Rare Disease Genetic Testing Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

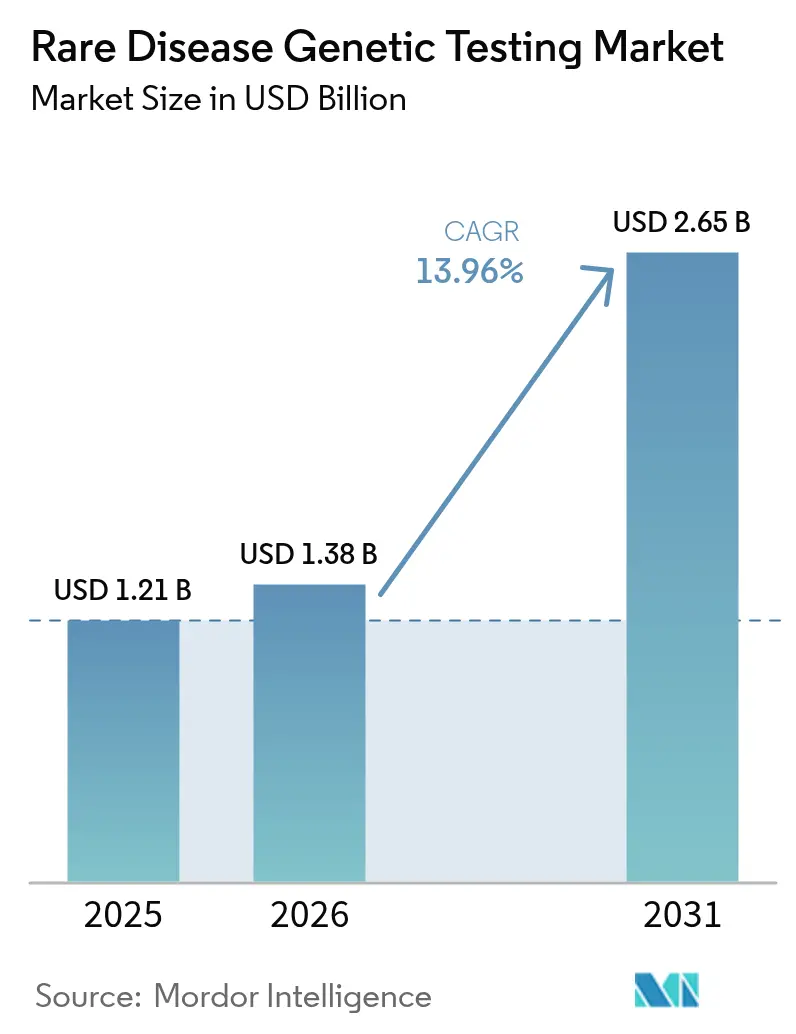

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 2.65 Billion |

| Growth Rate (2026 - 2031) | 13.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rare Disease Genetic Testing Market Analysis by Mordor Intelligence

rare disease genetic testing market size in 2026 is estimated at USD 1.38 billion, growing from 2025 value of USD 1.21 billion with 2031 projections showing USD 2.65 billion, growing at 13.96% CAGR over 2026-2031. Continuous drops in next-generation sequencing (NGS) prices, combined with AI-enabled variant-interpretation engines and wider reimbursement, move genetic testing from niche research toward mainstream clinical care Laboratories now deliver same-day genomic diagnoses, while regulators increasingly classify complex assays as essential medical infrastructure rather than experimental add-ons. Heightened demand also reflects the vibrant pipeline of gene therapies whose prescribing information requires a molecular diagnosis, reinforcing the clinical value proposition of broad-based sequencing.

Key Report Takeaways

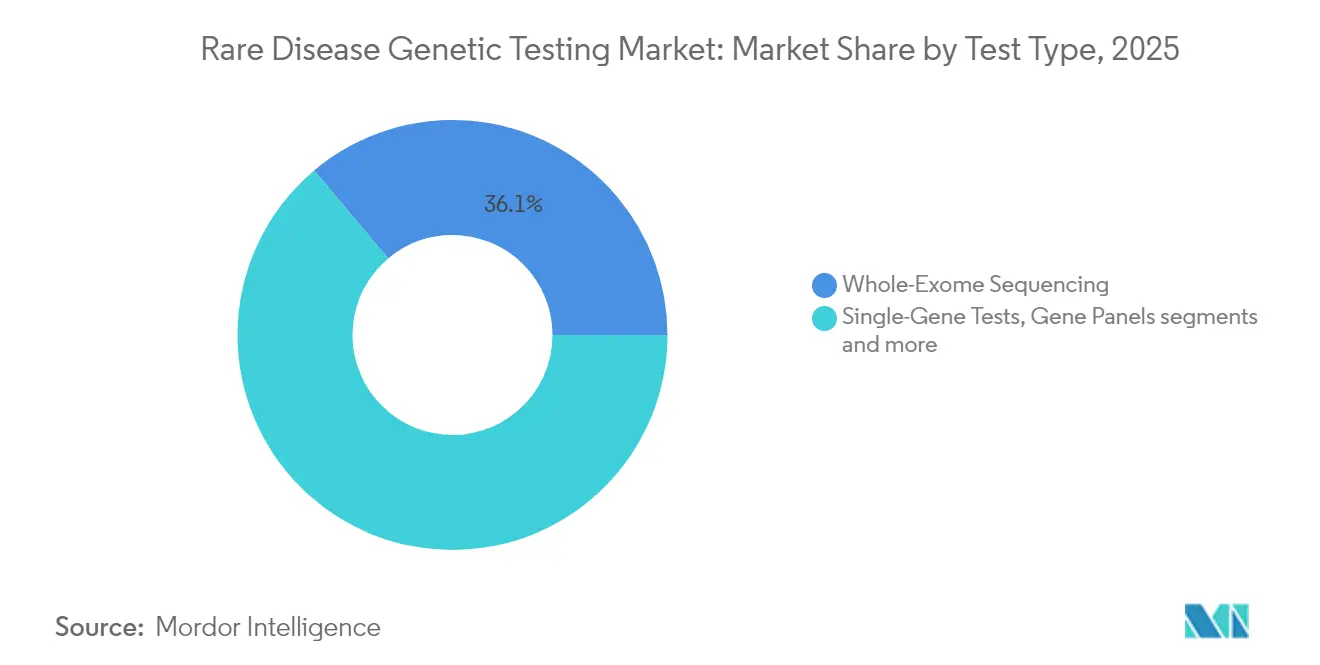

By test type, whole-exome sequencing commanded 36.54% of rare disease genetic testing market share in 2024.

By technology, long-read NGS is advancing at a 16.35% CAGR, outpacing short-read platforms already holding 72.34% revenue share.

By sample type, blood retained a 58.46% share of the rare disease genetic testing market size in 2024, yet saliva and buccal swabs are growing 14.89% annually.

By indication, neurological disorders held 31.23% revenue and are projected to accelerate at 16.21% through 2030.

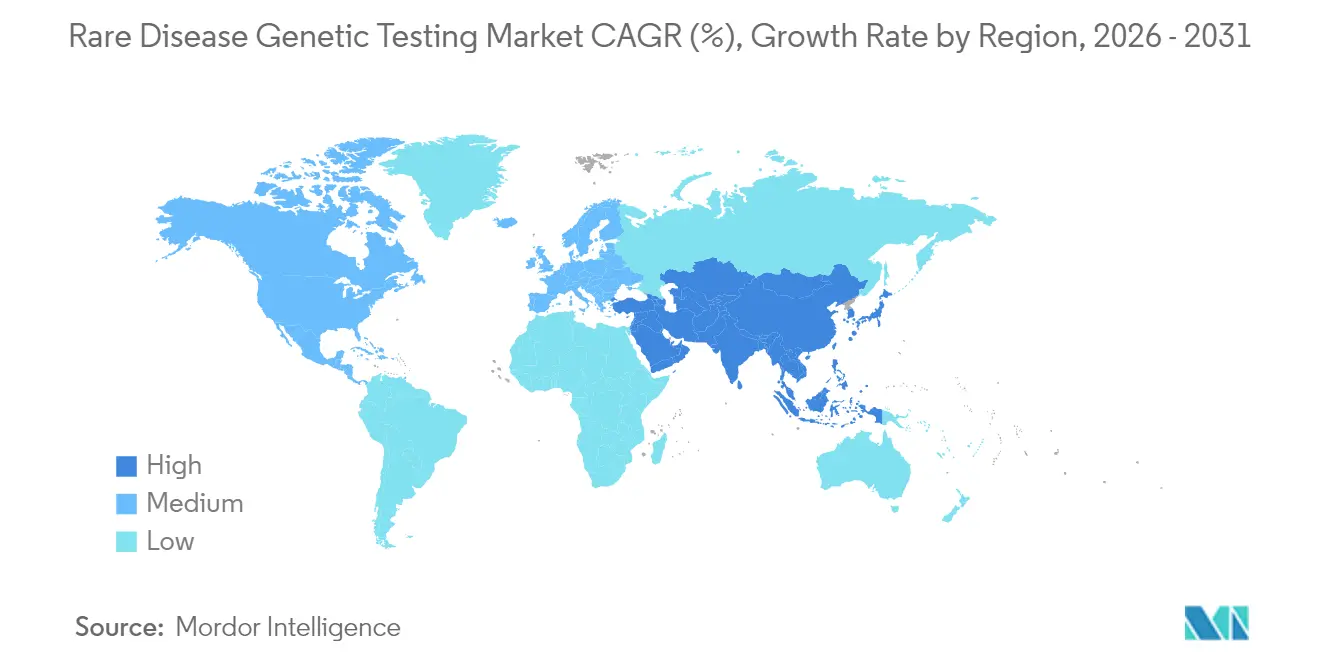

By geography, North America dominated with a 43.23% share in 2024, while Asia-Pacific is projected to expand at 16.45% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rare Disease Genetic Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining cost of next-generation sequencing | +3.2% | Global | Medium term (2-4 years) |

| National reimbursement expansion for rare-disease diagnostics | +2.8% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| AI-enhanced variant-interpretation platforms | +2.1% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Biopharma trial recruitment via rare-disease gene databases | +1.9% | Global, concentrated in North America & EU | Long term (≥ 4 years) |

| Newborn genomic-screening pilots | +1.7% | North America, UK, expanding globally | Long term (≥ 4 years) |

| Portable long-read sequencers in emerging markets | +1.4% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Cost of Next-Generation Sequencing

NGS reagent and instrument costs fell sharply, pushing whole-genome sequencing below USD 600 per sample by late 2024, a threshold that undercuts many multi-gene panels. Cost parity encourages hospitals to deploy genome-first protocols that replace sequential single-gene tests and shorten diagnostic odysseys. Real-world economic studies show mean savings of USD 100,440 per patient when rapid genome sequencing is used in neonatal intensive care units. Throughput gains from instruments such as Illumina’s NovaSeq X and Oxford Nanopore’s PromethION 2 Integrated further suppress per-base prices, while automation trims personnel expenses. As laboratories scale, the rare disease genetic testing market gains predictable price elasticity, unlocking pent-up demand among clinicians who previously rationed complex testing.

National Reimbursement Expansion for Rare-Disease Diagnostics

Public and private payers now reimburse comprehensive sequencing in several high-income regions. Texas Medicaid introduced coverage for whole-exome and whole-genome sequencing at USD 3,728.40 and USD 3,924.34 respectively in late 2024. North Carolina Medicaid soon followed, covering tests for Duchenne muscular dystrophy and Lynch syndrome. Medicare added hereditary transthyretin amyloidosis sequencing, setting clinical precedent for other payers. These policies reduce patient out-of-pocket exposure and nudge institutions toward routine genomic work-ups, a trend mirrored by nascent subsidy programs in China and India. Reimbursement certainty accelerates revenue capture for laboratories and magnifies the total addressable rare disease genetic testing market.

AI-Enhanced Variant-Interpretation Platforms

Interpretation, not data generation, long stood as the costliest bottleneck. AI-powered tools such as AI-MARRVEL now achieve 98% diagnostic precision, doubling solve rates versus manual curation. Machine learning parses structural variants in minutes and continuously improves by ingesting global patient data. Baylor Genetics cut turnaround times from several days to under eight hours after deploying automated classification pipelines. These efficiencies widen laboratory margins and let clinicians treat genetic testing much like routine blood chemistry, raising utilization rates across tertiary and community settings alike.

Biopharma Trial Recruitment via Rare-Disease Gene Databases

Testing companies increasingly monetize deidentified sequence data. GeneDx Discover offers sponsors curated access to more than 700,000 genomes, facilitating real-time feasibility assessments for orphan-drug studies. CENTOGENE’s platform holds over one million cases from 120 countries, feeding statistical power into ultra-rare genotype-phenotype models centogene.com. Revenue-sharing deals convert laboratories from one-off testing vendors into longitudinal research partners, anchoring sustainable data-services income and expanding the rare disease genetic testing market beyond pure diagnostics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket costs & limited payer coverage | -2.3% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Shortage of certified genetic counsellors | -1.8% | Global, most severe in rural and emerging markets | Medium term (2-4 years) |

| Fragmented genomic-privacy regulations | -1.5% | Global, with varying regional impacts | Medium term (2-4 years) |

| Low diagnostic yield for non-coding/ultra-rare variants | -1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Costs & Limited Payer Coverage

Although coverage is expanding, many patients still shoulder fees between USD 300 and USD 5,000 when insurance declines claims. Administrative hurdles such as prior authorization deter ordering clinicians and lengthen turnaround times. Direct-to-consumer firms attempt to bridge gaps with USD 99 monthly subscriptions, yet their recreational reports rarely meet clinical utility standards. In emerging economies, private pay may equal several months of average household income, limiting adoption and constraining the rare disease genetic testing market in regions most burdened by consanguinity-linked disorders.

Shortage of Certified Genetic Counsellors

The number of graduating genetic counselors has stagnated. Only 30% of 2024 program completers secured roles by May 2024 compared with 79% a year earlier, reflecting funding volatility[1]Source: National Society of Genetic Counselors, “2024 workforce report,” nsgc.org . Rural hospitals seldom employ dedicated counselors, instead relying on tele-genetics, which remains patchy where broadband is scarce. Lack of Medicare reimbursement for counseling services further depresses hiring. Without sufficient professional guidance, physicians hesitate to order complex panels, capping near-term penetration of the rare disease genetic testing industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Comprehensive Genomic Approaches Dominate Growth

Whole-exome sequencing led revenue with 36.12% of rare disease genetic testing market share in 2025, balancing cost and diagnostic yield for protein-coding mutations. Whole-genome sequencing, growing at 15.08% CAGR, captures non-coding and structural variants that exomes overlook, steadily eroding panel-based testing. Single-gene assays persist as confirmatory tools when a clear pathogenic variant runs in families.Clinical evidence underpins the transition. Genome sequencing delivers 23% higher yields than chromosomal microarray in neurodevelopmental cohorts while lowering cumulative costs across two years. Long-read workflows from Oxford Nanopore resolve tandem repeat expansions historically invisible to short-reads, positioning long-read genomes as the future gold standard. Rapid neonatal protocols that finish analysis inside 12 hours further reinforce genome testing as an urgent-care staple, cementing its role in the evolving rare disease genetic testing market.

By Technology: Next-Generation Sequencing Platforms Evolve Rapidly

Short-read NGS captured 71.58% revenue during 2025, but long-read platforms are trending up at 15.92% CAGR thanks to structural-variant sensitivity. Sanger sequencing retains utility for variant confirmation, especially when laboratories require orthogonal validation.Technology convergence accelerates. Illumina’s NovaSeq X now integrates single-flow-cell chips and AI-driven base-calling, cutting per-sample run time while lifting raw accuracy. Portable devices such as MinION bring near-lab quality to field sites, broadening geographic reach. As accuracy gaps narrow, cost curves favor holistic multi-omic platforms, expanding the rare disease genetic testing market size across hospital tiers and regional laboratories.

By Sample Type: Non-Invasive Collection Methods Gain Momentum

Blood samples still supply 57.92% of 2025 volume, prized for high DNA integrity. Nonetheless, saliva and buccal swabs are advancing 14.52% annually on patient comfort and room-temperature logistics. Volumetric absorptive microsampling now ships dried blood spots in paper envelopes without cold chain, making community-based programs viable.Buccal DNA often outperforms blood for mitochondrial heteroplasmy detection and removes phlebotomy scheduling hurdles. FDA-cleared OrageneDx kits unlock at-home sample collection for clinical-grade tests. These innovations ensure sample diversity, reduce no-show rates, and enlarge overall throughput for the rare disease genetic testing market.

By Indication: Neurological Disorders Lead Complex Diagnostic Landscape

Neurological disorders accounted for 30.85% of 2025 revenue and are growing at 15.84% CAGR, buoyed by gene-therapy pipelines for conditions such as spinal muscular atrophy and Duchenne muscular dystrophy. Metabolic syndromes remain significant via newborn screening mandates that rely on rapid sequencing to guide enzyme replacement.The neurological category benefits from AI phenotype-genotype matching that trims interpretation time for epilepsy panels and movement-disorder genomes. Early diagnosis determines eligibility for adeno-associated virus therapies, creating direct reimbursement incentives. These clinical drivers reinforce segment leadership and sustain momentum for the wider rare disease genetic testing market size.

By End User: Healthcare System Integration Accelerates Adoption

Hospitals and clinics held 45.93% of 2025 revenue thanks to EHR integration, while direct-to-consumer channels are surging at 16.88% CAGR. Diagnostic laboratories supply complex bioinformatics pipelines for community hospitals that lack the necessary infrastructure.Epic’s embedded ordering module for GeneDx rapid genome tests exemplifies frictionless workflows that embed genetics into acute care. Meanwhile, subscription-based consumer offerings extend optional clinical confirmation, bringing incremental demand from wellness-focused users and creating a two-tier flow of samples into the rare disease genetic testing market.

Geography Analysis

North America, with 42.76% share in 2025, benefits from broad payer coverage, payer-funded NICU sequencing, and clear FDA pathways that tie diagnostics to recently approved gene therapies. Whole-genome reimbursement for critically ill infants lowers barriers across state Medicaid programs and drives steady case volumes into regional reference labs.Asia-Pacific posts the highest growth, advancing at 16.02% CAGR on national registries and subsidized testing in India and China ijbscience.in. Local manufacturers develop cost-effective reagents, while portable sequencers circumvent infrastructure gaps. Government consortiums negotiate bulk pricing, making genome tests affordable for provincial hospitals and amplifying the rare disease genetic testing market footprint.Europe sustains mid-teen growth under the European Health Data Space, which mandates interoperable health records. Germany’s Digital Act simplifies cross-border data transfers, enhancing multi-country trial recruitment. Although reimbursement varies, pan-EU data pooling increases diagnostic odds for ultra-rare variants. Latin America and the Middle East remain nascent but leverage pilot programs such as Brazil’s Rare Genomes Project to highlight unmet need and justify new funding streams.

Regulatory Landscape

In the United States, oversight remains fluid for laboratory-developed tests (LDTs) that underpin many rare-disease sequencing offerings. In September 2025, the FDA formally rescinded the 2024 LDT final rule following a March 2025 federal court vacatur. This reverted key definitions to pre-2024 language and kept enforcement discretion for many LDT workflows used by clinical laboratories.

In Europe, compliance pressure is anchored to the EU IVDR transition pathway for legacy IVDs, including sequencing-related assays and components marketed as IVD devices. Under the extended transition milestones for Class C legacy devices, manufacturers must lodge an IVDR certification application with a Notified Body by 26 May 2026 and have a signed written agreement in place by 26 September 2026 to preserve extended eligibility for continued market access.

Value Chain Analysis

The value chain runs from patient identification and ordering (neurology, metabolic, and NICU settings) through pre-analytical steps, including blood, saliva, buccal swab, and dried blood spot collection, plus sample logistics and wet-lab processing. Sequencing on short-read and long-read platforms feeds into bioinformatics and clinical interpretation, where variant classification, phenotype matching, and report generation create differentiation. Bottlenecks often arise from variants of uncertain significance and the need for orthogonal confirmation in some workflows.

Downstream activities include clinical decision support, genetic counseling coordination, and longitudinal data services that connect diagnostic labs with biopharma for trial recruitment and natural-history research, including curated rare-disease genotype-phenotype databases. Quality systems and market access requirements shape who captures margin, such as CLIA/CAP/ISO 15189 accreditation readiness, GDPR and U.S. genetic privacy compliance, and shifting regulatory treatment of LDTs versus regulated IVD devices. These factors influence investments in documentation, software validation, and external partnerships across hospitals, reference laboratories, instrument vendors, and data-platform operators.

Competitive Landscape

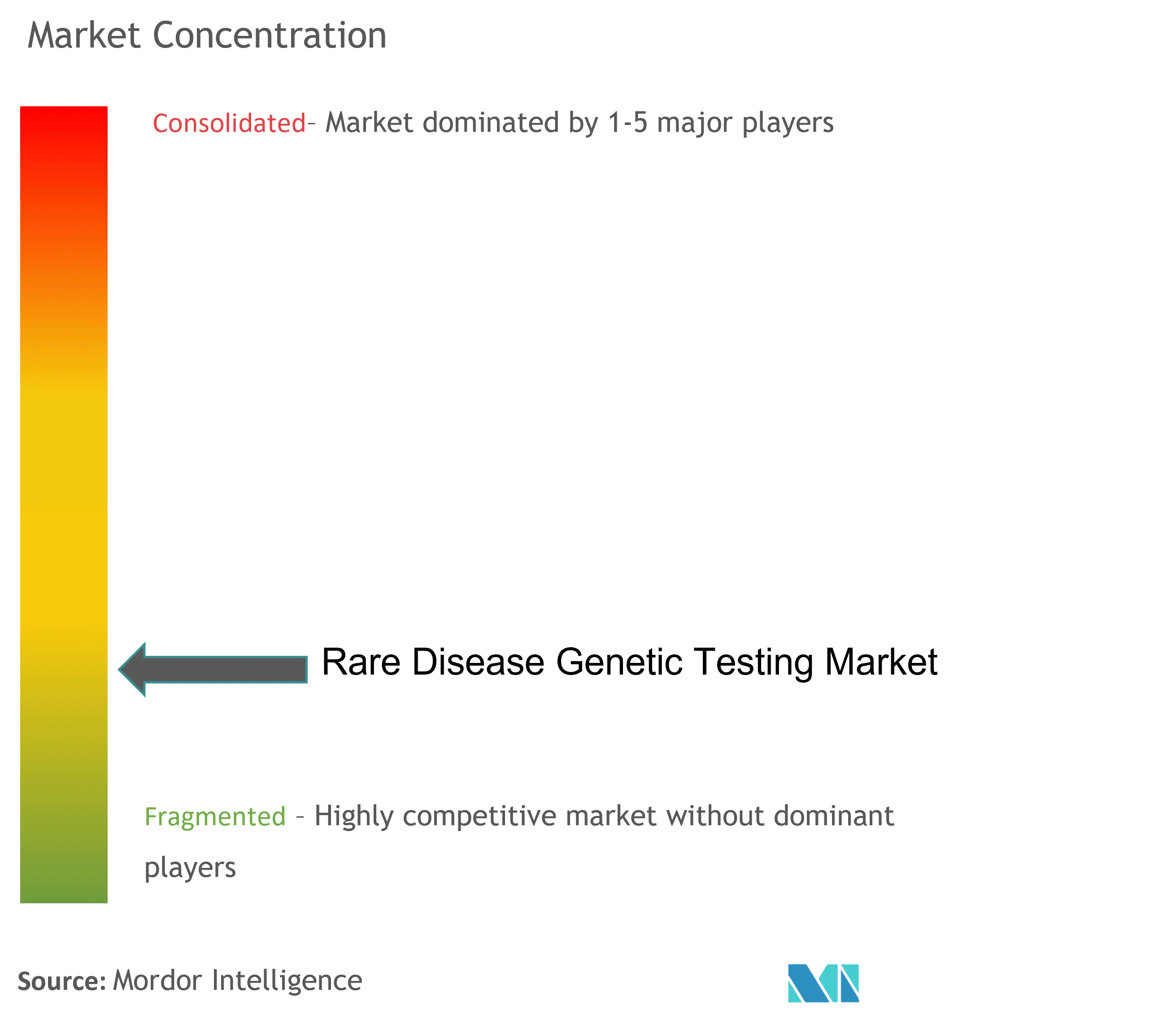

The landscape is moderately consolidated. Diagnostics conglomerates leverage automation and global logistics, while specialty companies curate deep phenotype-linked biobanks. Labcorp’s USD 239 million purchase of Invitae assets and Regeneron’s USD 256 million acquisition of 23andMe illustrate convergence of testing and drug discovery. Illumina expands into multi-omics, threatening single-platform rivals, whereas Oxford Nanopore pushes long-read accuracy forward, challenging short-read incumbents.

Strategic alliances are pivotal. CENTOGENE licenses data to pharma partners, turning static reports into recurring fee streams. GeneDx employs revenue-share models that finance no-cost diagnostic programs, channeling higher sample volumes. Regulatory tightening around laboratory-developed tests in the United States raises compliance costs, favoring firms with robust quality systems and potentially consolidating the rare disease genetic testing industry around well-capitalized players.

Rare Disease Genetic Testing Industry Leaders

Quest Diagnostics Incorporated

Invitae Corporation

3billion Inc.

Eurofins Scientific, Inc.

Centogene N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace sits in payer and guideline expansion for genome-wide testing beyond inpatient critical care into outpatient diagnostic pathways. In June 2026, Carelon updated clinical appropriateness guidance to include whole-genome sequencing for qualifying postnatal outpatient scenarios. This broadens ordering at hospitals and specialty clinics and increases throughput opportunities for laboratories with scalable WGS pipelines.

Reimbursement volatility is also creating room for cost-engineered workflows and differentiated service models. In Germany, the National Association of Statutory Health Insurance Physicians (KBV) announced reimbursement cuts for genetic testing and medical genetics services effective October 1, 2026, which raises the premium on automation, rapid interpretation, and efficient sample logistics. Additional opportunity comes from health-system deployment models, including hub-and-spoke genomic medicine programs and newborn genomic screening pilots, that integrate sequencing with multidisciplinary care and longitudinal follow-up, as well as from EU IVDR transition milestones that drive demand for compliant assays, validated software, and Notified Body-ready technical documentation.

Recent Industry Developments

- April 2026: 3billion announced a major expansion of its newborn genomic screening program, extending population-scale testing and integrating rapid reporting with pediatric care coordination. The move broadens testing reach and reinforces automation and data-interpretation capabilities across the value chain.

- September 2025: 3billion partnered with Kazakhstan's Center for Molecular Medicine (CMM) to expand access to AI-based rare disease diagnostics. The agreement advances a regional hub model that can improve patient reach where specialist genetics services are limited. It also reinforces the role of software and interpretation capability as a core differentiator alongside sequencing capacity.

- August 2024: Labcorp completed the acquisition of select assets of Invitae. The deal broadened Labcorp's genetic testing capabilities across oncology and select rare diseases, supporting menu expansion and scale advantages in laboratory operations. It also signaled continued consolidation among testing providers as they pursue larger datasets, automation, and payer contracting leverage.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from genetic tests used to diagnose or confirm rare diseases, including lab testing services and related consumables when they are part of the test delivered to a patient or clinician.

Scope exclusions: It does not count basic screening that is not tied to rare-disease evaluation, general ancestry testing, or research-only sequencing that is not used for clinical decision making.

Segmentation Overview

- By Test Type (Value)

- Single-Gene Tests

- Gene Panels

- Whole-Exome Sequencing

- Whole-Genome Sequencing

- By Technology (Value)

- Next-Generation Sequencing

- Sanger Sequencing

- PCR-Based Testing

- By Sample Type (Value)

- Blood

- Saliva/Buccal Swab

- Amniotic/Chorionic (Prenatal)

- By Indication (Value)

- Neurological Disorders

- Metabolic Disorders

- Immunological & Hematological Disorders

- Others

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the outer limits of the market and keep assumptions realistic across regions. We reviewed public health and science references such as the NIH Genetic and Rare Diseases Information Center, CDC materials on newborn screening, and resources from the National Organization for Rare Disorders to understand disease coverage and testing pathways.

For market signals, we also referred to sources such as OECD health statistics for system capacity context, peer reviewed genetics journals for technology adoption patterns (for example, NGS panel use), and publicly available payer and health system guidance to determine when testing is reimbursed. Company filings, investor presentations, and reputable press were then used to cross-check test menu focus and expansion plans. In addition, paid subscription databases for company financials and for patents were used selectively to confirm revenue exposure and innovation direction. These sources are illustrative and not exhaustive, and other public documents were also used during the work for validation and clarification.

Primary Interviews and Surveys

Primary work focused on turning published signals into usable pricing and volume ranges, especially where lists of tests exist but testing intensity is not clearly stated. We spoke with clinical laboratory leaders, hospital geneticists, payers, and distributors across the Americas, EMEA, and APAC to pressure-test assumptions on utilization, average selling price behavior, and the shift toward broader sequencing (for example, exome level approaches) in complex cases.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 44% |

| Mid tier: 46% | Functional/Unit leaders: 35% | EMEA: 31% |

| Smaller Players: 15% | Managers: 53% | Americas: 25% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where rare disease testing demand is reconstructed using diagnosed and suspected patient flows, test ordering behavior in key care settings, and the share of cases routed to genetic confirmation. Once this demand pool is set by region, revenue is derived by applying realistic pricing bands that reflect how panels, exome, and targeted methods are actually billed and reimbursed.

To keep the totals grounded, selective bottom-up checks were run using supplier exposure, lab capacity signals, and sampled price lists, and then the model was adjusted where the two views did not align. Inputs that mattered most included the mix shift toward NGS based approaches, average turnaround time expectations that affect lab throughput, payer coverage expansion for confirmatory testing, the split of testing between hospital labs and independent diagnostic labs, and the prevalence of re-testing when prior results are inconclusive.

For forecasting, we used scenario analysis supported by trend smoothing on core drivers, since policy and reimbursement changes can move faster than pure historical patterns. Growth rates by region were reviewed with interviewees and then applied to the demand pool and price layers separately, so volume and price were not forced to grow in the same way. Where information gaps existed for smaller countries, we used proxy markets with similar healthcare access and rare disease diagnostic pathways, and then scaled using population and specialist availability signals.

Data Validation & Update Cycle

Validation is done through several checks so the final number stays consistent with real world signals. We compare modeled testing volumes against independent indicators such as lab capacity discussions, reimbursement guidance shifts, and technology adoption clues from clinical literature, and then we re-check any sharp jumps that do not match these signals.

After the first build, another analyst reviews the logic, unit assumptions, and regional splits, and outliers are sent back for revision with notes. If a change in reimbursement, regulation, or a major lab expansion is spotted during review, experts are re-contacted to confirm whether it affects near-term volumes or pricing. Reports are refreshed at least once each year, with interim updates when material events make assumptions stale, and a final pre-delivery pass is completed so clients receive the latest view.

Mordor Intelligence's Rare Disease Genetic Testing Market Size Compared With Other Published Estimates

Published market sizes for rare disease genetic testing can differ because each publisher decides its own definition of what counts as a test, which end users are counted, and whether pricing reflects reimbursed rates or list prices. Timing also affects results, since base-year selection and currency conversion can shift totals even when the underlying storyline is similar.

The spread usually comes from scope and from how volumes are translated into revenue. Some estimates fold rare disease diagnostics more broadly into the number (including non-genetic diagnostics), while others include research-use sequencing and then apply a single global price uplift. The table points to these drivers, where clinical-only testing, reimbursement-weighted pricing, and country-level splits were kept explicit before the final total was set, a modeling choice used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.38 B (2026) | |

| Trade Journal A | USD 4.63 B (2023) | Uses a broader rare-disease diagnostic umbrella and may include adjacent clinical testing beyond rare-disease genetic confirmation, which can inflate revenue versus a genetics-only definition. |

| Regional Consultancy B | USD 1.47 B (2024) | Often anchors on headline vendor revenue signals and applies uniform pricing growth, with less transparency on country-level utilization differences and reimbursement-driven price ceilings. |

Overall, differences are mostly explained by what is counted as rare disease genetic testing, and how pricing is treated across regions and care settings. Our approach keeps assumptions traceable to patient flow, test mix, and reimbursement realities, which makes it easier for buyers to reconcile the number with what they see in the field.

Key Questions Answered in the Report

What underpins the 13.96% CAGR of the rare disease genetic testing market?

Declining NGS costs, AI-driven interpretation, and expanding reimbursement combine with gene-therapy demand to propel sustained double-digit growth.

How do regulatory changes shape market consolidation?

FDA oversight of laboratory-developed tests raises compliance costs, giving well-capitalized firms an edge, while the EU Health Data Space unlocks cross-border data access for smaller players.

Which technology will lead future adoption?

Long-read sequencing is gaining share thanks to structural variant detection and portability, yet improved short-read accuracy maintains a dual-technology landscape.

Why is Asia-Pacific the fastest-growing region?

Government-funded registries, subsidy programs, and domestic reagent production lower testing costs and expand access across populous nations.

Which region has the biggest share in Rare Disease Genetic Testing Market?

In 2025, the North America accounts for the largest market share in Rare Disease Genetic Testing Market.

Page last updated on: