Hepatitis Diagnostic Test Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 4.98 Billion |

| Market Size (2031) | USD 6.46 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

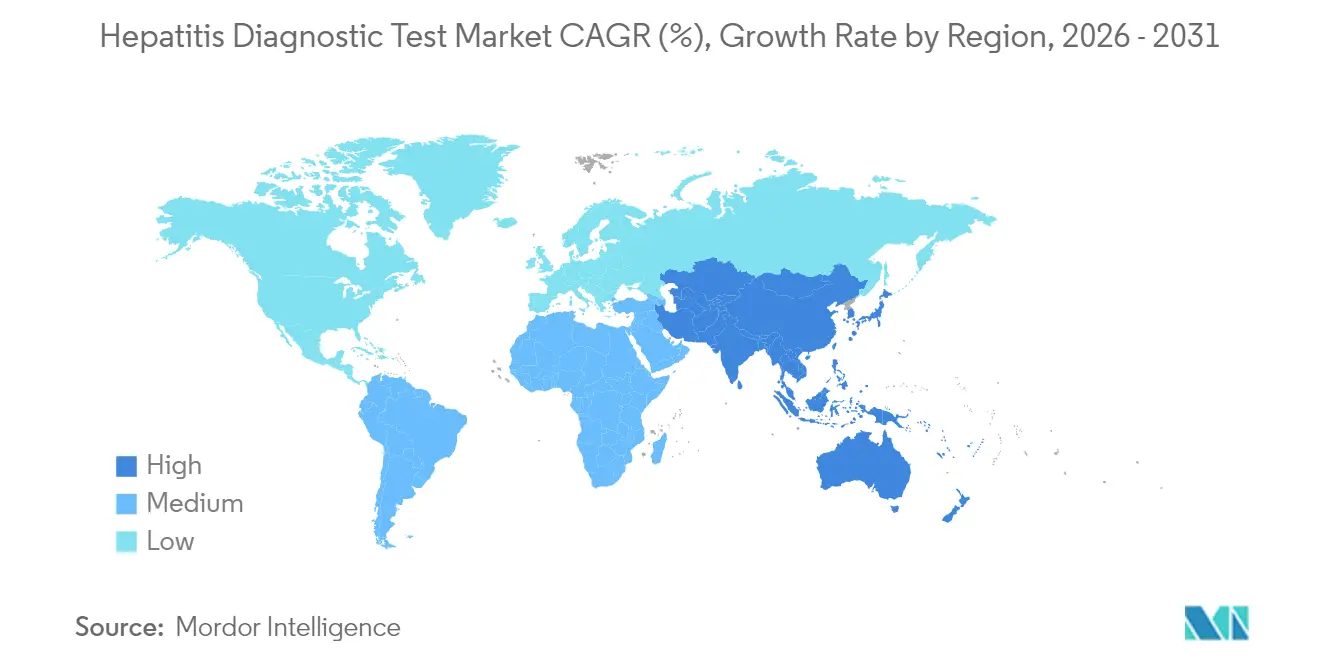

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hepatitis Diagnostic Test Market Analysis by Mordor Intelligence

Hepatitis diagnostic test market size in 2026 is estimated at USD 4.98 billion, growing from 2025 value of USD 4.73 billion with 2031 projections showing USD 6.46 billion, growing at 5.32% CAGR over 2026-2031. Demand is rising as governments race to meet the WHO goal of eliminating viral hepatitis as a public-health threat by 2030. Yet, diagnosis gaps remain wide—only 13% of chronic hepatitis B and 36% of hepatitis C cases are identified today. Technology is shifting fast toward molecular and AI-enabled platforms, exemplified by the FDA-cleared Cepheid Xpert HCV RNA finger-stick test that delivers results in about one hour. Regional growth imbalances are stark: North America leads with 40.34% 2024 revenue, while Asia-Pacific is the growth engine at 6.46% CAGR to 2030. Competitive intensity is moderate as global leaders leverage scale in molecular diagnostics and smaller firms push microfluidic and AI-driven point-of-care systems.

Key Report Takeaways

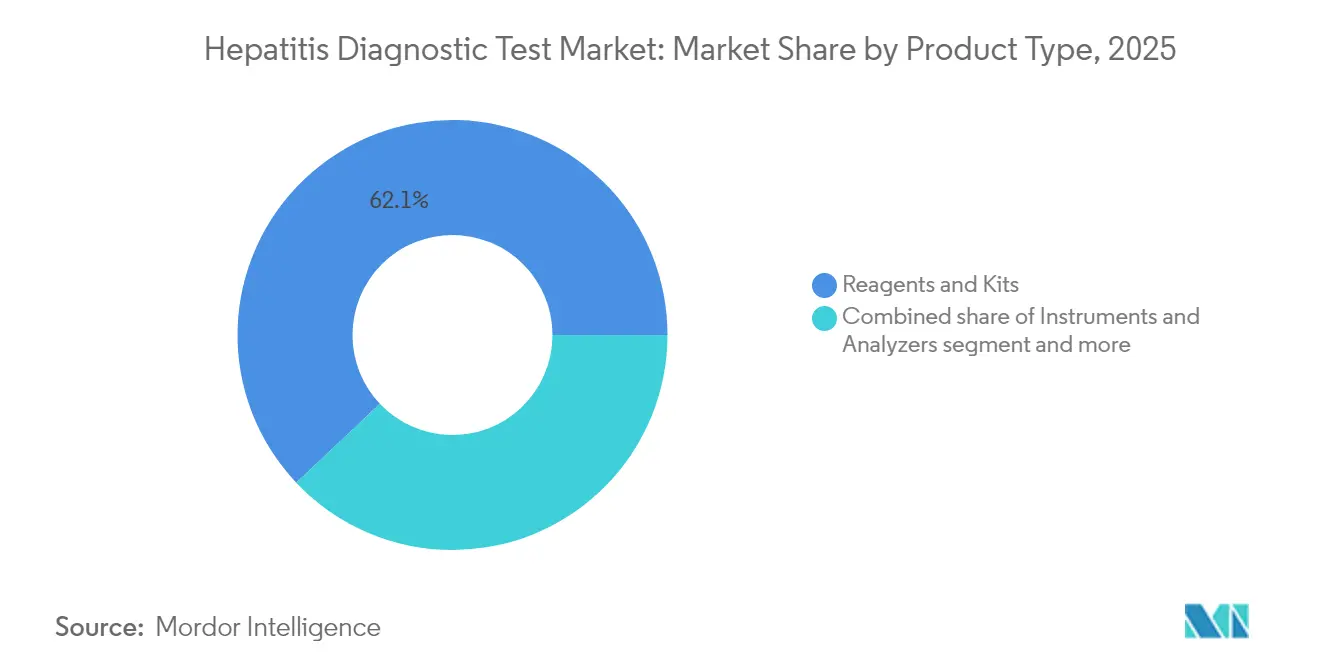

- By product type, reagents and kits led with 62.05% of the hepatitis diagnostic test market share in 2025, whereas software and services are projected to expand at a 6.21% CAGR through 2031.

- By disease type, hepatitis B testing captured 48.40% of the hepatitis diagnostic test market size in 2025; the “other hepatitis” segment (A, E, and D) is forecast to register a 6.33% CAGR to 2031.

- By technology, serology accounted for 45.90% of the hepatitis diagnostic test market in 2025, while next-generation sequencing panels are expected to advance at a 6.52% CAGR between 2026 and 2031.

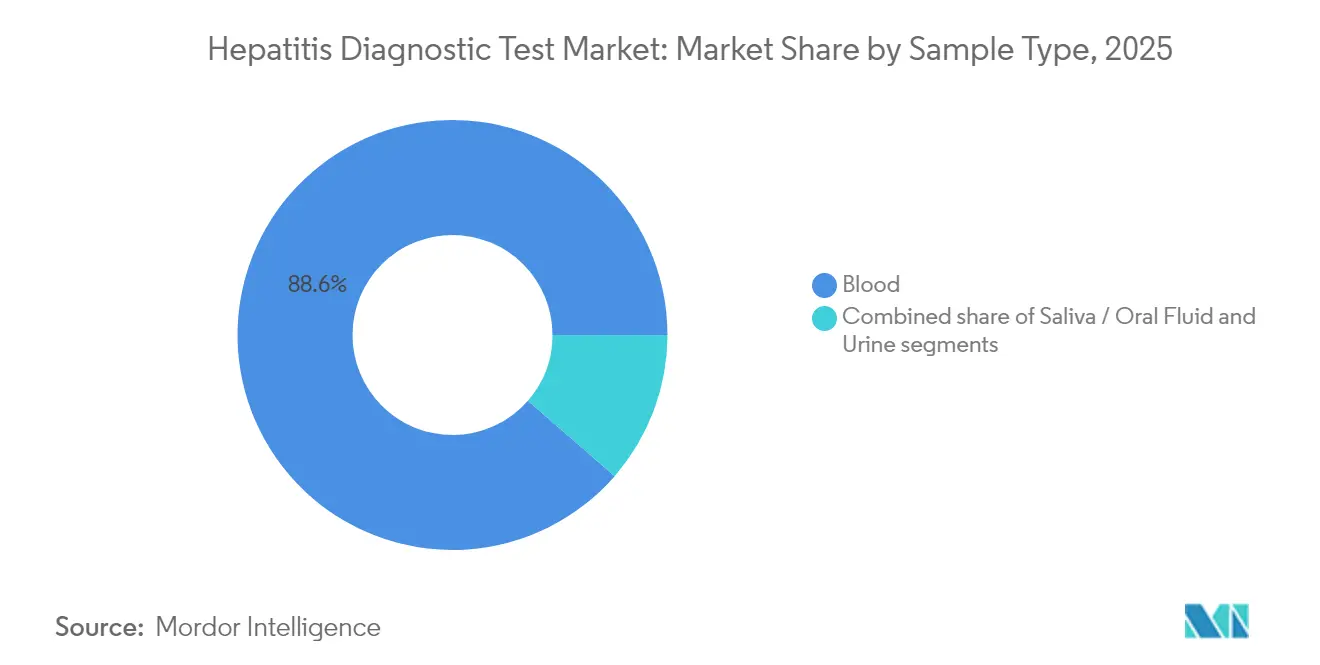

- By sample type, blood testing commanded an 88.60% share of the hepatitis diagnostic test market in 2025, and saliva/oral fluid collection is set to grow at a 7.24% CAGR to 2031.

- By test setting, hospital laboratories held 53.55% revenue share in 2025; home testing and self-collection is anticipated to rise at 6.15% CAGR during the forecast period.

- By geography, North America dominated with 39.88% revenue share in 2025, whereas Asia-Pacific remains the fastest-growing region at 6.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hepatitis Diagnostic Test Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global HBV & HCV Prevalence | +1.2% | Global, with highest impact in Asia-Pacific and sub-Saharan Africa | Long term (≥ 4 years) |

| Rapid Migration from Serology to High-Sensitivity Molecular Platforms | +1.0% | Global, led by developed markets, expanding to emerging economies | Medium term (2-4 years) |

| Expansion of Government-Funded Screening & Vaccination Programs | +0.8% | North America, Europe, with emerging impact in Asia-Pacific | Medium term (2-4 years) |

| Emergence of Microfluidic POC Viral-Load Analyzers | +0.6% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| AI-Assisted Elastography Improving Non-Invasive Liver Assessment | +0.4% | North America, Europe, with gradual expansion to Asia-Pacific | Long term (≥ 4 years) |

| Adoption of Self-Collection Dried-Blood-Spot Kits for Remote Testing | +0.3% | Global, particularly relevant for rural and underserved populations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global HBV & HCV Prevalence

More than 254 million people live with chronic hepatitis B and 50 million with hepatitis C, with Asia-Pacific bearing 75% of chronic HBV cases. Rising incidence keeps diagnostic demand high, particularly in China where new HCV infections are projected to reach 17.92 per 100,000 by 2030[1]Guo Tian, “Epidemiological trends of hepatitis C incidence and death in Mainland China between 2004 and 2018 and its predictions to 2030,” BMC Infectious Diseases, bmcinfectdis.biomedcentral.com. Regional disparities linger—southern Korea still reports elevated HCV prevalence[2]Hwa Young Choi, “Temporal and geospatial patterns of hepatitis C virus prevalence: a longitudinal examination using national health insurance service data in the Republic of Korea (2005–2022),” BMC Public Health, bmcpublichealth.biomedcentral.com despite national declines. Uncommon genotypes such as HCV 1c dominate among chronic kidney-disease patients in West Bengal[3]Sagnik Bakshi, “Impact of hepatitis C virus genotype on the efficacy of the direct-acting antivirals in chronic kidney disease patients in West Bengal, India,” BMC Infectious Diseases, bmcinfectdis.biomedcentral.com, India, underscoring the need for robust genotyping. Combined, these patterns ensure a sustained base of at-risk patients requiring accurate and repeat testing.

Migration from Serology to High-Sensitivity Molecular Platforms

Targeted next-generation sequencing (NGS) now detects hepatitis viruses, even in extrahepatic tissue, where classical assays fail. High-throughput sequencing also tracks resistance-associated variants such as A1343V in hepatitis E during treatment. Artificial intelligence tools enable high-accuracy liver disease diagnosis with faster turnaround times and lower costs. Regulatory support accelerates adoption: the FDA reclassified HBV assays from Class III to Class II, streamlining the 510(k) pathway. As platforms migrate to clinics and community settings, the hepatitis diagnostic test market experiences a notable increase.

Government-Funded Screening & Vaccination Programs

The U.S. Viral Hepatitis National Strategic Plan proposes USD 12.3 billion in elimination funding, including universal HCV screening for adults aged 18-79. The WHO’s 2024 HBV guidance[4]World Health Organization, “WHO Publishes Updated Guidelines on Hepatitis B,” World Health Organization, who.int expands treatment eligibility and stresses point-of-care viral-load testing to close diagnosis gaps. Egypt’s previous HCV elimination model achieved a 90% drop in active infections via mass testing, providing a playbook for emerging economies. Funding boosts and policy alignment collectively advance testing volumes, reinforcing long-term growth in the hepatitis diagnostic test market.

Emergence of Microfluidic Point-of-Care Viral-Load Analyzers

Palm-sized wireless elastography devices now correlate strongly (r = 0.975) with conventional systems while boosting portability. Integrated microfluidic instruments like iPonatic cut total processing time to 30 minutes and deliver AUC > 0.98 for pathogen detection. In Ghanaian clinics, Bioline HCV point-of-care tests scored 88.7 on the System Usability Scale, showing readiness for routine use. Wearable bioadhesive ultrasound devices even enable 48-hour liver stiffness monitoring in preclinical models. These innovations shorten diagnostic turnaround and open new decentralized channels for the hepatitis diagnostic test market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Per-Test Cost of Molecular Assays in Low-Income Settings | -0.9% | Sub-Saharan Africa, South Asia, rural areas in emerging markets | Long term (≥ 4 years) |

| Regulatory Ambiguity Around Direct-To-Consumer Viral-Load Kits | -0.8% | North America, Europe, developed markets with established DTC frameworks | Short term (≤ 2 years) |

| Undetected Occult Infections Causing False-Negatives in Immunocompromised Patients | -0.7% | Global, with higher impact in regions with high HIV prevalence and organ transplant centers | Medium term (2-4 years) |

| Weak Cold-Chain Logistics for Sample Transport in Remote Areas | -0.6% | Rural areas globally, particularly in tropical and sub-tropical regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Per-Test Cost of Molecular Assays in Low-Income Settings

Surveys across 23 low- and middle-income countries confirm that many programs still limit hepatitis testing to blood donors because virological assays remain unaffordable. Complex confirmation algorithms push per-patient costs well beyond those of single-step serology. Product developers face an innovation-to-access gap, as environmental factors and regulatory fragmentation raise validation expenses. Until tiered pricing, pooled procurement or subsidy models expand, penetration of advanced platforms will lag in high-burden but cash-strapped markets.

Weak Cold-Chain Logistics for Sample Transport in Remote Areas

Audits in Ghana showed 53.8% of primary clinics experienced stock-outs of essential diagnostics due to supply-chain weaknesses, with compliance scoring just 53.5%. Molecular assays are especially temperature-sensitive, and tropical climates undermine sample integrity during transport, risking false results. While dried-blood-spot methods ease the burden, sensitivity gaps persist for some hepatitis markers. Absent sustained investment in integrated specimen-referral networks, cold-chain bottlenecks will continue to constrain the hepatitis diagnostic test market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Software Integration Drives Service Growth

Reagents and kits generated the largest slice of the hepatitis diagnostic test market size in 2025 with 62.05% revenue, underscoring the recurrent-consumables model that underpins laboratory workflows. Instruments benefited from miniaturization trends such as palm-sized elastography, yet capital budgets remained cyclical. Software and services, though still a smaller base, are on track for a 6.21% CAGR to 2031 as laboratories embed AI engines that streamline interpretation and automate reporting. Vendors that link cloud-based analytics to their reagent franchises lock-in customers while creating incremental subscription income.

The reagents segment faces mounting price transparency and generics, but demand persists through continuous innovation in lyophilized molecular master mixes and multiplex point-of-care kits. Instrument vendors increasingly bundle connectivity and decision-support dashboards, transforming once-stand-alone analyzers into networked devices. BioMérieux’s January 2025 purchase of SpinChip Diagnostics for EUR 111 million illustrates the race to secure ultra-fast sample-to-answer platforms that fit primary-care settings. As software layers expand, service models shift toward outcome-based contracts, giving the hepatitis diagnostic test market a new revenue vector tied to digital performance.

By Disease Type: Hepatitis B Dominance Faces C Elimination Push

Hepatitis B dominated 2025 revenue with a 48.40% of the hepatitis diagnostic test market share in 2025, mirroring its 254 million-patient prevalence. Testing panels remain complex—pregnant women require HBsAg, anti-HBc and anti-HBs screening every pregnancy under CDC guidance. Hepatitis C volumes are scaling quickly as elimination programs simplify algorithms; the Cepheid finger-stick RNA test enables single-visit diagnosis in primary care. “Other hepatitis” (A, E, D) is the fastest-growing group at 6.33% CAGR, propelled by increasing HAV and HEV outbreaks and new sequencing data confirming wider geographic spread.

Emerging data link specific HAV genotype IIIA and HEV-1 strains to more severe outcomes, pressuring hospitals to upgrade to molecular assays and genotyping. In parallel, hepatitis C elimination funding in the U.S. supports universal screening, driving consistent reagent pull-through. As novel therapies for hepatitis D roll out, demand for HDV reflex testing is likely to rise. This mix of chronic HBV burden, HCV elimination acceleration and broader recognition of other viral hepatitides secures long-term breadth for the hepatitis diagnostic test market.

By Technology: Molecular Platforms Accelerate NGS Adoption

Serology retained 45.90% of the hepatitis diagnostic test market size in 2025, reflecting its role as the first-line screen in many health systems. However, molecular assays and next-generation sequencing are eclipsing serology for confirmation and resistance monitoring, giving NGS the fastest forecast CAGR at 6.52%. The hepatitis diagnostic test market size attached to molecular workflows is set to expand further as 510(k) reclassification lowers U.S. entry barriers for HBV assays. Rapid tests keep traction where budgets are tight, but microfluidic advances now deliver molecular-grade sensitivity in decentralized devices.

NGS adds clinical value by detecting occult infections and characterizing mixed-genotype cases in a single run. Laboratories that already own high-throughput sequencers leverage the same platforms for oncology and microbiology, improving asset utilization. Vendors are bundling AI-curated resistance-variant reports, reducing bioinformatics friction for clinicians. Serology technology is also improving through full automation and higher throughput, ensuring it remains pivotal at massive scale. This dual track keeps every major modality relevant while shifting revenue toward data-rich molecular assays.

By Sample Type: Blood Dominance Challenged by Alternative Matrices

Blood specimens accounted for 88.60% of the hepatitis diagnostic test market share in 2025, solidifying their role as the high-sensitivity standard. Saliva and oral fluid sampling, despite a low base, is projected to grow at a 7.24% CAGR due to patient preference and easier logistics. Finger-stick capillary sampling, as used in the Cepheid Xpert HCV test, demonstrates that blood-based diagnostics can also migrate outside conventional phlebotomy. Dried-blood-spot innovations directly address transport hurdles, although some assays show only 80% sensitivity for HCV.

Saliva testing still faces challenges related to lower viral loads, particularly for HBV detection; however, diagnostic yields for specific antibodies are improving. Urine remains a niche option yet gains research traction for monitoring adherence and screening populations unwilling to provide blood samples. As alternative matrices mature, multiplex assays may combine blood and saliva inputs, creating more versatile sampling workflows. Nonetheless, until analytical sensitivity converges, blood will stay the anchor sample type within the hepatitis diagnostic test market.

By Test Setting: Home Testing Disrupts Traditional Laboratory Models

Hospital laboratories controlled 53.55% of the hepatitis diagnostic test market size in 2025, reflecting comprehensive test menus and tight links to clinical decision-making. Reference labs retain high throughput for genotyping and resistance panels but face margin squeeze from payer price cuts. Home testing and self-collection, though nascent, carries the highest growth at 6.15% CAGR, propelled by consumer demand for privacy and convenience within CLIA-waived frameworks. Point-of-care platforms are gaining share in physician offices and community clinics as one-step molecular cartridges go mainstream.

Digital-first players bundle subscription telehealth for result interpretation, potentially detaching some volume from hospital labs. Blood bank screening remains a regulatory mandate, ensuring a stable, though mature, revenue stream. Physician offices benefit from palm-sized elastography that brings liver fibrosis evaluation closer to primary care. The net effect is a diversifying channel mix where decentralized models grow fastest, pressuring traditional lab operators to add connectivity, same-day turnaround and patient-friendly reporting to protect share.

Geography Analysis

North America held 39.88% of the global hepatitis diagnostic test market share in 2025 due to structured government screening and early adoption of molecular platforms. U.S. policy momentum, including the proposed USD 12.3 billion hepatitis C elimination budget, ensures a steady 4.84% CAGR for the regional hepatitis diagnostic test market. FDA approvals, such as Cepheid’s HCV point-of-care RNA test, accelerate decentralized uptake. Laboratory networks integrate AI-enhanced interpretation pathways like iLFT to boost chronic liver-disease detection, demonstrating a mature ecosystem that rapidly scales innovation.

Europe posts a 5.17% CAGR as harmonized regulations and robust clinical guidelines sustain investment. EASL’s updated hepatitis B management protocol mandates advanced diagnostics, reinforcing demand for molecular panels. Roche’s 18-minute Elecsys PRO-C3 fibrosis test exemplifies the region’s appetite for rapid, non-invasive tools. Yet, care gaps remain, with only 70% of Spanish hospitals performing reflex tests for HBV and under 50% for HDV, spotlighting workflow opportunities. Innovation in wearable ultrasound monitoring further differentiates European offerings.

Asia-Pacific is the fastest-expanding territory at 6.23% CAGR to 2031, fueled by its disproportionate hepatitis burden and rising healthcare investment. China, Japan, and South Korea host half of all chronic HBV patients, creating unparalleled testing demand. China’s HCV incidence is projected to reach 17.92 per 100,000 by 2030, urging an upgrade to high-throughput diagnostics. Japan’s reimbursement for the Enhanced Liver Fibrosis score underscores policy support for advanced tools. Sophisticated genotyping needs are rising in India due to uncommon subtypes like HCV 1c. Regulatory collaboration across ASEAN and East-Asia regulators is improving device approval timelines, fostering broader market access.

Regulatory Landscape

Regulation is tightening around both high-volume hepatitis IVDs and laboratory-developed tests (LDTs), which is affecting go-to-market strategies for serology, molecular viral-load, and emerging self-testing workflows. In the United States, the FDA published a final rule in May 2024 (effective July 5, 2024) to phase out the historic general enforcement discretion approach for LDTs over a four-year period, raising compliance expectations for laboratories that previously ran hepatitis panels outside conventional device pathways.

At the IVD product level, the FDA reclassified qualitative hepatitis B virus (HBV) antigen assays, HBV antibody assays, and quantitative HBV nucleic acid-based assays from Class III to Class II with special controls, effective October 20, 2025 (Federal Register, September 2025). This change improves the feasibility of 510(k) clearance for HBV assays and can accelerate competitive entry for automated and cartridge-based platforms. In Australia, HBV/HCV self-tests are regulated as Class 4 IVDs under the Therapeutic Goods (Medical Devices) Regulations 2002, with requirements to include products in the ARTG and conform to relevant performance and labeling guidance.

Value Chain Analysis

The hepatitis diagnostic test value chain covers specialized biological inputs (antigens, antibodies, enzymes, primers/probes, calibrators/controls), assay design and software, kit manufacturing and instrument assembly, regulatory and quality release, and distribution into hospitals, reference labs, blood banks, and decentralized settings. Upstream supply is sensitive to the availability of high-quality biological materials and to the concentration of critical molecular inputs, including polymerases and oligonucleotide components, while midstream scale advantages generally rest with large IVD manufacturers and selected contract manufacturers that can assemble automated analyzers, microfluidic cartridges, and connectivity-enabled systems under ISO-aligned quality regimes.

Downstream performance depends on cold-chain capable logistics and stable procurement cycles, especially where specimen referral networks and reagent stock-outs affect continuity of testing. Documented bottlenecks include increasing scarcity of native high-titer patient samples used for controls and calibrators, which can drive substitution toward synthetic materials that then require additional validation, and cold-chain logistics for frozen plasma in decentralized models, which adds cost and complexity. Manufacturers are also regionalizing parts of production and supply to reduce tariff and procurement friction, including Roche Diagnostics starting a new manufacturing project in July 2025 in Suzhou Industrial Park to localize supply for China and strengthen resilience for high-throughput immunoassay and molecular workflows.

Competitive Landscape

The hepatitis diagnostic test market is moderately consolidated. Roche, Abbott and Danaher together generate multibillion-dollar diagnostics revenue and command significant molecular and immunoassay portfolios. Roche’s USD 16.76 billion diagnostics sales in 2023 evidence scale-driven advantages, while Abbott leverages its Alinity and m2000 systems globally. Danaher’s Cepheid earned first-mover status in point-of-care HCV RNA testing after FDA clearance, underscoring the value of cartridge-based molecular leadership.

Acquisition activity centers on speed and ease-of-use. BioMérieux’s EUR 111 million purchase of SpinChip Diagnostics added 10-minute microfluidic capability aimed at community clinics. Partnerships marry complementary assets: IBL International and Grifols collaborate on single-molecule counting biomarker panels to raise sensitivity thresholds. Vendors also invest heavily in AI algorithms that interpret elastography and serology in real time.

Emerging challengers exploit regulatory tailwinds. FDA reclassification of high-risk hepatitis assays from Class III to Class II reduces time-to-market and compliance costs, opening doors for nimble microfluidic and AI-first entrants. White-space remains in wearable diagnostics and remote-monitoring ecosystems; early-stage firms developing bioadhesive ultrasound platforms illustrate the shift toward continuous liver assessment. As incumbents defend share with full-suite offerings and service contracts, competitive pressure will pivot on speed of innovation adoption and footprint in fast-growing Asia-Pacific markets.

Hepatitis Diagnostic Test Industry Leaders

Abbott Laboratories

bioMérieux SA

Bio-Rad Laboratories

Danaher Corporation

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large diagnosis gaps, with only 13% of chronic hepatitis B and 36% of hepatitis C cases identified in the current landscape, create near-term whitespace for programs and vendors that simplify end-to-end pathways from screening to confirmatory testing. This is especially relevant where primary care, emergency departments, and community clinics are being asked to implement universal adult screening. Policy and guideline signals are moving toward broader coverage, including CDC recommendations for universal hepatitis C screening for adults aged 18 and older (and during each pregnancy) and universal hepatitis B screening at least once in a lifetime for adults aged 18 and older. WHO guidance and operational materials on hepatitis testing also emphasize integrating HBV and HCV testing services into routine care delivery.

On the product side, opportunities cluster around (i) automation of specialized assays, including reflex algorithms and high-throughput workflows, and (ii) menu expansion beyond HBV/HCV into broader viral hepatitis workups. FDA actions in 2026 provide evidence of pipeline conversion into cleared products, including Diasorin receiving De Novo authorization in January 2026 for the Liaison Murex Anti-HDV immunoassay (an automated HDV test in the United States), Abbott obtaining FDA clearance in April 2026 for the Anti-HCV Next assay, and Diasorin securing FDA clearance in June 2026 for the LIAISON Murex HBsAg Qual assay. Together, these moves support broader, instrument-anchored test menus that can pull recurring reagent revenue, help hospitals and reference labs standardize testing, and reduce reliance on manual or lab-developed approaches for niche hepatitis markers.

Recent Industry Developments

- July 2026: Roche launched the cobas Hepatitis D Virus (HDV) test, an automated solution for detection and quantification of HDV RNA for use on cobas 5800/6800/8800 systems in CE-marking countries. The launch expands automated viral hepatitis capability into HDV RNA quantification, supporting standardized monitoring in laboratories that already run high-throughput cobas workflows.

- April 2026: Abbott received US FDA 510(k) clearance for the Anti-HCV Next assay (K252424) for hepatitis C virus detection. The clearance strengthens Abbott's hepatitis testing portfolio within regulated immunoassay workflows and supports broader placement where labs standardize on cleared, predicate-based assays.

- May 2025: Medway NHS Foundation Trust launched an NIHR-backed program to screen all Emergency Department patients aged 16 and older for HIV, HBV, and HCV on an opt-out basis. The initiative embeds viral hepatitis testing into high-throughput acute-care settings, increasing routine screening volumes and reinforcing demand for automated serology and confirmatory pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the hepatitis diagnostic test market covers revenues from tests used to detect and assess viral hepatitis in clinical and screening settings, including lab and near-patient testing workflows.

Scope exclusions: We exclude hepatitis treatment drugs, vaccines, and routine liver health testing that is not ordered for suspected or confirmed hepatitis.

Segmentation Overview

- By Product Type

- Reagents & Kits

- Instruments & Analyzers

- Software & Services

- By Disease Type

- Hepatitis B

- Hepatitis C

- Other Hepatitis

- By Technology

- Serology Tests

- Rapid Diagnostic Tests

- Molecular Tests

- Next-Gen Sequencing Panels

- By Sample Type

- Blood

- Saliva / Oral Fluid

- Urine

- By Test Setting

- Hospital Laboratories

- Reference Laboratories

- Blood Banks

- Point-of-Care / Physician Offices

- Home Testing & Self-Collection

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the disease and testing context so the model uses realistic demand signals. We refer to public health disease-burden and screening guidance from sources such as the World Health Organization and the US CDC, which helps us map where testing volume is structurally supported.

To ground the supply side and adoption patterns, we also review sources such as US FDA public databases (test authorizations and labeling), peer reviewed clinical journals that describe test performance and typical algorithms, and national health statistics where available. Trade and customs releases, along with hospital and laboratory association publications, are used to sanity check import intensity and the practical split between central labs and point-of-care settings. We also use paid subscriptions for company financials and intelligence, plus patent databases and shipment-level trade data where it clarifies technology shifts and country mix. These examples are illustrative, and many other public sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to verify how testing is purchased and used across regions, then to pressure-test assumptions that desk sources cannot fully resolve, such as channel mix and pricing changes. We speak with a mix of diagnostic laboratories, hospital buyers, distributors, and product and commercial leaders, covering APAC, EMEA, and the Americas so regional screening intensity and reimbursement realities are reflected.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 38% |

| Mid tier: 54% | Functional/Unit leaders: 33% | EMEA: 37% |

| Smaller Players: 18% | Managers: 54% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up checks, with the main spine coming from a demand-pool build that ties testing to the diagnosed and screened population. In practice, we reconstruct market value by combining hepatitis screening and monitoring intensity with test setting mix, and then convert that into revenue using realistic price bands.

Inputs used in the model include hepatitis prevalence and diagnosed share, screening policy coverage for priority cohorts, the share of testing done in central labs versus point-of-care settings, the mix between immunoassays and nucleic acid testing in the typical diagnostic pathway, and average selling price movement for kits and reagents by region. Once these signals are combined and reviewed, the market total becomes clearer at the end of the workflow.

Forecasting uses scenario analysis supported by simple multivariate relationships, where demand drivers like screening expansion, lab capacity, and test menu modernization are varied within realistic bounds agreed in expert discussions. Bottom-up approximations are used as a cross-check by rolling up sampled supplier revenues and applying volume times ASP logic in a few representative countries, and then gaps are handled through proxy markets where testing behavior and care access look comparable.

Data Validation & Update Cycle

Outputs are checked against independent indicators such as infectious disease diagnostics spend direction, public screening targets, and observable shifts in test-setting adoption. If a country result looks out of line, we re-check the assumptions, rerun sensitivity bands, and, when needed, circle back to a small set of interviewees to understand the variance.

Before sign-off, the model and narrative go through multi-step analyst reviews so unit logic, price ranges, and regional weighting stay consistent. Reports are refreshed annually, and interim updates are made when material events occur, such as changes in screening guidance or major regulatory actions. Right before delivery, a final pass is completed so the client receives the latest updated view available.

Mordor Intelligence's Hepatitis Diagnostic Test Market Size Compared Against Other Published Estimates

Published market sizes for hepatitis diagnostic tests can vary even when the topic name looks the same, because each publisher draws the line differently on what counts as a test market and which years and currencies are used. Differences also come from how pricing is treated, and whether lab testing and point-of-care testing are blended using realistic mix assumptions.

The table shows a spread that is largely explained by scope and conversion choices, where Mordor Intelligence's model treats the market as hepatitis-focused diagnostic testing revenues across blood-based testing, imaging, and biopsy pathways, and keeps the year mapping consistent with the stated study window instead of mixing older base years into current-year totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.73 B (2025) | |

| Industry Publisher A | USD 4.08 B (2024) | Uses 2024 as the base and emphasizes sales revenue tracking by type and application, which can understate near-term value if screening intensity and price movements are not carried forward into a current-year estimate. |

| Industry Publisher B | USD 3.62 B (2024) | Relies on a 2023 base-year structure with a longer forecast window, and the pricing and technology mix assumptions are not always aligned to how testing shifts between immunoassays and NAT across regions. |

Looking across the three figures, the gap is mainly driven by base-year alignment and what is counted inside the diagnostic pathway, followed by how ASP progression is applied. By keeping the demand pool tied to screening and monitoring intensity and then checking it with selective supplier and channel signals, the final number stays traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

Which diagnostic technology is gaining momentum for hepatitis testing?

Molecular platforms—particularly point-of-care RNA assays—are displacing traditional serology because they deliver same-day results and enable on-the-spot treatment decisions.

Why are reagents and kits expected to retain a leading role despite rising software adoption?

Every viral-load or antibody test still requires a consumable kit, so laboratories must replenish reagents even as they add AI-driven analytics layers.

How are governments influencing demand for hepatitis diagnostics?

Expanded universal-screening policies and elimination campaigns are driving routine testing in primary care, emergency departments, and even community pharmacies.

What makes Asia-Pacific a key focus for diagnostic companies?

The region houses the world’s highest concentration of chronic hepatitis B and C cases, motivating health systems to adopt faster, more sensitive testing algorithms.

Which sample types are emerging as alternatives to venous blood draws?

Finger-stick capillary blood and saliva/oral fluid collections are gaining favor for their convenience, enabling wider outreach in remote and resource-limited settings.

How is artificial intelligence reshaping hepatitis diagnostics?

AI tools now interpret elastography and laboratory data in real time, helping clinicians detect liver fibrosis earlier and reduce manual review workloads.

Page last updated on: