COVID Testing Kit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

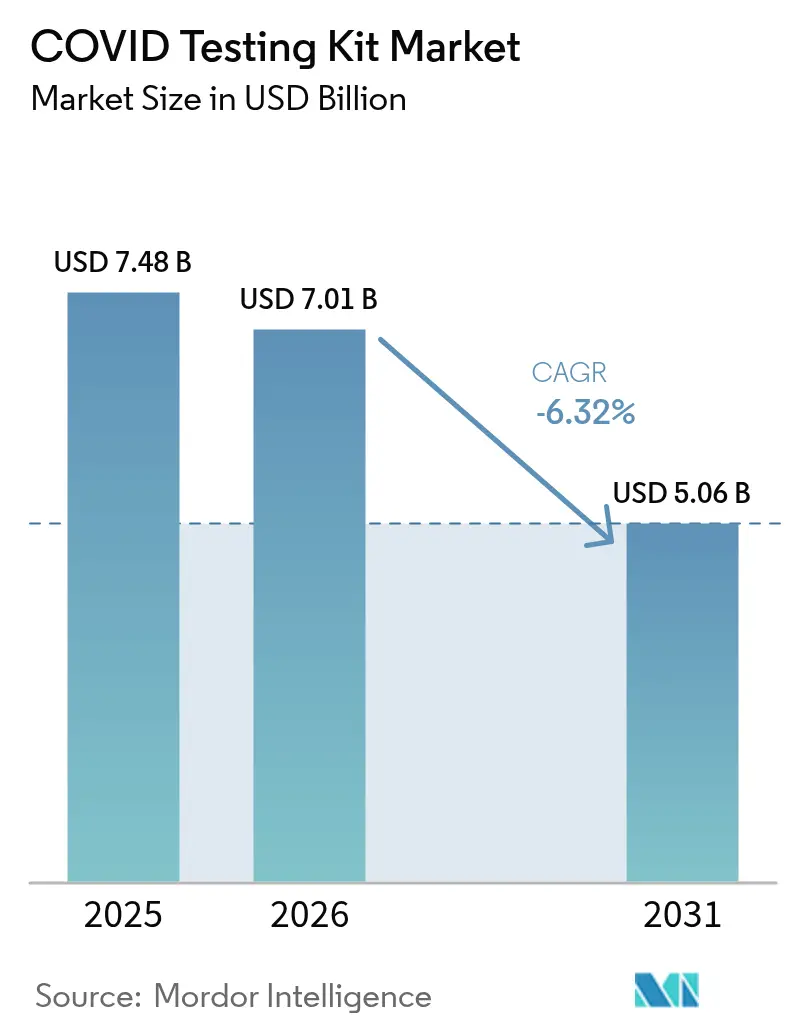

| Market Size (2026) | USD 7.01 Billion |

| Market Size (2031) | USD 5.06 Billion |

| Growth Rate (2026 - 2031) | -6.32% CAGR |

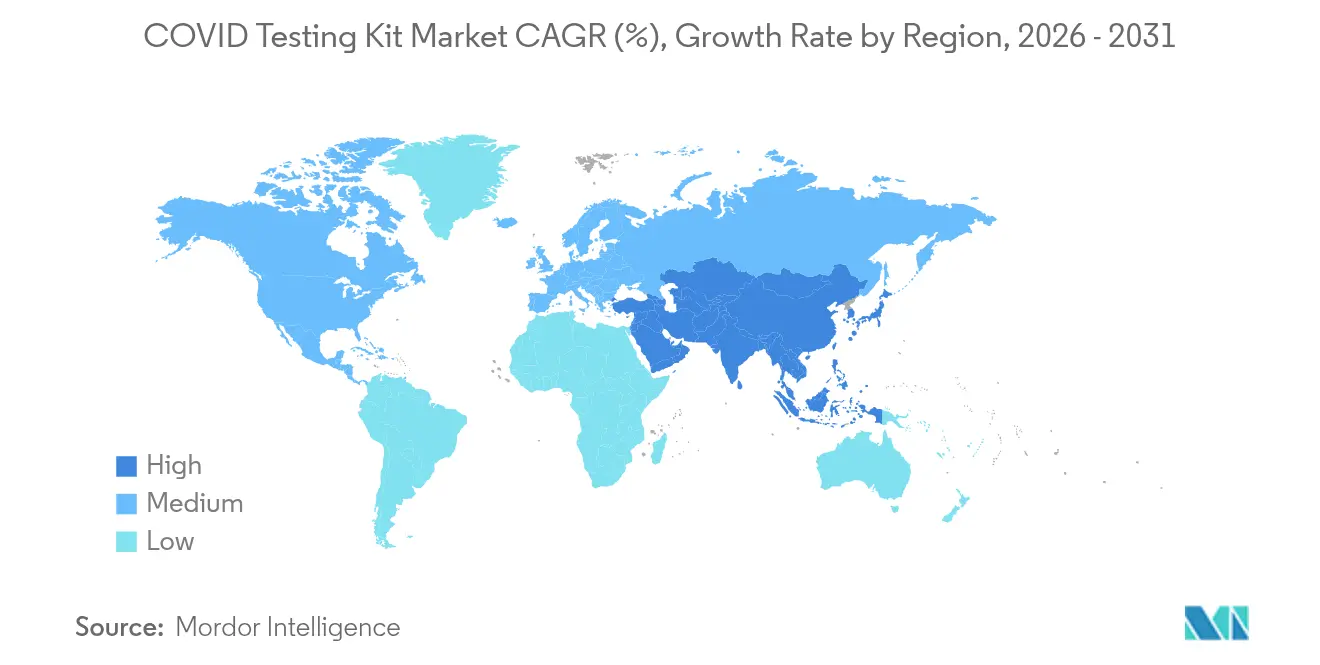

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

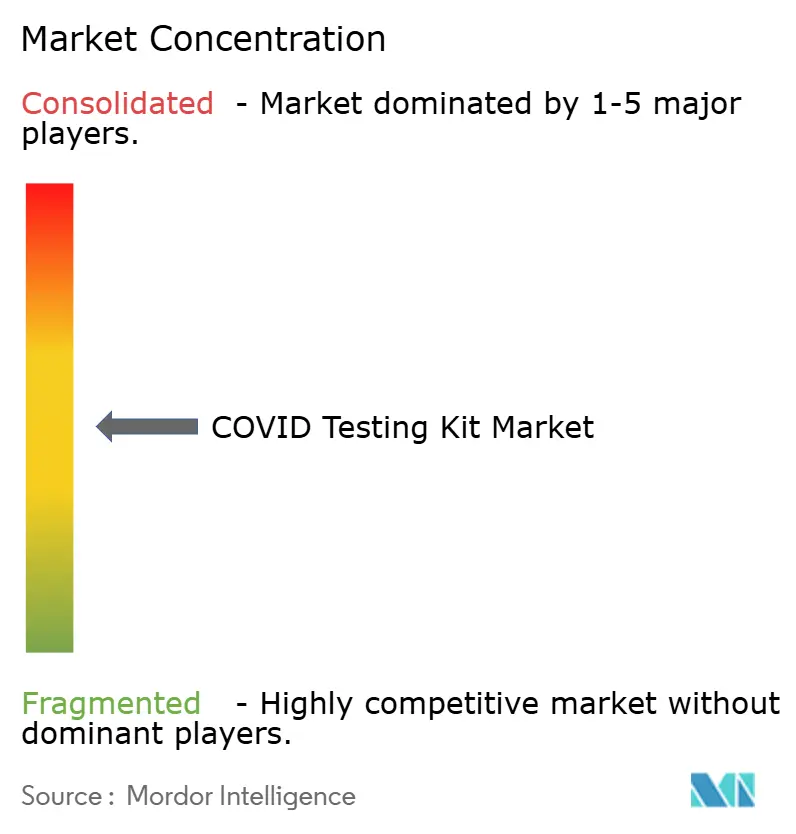

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

COVID Testing Kit Market Analysis by Mordor Intelligence

The COVID Testing Kit Market size was valued at USD 7.48 billion in 2025 and estimated to grow from USD 7.01 billion in 2026 to reach USD 5.06 billion by 2031, at a CAGR of -6.32% during the forecast period (2026-2031).

This downward trajectory conceals rapid post-pandemic innovation, rising demand for ultra-rapid molecular platforms, and growing government stockpiles that together soften the pace of revenue decline. Enterprises that dominated pandemic-era volumes now pivot toward multiplex respiratory panels, digital result reporting, and direct-to-consumer channels to protect margins and manufacturing scale. Payors are dismantling blanket reimbursement for routine COVID tests, yet institutional procurement programs from health ministries, the U.S. Strategic National Stockpile, and other government buyers keep baseline demand intact. Market leaders are therefore optimizing production footprints for lower volumes, adding AI-enabled connectivity, and pairing test kits with telehealth services to sustain recurring revenue.

Key Report Takeaways

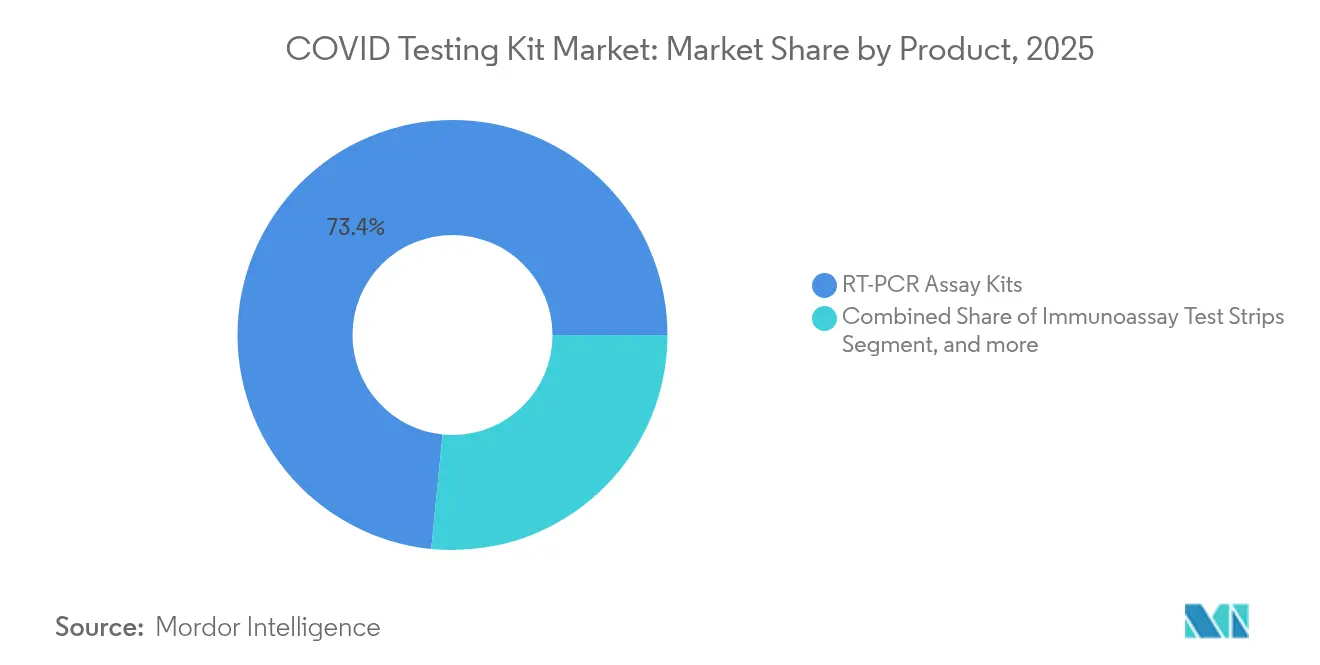

- By product, RT-PCR assay kits led with 73.42% of COVID testing kit market share in 2025; CRISPR-based molecular kits are projected to expand at a 1.90% CAGR through 2031.

- By specimen, nasopharyngeal swabs accounted for 58.35% of the COVID testing kit market size in 2025, whereas saliva testing is advancing at a 2.08% CAGR over the forecast window.

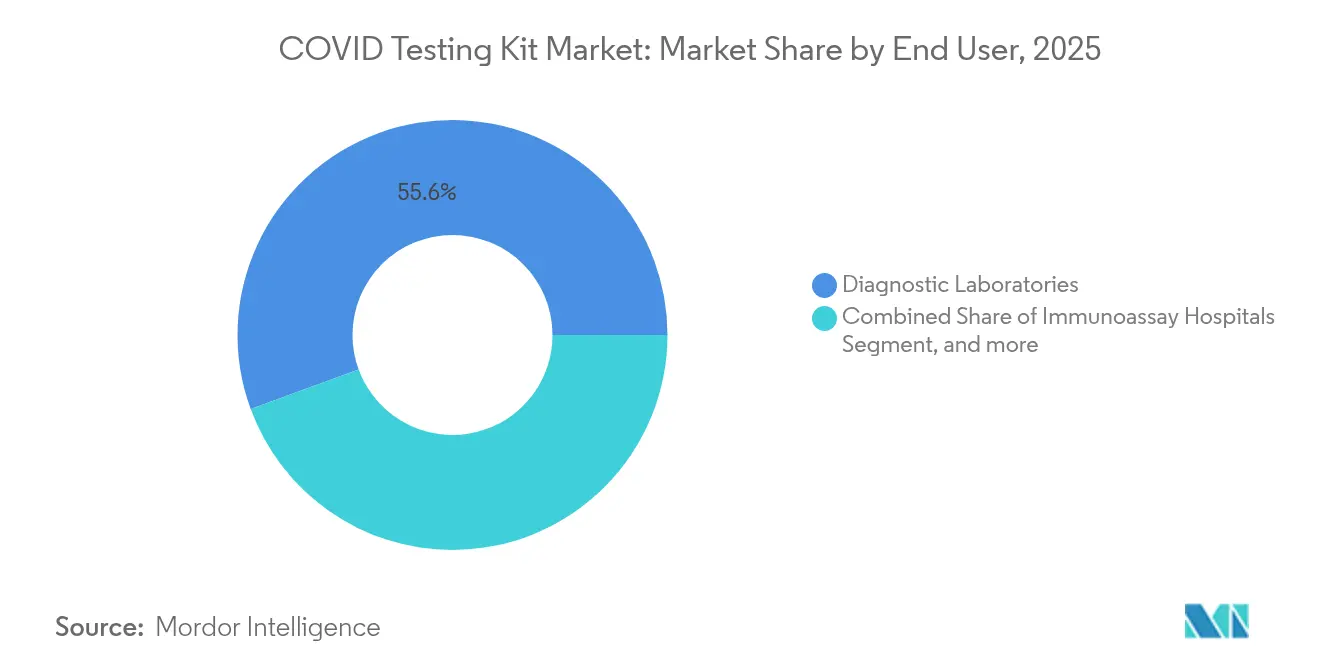

- By end user, diagnostic laboratories held 55.60% revenue share in 2025; home care settings are set to grow at a 2.18% CAGR to 2031.

- By geography, North America commanded 39.30% of the COVID testing kit market in 2025, while Asia-Pacific represents the fastest-growing region at a 1.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global COVID Testing Kit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Incidence of COVID-19 & Continuous Variant Emergence | -2.1% | Global, with concentrated impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Expanding Governmental Stock-Piling Programs for Future Outbreaks | +1.8% | North America, Europe, select APAC countries | Long term (≥ 4 years) |

| Rapid Consumer Shift to Self-Testing & Tele-Health Integration | +1.2% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Commercialisation of CRISPR-Based Ultra-Rapid Diagnostics | +0.9% | North America, Europe, urban APAC centers | Medium term (2-4 years) |

| Digital Connectivity/AI-Enabled Result Reporting Mandates | +0.7% | Developed markets, select urban centers globally | Long term (≥ 4 years) |

| Multiplex Respiratory Panels Replacing Single-Pathogen Tests | +1.4% | Global healthcare systems, institutional buyers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Incidence of COVID-19 Variants

The virus’s evolution toward seasonal patterns similar to influenza reduces the urgency for mass testing but preserves baseline surveillance requirements. The WHO’s advisory group now focuses on XBB-lineage strains, signaling a move to vaccinate and monitor rather than broadly screen entire populations.[1]World Health Organization, “Technical Advisory Group on COVID-19 Vaccine Composition,” who.int Labcorp reported a sequential fall in COVID testing revenue of 1.9% in Q1 2024 and 0.9% in Q2 2024, a pattern echoed across major laboratories as acute-phase demand subsides. Diagnostic companies must therefore balance lower volumes with the need to maintain sequencing capacity for variant detection. Platform flexibility and integrated data reporting become important differentiators as health agencies continue to rely on laboratories for genomic surveillance. Manufacturers that embed variant-specific primers into existing assays can capture ongoing institutional demand without incurring the cost of new kit development.

Expanding Governmental Stockpiling Programs

Government preparedness initiatives create a demand floor even as private-sector ordering wanes. The U.S. Department of Health and Human Services has invested more than USD 3 billion to maintain domestic rapid test production and procured 500 million at-home tests for strategic reserves.[2]U.S. Department of Health & Human Services, “Rapid Test Procurement Contracts,” hhs.gov Similar procurement frameworks in the European Union guarantee manufacturers multi-year purchase commitments, offsetting margin erosion in retail channels. By stabilizing baseline production, these contracts help suppliers retain skilled labor and sustain quality systems required under ISO 13485 and FDA Quality System Regulation. In return, governments gain assured surge capacity for future outbreaks, supporting broader national security goals.

Rapid Consumer Shift to Self-Testing

Saliva-based diagnostics that users can collect at home reach 97.8% detection rates when processed with optimized bead-mill homogenizers, closely matching laboratory-collected nasopharyngeal swabs.[3]Brian Labus, “Self-Collected Saliva Shows High Sensitivity for SARS-CoV-2,” Science Daily, sciencedaily.com At-home sampling eliminates healthcare-worker exposure and reduces personal protective equipment use, lowering overall system costs. Digital apps that interpret line-intensity and transmit results to public-health dashboards further strengthen adoption in North America and Europe. Integration with telehealth services allows physicians to issue antiviral prescriptions and isolation guidance within minutes, transforming a single-use test into a gateway for virtual care. Kit makers that package intuitive instructions, companion apps, and multilingual support see higher repeat purchase rates, particularly among elderly and pediatric populations.

Commercialization of CRISPR-Based Diagnostics

CRISPR-Cas systems coupled with isothermal amplification now deliver results in nearly real time. Mammoth Biosciences’ DETECTR BOOST kit processes roughly 1,500 samples per eight-hour shift while bypassing supply-chain constraints associated with conventional enzymes. Columbia Engineering researchers have demonstrated a plasmonic nanoparticle RT-PCR platform that cuts turnaround time to 23 minutes without sacrificing sensitivity. Such innovations are crucial for emergency-department triage and for airports aiming to reopen international travel with minimal delays. While regulatory pathways remain complex, early-adopting hospitals that run CRISPR-based assays alongside traditional RT-PCR are reporting workflow efficiencies and lower reagent costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Test Volumes as Pandemic Moves to Endemic Phase | -4.2% | Global, most pronounced in developed markets | Short term (≤ 2 years) |

| Price Commoditisation Squeezing Margins for Kit Makers | -2.8% | Global, particularly competitive in North America and Europe | Medium term (2-4 years) |

| Accuracy Concerns with Unsupervised Home Sample Collection | -1.1% | Primarily developed markets with high self-testing adoption | Short term (≤ 2 years) |

| Bio-Hazardous Plastic Waste & Disposal Compliance Costs | -0.7% | Global, with stricter enforcement in Europe and developed APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Test Volumes as Pandemic Subsides

Diagnostic companies have reported 70-90% drops in COVID test orders compared with peak 2021 levels. Abbott cut 199 jobs at its Maine facility, and Cue Health reduced headcount by 170 as public funding pivoted toward vaccines and therapeutics. Fixed manufacturing overhead now spreads across smaller batches, intensifying cost pressures. Laboratories are rationalizing inventories, carrying just-in-time stocks rather than months of safety supplies. In this environment, suppliers are shuttering satellite plants, automating packaging lines, and renegotiating raw-material contracts to align capacity with new baseline demand.

Price Commoditization Squeezing Margins

Emergency premium pricing has evaporated, placing commodity-level price caps on most antigen and RT-PCR kits. Major diagnostics firms disclosed sharp revenue declines linked to COVID testing: DiaSorin –13.7%, Quest Diagnostics –6.4%, Danaher –11.7%, and Abbott –39.4% year-on-year in 2024 earnings reports. Competitive tenders from pharmacies and online retailers now favor low-cost suppliers, compressing gross margins. To protect profitability, manufacturers are expanding value-added services such as digital result archiving, workplace screening programs, and assay customization for combined respiratory panels. Those unable to bundle software, analytics, or multi-pathogen capability risk competing purely on price, triggering further consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Innovation Offsets Volume Decline

RT-PCR assay kits sustained their lead with 73.42% COVID testing kit market share in 2025 as hospitals and reference labs trust their accuracy for regulatory and reimbursement compliance. However, the CRISPR-based molecular subgroup is projected to log the highest 1.90% CAGR through 2031, reflecting laboratory demand for rapid, point-of-care workflows. Immunoassay cassettes capture mass-screening orders yet face margin erosion, while next-generation sequencing panels remain confined to variant surveillance programs. Multiplex respiratory assays that detect SARS-CoV-2, influenza A/B, and RSV in a single run clock in at 97-100% accuracy with sub-hour turnaround, a capability that supports their premium pricing.

The segment reveals a split between commodity tests and higher-value specialized diagnostics. Companies that deploy modular cartridge systems can swap reagents to meet seasonal pathogen patterns, thereby shielding revenue. Columbia Engineering’s 23-minute RT-PCR prototype hints at future benchmarks for emergency-department throughput. Simultaneously, CRISPR assays that distinguish active viral replication from residual fragments could guide quarantine decisions and antiviral prescriptions, carving out clinical niches even as total test numbers fall. Suppliers that merge these technical advances with automated result reporting stand to capture enduring demand in a downsized yet technology-savvy marketplace.

By Specimen: Self-Collection Redefines Preferences

Nasopharyngeal swabs continue to hold 58.35% of 2025 revenue owing to long-standing clinical validation, but saliva collection is on track for a 2.08% CAGR to 2031 as consumers demand non-invasive options. Studies report 97.8% viral detection in saliva processed with bead-mill homogenizers, far exceeding the 78.9% achieved by nasopharyngeal swabs under standard lab conditions. Nasal swabs offer a compromise between comfort and accuracy, whereas oropharyngeal sampling remains protocol-driven for certain hospital settings. Finger-prick blood tests continue to serve antibody surveillance rather than acute diagnosis.

Self-collection changes logistics, shifting kit distribution from hospital supply chains to retail and e-commerce outlets. Digital apps guide users through collection, reducing indeterminate results and boosting consumer confidence. Public-health agencies gain timely data when apps push anonymized positives to epidemiological dashboards, aligning specimen innovation with surveillance objectives. Manufacturers are enhancing stabilizing buffers to extend sample viability during shipment, opening avenues for mail-in laboratory PCR services that circumvent cold-chain requirements.

By End User: Households Emerge as Growth Engine

Diagnostic laboratories accounted for 55.60% of 2025 revenue, leveraging automated sample handling and consolidated purchasing. Home care settings, however, are forecast to expand at a 2.18% CAGR through 2031 as consumers normalize routine self-testing before travel, family gatherings, or work. Hospitals retain acute-care testing yet increasingly rely on in-house panels that bundle COVID with other respiratory pathogens to justify operational costs. Public-health agencies now focus on sentinel surveillance rather than universal testing, purchasing kits in bulk for targeted community programs.

Expansion in the home segment reflects broader decentralization in healthcare delivery. PLoS ONE studies show self-collected swabs achieving 99% gonorrhea detection accuracy, reinforcing consumer trust in self-sampling across disease states. Kit makers capitalize by offering family-size packs and subscription models with telemedicine consults, lifting lifetime customer value beyond a single diagnostic sale. Platforms that combine Bluetooth-enabled readers with cloud dashboards enable physicians to monitor patient status, aligning kit sales with long-term digital-health revenue.

Geography Analysis

North America retained its leading 39.30% slice of the COVID testing kit market in 2025, buffered by USD 3 billion in federal funding for rapid-test procurement and manufacturing resilience. Yet commercial volumes shrank sharply after insurers curtailed blanket coverage, prompting manufacturers to streamline plants and prioritize higher-margin multiplex panels. Abbott Laboratories disclosed that lower COVID testing revenue and export tariffs will trim more than USD 1 billion from 2025 sales, illustrating the pressure on incumbents. FDA rulemaking on laboratory-developed-test oversight introduces new validation costs but promises a harmonized pathway for rapid approvals, benefitting firms that can meet stringent performance benchmarks.

Asia-Pacific recorded the fastest regional expansion at a 1.98% CAGR and is expected to keep that momentum through 2031 as urban hospitals prioritize combined respiratory panels to manage overlapping flu and COVID seasons. Governments are channeling recovery funds into molecular-diagnostic capacity, including subsidies for domestic reagent manufacturing. Public-private partnerships in India and China are building centralized data platforms that connect test readers to cloud analytics, transforming discrete kits into surveillance assets for health ministries. Nevertheless, uneven insurance coverage and variable reimbursement slow widespread adoption outside tier-one cities.

Europe continues to emphasize institutional purchasing, guided by the European Medicines Agency’s collaboration on global vaccine and diagnostic standards. Health systems are adding sustainability clauses to contracts, rewarding vendors that use recyclable plastics or supply take-back services. This environmental focus raises cost-of-goods for some suppliers but differentiates early movers in public tenders. In Latin America and Africa, donor-funded initiatives are improving laboratory networks, yet budget constraints keep average selling prices below global norms. Suppliers addressing these regions tailor stripped-down kits that retain core sensitivity while accommodating hot-chain shipping and minimal instrumentation.

Regulatory Landscape

COVID-19 testing kits operate under a mix of emergency and conventional regulatory pathways, with regulators tightening long-term requirements for performance, quality systems, and post-market oversight. In the United States, the FDA continues to maintain EUAs for in vitro diagnostics and publishes dedicated policies and FAQs for SARS-CoV-2 testing and OTC home diagnostics, while the Federal Register (September 23, 2025) finalized FDA guidance on enforcement policies for IVD tests during a Section 564 declared emergency. That clarification specifies the criteria for when unapproved tests may be offered during future declared emergencies.

In Europe, implementation of the In Vitro Diagnostic Regulation (IVDR) continues to reshape market access for SARS-CoV-2 tests through transitional timelines and reclassification impacts. Regulation (EU) 2024/1860, in force from July 9, 2024, extended transition periods for legacy IVDs to reduce supply disruption. Updated European Commission and MDCG-aligned classification guidance for SARS-CoV-2 tests also tightened expectations for higher-risk classifications, raising the bar for notified-body engagement, quality management system alignment (commonly ISO 13485), and conformity assessment planning, particularly for products migrating into higher classes with nearer-term submission deadlines.

Competitive Landscape

Market concentration is moderate as diversified giants counterbalance shrinking COVID revenue with broader diagnostics portfolios, while niche players seek mergers or pivot to adjacent respiratory tests. Abbott offset declining COVID kit sales with 7.5% organic growth across cardiovascular and diabetes franchises in Q2 2025, underscoring the benefit of portfolio breadth. Roche is re-routing PCR instrument capacity toward oncology and transplant virology assays, preserving utilization rates despite lower SARS-CoV-2 volumes. Thermo Fisher Scientific is bundling consumables with cloud analytics to lock customers into multi-year reagent agreements.

Specialized manufacturers face a fork: invest in next-generation technologies or exit. Becton Dickinson announced plans to divest USD 3.4 billion of in-vitro diagnostics assets by 2026 to sharpen focus on core medical-device lines. Cepheid leverages its installed GeneXpert base, now spanning more than 40,000 instruments, to offer over 20 FDA-cleared tests, enabling scale across infectious diseases beyond COVID. Companies developing CRISPR-based or AI-supported tests attract strategic investors eager to hedge against future pandemics, yet the path to volume production and regulatory clearance remains long.

Partnerships with telemedicine providers are redefining go-to-market models. iHealth’s direct-to-consumer 3-in-1 Flu A/B-COVID test launched exclusively on Costco’s online platform, demonstrating the clout of big-box retailers in diagnostics distribution. Meanwhile, emerging suppliers in Asia are negotiating technology-transfer agreements that swap intellectual-property licensing for local manufacturing access, securing price-competitive supply in their home markets. As the market contracts, operational excellence, multiplex capability, and digital integration outweigh simple scale in establishing competitive advantage.

COVID Testing Kit Industry Leaders

Abbott

F.Hoffmann-La Roche

Becton, Dickinson and Company

bioMérieux

BGI Genomics

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An opportunity is emerging around test formats and workflows aligned to routine respiratory-virus surveillance and care pathways, rather than mass one-pathogen screening. Government procurement and preparedness programs provide demand anchors for manufacturers that can supply compliant, scalable products. The US Department of Health and Human Services has invested more than USD 3 billion to sustain domestic rapid test production and has procured 500 million at-home tests for strategic reserves, helping suppliers maintain validated production lines and quality systems as commercial volumes normalize.

Regulatory normalization also creates room for companies transitioning portfolios from EUA to traditional authorization, with differentiation increasingly tied to multiplexing and connectivity. In June 2026, the FDA classified a simple point-of-care device to directly detect SARS-CoV-2 into class II with special controls (21 CFR 866.3982), reinforcing a clearer long-term pathway for point-of-care COVID tests and supporting investment in cleared product lines rather than emergency-only offerings. On the public-health side, multi-pathogen surveillance and sentinel approaches continue to expand, including wastewater-based monitoring. In 2026, Australia launched a three-year National Wastewater Surveillance Program across 47 sentinel sites, pointing to ongoing institutional spend on SARS-CoV-2 monitoring infrastructure that complements clinical testing and supports demand for high-throughput molecular platforms and integrated reporting.

Recent Industry Developments

- May 2026: Roche announced a definitive agreement to acquire PathAI for USD 750 million upfront, with additional milestones of up to USD 300 million. The deal strengthens its AI-enabled diagnostics and data interpretation capabilities, and while it is centered on digital pathology, it also supports broader diagnostic workflow digitization tied to connected respiratory testing strategies. The transaction reinforces the shift toward software-supported differentiation as standalone COVID test volumes decline.

- November 2025: Roche entered a strategic agreement with Sapphiros that provides Roche access to up to 1 billion lateral flow tests per year of manufacturing capacity and a pathway to future molecular point-of-care tests. The added capacity and platform access improve surge readiness and supply assurance for rapid tests, a key requirement for government stockpiling and outbreak response programs. It also signals continued investment in scalable rapid testing capabilities as the market transitions to more normalized demand.

- July 2025: Becton, Dickinson and Company received FDA 510(k) clearance for the BD Veritor System for SARS-CoV-2 antigen testing for point-of-care use. The clearance supports the industry-wide migration from EUA-based commercialization to standard FDA pathways, helping enable longer product lifecycles and more stable institutional purchasing. It also strengthens BD's position in decentralized testing settings where rapid turnaround and simplified workflows remain important.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from kits used to detect SARS-CoV-2 infection, including molecular and immunoassay formats, across clinical and point-of-care testing settings. Our sizing focuses on kit-level sales tied to routine diagnosis, screening, and surveillance demand across major regions.

Scope exclusions: We exclude COVID-19 vaccines, therapeutic drugs, general lab instruments (unless bundled in a kit price), and non-COVID respiratory panels that do not report a SARS-CoV-2 result.

Segmentation Overview

- By Product

- RT-PCR Assay Kits

- Immunoassay Test Strips / Cassettes

- CRISPR-based Molecular Kits

- Next-Gen Sequencing Panels

- By Specimen

- Nasopharyngeal Swab

- Nasal Swab

- Oropharyngeal Swab

- Saliva

- Blood / Finger-prick

- By End User

- Hospitals

- Diagnostic Laboratories

- Home Care Settings

- Public Health Agencies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping how many tests are being run and what kinds of tests they are, before converting that activity into kit demand and revenue. For this, we rely on public health reporting and surveillance releases such as WHO situation updates, CDC testing guidance and surveillance dashboards, and ECDC monitoring notes, since these sources help explain shifts from surge testing to more targeted testing.

We also pull supporting inputs from sources such as national health ministry procurement notices, customs and trade statistics for diagnostic reagents and swabs where available, and peer-reviewed studies that report positivity rates, testing frequency, and clinical practice changes over time. Company annual reports, investor decks, and reputable press are used to understand price movements, supply constraints, and channel mix, and then a paid subscription database is used selectively for company financials, news screening, and patent lookups that clarify product pipelines. These sources are not exhaustive, and many additional public references were reviewed to collect data, validate assumptions, and clarify unclear points.

Primary Interviews and Surveys

Primary inputs are gathered from laboratory managers, procurement teams, distributors, and diagnostic industry experts to confirm the realistic split between PCR and rapid formats, the pace of price erosion, and how frequently testing is ordered across settings. These discussions also help check how policy changes, travel testing, and outbreak cycles influence demand across APAC, EMEA, and the Americas, and they tighten assumptions that were weak or inconsistent in desk findings.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | APAC: 46% |

| Mid tier: 41% | Functional/Unit leaders: 34% | EMEA: 31% |

| Smaller Players: 22% | Managers: 51% | Americas: 23% |

Market-Sizing & Forecasting

The main model uses a top-down approach where reported testing volumes and testing mix are translated into kit consumption, and then valued using region-level average selling prices that reflect channel and product type. Because demand changed quickly after the peak pandemic years, we pay close attention to how test frequency per suspected case, positivity rates, and policy-driven screening requirements move the addressable testing pool.

Key inputs used in the model include the share of molecular versus antigen testing, average kits used per test (including controls where relevant), public procurement intensity, the shift between centralized labs and decentralized testing sites, and observed price declines as supply normalized. The totals are then corroborated through selective bottom-up approximations, such as rolling up sampled supplier revenues and checking implied kits shipped versus estimated tests performed, and gaps are handled by applying conservative ranges when a country has incomplete reporting.

For forecasting, scenario analysis is applied around expected outbreak waves, surveillance testing persistence, and guideline-driven testing in hospitals and long-term care. The final path is chosen after aligning the scenarios with expert views on likely testing cadence and the realistic price trajectory for common kit formats.

Data Validation & Update Cycle

Validation is done through multiple passes, starting with simple variance checks across regions and then drilling into outliers such as sudden revenue jumps that do not match testing intensity. We compare outputs against independent signals like public testing counts, procurement headlines, and supplier commentary to make sure the model is behaving in a believable way.

Before sign-off, assumptions that drive the most value impact, mainly pricing and testing volumes, are reviewed by another analyst, and clarifying calls are triggered when a mismatch stays unresolved. Reports are refreshed annually, with interim updates when major policy shifts, new variants, or large procurement events materially change demand, and a final pre-delivery review is done so clients receive the latest updated view.

Mordor Intelligence's Covid 19 Detection Kits Market Size Compared Against Other Published Estimates

Published market sizes for COVID-19 detection kits often differ because the market moved from emergency demand to steadier surveillance, and each publisher locks in different years, scopes, and pricing logic. Numbers can also spread when some studies include consumables beyond kits or treat point-of-care and lab testing boundaries differently.

Testing volume signals and the observed mix between RT-PCR and rapid formats are the checks that keep Mordor Intelligence's 2025 estimate tied to kit demand rather than wider lab spend, which is a common reason totals drift. Other estimates also vary based on whether they use a conservative decline path after 2021, whether they report factory-gate versus end-market values, and how they handle currency timing during periods of fast price drops.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.48 B (2025) | |

| Global Research Publisher A | USD 8.35 B (2025) | This figure expands the scope to include consumables and related services alongside kits, and it is presented as a factory-gate value, which can lift totals even when testing volumes are easing. |

| Industry Research Publisher B | USD 5.40 B (2024) | This estimate is anchored to an earlier base year with a different decline curve, and its average price assumptions can move faster downward when rapid tests dominate the mix in the modeled period. |

Overall, the spread is largely explained by what gets counted with the kit, the chosen base year, and how quickly prices are assumed to fall as demand normalizes. By tying revenue back to testing activity and practical price bands that can be cross-checked, the approach gives a traceable number that can be repeated and updated when the next demand shift happens.

Key Questions Answered in the Report

What is the projected value of the COVID testing kit market in 2031?

The market is forecast at USD 5.06 billion by 2031, reflecting a -6.32% CAGR from 2026.

Which product type is growing fastest?

CRISPR-based molecular kits lead growth with a projected 1.90% CAGR as laboratories adopt ultra-rapid diagnostics.

How quickly are home care settings expanding?

Home care channels are expected to register a 2.18% CAGR through 2031 as self-testing becomes routine.

Which region offers the highest growth potential?

Asia-Pacific is poised for the fastest regional expansion at a 1.98% CAGR driven by investments in diagnostic infrastructure.

Why are government stockpiles important to suppliers?

Long-term procurement contracts stabilize baseline demand and help manufacturers maintain production capacity for future outbreaks.

How is price pressure affecting manufacturers?

As emergency premiums disappear, suppliers are focusing on multiplex capability, digital add-ons, and operational efficiency to protect margins.

Page last updated on: