanent | +2.7 | Global, with highest impact in North America | Short term (≤2 yrs) |

| Chronic Intensivist Shortage Triggering Outsourced e-ICU Staffing in Europe | +2.4 | Europe, with spillover to North America and APAC | Medium term (≈3-4 yrs) |

| Source: Mordor Intelligence | |||

Aging Population Intensifies ICU Demand

Demand for critical-care beds climbs as older adults represent a growing share of admissions. The American Hospital Association notes that people aged 65 and older will surpass 20% of the United States population by 2030, a shift that elevates chronic disease complexity and raises ICU utilization [1]Source: American Hospital Association, “Fact Sheet: Telehealth,” aha.org . Hospitals report rising ventilation hours and longer monitoring requirements, prompting administrators to add tele-ICU coverage across multisite systems. Tele-ICU programs show mortality reductions of up to 40% in recent multisite cohorts because remote intensivists can intervene earlier during deterioration events criticalcaremedicine. These outcomes strengthen the business case for virtual oversight in geriatric hotspots and encourage payers to maintain reimbursement codes tied to population.

Accelerated Adoption of 5G-Ready Hospital Networks

Hospital-owned 5G stand-alone networks now carry bedside video, imaging, and device telemetry with sub-10 ms latency, a threshold that supports telesurgery guidance and continuous computer-vision analytics. Finland’s Hola 5G Oulu project recorded instantaneous transmission of MRI sequences and live ultrasound streams, reducing clinical decision lag and driving new quality benchmarks. Singapore’s National University Health System achieved 1 Gbps downlink speeds on a hybrid 5G enterprise network, paving the way for bandwidth-heavy tele-ICU dashboards. Early adopters report 44.5% fewer patient falls after integrating smart cameras and 5G backbones, highlighting the operational impact of seamless, high-definition video monitoring valleyhealth. Capital budgets increasingly earmark 5G upgrades as network resilience becomes a prerequisite for advanced virtual-care services.

Remote Patient Monitoring Adoption

Continuous, cloud-connected biosensors and ceiling-mounted smart cameras extend surveillance beyond traditional ICUs to step-down and home settings. AI-enabled analytics now detect hemodynamic instability up to six hours before conventional vital-sign thresholds, allowing pre-emptive therapy that can avert transfers into high-acuity units. Wearable devices linked to electronic records improve chronic-disease tracking while reducing unscheduled visits, a trend that eases staff shortages. A 2025 study on hypertension monitoring demonstrated a 22.2% positive return on investment once patient adherence exceeded 55%, underscoring the financial viability of RPM-driven tele-ICU pathways. Hospital groups are therefore bundling remote patient monitoring platforms with central command centers to optimize workforce allocation.

Post-COVID Telehealth Waivers Become Permanent

Temporary flexibilities extended during the pandemic now influence permanent payment policy. The Centers for Medicare & Medicaid Services kept core waivers through March 2025, including permission for patients to receive tele-ICU services from non-rural homes[2]Source: Centers for Medicare & Medicaid Services, “Medicare Learning Network Newsletter,” cms.gov . Legislative coalitions aim to make these geographic waivers indefinite, citing reductions in readmission rates for patients supported by home monitoring programs. New billing codes in the 2025 Medicare Physician Fee Schedule cover advanced primary-care integration with tele-ICU dashboards, broadening the eligible clinician pool. Hospitals scale virtual critical-care lines faster because reimbursement visibility now spans the full forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Analysis |

|---|---|---|---|

| Limited Reimbursement | -2.3 | Global, with highest impact in emerging markets | Medium term (≈3-4 yrs) |

| High Cost of Treatment and Expensive Setup | -2.5 | Global, with highest impact in emerging markets | Short term (≤2 yrs) |

| Data-Integration Silos Between EMR Vendors & Tele-ICU Platforms | -1.9 | Global, with highest impact in fragmented healthcare systems | Medium term (≈3-4 yrs) |

| Nurse & Intensivist Resistance to Remote Oversight in Tier-2 Hospitals | -1.6 | APAC and emerging markets, with moderate impact in Europe | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

High Implementation Cost

Launch budgets still approach USD 50,000 to 100,000 per monitored bed when factoring servers, audiovisual endpoints, integration software, and 24 × 7 clinical staffing. University pilot sites report initial capital outlays above USD 1.1 million and annual operating expenses near USD 2.5 million, figures that deter smaller hospitals from full-scale adoption. Despite an incremental cost-effectiveness ratio of USD 45,320 per quality-adjusted life year, financial sustainability hinges on patient volume. Break-even models show large centers recoup investment within three years, whereas sub-200-bed facilities often require grant support to offset start-up costs. Vendors respond with subscription-based packages and shared-service contracts aimed at lowering the entry barrier.

Limited Reimbursement Variability

The 2025 Medicare conversion factor falls by 2.8%, trimming professional-fee margins for tele-ICU physicians and intensifying pressure on hospital-based groups. Private payers differ on eligible originating sites and coding rules, with modifiers such as GQ, GT, or 95 applied inconsistently. Medicaid programs likewise vary by state, creating administrative complexity and revenue uncertainty for multistate health systems. Policy analysts warn that abrupt reversals of audio-only allowances could exclude vulnerable patient cohorts and diminish return on investment. This uncertainty slows multi-hospital rollouts and encourages phased deployments aligned with favorable payer mixes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software & Services Dominate as Smart Cameras Accelerate

Software & Services contributed 59.65% of the tele-intensive care unit market size in 2025 because remote intensivist coverage, nursing triage, and analytics support remain indispensable for continuous patient oversight. Outsourcing clinical expertise lets hospital administrators compensate for regional workforce gaps while standardizing practice across networks. Vendors bundle 24 × 7 coverage, quality-metric reporting, and change-management programs, raising switching costs and reinforcing service revenues. At the same time, AI-enabled workflow engines now filter waveform and laboratory streams, reducing alert fatigue and allowing a single clinician to supervise a larger census.

Hardware revenue stems from physiological monitors, ceiling-mounted cameras, and command-center displays. Smart cameras stand out, expanding at a 13.92% CAGR as computer-vision algorithms classify posture, detect apnea events, and trigger fall alerts with macro F1-scores above 0.92. Software portfolios increasingly integrate decision-support modules such as Multiscale Vision Transformers capable of estimating nursing-activity scores, which helps staffing managers fine-tune resource deployment. This convergence of hardware, software, and services heightens differentiation among vendors and sustains long-term subscription growth inside the tele-intensive care unit market.

By Model Type: Hybrid Configurations Gain Momentum

Centralized command centers captured 50.30% of 2025 revenue because pooled intensivists can supervise multiple spoke hospitals from one location, securing economies of scale and standard protocols criticalcaremedicine. Evidence from multi-site rollouts links centralized decision authority with a 23% reduction in hospital mortality within three years, supporting payer negotiations for outcome-based contracts.

The hybrid model is forecast to record a 15.24% CAGR, making it the fastest-growing configuration in the tele-intensive care unit market. Under this structure, bedside teams retain autonomy for routine decisions while escalating complex cases to remote specialists, balancing clinician acceptance with resource efficiency. AI-driven predictive analytics embedded in hybrid networks facilitate early sepsis alerts and ventilator-weaning optimization. Decentralized arrangements persist in academic ecosystems that already house dispersed subspecialists; however, capacity constraints and cost pressures steer most expansion plans toward hybrid hubs.

By Hospital Size: Mid-Sized Facilities Adopt Rapidly

Hospitals with more than 500 beds dominated 2025 revenue at 51.70%, leveraging existing IT staff, enterprise networks, and high patient flow to justify command-center investments. Many large systems serve as spokes for smaller affiliated hospitals, deepening referral ties and capturing downstream specialist revenue.

Mid-sized hospitals in the 200–499 bed range are projected to expand tele-intensive care unit market size at a 14.12% CAGR as leaders seek to maintain local admissions while meeting quality benchmarks. Economic models show break-even points within four years when these hospitals reach 150 monitored beds, making tele-ICU financially attractive without major building projects. Facilities below 200 beds rely on grant funding and subscription models to launch limited virtual coverage during nights and weekends. As vendors roll out cloud-native platforms that remove on-premise server requirements, entry costs fall, supporting broader adoption across community settings.

Geography Analysis

North America held 43.10% of global revenue in 2025 and remains the center of commercial innovation in the tele-intensive care unit market. U.S. hospital networks deploy virtual critical-care dashboards that integrate electronic medical records with live camera feeds, providing clinicians unified patient views at local and remote sites. The American Hospital Association supports legislation to eliminate geographic restrictions permanently and to extend provider eligibility, moves that would further stabilize reimbursement. The Department of Veterans Affairs funds access points in rural communities, bringing specialist oversight to dispersed veteran populations.

Asia-Pacific is forecast to grow at 15.42% CAGR, the fastest among all regions. Health ministries in Singapore, Australia, and South Korea subsidize 5G private networks inside tertiary hospitals, clearing capacity for high-bandwidth tele-ICU video streams. Thailand pilots telemedicine kiosks to route non-critical cases away from crowded urban centers. Local start-ups partner with academic centers to deliver multilingual user interfaces that address cultural and regulatory heterogeneity.

Europe occupies a solid third position, supported by national e-health strategies in 40 countries and sustained investment from public payers. Projects like Hola 5G Oulu demonstrate clinical utility for sub-second data exchange, inspiring similar initiatives in Germany and Spain. The European Society of Intensive Care Medicine highlights persistent intensivist shortages, prompting outsourced e-ICU staffing contracts that allow hub hospitals to supervise smaller spokes across borders . EU programs such as Thera4Care channel research funds into AI-enabled theranostics, which dovetail with tele-ICU analytics to create integrated care pathways.

The Middle East and Africa and South America represent smaller but accelerating opportunities. Gulf states showcase digital-first hospitals, and regional exhibitions like Arab Health feature command-center demonstrations that link operating rooms with remote anesthesiologists. Latin American ministries negotiate public-private partnerships that equip provincial hospitals with cloud-based monitoring platforms, aligning with workforce-development goals.

Competitive Landscape

Competition is moderately concentrated, with diversified imaging vendors, telehealth platforms, and cloud service providers vying for enterprise contracts. Philips couples patient-monitoring hardware with AI-enabled clinical-decision software and recently unveiled helium-free MRI scanners designed to integrate with tele-ICU dashboards, cutting service interruptions during remote consultations. GE HealthCare collaborates with AWS to embed generative AI inside its Command Center software, which reduces bed-assignment times by 66% at early adopter sites. Teladoc Health enhances its Prism platform by adding AI-enabled clinical transcription and automated referrals, strengthening links between virtual critical care and community providers.

Strategic partnerships dominate growth agendas. Philips joined ST Engineering to co-develop cybersecurity-hardened digital-health suites for Asia-Pacific hospitals stengg. GE HealthCare forged a seven-year pact with Sutter Health that will upgrade imaging fleets across California, cementing an installed base receptive to tele-ICU overlays. Avel eCare’s acquisition of Amwell Psychiatric Care extends behavioral-health capabilities into 46 states, positioning the firm to provide ancillary psychiatry consults to ICU patients presenting with delirium or withdrawal.

White-space opportunities focus on underserved rural hospitals where capital budgets lag. Vendors test subscription models bundled with analytics licenses and hardware leasing to lower adoption barriers. Early pilots that integrate AI-powered hybrid chatbots report 25% fewer readmissions and 30% higher patient engagement, hinting at next-generation service layers that could differentiate offerings.

Tele Intensive Care Unit Industry Leaders

Inova

INTeLeICU

InTouch Technologies Inc.

Koninklijke Philips NV

Advanced ICU Care

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Philips agreed to sell its Emergency Care business to Bridgefield Capital to focus on high-growth patient-monitoring markets.

- January 2025: GE HealthCare launched a seven-year strategic collaboration with Sutter Health to expand access to AI-powered imaging across California.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the tele-intensive care unit (tele-ICU) market as all integrated hardware, software, and managed service bundles that enable real-time, off-site monitoring of critically ill patients through high-bandwidth audio-visual links and decision-support dashboards. The value estimate captures only new system deployments and annual support revenues booked by vendors or health-system command centers across hospitals of every bed size worldwide.

Scope exclusion: post-acute home telemetry kits and single-function remote patient monitors that are not licensed for ICU workflows are left outside the model.

Segmentation Overview

- By Component

- Hardware

- Software & Services

- By Model Type

- Centralized Model

- Decentralized Model

- Hybrid / Distributed Hub-and-Spoke Model

- By Hospital Size

- More than 500 Beds

- 200–499 Beds

- Less than 200 Beds

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia- Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and pulse surveys with intensivists, biomedical engineers, hospital procurement leads, and regional tele-health coordinators across North America, Europe, Asia-Pacific, and the Gulf were conducted. Their insights refined adoption lags, average service fees, and replacement cycles, giving us confidence to reconcile desktop findings with frontline realities.

Desk Research

Mordor analysts began with hospital infrastructure datasets from organizations such as the American Hospital Association, Eurostat, and the OECD, which helped us profile the universe of staffed ICU beds. Policy updates from CMS and India's National Tele-health Authority clarified reimbursement triggers that influence deployment timing. Peer-reviewed evidence accessed through PubMed and IEEE Xplore described clinical efficacy rates and average connected-bed costs.

To size vendor revenues, we screened company filings, investor decks, and selected news archives in Dow Jones Factiva, supplementing them with customer counts retrieved from D&B Hoovers. These desk inputs built the structural backbone of our market model; many additional public and subscription sources were consulted, though not exhaustively listed here.

Market-Sizing & Forecasting

A top-down reconstruction began by multiplying the global ICU bed inventory with tele-ICU penetration rates that vary by hospital size and broadband availability, followed by region-specific average revenue per connected bed. Supplier roll-ups and channel checks served as bottom-up reasonableness tests before values were finalized. Key variables incorporated include intensivist vacancy ratios, 5G coverage growth, ICU mortality differentials, regulated tele-consult tariff schedules, and capital cost curves for cameras and servers. Multivariate regression, stress-tested through three econometric scenarios, projects values through 2030 while capturing sensitivity to policy or technology shocks.

Data Validation & Update Cycle

Outputs are subjected to variance scans against historical adoption curves, cross-checked by a second analyst, and cleared in a weekly review huddle. Reports are fully refreshed each year, with interim updates released if reimbursement rules, major mergers, or public-health emergencies materially shift demand.

Why Mordor's Tele Intensive Care Unit Baseline Commands Reliability

Published figures often diverge because firms pick different component mixes, revenue recognition rules, and update cadences.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.81 B (2025) | Mordor Intelligence | - |

| USD 4.86 B (2025) | Global Consultancy A | excludes service fees below five-year contracts |

| USD 6.27 B (2025) | Research Publisher B | folds in remote ward-monitoring platforms that sit outside ICUs |

| USD 3.50 B (2023) | Trade Journal C | hardware-only baseline, older currency conversion |

These comparisons show that once like-for-like scope and currency choices are harmonized, Mordor's balanced mix of desk evidence and practitioner validation produces a dependable, decision-ready baseline that clients can trace back to transparent assumptions and replicable steps.

Key Questions Answered in the Report

How big is the Tele Intensive Care Unit Market?

The Tele Intensive Care Unit Market size is expected to reach USD 5.52 billion in 2026 and grow at a CAGR of 14.81% to reach USD 11.01 billion by 2031.

What is the current Tele Intensive Care Unit Market size?

In 2026, the Tele Intensive Care Unit Market size is expected to reach USD 5.52 billion.

Which is the fastest growing region in Tele Intensive Care Unit Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

What years does this Tele Intensive Care Unit Market cover, and what was the market size in 2025?

In 2025, the Tele Intensive Care Unit Market size was estimated at USD 5.52 billion. The report covers the Tele Intensive Care Unit Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Tele Intensive Care Unit Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: