Catalog Management System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.37 Billion |

| Market Size (2031) | USD 3.73 Billion |

| Growth Rate (2026 - 2031) | 9.56% CAGR |

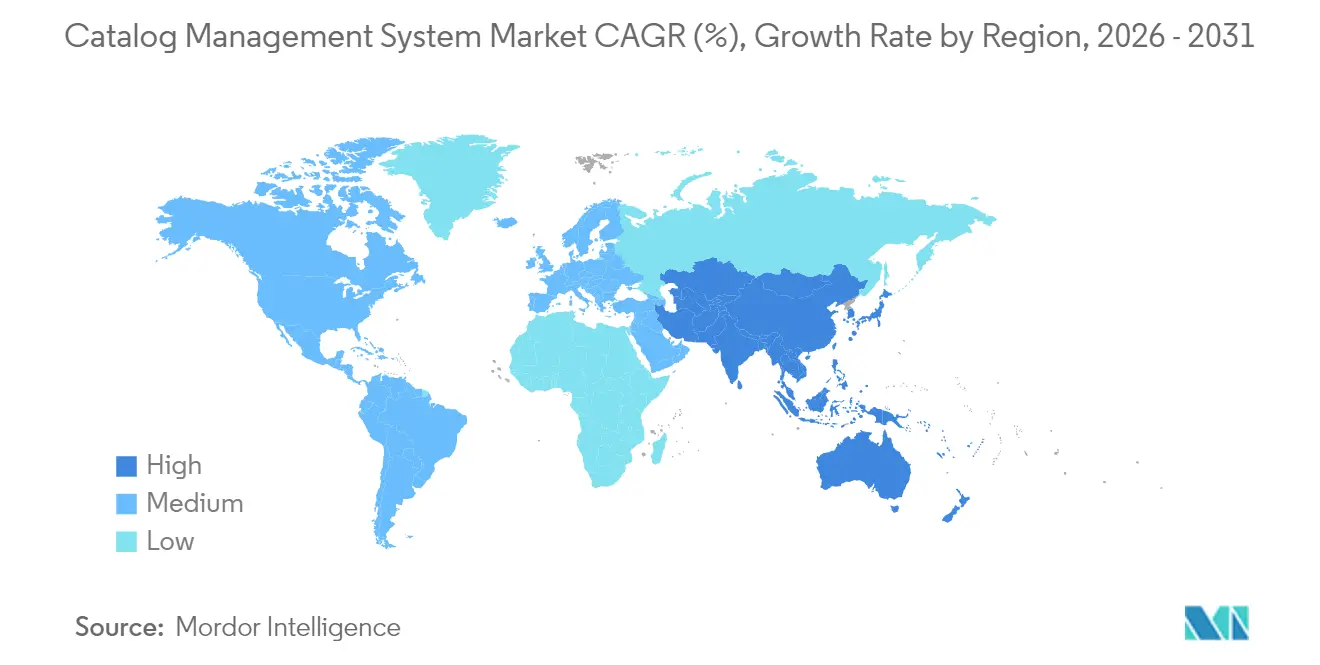

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

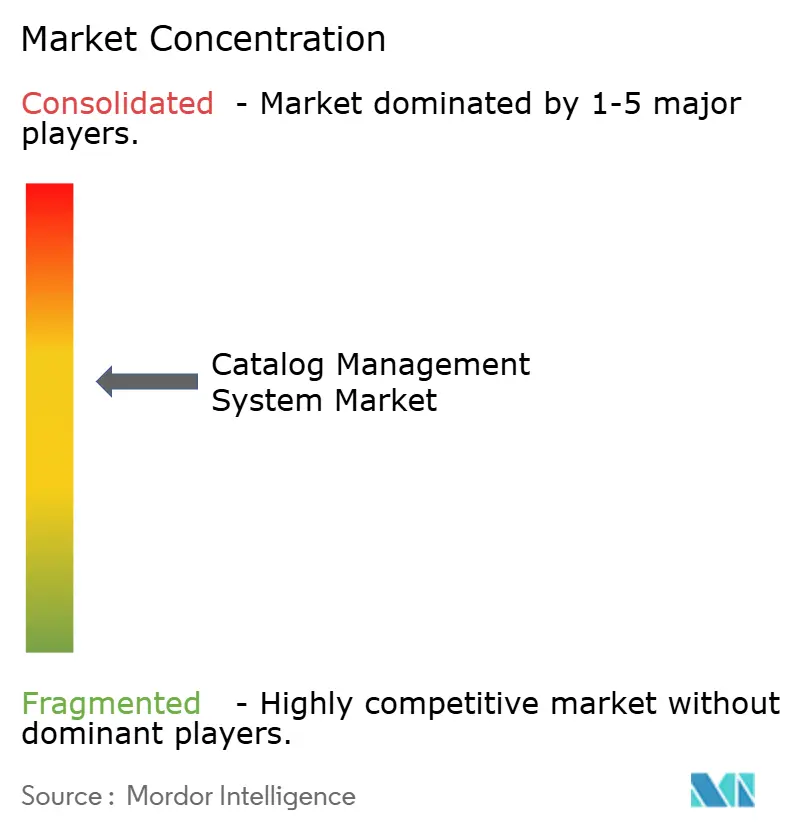

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Catalog Management System Market Analysis by Mordor Intelligence

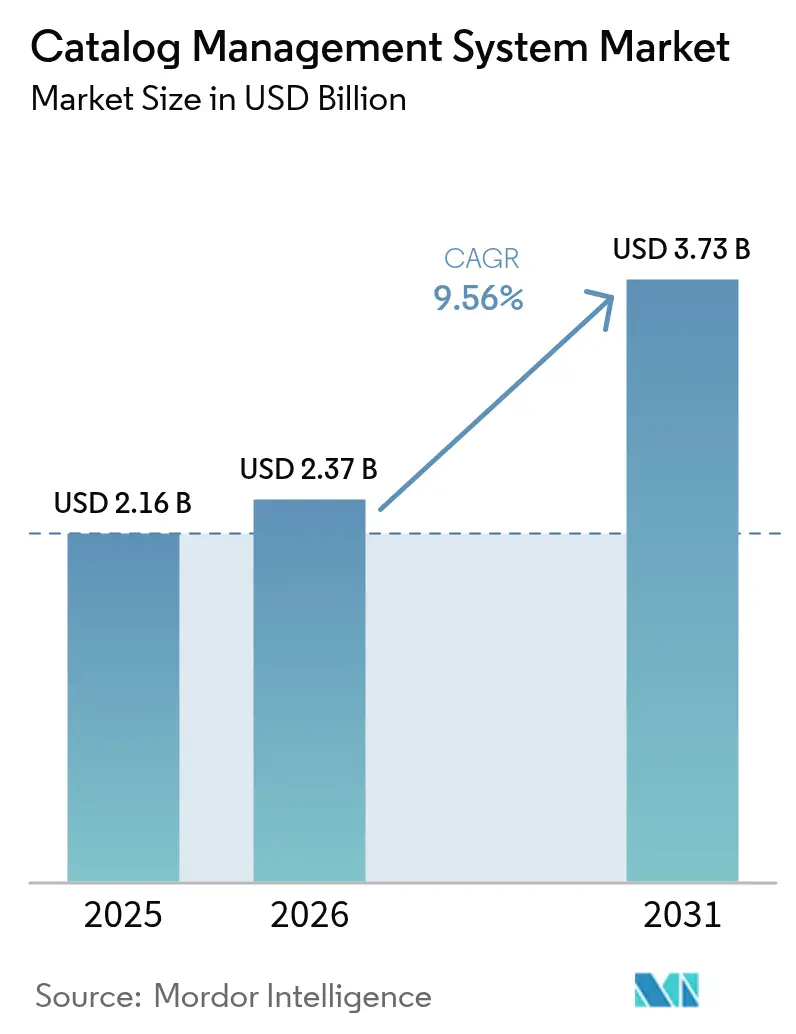

The Catalog Management System market size was valued at USD 2.16 billion in 2025 and estimated to grow from USD 2.37 billion in 2026 to reach USD 3.73 billion by 2031, at a CAGR of 9.56% during the forecast period (2026-2031). This growth stems from enterprises unifying product, service, and price data to power omnichannel commerce, hyper-personalization, and compliance with mandates such as the European Union’s Digital Product Passport requirement. Cloud software suites that combine low-code integration, AI-driven enrichment, and pre-built connectors continue to displace on-premises platforms, while service engagements expand as buyers seek external data-governance expertise. Retailers account for the largest share because they must synchronize millions of SKUs across various channels, including websites, mobile apps, marketplaces, and physical stores. In contrast, discrete manufacturers post the fastest growth as they embed catalog data into PLM and digital-twin workflows.[1]Siemens, “Teamcenter PLM Software,” plm.sw.siemens.com The shortage of catalog data stewards, ongoing cybersecurity threats, and the complexity of legacy ERP and CRM integrations temper the overall momentum; yet, aggressive investment by cloud providers and specialized PIM vendors keeps the outlook firmly positive.

Key Report Takeaways

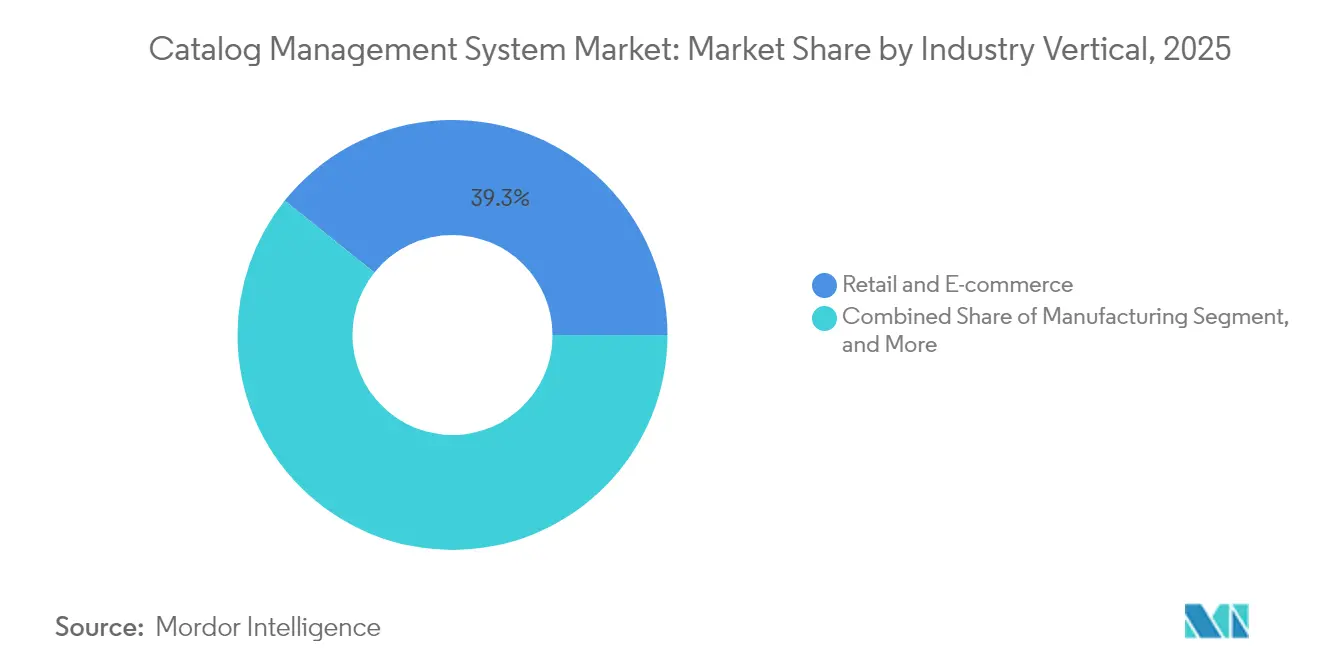

- By industry vertical, retail and e-commerce led with a 39.25% share of the Catalog Management System market in 2025; manufacturing is forecast to expand at a 13.86% CAGR through 2031.

- By deployment mode, cloud solutions commanded a 69.12% market share of the Catalog Management System market in 2025 and are projected to advance at a 11.09% CAGR through 2031.

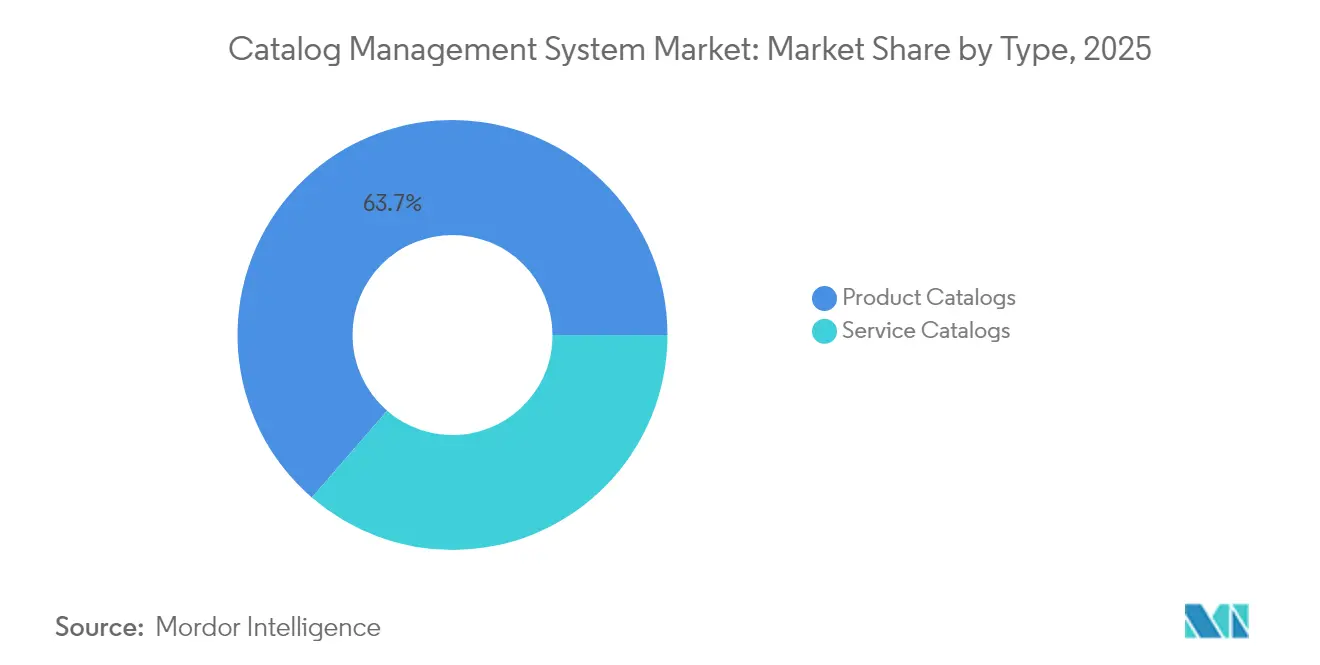

- By type, product catalogs held 63.65% of the Catalog Management System market share in 2025, while service catalogs are projected to grow at an 10.96% CAGR through 2031.

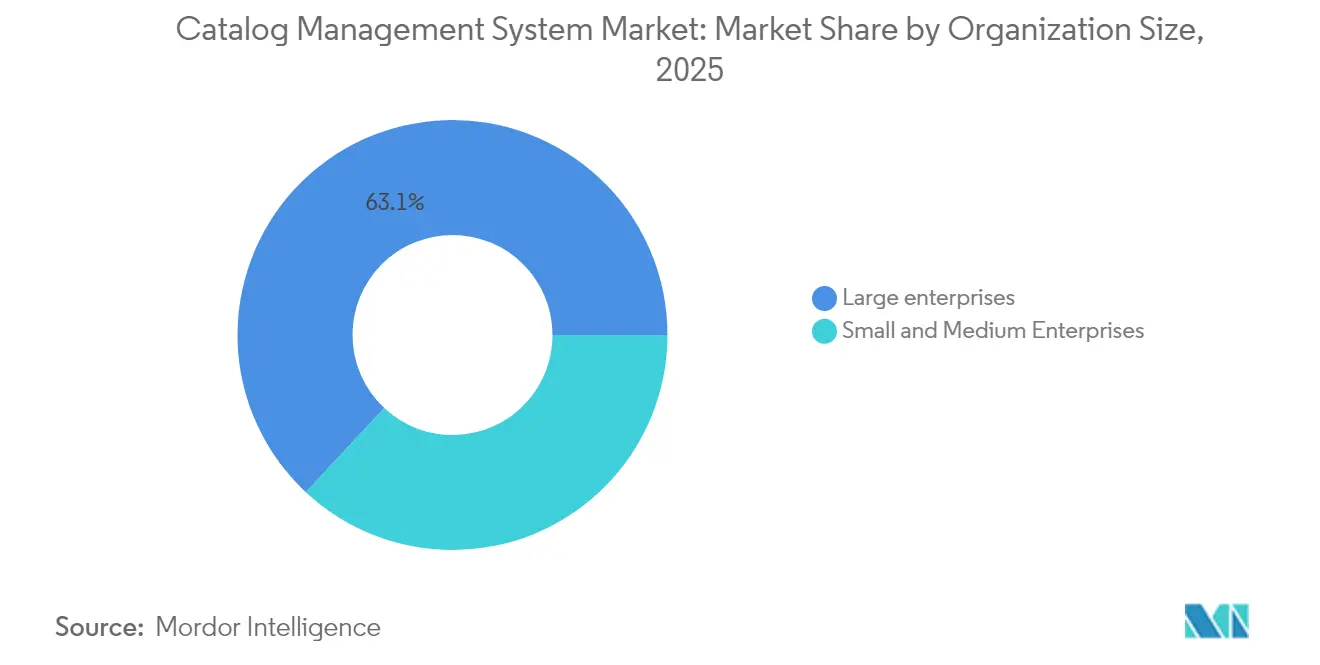

- By organization size, large enterprises accounted for 63.05% of the Catalog Management System market share in 2025, whereas small and medium enterprises are expected to expand at a 11.44% CAGR from 2025 to 2031.

- By component, solutions retained 59.55% of the Catalog Management System market share in 2025; services are set to rise at a 11.92% CAGR through 2031.

- By geography, North America captured 37.85% of the Catalog Management System market share in 2025, and the Asia Pacific is projected to grow at a 12.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Catalog Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven product enrichment and automated onboarding | +1.8% | Global, early uptake in North America and Europe | Short term (≤ 2 years) |

| Rapid expansion of omnichannel and headless commerce platforms | +2.1% | Global, strongest in North America, Europe, and Asia Pacific | Medium term (2-4 years) |

| Need for unified product data to enable hyper-personalization | +1.5% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Cloud migration strategies accelerating catalog SaaS adoption | +1.9% | Global | Short term (≤ 2 years) |

| Regulatory push for product-data transparency | +1.2% | Europe primary, spillover to North America and Asia Pacific | Long term (≥ 4 years) |

| Low-code integrations reducing deployment time and cost | +1.3% | Global, faster uptake in North America and Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Driven Product Enrichment and Automated Onboarding

Generative AI shortens onboarding cycles from weeks to hours by extracting attributes from unstructured supplier files, generating multilingual descriptions, and tagging images. Akeneo’s 2024 release utilizes large language models, reducing manual content creation by approximately 60% among early adopters.[2]Akeneo, “Akeneo PIM Platform,” akeneo.com Wayfair achieved 95% attribute-extraction accuracy for millions of SKUs, improving search relevance and conversions. Financial institutions now treat loans and policies as catalog items, parsing regulatory filings into structured records that feed customer-facing portals. The rise of agentic AI, which proposes catalog edits and flags inconsistencies, will deepen adoption, although safeguards such as human-in-the-loop reviews and explainable AI dashboards remain essential.

Rapid Expansion of Omnichannel and Headless Commerce Platforms

Headless architectures decouple front-end applications from back-end catalogs, enabling a single source of truth across web, mobile, voice, kiosk, and social channels. Adobe Commerce embeds generative AI to tailor recommendations and dynamic content blocks in real time. VTEX customers who automated catalog updates for more than 14,000 SKUs saw 30% conversion gains by synchronizing inventory across 100+ stores. Telecom operators deploy catalog-driven BSS suites to bundle connectivity, digital content, and IoT services; Ericsson’s solution at Grameenphone processes over 6 billion records daily. Composable commerce adoption drives demand for RESTful endpoints and event-driven catalogs that integrate seamlessly into iPaaS tools, such as Boomi.

Need for Unified Product Data to Enable Hyper-Personalization

Retailers and banks rely on consolidated catalogs to fuel recommendation engines and real-time pricing. Oracle has integrated AI Vector Search into Database 23ai, allowing merchandisers to instantly surface semantically similar products across SKU sets. ServiceNow’s Now Assist anticipates user intent, auto-populating request forms, and achieving 53% self-service resolution rates in pilots. As brands shift toward micro-segmentation, they syndicate rich product attributes, including sustainability and repair data, across channels, forcing governance teams to harmonize taxonomies company-wide. Success hinges on continuous data-quality monitoring and lineage tracking to prevent drift.

Cloud Migration Strategies Accelerating Catalog SaaS Adoption

Multi-tenant SaaS eliminates infrastructure overhead while delivering elastic scale and automatic upgrades. Oracle, ServiceNow, and Fujitsu introduced AI assistants and low-code tools throughout 2024-25, reducing the total cost of ownership by up to 50% and shortening the time-to-value by three months for enterprises migrating from legacy PIM installations. Informatica’s CLAIRE GPT recommends data-quality rules and enrichment steps, giving non-technical users direct control over catalog stewardship. Vendor R&D increasingly centers on cloud-first features, widening the capability gap with on-premises releases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy ERP and CRM integration complexity | -1.4% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Data-privacy and cybersecurity vulnerabilities | -1.1% | Global, heightened scrutiny in Europe and North America | Short term (≤ 2 years) |

| Shortage of skilled catalog data stewards | -0.9% | Global | Medium term (2-4 years) |

| Rising total cost of ownership for multi-domain PIM suites | -0.7% | Global, impacting mid-market buyers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy ERP and CRM Integration Complexity

Organizations running SAP ECC, Oracle E-Business Suite, or Salesforce spend months reconciling catalog schemas, pricing rules, and workflow triggers, often inflating project budgets by up to 50%. SAP’s RISE initiative simplifies some patterns yet still requires significant re-mapping. iPaaS vendors, such as Boomi, offer AI-generated data maps, but skilled staff remain necessary to fine-tune and maintain these integrations.[3]Boomi, “Boomi Enterprise Platform,” boomi.com Enterprises are increasingly adopting federated models that expose a unified API layer above disparate data sources, although this strategy requires robust master data governance and real-time quality monitoring.

Data-Privacy and Cybersecurity Vulnerabilities

Catalogs contain sensitive product specifications, margin data, and customer preferences, making them prime targets for ransomware. GDPR and CCPA require encryption, role-based access, and breach notifications for any personal data stored in catalog platforms. Vendors embed zero-trust architectures and anomaly detection, but misconfigured identity policies on the customer side can still expose data. Securiti’s automated masking and audit capabilities address these gaps, yet mid-market buyers often lack in-house security expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Service Catalogs Gain Momentum in IT and Telecom

Service catalogs accounted for 36.35% of the Catalog Management System market in 2025; however, they are projected to grow at a 10.96% CAGR through 2031, outpacing product catalogs. Product catalogs held a 63.65% market share in the Catalog Management System market in 2025, underscoring their foundational role in retail and manufacturing. ServiceNow’s Now Assist automatically populates service-request forms and recommends relevant offerings, raising self-service closure rates and supporting telecom operators that bundle connectivity with digital add-ons.

The convergence of product and service catalogs within unified platforms blurs traditional boundaries, allowing banks to treat loans and insurance as catalog items and manufacturers to sell product-as-a-service bundles. Telecom deployments such as Ericsson Catalog Manager at Grameenphone demonstrate how unified data models accelerate offer creation and billing for more than 6 billion records daily. Enterprises adopting hybrid models enjoy streamlined governance and analytics across tangible goods and intangible services, positioning service catalogs as a growth engine within the broader Catalog Management System market.

By Deployment Mode: Cloud Dominance Reflects SaaS Economics

Cloud deployments accounted for 69.12% of the Catalog Management System market size in 2025 and are projected to advance at a 11.09% CAGR through 2031. Oracle added AI Vector Search to its Fusion Cloud suite, enabling semantic queries over massive SKU libraries with millisecond latency. Informatica’s Intelligent Data Management Cloud introduced CLAIRE GPT to generate data-quality rules and natural-language queries, broadening access to catalog insights.

On-premises deployments persist in highly regulated sectors where data residency or air-gapped requirements remain strict, yet the feature gap is widening. Hybrid architectures catalog master data on-premises, but AI enrichment and syndication in the cloud serve as transitional models. Vendors now direct the bulk of their R&D efforts toward cloud-native capabilities, such as rapid AI model updates, low-code configuration, and embedded analytics, thereby reinforcing the cloud’s leadership position within the Catalog Management System market.

By Industry Vertical: Manufacturing Leads Growth as Digital Twins Mature

Retail and e-commerce retained 39.25% of 2025 revenue, while manufacturing is forecast to expand at a 13.86% CAGR through 2031. Siemens’ Teamcenter X synchronizes catalog data with engineering change orders and digital twin simulations, allowing global teams to collaborate in real-time. PTC’s Windchill and Dassault Systèmes’ 3DEXPERIENCE offer comparable capabilities, and together they encourage manufacturers to adopt unified catalog architectures that integrate engineering and commerce.

Banks and insurers modernize product catalogs to streamline origination and compliance, turning financial offerings into configurable catalog items that feed omnichannel portals. Telecom operators use catalog-driven BSS to bundle 5G connectivity with content and IoT services, while travel and hospitality providers adopt IATA-aligned offer-and-order catalog models. Healthcare, media, and other verticals adopt more gradually due to their fragmented IT landscapes, but they still recognize the strategic value of catalog governance.

By Organization Size: SMEs Accelerate as Vendors Simplify Onboarding

Large enterprises contributed 63.05% of the total 2025 revenue, driven by complex requirements and budgets that support enterprise-scale PIM suites. Small and medium enterprises are projected to grow at an 11.44% CAGR as vendors roll out tiered pricing and guided setup wizards. Plytix targets the mid-market with subscription plans and intuitive interfaces that allow non-technical staff to manage catalogs efficiently.

Low-code platforms reduce the skills barrier, letting SMEs configure taxonomies, workflows, and channel syndication without writing code. Marketplace operators, such as VTEX, enable sellers to update catalogs directly, thereby speeding up onboarding and minimizing administrative overhead. As these features mature, the Catalog Management System market is expected to see a more balanced revenue mix between large enterprises and SMEs.

By Component: Services Outpace Solutions Amid Governance Complexity

Solutions accounted for 59.55% of 2025 revenue; however, services, including implementation, managed governance, and ongoing catalog operations, are expected to grow at a faster rate of 11.92% CAGR. Systems integrators package industry templates and accelerators to shorten time-to-production, while managed-service providers handle continuous enrichment, quality monitoring, and syndication. Akeneo bundles managed services with its platform to help retailers keep content fresh and compliant.

Catalog success depends on both organizational change management and data stewardship as much as it does on software features. Enterprises that underinvest in services often encounter catalog drift, which diminishes their return on investment. Vendors respond with outcome-based contracts that tie service fees to accuracy, completeness, and business-metric improvements, reinforcing services as a critical growth lever in the Catalog Management System market.

Geography Analysis

North America led the Catalog Management System market with a 37.85% share in 2025, thanks to the early adoption of technology, retail, and financial services firms that embed AI enrichment, real-time pricing, and omnichannel syndication into their catalog workflows. Oracle’s Fusion Cloud AI Vector Search saw rapid uptake among U.S. enterprises seeking sub-second semantic queries across extensive SKU libraries. ServiceNow’s Now Assist achieved a 53% self-service resolution rate in Canadian pilot programs, underscoring the regional appetite for AI-driven catalog automation. Mexico and Canada accelerate adoption as cross-border commerce demands unified catalogs that support USMCA rules.

The Asia Pacific is forecast to advance at a 12.88% CAGR through 2031, driven by the expansion of e-commerce in China, India, Southeast Asia, and Australia. VTEX customers, such as Magazine Luiza, integrated 4.5 million SKUs and recorded a 30% month-over-month sales growth after expanding into Mexico. Chinese exporters utilize multinational PIM suites to synchronize data across domestic and international marketplaces, while Japanese manufacturers integrate catalogs into digital twin environments. South Korea, India, and Australia benefit from government support for digital transformation, further encouraging catalog investments.

Europe’s growth centers on regulatory compliance. The Digital Product Passport mandate obliges manufacturers to store granular sustainability metadata, driving catalog upgrades across Germany, France, Italy, Spain, and the United Kingdom. Russia’s market slows amid restricted access to Western cloud platforms, prompting domestic vendors to fill gaps. South America is witnessing an accelerating adoption as retailers, such as Magazine Luiza, modernize their catalogs to compete with Amazon and Mercado Libre. The Middle East and Africa remain smaller but opportunity-rich; telecom operators in Saudi Arabia, the UAE, and South Africa are deploying catalog-driven BSS solutions to support 5G launches, with Ericsson and Amdocs securing notable contracts.

Competitive Landscape

The Catalog Management System market is moderately fragmented. Enterprise software giants Oracle, SAP, and IBM embed catalog capabilities into their broader ERP and data-fabric suites, enabling customers to manage product, service, and customer records in a single environment. Specialized PIM vendors, including Akeneo, Salsify, Stibo Systems, and Syndigo, differentiate themselves through vertical depth, rapid deployment, and AI-powered enrichment. Telecom-focused suppliers such as Ericsson and Amdocs provide catalog-driven BSS platforms that orchestrate offers, pricing, and fulfillment at telecom scale.

White-space opportunities include SME-centric platforms with low-code onboarding, AI-generated multilingual content, and Digital Product Passport functionality. VTEX and Plytix capture mid-market demand with subscription pricing and simplified workflows. Generative AI integration becomes a key differentiator as vendors embed large language model capabilities for auto-population, bundling recommendations, and anomaly detection. Compliance modules, audit trails, lineage tracking, and sustainability templates gain importance in Europe, influencing buying decisions and shaping the competitive landscape.

Catalog Management System Industry Leaders

IBM Corporation

Oracle Corporation

SAP SE

Coupa Software Inc.

ServiceNow Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Aurachain introduced a banking-focused product-catalog use case that centralizes product lifecycle workflows across up to 10 departments.

- May 2025: Sabre unveiled SabreMosaic, an intelligent retailing platform for airlines that creates dynamic, personalized offers aligned with IATA’s Offer-and-Order framework.

- February 2025: Amdocs released CES25, integrating AI-driven catalog and GenAI Copilot features to automate offer creation and personalize telecom experiences.

- February 2025: Oracle has launched the Banking Originations Cloud Service, featuring dynamic product catalogs that enhance banker-customer conversations and expedite loan approvals.

- February 2025: VTEX reported that customers using its Seller Portal and Data Pipeline modules increased conversions by 30% by automating catalog updates for more than 14,000 SKUs.

- February 2025: Ericsson and Grameenphone extended their AI-powered BSS partnership, deploying Ericsson Catalog Manager to process 6 billion records daily and speed new-service launches.

- January 2025: Fujitsu expanded a strategic collaboration with AWS to train 12,000 engineers and migrate catalog workloads to Amazon Bedrock, accelerating digital transformation for automotive, finance, and retail clients.

Global Catalog Management System Market Report Scope

The Catalog Management System Market Report segments its analysis by Type, distinguishing between Product Catalogs and Service Catalogs. It further categorizes Deployment Mode into Cloud and On-Premises. Industry Verticals span IT and Telecom, Retail and E-Commerce, BFSI, Media and Entertainment, Travel and Hospitality, Manufacturing, Healthcare and Life Sciences, and Other Verticals. Organization Size is divided into Large Enterprises and Small and Medium Enterprises. Lastly, the report breaks down Components into Solutions and Services, the latter encompassing Professional Services and Managed Services. On a geographical scale, the report encompasses North America, South America, Europe, the Asia-Pacific region, and the Middle East and Africa, presenting market forecasts in terms of value (USD).

| Product Catalogs |

| Service Catalogs |

| Cloud |

| On-Premises |

| IT and Telecom |

| Retail and E-commerce |

| BFSI |

| Media and Entertainment |

| Travel and Hospitality |

| Manufacturing |

| Healthcare and Life Sciences |

| Other Industry Verticals |

| Large Enterprises |

| Small and Medium Enterprises |

| Solutions | |

| Services | Professional Services |

| Managed Services |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Type | Product Catalogs | ||

| Service Catalogs | |||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| By Industry Vertical | IT and Telecom | ||

| Retail and E-commerce | |||

| BFSI | |||

| Media and Entertainment | |||

| Travel and Hospitality | |||

| Manufacturing | |||

| Healthcare and Life Sciences | |||

| Other Industry Verticals | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Component | Solutions | ||

| Services | Professional Services | ||

| Managed Services | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Catalog Management System market?

The Catalog Management System market reached USD 2.37 billion in 2026 and is projected to hit USD 3.73 billion by 2031.

Which deployment model is growing fastest?

Cloud deployments are advancing at an 11.09% CAGR as enterprises favor SaaS economics and continuous feature updates.

Why are manufacturers investing heavily in catalog platforms?

They link catalogs to PLM and digital-twin tools, enabling configure-to-order models and real-time collaboration across global design teams.

How does AI improve catalog onboarding?

Generative models extract attributes, generate multilingual descriptions, and tag images, cutting manual effort by about 60%.

What role do regulations play in Europe?

The EU Digital Product Passport requirement compels catalog systems to store sustainability metadata, driving compliance-focused upgrades.

Why are services growing faster than software licenses?

Enterprises need external expertise for taxonomy design, governance, and continuous enrichment, making managed services a preferred option.

Page last updated on: