High Purity Gas/Ultra-high Purity Gas/Pure Gas Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 43.32 Billion |

| Market Size (2031) | USD 56.18 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Purity Gas/Ultra-high Purity Gas/Pure Gas Market Analysis by Mordor Intelligence

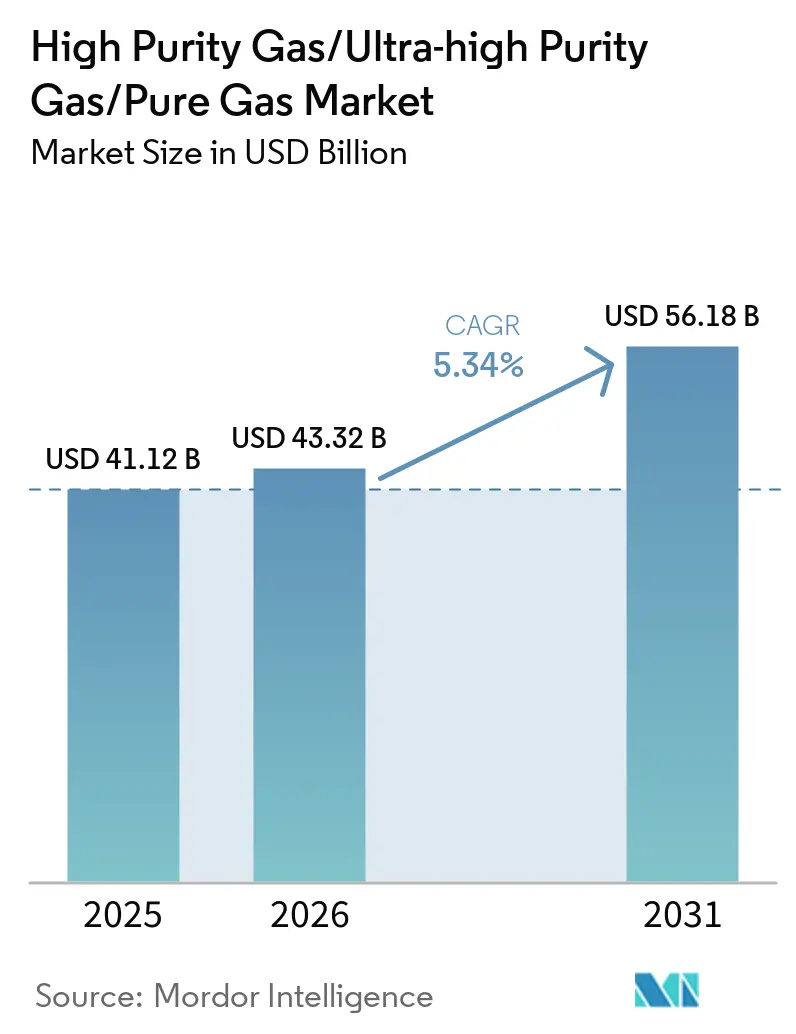

The High Purity Gas/Ultra-high Purity Gas/Pure Gas Market size was valued at USD 41.12 billion in 2025 and is estimated to grow from USD 43.32 billion in 2026 to reach USD 56.18 billion by 2031, at a CAGR of 5.34% during the forecast period (2026-2031). In the Asia-Pacific region, advanced semiconductor fabs are expanding, and green-hydrogen electrolyzer farms are on the rise. These initiatives are securing multi-year supply contracts for ultra-high-purity nitrogen, argon, and oxygen, often locking in deals even before production commences. Earlier this year, a helium embargo from Qatar significantly curtailed global supply, highlighting the geopolitical vulnerabilities in the high-purity gas market. In light of these market dynamics, investors are modernizing legacy air-separation units. They are incorporating membrane or molecular-sieve polishing to meet the ultra-high purity standards crucial for electrolyzer stacks and biopharma fill-finish lines. At the same time, AI-driven purity-analytics platforms are providing established suppliers with a competitive advantage by minimizing analyzer downtime and enhancing product recovery.

Key Report Takeaways

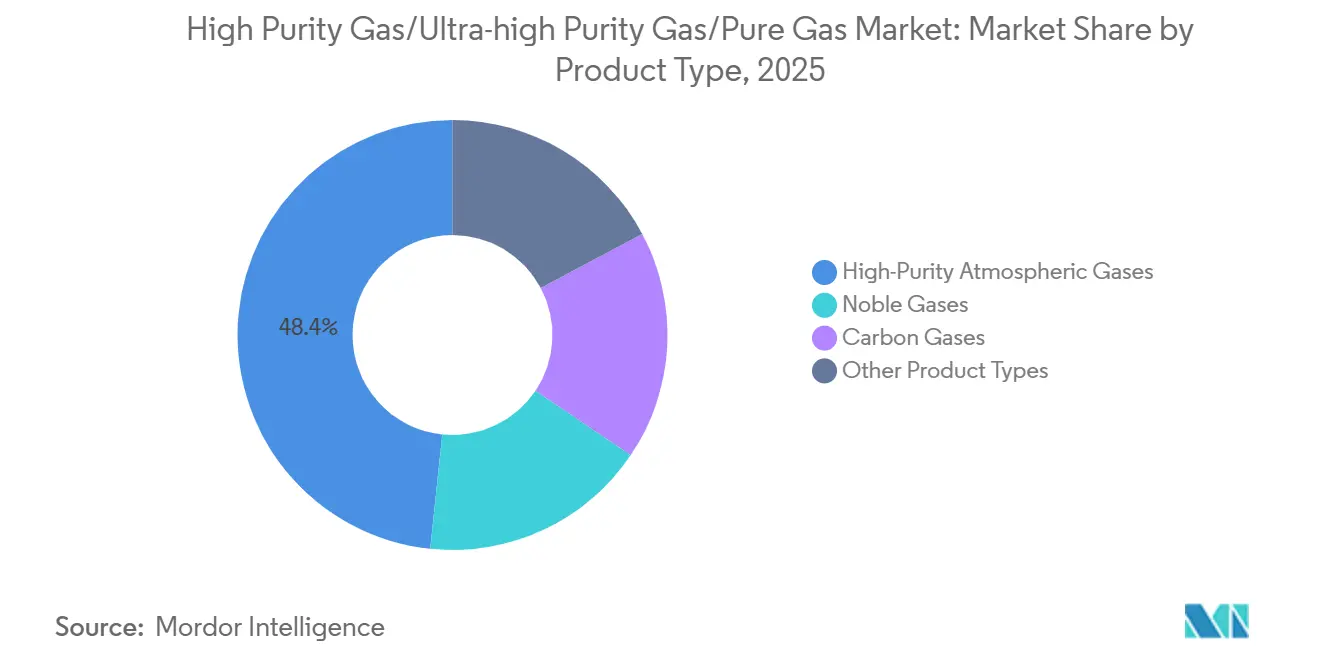

- By product type, high-purity atmospheric gases led with 48.35% revenue share in 2025, while noble gases are projected to expand at a 5.72% CAGR through 2031.

- By application, insulation captured 34.72% of the High purity gas market share in 2025 and coolant applications are advancing at a 5.88% CAGR through 2031.

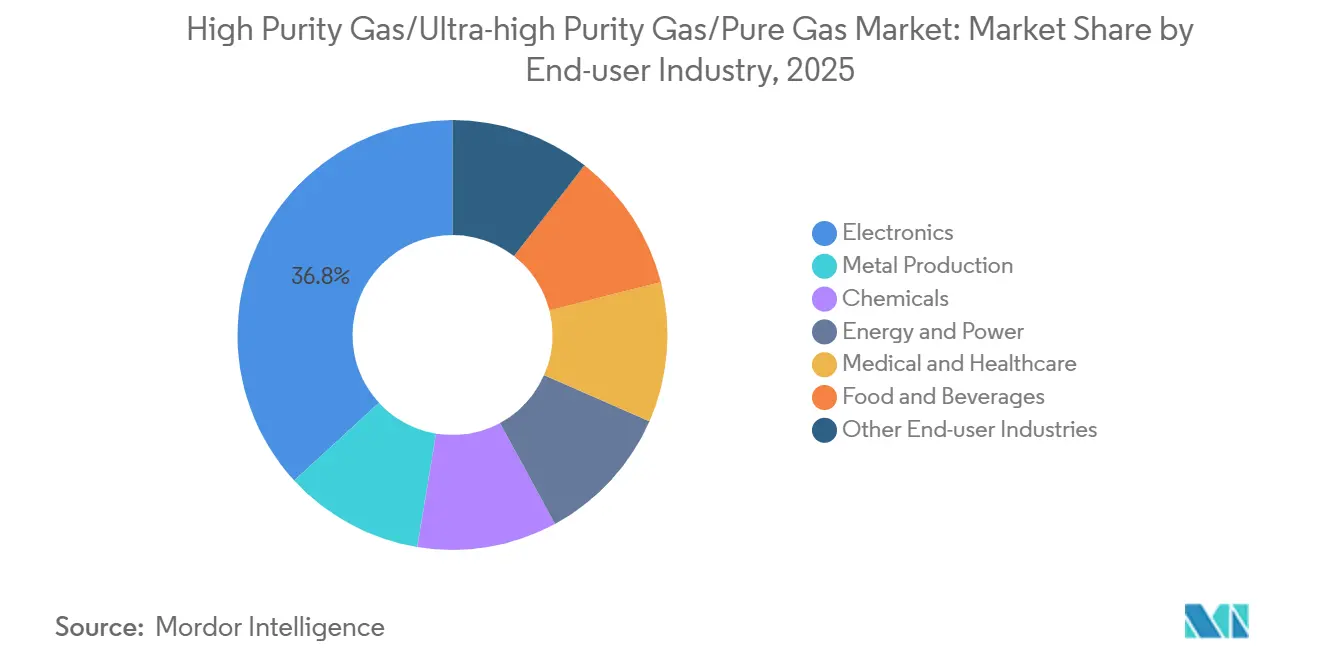

- By end-user industry, electronics commanded 36.84% share of the High purity gas market size in 2025, whereas medical and healthcare is the fastest-growing segment at a 5.56% CAGR to 2031.

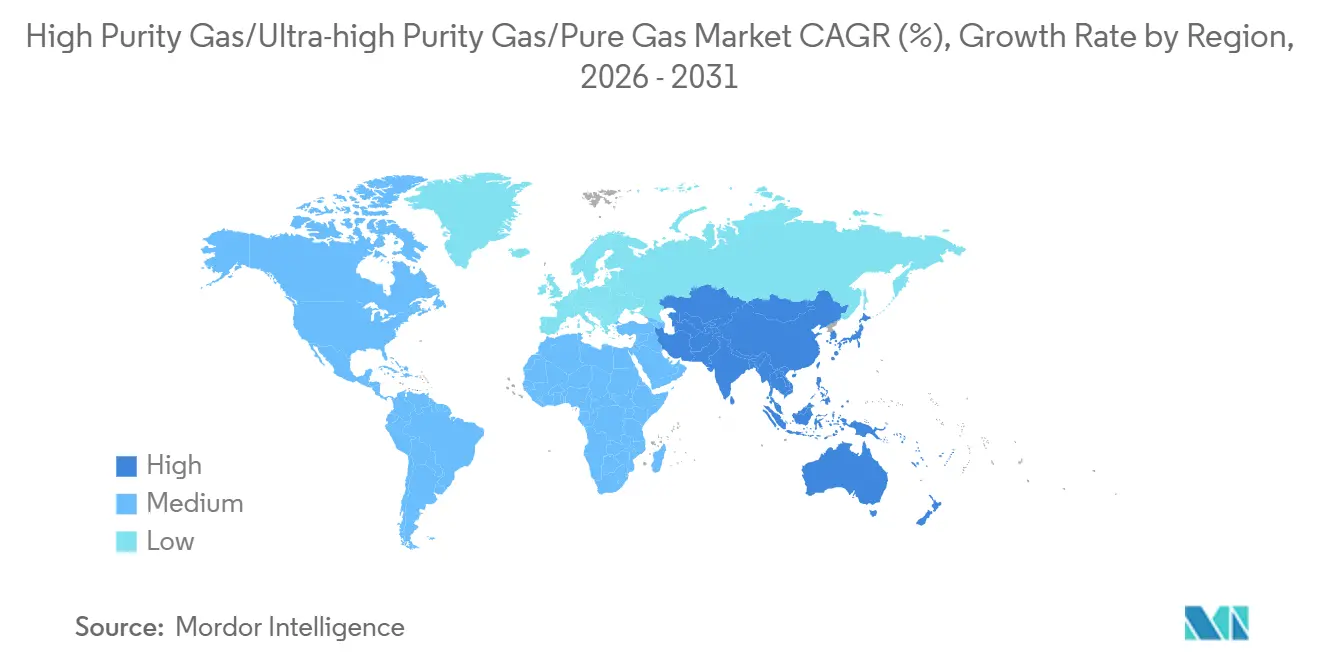

- By geography, Asia-Pacific accounted for 46.57% of 2025 revenue and is set to grow at a 5.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High Purity Gas/Ultra-high Purity Gas/Pure Gas Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Solar PV and green-hydrogen build-out | +0.90% | Global, with concentration in APAC (China, India) and Middle-East (Saudi Arabia, UAE) | Long term (≥ 4 years) |

| Healthcare and biopharma ultra-clean needs | +0.70% | North America and Europe, expanding to APAC urban centers | Medium term (2-4 years) |

| Industrial on-site generation economics | +0.50% | Global, early adoption in North America and Western Europe | Short term (≤ 2 years) |

| AI-driven purity-analytics deployment | +0.40% | APAC core (Japan, South Korea), spill-over to North America | Medium term (2-4 years) |

| Government incentives for noble-gas recycling | +0.30% | North America (DOE SBIR grants), Europe (Horizon Europe), Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Solar PV and Green-Hydrogen Build-Out

Electrolyzer stacks, employing both proton-exchange-membrane and alkaline technologies, require oxygen purities surpassing 99.999%. Achieving this level of purity necessitates downstream molecular-sieve polishing of cryogenic air separation streams. Once fully operational in 2026, Saudi Arabia’s NEOM complex is poised to be a major consumer of high-purity oxygen annually. Photovoltaic cell manufacturers, using tunnel-oxide passivated-contact architectures, require nitrogen moisture levels to be below 10 ppb[1]IEEE, “Moisture Control in PV Manufacturing,” ieee.org . This is vital to prevent wafer contamination during the selective-emitter laser doping process. In a notable development, India’s production-linked incentive scheme earmarked a significant sum for solar modules, leading to orders for two on-site nitrogen plants in Gujarat. Moreover, life-cycle studies confirm that combining on-site electrolytic hydrogen with low-carbon grids can markedly lower CO₂ intensity compared to steam-methane reforming.

Healthcare and Biopharma Ultra-Clean Needs

ISO class 5 aseptic-filling suites are now using high-purity nitrogen for biologics. This decision follows regulators pointing to oxygen ingress as a factor in potency loss incidents. Shipments of home oxygen concentrators have risen, with newer membrane units offering high purity and quieter operation, making them more popular among sleep-apnea patients. MRI scanners generally need a considerable amount of liquid helium per quench. Yet, a supply outage in Qatar caused hospitals to postpone elective scans, highlighting supply chain vulnerabilities. Europe’s Medical Device Regulation now mandates traceability of medical gases from cradle to patient, driving the adoption of blockchain for cylinder tracking. Additionally, recent CAR-T approvals have led to a surge in demand for vapor-phase liquid nitrogen storage at biorepositories, necessitating extremely low temperatures.

Industrial On-Site Generation Economics

A study showed that a steel mill, running at a high capacity, recouped its investment in an on-site PSA nitrogen generator within a few years, provided electricity rates stayed below a certain level. Customers of Purity Gas saw significant cost savings after adopting high-purity membrane generators. While suitable for MAP food packaging, these generators are not ideal for semiconductor fabrication. Air Products has launched SmartFuel modules, combining PEM electrolyzers with high-pressure compressors. This development eliminates the need for tube-trailer logistics and cuts costs for hydrogen stations with lower capacities. Advanced fabrication units still rely on cryogenic distillation for parts-per-billion purity. They have also secured long-term contracts with major suppliers to leverage scale economics. Cost-of-ownership models suggest on-site solutions become economically feasible when purity hits a certain mark and consumption reaches defined levels. These solutions are beneficial for applications like laser cutting and chemical blanketing, but they do not meet the standards of the electronics sector.

AI-Driven Purity-Analytics Deployment

Yokogawa’s AI-enhanced gas chromatograph at Ras Tanura has transformed hydrogen analysis, slashing cycle times and enhancing recovery. Emerson’s X-STREAM analyzers have made headway in ammonia units reliant on high-purity nitrogen. By forecasting sensor drift, they have curtailed unplanned downtimes. Chip manufacturers are linking cabinet purity metrics with wafer-defect analyses. This tactic has diminished scrap rates and hastened root-cause investigations. ISA recommends predictive-maintenance strategies to significantly prolong compressor lifespans. Yet, the hefty costs of retrofitting older plants with modern sensor technologies have restricted this trend mainly to lucrative sectors like electronics and pharmaceuticals.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Helium and neon supply volatility | -0.60% | Global, acute in North America (MRI), APAC (semiconductors) | Short term (≤ 2 years) |

| Skilled-operator talent gap | -0.40% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Tariff-related equipment import hurdles | -0.30% | North America (USMCA), spill-over to South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled-Operator Talent Gap

By 2030, the United Kingdom anticipates a notable rise in technician demand; however, in 2025, graduates only partially filled this gap. In North America, the median age of operators suggests that by 2028, retirements will significantly diminish the pool of experienced professionals. Two hydrogen plants in Europe faced delays due to labor shortages, leading to hefty carrying charges for Air Liquide. Although artificial intelligence technology can oversee compressors, the expertise of skilled technicians remains crucial for emergency shutdowns and leak repairs.

Tariff-Related Equipment Import Hurdles

United States tariffs on gases and cryogenic equipment from Germany and Japan, not covered by the USMCA, have driven up nitrogen delivery costs and tightened margins for distributors[2]U.S. International Trade Commission, “Tariff Schedules 2025,” usitc.gov . Grupo Infra, citing rising capital expenditures, has postponed two air separation unit projects in Tijuana and Monterrey. In 2025, Atlas Copco witnessed a year-over-year decline in United States orders for on-site generators, as clients held off, seeking clarity on trade regulations. After European suppliers priced themselves out of the market, South American buyers turned to lower-precision equipment from China, raising concerns about quality among pharmaceutical users. In early 2026, the Compressed Gas Association's pending exemption petition added to the cloud of investment uncertainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Atmospheric Gases Anchor Share, Noble Gases Accelerate

In 2025, high-purity atmospheric gases captured 48.35% of the market's revenue. Noble gases, however, are projected to grow at the fastest rate, boasting a 5.72% CAGR through the forecast period of 2026-2031. Nitrogen, a staple for inerting in steel mills and fabs, leads in volume consumption. However, with the expansion of electrolyzer farms, oxygen demand is witnessing a notable surge. Argon, pivotal in the additive manufacturing of turbine blades, is carefully monitored; exceeding certain oxygen levels can induce porosity. On the premium side, xenon prices have seen a significant uptick. Meanwhile, helium-4, buoyed by the lifting of the Qatar embargo, underscores its own scarcity.

Industrial users are now segmenting the atmospheric stream: customer-owned PSA units are producing commodity grades, while major players, leveraging mega-fabs to spread distillation costs, maintain control over parts-per-billion specifications. Carbon gases, especially CO₂, play a crucial role in modified-atmosphere packaging, making up a large portion of the tray-gas volume. Specialty gas blends, essential for spectroscopy and welding, fetch much higher prices than their bulk counterparts, thanks to stringent composition tolerances. Regulatory mandates further escalate costs; for instance, medical oxygen, which undergoes cGMP testing, incurs added production expenses.

By Application: Insulation Leads, Coolant Surges

Insulation accounted for 34.72% of the market's 2025 value. Double-glazed windows, filled with argon, effectively reduce U-values, while LNG tanks rely on nitrogen purges to uphold vacuum integrity. The market for high-purity gases in coolant services is projected to grow at a 5.88% CAGR during the forecast period of 2026-2031, fueled by the needs of data-center immersion cooling and dilution refrigerators for quantum computers. Liquid-nitrogen systems not only support rack densities surpassing 50 kW but also aid in phasing out HFC refrigerants, now banned under the Kigali Amendment.

Despite a broad shift to LED lighting, the demand for krypton-fluoride and argon-fluoride in excimer lasers for 5 nm lithography remains strong. In 2025, retailers leveraged modified-atmosphere packaging with CO₂ and N₂ to prolong meat shelf life. Helium boil-off, vital for superconducting-magnet quench protection, faced a shortage in 2026, causing CERN to postpone maintenance and risking unplanned downtime. By 2028, data-center cooling is poised to represent a significant share of the total site load, positioning liquid-nitrogen as a crucial efficiency asset.

By End-User Industry: Electronics Dominates, Healthcare Accelerates

Electronics dominated in 2025, holding 36.84% share of the market. Samsung's ramp-up at P4-P5 significantly boosted nitrogen demand, while TSMC's Arizona facility clinched sub-ppb contracts with Air Liquide. Etching gases, notably NF₃ and WF₆, not only generated substantial revenue in 2024 but are also on track for further growth by 2032.

The medical and healthcare sector, buoyed by the rising adoption of portable concentrators and increased MDR traceability, is set to expand at a 5.56% CAGR during the forecast period of 2026-2031. In 2025, argon consumption in steelmaking positioned it as the second-largest user in the metal production sector. The chemicals, energy, and food sectors, each holding mid-single-digit market shares, harness high-purity gases for applications ranging from hydrogenation and pipeline pressurization to cryogenic freezing. While aerospace and research laboratories constitute a smaller market segment, they command higher margins through specialized applications like helium leak-testing and argon sputtering targets.

Geography Analysis

Asia-Pacific, accounting for 46.57% of 2025's revenue, is projected to achieve a 5.23% CAGR through the 2026-2031 period. This growth is driven by record semiconductor capital expenditures in South Korea, Taiwan, and Japan. China is steering its steel mills toward hydrogen-DRI processes, emphasizing high-purity argon, with a mandate to cut carbon intensity by 2030. In India, solar module incentives have catalyzed the establishment of new nitrogen plants in Gujarat. South Korea sees a significant investment in cluster gas lines. ASEAN nations attracted substantial electronics foreign direct investment in 2025, prompting companies such as Messer and Linde to establish regional hubs.

North America benefited from CHIPS Act grants, leading to new fabs in Arizona, Ohio, and Texas. Air Products is heavily investing in three nitrogen facilities, with a combined capacity exceeding several tons per day. Quebec's hydrogen strategy in Canada is supporting a major electrolyzer, secured with a long-term oxygen off-take agreement. However, Mexico’s maquiladora belt faces challenges, delaying expansion plans due to tariff-induced capital expenditure inflation. The depletion of helium reserves has posed challenges for MRI operators.

Europe, a significant player in 2025, is seeing a plant in Dresden set to supply high-purity gases to an undisclosed semiconductor client, highlighting the continent's push for localized chip supply. While compliance costs have risen due to blockchain cylinder tracing mandates, this initiative has notably minimized dispensing errors. Horizon Europe is championing pilots for noble-gas circularity, yet Britain faces delays in two hydrogen projects due to a technician shortage.

South America, though modest in share, is eyeing growth in Argentina’s lithium brine ventures and Petrobras’s hydrogen initiatives. The Middle East, while having a smaller share, is strategically significant, as evidenced by NEOM's anticipated annual consumption of several tons of oxygen starting mid-2026.

Competitive Landscape

The high-purity gas market is moderately consolidated. Air Liquide, Linde, Air Products, Messer, and Taiyo Nippon Sanso dominate global capacity. Their scale not only secures cost leadership in cryogenic distillation but also enables long-term on-site contracts with major fabs and electrolyzer farms. Regional players such as INOX Air Products and Yingde Gases are gaining traction through faster installations and localized services.

Technology is a key differentiator: Yokogawa’s 90-second GC cycle at Ras Tanura boosted hydrogen recovery for Saudi Aramco, while Emerson’s predictive analyzers reduced ammonia-plant downtime. Air Products’ modular SmartFuel units challenge traditional hydrogen delivery, especially for stations with lower daily consumption, with forecasts indicating a potential merchant volume decline by 2030. The European Patent Office highlights a competition among Air Liquide, Linde, and Evonik to commercialize high-purity hollow-fiber membranes, which promise lower capital expenditure than standard PSA units.

The Qatar embargo has spotlighted the need for diversified sourcing. Companies with helium assets in North America, Russia, or Tanzania have strengthened their pricing power, unlike distributors dependent on singular sources who have seen clientele losses. Despite its potential, noble-gas recycling remains underutilized, with fewer than 20 commercial plants active, even as closed-loop xenon recovery from anesthesia machines offers a chance to reclaim a significant amount of gas currently vented.

High Purity Gas/Ultra-high Purity Gas/Pure Gas Industry Leaders

Air Liquide

Air Products and Chemicals, Inc

Linde plc

Messer Group

TAIYO NIPPON SANSO CORPORATION

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Air Liquide announced to invest EUR 130 million to build, own, and operate two advanced industrial gas facilities in Singapore, supporting the expansion of a leading semiconductor manufacturer. These facilities will supply ultra-high purity nitrogen for advanced chip production and are expected to be operational by 2027.

- November 2025: INOX Air Products has partnered with Grew Energy Private Limited to supply ultra-high purity (UHP) nitrogen for its upcoming 3 GW Solar PV Cell manufacturing facility in Narmadapuram, Madhya Pradesh, India.

Global High Purity Gas/Ultra-high Purity Gas/Pure Gas Market Report Scope

High-purity gases are characterized by extremely low impurity levels and are refined to consist almost entirely of the intended gas molecules. Their purity levels typically exceed 99.995%, with some reaching over 99.99999%. These gases are classified based on the number of '9s' in their purity level.

The High Purity Gas/Ultra-high Purity Gas/Pure Gas Market is segmented by product type, application, end-user industry, and geography. By product type, the market is segmented into high-purity atmospheric gases, noble gases, carbon gases, and other product types. By application, the market is segmented into insulation, lighting, coolant, and other applications. By end-user industry, the market is segmented into electronics, metal production, chemicals, energy and power, medical and healthcare, food and beverages, and other end-user industries. The report also covers the market size and forecasts for high purity gas/ultra-high purity gas/pure gas in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| High-Purity Atmospheric Gases |

| Noble Gases |

| Carbon Gases |

| Other Product Types |

| Insulation |

| Lighting |

| Coolant |

| Other Applications |

| Electronics |

| Metal Production |

| Chemicals |

| Energy and Power |

| Medical and Healthcare |

| Food and Beverages |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | High-Purity Atmospheric Gases | |

| Noble Gases | ||

| Carbon Gases | ||

| Other Product Types | ||

| By Application | Insulation | |

| Lighting | ||

| Coolant | ||

| Other Applications | ||

| By End-user Industry | Electronics | |

| Metal Production | ||

| Chemicals | ||

| Energy and Power | ||

| Medical and Healthcare | ||

| Food and Beverages | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR is projected for the High purity gas market between 2026 and 2031?

The high purity gas/ultra-high purity gas/pure gas market size stands at USD 43.32 billion in 2026, and it is projected to reach USD 56.18 billion by 2031 at a 5.34% CAGR.

Which segment commands the largest High purity gas market share today?

Atmospheric gases lead the mix with 48.35% revenue share in 2025.

Why did helium prices spike in early 2026?

Qatar’s export suspension removed 30% of global supply and doubled MRI-grade prices within six weeks.

Which end-user will grow fastest through 2031?

Medical and healthcare demand is set to rise at a 5.56% CAGR as home oxygen therapy expands.

How does on-site generation affect gas procurement costs?

For medium-purity nitrogen, on-site PSA units can cut delivered-gas costs by roughly 35%.

Which region will add the most new capacity to the High purity gas market by 2031?

Asia-Pacific, driven by semiconductor investments and green-hydrogen projects, will add the bulk of new capacity.

Page last updated on: