Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

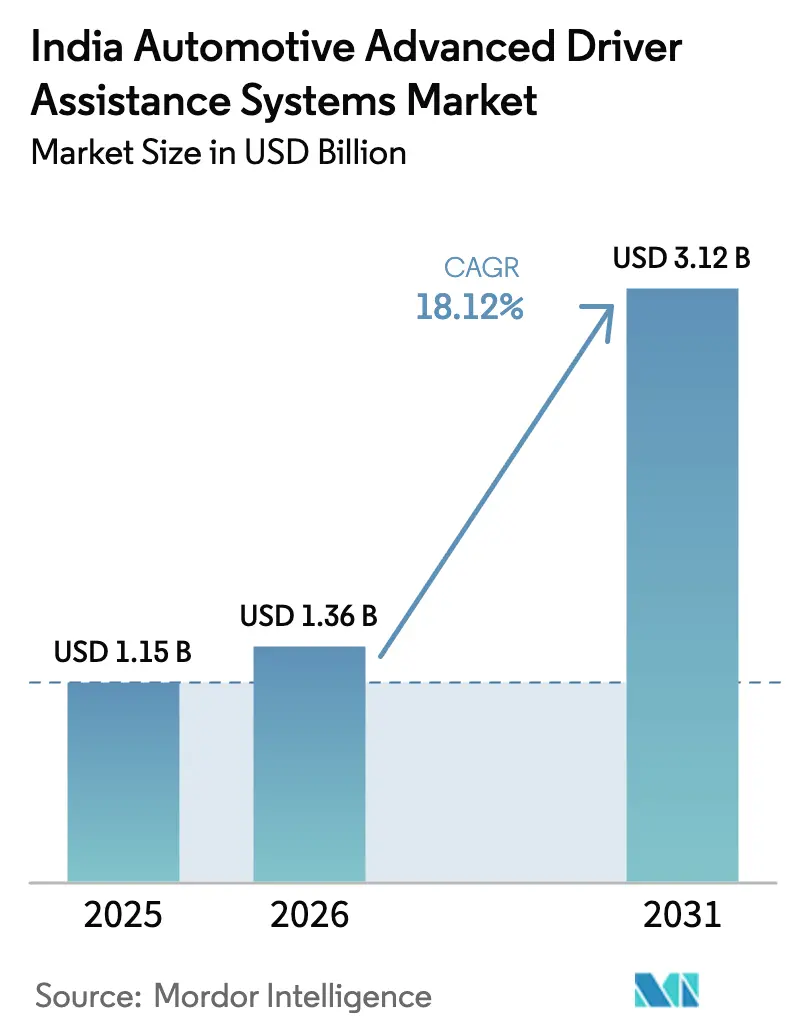

| Base Year Market Size (2025) | USD 1.15 Billion |

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 3.12 Billion |

| Growth Rate (2026 - 2031) | 18.12% CAGR |

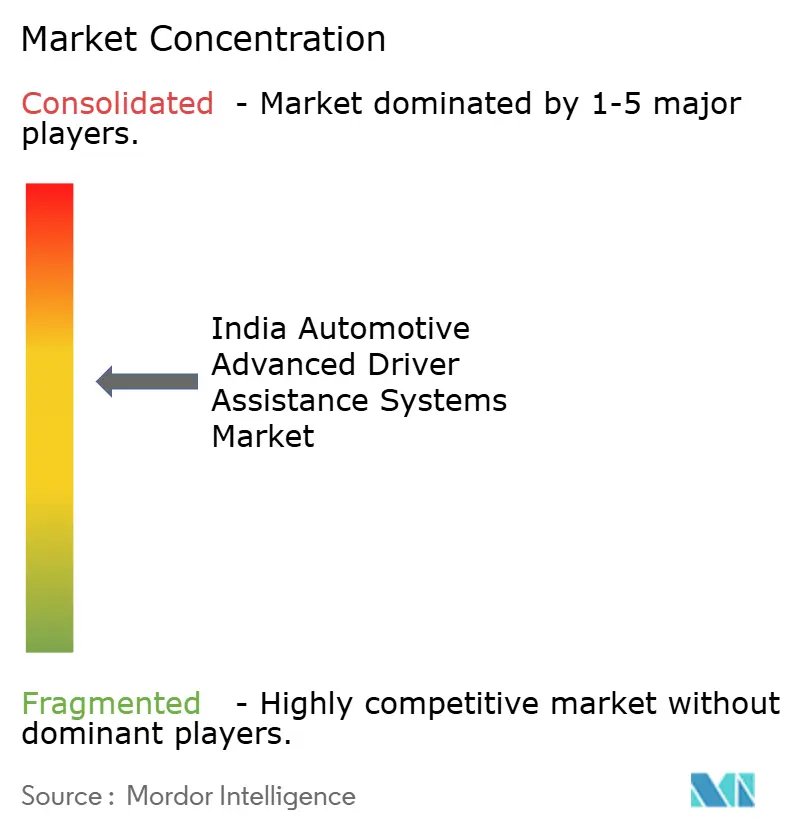

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automotive Advanced Driver Assistance Systems Market Analysis by Mordor Intelligence

The Indian automotive advanced driver assistance systems market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.36 billion in 2026 to reach USD 3.12 billion by 2031, at a CAGR of 18.12% during the forecast period (2026-2031). Accelerated growth stems from the Bharat NCAP mandate that shifts advanced driver-assistance systems from optional upgrades to compulsory fitments, steady sensor price declines, and the entry of Level 2+ functions into mid-segment cars. Original equipment manufacturers are also supported by the Production Linked Incentive (PLI) scheme, which expands local component capacity and softens foreign-exchange risk. Competitive intensity is moderate as Bosch, Continental, DENSO, and ZF adapt global platforms to India-specific conditions while new software-centric entrants pursue white-space opportunities. Strategic risks concentrate on inadequate lane markings, a shortage of certified calibration workshops, and incremental cybersecurity costs under AIS-189 that could temper mass-market adoption.

Key Report Takeaways

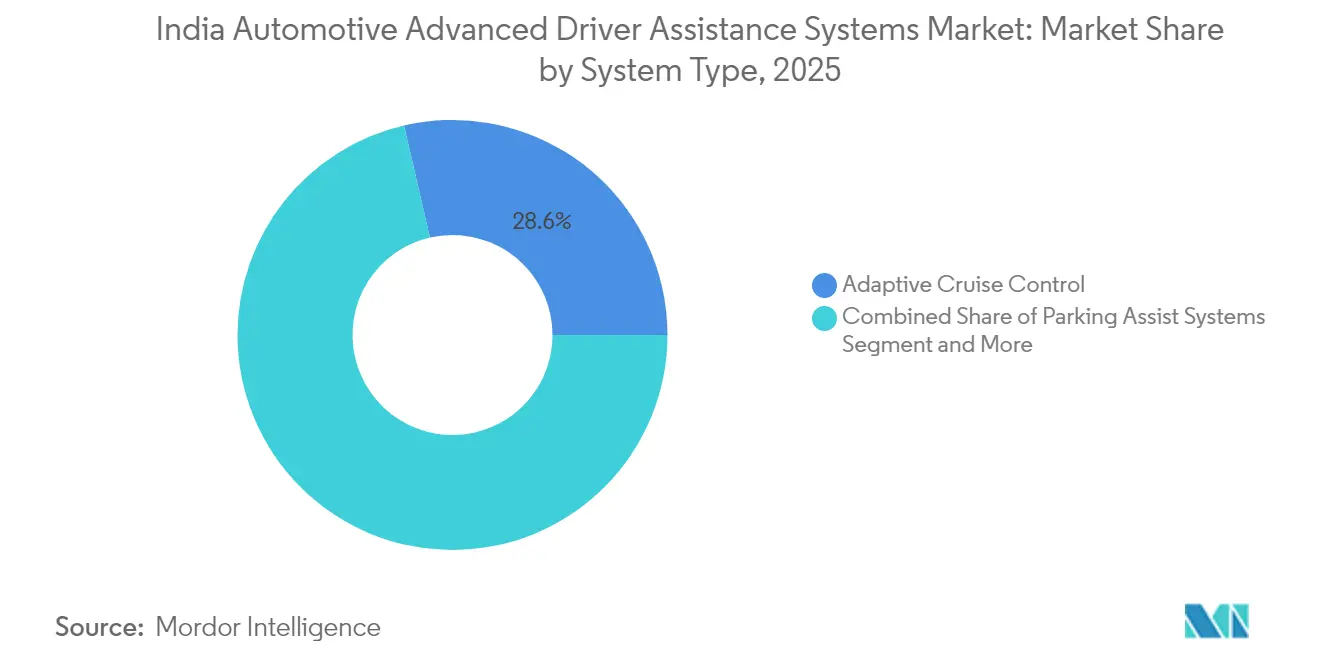

- By system type, Adaptive Cruise Control held 28.62% of the Indian automotive advanced driver assistance systems market share in 2025, whereas Automatic Emergency Braking is projected to post a 20.10% CAGR through 2031.

- By sensor technology, camera-based solutions commanded 42.70% of the Indian automotive advanced driver assistance systems market size in 2025, while LiDAR is forecast to expand at a 20.55% CAGR to 2031.

- By vehicle type, passenger cars accounted for 71.80% of the Indian automotive advanced driver assistance systems market size in 2025; two-wheelers are set to grow fastest at a 19.20% CAGR through 2031.

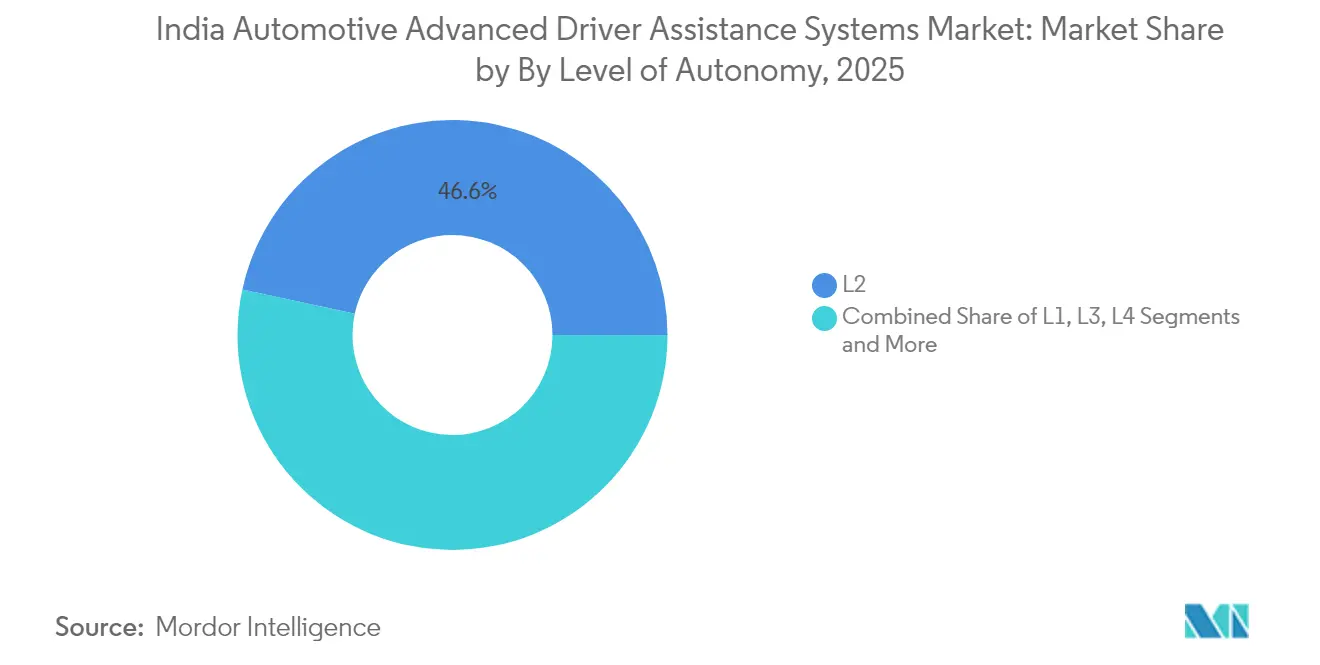

- By level of autonomy, Level 2 captured 46.60% of the market share in 2025, and Level 4 capabilities are projected to register at 22.70% CAGR by 2031.

- By sales channel, OEM-fitted solutions accounts 89.40% of the Indian automotive ADAS market share in 2025, whereas aftermarket retrofit solutions are projected to grow at a 20.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Automotive Advanced Driver Assistance Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bharat-NCAP Accelerates OEM Fitment | +4.5% | National; Delhi, Mumbai, Bangalore lead | Short term (≤ 2 years) |

| Usage-Based Insurance Discounts | +3.8% | Nationwide, metros adopt early | Short term (≤ 2 years) |

| PLI Incentives for ADAS | +3.2% | Automotive hubs nationwide | Long term (≥ 4 years) |

| Falling Radar and Camera Costs | +3.1% | Nationwide, aided by localized assembly | Medium term (2-4 years) |

| ADAS Reaches Mid-Segment Cars | +2.8% | Urban centers, expanding to Tier-2 cities | Medium term (2-4 years) |

| Radar-Based Rider Assistance | +2.5% | High two-wheeler density metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Bharat-NCAP Safety Mandate Accelerates OEM Fitment

The new Bharat NCAP protocol converts ADAS from a premium differentiator into a legal requirement across passenger and commercial platforms, forcing automakers to embed collision warning and automatic braking as standard equipment. Honda has already placed several ADAS-equipped vehicles on Indian roads, signaling industry readiness to meet stricter star-rating thresholds. Because safety scores now figure prominently in consumer purchase decisions, OEMs re-prioritize R&D budgets toward active-safety content rather than passive hardware. Parallel proposals from the Ministry of Road Transport and Highways to broaden ADAS obligations to buses and heavy trucks extend the addressable opportunity beyond personal mobility. Early compliance also mitigates regulatory uncertainty, allowing suppliers to lock in multi-year production volumes.

Usage-Based-Insurance Discounts Tied to ADAS Adoption

Telematics-enabled “Pay As You Drive” and “Pay How You Drive” policies now offer motorists premium reductions that can reach 15–25%, providing a direct financial return on ADAS-equipped vehicles. Leading insurers such as Tata AIG, Bharti AXA, and ICICI Lombard embed real-time driving-behavior scores into underwriting, which lowers claim frequency and severity while motivating safer habits. OEMs leverage these savings in showroom messaging to justify the ADAS price uplift, particularly for first-time buyers focused on monthly outlay. Fleet operators gain an additional margin lever because lower accident ratios translate into fewer unplanned repairs and reduced downtime for delivery vehicles. Data-sharing agreements between insurers and automakers also build anonymized crash databases that refine future ADAS algorithms, creating a virtuous circle that further accelerates feature penetration.

PLI Incentives for Local ADAS Component Manufacturing

The PLI scheme reimburses a significant share of incremental sales for eligible ADAS sensors, processors, and harnesses, encouraging global Tier-1s to co-locate lines with Indian partners. Domestic revenue from auto components climbed in FY 2024, signaling a supply base ready to absorb advanced electronics [1]“PLI-Auto adds three more firms to roster,” Mint, livemint.com. Tata Electronics’ wafer-fab in Gujarat and an assembly site in Assam promise secure chip pipelines for safety ECUs. Localization trims logistics costs, lowers currency-related volatility, and tailors hardware tolerances for India’s heat, dust, and vibration extremes. It also fosters joint R&D that embeds India-specific traffic datasets into perception stacks, elevating competitive moats for resident suppliers.

Falling Radar and Camera Costs Reach Sub-USD 20/Vehicle

Moore’s Law gains in semiconductor fabrication and component commonality with smartphones have pushed radar and camera bills-of-material below USD 20 per vehicle in 2025. Hyundai’s Venue variant illustrates how OEMs absorb modest cost upticks to defend share in the sub-INR 15 lakh bracket. The lower entry barrier unlocks demand in cost-sensitive city-car and micro-SUV segments that collectively command a large slice of domestic production. Sensor fusion architectures using radar and camera streams now hit acceptable price-performance ratios for dense, mixed-traffic conditions, improving monsoon and low-light settings reliability. As cost parity approaches traditional passive safety add-ons, ADAS becomes a de facto standard even in first-time-buyer vehicles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Incremental Vehicle Price (INR 70–90k) | -1.2% | Nationwide; acute in entry variants | Short term (≤ 2 years) |

| Shortage of Certified ADAS-Calibration Workshops | -0.9% | Tier-2/Tier-3 cities | Medium term (2-4 years) |

| Poor Road Markings and Infrastructure Noise | -0.8% | Rural, semi-urban, monsoon corridors | Long term (≥ 4 years) |

| AIS-189 Cybersecurity Compliance Adds ECU Cost | -0.6% | All OEMs and Tier-1s | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Incremental Vehicle Price (INR 70-90k)

Adding ADAS hardware inflates ex-showroom prices by INR 70,000–90,000 (~USD 789-1,015) or roughly 7–9% on a typical car, enough to push EMI-focused buyers toward lower trims. Consumers in value-driven A- and B-segment categories remain skeptical that insurance savings will offset the upfront outlay. Fleet operators display similar caution unless telematics proves direct accident-cost reductions. OEMs bundle ADAS only on top grades or offer limited-function packs to maintain showroom traffic, slowing penetration outside metro clusters. Over time, scale economies and stronger used-car residuals are expected to neutralize the sticker-shock barrier.

Shortage of Certified ADAS-Calibration Workshops

Only a limited network of manufacturer-approved service centers possesses the laser targets, alignment rigs, and software licenses required for post-repair sensor calibration, forcing many owners in Tier-2 and Tier-3 cities to travel over 150 km for a routine windshield replacement. Each calibration session costs raise the total cost of ownership and discourage feature activation on budget trims. Prolonged booking queues extend vehicle downtime for ride-hailing and logistics fleets that depend on high utilization rates. Improper or skipped calibration undermines system accuracy, heightening liability risks for dealers and insurers and eroding public trust in ADAS reliability. The gap has prompted OEMs to introduce mobile calibration vans and to subsidize technician training. Nationwide coverage is unlikely before 2028, temporarily constraining market growth in non-metro regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Regulatory Momentum Lifts Intervention Features

Adaptive Cruise Control still held the largest slice of the Indian automotive ADAS market share at 28.62% in 2025, favored by motorists traveling the Delhi–Mumbai and Hyderabad–Bangalore expressways. The Indian automotive ADAS market size attributable to collision-warning suites is expanding faster than comfort-oriented modules, underscoring a policy tilt toward active intervention. Secondary functions—Driver Drowsiness Alerts, Parking Assist, and Night Vision—ride on the same sensor stack, enabling OEMs to upsell via software toggles. Over-the-air updates keep feature roadmaps fluid, allowing manufacturers to monetize after-sales upgrades once regulatory approvals are secured.

Automatic Emergency Braking is on course for a 20.10% CAGR to 2031 as regulators and insurers converge on forward-collision mitigation metrics. Camera-centric lane departure warnings perform best on newly resurfaced corridors but struggle in patchy suburban stretches, prompting dual-sensor approaches that fuse short-range radar for lateral coverage. Traffic Sign Recognition, validated at 98% accuracy on Indian signage in a recent ICTACT Journal study, gains traction in speed-camera-dense zones where compliance avoids fines . The heightened emphasis on crash avoidance favors suppliers with proprietary datasets of local traffic idiosyncrasies, reinforcing first-mover advantages.

By Sensor Technology: LiDAR Gains as Costs Tumble

Camera modules benefited from smartphone-scale production, grabbing 42.70% of the Indian automotive ADAS market size in 2025. Radar’s all-weather capability secures its place in sensor fusion stacks indispensable for monsoon-season reliability. LiDAR shipments, once hampered by four-figure unit pricing, now pursue a 20.55% CAGR to 2031 as solid-state architectures drop below USD 500. The Indian automotive ADAS market finds value in LiDAR’s dense point clouds that resolve lane edges and vulnerable road users even in low-light or debris-laden conditions. Honda’s joint project with IIT Delhi and IIT Bombay pairs LiDAR with cameras and radar to map mixed-traffic layers involving rickshaws, cyclists, and jaywalkers. Ultrasonic sensors remain essential for close-range parking assistance where centimeter-level resolution trumps long-range reach.

Evolving ECU designs integrate dedicated AI accelerators, enabling in-vehicle sensor fusion. This filter redundant signals before cloud upload, conserving bandwidth. Suppliers differentiate through power-optimized ASICs that meet India’s high-temperature thresholds without active cooling, a key spend driver in compact engine bays.

By Vehicle Type: Two-Wheelers Emerge as the Next Frontier

Passenger cars commanded a 71.80% share in 2025, yet growth curves reveal a 19.20% CAGR for two-wheelers, the fastest in the Indian automotive ADAS market. Continental’s radar-based blind-spot detection kits debut on premium motorcycles but are expected to cascade to 125 cc commuter bikes as economies of scale kick in. The Indian automotive ADAS market size still skews toward four-wheelers, but new safety norms and consumer awareness signal a pivot. Commercial fleets adopt collision-warning and driver-monitoring suites to trim downtime and insurance overheads, particularly in e-commerce logistics where delivery uptime is revenue-critical.

The mass of two-wheeler users in Tier-2 cities creates a sizeable after-market for retrofit safety kits. However, packaging constraints and unit-cost ceilings require miniaturized radar modules and simplified HMIs, areas where domestic electronics makers seek licensing deals with global IP owners. OEMs that align two-wheeler ADAS rollouts with connected-helmet mandates could cement early mover reputations.

By Level of Autonomy: Controlled Level 4 Pilots Accelerate

L2 (partial automation) accounted for 46.60% of total deployments in 2025, making it the pragmatic ceiling under current traffic heterogeneity and legislative guardrails. L3 volumes remain marginal amid liability ambiguities, yet sandbox pilots proceed on select expressways with digital-twin mapping. L4 is projected to log a 22.70% CAGR through 2031 as OEMs and state authorities exploit fenced environments to validate near-autonomous shuttles.

The Indian automotive ADAS market thus incubates autonomy in niche operating domains before scaling outward. Behavioral data harvested in closed sites feed machine-learning loops that gradually extend to public-road pilots once safety regulators codify performance benchmarks. Full L5 remains a long-tail target pending uniform infrastructure and cross-state harmonization.

By Sales Channel: Aftermarket Disrupts OEM Dominance

OEM-fitted solutions captured 89.40% of the Indian automotive ADAS market share in 2025, underlining automakers’ advantage in factory validation, warranty integration, and cost-efficient scale. Factory installation streamlines calibration and over-the-air update routines, assuring regulators that every unit leaving the assembly line meets the Bharat NCAP compliance threshold. The Indian automotive ADAS market size is tied to OEM channels; therefore, it continues to expand as new vehicle sales grow. Yet, its percentage share will gradually compress as retrofit activity accelerates. Automakers also leverage tightly knit supplier contracts to bundle multiple safety functions into cohesive suites, reducing per-feature pricing and reinforcing showroom dominance among first-time buyers.

Despite their small base, aftermarket retrofit solutions are projected to grow at a 20.70% CAGR through 2031 as existing vehicle owners seek cost-effective safety upgrades. The Indian automotive ADAS market size for retrofit kits benefits from modular plug-and-play architectures that let consumers select discreet functions, collision warning, lane departure alarms, or parking assist, rather than purchasing an entire factory package. Rising awareness, falling sensor costs, and longer average vehicle lifespans widen the retrofit addressable pool, especially in metros where insurance discounts favor ADAS-equipped cars.

Geography Analysis

Metropolitan clusters, Delhi-NCR, Mumbai-Pune, Bengaluru, and Chennai, form the epicenter of the Indian automotive ADAS market, thanks to higher disposable incomes, better lane discipline on newer expressways, and dealership networks equipped for advanced calibration. The corridor linking Delhi and Mumbai alone hosts a dense mix of ADAS-ready models and service centers, accounting for an outsized slice of early-adopter volume. Insurance products tied to usage-based telematics debut first in these metros, sharpening the value proposition through tangible premium savings.

Tier-2 hubs such as Hyderabad, Ahmedabad, and Coimbatore now witness follow-on demand as OEMs promote ADAS features in mid-tier trims. The Indian automotive ADAS market faces infrastructure gaps, sporadic lane markings, and fewer certified workshops, yet consumer aspiration spurs uptake, particularly among tech-savvy millennials. Manufacturers deploy mobile calibration vans and cloud-based diagnostics to bridge the service void and prevent buyer hesitation.

Rural and semi-urban belts remain the slowest adopters due to fragmented after-sales ecosystems and rough road geometry that challenge camera algorithms. Nevertheless, radar-centric collision warnings find relevance on national highways where livestock and slow-moving tractors pose unique hazards. Government PLI clusters in Gujarat, Tamil Nadu, and Haryana are expected to radiate economic spillovers that progressively raise safety feature penetration in adjoining districts.

Competitive Landscape

Global Tier-1 companies, including Bosch, Continental, DENSO, and ZF, anchor a significant share of the Indian automotive ADAS market, reflecting the scale and certification hurdles that guard entry. Bosch’s AI fund accelerates perception-stack enhancements, while Continental’s Aumovio pivot underscores a bet on software-defined vehicles tailored to India’s traffic complexity [3]Market Desk, “Continental rebrands software unit as Aumovio,” Business Standard, business-standard.com. Despite consolidation at the top, the market remains open to agile software houses such as KPIT and Tata Elxsi, which license perception algorithms and middleware to multiple OEMs.

Domestic suppliers gain an edge through cost-optimized hardware and localized data labeling. Varroc Engineering partners with Israeli sensor firms to co-design sub-USD 200 radar modules targeting two-wheeler OEMs. Meanwhile, Mobileye deploys its EyeQ SoCs inside Mahindra and Tata platforms, banking on a robust local integrator ecosystem for scalability. White-space pockets include aftermarket retrofits for commercial trucks and ADAS-ready ECUs for electric three-wheelers, segments neglected by legacy giants.

Price pressure compels top players to re-architect sensor suites into modular kits adaptable across vehicle categories. Strategic alliances with telecom operators aim to leverage 5G low-latency links for edge-cloud cooperation, vital for high-definition map updates in chaotic city grids. Suppliers able to navigate cost limits while ensuring AIS-189 cybersecurity compliance will solidify long-term moats.

India Automotive Advanced Driver Assistance Systems Industry Leaders

Robert Bosch GmbH

Continental AG

DENSO Corporation

ZF Friedrichshafen AG

Valeo SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The Automotive Research Association of India inaugurated the nation’s first ADAS Test City in Pune to validate systems under controlled yet India-realistic traffic scenarios.

- September 2025: Tata Motors equipped the Nexon EV with an ADAS bundle—including lane-keep assist and autonomous emergency braking—making it the most affordable electric SUV in India with such features.

- June 2025: Mahindra & Mahindra launched Level 2 ADAS in the Scorpio-N Z8L variant, adding adaptive cruise, lane-keeping, and smart pilot assist to its mid-size SUV.

- March 2025: The Ministry of Road Transport and Highways proposed mandatory AEBS, DDAWS, and LDWS for vehicles carrying more than eight passengers starting April 2026.

India Automotive Advanced Driver Assistance Systems Market Report Scope

Vehicle manufacturers develop and deploy advanced driver assistance systems (ADAS) to improve road safety. These systems have the potential to avoid crashes, reduce crash severity, and offer protection.

The Indian automotive advanced driver assistance systems market is segmented by type, technology, and vehicle. By type, the market is segmented into parking assist systems, adaptive front-lighting, night vision systems, blind spot detection, advanced automatic emergency braking systems, collision warning, driver drowsiness alert, traffic sign recognition, lane departure, and adaptive cruise control. By technology, the market is segmented into RADAR, LiDAR, and camera. By vehicle type, the market is segmented into passenger cars and commercial vehicles. The report offers market size and forecasts for all the mentioned segmentation in terms of value (USD).

By System Type

| Parking Assist Systems |

| Adaptive Front-Lighting |

| Night Vision Systems |

| Blind-Spot Detection |

| Automatic Emergency Braking |

| Forward Collision Warning |

| Driver Drowsiness Alert |

| Traffic Sign Recognition |

| Lane Departure Warning |

| Adaptive Cruise Control |

By Sensor Technology

| Radar |

| LiDAR |

| Camera |

| Ultrasonic |

| Infra-red |

By Vehicle Type

| Two-Wheelers |

| Passenger Cars |

| Medium and Heavy Commercial Vehicles |

By Level of Autonomy

| L1 |

| L2 |

| L3 |

| L4 |

| L5 |

By Sales Channel

| OEM-Fitted |

| Aftermarket Retrofit |

| By System Type | Parking Assist Systems |

| Adaptive Front-Lighting | |

| Night Vision Systems | |

| Blind-Spot Detection | |

| Automatic Emergency Braking | |

| Forward Collision Warning | |

| Driver Drowsiness Alert | |

| Traffic Sign Recognition | |

| Lane Departure Warning | |

| Adaptive Cruise Control | |

| By Sensor Technology | Radar |

| LiDAR | |

| Camera | |

| Ultrasonic | |

| Infra-red | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Medium and Heavy Commercial Vehicles | |

| By Level of Autonomy | L1 |

| L2 | |

| L3 | |

| L4 | |

| L5 | |

| By Sales Channel | OEM-Fitted |

| Aftermarket Retrofit |

Key Questions Answered in the Report

What is the current value of the India automotive ADAS market?

The market stands at USD 1.36 billion in 2026 and is on track to reach USD 3.12 billion by 2031.

Which ADAS feature holds the largest share today?

Adaptive Cruise Control leads with 28.62% share of system-level revenue.

Which vehicle category is growing fastest in ADAS adoption?

Two-wheelers show the quickest uptake, projected at a 19.20% CAGR through 2031.

Which sensor technology is set to see the sharpest growth?

LiDAR is poised for a 20.55% CAGR as solid-state prices fall.

Page last updated on: