High Volume Dispensing Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

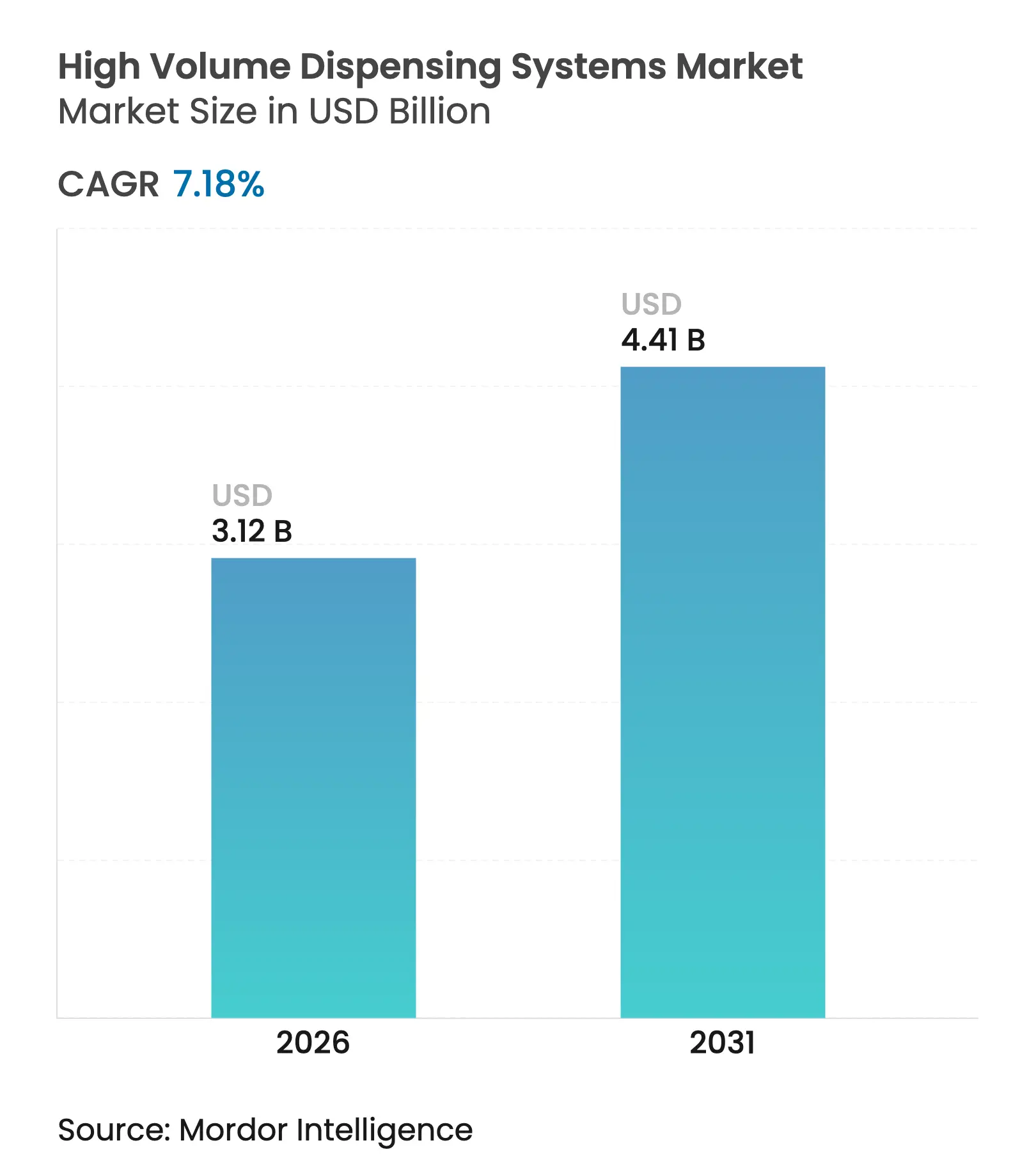

| Market Size (2026) | USD 3.12 Billion |

| Market Size (2031) | USD 4.41 Billion |

| Growth Rate (2026 - 2031) | 7.18 % CAGR |

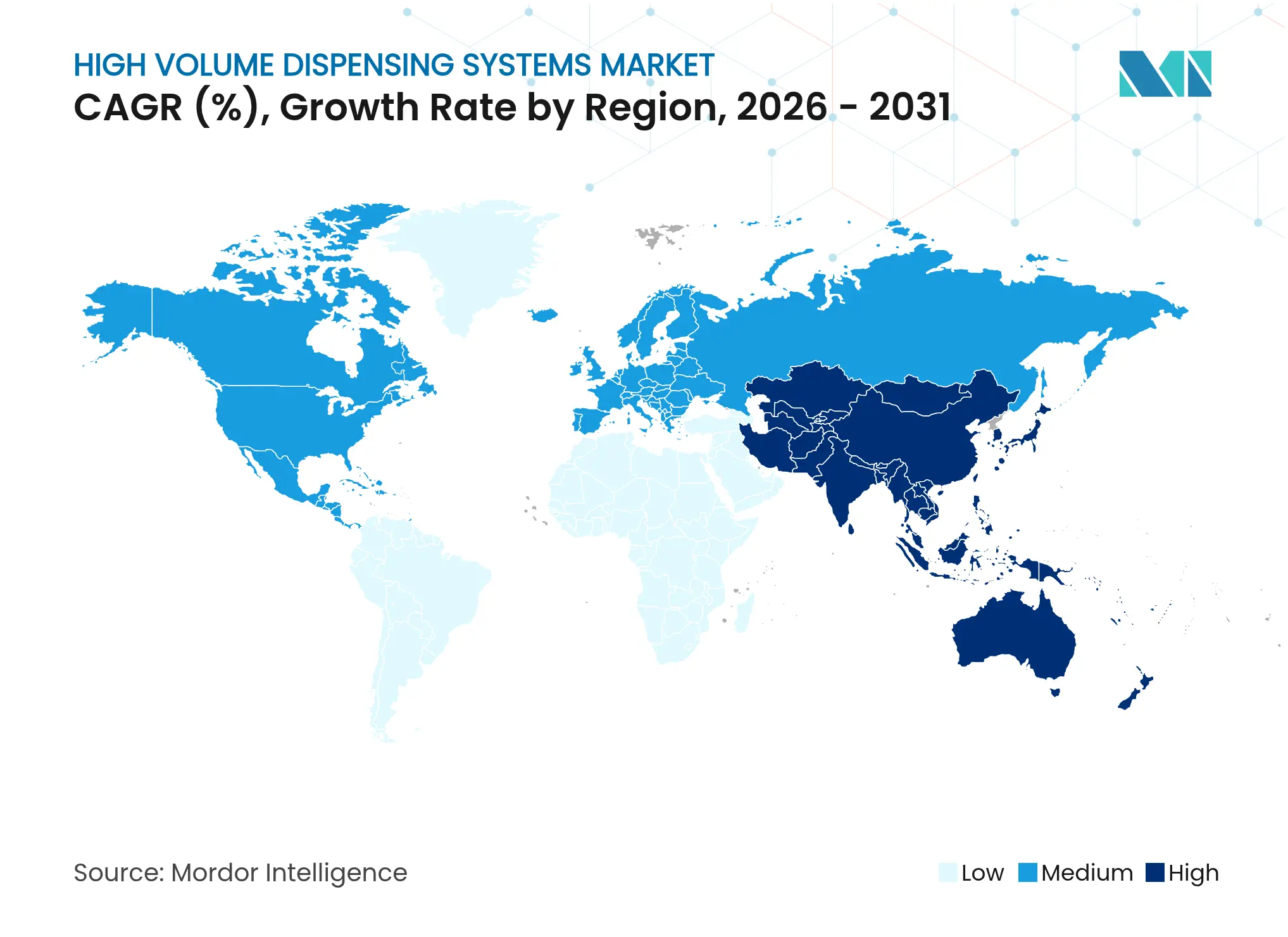

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

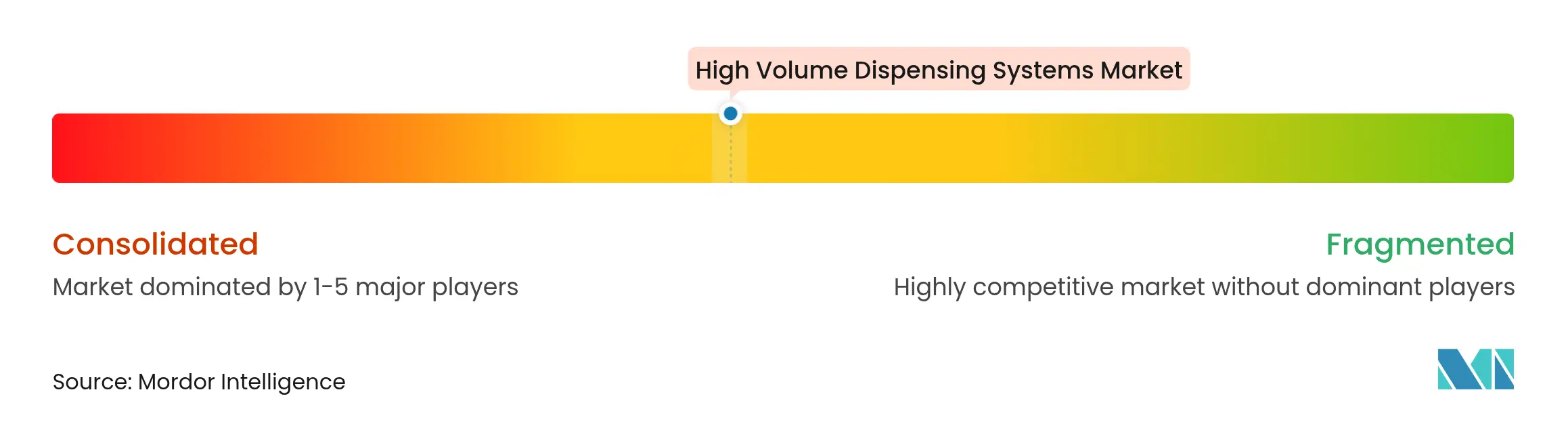

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

High Volume Dispensing Systems Market Analysis by Mordor Intelligence

The high-volume dispensing systems market size was valued at USD 2.91 billion in 2025 and estimated to grow from USD 3.12 billion in 2026 to reach USD 4.41 billion by 2031, at a CAGR of 7.18% during the forecast period (2026-2031). Demand acceleration stems from mandatory drug-traceability rules, the pharmacy sector’s labor squeeze, and mounting prescription loads that manual workflows can no longer absorb. Hardware still anchors most installations, yet competitive advantage is shifting toward cloud software that orchestrates robotics, assures Drug Supply Chain Security Act (DSCSA) compliance, and converts transaction data into inventory intelligence. Central-fill hubs are proliferating in North America and now gaining regulatory backing in Europe and Asia-Pacific, creating a market environment in which scale, analytics, and cyber-resilience determine supplier success. The rising threat landscape—underscored by the February 2024 Change Healthcare ransomware incident—has also made hardened security architectures a purchase criterion equal to mechanical throughput.

Key Report Takeaways

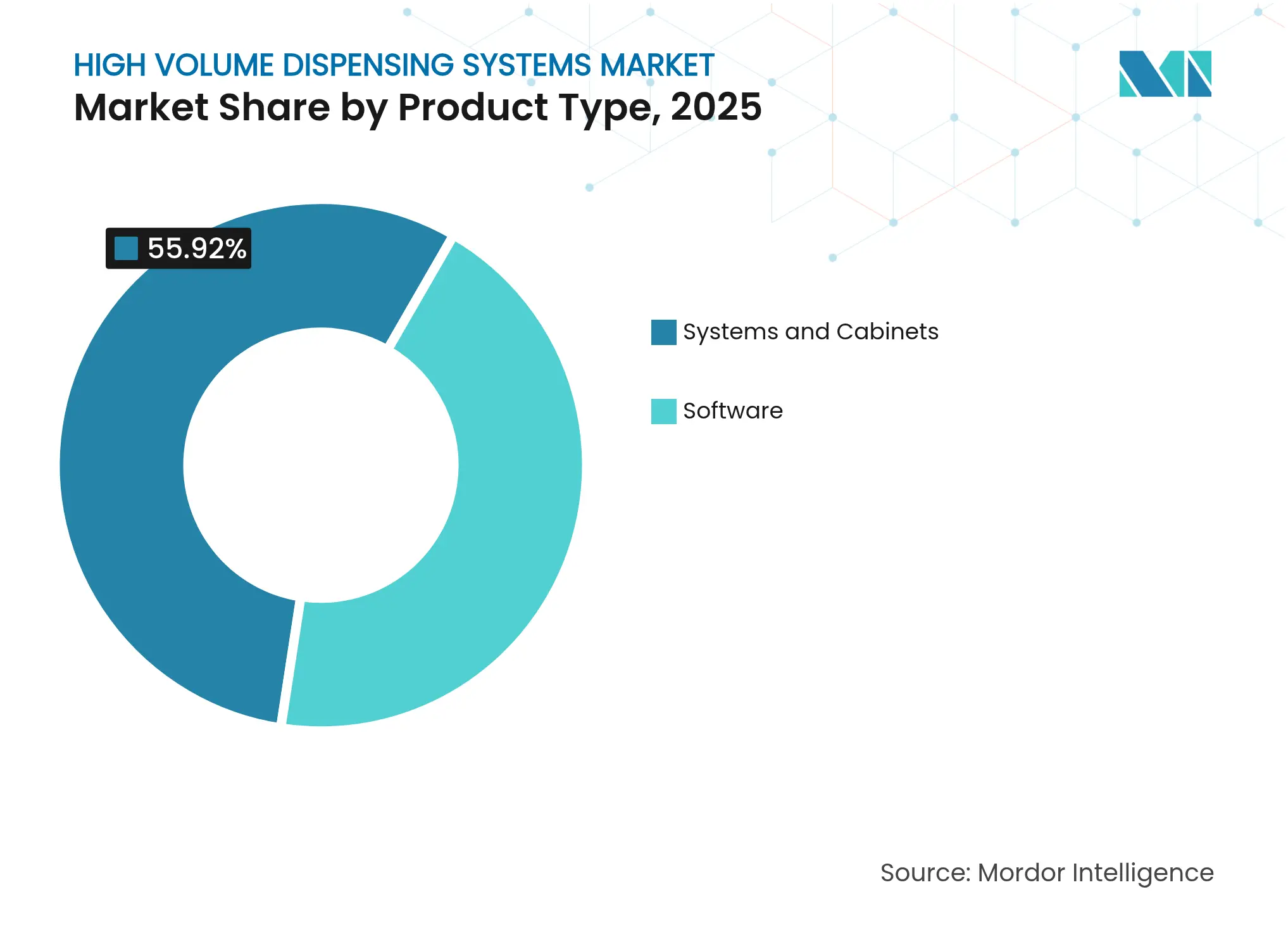

- By product type, systems & cabinets provided 55.92% of 2025 revenue, whereas software is expanding at a 10.42% CAGR through 2031.

- By end user, mail-order and central-fill facilities are tracking a 14.32% CAGR, while retail chains retained 50.88% revenue share in 2025.

- By geography, North America contributed a 37.14% slice of 2025 turnover, but Asia-Pacific is on course for 10.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High Volume Dispensing Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing adoption of pharmacy automation platforms

Growing adoption of pharmacy automation platforms

| +2.1% | Global, led by North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.1%

| Geographic Relevance:

Global, led by North America

| Impact Timeline:

Medium term (2-4 years)

|

Rising prescription volumes & ageing population

Rising prescription volumes & ageing population

| +1.8% | Global, especially developed markets | Long term (≥ 4 years) | |||

Pharmacist labour shortages & wage pressure

Pharmacist labour shortages & wage pressure

| +1.6% | North America & Europe | Short term (≤ 2 years) | |||

Regulatory mandates for dispensing accuracy &

serialisation

Regulatory mandates for dispensing accuracy &

serialisation

| +1.4% | North America, expanding globally | Medium term (2-4 years) | |||

Expansion of hub-and-spoke central-fill models

Expansion of hub-and-spoke central-fill models

| +1.2% | UK, US, Canada first | Medium term (2-4 years) | |||

AI-led predictive inventory & workflow optimisation

AI-led predictive inventory & workflow optimisation

| +0.9% | APAC core, spill-over to NA & EU | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Adoption of Pharmacy Automation Platforms

Healthcare operators increasingly view robotics, automated storage, and SaaS workflow engines as infrastructure rather than optional add-ons. Walgreens’ micro-fulfillment network now processes nearly 35,000 scripts daily at each hub, trimming on-site pharmacist load by 25% and yielding USD 1 billion in annual savings. Subscription-based “central fill as a service” contracts extend similar efficiencies to independent outlets, replacing capex with per-script fees. Freed from repetitive counting, pharmacists can allocate time to vaccinations and chronic-disease counseling, activities with higher reimbursement potential. Vendors are also bundling analytics dashboards that identify slow-moving stock and automate reorder points, further cementing the value proposition. Because these gains are measurable within one budget cycle, boards are green-lighting automation projects despite capital constraints.

Rising Prescription Volumes & Ageing Population

Global life-expectancy gains and the surge in chronic-disease prevalence are swelling annual script counts beyond the capacity of manual fulfillment. In developed economies, polypharmacy for seniors now averages eight concurrent medications, increasing interaction risk and scheduling complexity. Automated dispensers synchronize refill dates, print patient-specific labels, and flag contraindications with near-perfect accuracy. Specialty therapeutics, many of which require temperature-controlled packaging, also benefit: integrated robots maintain 2-8 °C storage without human intervention. Health ministries across Europe and Japan cite automation as a linchpin for sustaining pharmaceutical care amid workforce shortages. Consequently, the high-volume dispensing systems market is poised to ride long-term demographic tailwinds while alleviating immediate workload stress.

Pharmacist Labour Shortages & Wage Pressure

Post-pandemic burnout has pushed community-pharmacist turnover above 25% and lifted average wages faster than reimbursement schedules. Automation offers a productivity lever that offsets wage inflation while improving job satisfaction. Rural stores, where recruitment is toughest, use telepharmacy oversight coupled with robotic dispensing to keep doors open, preserving medicine access for underserved populations. Technician roles are simultaneously upskilling; with robots managing counting and labeling, certified technicians perform quality checks, extending pharmacist reach. Union discussions now often frame automation not as a threat, but as a prerequisite for clinical career progression. These workforce economics make capital allocation toward automation increasingly defensible in boardrooms.

Regulatory Mandates for Dispensing Accuracy & Serialisation

The DSCSA’s November 2024 enforcement milestone obliges US pharmacies to capture, verify, and store unit-level transaction data electronically[1]Center for Drug Evaluation and Research, “FDA's Implementation of Drug Supply Chain Security Act (DSCSA) Requirements,” Food and Drug Administration, fda.gov. Manual compliance is impractical at today’s volume scale, driving accelerated purchases of vision-inspection modules, barcode readers, and cloud traceability software. Comparable frameworks are emerging in Canada, the EU, and several Gulf states, making serialization a global norm. Automated solutions achieve 99.99% dispensing accuracy, dramatically reducing error-related liability and positioning compliance as a built-in feature rather than an added workflow. Consequently, serialization mandates function as a growth catalyst, especially for cloud software able to integrate package-level data into enterprise resource planning stacks.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital & integration costs

High capital & integration costs

| -1.2% | Global, smaller independents hardest hit | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-1.2%

| Geographic Relevance:

Global, smaller independents hardest hit

| Impact Timeline:

Short term (≤ 2 years)

|

Data-security / system-interoperability hurdles

Data-security / system-interoperability hurdles

| -0.8% | North America & Europe | Medium term (2-4 years) | |||

PBM consolidation delaying chain capex

PBM consolidation delaying chain capex

| -0.6% | North America | Medium term (2-4 years) | |||

Shortage of automation-skilled technicians in rural areas

Shortage of automation-skilled technicians in rural areas

| -0.4% | Developing markets worldwide | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital & Integration Costs

Robotic dispensers, conveyor systems, and serialization cameras demand six-figure investments even before software licenses and facility renovations. Independents with thin operating margins often cannot secure financing, especially when interest rates exceed 6%. Integration adds complexity: legacy pharmacy management systems require custom middleware, data migration, and staff re-training that can extend project timelines by nine months. To mitigate sticker shock, vendors are promoting subscription models in which ownership remains with the supplier and pharmacies pay usage fees. Proof-of-concept deployments in small chains have shown positive cash flow within the first year of service, indicating that the upfront-cost barrier is eroding but not yet eliminated.

Data-Security / System-Interoperability Hurdles

The Change Healthcare ransomware attack exposed the vulnerability of interconnected dispensing and claims networks, inciting board-level scrutiny of cyber protocols. Automated hardware multiplies endpoints, each of which must be patched, monitored, and audited. Meanwhile, differing HL7, FHIR, and proprietary data standards impede seamless linkage between robots, electronic health records, and payer portals. API standardization is improving, but smaller IT teams still face steep learning curves. Vendors now embed zero-trust security frameworks and offer managed detection services, but reputational risk remains an adoption drag, especially in Europe where GDPR penalties loom large.

Segment Analysis

By Product Type: Software Drives Innovation

The software layer captured only 44.08% revenue in 2025, yet it is expanding at a 10.42% CAGR, outpacing hardware and signaling an intelligence-first future for the high-volume dispensing systems market. Modern cloud suites integrate robotic workflows, inventory management, and DSCSA traceability into a single console, lifting utilization rates across multiple hubs. Omnicell’s OmniSphere launch demonstrates this shift, adding HITRUST-certified data protection and role-based access that health systems demand. Software’s value proposition also scales: incremental users or pharmacies can be activated without new physical assets, protecting cash flow and speeding ROI.

Systems & cabinets nonetheless remain essential; they generated 55.92% of 2025 turnover by physically executing high-throughput counting, labeling, and pouch packaging. Advances include vision-guided pick-and-place arms capable of 120 fills per hour and shuttle-based storage modules that double density per square meter. The high-volume dispensing systems market size attributable to central-fill robotic lines alone is projected to grow from USD 1.65 billion in 2025 to USD 2.42 billion by 2031, mirroring chain-wide adoption. Integration between hardware and SaaS platforms is evolving toward plug-and-play standards, allowing pharmacies to upgrade software capabilities without forklift hardware replacements.

Note: Segment shares of all individual segments available upon report purchase

By End User: Central-Fill Models Transform Operations

Mail-order and central-fill hubs are the fastest movers, racing at a 14.32% CAGR as legislation and consumer preference converge. The segment handled 26% of US retail prescriptions in 2025 and is expected to top 40% by 2031, supported by payer incentives for 90-day supplies. The UK mandate that every local pharmacy access a hub by 2025 further cements the model’s momentum. For vendors, the migration creates recurring revenue opportunities in software licensing, maintenance, and replenishment services.

Traditional retail chains still dominate absolute volume; they controlled 50.88% of 2025 revenue. Yet, their role is evolving toward patient engagement centers where medication synchronization, counseling, and vaccination occur. Hospital and health-system pharmacies trail retail on adoption but are accelerating purchases to mitigate sterile-compounding risks and technician shortages. The high-volume dispensing systems market share captured by health-system networks is forecast to climb two percentage points by 2031 as integrated delivery networks bring outpatient and inpatient fulfillment onto shared robotic platforms. Long-term care and specialty providers round out end-user demand, valuing the precision and traceability that robots deliver for high-acuity medications.

Geography Analysis

North America held a commanding 37.14% slice of 2025 sales, buoyed by early robotics rollouts, DSCSA compliance deadlines, and a dense network of chain pharmacies able to amortize investments across thousands of stores. The United States alone deployed 180 additional central-fill lines in 2024, a figure expected to rise again in 2025 as reimbursement pressures push chains toward scale economies. Canada’s health authorities are financing automation pilots in provincial drug programs, while Mexico’s private sector is installing small-footprint robots to meet urban demand.

Asia-Pacific is the pace-setter, projected to register 10.38% CAGR into 2031. China’s pharmaceutical modernization and robust e-commerce penetration foster rapid central-fill uptake; the high-volume dispensing systems market size sourced from Chinese installations is forecast to double over the forecast horizon. Japan’s digitally driven outpatient reforms have already mechanized 90% of dispensing tasks at some Tomod’s locations. India’s SAMARTH Udyog Bharat 4.0 initiative is channeling incentives toward automated material-handling suppliers, accelerating adoption in tier-1 hospital chains. South Korea and Australia contribute complementary demand, anchored in robust medicare-like payer systems that reimburse remote dispensing services.

Europe, the Middle East & Africa, and South America together contribute less than one-third of global revenue today but exhibit diverse high-growth pockets. Germany and France are standardizing e-prescriptions, clearing a pathway for fully automated refill services. GCC nations fund hospital megaprojects with robotics baked into initial blueprints, while Brazil’s large private-insurance market is piloting hub-and-spoke designs in São Paulo. Across these regions, the high-volume dispensing systems market is often catalyzed by public-private partnerships that bundle technology transfer with workforce training.

Competitive Landscape

Market Concentration

Incumbent suppliers—Omnicell, BD-Parata, and McKesson—command the majority of revenue share, yet the arena remains only moderately concentrated. Competitive intensity now centers on software ecosystems rather than mechanical throughput. BD’s USD 1.52 billion purchase of Parata extended its reach from medication delivery devices into retail automation, unlocking cross-selling opportunities.

Start-ups such as Asepha are entering with AI-first strategies that emphasize predictive restocking and anomaly detection; the firm closed a USD 4 million seed round in July 2025. Cybersecurity specialists are also carving niches, offering zero-trust appliances that bolt onto legacy robots to safeguard against ransomware. Hardware manufacturers respond by embedding secure-boot firmware and encrypted communications, turning security from an after-sales bolt-on into a core product feature.

Strategic partnerships are proliferating across the value chain. McKesson expanded specialty capabilities by acquiring Prism Vision Holdings in February 2025. At the same time, telepharmacy provider Avel eCare bought Hospital Pharmacy Management to integrate remote verification with automated compounding. These moves underline a convergence trend where hardware, software, and clinical services merge into unified platforms capable of delivering medication from factory to bedside.

High Volume Dispensing Systems Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Walgreens opened a micro-fulfillment center in Brooklyn Park, Minnesota, to support 200 regional stores.

- August 2024: Capsa Healthcare showcased central-fill and mail-order capabilities at the NACDS Total Store Expo in Boston.

Table of Contents for High Volume Dispensing Systems Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing Adoption Of Pharmacy Automation Platforms

- 4.2.2Rising Prescription Volumes & Ageing Population

- 4.2.3Pharmacist Labour Shortages & Wage Pressure

- 4.2.4Regulatory Mandates For Dispensing Accuracy & Serialisation

- 4.2.5Expansion Of Hub-And-Spoke Central-Fill Models

- 4.2.6AI-Led Predictive Inventory & Workflow Optimisation

- 4.3Market Restraints

- 4.3.1High Capital & Integration Costs

- 4.3.2Data-Security / System-Interoperability Hurdles

- 4.3.3PBM Consolidation Delaying Chain Capex

- 4.3.4Shortage Of Automation-Skilled Technicians In Rural Areas

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers/Consumers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitute Products

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Systems & Cabinets

- 5.1.1.1Central-Fill Robotic Dispensing Systems

- 5.1.1.2Automated Counting & Filling Machines

- 5.1.1.3Packaging & Labelling Systems

- 5.1.1.4Automated Storage & Retrieval Cabinets

- 5.1.2Software

- 5.1.2.1Workflow-Management Software

- 5.1.2.2Inventory-Management Platforms

- 5.1.2.3Analytics & Reporting Suites

- 5.1.2.4Cloud-Based SaaS Platforms

- 5.2By End User

- 5.2.1Retail Pharmacy Chains

- 5.2.2Hospital Pharmacy

- 5.2.3Mail-Order & Central-Fill Pharmacies

- 5.2.4Long-Term Care & Specialty Pharmacies

- 5.2.5Pharma Manufacturers & 3PLs

- 5.3Geography

- 5.3.1North America

- 5.3.1.1United States

- 5.3.1.2Canada

- 5.3.1.3Mexico

- 5.3.2Europe

- 5.3.2.1Germany

- 5.3.2.2United Kingdom

- 5.3.2.3France

- 5.3.2.4Italy

- 5.3.2.5Spain

- 5.3.2.6Rest of Europe

- 5.3.3Asia-Pacific

- 5.3.3.1China

- 5.3.3.2Japan

- 5.3.3.3India

- 5.3.3.4South Korea

- 5.3.3.5Australia

- 5.3.3.6Rest of Asia-Pacific

- 5.3.4Middle East and Africa

- 5.3.4.1GCC

- 5.3.4.2South Africa

- 5.3.4.3Rest of Middle East and Africa

- 5.3.5South America

- 5.3.5.1Brazil

- 5.3.5.2Argentina

- 5.3.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Omnicell Inc.

- 6.3.2Becton Dickinson & Co. (Parata/BD Rowa)

- 6.3.3McKesson Corporation

- 6.3.4Innovation Associates

- 6.3.5ARxIUM

- 6.3.6ScriptPro LLC

- 6.3.7Healthmark Services

- 6.3.8RxSafe LLC

- 6.3.9Swisslog Healthcare

- 6.3.10Talyst Systems

- 6.3.11Capsa Healthcare

- 6.3.12Yuyama Co. Ltd.

- 6.3.13Tosho Inc.

- 6.3.14Willach Pharmacy Solutions

- 6.3.15Tension Packaging & Automation

- 6.3.16Rowa Pharmacy Solutions (legacy brand)

- 6.3.17R/X Automation Solutions

- 6.3.18Medi-Dose Inc.

- 6.3.19Capsule Technologie (Central-Fill EU)

- 6.3.20Aesynt (now part of Omnicell)

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global High Volume Dispensing Systems Market Report Scope

As per the scope of the report high volume dispensing systems are cabinets for handling and provision of large volume medication catalogue. This report is segmented by product type, by end user, and by geography.