CXL Attached DRAM Module Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

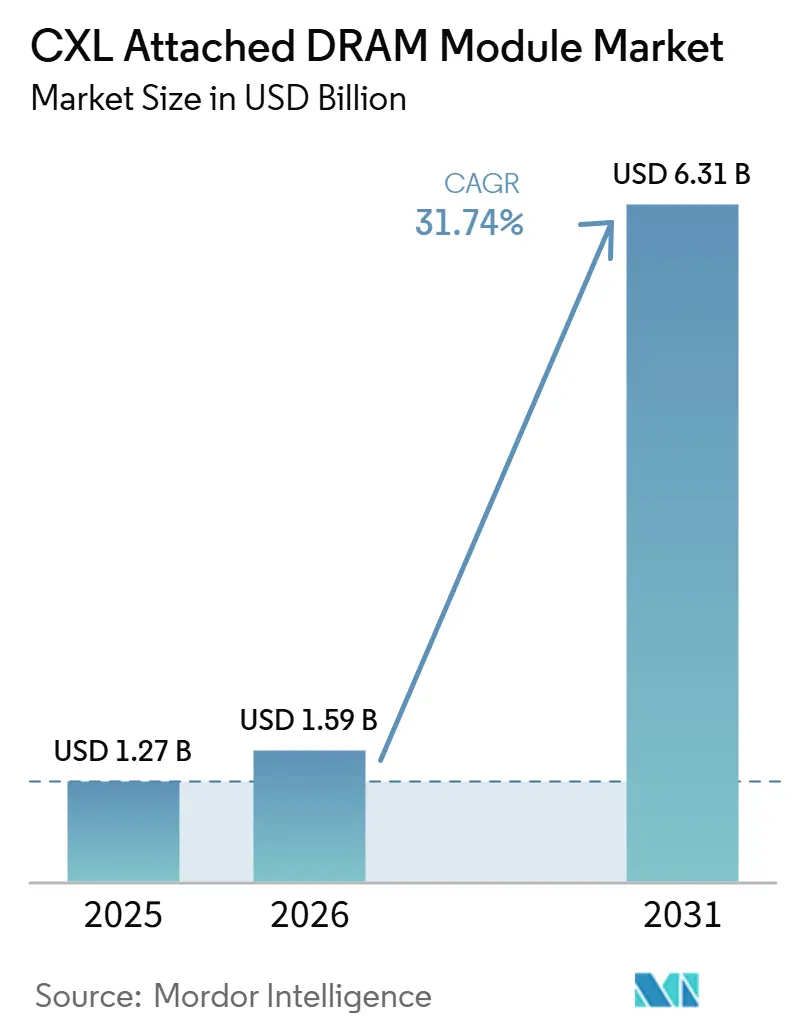

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 6.31 Billion |

| Growth Rate (2026 - 2031) | 31.74% CAGR |

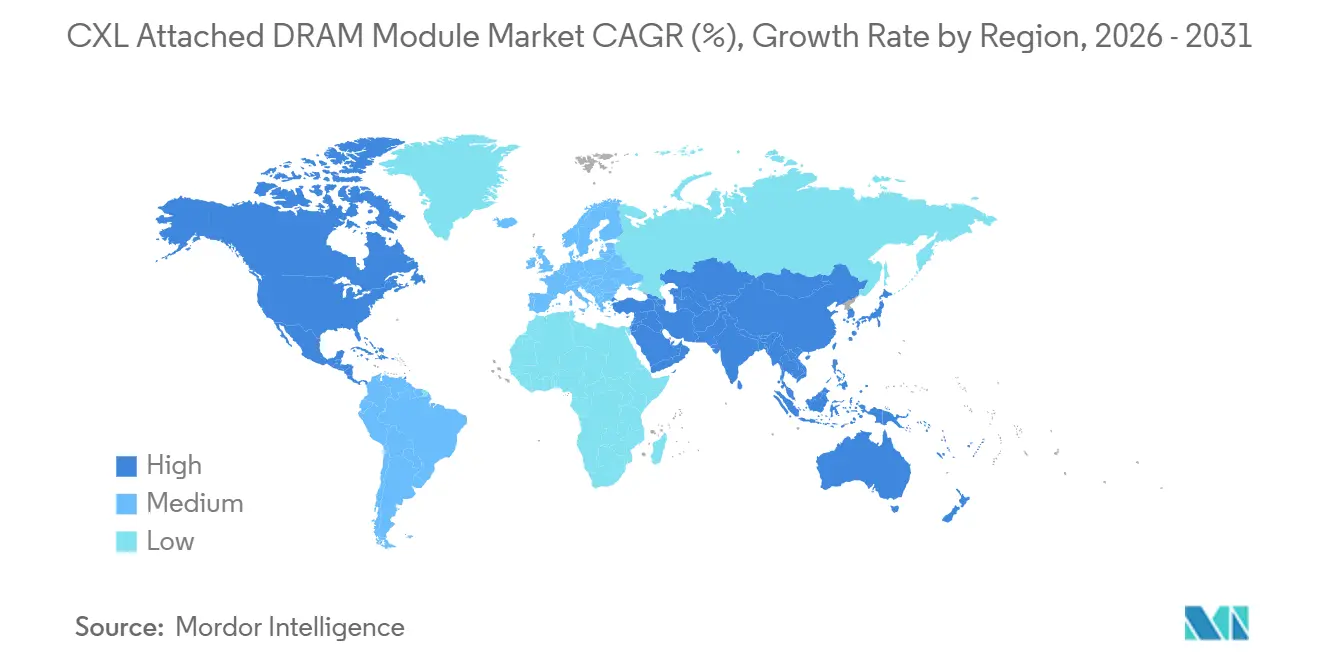

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

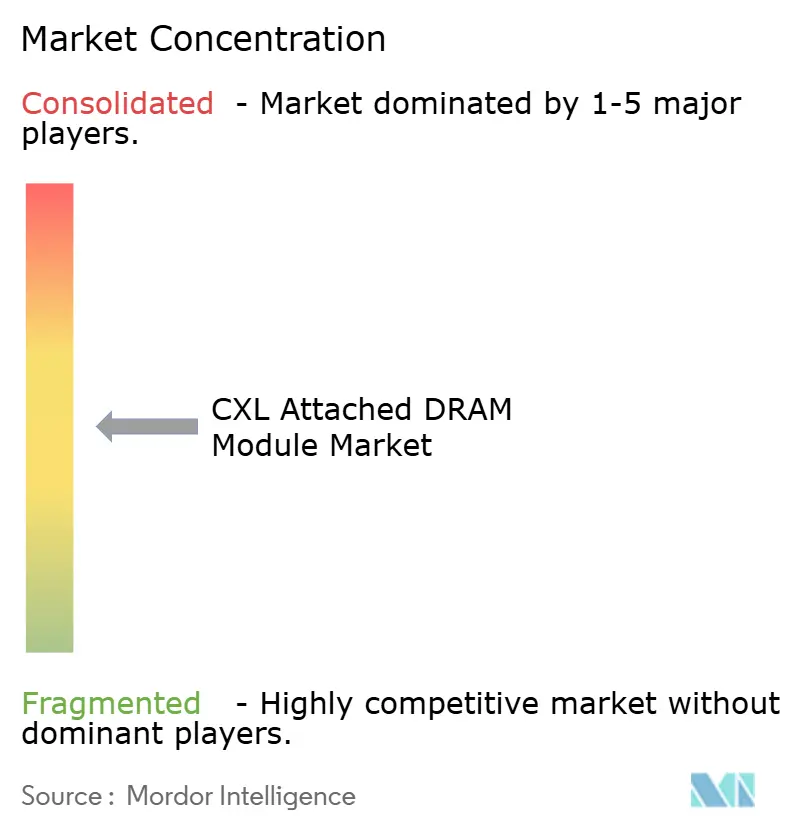

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CXL Attached DRAM Module Market Analysis by Mordor Intelligence

The CXL attached DRAM module market size is projected to be USD 1.27 billion in 2025, USD 1.59 billion in 2026, and reach USD 6.31 billion by 2031, growing at a CAGR of 31.74% from 2026 to 2031. This growth reflects a clear shift in data center memory design as AI training and inference workloads push servers beyond the limits of local DIMM capacity. Large language model deployments now require very large key-value cache buffers, which makes memory capacity a more immediate bottleneck than compute throughput in many production environments. CXL attached memory is gaining traction because it extends byte-addressable DRAM over PCIe while preserving hardware cache coherence at the CPU level, which makes it more practical than alternatives built around remote memory sharing or persistent tiers alone. Hyperscale operators and HPC environments are already moving from evaluation to live deployment, which is strengthening demand for modules, controllers, switches, and memory management software across the CXL attached DRAM module market. Higher latency than native DDR5 and the software effort needed for memory tiering still slow adoption in some enterprise settings, but they have not changed the long-term direction of the CXL attached DRAM module market.

Key Report Takeaways

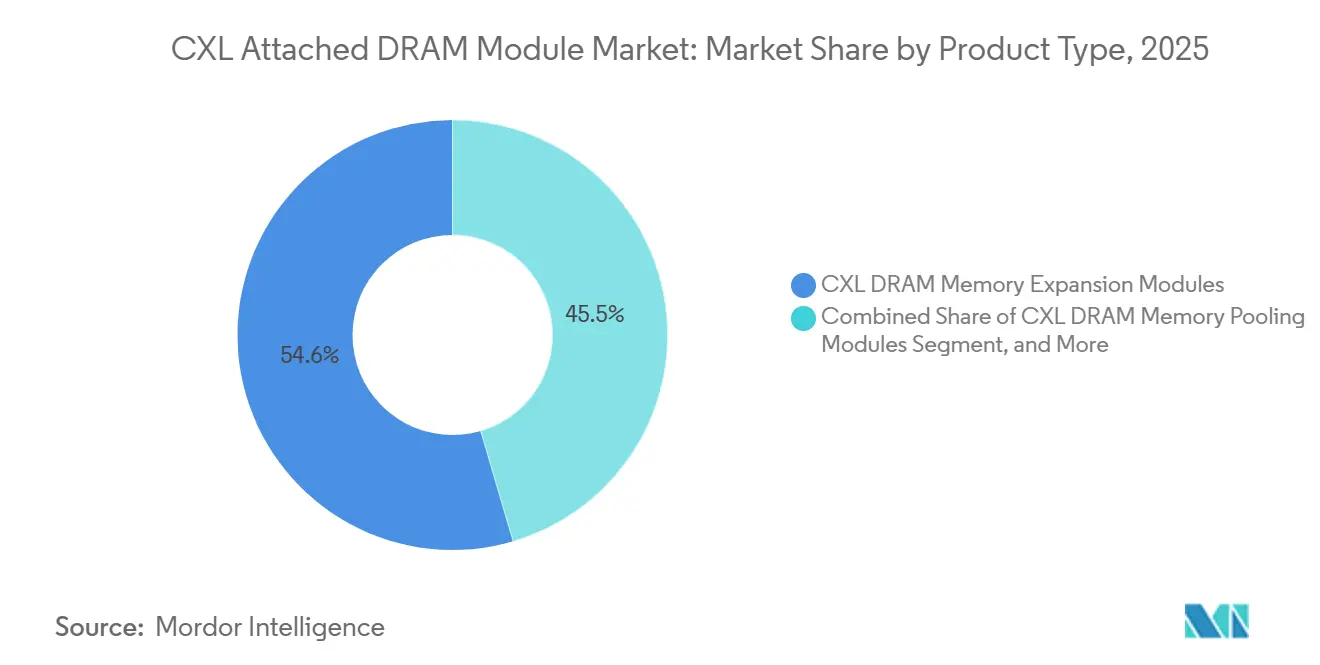

- By product type, CXL DRAM Memory Expansion Modules led with 54.55% share in 2025, while CXL DRAM Memory Pooling Modules are projected to expand at a 32.11% CAGR through 2031.

- By form factor, EDSFF-based CXL DRAM modules held 46.43% share in 2025, while Rack-Level CXL DRAM Expansion Systems are projected to grow at a 32.76% CAGR through 2031.

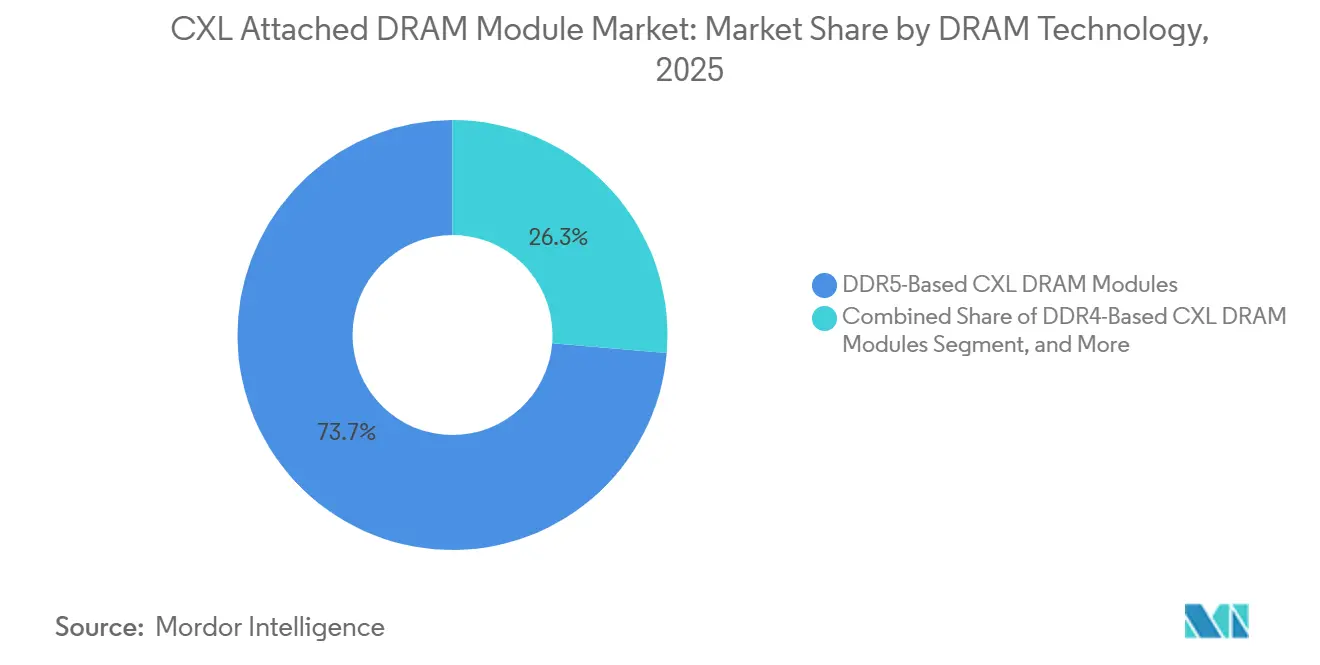

- By DRAM technology, DDR5-based CXL DRAM modules accounted for 73.67% share in 2025, while Advanced and Next-Generation DRAM-Based CXL Modules are forecast to expand at a 32.45% CAGR through 2031.

- By capacity class, the 256 GB-512 GB segment captured 41.44% share in 2025, while Above 1 TB modules are projected to advance at a 32.56% CAGR through 2031.

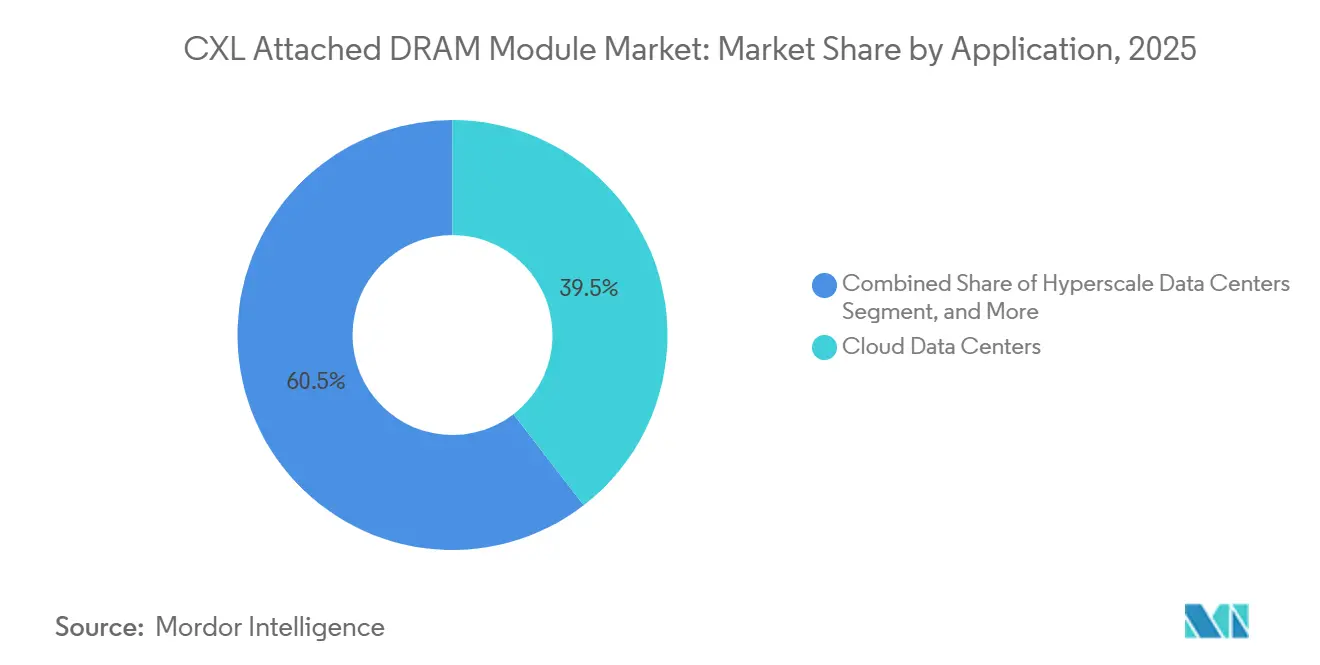

- By application, cloud data centers held 39.54% share in 2025, while AI infrastructure is projected to expand at a 32.34% CAGR through 2031.

- By geography, Asia-Pacific held 43.44% share in 2025, while North America is projected to grow at a 32.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CXL Attached DRAM Module Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging AI Infrastructure Memory Density Requirements | +9.5% | Global, early concentration in North America and East Asia, including South Korea, Japan, and Taiwan | Short term (≤ 2 years) |

| Hyperscale Memory Pooling To Reduce Stranded Capacity | +7.8% | Global, highest impact in North America, China, and South Korea | Medium term (2-4 years) |

| Standardization Around CXL 2.0, CXL 3.0, and CXL 3.1 Ecosystem Readiness | +5.2% | Global, strongest pull in regions with advanced server OEM ecosystems, including North America and Asia-Pacific | Medium term (2-4 years) |

| Rack-Scale Composability For Cloud and Enterprise Server Modernization | +4.1% | North America and Europe, with emerging uptake in Asia-Pacific | Medium term (2-4 years) |

| Accelerating HPC and Scientific Computing Memory Expansion Needs | +2.8% | North America and Europe core, with early gains in Japan and South Korea | Long term (≥ 4 years) |

| Rising Demand for In-Memory Databases and Memory-Intensive Virtualization | +1.9% | Global, with early deployment concentration in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging AI Infrastructure Memory Density Requirements

AI training and inference workloads are exposing a direct gap between GPU scale and per-node DRAM availability, which is creating sustained demand in the CXL attached DRAM module market. Long-context large language model inference requires key-value cache capacity that rises with context length, so memory capacity is becoming the operational limit in many production AI clusters. Astera Labs showed at GTC 2026 that Leo-based CXL deployments delivered 3.6x memory expansion and improved GPU utilization by keeping key-value cache on DDR5 instead of using only high-bandwidth memory.[1]Astera Labs, “Inference Tokenomics, How CXL Memory Expansion Improves AI Economics,” Astera Labs, asteralabs.com Alibaba Cloud’s Beluga architecture also showed that routing GPU key-value cache access to CXL-pooled memory through a switch fabric improved response behavior versus RDMA-based pooling. That matters because operators can support larger models and more persistent sessions without redesigning the full compute stack. It also supports higher multi-model concurrency, which improves utilization and strengthens near-term demand across the CXL attached DRAM module market.

Hyperscale Memory Pooling to Reduce Stranded Capacity

Static memory allocation at the server level still leaves a meaningful share of installed DRAM unused, and that is making pooling more attractive in the CXL attached DRAM module market. A rack-scale shared memory fabric lets operators assign capacity where it is needed in real time instead of sizing every node for peak demand. Microsoft Research showed through its Octopus work that sparse CXL topologies can scale pooling pods without requiring expensive full-mesh switch designs.[2]Microsoft Research, “Octopus, Enhancing CXL Memory Pods via Sparse Topology,” Microsoft Research, microsoft.com That architecture lowers deployment cost and improves the economic case for pooled memory at hyperscale. The case became stronger in 2025 and 2026 as tight DRAM supply and HBM-led allocation pressure pushed operators to extend the useful life of existing platforms. As production interest broadened beyond lab pilots, memory pooling moved closer to a standard infrastructure decision within the CXL attached DRAM module market.

Standardization Around CXL 2.0, CXL 3.0, And CXL 3.1 Ecosystem Readiness

The move from CXL 2.0 to CXL 3.1 expanded the addressable opportunity in the CXL attached DRAM module market from simple single-host expansion to multi-host memory pooling. The CXL 3.1 specification added DRAM-focused features such as memory maintenance, scrub control, error-threshold management, and capacity reduction reporting, which are important for enterprise qualification.[3]CXL Consortium, “Enabling CXL Memory Expansion Module with the CXL 3.1 Specification,” CXL Consortium, computeexpresslink.org JEDEC also published JESD405-1B in July 2024, which set label standards for CXL memory modules and reduced ambiguity around interoperability and qualification. Native support on AMD EPYC Turin and Intel 5th-generation Xeon platforms means the protocol now sits inside mainstream server roadmaps instead of remaining a niche add-on. That gives server OEMs and cloud buyers a clearer path to multi-vendor validation. It also reduces timing risk for broader deployment, which supports steady expansion in the CXL attached DRAM module market.

Rack-Scale Composability for Cloud and Enterprise Server Modernization

Rack-scale composability treats memory as an independent infrastructure resource, and that is changing how buyers view expansion in the CXL attached DRAM module market. This approach lets operators scale memory capacity without replacing the CPU platform, which extends asset life and limits refresh spending. Marvell’s Structera S 30260, announced in March 2026, supports 260 CXL lanes, up to 4 TB/s of aggregate bandwidth, and shared memory pools of up to 48 TB per rack. Panmnesia’s CXL 3.x composable server evaluation showed 1.8x better performance for plasma simulation workloads than a network-based reference system, which demonstrated a clear benefit for memory disaggregation in HPC settings. The same architecture is relevant to cloud environments that want to treat memory as a pool rather than as a fixed server part. Over time, that changes procurement behavior and supports recurring pool expansion across the CXL attached DRAM module market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Latency Versus Native DDR5 Memory | -4.2% | Global, with greatest friction in latency-sensitive enterprise applications in North America and Europe | Short term (≤ 2 years) |

| Software Orchestration and Tiering Complexity | -3.1% | Global, most acute in multi-tenant cloud and enterprise virtualization environments | Medium term (2-4 years) |

| Elevated Platform and Integration Cost for Early Deployments | -2.4% | Global, with concentration in regions where hyperscale infrastructure investment is nascent | Short term (≤ 2 years) |

| Ecosystem Qualification Delays Across CPU, Memory, Switch, and Software Stacks | -1.8% | Global, concentrated in North America and East Asia where OEM qualification cycles are most rigorous | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Latency Versus Native DDR5 Memory

CXL attached memory still introduces round-trip latency of 200-400 nanoseconds versus 75-85 nanoseconds for locally attached DDR5, and that remains a direct limit on some use cases in the CXL attached DRAM module market. Research presented at ASPLOS 2025 also found unfair queuing behavior and DDR bandwidth degradation of up to 81% under heavy concurrent loads. Microsoft Research showed that hardware-managed tiering in Flat Memory Mode held degradation within 5% for more than 82% of workloads, but some outlier cases still saw performance fall by up to 34%. That means service-level predictability matters as much as average latency in enterprise qualification. The current mitigation is to keep hot pages in local DDR5 and move colder pages to the CXL tier. That works for several database and AI inference patterns, but it requires application-level profiling and slows deployment across the CXL attached DRAM module market.

Software Orchestration and Tiering Complexity

The full cost and capacity benefit of CXL attached memory depends on operating system policies, hypervisor support, and orchestration tools, and that stack is still maturing across the CXL attached DRAM module market. Research presented at USENIX OSDI 2025 showed that Linux tiering policies can underperform even simple first-touch allocation when the bandwidth gap between fast and slow memory narrows. SK Hynix addressed part of this challenge through HMSDK and its Linux integration for CMM-DDR5 modules, which helps customers that already validated that specific hardware path. Even so, multi-tenant cloud environments still face contention and tail-latency issues when workloads compete for access to the slower memory tier. Samsung’s SCMC management layer shows that software-defined memory control is improving, but it still lacks the operating maturity seen in established CPU and storage tooling. As a result, software readiness continues to delay broad production rollouts in the CXL attached DRAM module market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Expansion Modules Anchor Deployments, Pooling Accelerates

CXL DRAM Memory Expansion Modules held 54.55% of the CXL attached DRAM module market in 2025, which made them the largest product category. Their lead came from a simple adoption path because they support single-host expansion, require no switch fabric, and fit existing PCIe 5.0 server infrastructure. That lower hardware complexity also gives server OEMs a more familiar qualification path. Interoperability work under the CXL Type 3 model and JEDEC labeling standards has further reduced adoption friction for this part of the CXL attached DRAM module market. The segment also benefits from a direct cost case because it lets buyers increase memory headroom without replacing the full server.

CXL DRAM Memory Pooling Modules are projected to grow at a 32.11% CAGR through 2031, which makes them the fastest-growing product type in the CXL attached DRAM module market. Their appeal is shifting buyer attention from one-server capacity expansion to shared memory fabrics that serve multiple compute nodes. Samsung demonstrated this direction through the CMM-B pooling appliance, which delivered up to 2 TB of shared CXL capacity at up to 60 GB/s bandwidth for AI, in-memory database, and analytics use cases. Add-in card products still matter as a bridge for legacy platforms, while controller-based modules and expansion appliances are likely to gain share as integration improves and buyers seek centrally managed memory pools across the broader CXL attached DRAM module industry.

By Form Factor: EDSFF Leads as Rack-Level Systems Drive Growth

EDSFF-based CXL DRAM modules captured 46.43% of the CXL attached DRAM module market size in 2025, which made EDSFF the leading form factor. Their lead reflects strong fit with standard server drive bays, especially E3.S and E3.L layouts that avoid major chassis redesign. Hot-plug serviceability also matters because operators want to manage live data center environments without full system shutdowns. The E3.S 2T format adds support for dual-port connectivity, which supports failover and higher-availability configurations in production systems. Micron’s CZ120 and SK Hynix’s CMM-DDR5 are current product examples that validate this form factor in commercial deployments.

Rack-Level CXL DRAM Expansion Systems are projected to grow at a 32.76% CAGR through 2031, giving them the fastest growth profile in the CXL attached DRAM module market. Buyers are increasingly looking at centralized memory appliances that can serve many compute nodes from one rack-scale pool. PCIe add-in card modules remain useful for older installed systems, but they are likely to lose relative weight as EDSFF-ready platforms become standard in new procurement cycles. The CMM-D format is also gaining ground because it combines DRAM chips and a dedicated CXL controller on one board, which supports cleaner deployment paths for large-scale hyperscale programs in the CXL attached DRAM module industry.

By DRAM Technology: DDR5 Dominates Today, Advanced Platforms Define Tomorrow

DDR5-based CXL DRAM modules held 73.67% of the CXL attached DRAM module market in 2025, which made DDR5 the dominant memory technology. This lead reflects the server platform transition already underway on AMD EPYC Turin and Intel 5th-generation Xeon systems. DDR5 also fits the throughput needs of AI inference, in-memory analytics, and mixed read-write environments better than DDR4. SK Hynix’s validated 96 GB CMM-DDR5 reached 36 GB/s throughput, with a 30% bandwidth improvement and a 50% capacity increase over standard DDR5 modules in server configurations. That product-level benchmark gives OEMs a clearer basis for current generation qualification in the CXL attached DRAM module market.

Advanced and Next-Generation DRAM-Based CXL Modules are projected to grow at a 32.45% CAGR through 2031, which gives this category the strongest expansion pace inside the technology split. This group includes higher-generation DDR5 process nodes and hybrid approaches that move beyond simple all-DRAM capacity extension. The direction matters because buyers are starting to value bandwidth-per-watt and workload-specific optimization as much as raw capacity. DDR4-based CXL modules will still serve retrofit demand on older systems, but their role should narrow as new builds center on DDR5 and newer architectures across the CXL attached DRAM module market.

By Capacity Class: Mid-Range Density Anchors Current Deployments, Ultra-High Capacity Leads Growth

The 256 GB-512 GB capacity class held 41.44% of the CXL attached DRAM module market size in 2025, which made it the largest density band. That position reflects a practical balance between module cost, platform compatibility, and immediate workload fit. This class is large enough to extend servers supporting in-memory databases, dense virtualization, and multi-model inference without creating the design and bandwidth burden of the highest-capacity builds. The up to 256 GB range remains the commercial entry point for buyers running early qualification or lower-scale deployments. At the same time, the 512 GB-1 TB class already serves higher-end AI and HPC nodes that need more local memory headroom, with Micron’s CZ120 standing out as a commercial example on Supermicro Petascale X13 and H13 platforms.

Above 1 TB modules are projected to grow at a 32.56% CAGR through 2031, which makes them the fastest-growing capacity class in the CXL attached DRAM module market. Growth here is tied to inference clusters serving very large models, where key-value cache depth can create absolute memory requirements that smaller modules cannot meet efficiently. The category also benefits from the rise of pooled appliances that aggregate multiple modules into multi-terabyte memory pools for shared use. As model sizes and persistent context needs keep rising, ultra-high-capacity modules will become more central to procurement decisions across the CXL attached DRAM module market.

By Application: Cloud Data Centers Lead, AI Infrastructure Defines the Growth Vector

Cloud data centers held 39.54% of the CXL attached DRAM module market in 2025, which made them the leading application area. Their lead came from the need to raise per-node memory capacity for analytics, key-value cache offload, and memory-heavy service workloads without waiting for complete server replacement cycles. Astera Labs’ Azure M-series deployment preview fits this demand profile because each Leo controller supports over 1.5x memory scale-up and up to 2 TB of DDR5-5600 RDIMM-based CXL memory capacity per controller. That production reference is important because it shows that CXL expansion is no longer limited to lab validation. It also creates a stronger buying signal for memory modules, controllers, and orchestration software across the CXL attached DRAM module market.

AI infrastructure is projected to grow at a 32.34% CAGR through 2031, making it the fastest-growing application in the CXL attached DRAM module market. Demand is being driven by generative AI deployment, agentic AI workloads with uneven memory footprints, and the commercial need to shift key-value cache away from expensive GPU memory. HPC also remains a meaningful growth lane, with Panmnesia’s composable CXL server and PNNL’s Crete testbed showing how shared memory designs can support scientific AI and simulation workloads at larger scale. Enterprise servers still matter, but their pace is slower because buyers need stronger proof on qualification timelines, workload fit, and total cost outcomes before expanding within the CXL attached DRAM module market.

Geography Analysis

Asia-Pacific held 43.44% of the CXL attached DRAM module market share in 2025, which made it the largest regional segment. The region combines supply strength in DRAM manufacturing with growing demand from AI infrastructure buildouts. South Korea remains central because Samsung Electronics and SK Hynix supply the DDR5 memory used across a large share of commercial CXL module programs, and both companies continue to advance dedicated CXL product lines. Taiwan also matters because controller silicon is becoming a key differentiator as the market moves from simple expansion to pooled architectures. Montage Technology’s sampling of its CXL 3.1 Memory eXpander Controller in September 2025 showed that controller readiness in Asia-Pacific is advancing alongside module demand.

North America is projected to grow at a 32.73% CAGR, which gives it the fastest regional trajectory in the CXL attached DRAM module market. The region benefits from the presence of the largest hyperscale cloud operators, which are the first buyers able to absorb new memory architectures at scale. Astera Labs’ production deployment on Microsoft Azure M-series virtual machines is a strong reference point because it moved CXL memory expansion into a public cloud production setting. PNNL’s Crete testbed broadens demand beyond commercial cloud by showing how scientific AI systems can use Micron memory and custom CXL controller boards in high-memory computing environments. The region is also supported by strong standards involvement from Intel and AMD and by local switch and controller suppliers such as Marvell and Astera Labs, which helps the CXL attached DRAM module market move faster from validation into production.

Europe held the third-largest position in the CXL attached DRAM module market, with demand tied to hyperscale expansion in Ireland, the Netherlands, and Germany and to HPC procurement at national supercomputing centers. The region’s focus on power efficiency and total cost control fits well with the logic of memory pooling because shared fabrics can reduce redundant DRAM provisioning across fleets. That makes Europe a good long-term fit for composable rack architectures as qualification barriers fall. Rest of the World remains an earlier-stage opportunity in the CXL attached DRAM module market, but sovereign AI buildouts in the Gulf are creating a credible near-term path for high-capacity memory deployments.

Competitive Landscape

The CXL attached DRAM module market is moderately concentrated in memory media but more fragmented across controllers, switches, software, and systems. Samsung Electronics, SK Hynix, and Micron Technology remain central because they supply the DDR5 foundation that underpins most commercial module designs. Samsung stands out for vertical integration because it pairs DRAM supply with dedicated CXL memory hardware and its SCMC management layer, which gives it control across both device and orchestration functions. SK Hynix strengthened its position in 2025 by completing customer validation of its 96 GB CMM-DDR5 and by pairing hardware with HMSDK software support. Micron remains important through the commercial shipment of the CZ120 module on Supermicro platforms, which tied its memory roadmap to real HPC and AI server deployments.

The controller and switch layer is more open, and that is where design wins may reshape the CXL attached DRAM module market over the next few years. Astera Labs has an early lead in production visibility because Leo controllers are already deployed in Microsoft Azure M-series virtual machines for memory-heavy cloud workloads. Marvell is pushing a broader infrastructure play through Structera, with a switch roadmap built around large memory pools, high lane counts, and support for heterogeneous compute fabrics. Montage Technology is also becoming more relevant as controller sampling progresses and buyers seek alternatives that support newer CXL memory expansion architectures.

White space remains most visible in software-defined memory management and end-to-end qualification tooling for multi-vendor deployments in the CXL attached DRAM module market. That gap matters because hardware availability alone does not guarantee stable operation across virtualized cloud and enterprise environments. Standards work also remains a useful signal because companies that shape DRAM-focused CXL definitions often move earlier in commercial validation cycles. The result is a market where memory suppliers still carry structural weight, but controller, switch, and software specialists have room to gain share as production architectures become more complex.

CXL Attached DRAM Module Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

Intel Corporation

Astera Labs, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SMART Modular Technologies, a Penguin Solutions brand, completed one year of sampling its Non-Volatile CXL E3.S Memory Module, NV-CMM, to Tier 1 OEMs, combining non-volatile high-performance DRAM, persistent flash memory, and an energy source in a single EDSFF E3.S 2T form factor, supporting checkpointing, snapshotting, and low-latency write cache for data center applications via PCIe Gen 5 and CXL 2.0.

- March 2026: Marvell Technology announces the Structera S 30260 CXL 3.0 switch at OFC 2026 in Los Angeles, featuring 260 lanes, up to 4 TB/s aggregate bandwidth, and shared memory pool capacity of up to 48 TB per rack; customer sampling is targeted for Q3 2026, extending Marvell's position as the only CXL vendor with a portfolio spanning memory expansion, near-memory acceleration, and pooling.

- November 2025: Astera Labs announces that its Leo CXL Smart Memory Controllers are deployed on Microsoft Azure M-series virtual machines in the cloud industry's first publicly disclosed production deployment of CXL memory expansion, enabling server memory to scale by over 1.5x per controller with up to 2 TB of DDR5-5600 RDIMM-based CXL memory capacity per controller for in-memory databases, AI inference, and LLM KV cache applications.

- September 2025: Montage Technology introduces the CXL 3.1 Memory eXpander Controller, MXC, Part No. M88MX6852, in sampling phase to key customers including SK Hynix, supporting both CXL.mem and CXL.io protocols; AMD's corporate vice president for data center ecosystems describes the product as aligned with AMD's long-term vision for memory tiering and AI workload expansion.

Global CXL Attached DRAM Module Market Report Scope

The Global CXL Attached DRAM Module Market refers to the emerging industry segment centered on the development and deployment of Dynamic Random-Access Memory (DRAM) modules that leverage Compute Express Link (CXL) technology to provide high-bandwidth, low-latency memory expansion and pooling capabilities for advanced computing systems.

The CXL Attached DRAM Module Market Report is Segmented by Product Type (CXL DRAM Memory Expansion Modules, CXL DRAM Memory Pooling Modules, CXL DRAM Add-in Cards, CXL DRAM Expansion Appliances / Systems, and CXL DRAM Controller-Based Memory Modules), Form Factor (EDSFF-Based CXL DRAM Modules, PCIe Add-in Card CXL DRAM Modules, CXL Memory Module - DRAM / CMM-D Type Modules, and Rack-Level CXL DRAM Expansion Systems), DRAM Technology (DDR5-Based CXL DRAM Modules, DDR4-Based CXL DRAM Modules, and Advanced / Next-Generation DRAM-Based CXL Modules), Capacity (Up to 256 GB, 256 GB-512 GB, 512 GB-1 TB, and Above 1 TB), Application (AI Infrastructure, Cloud Data Centers, Hyperscale Data Centers, High-Performance Computing, Enterprise Servers, and Other Applications (In-Memory Databases and Analytics, Memory-Intensive Virtualization Workloads)), and Geography (North America, Europe, Asia Pacific, Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

| CXL DRAM Memory Expansion Modules |

| CXL DRAM Memory Pooling Modules |

| CXL DRAM Add-in Cards |

| CXL DRAM Expansion Appliances / Systems |

| CXL DRAM Controller-Based Memory Modules |

| EDSFF-Based CXL DRAM Modules |

| PCIe Add-in Card CXL DRAM Modules |

| CXL Memory Module - DRAM / CMM-D Type Modules |

| Rack-Level CXL DRAM Expansion Systems |

| DDR5-Based CXL DRAM Modules |

| DDR4-Based CXL DRAM Modules |

| Advanced / Next-Generation DRAM-Based CXL Modules |

| Up to 256 GB |

| 256 GB-512 GB |

| 512 GB-1 TB |

| Above 1 TB |

| AI Infrastructure |

| Cloud Data Centers |

| Hyperscale Data Centers |

| High-Performance Computing |

| Enterprise Servers |

| Other Applications, In-Memory Databases and Analytics, Memory-Intensive Virtualization Workloads |

| North America | |

| Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia Pacific | |

| Rest of the World |

| By Product Type | CXL DRAM Memory Expansion Modules | |

| CXL DRAM Memory Pooling Modules | ||

| CXL DRAM Add-in Cards | ||

| CXL DRAM Expansion Appliances / Systems | ||

| CXL DRAM Controller-Based Memory Modules | ||

| By Form Factor | EDSFF-Based CXL DRAM Modules | |

| PCIe Add-in Card CXL DRAM Modules | ||

| CXL Memory Module - DRAM / CMM-D Type Modules | ||

| Rack-Level CXL DRAM Expansion Systems | ||

| By DRAM Technology | DDR5-Based CXL DRAM Modules | |

| DDR4-Based CXL DRAM Modules | ||

| Advanced / Next-Generation DRAM-Based CXL Modules | ||

| By Capacity Class | Up to 256 GB | |

| 256 GB-512 GB | ||

| 512 GB-1 TB | ||

| Above 1 TB | ||

| By Application | AI Infrastructure | |

| Cloud Data Centers | ||

| Hyperscale Data Centers | ||

| High-Performance Computing | ||

| Enterprise Servers | ||

| Other Applications, In-Memory Databases and Analytics, Memory-Intensive Virtualization Workloads | ||

| By Geography | North America | |

| Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the size of the CXL attached DRAM module market in 2026?

The CXL attached DRAM module market size stands at USD 1.59 billion in 2026 and is forecast to reach USD 6.31 billion by 2031 at a 31.74% CAGR.

Which product type leads current demand for CXL attached DRAM modules?

CXL DRAM Memory Expansion Modules lead current demand with a 54.55% share in 2025 because they offer the simplest entry path and work with existing PCIe 5.0 server infrastructure.

Which form factor is growing the fastest in CXL memory deployments?

Rack-Level CXL DRAM Expansion Systems are growing the fastest at a 32.76% CAGR through 2031 as operators move toward centralized memory appliances and shared rack-scale pools.

Why are cloud operators adopting CXL attached DRAM modules?

Cloud operators use them to expand memory for in-memory databases, analytics, and AI inference without waiting for full server replacement, and cloud data centers held 39.54% of demand in 2025.

What is the main challenge slowing enterprise adoption of CXL attached memory?

The main challenge is the mix of higher latency than native DDR5 and the software complexity of memory tiering, especially in virtualized and multi-tenant environments.

Which region is expanding the fastest for CXL attached DRAM modules?

North America is the fastest-growing region with a 32.73% CAGR through 2031 because hyperscale cloud providers there are moving from qualification into production deployments.

Page last updated on: