Hysteroscope Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

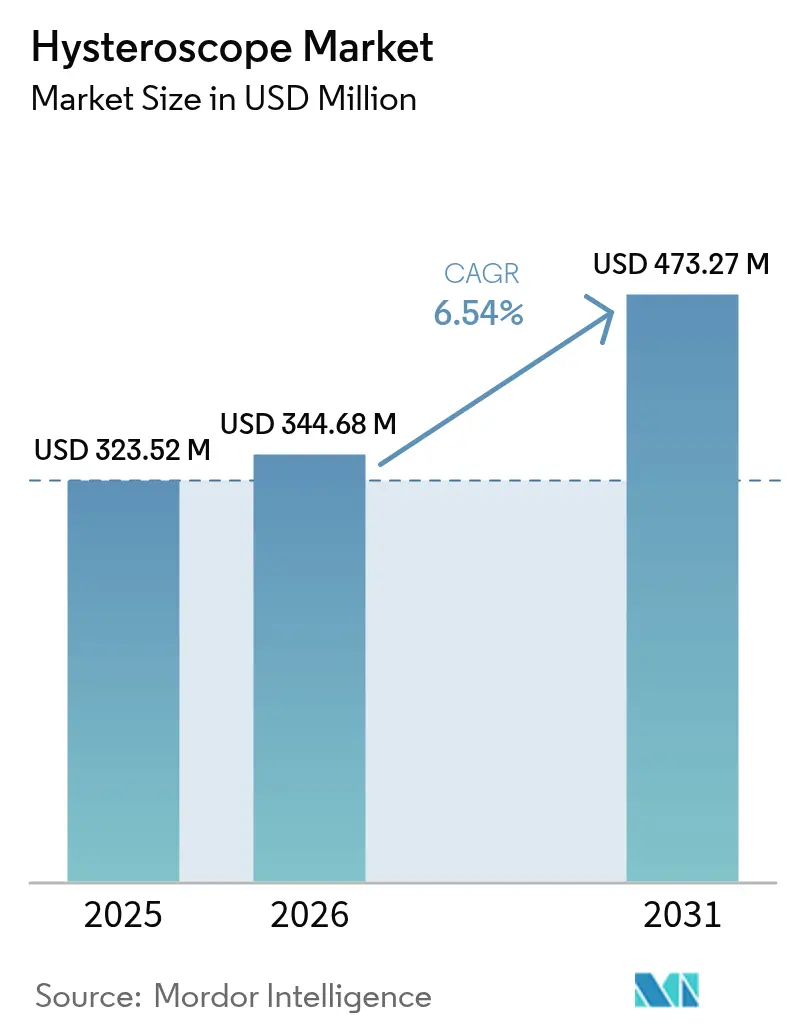

| Market Size (2026) | USD 344.68 Million |

| Market Size (2031) | USD 473.27 Million |

| Growth Rate (2026 - 2031) | 6.54% CAGR |

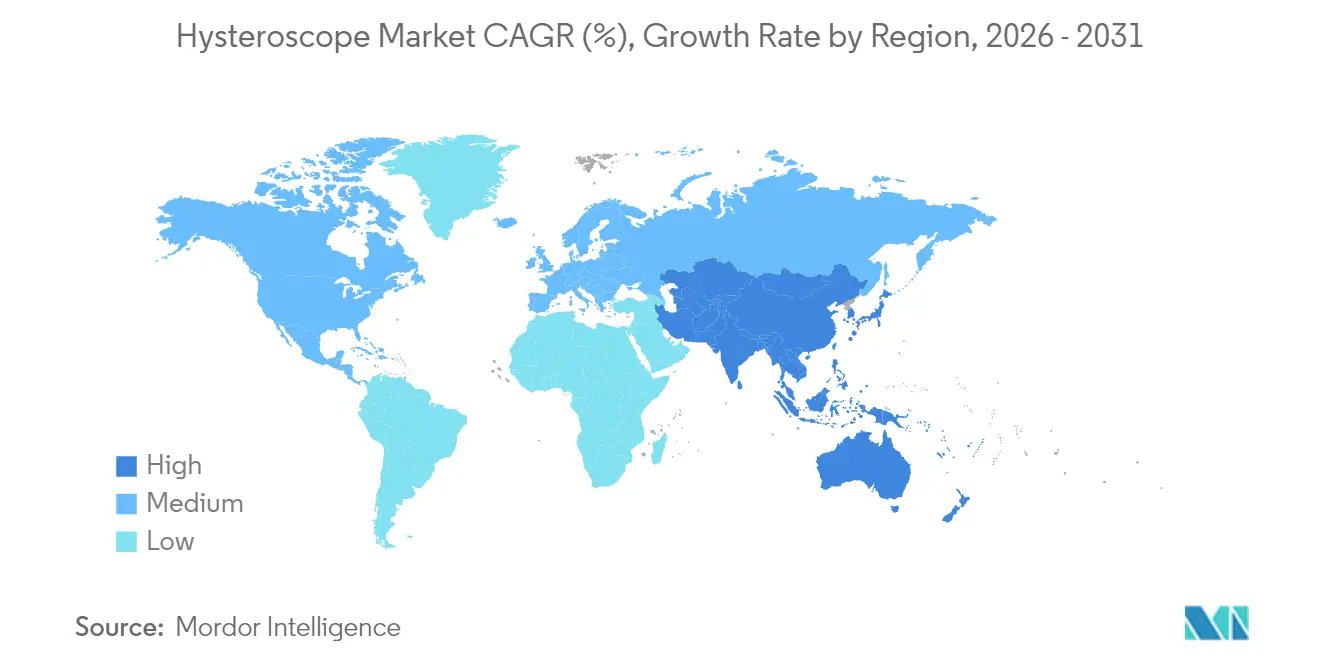

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hysteroscope Market Analysis by Mordor Intelligence

The hysteroscope market size was valued at USD 323.52 million in 2025 and estimated to grow from USD 344.68 million in 2026 to reach USD 473.27 million by 2031, at a CAGR of 6.54% during the forecast period (2026-2031). Growth is propelled by broader uptake of minimally invasive gynecologic surgery, widening payer support for office-based care, and rapid product innovation that blends advanced optics with rigorous infection-control protocols. Single-use device platforms, cloud-connected imaging, and artificial-intelligence (AI) decision support are reshaping workflows and lowering total procedural costs, giving early adopters measurable clinical and financial advantages. Hospitals still anchor procurement volumes, yet independent gynecology clinics now capture a rising share of elective procedures as reimbursement rules reward outpatient settings. Rigid hysteroscopes remain the platform of choice inside complex surgical theaters, but disposable offerings are driving incremental procedure growth, especially where reprocessing capacity is limited. Competitive intensity is increasing as leading manufacturers pursue acquisitions to secure differentiated technologies and regional footholds.

Key Report Takeaways

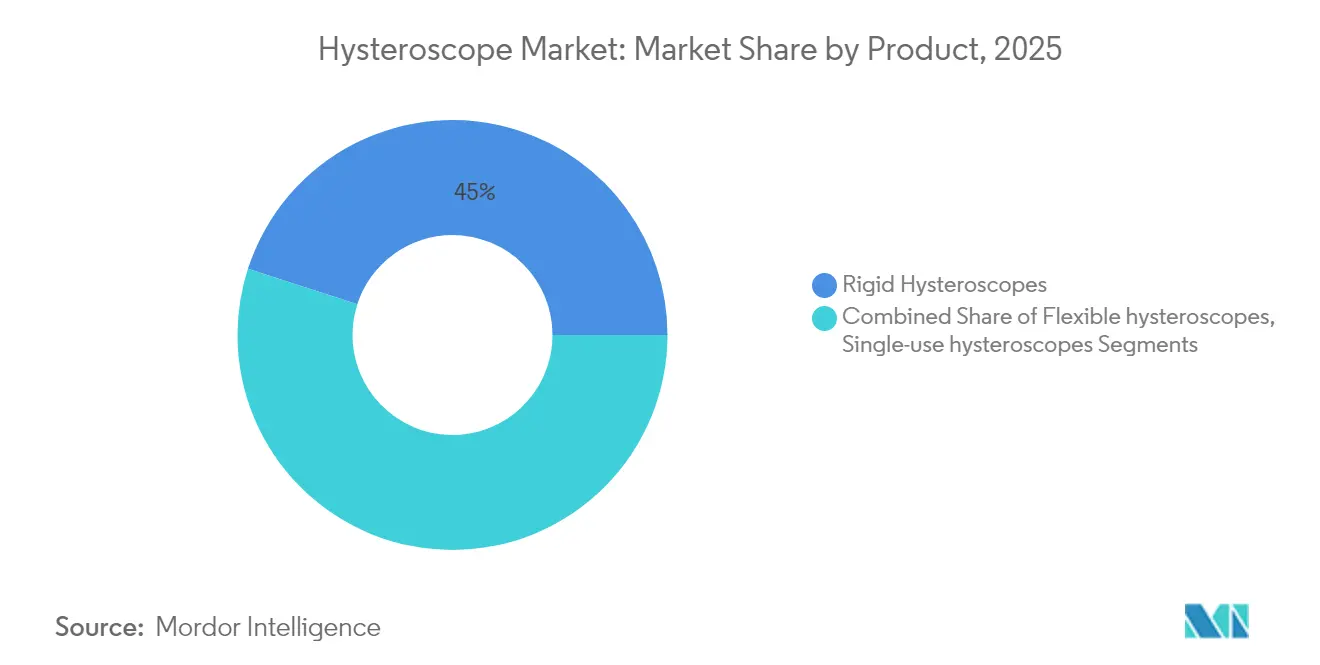

- By product type rigid systems led with 45.02% of hysteroscope market share in 2025, whereas single-use scopes are projected to rise at 14.40% CAGR to 2031.

- By modality diagnostic procedures accounted for 62.11% revenue in 2025; operative hysteroscopy is slated to grow at a 9.60% CAGR through 2031.

- By component scope shafts and optics held 51.40% share of the hysteroscope market size in 2025, while accessories and consumables expand at 10.05% CAGR.

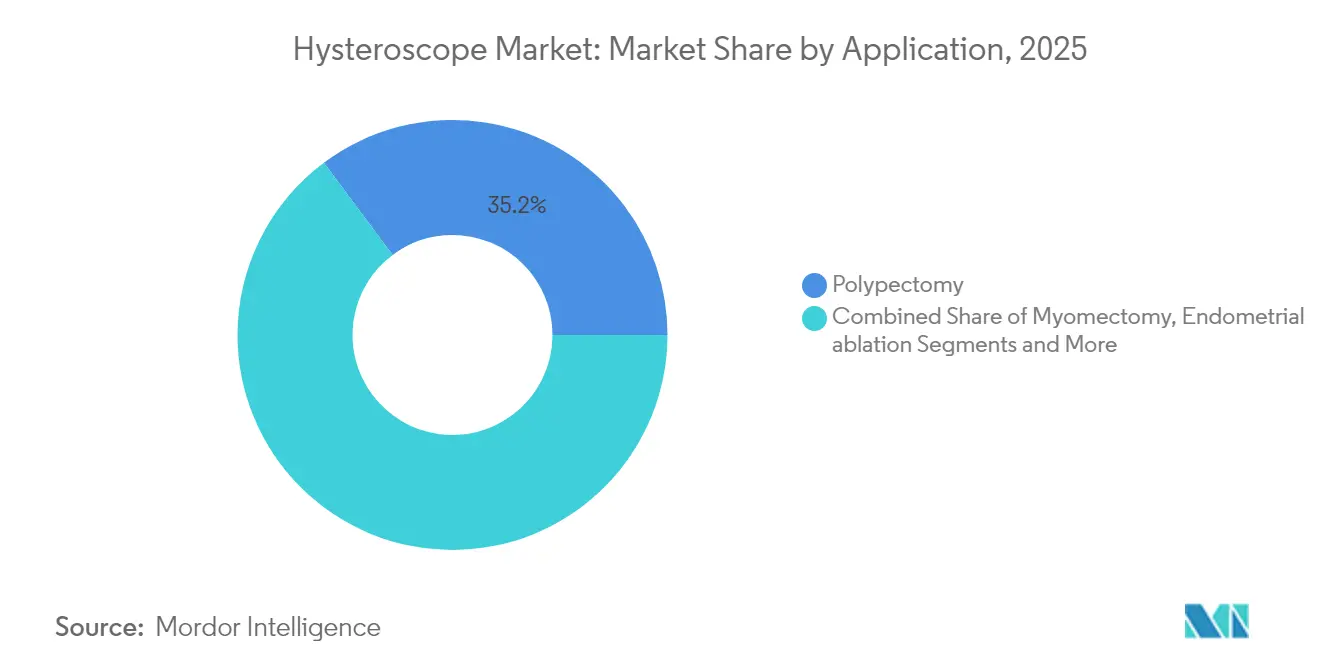

- By application polypectomy captured 35.21% revenue in 2025; endometrial ablation is the fastest-growing application with a 9.92% CAGR to 2031.

- By end user hospitals retained 59.65% of 2025 revenues, but office-based clinics are advancing at 12.19% CAGR through 2031.

- By geography, North America commanded 37.20% of 2025 sales; Asia-Pacific is the highest-growth geography, exhibiting a 9.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hysteroscope Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased incidence of uterine diseases & abnormalities | +1.2% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Growing demand for minimally invasive gynecologic surgery | +1.8% | North America, Europe | Medium term (2-4 years) |

| Technological advances in optics & miniaturization | +1.1% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Rapid adoption of single-use hysteroscopes for infection control | +1.5% | Global, post-COVID acceleration | Short term (≤ 2 years) |

| Shift toward office-based hysteroscopy | +0.8% | North America, Europe | Medium term (2-4 years) |

| Integration of AI-guided imaging & cloud analytics | +0.7% | Initially developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Minimally Invasive Gynecologic Surgery

Clinicians now favor uterine-preserving, incision-free options that shorten recovery and limit complications. Prospective data show vaginal natural orifice transluminal endoscopic hysterectomy can cut median return-to-work from 3 months to 2 months compared with laparoscopy, a finding that resonates with payers evaluating value-based reimbursement[1]Xinyi Shi, “Comparison of Rapid Recovery Outcomes Between vNOTES and Laparoscopic Hysterectomy,” bmcsurg.biomedcentral.com. The Mayo Clinic cites hysteroscopic approaches as a first-line solution for intrauterine pathologies because they avoid abdominal incisions and reduce hospital stay. Emerging techniques, including high-intensity focused ultrasound and radiofrequency ablation, are opening new therapy segments for adenomyosis and fibroids. Robotic articulation, AI-enabled targeting, and enhanced visualization further improve precision, positioning operative hysteroscopy to capture share from traditional open or laparoscopic alternatives.

Rapid Adoption of Single-Use Hysteroscopes for Infection Control

Heightened scrutiny of endoscope reprocessing failures is prompting facilities to reevaluate the risk-benefit equation of reusable devices. FDA safety communications underscore contamination hazards, especially in low-volume centers where reprocessing validation is cost-prohibitive. ACOG notes the absence of definitive cost-effectiveness research but warns that surface defects and improper decontamination raise failure rates[2]American College of Obstetricians and Gynecologists, “Reprocessed Single-Use Devices,” journals.lww.com. Manufacturers such as Minerva Surgical have responded with fully disposable platforms that remove the reprocessing step while offering optics comparable to reusable scopes. If future Medicare payment adjustments cover higher per-procedure consumable costs, adoption curves could steepen quickly across ambulatory sites.

Technological Advances in Optics & Miniaturization

The transition from HD to native 4K and beyond provides four-fold pixel density improvement, enabling clinicians to discern microvascular and textural details that influence intraoperative decisions. Olympus’s Extended Depth-of-Field optics, coupled with Narrow Band Imaging, heighten lesion detection and reduce diagnostic uncertainty. Ultra-slim 3.1 mm hysterofiberscopes eliminate cervical dilation in many office workflows, reducing procedure time and enhancing patient comfort. These advancements extend the procedural reach of community clinics and resource-constrained hospitals, democratizing access to precision hysteroscopy.

Integration of AI-Guided Imaging & Cloud Analytics

AI engines trained on endoscopic image libraries now deliver real-time polyp detection and tissue characterization, reducing operator dependence while standardizing interpretation. Cloud-hosted platforms facilitate remote consultation and aggregate performance data to refine algorithms continually. Hologic’s collaboration with Google Cloud exemplifies the convergence of diagnostics and machine learning in women’s health. Over time, AI triage tools could shorten learning curves for new hysteroscopists, a benefit especially relevant in regions facing specialist shortages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection risk from reusable hysteroscopes | -0.9% | Developed markets | Short term (≤ 2 years) |

| Shortage of trained hysteroscopists in emerging markets | -1.2% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Sustainability concerns over disposable devices | -0.6% | Europe, North America | Medium term (2-4 years) |

| Regulatory scrutiny of morcellation & fluid-management events | -0.8% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infection Risk from Reusable Hysteroscopes

Complex device geometries challenge sterile-processing teams, and misalignment between manufacturer instructions and facility resources drives reprocessing errors. ANSI/AAMI ST108 water-quality guidelines raise infrastructure costs, while litigation fear over contamination events pushes administrators toward disposable options. NYU Langone Health reduced defects by deploying dedicated cross-functional teams, yet the resource burden is substantial, underscoring why smaller sites embrace single-use scopes despite higher unit costs.

Sustainability Concerns Around Disposable Devices

Healthcare generates nearly 6 million tons of waste annually, with plastics forming 25%—yet less than 1% is recycled[3]AAMI News, “Addressing the Healthcare Sector’s Medical Waste Problem,” array.aami.org. European directives will soon compel manufacturers to document full lifecycle impact, placing pressure on resin choices and packaging. Life-cycle assessments reveal that manufacturing and disposal footprints can exceed those of reusable systems if procedure volume is high. Facilities now form “green teams” to weigh environmental metrics against infection-prevention priorities, but standardized benchmarks remain elusive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Single-Use Innovation Reshapes Traditional Preferences

Rigid scopes held 45.02% of 2025 revenue, reflecting proven optical clarity and maneuverability during complex intrauterine surgery. The hysteroscope market size for rigid platforms reached USD 145.66 million in 2025, supported by high capital utilization rates inside tertiary centers. In contrast, single-use scopes recorded the highest growth trajectory at 14.40% CAGR, gaining rapid traction where reprocessing capacity is limited and liability insurance premiums are rising. Greater comfort for patients in office settings, coupled with reduced turnaround time between cases, makes disposables attractive for throughput-oriented clinics.

Hybrid solutions that combine a reusable imaging unit with disposable sheaths blur traditional product boundaries and may accelerate adoption by balancing cost and infection-control goals. Meditrina’s second-generation platform, cleared by FDA in May 2024, highlights innovation that marries lightweight ergonomics with 4K visualization, narrowing the perceived performance gap between rigid and flexible formats. Flexible scopes remain niche, favored in anatomically difficult cases or where patient tolerance is paramount, yet higher acquisition costs and narrower procedure indications keep share growth moderate.

By Modality: Operative Procedures Drive Future Growth

Diagnostic hysteroscopy represented 62.11% of total 2025 procedures, reflecting its universal role in first-line uterine assessment. Clinicians favor diagnostic scopes for their smaller diameter and simplified workflow, making them ideal for outpatient evaluation without anesthesia. Operative procedures, expanding at 9.60% CAGR, benefit from tissue-removal systems and energy devices that allow polypectomy, myomectomy, and ablation during a single encounter. Evidence from a 2025 cohort study shows cold-knife hysteroscopic separation plus hormonal therapy achieved a 94.07% success rate in severe intrauterine adhesion, outperforming historical standards.

Hospitals and advanced ambulatory centers are investing in integrated imaging stacks and AI-enabled guidance that streamline complex operative workflows. These upgrades increase capital budgets but also elevate reimbursement potential because combined diagnostic-therapeutic sessions reduce overall episode-of-care costs. Growing surgeon proficiency, aided by simulation training and telementoring, is expected to sustain double-digit procedure expansion in operative subsegments across both developed and emerging geographies.

By Component: Consumables Model Drives Revenue Growth

Scope shafts and optical assemblies contributed 51.40% of 2025 revenues, underscoring their pivotal role in image quality and durability. Multi-coated lenses, robust light guides, and anti-fog channels require precision manufacturing, justifying premium pricing. However, accessories and consumables—including disposable distension media tubing, retrieval forceps, and single-use camera-caps—are forecast to see 10.05% CAGR through 2031, reflecting the shift toward recurring revenue. Each procedure may consume multiple accessory SKUs, creating an attractive annuity model for suppliers.

LED light sources and 4K camera heads are on faster replacement cycles than base scopes, fostering a secondary upgrade market. Modular platform design allows clinics to incrementally adopt new imaging blocks or AI-software updates without replacing the entire tower, fitting constrained capital budgets. The hysteroscope market size for consumables is projected to surpass USD 279.1 million by 2031 as disposable scope adoption and higher procedural volumes converge.

By Application: Endometrial Ablation Leads Therapeutic Innovation

Polypectomy remained the leading indication, capturing 35.21% of 2025 procedures, thanks to clear diagnostic algorithms and straightforward reimbursement. Nevertheless, endometrial ablation shows the strongest momentum at 9.92% CAGR, as patients and physicians seek uterus-sparing treatments for abnormal uterine bleeding. Next-generation radiofrequency wands and balloon-based thermal systems reduce operative time and anesthesia requirements, broadening eligibility to lower-risk outpatient environments.

Myomectomy is increasingly preferred by patients aiming to preserve fertility, aided by AI-guided imaging that delineates fibroid margins and vascularity. Adhesiolysis and septum resection, while smaller segments, benefit from heightened awareness of uterine cavity abnormalities on fertility outcomes. Collectively, therapeutic applications are expected to outpace purely diagnostic use as technology closes the complexity gap and training programs prioritize operative competence.

By End User: Office-Based Care Transformation

Hospitals accounted for 59.65% of 2025 revenues, leveraging operating-room infrastructure, anesthetic support, and reimbursement familiarity. The hysteroscope market size associated with hospital settings approached USD 193 million in 2025. Yet, office-based gynecology clinics lead growth at 12.19% CAGR, catalyzed by payer incentives that reward lower facility fees and shorter patient stays. Updated clinical guidelines confirm that many diagnostic and limited operative procedures deliver equivalent outcomes in office environments, reducing the need for general anesthesia.

Ambulatory surgical centers offer a middle ground, combining dedicated procedure rooms with anesthesia capabilities at lower overhead than hospitals. Fertility clinics, meanwhile, integrate hysteroscopic evaluation into comprehensive reproductive workflows, reinforcing diagnostic throughput. As capital equipment becomes lighter and more portable, and disposable optics reduce cleaning infrastructure, adoption across decentralized settings will accelerate, reinforcing procedure migration away from inpatient environments.

Geography Analysis

North America led with 37.20% share in 2025, buoyed by advanced payer models, extensive sub-specialty training, and rapid uptake of AI-enhanced visualization systems. The United States maintains dominant procedure volume, while Canada adopts similar technologies under its publicly funded healthcare scheme. Mexico’s growing private hospital sector and medical tourism initiatives attract regional patients seeking minimally invasive care.

Asia-Pacific is the fastest-growing territory at a projected 9.63% CAGR to 2031. Rising disposable income, expanded insurance coverage, and high gynecological disease burden underpin demand. A systematic 2025 analysis forecasts persistent growth in cervical and uterine cancers, particularly across South Asia, intensifying screening and operative requirements. China and Japan invest heavily in domestic device production, shortening supply chains and supporting local installations, whereas India’s new marketing code underscores regulatory maturation that should accelerate market entry for global suppliers.

Europe maintains stable growth amid stringent safety and environmental regulations that influence global manufacturing standards. The region’s push toward life-cycle transparency encourages design innovation around recyclable components. Meanwhile, Middle East & Africa and Latin America see incremental adoption led by private hospitals and fertility centers in urban hubs, though workforce shortages and uneven reimbursement slow broader penetration. Targeted training collaborations and cloud-enabled remote mentoring are expected to narrow the capability gap over the forecast horizon.

Competitive Landscape

The hysteroscope market remains moderately fragmented, though consolidation is accelerating. Hologic’s USD 350 million acquisition of Gynesonics in January 2025 strengthens its minimally invasive fibroid treatment portfolio, while Karl Storz’s purchase of Asensus Surgical extends its robotic-enabled platform. CooperSurgical added obp Surgical for USD 100 million, broadening single-use visualization options.

Competitive differentiation revolves around optical resolution, AI integration, and disposable scope economics. Leading vendors invest in vertically integrated ecosystems that control scopes, imaging hardware, software, and consumables, locking customers into upgrade paths and service contracts. Smaller innovators focus on ultra-slim scopes, ergonomic handpieces, or region-specific price points to penetrate cost-sensitive markets.

Training support, cloud analytics, and post-market surveillance capability are emerging as key tender criteria, especially for public hospitals in emerging economies. Partnerships with academic centers to validate AI algorithms and with payers to model cost offsets from infection avoidance are becoming standard. Over the next five years, platform interoperability and sustainability credentials will likely weigh more heavily in procurement decisions, potentially redefining competitive hierarchies.

Hysteroscope Industry Leaders

Hologic Inc.

CooperSurgical Inc.

Olympus Corporation

Medtronic plc

Stryker Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Caldera Medical announced the acquisition of UVision 360, developer of the LUMINELLE hysteroscopy and cystoscopy systems.

- May 2024: Meditrina secured FDA clearance for its Gen 2 hysteroscopy system, introducing advanced imaging capabilities and enhanced workflow features.

Global Hysteroscope Market Report Scope

As per the scope of the report, a hysteroscope is a device that carries optical and light channels or fibers helping to diagnose and treat abnormalities in or around the uterine cavity. The hysteroscope market is segmented by product (rigid hysteroscopes and flexible hysteroscopes), application (polypectomy, myomectomy, endometrial ablation, and others), end user (hospitals, ambulatory surgical services, and others) and geography (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Rigid Hysteroscopes |

| Flexible Hysteroscopes |

| Single-use / Disposable Hysteroscopes |

| Diagnostic |

| Operative |

| Scope Shaft & Optics |

| Camera Head / Imaging System |

| Light Source |

| Distension Media & Pumps |

| Accessories & Consumables |

| Polypectomy |

| Myomectomy |

| Endometrial Ablation |

| Infertility Assessment & Treatment |

| Adhesiolysis / Septum Resection |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Office-based Gynecology Clinics |

| Fertility Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Rigid Hysteroscopes | |

| Flexible Hysteroscopes | ||

| Single-use / Disposable Hysteroscopes | ||

| By Modality | Diagnostic | |

| Operative | ||

| By Component | Scope Shaft & Optics | |

| Camera Head / Imaging System | ||

| Light Source | ||

| Distension Media & Pumps | ||

| Accessories & Consumables | ||

| By Application | Polypectomy | |

| Myomectomy | ||

| Endometrial Ablation | ||

| Infertility Assessment & Treatment | ||

| Adhesiolysis / Septum Resection | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Office-based Gynecology Clinics | ||

| Fertility Centers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hysteroscope market?

The hysteroscope market is valued at USD 344.68 million in 2026 and is forecast to reach USD 473.27 million by 2031.

Which product category is expanding the fastest?

Single-use disposable hysteroscopes are projected to grow at a 14.40% CAGR through 2031, driven by infection-control priorities and lower reprocessing costs.

Why are office-based clinics gaining share?

Payer incentives for outpatient care, lighter capital requirements, and improved patient convenience are propelling 12.19% CAGR growth for office-based clinics between 2026 and 2031.

How is AI influencing hysteroscopic procedures?

AI-guided imaging delivers real-time lesion detection, reduces operator variability, and enables remote consultation, enhancing diagnostic accuracy across varying skill levels.

What restrains broader adoption of disposable scopes?

Environmental concerns about medical plastic waste and evolving regulatory directives in Europe and North America temper the otherwise rapid uptake of single-use devices.

Page last updated on: