Smoking Cessation Aids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

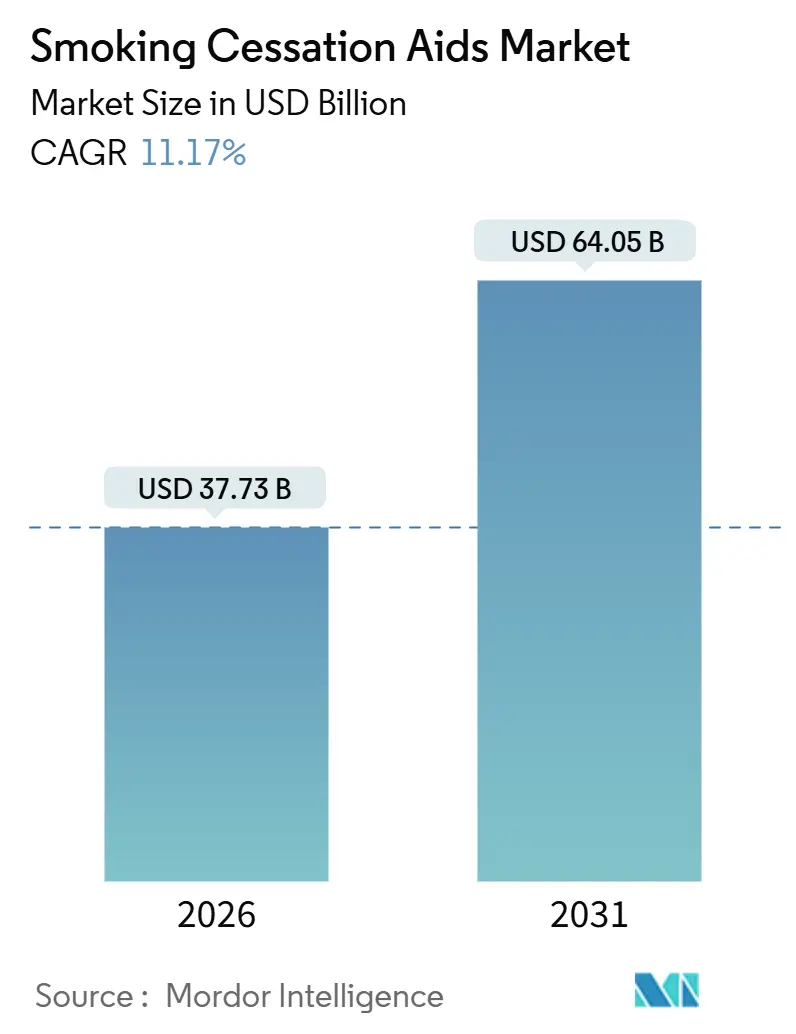

| Market Size (2026) | USD 37.73 Billion |

| Market Size (2031) | USD 64.05 Billion |

| Growth Rate (2026 - 2031) | 11.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smoking Cessation Aids Market Analysis by Mordor Intelligence

The Smoking Cessation Aids Market size is estimated at USD 37.73 billion in 2026, and is expected to reach USD 64.05 billion by 2031, at a CAGR of 11.17% during the forecast period (2026-2031).

Heightened tobacco taxes, rising employer-funded wellness plans, and broader reimbursement for over-the-counter (OTC) nicotine-replacement products continue to redirect smokers toward regulated nicotine delivery and behavioral support. Electronic nicotine delivery systems (ENDS) remain the leading revenue contributor, yet payers increasingly fund counseling add-ons because pharmacotherapy alone delivers sub-30% long-term abstinence. Retail pharmacies still provide the broadest shelf exposure, but e-commerce is closing the gap, helped by fast fulfillment models from Amazon Pharmacy and digital health integration at CVS. End-user behavior is also shifting: individual self-use dominates today, though insurer-mandated supervision is gaining traction. Regionally, North America commands the greatest share, but Asia-Pacific is expanding faster as hard-edged bans on flavored e-cigarettes spur demand for low-price patches and gums.

Key Report Takeaways

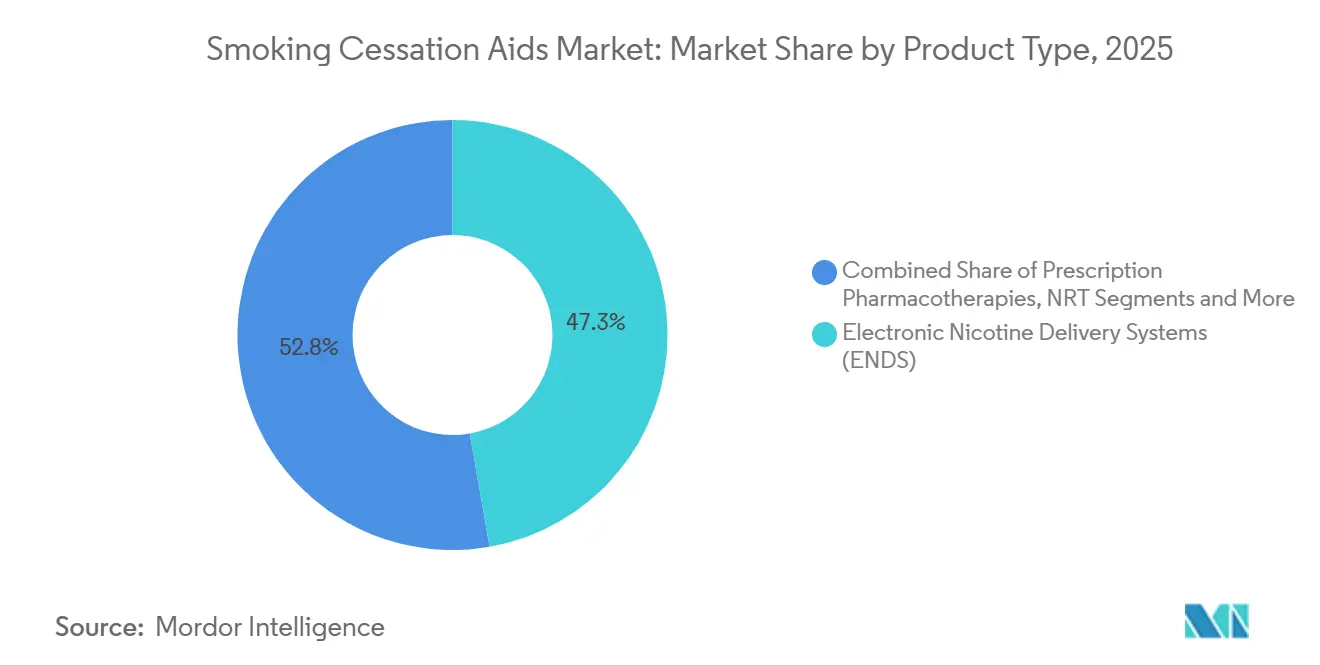

- By product type, electronic nicotine delivery systems accounted for 47.25% of smoking cessation aids market share in 2025, while behavioral support and services are forecast to expand at a 14.76% CAGR through 2031.

- By distribution channel, retail pharmacies and drug stores led with 41.85% of the smoking cessation aids market share in 2025; online pharmacies and e-commerce are advancing at a 15.03% CAGR to 2031.

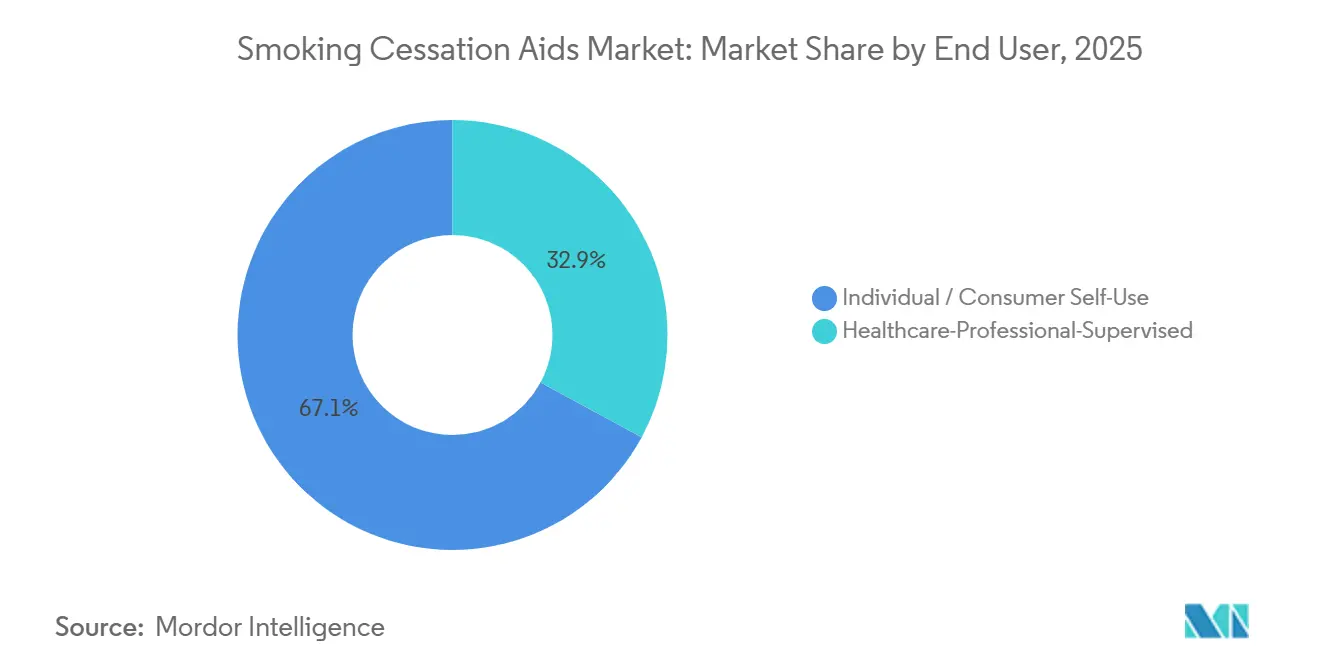

- By end user, individual self-use captured 67.12% of smoking cessation aids market size in 2025 and professional-supervised programs are on course for a 13.32% CAGR through 2031.

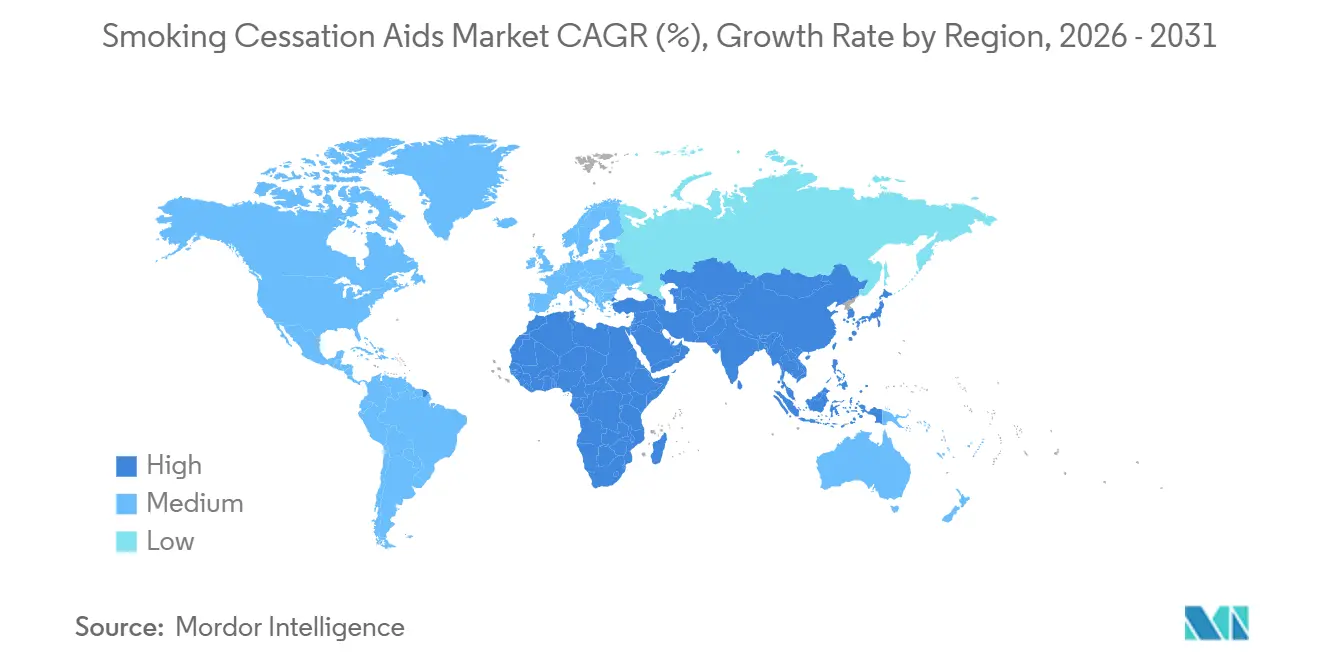

- By geography, North America held 34.83% of 2025 revenue and Asia-Pacific is on track for a 12.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smoking Cessation Aids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising quit attempts post-COVID-19 pandemic | +2.1% | Global, peak in North America and Europe | Short term (≤ 2 years) |

| Government tobacco-control taxes and smoke-free laws | +2.3% | Australia, UK, Canada, India, Brazil | Medium term (2-4 years) |

| OTC switch and wider reimbursement of NRT products | +1.8% | North America, Europe, GCC, South Africa | Medium term (2-4 years) |

| Digital health integration (apps, quitlines) | +1.5% | North America, Europe, Australia, urban Asia-Pacific | Short term (≤ 2 years) |

| Venture-backed psychedelic-assisted cessation trials | +0.9% | US, Canada, early Europe | Long term (≥ 4 years) |

| Employer-funded cessation benefits in emerging markets | +1.2% | India, China, Brazil, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Quit Attempts Post-COVID-19 Pandemic

Hospital admission data showed smokers experienced a 1.8-fold higher risk of severe COVID-19, driving a 23% spike in quitline calls during 2024 compared with pre-pandemic levels. Persisting respiratory complications make continued use physiologically difficult for many former patients, so cessation is now seen as essential care. The United Kingdom’s Swap to Stop campaign distributed free starter vape kits to 350,000 adults by mid-2025 and doubled six-month quit rates compared with unaided attempts.[1]Department of Health and Social Care, “Smokers Urged to Swap Cigarettes for Vapes in World-First Scheme,” GOV.UK, gov.uk Although the surge is expected to plateau by 2028, sustained public-health messaging under the WHO Framework Convention on Tobacco Control keeps the pressure high. These combined forces provide the smoking cessation aids market with a large influx of motivated quitters.

Government Tobacco-Control Taxes and Smoke-Free Laws

Australia lifted pack prices to AUD 50 (USD 33) in 2024 and cut adult smoking prevalence to 8.3%.[2]Michelle Scollo and Anita Lal, “What Tobacco Taxes Apply in Australia?,” Tobacco in Australia: Facts and Issues, tobaccoinaustralia.org.au Similar tax escalators in Canada and India narrowed the price gap between cigarettes and OTC patches that cost CAD 35 per two-week supply. Brazil’s 2025 extension of smoke-free zones reduces social triggers and normalizes abstinence. These measures compress combustibles’ affordability, inducing more quit attempts and buoying the smoking cessation aids market.

OTC Switch and Wider Reimbursement of NRT Products

The US FDA cleared stronger 4 mg lozenges for behind-the-counter sale in 2024, broadening access for heavy users. Fifteen US states dropped co-pays for all FDA-approved cessation medicines in 2025, prompting a 41% prescription jump among seniors. NICE in the UK began favoring dual-form NRT the same year, which doubled reimbursement claims. Patchy policies persist in Germany and elsewhere, but harmonized EU rules are likely after 2027, keeping reimbursement momentum positive.

Digital Health Integration (Apps, Quitlines)

Three smoking-cessation apps received 510(k) clearance in 2024, marking the FDA’s first software-only approvals in tobacco control. These mobile tools, paired with harm reduction-based smoking cessation approaches, show increased efficacy in smoking abstinence rates.[3]Yiqing Guo et al., “Effectiveness of Smartphone App–Based Interventions for Smoking Cessation: Systematic Review and Meta-analysis,” JMIR mHealth and uHealth, ncbi.nlm.nih.gov Quitline calls rose 34% in Australia once toll-free numbers appeared inside cigarette packs. While rural bandwidth limits adoption in parts of India, urban populations welcome this digital layer, further enlarging the smoking cessation aids market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-event recalls (varenicline nitrosamines) | -1.1% | Global, sharpest in North America and Europe | Short term (≤ 2 years) |

| Stringent e-cigarette flavor bans | -0.8% | UK, EU, California, Massachusetts | Short term (≤ 2 years) |

| Stagnant pharmacy shelf space | -0.6% | North America, Western Europe | Medium term (2-4 years) |

| High relapse rates | -0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse-Event Recalls (Varenicline Nitrosamines)

Pfizer’s recall removed varenicline for three years, forcing physicians to default to less effective options until reformulated tablets returned in 2024. By late 2024, prescriptions regained only 62% of prior volume, as clinicians waited for long-term safety data. New generics from Indian manufacturers entered Europe at lower prices yet face batch-testing rules that raise costs. The episode dented patient trust, with 34% now favoring unregulated alternatives.

Stringent E-Cigarette Flavor Bans

The UK outlawed fruit-flavored disposables in 2024, removing 68% of SKUs and shrinking legal sales 22%. Illicit imports quickly filled some demand, but patch sales also increased. California applied similar restrictions, eliminating 9,000 SKUs and cutting shelf space 40%. A draft EU directive aims to harmonize bans by 2027. These policies curtail youthful uptake but risk sending some users back to cigarettes, limiting ENDS growth inside the smoking cessation aids market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: ENDS Dominance Masks Behavioral Support Surge

Electronic nicotine delivery systems accounted for 47.25% of smoking cessation aids market revenue in 2025. Heated tobacco devices and nicotine pouches grew fastest inside the segment, fueled by IQOS ILUMA and Zyn distribution. Nicotine-replacement therapy (NRT) held 28%, with patches making up 42% of NRT receipts thanks to once-daily dosing and established reimbursement tracks. Prescription therapies contributed 18% but still lag due to the recent varenicline recall and uneven cytisine approvals.

Behavioral support and services will outpace all other lines with a 14.76% CAGR through 2031 as payers bundle counseling with medicines. Digital apps and quitlines, while small today, are mandatory components for many insurance plans. That shift enlarges total addressable demand and broadens competitive entry points for software-only players. Overall, the product mix highlights an incremental transition from pure pharmacotherapy toward holistic packages that blend devices, drugs, and coaching, a structure that broadens smoking cessation aids market share opportunities for newcomers.

By Distribution Channel: E-Commerce Disrupts Pharmacy Incumbency

Retail pharmacies owned 41.85% of 2025 revenue, yet their share slipped as Amazon Pharmacy launched same-day patch and gum delivery in 12 US metro areas. CVS added telehealth consults at online checkout, moving the in-store counseling model to the web. Hospital pharmacies commanded 22% because inpatient programs mandate cessation before discharge. Specialist vape shops accounted for 14% but now confront biometric ID rules that cut traffic 29% overall.

Online pharmacies and general e-commerce will compound at 15.03% through 2031, eroding brick-and-mortar dominance. Workplace wellness portals and direct-to-consumer subscriptions round out the remaining 22%, bypassing retail margins altogether. Omnichannel integration therefore becomes central to defending smoking cessation aids market share, especially as payment networks tighten compliance checks on cross-border flavor sales.

By End User: Professional Supervision Gains Reimbursement Traction

Individual self-use represented 67.12% of 2025 revenue. High relapse and low refill rates weaken its growth arc, but easy OTC access still pulls volume. In contrast, professional-supervised programs will see a 13.32% CAGR because insurers now require counseling records before reimbursing medicines. The United States permits eight funded counseling sessions per attempt with no annual cap.

Germany covers 80% of supervised program costs, prompting similar moves elsewhere. Workforce capacity remains a bottleneck, with only one tobacco-treatment specialist for every 15,000 smokers in the US. Telehealth eases some strain, yet state licensing barriers restrict interstate practice. The segment’s progress is therefore tied to policy reforms and digital service deployment, factors that reinforce long-run expansion of the smoking cessation aids market.

Geography Analysis

North America generated 34.83% of 2025 revenue. The United States alone contributed USD 12.4 billion, buoyed by Medicare’s expanded counseling coverage and private payers’ willingness to fund dual-form NRT. Flavor bans in several states created a near-term drag on ENDS but simultaneously drove patch and gum sales. Canada’s indexed excise tax further narrowed price gaps, sustaining demand for regulated substitutes.

Asia-Pacific posted the fastest growth, projected at a 12.79% CAGR. China’s ban on flavored e-cigarettes in 2024 redirected consumers to hospital pharmacy channels where patches and prescriptions dominate. India’s 2024 legal age hike and expanded pictorial warnings increase quit attempts, especially among urban smokers who already face higher cigarette prices. Employers in both countries now subsidize cessation programs, broadening access for middle-income groups. Low-cost cytisine also resonates in budget-constrained populations.

Europe supplied nearly 1/4th of 2025 turnover, led by the UK, Germany, and France. The UK’s Swap to Stop added 360,000 users and showed policy openness to harm-reduction pathways. Eastern European markets embraced cytisine due to attractive pricing, while Western payers still prioritize varenicline and dual-form NRT. The Middle East & Africa is supported by Gulf state investments in national quitlines, while South America is anchored by Brazil’s promise of universal pharmacotherapy coverage despite distribution gaps in remote regions. Collectively, these dynamics underscore varied regional drivers yet all funnel additional revenue into the smoking cessation aids market.

Competitive Landscape

The five largest suppliers include Haleon, Pfizer, Philip Morris International, British American Tobacco, and Johnson & Johnson, and together held a sizable share of 2025 sales, confirming moderate fragmentation. PMI’s USD 16 billion purchase of Swedish Match secured Zyn pouches and a broad U.S. store footprint, enabling cross-promotion with IQOS devices. Pfizer filed 14 patents on extended-release varenicline and GABA-combo formulas during 2024-2025, pointing to life-cycle management strategies.

New entrants such as Ditch Labs and Lucy Goods exploit direct-to-consumer subscriptions, trimming acquisition costs 40% below sector norms and targeting millennials who treat quitting as part of broader wellness routines. Tech-heavy plays include Haleon’s prototype smart patch that transmits dose data to companion apps. At the same time, psychedelic developers like Compass Pathways chase FDA breakthrough status, although reimbursement debate clouds commercial timelines.

Competitive white space clusters around low-price combination therapies for emerging markets, long-acting formats that improve adherence, and AI-driven digital coaching that predicts cravings. Players with in-house API capacity and advanced analytics stand to navigate tightening nitrosamine rules and batch-testing mandates most smoothly. As capital moves toward integrated device-drug-data portfolios, nimble software firms may partner or be absorbed, reshaping future smoking cessation aids market share allocations.

Smoking Cessation Aids Industry Leaders

British American Tobacco plc

Haleon plc

Johnson & Johnson (McNeil)

Pfizer Inc.

Philip Morris International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Achieve Life Sciences’ cytisinicline NDA received FDA acceptance with a PDUFA date of June 2026.

- August 2025: Zydus Lifesciences gained Health Canada approval for varenicline 0.5 mg / 1 mg tablets.

- May 2025: Aurobindo Pharma obtained final FDA approval for an abbreviated new drug application for varenicline tablets.

- January 2025: The FDA authorized marketing of 20 Zyn nicotine pouch SKUs via the PMTA pathway.

Global Smoking Cessation Aids Market Report Scope

As per the scope of the report, Smoking cessation aids include products, medications, therapies, and support systems that help individuals quit smoking by reducing cravings and withdrawal symptoms. These aids deliver nicotine without tobacco or act on brain chemistry and often incorporate behavioral support like counseling or therapy to address addiction's psychological aspects.

The smoking cessation aids market is segmented by product, distribution channel, end user, and geography. By Product Type, market is segmented by Nicotine Replacement Therapy (NRT), Prescription Pharmacotherapies, Electronic Nicotine Delivery Systems (ENDS), Behavioral Support & Services. By Distribution Channel, market is segmented by Retail Pharmacies, Hospital Pharmacies, Online Pharmacies, Specialist Shops. By End User, market is segmented into Individual Self-Use, Healthcare-Professional-Supervised). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in value (USD) for the above segments.

| Nicotine Replacement Therapy (NRT) | Patches |

| Gums | |

| Lozenges | |

| Sprays & Inhalers | |

| Other Oral & Transdermal | |

| Prescription Pharmacotherapies | Varenicline |

| Bupropion | |

| Cytisine | |

| Combination Therapies | |

| Electronic Nicotine Delivery Systems (ENDS) | E-cigarettes / Vaping Devices |

| Heated Tobacco Products | |

| Nicotine Pouches (Tobacco-Free Oral) | |

| Behavioral Support & Services | Digital / Mobile Apps |

| Telephone Quitlines | |

| In-person Counseling Programs |

| Retail Pharmacies & Drug Stores |

| Hospital Pharmacies |

| Online Pharmacies & E-commerce |

| Specialist Smoke/Vape Shops |

| Individual / Consumer Self-Use |

| Healthcare-Professional-Supervised (Clinics & De-addiction Centers) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Nicotine Replacement Therapy (NRT) | Patches |

| Gums | ||

| Lozenges | ||

| Sprays & Inhalers | ||

| Other Oral & Transdermal | ||

| Prescription Pharmacotherapies | Varenicline | |

| Bupropion | ||

| Cytisine | ||

| Combination Therapies | ||

| Electronic Nicotine Delivery Systems (ENDS) | E-cigarettes / Vaping Devices | |

| Heated Tobacco Products | ||

| Nicotine Pouches (Tobacco-Free Oral) | ||

| Behavioral Support & Services | Digital / Mobile Apps | |

| Telephone Quitlines | ||

| In-person Counseling Programs | ||

| By Distribution Channel | Retail Pharmacies & Drug Stores | |

| Hospital Pharmacies | ||

| Online Pharmacies & E-commerce | ||

| Specialist Smoke/Vape Shops | ||

| By End User | Individual / Consumer Self-Use | |

| Healthcare-Professional-Supervised (Clinics & De-addiction Centers) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the smoking cessation aids market in 2026?

It reached USD 37.73 billion in 2026 and should expand to USD 64.05 billion by 2031.

What is the forecast CAGR for smoking cessation aids through 2031?

Mordor Intelligence projects an 11.17% CAGR for the period 2026-2031.

Which product category grows fastest over the forecast?

Behavioral support and services lead with a 14.76% CAGR.

Why is Asia-Pacific growing faster than North America?

Flavor bans and new tobacco-control laws in China and India are boosting demand for lower-cost patches and gums.

What role does e-commerce play in distribution?

Online pharmacies and e-commerce are increasing at a 15.03% CAGR, eroding traditional retail share by offering fast delivery and integrated digital coaching.

Page last updated on: