High-Purity Methane Gas Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.52 Billion |

| Market Size (2031) | USD 10.89 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

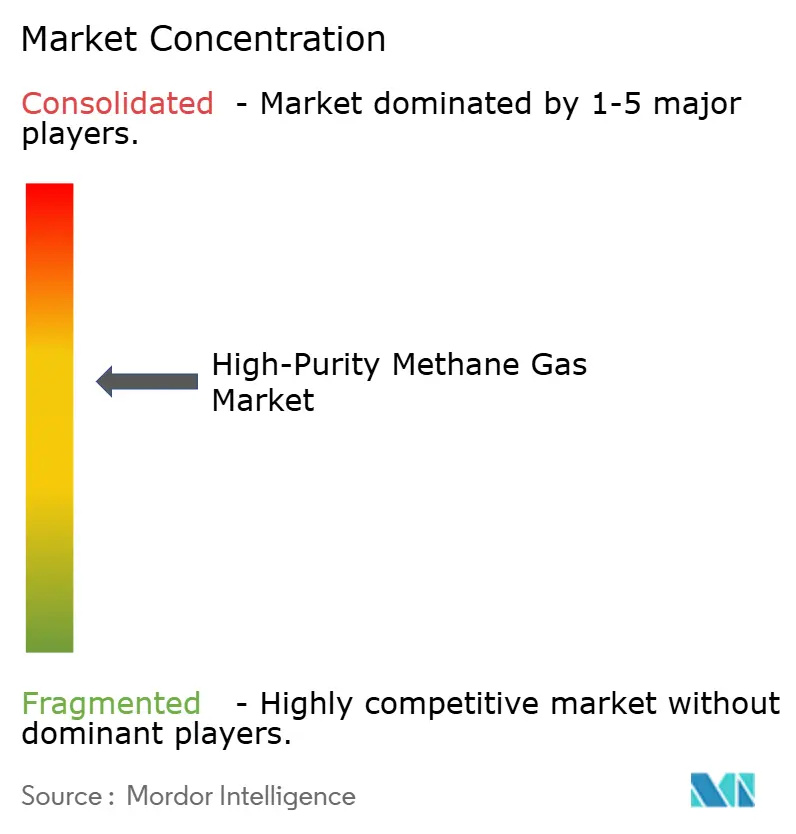

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-Purity Methane Gas Market Analysis by Mordor Intelligence

The High-Purity Methane Gas Market size was valued at USD 8.11 billion in 2025 and is estimated to grow from USD 8.52 billion in 2026 to reach USD 10.89 billion by 2031, at a CAGR of 5.03% during the forecast period (2026-2031). The demand for high-purity methane is being buoyed by a mix of factors: heightened semiconductor capital expenditures, mandates for renewable gases, and increased investments in specialty chemicals. While natural-gas purification remains the cost leader, there's a notable surge in biomethane upgrading. This uptick is largely driven by incentives in Europe and the Asia-Pacific for the grid-injection of renewable gases. The momentum in applications is firmly rooted in front-end wafer fabrication. Here, the stringent sub-10-parts-per-billion impurity limits necessitate on-site purification skids. Additionally, petrochemical complexes are retrofitting their steam-methane reformers with carbon-capture loops, tightening their feed-gas specifications. As industrial-gas giants integrate purification trains within mega-fabs, supply contracts are extending to 10-20 years. Meanwhile, niche suppliers are capitalizing on isotopic enrichment for quantum-computing labs, with carbon-12 methane fetching a premium of USD 5,000-15,000 per kg.

Key Report Takeaways

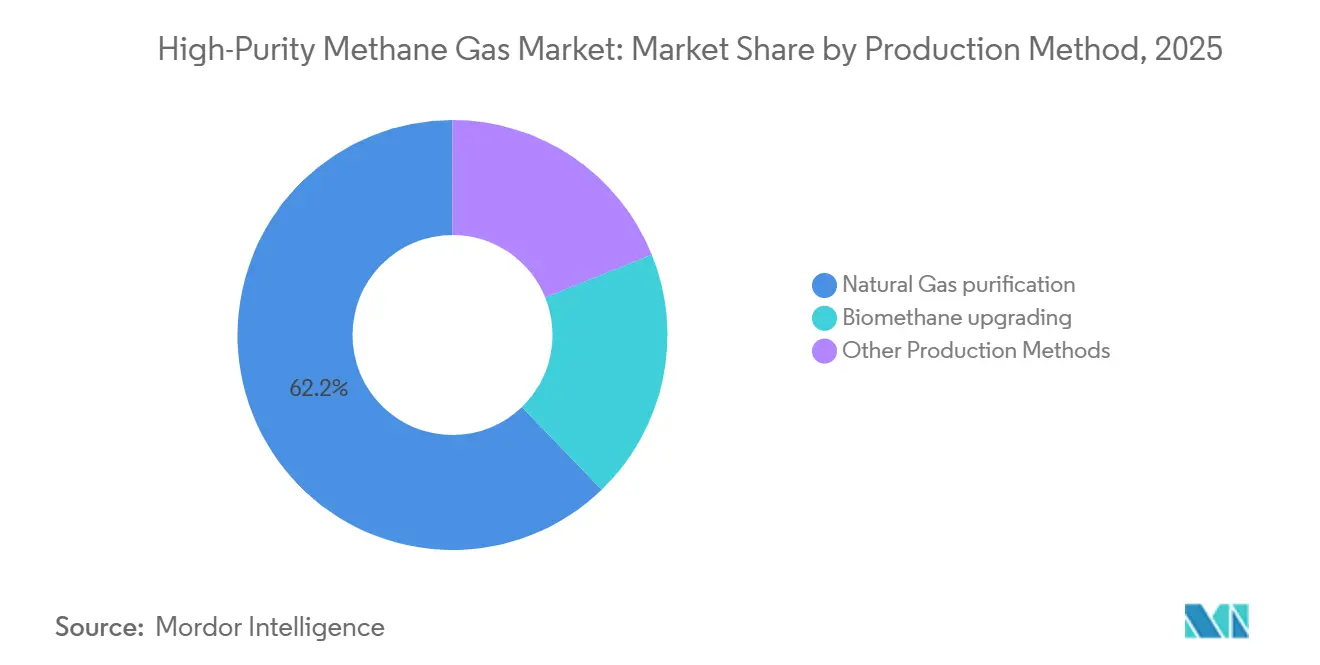

- By production method, natural-gas purification held 62.21% of the High-Purity Methane Gas market share in 2025, while biomethane upgrading is advancing at a 5.68% CAGR from 2026 to 2031.

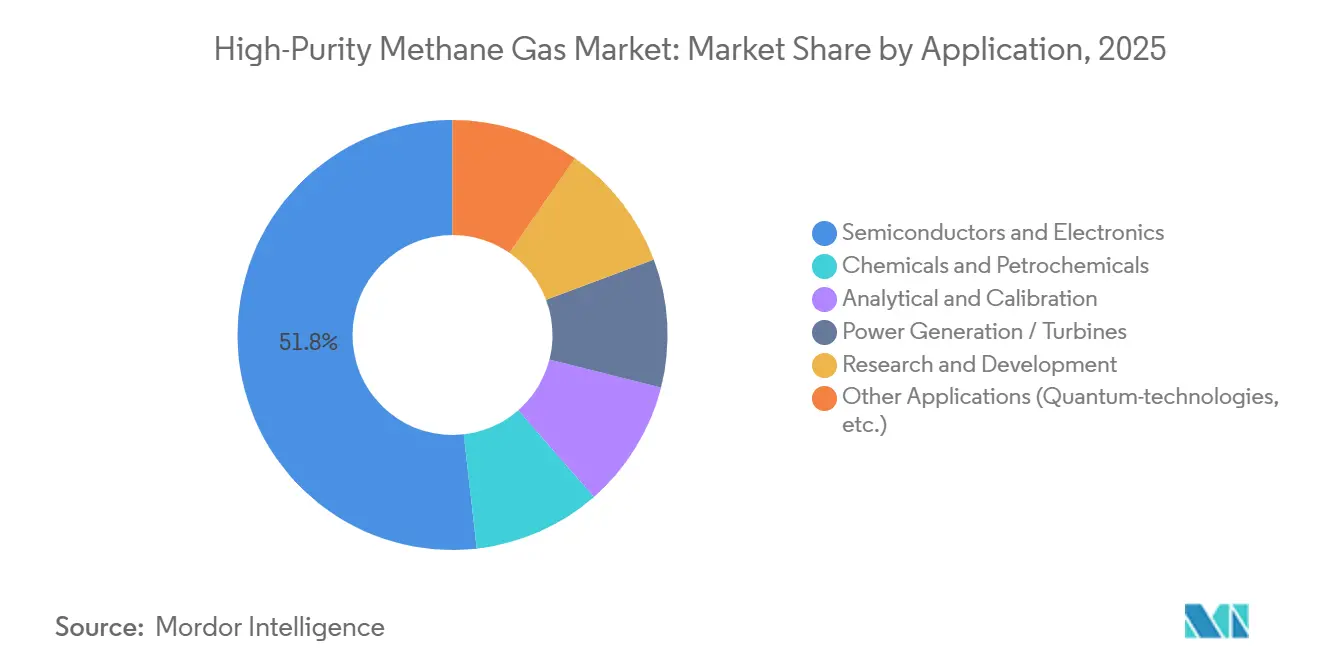

- By application, semiconductors and electronics led with 51.78% revenue share in 2025; chemicals and petrochemicals are projected to expand at a 5.91% CAGR from 2026 to 2031.

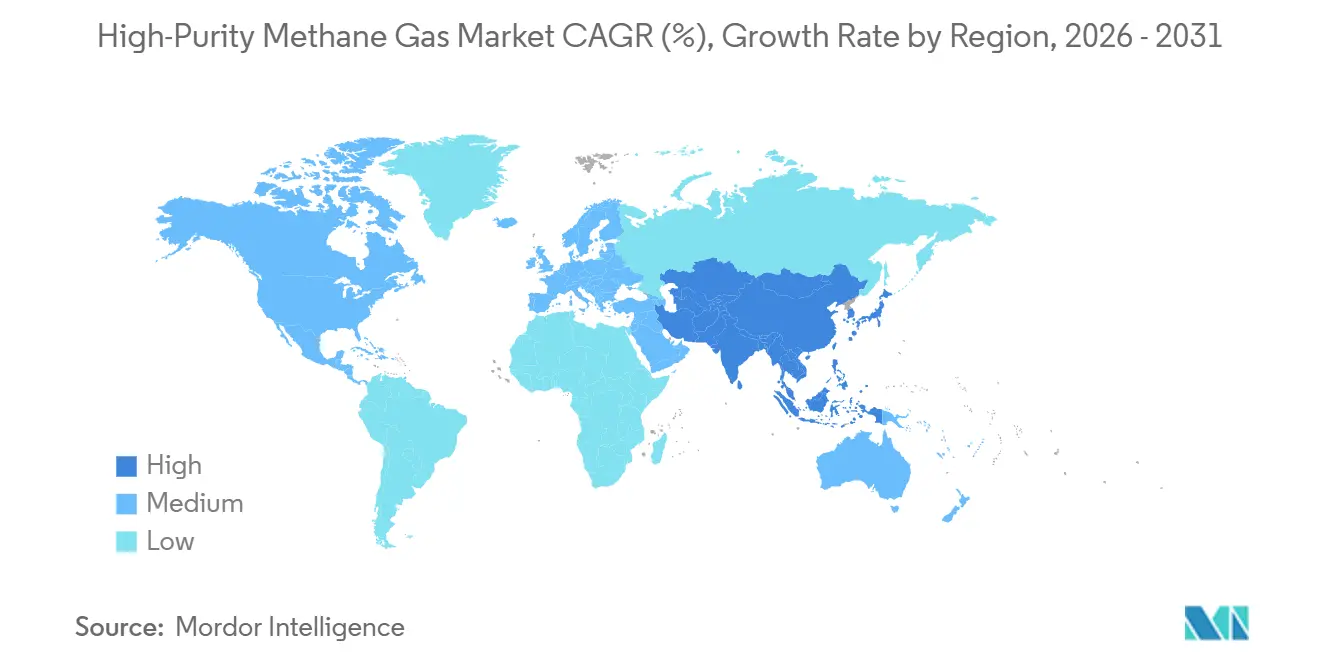

- By geography, Asia-Pacific accounted for 43.11% of the High-Purity Methane Gas market size in 2025 and is forecast to grow at a 5.78% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High-Purity Methane Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Fab Capacity Additions | +1.8% | Global, concentrated in Asia-Pacific (China, South Korea, Taiwan, India), North America (Arizona, Texas, Ohio), Europe (Germany, Ireland) | Medium term (2-4 years) |

| Growth in Specialty-Chemical Synthesis Demand | +1.2% | Global, with spill-over from Asia-Pacific petrochemical hubs (China, India, ASEAN) to Middle East (Saudi Arabia, UAE) | Medium term (2-4 years) |

| Clean-Energy and Hydrogen-Economy Expansion | +1.0% | Europe (Germany, Netherlands, UK), North America (California, Texas), Asia-Pacific (Japan, South Korea, Australia) | Long term (≥ 4 years) |

| Uptake of Ultra High Purity Gases in Analytical Instrumentation | +0.6% | Global, early gains in North America, Europe, and developed Asia-Pacific markets (Japan, Singapore) | Short term (≤ 2 years) |

| Growing Requirement of Quantum Grade Methane for Diamond-CVD Qubits | +0.4% | National, with early gains in United States (Boston, Silicon Valley), South Korea (Seoul), Germany (Munich) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Fab Capacity Additions

In 2025, global wafer fabrication investments reached USD 160 billion. New 300 mm lines require precise conditions, specifying methane with oxygen and moisture levels below 10 ppb for silicon-carbide epitaxy. Air Liquide allocated over USD 250 million to establish on-site units in Arizona, Singapore, and Dresden. These units, achieving 99.9995% methane purity, incorporate cryogenic, PSA, and catalytic polishing steps. In Nevada, Taiyo Nippon Sanso and Nikkiso are collaborating on a cryogenic air-separation plant. This facility is designed to support advanced packaging needs, providing a cylinder backup for process-control gases. In 2025, Central Glass and Foosung launched a KRW 4 billion project in South Korea to localize electronic specialty gases. As export controls become stricter, prompting chipmakers to focus on regionalization, the High-Purity Methane Gas market is expected to align purification processes with the needs of each emerging fab cluster.

Growth in Specialty-Chemical Synthesis Demand

Methane, a key component in the production of methanol and an indirect hydrogen vector for ammonia, is increasingly significant as decarbonization targets drive the need for cleaner molecules to protect precious metal catalysts. PetroChina's Dalian complex has installed PSA units, each rated at 120,000 Nm³ h⁻¹, to recycle purge gases. This has created in-house demand for calibration-grade methane, which ensures emissions-monitor accuracy. Similarly, Sinopec's Tahe cracker, with a budget of RMB 29.987 billion, incorporates hydrogen recovery loops with a capacity of 80,000 Nm³ h⁻¹, relying on 99.995% pure methane as a calibration standard. Additionally, Asahi Kasei, Mitsui, and Mitsubishi formed a JPY 21.2 billion alliance in 2026 to electrify ethylene production[1]Asahi Kasei Corporation, “Joint Venture for Ethylene Decarbonization,” asahi-kasei.com. This initiative is expected to use ultra-pure methane in pilot-scale batches for catalyst screening. These developments highlight methane's evolving role from a commodity to a precision reagent, driven by its critical applications in the High-Purity Methane Gas market.

Clean-Energy and Hydrogen-Economy Expansion

Biomethane upgrading plants utilize membrane cascades and cryogenic CO₂ removal to achieve purities of 98-99.5%. They then further refine these streams to reach 99.995% purity, especially when supplying semiconductor or laboratory networks. Plasma-catalytic methanation pilots, using nickel catalysts, achieve over 95% methane yield. This positions power-to-methane loops as suppliers of both energy and specialty gases. BASF is exploring methane pyrolysis for turquoise hydrogen. This method not only produces solid carbon coproducts and sidesteps CO₂ emissions but also demands ultra-clean feed gas to prolong catalyst life. Osaka Gas India is testing e-methane blending in 10% of its network. This initiative sets the stage for local purification hubs, potentially servicing electronics clusters near Dholera. As the hydrogen economy evolves, these developments promise sustained volume growth for the High-Purity Methane Gas market.

Uptake of Ultra-High-Purity Gases in Analytical Instrumentation

As air-quality standards become stricter and refinery emissions face tighter caps, the demand for traceable methane calibration mixtures is increasing. These mixtures ensure a total hydrocarbon uncertainty of under 1 ppm. In response to new EPA and EU directives mandating quarterly analyzer verification, environmental labs across the U.S. and Europe have increased their procurement of 5.0 and 6.0-grade methane, doubling their purchases since 2024. Instrument OEMs are incorporating built-in purge routines, rejecting gas with moisture levels exceeding 10 ppb. This change is driving suppliers to improve their cylinder-filling lines with dew-point sensors. To maintain regulatory compliance and prevent contamination events, companies like Air Liquide and Linde are using digital cylinder-tracking. This technology certifies both the shelf life and chain of custody of the gas. Additionally, the ongoing miniaturization of sensors in portable gas analyzers is expanding the customer base, contributing to steady growth in the High-Purity Methane Gas market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Purification and Isolation Cost | -0.9% | Global, acute in emerging markets (India, Southeast Asia, Latin America) with limited local purification infrastructure | Medium term (2-4 years) |

| Complex Storage and Transport Safety Norms | -0.6% | Global, with regional variations (ISO/IEC in Europe, PHMSA in North America, national standards in Asia-Pacific) | Short term (≤ 2 years) |

| Scarce Supply of Isotopically-Enriched Methane | -0.3% | National, concentrated in United States, Germany, South Korea, Japan with isotope-separation capabilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Purification and Isolation Cost

Staged PSA, cryogenic, and catalytic polishing trains can increase costs by USD 0.50-1.20 per kg to achieve 99.995% purity. While membrane alternatives present an option for lower capex, they encounter challenges such as selectivity trade-offs between CO₂ and CH₄ and fouling issues when processing raw biogas. Laser isotope separation, requiring 97 eV per atom and advanced optics, contrasts with cryogenic distillation cascades, which consume over 10 MWh per kg to reach 99.9% purity in carbon-12 methane. In India and Southeast Asia, independents often import pre-purified cylinders, incurring freight premiums that reduce their margins. Establishing a greenfield high-purity plant involves an investment of USD 20-50 million, and with payback periods exceeding five years, the still-developing semiconductor demand creates barriers for new entrants, limiting growth in segments of the High-Purity Methane Gas market.

Complex Storage and Transport Safety Norms

ISO 11118:2025 and ISO 11114-1:2020 require periodic hydrostatic testing and material-compatibility assessments, adding costs of USD 50-150 per cylinder cycle[2] ISO, “ISO 11118:2025 Gas Cylinders—Non-refillable Gas Cylinders,” iso.org. Although PHMSA's 2024 harmonization has simplified interstate movement in the U.S., ASEAN members continue to enforce varied import permits, increasing cross-border shipment times. Semiconductor fabs, which comply with AIGA and EIGA leak-tight standards, experience installation costs that are 15-25% higher than standard gas lines. The export of isotopically enriched methane is subject to dual-use licensing requirements, causing delays of four to eight weeks and necessitating specialized documentation. These regulatory requirements provide an advantage to larger, vertically integrated multinationals, while limiting the ability of smaller suppliers to enter the market, thereby constraining the near-term growth of the High-Purity Methane Gas market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Method: Biomethane Upgrading Gains Momentum Despite Natural-Gas Dominance

In 2025, natural-gas purification accounted for 62.21% of the High-Purity Methane Gas market share, supported by more than 580 operational Linde plants globally, utilizing established cryogenic and PSA infrastructure. The market for natural-gas purification in High-Purity Methane Gas is expected to grow at a 5.12% CAGR from 2026 to 2031, driven by on-site systems supplying mega-fabs in Arizona, Dresden, and Hsinchu. Biomethane upgrading, which currently represents a smaller segment, is projected to grow at a 5.68% CAGR through 2031. This growth is attributed to Renewable Energy Directive quotas in Europe and feed-in-tariff incentives in China and India. Membrane cascades combined with low-temperature polishing achieve 99.995% purity, enabling upgraded gas to cater to semiconductor clients that previously relied on fossil pipelines. Investment decisions are influenced by carbon-credit premiums and proximity to agricultural feedstock, shifting project pipelines toward the Midwest U.S., Northern France, and coastal China. Although synthetic power-to-methane represents less than 5% of the market, increased renewable-electricity adoption could drive its growth in the latter half of the decade, potentially impacting the cost structure of the High-Purity Methane Gas market.

Natural-gas purification remains a preferred option in regions with strong pipeline networks. For example, integrated petrochemical hubs in Texas, Jiangsu, and the Gulf Cooperation Council can integrate specialty-gas skids into existing fractionation columns with minimal additional capital expenditure. In contrast, biogas facilities in Europe's agricultural clusters utilize local feedstock and carbon pricing to offer competitive pricing on high-purity molecules for laboratory and analytical applications. Synthetic methods, such as plasma-catalytic CO₂ methanation, are advancing in technology readiness levels (TRL) as electrolyzer prices decline, providing a potential alternative to address fossil supply challenges. From 2026 to 2031, diversifying portfolios is expected to be a key strategy for suppliers aiming for balanced exposure across the High-Purity Methane Gas market.

By Application: Semiconductor Demand Anchors Market While Chemicals Accelerate

In 2025, the semiconductors and electronics segment accounted for 51.78% of the High-Purity Methane Gas market. This share is expected to remain above 50% through 2031, supported by the increase in wafer starts across Asia-Pacific and North America. Key OSAT facilities in Penang, Hsinchu, and Suwon utilize high-purity methane for chamber conditioning and low-κ dielectric deposition. Since 2025, every gigafab signing has included offtake clauses to secure a supply of 99.9995% methane throughout the equipment's depreciation cycle. The chemicals and petrochemicals sector is projected to be the fastest-growing application, with a 5.91% CAGR. Growth in this segment is driven by methanol, ammonia, and Fischer-Tropsch plants that integrate CCU and hydrogen recovery loops, which require stable calibration gases. Additionally, hydrogen hubs in Rotterdam, Jubail, and Louisiana are expanding methane applications into carbon-intensity validation and catalyst protection, contributing to incremental volume in the High-Purity Methane Gas market.

Analytical and calibration users are experiencing steady growth as environmental monitoring expands and portable sensors become more common, though their market share remains in the mid-single digits. In the power generation segment, most users accept 95-98% fuel, but turbine efficiency trials and hydrogen co-firing pilots occasionally require 99.9% methane for baseline comparisons. Research and quantum technologies represent less than 3% of the market share but contribute significantly to revenue due to premium pricing. This diverse application mix helps stabilize the High-Purity Methane Gas market against fluctuations in the semiconductor segment, while petrochemical developments and environmental compliance programs provide additional demand.

Geography Analysis

In 2025, Asia-Pacific commanded a significant 43.11% share of the High-Purity Methane Gas market. Projections indicate a robust growth trajectory, with an anticipated CAGR of 5.78% from 2026 to 2031. Between 2024 and 2026, China's National Integrated Circuit Fund Phase III allocated over USD 45 billion, backing new fabs in Wuxi and Wuhan. These fabs are equipped with on-site purification skids for methane, nitrogen, and argon. Meanwhile, South Korea's ambitious KRW 29 trillion stimulus for advanced packaging is channeling funds towards domestic gas suppliers. These suppliers are collaborating with Japanese licensors to customize gas cabinets and analytical services. In India, the Semiconductor Mission is directing a substantial INR 76,000 crore towards the Dholera and Mysuru clusters. Concurrently, INOX Air Products is set to launch a hub in Gujarat, producing 12,000 tons annually of ultra-clean gases by early 2027. ASEAN nations, now home to over 20% of global back-end operations, see Malaysia and Vietnam's governments streamlining duty exemptions on specialty-gas equipment. This move aims to attract tier-one OSATs, significantly boosting regional demand for the High-Purity Methane Gas market.

North America stands as the second-largest player in the market. Key investments include Air Liquide's USD 250 million venture in Arizona and Air Products' expansion efforts in Ohio. Notably, fabs from Intel and TSMC emphasize the importance of redundant railcar and pipeline back-ups for 5.0-grade methane. The Inflation Reduction Act offers tax credits for clean hydrogen, hinting at a potential shift in the gas balance towards methane pyrolysis, contingent on favorable cost curves. Europe's focus is shifting towards biomethane and hydrogen corridors. Germany's H₂ core network is set to integrate with hubs from Linde and Messer. Simultaneously, the Netherlands is experimenting with deed-restricted biomethane clusters, refining streams to meet electronics-grade standards. While the Middle East and Africa hold a smaller share, it's on the rise. A collaborative venture between Linde, Aramco, and SLB in Jubail aims for a 9 Metric tons per year CO₂ capture by 2027, bolstering the demand for calibration gas. In South America, Brazil's biogas resources and Argentina's shale assets present opportunities for purification projects, contingent on the establishment of consistent policies.

Regional disparities necessitate localized strategies for suppliers. In Asia-Pacific, positioning within petrochemical parks and gigafabs streamlines operations, reducing both transit times for cylinders and the complexities of import paperwork. Europe witnesses a surge in merger activities, with industrial-gas giants joining forces with biogas developers to align with renewable-gas quotas. North America's extensive midstream assets favor the use of vapor-return trailers and large-volume tube modules, ensuring efficient service to expansive fab campuses. These regional intricacies not only influence capital distribution but also play a pivotal role in shaping competitive dynamics within the High-Purity Methane Gas market.

Competitive Landscape

The High-Purity Methane Gas market is moderately consolidated. Air Liquide, Linde, and Air Products collectively account for majority of global revenue. They achieve this through vertically integrated plants, on-site contracts, and extensive logistics networks. Air Liquide recently invested USD 250 million in fab-adjacent installations, securing 10-20 year offtake agreements. These agreements ensure sub-10 ppb impurity levels, highlighting Air Liquide's focus on service-oriented strategies over commodity sales. Linde's acquisition of Airtec increases its presence in the Middle East to over 90%. This move positions Linde's cryogenic units near Saudi Arabia’s carbon-capture hub, improving its geographical reach. Air Products is concentrating on hydrogen and a restructured LNG portfolio, enabling capital reallocation to specialty gases for Ohio fabs and Texas petrochemicals.

Specialty independents such as Bhoruka Specialty Gases, Element Solutions Inc, and Yingde Gases are addressing regional gaps with customized cylinder blends and isotopic services. Bhoruka has established 99.9998% purity methane plants in Karnataka and Maharashtra, powered by renewable electricity, emphasizing its low-carbon approach. Element Solutions is aligning its portfolio with its 2026 acquisition of EFC Gases, integrating aerospace and semiconductor opportunities to offer a combined supply of xenon, krypton, and methane.

Service differentiation is becoming more significant than price competition. Customers are increasingly demanding real-time purity telemetry, automated leak-detection systems, and transparency in carbon-footprint reporting. Patents on catalytic deoxygenation, moisture-scrubbing adsorbents, and IoT-enabled valve traceability are emerging as competitive advantages, though their prevalence in the market is less pronounced compared to hydrogen or helium. This creates opportunities for new entrants, particularly those introducing innovative membranes or process intensification. Companies that effectively combine renewable-gas sourcing, isotopic enrichment, and digital logistics are better positioned to meet the changing requirements of the High-Purity Methane Gas market.

High-Purity Methane Gas Industry Leaders

Air Liquide S.A.

Air Products and Chemicals Inc.

Taiyo Nippon Sanso Corporation

Messer Group GmbH

Linde PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Element Solutions Inc, a global and diversified specialty chemical technology company, announced the acquisition of EFC Gases & Advanced Materials. EFC will operate as a standalone business unit reported within Element Solutions Inc.

- September 2025: Linde raised its Airtec stake above 90%, bolstering the Gulf Cooperation Council's footprint for specialty-gas infrastructure.

Global High-Purity Methane Gas Market Report Scope

High-purity methane gas is a highly refined methane with minimal trace contaminants. It is produced by removing impurities from natural gas or liquefied natural gas (LNG) for use in critical industrial, scientific, and electronic applications.

The market is segmented by production method, application, and geography. By production method, the market is segmented into natural-gas purification, biomethane upgrading, and other production methods (including synthetic/power-to-methane (PtM) and methane-pyrolysis recycle). By application, the market is segmented into semiconductors and electronics, chemicals and petrochemicals, analytical and calibration, power generation/turbines, research and development, and other applications (including quantum technologies). The report also covers the market size and forecasts for High-Purity Methane Gas in 17 countries across the world. For each segment, market sizing and forecasts are provided in terms of value (USD).

| Natural-gas purification |

| Biomethane upgrading |

| Other Production Methods (Synthetic / Power-to-Methane (PtM), Methane-pyrolysis recycle) |

| Semiconductors and Electronics |

| Chemicals and Petrochemicals |

| Analytical and Calibration |

| Power Generation / Turbines |

| Research and Development |

| Other Applications (Quantum-technologies, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Production Method | Natural-gas purification | |

| Biomethane upgrading | ||

| Other Production Methods (Synthetic / Power-to-Methane (PtM), Methane-pyrolysis recycle) | ||

| By Application | Semiconductors and Electronics | |

| Chemicals and Petrochemicals | ||

| Analytical and Calibration | ||

| Power Generation / Turbines | ||

| Research and Development | ||

| Other Applications (Quantum-technologies, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast will the High-Purity Methane Gas market grow through 2031?

The market is forecast to reach USD 10.89 billion by 2031, growing at a 5.03% CAGR from USD 8.52 billion in 2026.

How fast will the Asia-Pacific region grow through 2031?

Asia-Pacific is forecast to expand at a 5.78% CAGR between 2026-2031, buoyed by semiconductor and petrochemical capacity additions.

Which production method is growing the fastest?

Biomethane upgrading is the fastest-growing route, projected to register a 5.68% CAGR through 2031.

Why does the semiconductor sector dominate demand?

Front-end wafer fabrication requires methane with sub-10 ppb impurities for silicon-carbide epitaxy and chamber conditioning, driving more than 50% of global consumption.

Page last updated on: