Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.92 Billion |

| Market Size (2026) | USD 7.28 Billion |

| Market Size (2031) | USD 9.37 Billion |

| Growth Rate (2026 - 2031) | 5.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China POS Terminals Market Analysis by Mordor Intelligence

The China POS Terminals Market size was valued at USD 6.92 billion in 2025 and estimated to grow from USD 7.28 billion in 2026 to reach USD 9.37 billion by 2031, at a CAGR of 5.17% during the forecast period (2026-2031). The upward trajectory reflects Beijing’s cash-lite policy push, Digital-Yuan pilots, and compulsory EMV-L3 certification in transit systems. Contactless payment acceptance, wider smartphone penetration, and quick-response regulation from the People’s Bank of China are propelling demand for NFC-ready devices. Consolidation among payment enterprises, stricter data-localization laws, and rising AI-powered fraud detection adoption are reshaping vendor strategies. Meanwhile, SoftPOS growth, semiconductor supply-chain volatility, and heightened cybersecurity risks continue to pressure margins yet open new service niches for agile players.

Key Report Takeaways

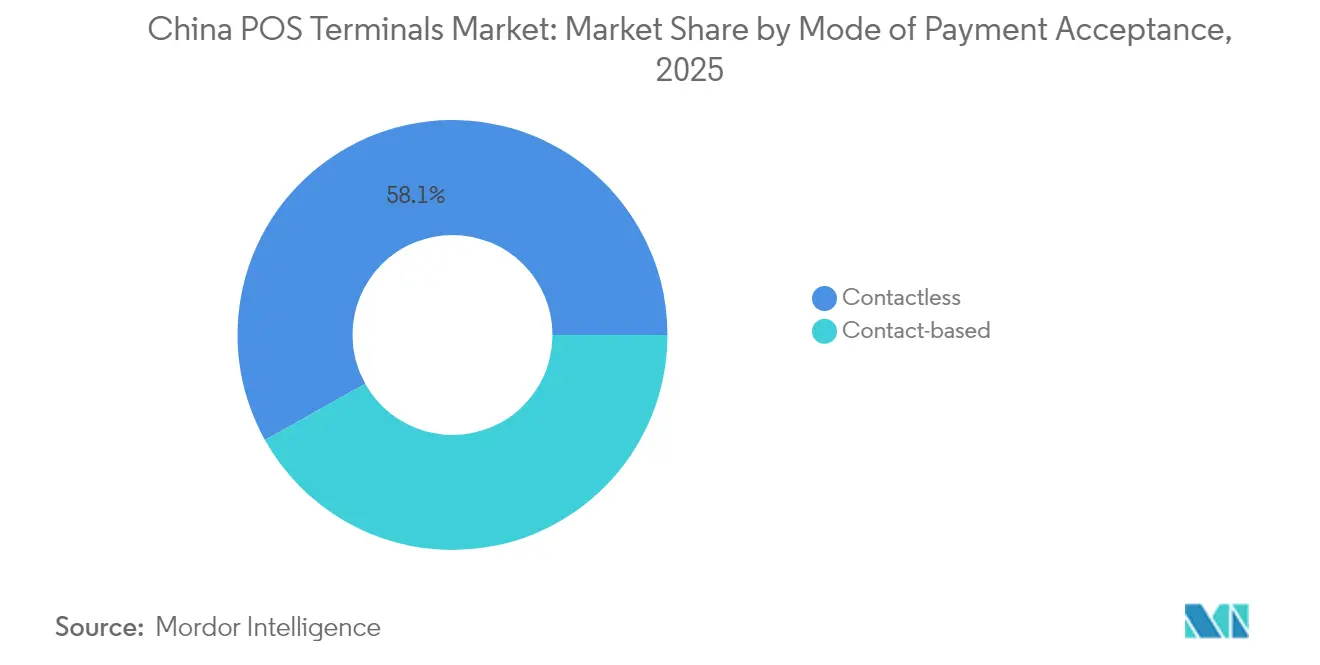

- By mode of payment, contactless solutions led with 58.12% of the China POS terminals market share in 2025 and are expanding at a 6.71% CAGR through 2031.

- By POS type, mobile and portable devices accounted for 63.10% of the China POS terminals market size in 2025 and will post a 6.79% CAGR during 2026-2031.

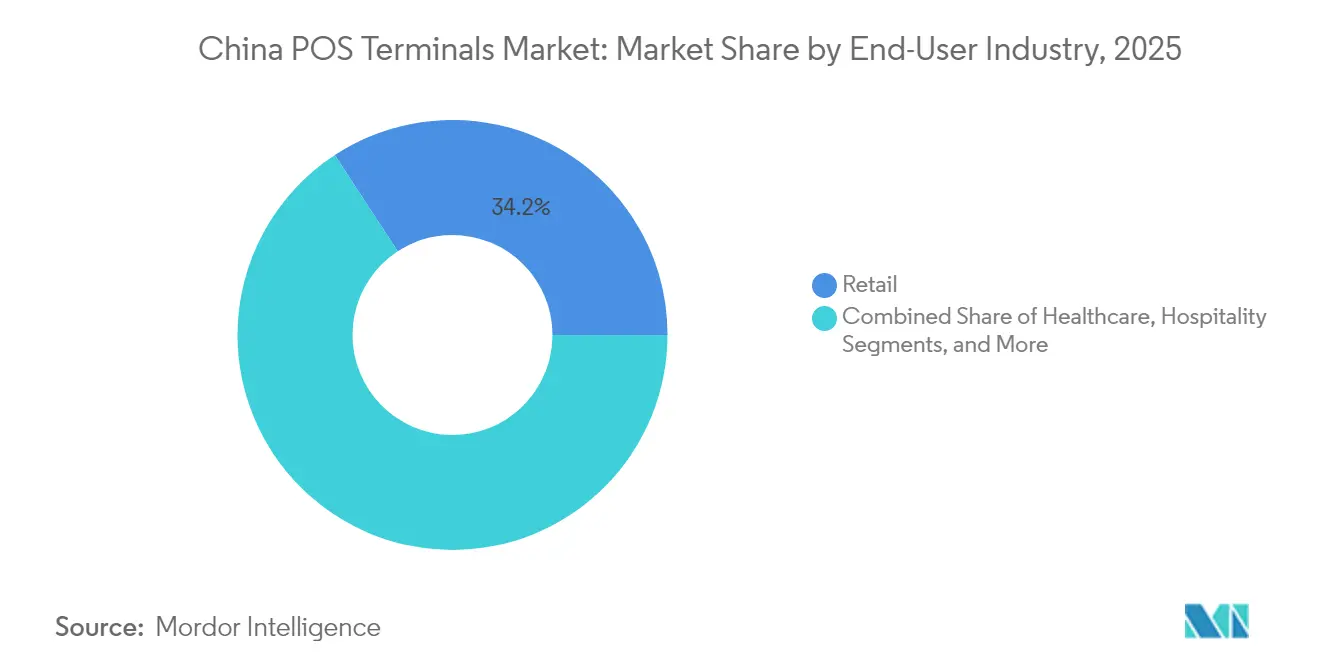

- By end-user, retail captured 34.22% revenue share in 2025 in the China POS terminals market, whereas healthcare registers the highest forecast CAGR at 6.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China POS Terminals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Push for Cashless Economy via Digital-Yuan Pilots | +1.2% | National, with early gains in major cities and pilot zones | Medium term (2-4 years) |

| Rapid Expansion of Mobile-Wallet-Ready NFC POS | +1.8% | National, accelerated in tier-1 and tier-2 cities | Short term (≤ 2 years) |

| Increasing Adoption by SMEs and QSRs | +1.1% | National, concentrated in urban commercial districts | Medium term (2-4 years) |

| Integration of AI-Powered Fraud-Detection Chips | +0.7% | National, priority in high-transaction venues | Long term (≥ 4 years) |

| Rise of Unattended Smart POS in Tier-3 Cities | +0.9% | Rural and tier-3 cities, expanding to county-level markets | Medium term (2-4 years) |

| Mandated EMV-L3 Certification for Transit POS | +0.6% | National transportation hubs, metro systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Push for Cashless Economy via Digital-Yuan Pilots

Expanded digital-currency pilots now allow foreign visitors to top up wallets with single-transaction limits of USD 5,000 and annual caps of USD 50,000, stimulating demand for dual-acceptance terminals capable of processing Digital Yuan and international card schemes. Tourist-facing venues must deploy multi-scheme hardware, while cryptography regulations enforce on-device encryption modules. Established vendors with deep regulatory expertise benefit from the resulting certification complexity.

Rapid Expansion of Mobile-Wallet-Ready NFC POS

Alipay’s “Tap-to-Pay” campaign and the rollout of 1.12 billion medical-insurance QR codes across 800,000 healthcare sites accelerate NFC terminal orders. QSR chains leverage biometric NFC devices, and Beijing Metro’s acceptance of foreign bank cards underscores the shift toward multi-wallet tap solutions. Terminal specifications now encompass social-insurance system links and biometric ID checks.

Increasing Adoption by SMEs and QSRs

State Council directives compel SMEs to accept multiple cash-lite methods, heightening POS demand in tier-3 cities. Merchant preferences lean toward all-in-one Android terminals bundling payment, CRM, and inventory functions. Yet SoftPOS platforms entice price-sensitive micro-merchants, challenging hardware margins.

Integration of AI-Powered Fraud-Detection Chips

UnionPay’s “Eagle Eye” and ICBC’s analytics programs illustrate rising AI deployment in POS risk control. Chip-level machine-learning cuts latency, aligns with China’s data-localization laws, and differentiates domestic suppliers like PAX Technology, whose HarmonyOS devices embed on-board AI.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cyber-attacks Targeting POS Networks | -0.8% | National, concentrated in high-transaction urban areas | Short term (≤ 2 years) |

| Price Pressure from SoftPOS Smartphone Apps | -1.2% | National, accelerated in SME and micro-merchant segments | Medium term (2-4 years) |

| Semiconductor Supply-Chain Volatility | -0.6% | National, affecting all terminal manufacturers | Short term (≤ 2 years) |

| Data-Localization Compliance Cost Spike | -0.4% | National, regulatory compliance requirements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cyber-attacks Targeting POS Networks

Sophisticated breaches now target firmware and cloud gateways, inflating compliance budgets under the Personal Information Protection Law. Smaller acquirers struggle with 24/7 monitoring and may exit the market if license revocation risks escalate.

Price Pressure from SoftPOS Smartphone Apps

Lakala’s PCI-MPoC-certified SoftPOS attracted 350,000 users, highlighting a shift toward low-capex smartphone acceptance. Hardware vendors confront margin erosion and must pivot to hybrid models or embedded software offerings to sustain competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contactless Dominance Accelerates

Contactless systems captured 58.12% of the China POS terminals market share in 2025 and will grow at a 6.71% CAGR through 2031 as tap-and-go convenience aligns with hygiene preferences. The segment enjoys support from government rules lifting single-transaction caps for foreign visitors, spurring merchant upgrades to dual-scheme NFC terminals.

Biometric authentication layers, from facial recognition to fingerprint sensors, now accompany contactless flows, deepening solution complexity. Chip-and-PIN remains for high-value and cross-border transactions, preserving niche relevance. Beijing Metro’s multi-wallet acceptance proves that contactless devices can merge transport, retail, and international use cases under one chassis.

By POS Type: Mobile Solutions Drive Market Evolution

Mobile devices commanded 63.10% of the China POS terminals market size in 2025 and are set to clock a 6.79% CAGR through 2031, buoyed by SME mobility needs and unattended kiosk rollouts. Extended battery life, 5G modules, and cloud analytics elevate value propositions, while hybrid form factors blend printer docks with handhelds for QSR table-side service.

Fixed terminals persist in high-throughput venues demanding receipt printers, cash drawers, and multi-terminal synchronization. Yet transaction share concentration, up to 50% for the top five processors by March 2024, gives scaled acquirers bargaining leverage on hardware procurement. Vendors therefore pursue differentiated firmware, AI fraud modules, and service bundles to protect average selling prices.

By End-User Industry: Healthcare Emerges as Growth Engine

Retail remained the largest vertical with 34.22% revenue in 2025, benefitting from omnichannel payment consolidation mandates. However, healthcare leads growth at a 6.12% CAGR as 800,000 institutions integrate medical-insurance QR settlement, driving specialized Android terminals with insurance network APIs.

Hospitals require tight linkage to HIS platforms, co-payment splits, and PIPL-compliant patient data handling, setting entry barriers. Transportation, hospitality, and government services increasingly install certified terminals to meet foreign-visitor acceptance quotas, expanding addressable demand for multi-scheme hardware.

Geography Analysis

Tier-1 hubs, Beijing, Shanghai, Guangzhou, Shenzhen, anchor advanced deployments. Beijing’s Central Axis demonstration zone showcases foreigners’ tap-to-ride capability, while Shanghai outfitted 36,000 international-card-ready POS in commerce and tourism venues. These cities pilot AI risk controls, biometric layers, and Digital-Yuan cashier modes that cascade nationwide.

Tier-2 and tier-3 cities deliver the fastest shipment growth as rural modernization funds propel unattended smart POS across agriculture markets, bus depots, and government service halls. Vendors tailor ruggedized casings, solar power inputs, and simplified UIs to variable telecom conditions, capturing loyalty in price-sensitive clusters.

Cross-border gateways like the Greater Bay Area demand multi-currency settlement. UnionPay’s Project Excellence raised acceptance to 93.4% across 41 cities, recording 85.2% annual growth in foreign-card volumes by May 2024. Terminals must juggle UnionPay, Visa, Mastercard, JCB, and e-wallet QR codes while conforming to both PBOC and global scheme standards.

Competitive Landscape

Industry concentration intensified as POS transaction share of the top five processors climbed from 43% to 50% between June 2022 and March 2024, while licensed acquirers shrank to roughly 50 entities. PAX Technology posted USD 778 million revenue in 2024, scaling new Huizhou production to meet AI terminal demand.[3]Finance Sina Analysts, “新国都深度报告:深耕‘支付+终端’,” finance.sina.com.cn Newland Global Technology secured Luxembourg, Hong Kong, and U.S. regulatory clearances, expanding export breadth.

Competition pivots on vertical integration, overseas diversification, and compliance mastery. SoftPOS disrupts entry-level hardware, exemplified by Lakala’s 350,000-user base, yet hardware vendors counter with hybrid soft-hardware stacks delivering on-device security chips. HarmonyOS adoption reduces reliance on foreign OS kernels and optimizes domestic protocol handling.

White-space niches include healthcare insurance settlement, cross-border tourism sectors, and county-level unattended kiosks. Companies offering turnkey cyber-secure, AI-enabled, multi-scheme terminals aligned with local regulations command premium contracts despite price aggression from smartphone-based entrants.

China POS Terminals Industry Leaders

Fujian Newland Payment Technology Co., Ltd.

Verifone Systems LLC

Ingenico Group SA

PAX Global Technology Limited

New POS Technology Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Beijing unveiled a payment service zone along the Central Axis, introducing foreign-card tap-to-ride metro services for travelers from 100+ countries.

- February 2025: Alipay reported inbound visitor spending in Harbin jumped nearly fivefold during the Asian Winter Games.

- December 2024: PAX Technology opened its Huizhou industrial park to ramp AI-ready POS production capacity.

- October 2024: Newland Global Technology accelerated globalization, adding localized delivery in Europe, the United States, and Japan.

China POS Terminals Market Report Scope

The Point of sale is the time and location where a transaction is completed. A POS system is computer hardware and software that manages the transaction while selling a product or a service. It helps to store, capture, share, and report data related to sales transactions. It eases the shopping experience and helps to expedite the checkout process, resulting in customer satisfaction. Inventory management, stock in hand, availability of a product, and pricing information are primary data acquired from the systems.

China's POS Terminals Market is segmented by type (fixed point-of-sale systems, mobile/portable point-of-sale systems) and end-user industry (retail, hospitality, healthcare, and others).

The market sizes and forecasts are in terms of value (USD) for all the above segments.

By Mode of Payment Acceptance

| Contact-based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-User Industries |

| By Mode of Payment Acceptance | Contact-based |

| Contactless | |

| By POS Type | Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the forecast value of the China POS terminals market by 2031?

The market is projected to reach 9.37 billion USD by 2031.

Which payment mode is growing fastest in China’s POS ecosystem?

Contactless transactions, driven by NFC and biometric enhancements, are advancing at a 6.71% CAGR through 2031.

Why is healthcare a key opportunity for POS vendors in China?

Over 800,000 medical institutions now integrate insurance QR codes, pushing healthcare POS demand to a 6.12% CAGR.

How are SoftPOS apps affecting traditional POS hardware sales?

Smartphone-based acceptance solutions cut deployment costs, drawing 350,000 merchants and pressuring hardware margins.

What regulations most influence POS terminal design in China?

Digital-Yuan pilot rules, EMV-L3 transit standards, and strict data-localization laws shape hardware and software specifications.

Page last updated on: