Pregnancy Detection Kits Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

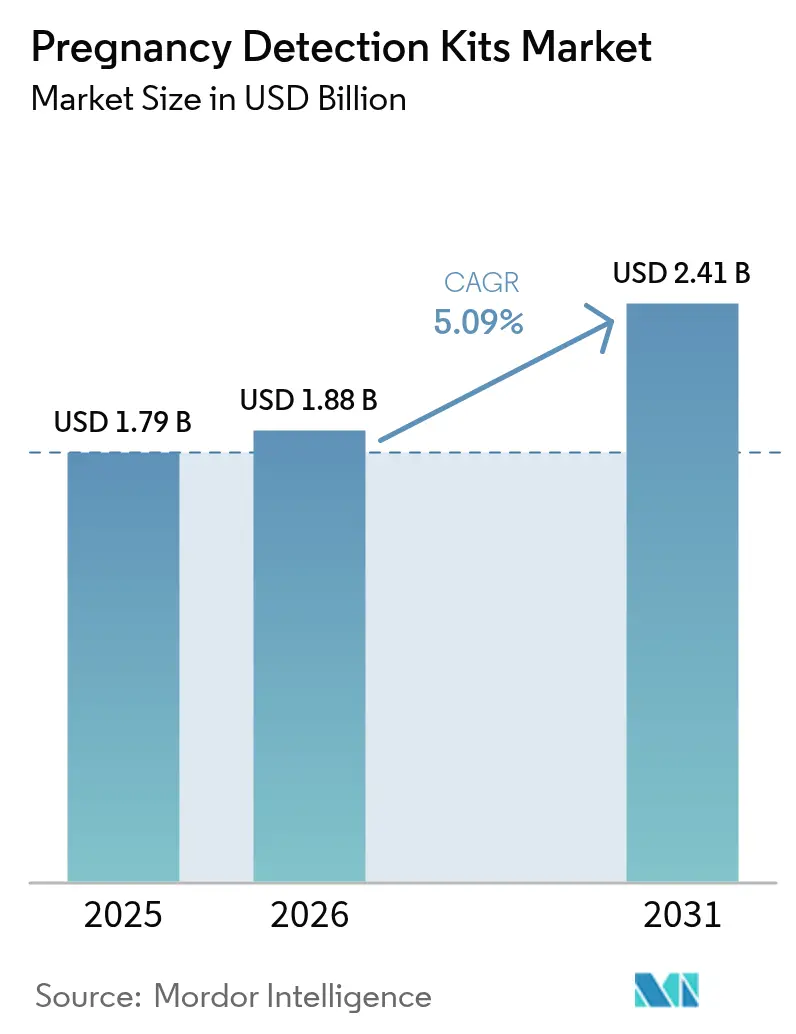

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

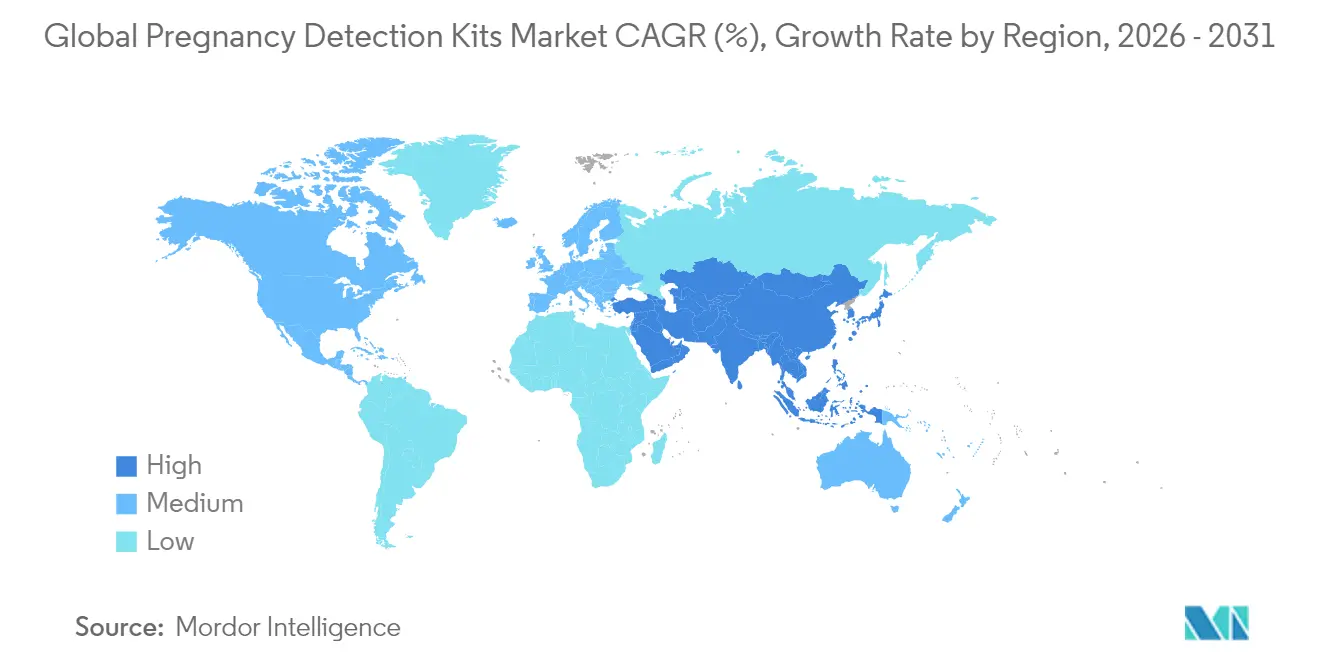

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pregnancy Detection Kits Market Analysis by Mordor Intelligence

The pregnancy detection kits market size is expected to grow from USD 1.79 billion in 2025 to USD 1.88 billion in 2026 and is forecast to reach USD 2.41 billion by 2031 at 5.09% CAGR over 2026-2031. Rising unplanned pregnancy incidence, rapid e-commerce penetration, and the shift toward home-based self-care position pregnancy tests as essential primary‐care tools that link consumers to broader reproductive-health ecosystems. Affordable line-format products continue to anchor high-volume sales, while digital and smart-connected devices carve a premium sub-segment by coupling Bluetooth-enabled readers with mobile-health apps. Regionally, North America retained a 39.72% share in 2024, yet Asia-Pacific is expanding faster at a 6.17% CAGR, helped by urbanization, rising disposable incomes, and improving retail infrastructure. Competitive differentiation now pivots on balancing cost leadership in commodity strips with investment in digital platforms that deliver recurring engagement, data analytics, and subscription-based revenue streams.

Key Report Takeaways

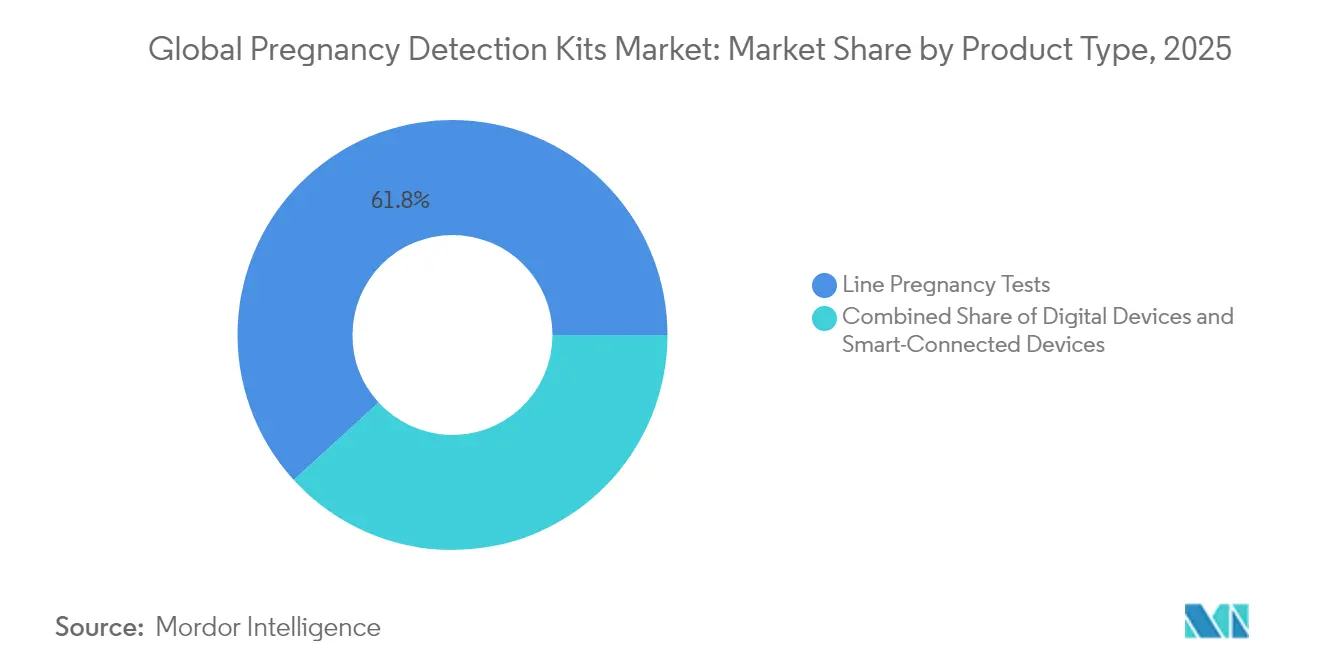

- By product type, line pregnancy tests captured 61.78% of the pregnancy detection kits market share in 2025, whereas smart-connected devices are forecast to accelerate at a 6.62% CAGR through 2031.

- By test type, urine hCG formats commanded 92.61% of the pregnancy detection kits market size in 2025, while blood hCG formats represent the fastest-growing segment at a 5.73% CAGR between 2026 and 2031.

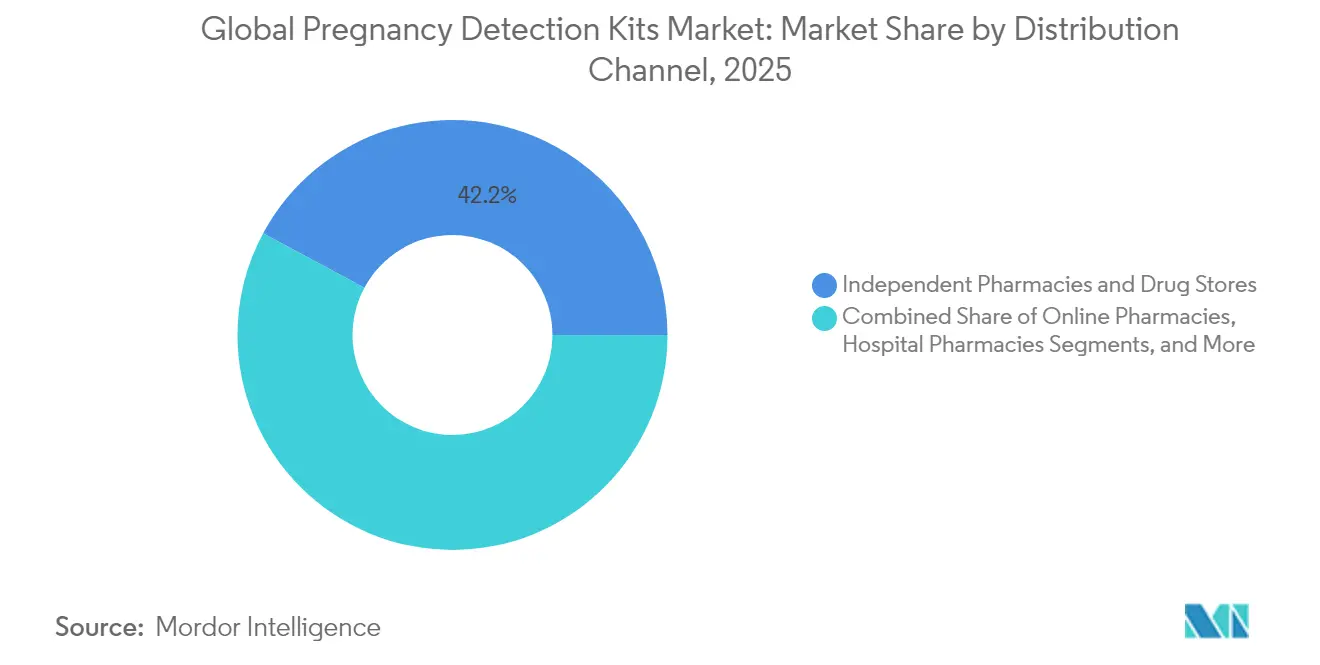

- By distribution channel, independent pharmacies & drug stores led with 42.15% revenue share in 2025; online pharmacies post the highest projected CAGR at 6.14% over the same period.

- By end user, home-care accounted for an 79.84% share of the pregnancy detection kits market size in 2025 and advances at a 5.92% CAGR to 2031.

- By geography, North America held 39.28% of global revenue in 2025, whereas Asia-Pacific is the fastest-advancing region at a 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pregnancy Detection Kits Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing incidence of unplanned pregnancies | +0.8% | Global with higher impact in developing regions | Medium term (2–4 years) |

| Increasing disposable income and willingness to spend on self-care | +0.7% | Core APAC; spill-over to MEA | Long term (≥ 4 years) |

| Wider retail & e-commerce penetration of home-testing products | +0.6% | Global led by North America & EU | Short term (≤ 2 years) |

| Regulatory backing for self-diagnostics in major markets | +0.5% | North America & EU expanding to APAC | Medium term (2–4 years) |

| Smartphone-linked digital test innovation | +0.4% | Global with early adoption in developed markets | Long term (≥ 4 years) |

| Male-partner involvement campaigns boosting early testing | +0.3% | Global with cultural variations | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Incidence of Unplanned Pregnancies

The World Health Organization estimates 121 million unintended pregnancies occur worldwide each year, sustaining baseline demand that buffers the pregnancy detection kits market against economic cycles. Demographic momentum in developing regions enlarges the target population, while delayed childbearing in developed markets elevates testing frequency as older women monitor fertility more closely. Pregnancy tests thus function as necessity goods rather than discretionary purchases, preserving revenue even when household budgets tighten. Public-health campaigns promoting early detection further normalize repeat self-testing. Combined, these factors anchor stable unit volumes and underpin incremental upgrades to higher-margin digital formats.

Increasing Disposable Income and Willingness to Spend on Self-care

Rising middle-class income in Asia-Pacific strengthens spending power and unlocks premiumization opportunities for Bluetooth-enabled devices that deliver app-based guidance and data tracking. Consumers view pregnancy testing as part of a proactive wellness routine, aligning with broader self-care and quantified-health trends. Employers in technology and finance add fertility benefits that reimburse pregnancy tests, integrating them into comprehensive reproductive-health programs led by platforms such as Maven and Kindbody. As reimbursement expands, manufacturers can justify price premiums by emphasizing accuracy, connectivity, and data security.

Wider Retail & E-commerce Penetration of Home-testing Products

Digital marketplaces remove geographic and social barriers, offering discreet delivery that resonates in culturally sensitive regions. Post-pandemic habits shifted consumers toward online checkout for health products, propelling pregnancy detection kits market growth via higher-margin direct-to-consumer channels. Subscription models boost repeat sales and capture life-cycle data valuable for cross-selling prenatal vitamins or ovulation kits. Meanwhile, brick-and-mortar pharmacies remain important for immediate need and professional counsel, underscoring the need for omnichannel inventory and pricing strategies.

Regulatory Backing for Self-diagnostics in Major Markets

The U.S. Food and Drug Administration has cleared more than 500 CLIA-waived urine hCG devices, signaling confidence in over-the-counter diagnostics and shortening time-to-market for incremental innovations[1]U.S. Food and Drug Administration, “Premarket Notification Database for hCG Tests,” fda.gov. The agency’s 2024 Laboratory Developed Test Final Rule imposes clearer quality-system obligations that advantage scale players able to absorb compliance overhead. European authorities likewise encourage self-testing under the In Vitro Diagnostic Regulation framework, further legitimizing home-use kits. A supportive regulatory climate lowers entry barriers for digital formats yet simultaneously pressures small firms to partner or consolidate.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low awareness and access in low-income nations | −0.4% | Sub-Saharan Africa, parts of South Asia | Long term (≥ 4 years) |

| Social stigma in parts of MEA & South Asia | −0.3% | MEA, South Asia, rural areas globally | Medium term (2–4 years) |

| Supply-chain Counterfeit Risks | -0.2% | Global | Short term (1-2 years) |

| Data-privacy Concerns with Connected Test Apps | -0.1% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Low Awareness & Access in Low-income Nations

Gaps in healthcare infrastructure restrict the pregnancy detection kits market in rural Africa and South Asia, where pharmacies are scarce and supply chains fragmented. Studies in Kenya and Uganda show many women are unaware of home-testing alternatives, relying instead on clinic visits that entail travel costs and wait times. Price sensitivity further limits adoption of digital formats, reinforcing reliance on the lowest-cost strips. Development agencies and NGOs pilot educational outreach and subsidized distribution, yet results remain localized. Until connectivity and retail logistics improve, market penetration in these areas will progress slowly, capping global CAGR uplift.

Social Stigma in Parts of MEA & South Asia

Cultural norms can discourage women from purchasing pregnancy tests openly, particularly outside marriage. Qualitative research in Cameroon and Pakistan finds that fear of community judgment steers consumers toward anonymous online purchases or away from testing altogether. Retail strategies such as discreet packaging and unbranded shipping partly mitigate the barrier, but broader attitudinal shifts require sustained public-health messaging and gender-equity programs. Manufacturers must tailor marketing content and product aesthetics to respect local sensitivities, balancing brand visibility with consumer privacy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Innovation Drives Premium Growth

Line pregnancy tests retained 61.78% revenue in 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au0 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au5, reflecting cost leadership and universal pharmacy presence. That dominance translates into a (USD 1.11 billion) slice of the pregnancy detection kits market size and underpins the category’s scale efficiencies. Yet smart-connected devices post a 6.6 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au% CAGR to 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au0 3EUROIMMUN AG, “FDA Clears EUROIMMUN hCG Assay,” euroimmun.com1, outpacing any other format by layering Bluetooth readers, companion apps, and personalized content that justify higher price points. Digital devices occupy a middle position, offering electronic readouts without connectivity—attractive to consumers seeking clarity but wary of data privacy.

Competitive responses illustrate an innovation stair-step. Church & Dwight’s 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au0 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au4 Multi Check kit integrates an EasyCup collector that simplifies sampling while holding price premiums below fully connected tests. FDA clearances for MissLan™ and Clearblue® Early Digital reinforce regulatory confidence in enhanced readability. Pipeline products such as Salignostics’ saliva-based kit, cleared by Australia’s TGA in December 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au0 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au4, hint at future disruption by eliminating urine collection entirely. Manufacturers that bridge utility and affordability across formats are best placed to capture the evolving pregnancy detection kits market.

By Type of Test: Urine Dominance with Blood Innovation

Urine-based hCG tests represented 9 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au.61% of sales in 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au0 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au5 and form the baseline technology of the pregnancy detection kits market. Robust clinician acceptance, CLIA waivers, and consumer familiarity anchor this share while economies of scale keep unit prices low. Blood-based rapid tests, though small, expand at 5.7 3EUROIMMUN AG, “FDA Clears EUROIMMUN hCG Assay,” euroimmun.com% CAGR because they detect pregnancy 6–10 days earlier, appealing to fertility-focused couples.

Atomo Diagnostics and NG Biotech secured a CE-marked blood-based kit in 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au0 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au4, targeting professional and later home-use markets. Home finger-stick adoption faces hurdles: consumer comfort, safe lancet disposal, and added regulatory scrutiny. However, early-detection benefits position blood tests as complementary rather than replacement products, widening the clinical toolkit for obstetricians and tele-fertility platforms. If U.S. FDA clearance follows, blood tests could nudge the pregnancy detection kits market share away from the urine oligopoly.

By Distribution Channel: E-commerce Disrupts Traditional Retail

Independent pharmacies & drug stores controlled 4 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au.15% revenue in 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au0 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au5 due to widespread storefronts and pharmacist trust. However, online pharmacies grow at 6.14% CAGR, propelled by discreet shipping and auto-replenishment subscriptions. Hospital pharmacies retain relevance for high-risk pregnancies needing clinician oversight, while modern retail & hypermarkets compete on price but lack privacy.

Direct-to-consumer brands leverage social media to build communities around reproductive health, converting one-time test buyers into multi-product customers. Fulfillment data grants insight into purchase cadence, enabling predictive marketing that boosts lifetime value. Yet brick-and-mortar remains resilient; many consumers still value immediate availability and the reassurance of professional advice, underscoring the need for blended omnichannel strategies within the pregnancy detection kits market.

By End User: Home-care Dominance Reflects Consumer Empowerment

Home-care users held 79.84% share and deliver a 5.9 2Therapeutic Goods Administration, “Australian Register of Therapeutic Goods,” tga.gov.au% CAGR, emphasizing a shift toward self-directed healthcare. Affordable multi-packs and clear digital readouts empower consumers to monitor status privately, aligning with telehealth’s rise. Gynecology and obstetrics clinics continue to supply confirmatory testing for positive results, and hospitals cover high-risk or fertility-treatment populations, yet their growth lags as routine testing migrates to households.

Telemedicine providers integrate app-connected results into virtual consults, creating a feedback loop that reinforces digital kit adoption. NIH-backed programs demonstrated that CLIA-waived home tests can feed secure portals used by nurse navigators, enhancing continuity of care. As reimbursement models evolve, insurers may subsidize multi-pack purchases to decrease costly emergency visits, deepening the pregnancy detection kits market penetration across socioeconomic tiers.

Geography Analysis

North America’s leadership stems from high retail density, advanced health insurance coverage, and FDA approval efficiency that accelerates product launch cycles. Consumers demonstrate strong brand allegiance, which sustains high repeat-purchase rates and encourages premium line extensions. Regulatory transparency under the CLIA waiver program and data-privacy legislation fosters consumer confidence in connected devices, supporting upscale growth within the pregnancy detection kits market.

Asia-Pacific provides the steepest growth curve, with India and China alone adding millions of new households to the addressable base annually. Urban working women favor discreet e-commerce purchases, while rising smartphone penetration accelerates adoption of Bluetooth-enabled tests that channel results into local language mobile apps. Government maternal-health initiatives in Indonesia and Vietnam include subsidized pregnancy test distribution, widening retail reach and stimulating volume gains.

Europe presents a mature, quality-focused environment prioritizing clinical validation and environmental stewardship. Cross-border e-pharmacies thrive under harmonized EU regulations, though local language labeling requirements demand tailored packaging. Sustainability credentials, such as reduced single-use plastics, influence purchasing decisions and create differentiation angles for incumbents attuned to eco-conscious preferences. Overall, regional nuances dictate marketing mix, packaging design, and regulatory strategy within the global pregnancy detection kits market.

Competitive Landscape

Moderate concentration defines the pregnancy detection kits industry. Abbott, Church & Dwight, Roche, and SPD Development collectively hold an estimated 55–60% of global revenue, leveraging decades of brand equity, distribution reach, and regulatory experience. Their volume advantage lowers unit costs, allowing competitive pricing even as they introduce premium digital offerings. Mid-sized firms differentiate via technology; Salignostics, for instance, pioneered saliva-based detection, while digital-native brands deploy app ecosystems that harvest anonymized data for cycle-tracking analytics.

Strategic moves illustrate a bifurcated playbook. Volume players protect share with multi-pack promotions and retailer exclusives, whereas innovators pursue higher margins through connectivity and subscription bundles. NFI Consumer Healthcare’s 2024 acquisition of the legacy e.p.t. brand demonstrates consolidation aimed at cross-leveraging sales channels. Everly Health’s 2023 takeover of Natalist integrates pregnancy tests into mail-order fertility labs, signaling convergence between diagnostics and at-home lab testing.

Patents cluster around optical sensing, smartphone imaging, and AI-driven faint-line detection, underscoring the rising digital stakes. FDA 510(k) clearances for EUROIMMUN’s chemiluminescence assay and Clearblue® Early Digital emphasize regulatory acceptance of incremental innovation3EUROIMMUN AG, “FDA Clears EUROIMMUN hCG Assay,” euroimmun.com. Counterfeit risk persists on online platforms, prompting leading brands to introduce QR code authentication. Going forward, firms that marry cost-efficient strip production with secure data ecosystems are positioned to outpace rivals within the pregnancy detection kits market.

Pregnancy Detection Kits Industry Leaders

Abbott Laboratories

bioMérieux SA

Church & Dwight Co., Inc.

Germaine Laboratories Inc.

QuidelOrtho Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cadence OTC unveiled EarlyPT, a high-sensitivity strip capable of detecting pregnancy six days before missed period, targeting premium consumers seeking earlier confirmation.

- December 2024: Salignostics secured Therapeutic Goods Administration approval for its saliva-based pregnancy test, the first such device cleared in Australia, enabling commercial rollout and global regulatory expansion.

- October 2024: Church & Dwight launched the First Response® Multi Check Pregnancy Test Kit featuring an EasyCup sampler that simplifies specimen collection while preserving low per-test cost.

- September 2023: Mankind Pharma expanded its Prega News line to six variants, catering to diverse price points and packaging preferences in India’s high-growth e-commerce segment.

Global Pregnancy Detection Kits Market Report Scope

As per the scope of the report, pregnancy test kits are medical devices that are used to diagnose the possibility of pregnancy in females. The device detects the amount of hCG (Human Chorionic Gonadotrophin), which increases in amount during the early stages of pregnancy in the body. The Pregnancy Detection Kits Market is segmented by Product Type (Line Pregnancy Tests (Test Cassette Format, Test Strip Format, and Test Midstream Format) and Digital Devices), Type of Test (Urine test for HCG and Blood test for HCG), Distribution Channel (Hospital Pharmacies, Independent Pharmacies, and Drug Store, Online Pharmacies, and Other Distribution Channels) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD) for the above segments.

| Line Pregnancy Tests | Test Cassette Format |

| Test Strip Format | |

| Test Midstream Format | |

| Digital Devices | |

| Smart-Connected Devices |

| Urine hCG Test |

| Blood hCG Test |

| Hospital Pharmacies |

| Independent Pharmacies & Drug Stores |

| Online Pharmacies |

| Modern Retail & Hypermarkets |

| Home-care (Individuals) |

| Gynecology & Obstetrics Clinics |

| Hospitals & Diagnostic Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Line Pregnancy Tests | Test Cassette Format |

| Test Strip Format | ||

| Test Midstream Format | ||

| Digital Devices | ||

| Smart-Connected Devices | ||

| By Type of Test | Urine hCG Test | |

| Blood hCG Test | ||

| By Distribution Channel | Hospital Pharmacies | |

| Independent Pharmacies & Drug Stores | ||

| Online Pharmacies | ||

| Modern Retail & Hypermarkets | ||

| By End User | Home-care (Individuals) | |

| Gynecology & Obstetrics Clinics | ||

| Hospitals & Diagnostic Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How accurate are the latest smartphone-connected pregnancy tests?

FDA-cleared Bluetooth models report ≥99% sensitivity and specificity when users follow the instructions exactly, matching the performance of laboratory immunoassays.

Which product format currently records the highest global sales?

Line-format urine strip tests lead with 61.78% share of 2025 revenue, thanks to low unit cost and universal pharmacy availability.

What growth rate is projected for blood-based rapid pregnancy tests?

Blood hCG kits are forecast to expand at a 5.73% CAGR between 2026 and 2031, driven by their ability to detect pregnancy 6–10 days earlier than urine methods.

Why is Asia-Pacific experiencing the fastest uptake of home testing?

Rising disposable incomes, expanding e-commerce logistics, and greater women’s workforce participation push regional demand, translating into a 6.05% CAGR through 2031.

Can consumers buy pregnancy tests from online pharmacies?

Yes; online pharmacies represent the quickest-growing channel at a 6.14% CAGR because they offer discreet shipping, subscription bundles, and competitive pricing.

How will the FDA’s LDT Final Rule influence kit manufacturers?

The rule raises compliance costs that favor larger firms with established quality-systems, likely prompting partnerships or acquisitions among smaller players seeking scale.

Page last updated on: