Interventional Oncology Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

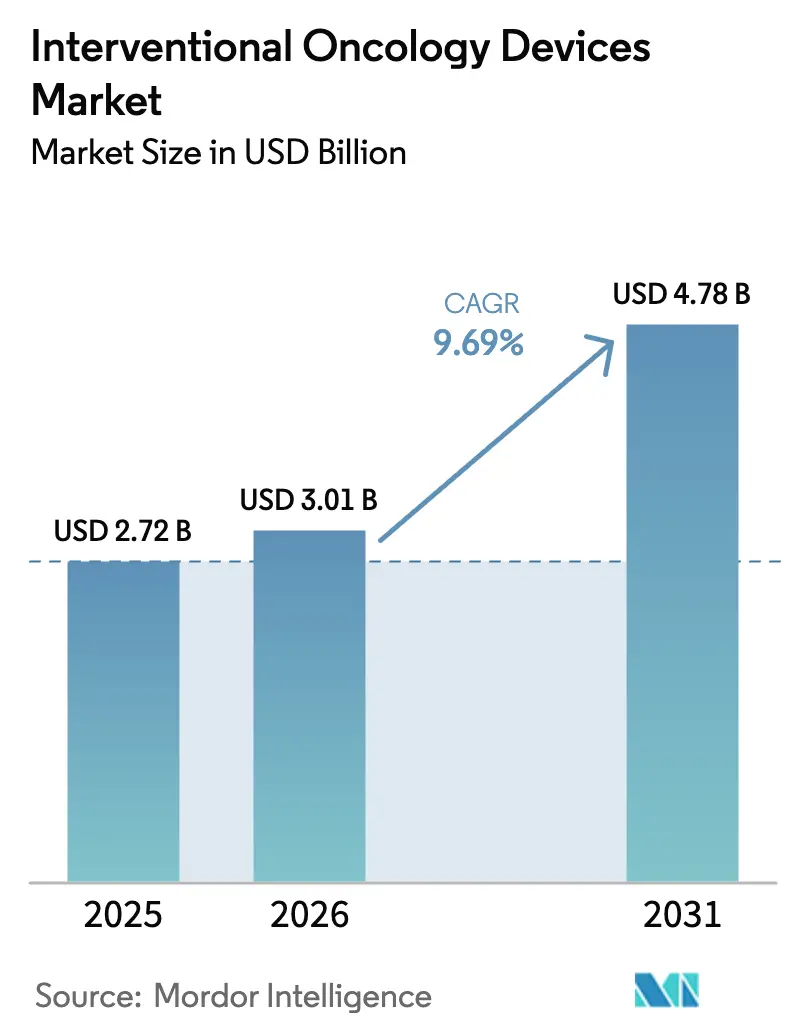

| Market Size (2026) | USD 3.01 Billion |

| Market Size (2031) | USD 4.78 Billion |

| Growth Rate (2026 - 2031) | 9.69% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Interventional Oncology Devices Market Analysis by Mordor Intelligence

The Interventional Oncology Devices Market size is expected to grow from USD 2.72 billion in 2025 to USD 3.01 billion in 2026 and is forecast to reach USD 4.78 billion by 2031 at 9.69% CAGR over 2026-2031.

This growth aligns with tight radiation-oncology capacity, periodic chemotherapy shortages, and the preference of patients and payers for outpatient, image-guided tumor control. Category I CPT reimbursement for irreversible electroporation in pancreatic cancer, effective January 2027, repositions ablation from salvage to front-line care and de-risks hospital capital spending. CMS further accelerates technology uptake through its Technology and Coverage Evaluation Pathway, which now ties provisional coverage to FDA clearance within 90 days rather than the historical 18-month lag. On the product front, long-acting drug-eluting beads that maintain localized chemotherapy for 30 days, rather than 14, are doubling tumor control rates in hepatocellular carcinoma and creating a premium segment within the interventional oncology devices market. At the procedural level, evidence supporting sequential chemoembolization plus microwave ablation is steering oncologists toward combination protocols that harness synergistic cytotoxicity while reducing hospital length of stay.

Key Report Takeaways

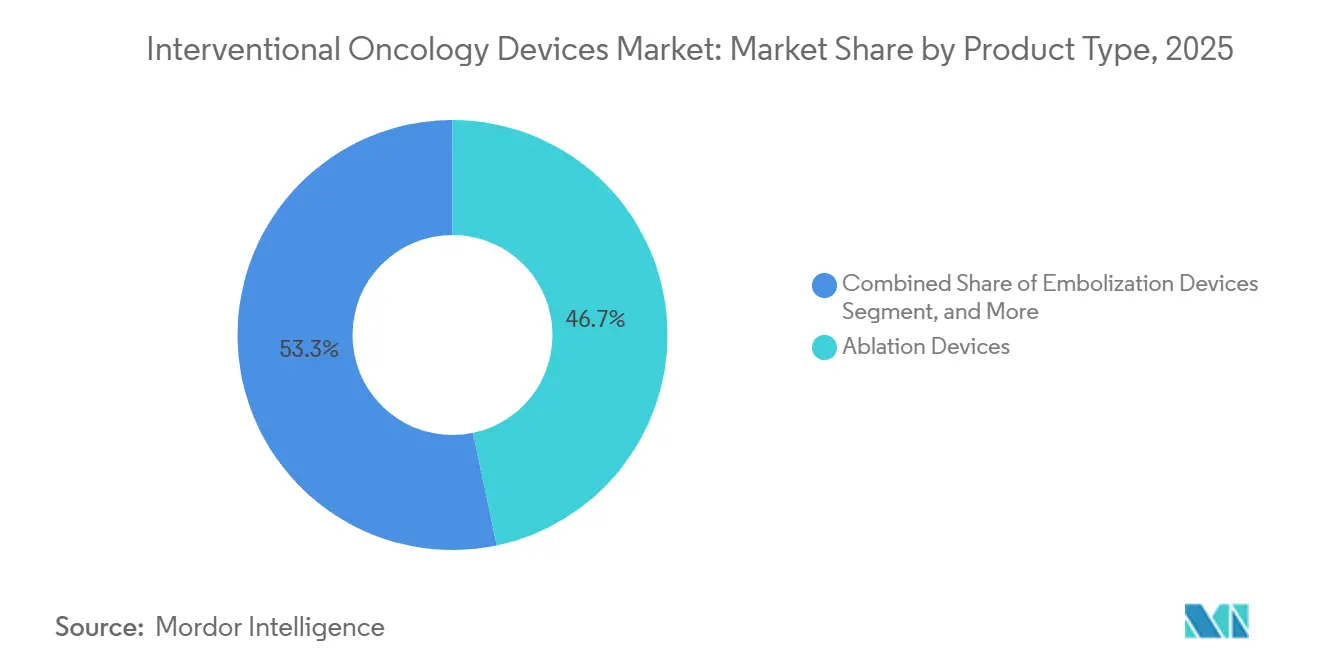

- By product type, ablation devices led the interventional oncology devices market, accounting for 46.71% of the market share in 2025. In contrast, embolization devices are expected to expand at a 12.29% CAGR through 2031.

- By procedure type, the ablation segment accounted for 49.13% of the interventional oncology devices market size in 2025, and combination therapies are projected to grow at a 13.09% CAGR over the same horizon.

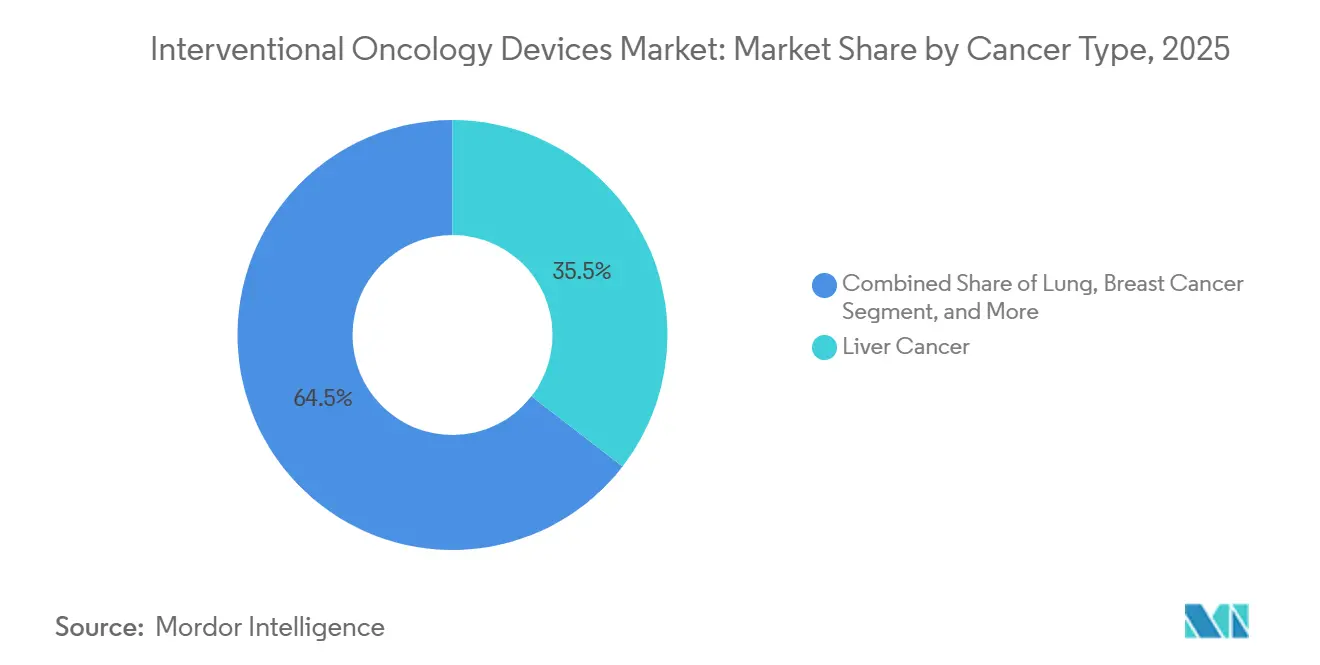

- By cancer type, liver cancer accounted for 35.48% of the revenue in 2025, while lung applications are forecasted to grow at 10.74% annually through 2031.

- By end user, hospitals accounted for 56.44% of revenue in 2025; however, ambulatory centers are projected to post a 15.50% CAGR from 2026 to 2031.

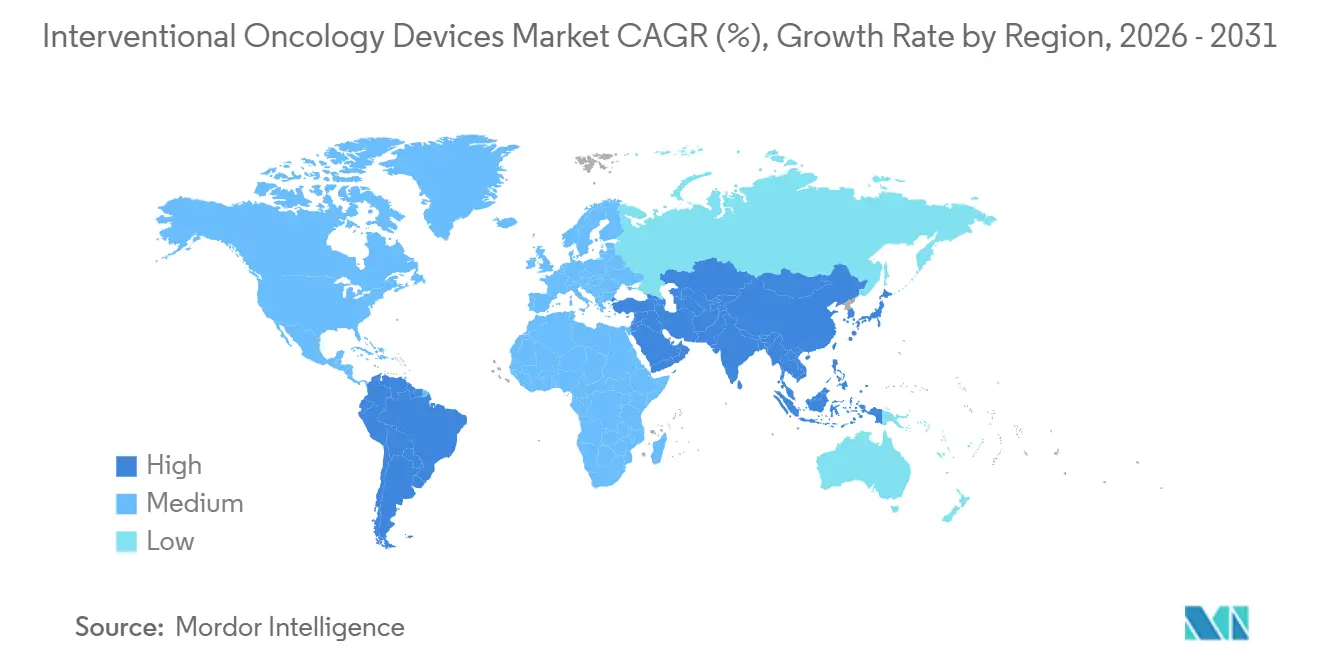

- By geography, North America accounted for 41.64% of revenue in 2025, and the Asia-Pacific region is poised for a 14.08% CAGR as China and Japan expand reimbursement and local approvals.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Interventional Oncology Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of cancer | +2.1% | Global; highest in Asia-Pacific and Sub-Saharan Africa | Long term (≥ 4 years) |

| Demand for minimally invasive therapies | +1.8% | North America and EU leading; expanding to Asia-Pacific | Medium term (2-4 years) |

| Advancements in image-guided ablation & embolization | +1.5% | Global; early adoption in developed markets | Medium term (2-4 years) |

| Favourable reimbursement & clinical guidelines | +1.2% | North America & EU primarily; selective Asia-Pacific | Short term (≤ 2 years) |

| AI-enabled navigation & robotic assistance | +1.0% | North America & EU core; spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Growing palliative-care demand | +0.9% | Global; emphasis on aging populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cancer Driving Interventional Demand

Global cancer incidence climbed to 20 million new cases in 2024, a 15% rise over 2020, with liver, lung, and kidney tumors prime targets for image-guided therapy, making up 4.2 million diagnoses.[1]World Health Organization, “GLOBOCAN 2024,” who.intThe International Atomic Energy Agency estimates a global deficit of 12,000 linear accelerators, prompting oncologists to turn to catheter-based embolization and percutaneous ablation as capacity substitutes. China’s 14th Five-Year Plan allocates USD 2.8 billion to establishing 500 cancer centers equipped with cone-beam CT suites by 2027, creating a pipeline that accounts for nearly one-fifth of the Asia-Pacific device shipments. Japan’s demographic profile, with 33% of citizens over 65 years, is linked to a 9% yearly increase in hepatocellular carcinoma, a cohort increasingly treated with radioembolization rather than resection. U.S. academic hospitals also report waitlists for external-beam therapy, prompting earlier referrals to interventional oncology clinics and increasing daily ablation throughput by 18%.

Advances in Image-Guided Navigation and Real-Time Fusion

AI navigation compresses pre-procedure planning from 45 minutes to 12 minutes, enabling radiologists to complete six cases daily instead of four.[2]Siemens Healthineers, “Investor Presentation Q4 2025,” siemens-healthineers.com Philips’ LumiGuide overlays real-time ultrasound on pre-acquired CT, cutting needle repositioning by 38% in lung biopsies. FDA-cleared LungVision combines bronchoscopic video with 3D maps, reducing peripheral-nodule ablation time by 22 minutes while lowering pneumothorax rates to 4.5%. Early clinical use of Apple Vision Pro at Massachusetts General Hospital projects holographic liver margins into the field of view, slicing positive margins by 19%. These innovations fortify the interventional oncology devices market as navigation evolves from accessory to standard-of-care capital equipment.

Growing Shift to Outpatient and Ambulatory Settings

CMS added 11 interventional oncology codes to the ASC list in its 2025 Outpatient Prospective Payment System, redirecting USD 340 million of yearly volume from hospital departments to ambulatory centers.[3]Centers for Medicare & Medicaid Services, “Technology and Coverage Evaluation Pathway,” cms.gov ASC facility fees run 58% below hospital outpatient rates, dovetailing with commercial payer contracts that reward site neutrality. Same-day discharge for uncomplicated liver ablation increased from 48% in 2023 to 67% in 2025, a swing that lifted throughput while trimming inpatient bed demand. AngioDynamics and SCA Health announced plans to place NanoKnife systems in 40 ASCs across Texas and Florida, targeting pancreas lesions previously eligible only for inpatient surgery. The FDA guidance finalized in 2024 affirmed that Class II ablation devices require no special facility certification beyond state licensure, thereby erasing an administrative hurdle for office-based procedures.

Expansion of Combination Therapy Protocols

A 2024 Lancet Oncology trial showed that chemoembolization followed by microwave ablation lifted 3-year survival in intermediate hepatocellular carcinoma from 58% to 71%. Boston Scientific’s TheraSphere, paired with ablation, achieved a 92% complete-response rate in tumors between 3 cm and 5 cm, compared with 67% for embolization alone. Medtronic’s Emprint Epoch integrates dual antennas with impedance feedback, extending ablation margins by 1.2 cm crucial when operators must avoid overlap injury. The FDA granted Breakthrough Device designation to three combination protocols in 2025, chopping trial timelines to 30 months and boosting reimbursement certainty. AASLD’s 2025 guidelines upgraded the protocol to Category 1A, prompting Medicare Advantage plans to issue rapid-coverage bulletins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Diagnostics in LMICs | -1.6% | Sub-Saharan Africa & South Asia | Long term (≥ 4 years) |

| Lack of Standardized Criteria / False Positives | -1.2% | Asia-Pacific & Latin America | Medium term (2-4 years) |

| Specialty Reagent Supply-Chain Vulnerabilities | -0.9% | North America & Europe | Short term (≤ 2 years) |

| Heightened Regulatory Scrutiny of Multiplex Assays | -0.8% | North America, Europe, expanding Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs Limiting Adoption in Resource-Constrained Settings

A turnkey interventional oncology suite costs USD 2.8 million, a figure exceeding the annual capital budgets of 78% of public hospitals in India and 65% in Brazil. Microwave generators alone sell for USD 180,000–USD 250,000, while per-case disposables add USD 8,500—four times the median out-of-pocket expenditure in Indonesia and Nigeria. Leasing penetration in Southeast Asia is only 12%, compared to 41% in Western Europe, which delays diffusion by four to six years. Import tariffs of 18%–35% and 90-day lead times further erode utilization, which falls below the 60% breakeven needed for payback.

Lack of Standardized Response Criteria and False-Positive Imaging

Inter-observer agreement on viable tumor after ablation ranges from 68% to 81%, producing a 14% false-positive rate in lung cases and driving unnecessary repeat procedures that cost USD 12,000 and extend recovery by three weeks. Contrast-enhanced ultrasound shows 19% discordance with MRI, while only 38% of U.S. practices adopted an SIR consensus template by December 2025. The evidence-generation cycle for payer coverage thus stretches another 18-24 months, tempering adoption in markets that rely on comparative-effectiveness dossiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Embolization Momentum Builds

Embolization devices are expected to grow at a 12.29% CAGR, outpacing the interventional oncology devices market, as 30-day drug-eluting beads double tumor control rates in hepatocellular carcinoma. Ablation devices still accounted for a 46.71% share of the interventional oncology devices market in 2025, driven by applications in the liver and lung. Yet, average selling prices have fallen 8% annually since 2023, pressured by low-cost Chinese entrants that price microwave generators 35% below those of incumbents. Irreversible electroporation is gaining traction in pancreatic indications after CPT reimbursement kicked in, resulting in a 77% increase in per-procedure revenue.

Navigation and imaging systems deliver 42% gross margins because proprietary AI algorithms reduce planning time and increase suite throughput, persuading hospitals that perform 200 or more cases annually to accept price tags of USD 350,000. Ancillary disposables mirror case volume but face double-digit price concessions under group-purchasing contracts negotiated by Premier Inc. Embolic microspheres command premium reimbursement, as irinotecan-loaded beads increase the objective response rate in colorectal metastases to 71% compared to 53% for bland embolization.

By Procedure Type: Synergy Fuels Combination Protocols

Combination therapies are on a 13.09% CAGR trajectory, fueled by survival benefits that earned Category 1A guideline status. Ablation held a 49.13% share of the 2025 interventional oncology devices market size, but growth is moderating to 8.2% as penetration plateaus in North America and Western Europe. Embolization procedures leverage Y-90 innovation to achieve a 10.1% CAGR; dosimetry advances now deliver 150 Gray to tumors while sparing parenchyma, thereby extending median survival in unresectable hepatocellular carcinoma from 10.7 to 16.4 months.

Chemoembolization reduces arterial flow by 68%, thereby mitigating the heat sink in vessels adjacent to tumors and enlarging the ablation margins by 1.2 cm. Medtronic’s impedance-regulated power control reduces charring and overlap injury, making the regimen feasible in previously risky locations. The FDA breakthrough designation shortens trial timelines and accelerates reimbursement, providing another tailwind.

By Cancer Type: Lung Growth Leads, Liver Remains Core

Lung indications will advance at a 10.74% CAGR to 2031, driven by microwave ablation achieving a 68% five-year survival rate in medically inoperable early-stage NSCLC, a parity result with stereotactic body radiation, but with half the treatment sessions. Liver cancer maintains its 35.48% revenue leadership, driven by approximately 900,000 annual cases. Kidney cryoablation continues at a steady rate of 9.1%, aided by 95% three-year cancer-specific survival and 92% renal function preservation in the elderly.

Prostate focal therapy posts an 11.3% CAGR; Profound’s MRI-guided ultrasound maintains erectile function in 78% of intermediate-risk patients. Bone metastasis ablation achieves a 60% pain reduction within 48 hours, expanding to orthopedic oncology clinics. Pancreatic irreversible electroporation expands at 16.8%, buoyed by reimbursement that lifts the number of eligible U.S. patients from 12,000 to 38,000 annually.

By End User: ASC Penetration Accelerates

Ambulatory centers are expected to log a 15.50% CAGR, outperforming hospitals by 5.8 points as CMS approves more outpatient codes. Hospitals still own 56.44% revenue because complex cases require overnight observation. However, same-day discharge after uncomplicated liver and lung ablation rose 19 percentage points in two years, eroding inpatient volume. ASC cost advantages, combined with payer incentives for site neutrality, are expected to increase penetration from 8% of procedures in 2024 to a projected 19% by 2029.

Specialty cancer centers grow at a rate of 10.2% on multidisciplinary care pathways. In comparison, academic medical centers and VA facilities together form an 8% niche that drives teaching and early adoption of investigational technologies.

Geography Analysis

North America generated 41.64% of 2025 revenue, supported by a 12% fee-schedule bump on microwave liver ablation to USD 3,847 per case and CMS’s 90-day provisional-coverage policy. U.S. penetration is high, 4,200 suites are already equipped with cone-beam CT, so growth slows to 7.8%. Canada's growth rate increased to 9.4% after Ontario and British Columbia added Y-90 radioembolization to public coverage, benefiting 12,000 patients. Mexico’s market expands at 11.2% as 18,000 U.S. patients crossed the border for 60% cheaper liver ablation and four-week shorter wait times in 2025.

Asia-Pacific is the growth engine with a 14.08% CAGR. China approved 47 devices for 2024–2025 and earmarked USD 2.8 billion for 500 cancer centers, accounting for 18% of regional shipments. Japan has added cryoablation of bone metastases to its fee schedule at JPY 420,000 (approximately USD 3,200) per procedure, catering to its large elderly population. India grows at the fastest rate of 16.1% under the Ayushman Bharat insurance plan, which now reimburses treatment for 500 million citizens.

Scandinavia offsets some softness by favoring minimally invasive care in value-based procurement tenders. The Middle East & Africa enjoy a 12.6% CAGR, aided by medical tourism hubs in Dubai and Riyadh that subsidize 40% of the costs for GCC nationals. South America advances at 10.9%, led by Brazil’s March 2025 reimbursement of microwave ablation under the SUS national health plan.

Competitive Landscape

The five leaders, Medtronic, Boston Scientific, AngioDynamics, Johnson & Johnson (Ethicon), and Siemens Healthineers, make the interventional oncology devices market moderately consolidated. Medtronic sells turnkey suites that bundle ablation generators, antennas, and O-arm imaging for USD 2.4 million, then secures 34% gross margins on service and disposables. Boston Scientific leverages its USD 420 million TheraSphere franchise to cross-sell cholangioscopy tools, lifting spend per radiology department by 18%. Siemens holds 47 AI-navigation patents, while Philips protects LumiGuide tracking with 12 patents that run into the mid-2030s, raising entry barriers.

White space remains in pancreatic ablation, where irreversible electroporation treats fewer than 8% of eligible patients, and in bone metastases, where pain-relief efficacy is strong but awareness is low. IceCure Medical’s ProSense cryo-system operates at -196 °C, 40 °C colder than argon units, yielding 96% complete ablation in breast tumors under 2 cm, and aims for a U.S. launch in 2027. Mirabilis Medical’s non-invasive MIRA-Q, cleared in November 2025, merges focused ultrasound with MRI thermometry to ablate fibroids and sarcomas without needles. A Q3 2025 resin shortage delayed Guerbet’s TheraSphere shipments by eight weeks, spotlighting raw-material risk in specialty microspheres.

Interventional Oncology Devices Industry Leaders

Boston Scientific Corporation

AngioDynamics

Sirtex Medical

Medtronic

Becton, Dickinson & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TriSalus Life Sciences launched the TriNav FLX infusion system to heighten targeted drug delivery.

- June 2025: FDA granted 510(k) clearance for the Visualase V2 MRI-guided laser platform treating brain lesions.

- June 2025: FDA approved UroGen Pharma’s mitomycin solution Zusduri for recurrent low-grade bladder cancer

- May 2025: Portal Access raised USD 7 million Series A to advance vascular-access devices for oncology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the interventional oncology devices market as the value generated by image-guided ablation probes, embolic particles, and delivery catheters, navigation or imaging consoles that enable tumor-directed therapy, and the single-use disposables deployed during such minimally invasive cancer procedures performed inside angio suites or hybrid ORs. According to Mordor Intelligence, revenues are booked at manufacturer selling prices and captured worldwide before distributor mark-ups.

Scope Exclusions: Conventional external-beam radiotherapy units, systemic oncology drugs, and open surgical resection tools fall outside this analysis.

Segmentation Overview

- By Product Type

- Ablation Devices

- Thermal Ablation

- Non-thermal Ablation

- Embolization Devices

- Embolic Agents

- Delivery Accessories

- Navigation & Imaging Systems

- Ancillary Disposables

- Ablation Devices

- By Procedure Type

- Ablation

- Embolization

- Combination Therapies

- By Cancer Type

- Liver

- Lung

- Breast

- Kidney

- Prostate

- Bone Metastases

- Pancreatic

- Other Cancers

- By End User

- Hospitals

- Cancer Specialty Centers

- Ambulatory Surgical Settings

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed interventional radiologists, oncology surgeons, cath-lab managers, and regional group purchasing officers across North America, Europe, Asia-Pacific, and select Middle-East hubs. These conversations validated disposable usage rates, typical capital budgeting cycles, and emerging indications, allowing us to plug information gaps identified during desk work.

Desk Research

We collated baseline data from respected public sources such as the WHO-IARC GLOBOCAN registry, SEER program tables, OECD Health statistics, United States FDA 510(k) device database, and annual procedure counts published by the Cardiovascular and Interventional Radiological Society of Europe. Company filings, hospital procurement tenders, and reputed trade press articles enriched pricing and channel insights. Subscription resources, including D&B Hoovers for company financials, Dow Jones Factiva for global news flow, and Questel for ablation-related patents, helped trace competitive footprints. This list is illustrative, with further databases referenced whenever clarification was required.

Market-Sizing & Forecasting

The top-down model begins with country-level new cancer incidence, liver and lung prevalence ratios, and procedure adoption curves, which are then layered with average selling prices harvested from tender logs. Supplier roll-ups and channel checks provide a bottom-up reasonableness screen before final totals are locked. Key variables tracked include: 1) annual microwave and radiofrequency ablation installs, 2) unit prices of drug-eluting beads, 3) interventional oncology fellowship output, 4) regulatory approvals trend, and 5) imaging suite capacity utilization. We forecast using a multivariate regression that links these drivers with macro indicators such as healthcare spending and oncology bed additions, producing base, optimistic, and caution scenarios reviewed with our primary experts.

Data Validation & Update Cycle

Outputs pass variance checks against historical procedure growth, abnormal ASP swings, and independent shipment statistics. Senior analysts re-review anomalies before sign-off. Reports refresh each year, with mid-cycle updates triggered by material recalls, reimbursement shifts, or blockbuster approvals, ensuring clients always receive the latest vetted view.

Why Mordor's Interventional Oncology Devices Baseline Remain Dependable

Published estimates often diverge; definitions differ, assumptions vary, and refresh cadences range from annual to biennial.

Key gap drivers include product scope, the share of navigation consoles counted as oncology spend, differing ASP progression methods, and whether recurrent disposable revenue is annualized or treated as one-time. Mordor's model captures the full therapy stack, adopts balanced price-volume curves vetted by clinicians, and updates every twelve months, which many peers do not.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.94 B (2025) | Mordor Intelligence | |

| USD 2.70 B (2024) | Global Consultancy A | Excludes navigation systems and applies straight-line growth without procedure validation |

| USD 2.39 B (2024) | Trade Journal B | Relies solely on prevalence data and ignores regional ASP dispersion and tender lags |

In sum, our disciplined scope selection, variable tracking, and timely refresh make Mordor Intelligence's baseline a balanced, transparent reference that decision-makers can trace back to clear real-world signals.

Key Questions Answered in the Report

How fast is the interventional oncology devices market expected to grow through 2031?

The market is projected to expand at a 9.69% CAGR, climbing from USD 3.01 billion in 2026 to USD 4.78 billion by 2031.

Which product category will grow the quickest?

Embolization devices are forecast for a 12.29% CAGR as 30-day drug-eluting beads drive demand for durable local control.

Why are ambulatory surgical centers important for adoption?

CMS added 11 procedure codes to the ASC list and facility fees run 58% lower than hospital outpatient, helping ASCs capture faster 15.50% CAGR growth.

Which cancer indication offers the strongest upside?

Lung applications are poised for a 10.74% CAGR, driven by evidence that microwave ablation matches SBRT survival rates in early-stage NSCLC, requiring fewer treatment sessions.

What is the main regulatory catalyst in the United States?

The CMS Technology and Coverage Evaluation Pathway now delivers provisional coverage 90 days after FDA clearance, shrinking the reimbursement gap for new devices.

Page last updated on: